Figures & data

Table 1. Descriptive statistics and univariate analysis.

Table 2. Auditor distraction and audit effort.

Table 3. Auditor distraction and clients’ earnings quality.

Table 4. Auditor distraction and market response to unexpected earnings.

Table 5. Auditor distraction and audit effort: Alternative measures of audit delay and audit fees.

Table 6. Auditor distraction and future audit effort and audit fees.

Table 7. Auditor distraction, audit effort, and earnings quality: Alternative measure of distraction.

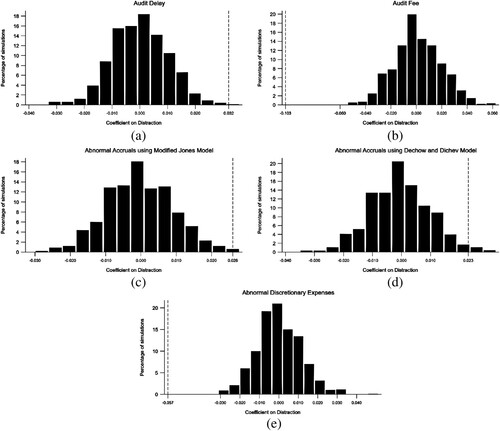

Figure 1. Auditor distraction, audit effort, and clients’ earnings quality: Placebo test.

Notes: This figure illustrates the results of a placebo test that randomly assigns Distraction. This procedure is repeated 1,000 times and the distribution of the estimated coefficients for Distraction from the regressions are reported. The dotted line represents the true coefficient estimates from Tables 2 and 3. Distraction is the ratio of an audit office’s audit fees stemming from financially distressed clients to total audit fees the office obtains in the given year. See subsection 3.1 for more details. ln (Audit Delay) is the natural logarithm of the difference between the completion date of the client’s audit report and the fiscal year-end date. ln (Audit Fee) is the natural logarithm of audit fees. Appendix A has the definitions of all other variables.

Table 8. Auditor distraction and audit effort: The effects of office size, industry specialisation, and audit firm tenure