?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Trapping refers to the event when a household falls into the area of poverty. Households that live or fall into the area of poverty are said to be in a poverty trap, where a poverty trap is a state of poverty from which it is difficult to escape without external help. Similarly, extreme poverty is considered as the most severe type of poverty, in which households experience severe deprivation of basic human needs. In this article, we consider an Omega risk process with deterministic growth and a multiplicative jump (collapse) structure to model the capital of a household. It is assumed that, when a household's capital level is above a certain capital barrier level that determines a household's eligibility for a capital cash transfer programme, its capital grows exponentially. As soon as its capital falls below the capital barrier level, the capital dynamics incorporate external support in the form of direct transfers (capital cash transfers) provided by donors or governments. Otherwise, once trapped, the capital grows only due to the capital cash transfers. Under this model, we first derive closed-form expressions for the trapping probability and then do the same for the probability of extreme poverty, which only depends on the current value of the capital given by some extreme poverty rate function. Numerical examples illustrate the role of capital cash transfers on poverty and extreme poverty dynamics.

1. Introduction

In development economics, households that live or fall below the poverty line are said to be in a poverty trap, where a poverty trap is a state of poverty from which it is difficult to escape without external help. Similarly, extreme poverty refers to the most severe type of poverty, characterised by severe deprivation of basic human needs, including food, safe drinking water, sanitation facilities, health, shelter, education and information (United Nations and World Summit for Social Development Citation1996).

According to the World Bank (Citation2018), the number of people living in extreme poverty declined from in 1990 to

of the world's population in 2015. However, this downward trend has been decelerating throughout the years. Indeed, recent research published by the United Nations University World Institute for Development Economics Research (UNU-WIDER) shows that, due to the COVID-19 crisis, global poverty could increase for the first time since 1990 (Sumner et al. Citation2020), therefore threatening one of the global public's priority: ending poverty. In 2015, owing to the importance of the topic, world leaders agreed on seventeen Sustainable Development Goals (SDGs) which engage not only public and private sectors but also society in attaining a better and more sustainable future for all. Among these goals, eradicating extreme poverty by 2030 is at the top of the list of priorities, followed by other targets among which, the reduction of at least by half of the proportion of people living in poverty and the implementation of appropriate social protection programmes, stand out (SDG 1: End poverty in all its forms everywhere) (United Nations Citation2015).

Poverty is not an individualised condition, as it does not affect only those who are poor. That is, poverty causes enormous economic, social and psychological costs to both the poor and the non-poor. Crime, access to and affordability of health care and economic productivity are just a few examples of common global concerns that are exacerbated by poverty (Rank et al. Citation2021). Child poverty is a clear example of how poverty affects us all. For instance, children who grow up in poverty are much more likely to commit crime as adults (Bjerk Citation2007). More crime means higher correction costs and a rise in private spending on crime prevention (e.g. in buying alarms and locks). Similarly, growing up in poverty can have harmful effects on a person's health (Brooks-Gunn & Duncan Citation1997, Case et al. Citation2002, Ravallion Citation2016). This causes hospitals and health insurers to spend more on the treatment of preventable diseases (CitationChildren's Defense Fund CitationU.S.), jeopardising access to and affordability of health care. Lastly, poor children are often less exposed to education (Rank et al. Citation2014) and they may therefore have fewer qualifications, which in turn translates into lower paid and more unstable jobs. This results in lower economic productivity in adulthood for poor children. Specifically, for the United States of America, McLaughlin & Rank (Citation2018) indicate the aggregate annual cost of child poverty amounts to USD 1.0298 trillion, representing 5.4% of the country's gross domestic product (GDP). Moreover, McLaughlin & Rank (Citation2018) also estimate that, for every dollar spent on reducing childhood poverty, the country would save at least seven dollars with respect the economic costs of poverty.

Cash transfer programmes are one of the main social protection strategies to reduce poverty and are therefore considered important mechanisms to help achieve SDG 1. In their simplest form, these programmes transfer cash, whether in small, regular amounts, or as lump sums, to people living below the poverty line and are generally funded by governments, international organisations, donors or nongovernmental organisations (NGOs) (Garcia & Moore Citation2012). Moreover, cash transfers are usually classified as unconditional (UCTs) or conditional (CCTs), with the former not requiring beneficiaries to undertake any specific actions nor meet any conditions whereas the latter needs them to have some specific behavioural conditions in exchange of the cash transfer (Baird et al. Citation2014), such as enrolling children in school or taking them to regular health check-ups (Handa & Davis Citation2006).

Adopting a ruin-theoretic approach, this article studies the impact of regular UCTs on poverty and extreme poverty dynamics and, particularly, their effectiveness in reducing the likelihood of a household living in poverty and extreme poverty. Previous research has addressed the role of UCTs as a pathway out of extreme poverty for households. Handa et al. (Citation2016) study two programmes, the Child Grant Programme (CGP) and the Multiple Category Targeted Programme (MCP), which were implemented in 2010 by the Ministry of Community Development, Mother and Child Health (MCDMCH) of the Government of Zambia. The authors find that both of these UCTs go far beyond their primary objective of protecting food security and consumption, as they also have an enormous impact on households' productive capacity. Although a flat transfer of USD 12 per month may not permanently lift households out of the poverty trap, their results suggest these programmes can help raise the standards of living of the country's population. In the same way, Ambler & Brauw (Citation2017) show that the Benazir Income Support Program (BISP), an UCT initiative introduced in 2008 by the Government of Pakistan, has increased women empowerment in the country, frequently associated with economic growth (Duflo Citation2012), which at the same time has been linked with poverty reduction (Adams Citation2003). As a matter of fact, UCTs have recently gained popularity as a cost-effective social protection strategy to attain some public policy objectives, including poverty alleviation (Aker Citation2013, Baird et al. Citation2014, Blattman & Niehaus Citation2014, Haushofer & Shapiro Citation2016, Jensen et al. Citation2017, Pega et al. Citation2022).

Despite the growing interest in studying the impact of UCTs on poverty dynamics over the years, most studies have adopted an empirical approach. This article is an attempt to attach a mathematically based theoretical framework to the vast empirical literature. In this paper, we extend the model proposed by Kovacevic & Pflug (Citation2011). Here, a household's capital process grows exponentially at a rate r>0, which incorporates household rates of consumption, income generation and investment or savings, above a critical capital level (or poverty line)

, whereas below a capital barrier level

, the capital also integrates external support in the form of direct transfers (capital cash transfers) provided by donors or governments at a rate

. At time

, the ith capital loss event time, the capital process jumps (downwards) to

, where

is a sequence of i.i.d. random variables with distribution function

supported in

, representing the proportions of remaining capital after each loss event (in the present paper, it will be regularly assumed the random variables are

distributed). A more comprehensive picture of this model is introduced in Section 2.

The probability of falling (trapping probability) and the moment at which a household falls (trapping time) into the poverty trap have recently attracted the interest of some researchers (see, for example, Kovacevic & Pflug (Citation2011), Azaïs & Genadot (Citation2015), Flores-Contró et al. (Citation2021), Henshaw et al. (Citation2023) and Flores-Contró (Citation2024)). These studies focus on analysing the behaviour of a household's capital above the critical capital, hence overlooking its evolution below this threshold. That is, under this set up, a household's capital process is killed at the trapping time . In this article, we assume households may escape from the poverty trap only due to external support received in the form of capital cash transfers. Therefore, we define the random variable

for

as the time of extreme poverty i.e. the moment at which a household becomes extremely poor and

as the probability of extreme poverty. Hence, under this new set up, a household's capital process is killed at the time of extreme poverty. The approach taken here differs from the aforementioned studies, where the area of poverty

was considered as an absorbing state from which it was not possible to escape. To explore these ideas, we consider an Omega risk process, which in classical risk theory, distinguishes between ruin (negative surplus) and bankruptcy (going out of business). Thus, it is assumed that, even with negative surplus levels, an insurance company can do business as usual and continue until bankruptcy occurs.

The Omega model was first introduced in Albrecher et al. (Citation2011), where closed-form formulas for the expected discounted dividends until bankruptcy under a dividend barrier strategy are obtained for the case in which the surplus of an insurance company is modelled as a Brownian motion. Similarly, Gerber et al. (Citation2012), Albrecher & Lautscham (Citation2013) and Wang et al. (Citation2016) derive explicit expressions for the expected discounted penalty function at bankruptcy and the probability of bankruptcy when the surplus of an insurance company is modelled as a Brownian motion, a compound Poisson risk model with exponential claim sizes and an Ornstein-Uhlenbeck process, respectively. Certainly, the Omega model has been extensively studied during the last decade in the actuarial science literature, with researchers incorporating the bankruptcy concept into traditional ruin models. A particular clear example of this is in Cui & Nguyen (Citation2016), where an Omega model with surplus-dependent tax payments and capital injections in a time-homogeneous diffusion setting is studied. This work not only incorporates features from the Omega model (Albrecher et al. Citation2011) but also from traditionally well-studied ruin models such as the risk model with tax (Albrecher & Hipp Citation2007) and the risk model with capital injections (Albrecher & Ivanovs Citation2014). More recently, Gao & He (Citation2019) and He et al. (Citation2019) obtain analytical results for the expected discounted penalty function and the probability of bankruptcy for surplus processes under three- and two-step premium rate settings, respectively. In like manner, Gao et al. (Citation2022) also derive results for the expected discounted dividends until bankruptcy for a jump-diffusion surplus process with a two-step premium rate under a dividend barrier strategy. Besides, alternative versions of the Omega model have also been considered. For instance, Kaszubowski (Citation2019) allows the surplus process to evolve below zero but assumes it is killed once it falls below some fixed level .

Under the classical risk theory set up, the probability of bankruptcy is quantified by a bankruptcy rate function , where x represents the value of the negative surplus. The bankruptcy rate function is defined in such a way in which the probability of bankruptcy increases when the deficit grows. Consequently, for the household capital process, the bankruptcy event is swaped for the extreme poverty one and an extreme poverty rate function

, which is assumed to be locally bounded and dependent on the capital level below the critical capital

, is defined on

. Namely, for some capital

and no prior extreme poverty event, the probability of extreme poverty on the time interval

is given by

. Moreover, we assume that

and

for

to reflect the likelihood of extreme poverty does not decrease as the capital approaches zero. Clearly, when

for all

, the probability of extreme poverty is equal to the trapping probability

.

In general, UCTs target the poor. However, in recent years, cash transfer programmes have reached unprecedented levels of coverage. For example, in 2020, in response to the COVID-19 pandemic, one out of six people in the world received at least one cash transfer payment (Gentilini Citation2022). As a consequence of this expansion, it is now more common to encounter UCTs targeting other population groups, such as the vulnerable non-poor (those living just above the poverty line). One example is Ingreso Solidario, an UCT programme in Colombia that was implemented in April 2020 as a response to the COVID-19 pandemic. Ingreso Solidario provided monthly transfers of approximately USD 40 to eligible households: poor households not covered by pre-existing social programmes and non-poor households deemed vulnerable based on an assessment of their living conditions (Vera-Cossio et al. Citation2023). The capital model considered in this article allows for the assessment of targeted UCTs, either to the poor only (letting ) or to both poor and vulnerable non-poor households (when

), on poverty dynamics. Moreover, the capital model is in line with the idea that spending on poverty reduction and prevention can help save on the economic costs of poverty. As such, when capital cash transfers target only the poor, the essential aim of the UCT programme is to lift households out of poverty. On the other hand, when the UCT programme targets both the poor and the vulnerable non-poor, the programme hopes to prevent the vulnerable non-poor from falling into poverty, apart from lifting the poor out of poverty. Nevertheless, both settings pursue one same objective: poverty reduction.

Particular attention should be paid to the fact that the targeted UCTs considered in this article, either to the poor only or to both poor and vulnerable non-poor households, prevent households from becoming extremely poor, as extreme poverty implies poverty (recall that a household is at risk of becoming extremely poor only when its capital lies below the critical capital or, in other words, a household can become extremely poor only when it is already poor). This is consistent with how extreme poverty is currently measured. For instance, the World Bank uses the International Poverty Line (IPL), set at USD 2.15 per person per day, to measure extreme poverty (Jolliffe et al. Citation2022). The IPL is also the most relevant poverty line to measure poverty in low-income countries, whereas in other countries, other poverty lines are used to measure poverty. For example, the poverty line is set at USD 3.65 and USD 6.85 per person per day, in lower and upper middle-income countries, respectively (Jolliffe et al. Citation2022). According to the World Bank's definition of extreme poverty, it is clear how extreme poverty implies poverty. In general, extreme poverty differs from conventional poverty in that it has greater depth (degree of deprivation), larger length (duration over time) and greater breadth (the number of dimensions such as illiteracy and malnutrition, among others) (Emran et al. Citation2014). Because of these characteristics, the economic costs of extreme poverty are also expected to be higher than those of conventional poverty. Hence, extreme poverty should be avoided by all means, and should be considered and studied separately.

The remainder of the paper is structured as follows. In Section 2, we introduce the capital model, with special emphasis on its behaviour inside and outside the poverty area. Explicit equations, their solutions and numerical illustrations for the trapping probability are given in Section 3 for the particular case in which the remaining proportions of capital are distributed. In particular, a comparison between the trapping probability of the original capital model introduced by Kovacevic & Pflug (Citation2011) and the one proposed in this article is presented in Appendix 2. The event of extreme poverty and the time when it occurs are discussed in Section 4. In addition, closed-form solutions and numerical illustrations for the probability of extreme poverty are derived in Section 4, assuming constant and exponential extreme poverty rate functions for the particular case in which the remaining proportions of capital are

distributed. Following Albrecher & Lautscham (Citation2013), Section 5 illustrates how to approximate the probability of extreme poverty for more general cases by making use of an efficient Monte Carlo simulation method. Finally, concluding remarks are discussed in Section 6.

2. The capital model

This paper extends the capital process originally proposed in Kovacevic & Pflug (Citation2011), where an individual household's income at time t comprises consumption

and savings (investments)

. Hence, as in the original capital process, income dynamics are given by

Moreover, consumption is an increasing function of income and its dynamics are given by

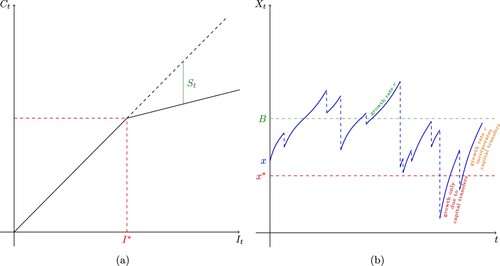

where 0<a<1. It is assumed that permanent consumption below

might result in severe adverse effects on health (Kovacevic & Pflug Citation2011). Figure (a) shows the dynamics of consumption and savings. Consider the accumulated capital

up to time t follows the dynamics

with

, and income is generated through capital

where 0<b holds.

Figure 1. (a) Consumption and savings (b) Trajectory of the stochastic process .

Putting all these pieces together and defining , one gets the dynamical system

where

and

represents the threshold below which a household lives in poverty, also interpreted as the amount of capital needed to acquire the critical income

as a perpetuity (Kovacevic & Pflug Citation2011).

We now also consider direct transfers (capital cash transfers) provided by donors or governments only to those deemed eligible. Assume a household qualifies to be a beneficiary of the unconditional capital cash transfer programme when its accumulated capital up to time t is below some capital barrier level

and that the external support will be provided at a rate

. The main objective of the proposed UCTs is to reduce the gap between the capital barrier level and the accumulated capital

up to time t for those households with capital levels below the capital barrier level

. Under this framework, one gets the dynamical system

(1)

(1) In line with the ideology that households are susceptible to the occurrence of capital losses, including severe illness, the death of a household member or breadwinner and catastrophic events such as floods and earthquakes, we model the occurrence of these events with a Poisson process with intensity λ and consider the capital process follows the dynamics of (Equation1

(1)

(1) ) in between events. On the occurrence of a loss, the household's capital at the event time is reduced by a random proportion

. Hence, the fraction of the capital not destroyed at the event time is given by

The sequence

is independent of the Poisson process and i.i.d. with common distribution function

. A trajectory of the capital process

is shown in Figure (b).

Here, the trajectories of the piecewise-deterministic process (Davis Citation1984) behave as follows: if the capital lies above the capital barrier level , then the capital grows exponentially at a rate r, whereas if the capital lies above the critical capital

but below the capital barrier level

, then the capital growth is composed by both the individual household rate r and the external support rate

; otherwise, the capital growth only incorporates the external support rate

. Note that, both the critical capital

and the capital barrier level

act as equilibrium levels for the process. That is, the further above the current value of the process is from the critical capital

, the faster the capital will depart from the critical capital

at the individual household rate r. Similarly, the further below the current value of the process is from the capital barrier level

, the faster the capital will grow to the capital barrier level

at the external support rate

(there is a “

reverting” effect where

is the rate of reversion).

3. When and how households become poor?

In this Section 3, we will study the trapping time , which is defined as the time at which a household with initial capital

falls into the area of poverty. That is,

Note that, we use the superscript

” to distinguish trapping-related variables and functions. Our analysis will involve the expected discounted penalty function, a concept commonly used in actuarial science (Gerber & Shiu Citation1998). The expected discounted penalty function contains information on the trapping time

itself and two related random variables, the capital surplus prior to the trapping time

and the capital deficit at the trapping time

.

For a force of interest and initial capital

, the expected discounted penalty function is defined as

(2)

(2) where

is the indicator function of a set A, and

, for

and

, is a non-negative penalty function of

, the capital surplus prior to the trapping time, and

, the capital deficit at the trapping time. For more details on the so-called Gerber-Shiu risk theory, interested readers may wish to consult Kyprianou (Citation2013). The function

is useful for deriving results in connection with joint and marginal distributions of

,

and

. For instance, (Equation2

(2)

(2) ) could also be viewed in terms of a Laplace transform when δ is serving as the argument. Indeed, if we let

, (Equation2

(2)

(2) ) is the Laplace transform of the trapping time

.Footnote1 Another choice is

for

, for which (Equation2

(2)

(2) ) leads to the joint distribution function of the capital surplus prior to the trapping time and the capital deficit at the trapping time. It is not difficult to realise that, by appropriately choosing a penalty function

and force of interest δ, various risk quantities can be modelled. A non-exhaustive list of such risk quantities is given in He et al. (Citation2023). In this article, we are mainly interested in studying the impact of capital cash transfers on the probability of falling into the poverty trap. Thus, we will focus our analysis on the risk quantity

, which can be derived by choosing

and

in (Equation2

(2)

(2) ).

Following Gerber & Shiu (Citation1998), our goal is to derive a functional equation for by applying the law of iterated expectations to the right-hand side of (Equation2

(2)

(2) ).

We point out that has different sample paths for

and

. Hence, we distinguish the two situations by writing

for

and

for

. Similarly, we write

for

and

for

.

Remark 3.1

Note that, when , above the critical capital

, the dynamics of the capital process follow those of the original process (Kovacevic & Pflug Citation2011). Thus, the trapping probability

and the expected discounted penalty function at the trapping time

, are equivalent to those studied in Henshaw et al. (Citation2023) and Flores-Contró (Citation2024), respectively. Clearly, this also holds true when

. Appendix 2 evidences this behaviour for a set of selected parameters.

Theorem 3.1

When , we have

(3)

(3) and when

, we have

(4)

(4) where the function

is given by

See Appendix A.1 for proof of Theorem 3.1.

Remark 3.2

We point out that the Integral Equations (IEs) (Equation3(3)

(3) ) and (Equation4

(4)

(4) ) allow us to consider the differentiability of the functions

and

. For instance, it is easy to see from (Equation3

(3)

(3) ) and (Equation4

(4)

(4) ) that

and

are differentiable in

and

, respectively. Furthermore, they satisfy the following condition

(5)

(5)

The existence and uniqueness of the required solution to the IEs derived in Theorem 3.1 should be justified in each case (see, for example, Mihálykó & Mihálykó Citation2011 for an analysis of the existence and uniqueness of the solution of an IE for the expected discounted penalty function of a risk process with dependent inter-arrival times and claim sizes). Now, by differentiating the IEs (Equation3(3)

(3) ) and (Equation4

(4)

(4) ), we obtain the Integro-Differential Equations (IDEs) for

and

in the following theorem

Theorem 3.2

When , we have

(6)

(6) and when

, we have

(7)

(7) In addition, the boundary conditions for

and

are given by (Equation5

(5)

(5) ),

and

.

Remark 3.3

Equation (Equation7(7)

(7) ) for

is independent of

. However,

is subject to the boundary condition (Equation5

(5)

(5) ) which is involved with

. Furthermore, it is easy to see from (Equation5

(5)

(5) ), (Equation6

(6)

(6) ) and (Equation7

(7)

(7) ) that

and

satisfy

(8)

(8)

3.1. The trapping time

Sometimes it is easier to work with a transformation rather than with the original distribution function of a random variable. In this article, we focus on studying the Laplace transform of the random variables of interest. The Laplace transform of a random variable characterises the probability distribution uniquely and is known to be a powerful tool in probability theory and, in particular, quite useful when studying nonnegative random variables. Recall that, by specifying the penalty function such that ,

becomes the Laplace transform of the trapping time, also interpreted as the expected present value of a unit payment due at the trapping time.

Thus, with , Equations (Equation6

(6)

(6) ) and (Equation7

(7)

(7) ) can then be written such that when

,

(9)

(9) and when

,

(10)

(10)

Proposition 3.1

Consider a household capital process with initial capital , capital growth rate r, capital barrier level B, capital transfer rate

, intensity

and remaining proportions of capital with distribution

where

; that is,

. The Laplace transform of the trapping time is given by

(11)

(11) where

is the force of interest for valuation,

is Gauss's Hypergeometric Function as defined in (EquationA8

(A8)

(A8) ),

,

,

,

,

with

,

,

and the constants

,

and

are given by (EquationA9

(A9)

(A9) ), (EquationA10

(A10)

(A10) ), and (EquationA11

(A11)

(A11) ), respectively.

The mathematical proof of Proposition 3.1 is presented in Appendix A.2.

Remark 3.4

As mentioned previously, the Laplace transform of the trapping time approaches the trapping probability as δ tends to zero, i.e.

for

. If the net profit condition

does not hold, then trapping would be certain (Henshaw et al. Citation2023).

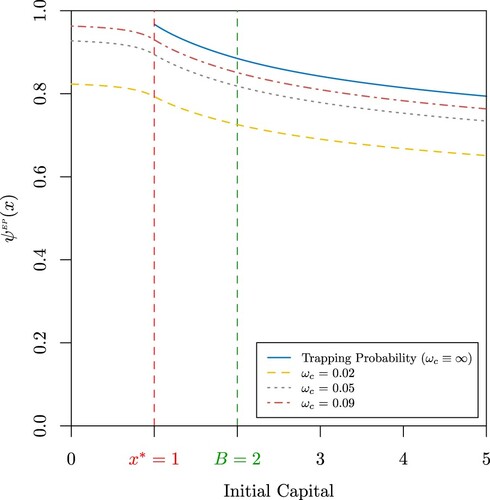

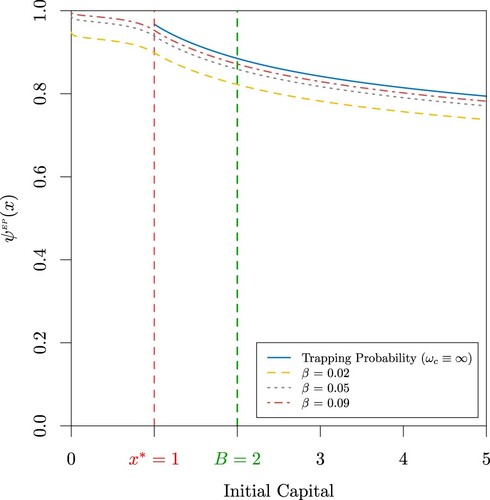

Figure (a,b)Footnote2 display the trapping probability for the capital process

. Not surprisingly, Figure (a) shows the trapping probability is a decreasing function of both the capital transfer rate

and the initial capital. In particular, it is worth noting the important role the capital transfer rate

can play in attaining lower trapping probabilities for households with initial capital below the capital barrier level B as very high capital transfer rates

have the potential to level the likelihood of becoming poor for this particular group. However, high capital transfer rates

seem to be less efficient for attaining lower trapping probabilities for households with initial capital above the capital barrier level B. This is due to the fact that households with initial capital above the capital barrier level B are exposed to never receiving a capital cash transfer. Indeed, if they experience a large loss, they are likely to fall directly into the poverty trap without ever receiving a capital cash transfer. From Figure (b), we can also highlight the importance of the capital barrier level B to reach lower values for the trapping probability. Although a higher capital transfer rate

and a higher capital barrier level B may lead to lower trapping probabilities, the sensitivity analyses shown in Appendices 2 and 3 suggest the trapping probability is less sensitive to these parameters compared to the probability of extreme poverty.

Figure 2. (a) Trapping probability when

, a = 0.1, b = 4,

, B = 2,

and

for

(b) Trapping probability

when

, a = 0.1,

,

,

,

and

for B = 1, 2, 3, 4.

4. When and how households become extremely poor?

We define the random variable for

as the time of extreme poverty i.e. the moment at which a household with initial capital x becomes extremely poor and

as the probability of extreme poverty. Note that, we use the superscript

” to distinguish extreme poverty-related variables and functions. The probability of extreme poverty is quantified by an extreme poverty rate function

, where x represents the value of capital below the critical capital

. The extreme poverty rate function is defined in such a way in which the probability of extreme poverty increases when the capital deficit

grows. Namely, for some capital

and no prior extreme poverty event, the probability of extreme poverty on the time interval

is given by

. The expected discounted penalty function at extreme poverty is therefore given by

where

, for

and

, is a non-negative penalty function of

, the accumulated capital prior to the time of extreme poverty, and

, the capital deficit at the time of extreme poverty. Note that, for the case of the expected discounted penalty function at extreme poverty, it is reasonable to consider the accumulated capital immediately before extreme poverty instead of the capital surplus, which was considered in (Equation2

(2)

(2) ) for the expected discounted penalty function at the trapping time.

We point out that has different sample paths for

,

and

. Hence, we distinguish the three situations by writing

for

,

for

and

for

. Similarly, we write

for

,

for

and

for

.

Proceeding as in Section 3, one derives the following IEs for the expected discounted penalty function at extreme poverty in the following theorem

Theorem 4.1

When , we have

(12)

(12) when

, we have

(13)

(13) and when

, we have

(14)

(14)

See Appendix A.3 for proof of Theorem 4.1.

Remark 4.1

We point out that the IEs (Equation12(12)

(12) ), (Equation13

(13)

(13) ) and (Equation14

(14)

(14) ) allow us to consider the differentiability of the functions

,

and

. For instance, it is easy to see from (Equation12

(12)

(12) ), (Equation13

(13)

(13) ) and (Equation14

(14)

(14) ) that

,

and

are differentiable in

,

and

, respectively. Furthermore, they satisfy the following condition

(15)

(15) and

(16)

(16)

As for Theorem 3.1, the existence and uniqueness of the required solution to the IEs derived in Theorem 4.1 should be justified in each case. Now, by differentiating the IEs (Equation12(12)

(12) ), (Equation13

(13)

(13) ) and (Equation14

(14)

(14) ), we obtain the IDEs for

,

and

in the following theorem

Theorem 4.2

When , we have

(17)

(17) when

, we have

(18)

(18) and when

, we have

(19)

(19) In addition, the boundary conditions for

,

and

are given by (Equation15

(15)

(15) ), (Equation16

(16)

(16) ) and

.

Remark 4.2

Equation (Equation19(19)

(19) ) for

is independent of

and

. However,

is subject to the boundary condition (Equation16

(16)

(16) ) which is involved with

. At the same time,

is subject to the boundary condition (Equation15

(15)

(15) ) which is involved with

. Furthermore, it is easy to see from (Equation17

(17)

(17) ), (Equation18

(18)

(18) ) and (Equation19

(19)

(19) ) that

,

and

satisfy

(20)

(20) and

(21)

(21)

4.1. The time of extreme poverty

Focusing again in studying the Laplace transform of the random variable of interest (the time of extreme poverty) we note that by specifying the penalty function such that ,

becomes the Laplace transform of the time of extreme poverty, also interpreted as the expected present value of a unit payment due at the time of extreme poverty. Thus, Equation (Equation19

(19)

(19) ) can then be written such that when

,

(22)

(22)

4.1.1. Examples of extreme poverty rate functions

4.1.1.1 Constant extreme poverty rate functions

Let with

. This is the simplest case of extreme poverty rate function and it could be interpreted as the situation in which the events of extreme poverty occur at discrete times. For instance, let

be i.i.d. exponential random variables with mean

and

denote the kth event of extreme poverty (e.g. unexpected loss of assets or health), with

. In this context, extreme poverty occurs when at such an event of extreme poverty the capital level is below

(Albrecher et al. Citation2013).

Proposition 4.1

Consider a household capital process with initial capital , capital growth rate r, capital barrier level B, capital transfer rate

, intensity

and remaining proportions of capital with distribution

where

; that is,

. For a constant extreme poverty rate function

, with

, the Laplace transform of the time of extreme poverty is given by

where

is the force of interest for valuation,

is Gauss's Hypergeometric Function as defined in (EquationA8

(A8)

(A8) ),

,

,

,

, with

,

,

,

,

,

,

and the constants

,

,

and

are obtained as explained in Appendix A.4.

See Appendix A.4 for proof of Proposition 4.1.

Remark 4.3

As for the trapping time, the Laplace transform of the time of extreme poverty approaches the probability of extreme poverty as δ tends to zero, i.e.

for

.

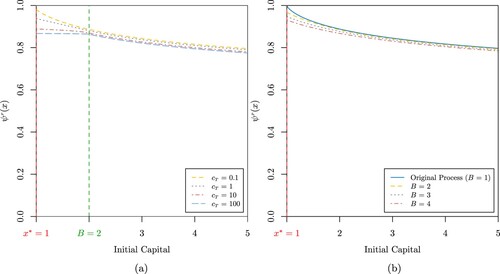

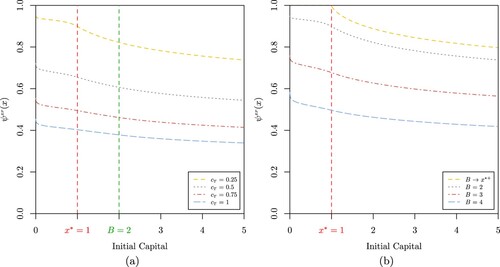

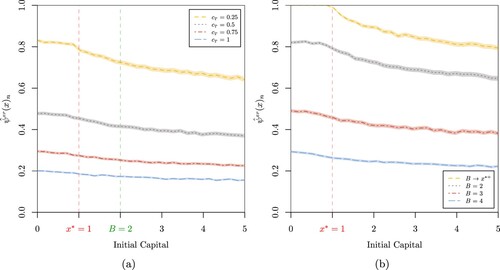

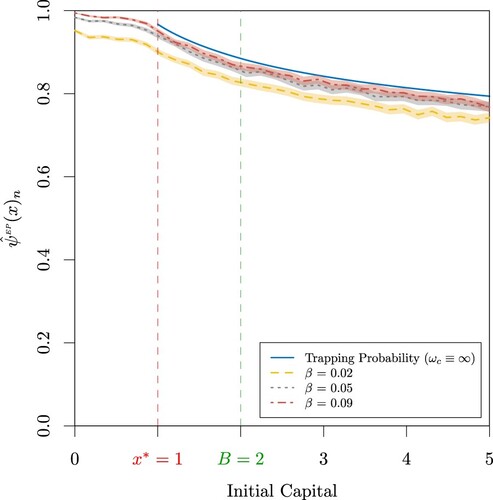

Figure shows the probability of extreme poverty for the capital process

for a constant extreme poverty rate function. As shown in Figure for the case of the trapping probability, Figure (a,b) reveal the probability of extreme poverty is also a decreasing function of the cash transfer rate

, the capital barrier level B and the initial capital. In addition, in line with the definition of the extreme poverty rate function, Figure demonstrates the probability of extreme poverty is an increasing function of the extreme poverty rate function. Furthermore, Figure also plots the trapping probability obtained in Section 3 for reference, which is given by the particular case when

and therefore represents an upper bound for the probability of extreme poverty. Appendix 3 provides a sensitivity analysis for the probability of extreme poverty with a constant extreme poverty rate function.

Figure 3. (a) Probability of extreme poverty when

, a = 0.1, b = 4,

, B = 2,

,

and

for

(b) Probability of extreme poverty

when

, a = 0.1, b = 4,

,

,

,

and

for

and

.

Figure 4. Probability of extreme poverty when

, a = 0.1, b = 4,

,

, B = 2,

,

and

for

.

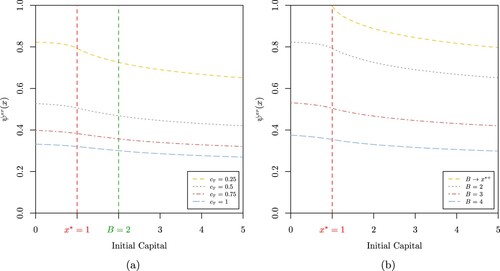

4.1.1.2 Exponential extreme poverty rate functions

Let now , for some

. In this case, the extreme poverty rates take fairly flat values for lower deficit levels and reach higher values when the capital level gets close to zero. Such a function could be considered as the analogous version of the exponential bankruptcy rate function studied in Albrecher & Lautscham (Citation2013).

Remark 4.4

In general, it is not straightforward to obtain the solution of (EquationA18(A18)

(A18) ) for more general extreme poverty rates

, as functions of

appear both in the coefficients of the homogeneous equation and in the inhomogeneous term. Thus, for the particular case of exponential extreme poverty rate functions

, we will only discuss the probability of extreme poverty.

Proposition 4.2

Consider a household capital process with initial capital , capital growth rate r, capital barrier level B, capital transfer rate

, intensity

and remaining proportions of capital with distribution

where

; that is,

. For an exponential extreme poverty rate function

, with

, the probability of extreme poverty is given by

where

is Gauss's Hypergeometric Function as defined in (EquationA8

(A8)

(A8) ),

, with

,

,

,

,

,

,

and

for

and the constants

,

,

and

are obtained as explained in Appendix A.5.

The mathematical proof of Proposition 4.2 is given in Appendix A.5.

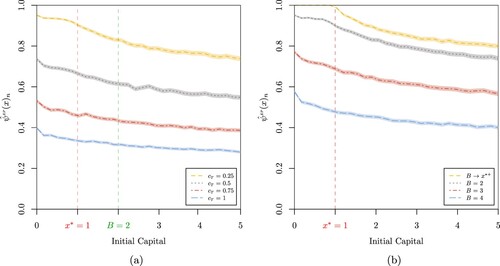

Figures and display the probability of extreme poverty when dealing with an exponential extreme poverty rate function. Evidently, under this setup, the probability of extreme poverty attains higher values compared to that under which a constant extreme poverty rate is considered. This can be verified by comparing Figures (a) and (a), for several cash transfer rates , Figures (b) and (b), for different capital barrier levels B, and Figures and , for different values of the extreme poverty rate, respectively. This result is not particularly surprising because of the fact that the exponential extreme poverty rate takes higher values for higher capital deficits while the constant extreme poverty rate remains flat for all capital levels. Appendix 3 also presents a sensitivity analysis of the probability of extreme poverty for an exponential extreme poverty rate function.

Figure 5. (a) Probability of extreme poverty when

, a = 0.1, b = 4,

, B = 2,

,

and

for

(b) Probability of extreme poverty

when

, a = 0.1, b = 4,

,

,

,

and

for

and

.

Figure 6. Probability of extreme poverty when

, a = 0.1, b = 4,

,

, B = 2,

,

and

for

.

As mentioned previously, Appendix 3 shows how sensitive the probability of extreme poverty is with respect to all the underlying parameters (for both constant and exponential extreme poverty rate functions). In particular, the sensitivity with respect to the cash transfer rate and the capital barrier level B is worth noting. These results accentuate the importance of selecting an appropriate cash transfer rate

(i.e. an adequate frequency or intensity of the capital cash transfers) and a suitable capital barrier level B (i.e. an opportune targeting), when designing the social protection strategy for achieving extreme poverty reduction.

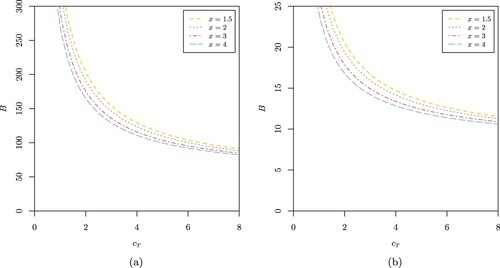

Figure (a,b) provide an example of the cash transfer rate and the capital barrier level B required to attain a given target trapping probability and probability of extreme poverty (for a constant extreme poverty rate function), respectively. Clearly, policymakers must decide between reducing the intensity of the capital cash transfers (lowering the capital cash transfer rate

) to a wider group of households (increasing the capital barrier level B) or increasing the intensity of the capital cash transfers (rising the capital cash transfer rate

) to a narrower group of households (lowering the capital barrier level B) in order to achieve the target probabilities, showing an evident trade-off between these two parameters.

Figure 7. (a) Cash transfer rate and capital barrier level B required to attain a given target trapping probability of

when

, a = 0.1, b = 4,

,

and

for initial capital

(b) Cash transfer rate

and capital barrier level B required to attain a given target probability of extreme poverty of

when

,

, b = 4,

,

,

and

for initial capital

.

5. Monte Carlo simulation

In general, it is not straightforward to derive explicit formulas for both the trapping probability and the probability of extreme poverty when more general cases are considered. Monte Carlo simulation is an alternative way to produce estimates for both quantities and is particularly useful when dealing with cases for which closed-form formulas are not available. In this section, following Albrecher & Lautscham (Citation2013), we introduce a simple and efficient methodology that allows to generate fairly accurate approximations for the probability of extreme poverty.

5.1. Methodology

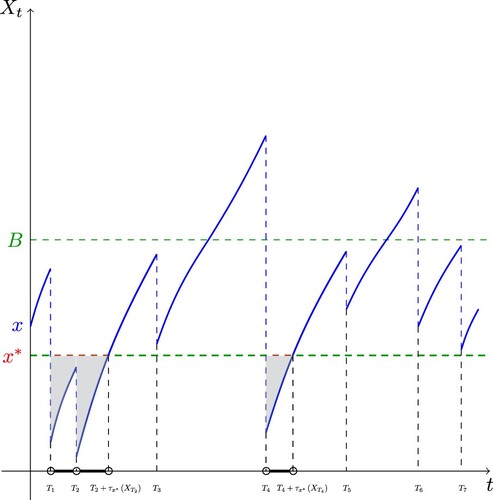

Following Albrecher & Lautscham (Citation2013), we note that for any capital level it holds that

as extreme poverty can only be avoided if there is no event of the Poisson process with level-dependent intensity

during the time the capital process spends below the critical capital

. The above expectation can then be computed by conditioning on the simulated sample path. Concretely, conditioning on the remaining proportions

, with

(23)

(23) with

, we can write

In particular, for the two choices ,

, and

,

, (Equation23

(23)

(23) ) reads

(24)

(24) and

(25)

(25) respectively. Figure depicts a particular path, and the shaded area refers to

as in (Equation23

(23)

(23) ).

Figure 8. Computation of conditional on a realised sample path.

In the following simulations, n capital process paths are generated and for the kth such path, the function is computed as per (Equation24

(24)

(24) ) and (Equation25

(25)

(25) ). The estimator of the probability of extreme poverty is given by

and the two sided

confidence interval of the estimator can be written as

with

, such that the bounds of the confidence interval converge to

for

.

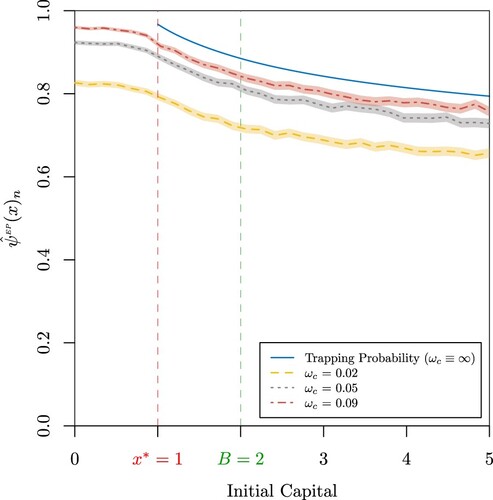

Figures , , and provide an example of the Monte Carlo methodology discussed in this Section 5. A comparison of Figure with Figure , Figure with Figure , Figure with Figure and Figure with Figure , respectively, provides insight into the ability of this method to produce approximations of the probability of extreme poverty when considering more general cases. Although, in general, Monte Carlo simulations produce fairly accurate approximations, it is especially important to note that, for some cases of selected parameters, Monte Carlo simulations may lead to less accurate approximations. Comparing Figures (a) and (a), and Figures (b) and (b), for higher capital cash transfer rates and higher capital barrier levels B, respectively, leads to a clear evidence of this imprecision. In this particular case, the differences between the closed-form formula and the Monte Carlo approximates are mainly due to the fact that for high capital cash transfer rates

and capital barrier levels B, the capital trajectory will grow rapidly up to the capital barrier level B, even in those cases where capital levels close to zero are reached, whereas for the closed-form formula, this would almost certainly be considered as an event of extreme poverty. Nevertheless, it is also worth noting that even though there are the aforementioned discrepancies, Monte Carlo estimates are able to capture the main trend in the probability of extreme poverty.

Figure 9. (a) Probability of extreme poverty when n = 10, 000,

, a = 0.1, b = 4,

, B = 2,

,

and

for

(b) Probability of extreme poverty

when n = 10, 000,

, a = 0.1, b = 4,

,

,

,

and

for

and

.

Figure 10. Probability of extreme poverty when n = 10, 000,

, a = 0.1, b = 4,

,

, B = 2,

,

and

for

.

Figure 11. (a) Probability of extreme poverty when n = 10, 000,

, a = 0.1, b = 4,

, B = 2,

,

and

for

(b) Probability of extreme poverty

when

, a = 0.1, b = 4,

,

,

,

and

for

and

.

Figure 12. Probability of extreme poverty when n = 10, 000,

, a = 0.1, b = 4,

,

, B = 2,

,

and

for

.

As mentioned previously, the proposed methodology could be of great advantage when dealing with dynamics for which closed-form formulas are not available. For instance, one could produce approximates of the probability of extreme poverty for situations under which the remaining proportions of capital after experiencing a loss are non distributed; i.e. when the random variables

follow another distribution with support in

.

6. Conclusion

Using standard techniques from actuarial science and, in particular, from ruin theory, this study analyses the efficiency of regular unconditional cash transfer (UCT) programmes in achieving one of the global public's priority: ending poverty in all its forms everywhere. Introducing an alternative version of the household's capital model originally proposed in Kovacevic & Pflug (Citation2011), where we consider a particular group of households are entitled to benefit from capital cash transfers and, adopting ideas from the Omega risk process, first introduced in Albrecher et al. (Citation2011), this article focuses in studying two main random variables: the trapping time and the time of extreme poverty. While the trapping time has been previously studied for more common risk processes (see, for example, Flores-Contró et al. (Citation2021) and Flores-Contró (Citation2024)), for the best of our knowledge, this is the first work that considers the trapping time and the time of extreme poverty under the dynamics of a household's capital process that incorporates capital cash transfers. Furthermore, for the particular case of the time of extreme poverty, this work also introduces the concept of the extreme poverty rate function for the first time. This article analyses the behaviour of two main risk measures associated to these random times: the trapping probability and the probability of extreme poverty.

From a ruin-theoretic perspective, our main contribution is obtaining closed-form solutions for both risk measures, which is considered to be the ideal situation when working with ruin probabilities (Asmussen & Albrecher Citation2010). We derive explicit formulas for both the trapping probability and the probability of extreme poverty assuming the proportion of the remaining capital of a household after experiencing a loss is distributed. Moreover, for the particular case of the probability of extreme poverty, we also consider two examples of extreme poverty rate functions for which closed-from solutions for the probability of extreme poverty are available: constant and exponential extreme poverty rate functions. Nevertheless, explicit formulas are generally not straightforward to obtain for more general cases. Hence, following Albrecher & Lautscham (Citation2013), in Section 5 we also illustrate how to produce approximates of the probability of extreme poverty via an efficient Monte Carlo simulation method.

Numerical examples presented in Sections 3 and 4 indicate that regular UCT programmes are an efficient social protection strategy to keep households out of poverty and extreme poverty, as their trapping probability and the probability of extreme poverty, respectively, decrease when they are part of such strategy. In particular, the role played by both the capital cash transfer rate and the capital barrier level B for attaining lower probabilities is outlined. Our findings can provide policy makers with a mathematically sound starting point for designing UCT programmes. That is, our model, for instance, could provide insights during the planning phase of an UCT programme to policy makers about the impact on the probability of (extreme) household impoverishment when targeting a particular group of households (depending on the selection of the capital barrier level B). Moreover, the sensitivity of the probability of (extreme) household impoverishment to the frequency or intensity of the capital cash transfers (depending on the choice of the capital cash transfer rate

) can also be assessed with our results. Furthermore, it is important to note that our analyses show that the probability of extreme poverty appears to be more sensitive to changes in these parameters, compared to the trapping probability, therefore suggesting that policy makers should specially watch out on these parameters when designing social protection strategies aimed at reducing extreme poverty.

From the point of view of development economics, previous empirical studies are in line with our findings. Furthermore, our work presents an alternative approach to analyse cash transfer programmes and may represent a point of departure for applying knowledge of another discipline, such as actuarial science, in development economics.

It is important to highlight some of the limitations of our study. For example, due to the construction of the model, our analysis does not capture the direct effect of an UCT programme on a household's consumption. Recently, Habimana et al. (Citation2021) show how Rwanda's UCT programme (VUP-Direct Support) increases a household's total and food consumption. In the same way, in its current form, the capital model is unable to incorporate the rationale behind conditional cash transfer (CCT) programmes, as it does not track any beneficiary actions such as: enrollment and attendance of children and adolescents in school, use of health services and uptake of food and nutritional supplements (Cruz et al. Citation2017). Alternative versions of the proposed model should address these issues.

Finally, future research should also consider the cost of an UCT programme. This cost could be estimated, for instance, by computing the total expected discounted value of capital cash transfers made to a household. This concept would be analogous to other well-known quantities previously studied in ruin theory, such as the expected discounted capital injections (Albrecher & Ivanovs Citation2014). These quantities could, for example, be useful for estimating the required capital cash transfer rate and capital barrier level B such that, for a given social protection budget, the trapping probability or probability of extreme poverty is minimised.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 We know from probability theory that, for a continuous random variable Y, with probability density function , the Laplace transform of

is given by the expected value

.

2 A GitHub repository with some code used in this paper is available at https://github.com/josemiguelflores/TheRoleofDirectCapitalCashTransfers.git.

References

- Abramowitz M. & Stegun I. A. (1972). Handbook of mathematical functions with formulas, graphs, and mathematical tables. Washington, D.C.: U.S. Department of Commerce.

- Adams R. H. (2003). Economic growth, inequality and poverty: findings from a new data set. Number 2972 in Policy Research Working Paper. Washington, D.C.: World Bank Publications.

- Aker J. C. (2013). Cash or coupons? testing the impacts of cash versus vouchers in the democratic Republic of Congo. Center for Global Development Working Paper (320).

- Albrecher H., Cheung E. C. K. & Thonhauser S. (2013). Randomized observation periods for the compound poisson risk model: the discounted penalty function. Scandinavian Actuarial Journal 2013(6), 424–452.

- Albrecher H., Gerber H. U. & Shiu E. S. W. (2011). The optimal dividend barrier in the gamma–omega model. European Actuarial Journal 1(1), 43–55.

- Albrecher H. & Hipp C. (2007). Lundberg's risk process with tax. Blätter der DGVFM 28(1), 13–28.

- Albrecher H. & Ivanovs J. (2014). Power identities for Lévy risk models under taxation and capital injections. Stochastic Systems 4(1), 157–172.

- Albrecher H. & Lautscham V. (2013). From ruin to bankruptcy for compound poisson surplus processes. ASTIN Bulletin 43(2), 213–243.

- Ambler K. & Brauw A. De (2017). The impacts of cash transfers on women's empowerment: learning from Pakistan's BISP program. Number 1702 in Social Protection and Labor Discssion. Washington, D.C.: World Bank Group.

- Asmussen S. & Albrecher H. (2010). Ruin probabilities. Singapore: World Scientific.

- Azaïs R. & Genadot A. (2015). Semi-parametric inference for the absorption features of a growth-fragmentation model. TEST 24(2), 341–360.

- Baird S., Ferreira F. H. G., Özler B. & Woolcock M. (2014). Conditional, unconditional and everything in between: a systematic review of the effects of cash transfer programmes on schooling outcomes. Journal of Development Effectiveness 6(1), 1–43.

- Bjerk D. (2007). Measuring the relationship between youth criminal participation and household economic resources. Journal of Quantitative Criminology 23(1), 23–39.

- Blattman C. & Niehaus P. (2014). Show them the money: why giving cash helps alleviate poverty. Foreign Affairs 93(3), 117–126.

- Brooks-Gunn J. & Duncan G. J. (1997). The effects of poverty on children. The Future of Children 7(2), 55–71.

- Case A., Lubotsky D. & Paxson C. (2002). Economic status and health in childhood: the origins of the gradient. American Economic Review 92(5), 1308–1334.

- Children's Defense Fund (U.S.) (1994). Wasting America's future: the children's defense fund report on the costs of child poverty. Boston: Beacon Press.

- Cruz R. C. d. S., Moura L. B. A. d. & Soares Neto J. J. (2017). Conditional cash transfers and the creation of equal opportunities of health for children in low and middle-income countries: a literature review. International Journal for Equity in Health 16(1), 161.

- Cui Z. & Nguyen D. (2016). Omega diffusion risk model with surplus-dependent tax and capital injections. Insurance: Mathematics and Economics 68, 150–161.

- Davis M. H. A. (1984). Piecewise-deterministic Markov processes: a general class of non-diffusion stochastic models. Journal of the Royal Statistical Society: Series B (Methodological) 46(3), 353–376.

- Duflo E. (2012). Women empowerment and economic development. Journal of Economic Literature50(4), 1051–1079.

- Emran M. S., Robano V. & Smith S. C. (2014). Assessing the frontiers of ultrapoverty reduction: evidence from challenging the frontiers of poverty reduction/targeting the ultra-poor, an innovative program in Bangladesh. Economic Development and Cultural Change 62(2), 339–380.

- Flores-Contró J. M. (2024). The Gerber–Shiu expected discounted penalty function: an application to poverty trapping. Working Paper.

- Flores-Contró J. M., Henshaw K., Loke S. H., Arnold S. & Constantinescu C. D. (2021). Subsidising inclusive insurance to reduce poverty. Working Paper.

- Gao Z. & He J. (2019). The Gerber–Shiu function for the compound poisson omega model with a three-step premium rate. Communications in Statistics - Theory and Methods 48(24), 6019–6037.

- Gao Z., He J., Zhao Z. & Wang B. (2022). Omega model for a jump-diffusion process with a two-step premium rate and a threshold dividend strategy. Methodology and Computing in Applied Probability24(1), 233–258.

- Garcia M. & Moore C. M. T. (2012). The cash dividend: the rise of cash transfer programs in Sub-Saharan Africa. Directions in Development -- Human Development. Washington, D.C.: The World Bank.

- Gauss C. F. (1866). Disquisitiones generales circa seriem infinitam. Ges. Werke Gottingen 2, 437–45.

- Gentilini U. (2022). Cash transfers in pandemic times: evidence, practices, and implications from the largest scale up in history. Washington, D.C.: World Bank.

- Gerber H. U. & Shiu E. S. W. (1998). On the time value of ruin. North American Actuarial Journal2(1), 48–72.

- Gerber H. U., Shiu E. & Yang H. (2012). The omega model: from bankruptcy to occupation times in the red. European Actuarial Journal 2(2), 259–272.

- Habimana D., Haughton J., Nkurunziza J. & Haughton D. M. A. (2021). Measuring the impact of unconditional cash transfers on consumption and poverty in Rwanda. World Development Perspectives23, 100341.

- Handa S. & Davis B. (2006). The experience of conditional cash transfers in Latin America and the Caribbean. Development Policy Review 24(5), 513–536.

- Handa S., Natali L., Seidenfeld D., Tembo G. & Davis B. (2016). Can unconditional cash transfers lead to sustainable poverty reduction? evidence from two government-led programmes in Zambia. Number 2016-21 in Innocenti Working Paper. Florence: UNICEF Office of Research.

- Haushofer J. & Shapiro J. (2016). The short-term impact of unconditional cash transfers to the poor: experimental evidence from Kenya. The Quarterly Journal of Economics 131(4), 1973–2042.

- He J., Gao Z. & Wang B. (2019). Omega model for a jump–diffusion process with a two-step premium rate. Journal of the Korean Statistical Society 48(3), 426–438.

- He Y., Kawai R., Shimizu Y. & Yamazaki K. (2023). The Gerber–Shiu discounted penalty function: a review from practical perspectives. Insurance: Mathematics and Economics 109, 1–28.

- Henshaw K., Ramirez J. M., Flores-Contró J. M., Thomann E. A., Loke S. H. & Constantinescu C. D. (2023). On the impact of insurance on households susceptible to random proportional losses: an analysis of poverty trapping. Working Paper.

- Jensen N. D., Barrett C. B. & Mude A. G. (2017). Cash transfers and index insurance: a comparative impact analysis from Northern Kenya. Journal of Development Economics 129, 14–28.

- Jolliffe D. M., Mahler D. G., Lakner C., Atamanov A. & Baah S. K. Tetteh (2022). Assessing the impact of the 2017 PPPs on the international poverty line and global poverty. Number WPS 9941 in Policy Research Working Paper. Washington, D.C.: World Bank Group.

- Kaszubowski A. (2019). Omega bankruptcy for different Lévy models. Slaski Przeglad Statystyczny23(17), 31–57.

- Kovacevic R. M. & Pflug G. C. (2011). Does insurance help to escape the poverty trap?—a ruin theoretic approach. Journal of Risk and Insurance 78(4), 1003–1028.

- Kyprianou A. E. (2013). Gerber–Shiu risk theory. Switzerland: Springer International Publishing.

- McLaughlin M. & Rank M. R. (2018). Estimating the economic cost of childhood poverty in the United States. Social Work Research 42(2), 73–83.

- Mihálykó E. O. & Mihálykó C. (2011). Mathematical investigation of the Gerber–Shiu function in the case of dependent inter-claim time and claim size. Insurance: Mathematics and Economics48(3), 378–383.

- Pega F., Pabayo R., Benny C., Lee E. Y., Lhachimi S. K. & Liu S. Y. (2022). Unconditional cash transfers for reducing poverty and vulnerabilities: effect on use of health services and health outcomes in low- and middle-income countries. Cochrane Database of Systematic Reviews 3, 201. https://www.cochranelibrary.com/cdsr/doi/10 .1002/14651858.CD011135.pub3/full

- Rank M. R., Eppard L. M. & Bullock H. E. (2021). Poorly understood: what America gets wrong about poverty. New York: Oxford University Press.

- Rank M. R., Hirschl T. A. & Foster K. A. (2014). Chasing the American dream: understanding what shapes our fortunes. New York: Oxford University Press.

- Ravallion M. (2016). The economics of poverty: history, measurement, and policy. New York: Oxford University Press.

- Seaborn J. B. (1991). Hypergeometric functions and their applications. New York: Springer-Verlag.

- Slater L. J. (1960). Confluent hypergeometric functions. New York: Cambridge University Press.

- Sumner A., Hoy C. & Ortiz-Juarez E. (2020). Estimates of the impact of COVID-19 on global poverty. UNU-WIDER 43, 1–14. https://www.econstor.eu/handle/10419/229267.

- United Nations (2015). Transforming our world: the 2030 agenda for sustainable development. Number A/RES/70/1. New York: United Nations.

- United Nations and World Summit for Social Development (1996). Report of the world summit for social development: copenhagen, 6–12 March 1995. Number 96.IV.8 in A/CONF. 166. New York: United Nations Publication.

- Vera-Cossio D. A., Hoffmann B., Pecha C., Gallego J., Stampini M., Vargas D., Medina M. P. & Álvarez E. (2023). Re-thinking social protection: from poverty alleviation to building resilience in middle-income households. Number IDB-WP-1412 in IDB Working Paper. Inter-American Development Bank.

- Wang X., Wang W. & Zhang C. (2016). Ornstein–Uhlenback type omega model. Frontiers of Mathematics in China 11(3), 737–751.

- World Bank (2018). Poverty and shared prosperity 2018: piecing together the poverty puzzle. Washington, D.C.: World Bank Group.

Appendices

Appendix 1.

Appendix 1. Mathematical Proofs

A.1. Proof of Theorem 3.1

For , the capital immediately before the first capital loss is

. Hence, by conditioning on the time and the remaining proportion of the first capital loss and discounting the expected values to time 0 at the force of interest δ, when

we obtain

(A1)

(A1) The above equation for

involves

for

. When the initial capital is below the capital barrier level B, the capital growth is driven by both the capital growth rate r and the capital transfer rate

before the capital returns to the capital barrier level B. Thus, for

, let

be the solution to

with

. Namely,

, which is the time when the capital returns to the capital barrier level B if no capital loss occurs prior to time

. Furthermore,

for

and

. Moreover,

is the capital at time

if no capital loss occurs prior to time

. Thus, by conditioning on the time and the remaining proportion of the first capital loss and discounting the expected values to time 0 at the force of interest δ, when

we obtain

(A2)

(A2) Now, changing variables

in (EquationA1

(A1)

(A1) ), we obtain (Equation3

(3)

(3) ). Moreover, first changing variables

in the integrals with respect to t from 0 to

in (EquationA2

(A2)

(A2) ), and then changing variables

in the integrals with respect to t from

to ∞ in (EquationA2

(A2)

(A2) ), we obtain (Equation4

(4)

(4) ).

A.2. Proof of Proposition 3.1

When , i.e.

with

, Equations (Equation9

(9)

(9) ) and (Equation10

(10)

(10) ) can be written such that when

,

(A3)

(A3) and when

,

(A4)

(A4) Applying the operator

to both sides of (EquationA3

(A3)

(A3) ) and (EquationA4

(A4)

(A4) ), together with a number of algebraic manipulations, yields to the following second order Ordinary Differential Equations (ODEs),

(A5)

(A5) and

(A6)

(A6) Letting

for i = u, l, such that

and

are associated with the change of variables

and

, respectively, Equations (EquationA5

(A5)

(A5) ) and (EquationA6

(A6)

(A6) ) reduce to Gauss's Hypergeometric Differential Equation (Slater Citation1960)

(A7)

(A7) for

,

,

,

and

with regular singular points at

(corresponding to

and ∞). A general solution of (EquationA7

(A7)

(A7) ) in the neighbourhood of the singular point

is given by

for arbitrary constants

(see for example, equations (15.5.7) and (15.5.8) of Abramowitz & Stegun (Citation1972)). Here,

(A8)

(A8) is Gauss's Hypergeometric Function (Gauss Citation1866) and

denotes the Pochhammer symbol (Seaborn Citation1991).

To determine the constants and

we use the boundary conditions at

and at ∞. In addition, we use (Equation5

(5)

(5) ), (Equation8

(8)

(8) ) and the differential properties of Gauss's Hypergeometric Function

The boundary condition

, by definition of

in (Equation2

(2)

(2) ), thus implies that

. Moreover, letting

in (Equation10

(10)

(10) ) yields

Hence, this yields to

(A9)

(A9)

(A10)

(A10) and

(A11)

(A11) where

denotes the Regularised Hypergeometric Function. Therefore, the Laplace transform of the trapping time is given by (Equation11

(11)

(11) ).

A.3. Proof of Theorem 4.1

Using similar arguments as those for Theorem 3.1, we know that for , the capital immediately before the first capital loss is

and the capital has three possibilities at time t, that it is more than B, that it is between

and B, and that it is between 0 and

. Thus, by conditioning on the time and the remaining proportion of the first capital loss and discounting the expected values to time 0 at the force of interest δ, when

we obtain

(A12)

(A12) Then, doing the change of variable

in the integrals with respect to t from 0 to ∞ in (EquationA12

(A12)

(A12) ), we obtain (Equation12

(12)

(12) ).

For , there are two possibilities. First,

and the capital has not yet reached the capital barrier level B. In this case, we know the capital immediately before time t is

and the capital has two possibilities at time t, that it is between

and B, and that it is between 0 and

. Second, for

, that is, no capital loss occurs before the capital exceeds the capital barrier B. In this case, we also know the capital immediately before time t is

and the accumulated capital has three possibilities at time t, that it is more than B, that it is between

and B, and that it is between 0 and

. Hence, by conditioning on the time and the remaining proportion of the first capital loss and discounting the expected values to time 0 at the force of interest δ, when

we obtain

(A13)

(A13) Now, first changing variables

in the integrals with respect to t from 0 to

in (EquationA13

(A13)

(A13) ), and then changing variables

in the integrals with respect to t from

to ∞ in (EquationA13

(A13)

(A13) ), we obtain (Equation13

(13)

(13) ).

For , let

be the solution to

Namely,

, which is the time when the capital returns to the critical capital

if no capital loss occurs prior to time

. Furthermore,

for

and

. Moreover,

is the capital at time

if no capital loss occurs prior to time

.

Thus, for , there are three possibilities. First,

and the capital up to time t has not reached the critical capital

. In this case, the capital immediately before time t is

. Second,

and the capital has not yet reached the capital barrier level B and no capital loss occurs before the capital exceeds the critical capital

. In this case, the capital immediately before time t is

and the capital up to time t has two possibilities, that it is between

and B, and that it is between 0 and

. Third,

, that is, no capital loss occurs before the capital up to time t exceeds the capital barrier level B. In this case, the capital immediately before time t is

and the capital up to time t has three possibilities, that it is more than B, that it is between

and B, and that it is between 0 and

. Hence, by conditioning on the time and the remaining proportion of the first capital loss and discounting the expected values to time 0 at the force of interest δ, when

we obtain

(A14)

(A14) Now, first changing variables

and

in the integrals with respect to t from 0 to

in (EquationA14

(A14)

(A14) ), then changing variables

in the integrals with respect to t from

to

in (EquationA14

(A14)

(A14) ) and lastly changing variables

in the integrals with respect to t from

to ∞ in (EquationA14

(A14)

(A14) ) we obtain (Equation14

(14)

(14) ).

A.4. Proof of Proposition 4.1

When , i.e.

with

, Equations (Equation17

(17)

(17) ), (Equation18

(18)

(18) ) and (Equation22

(22)

(22) ) can be written such that when

,

(A15)

(A15) when

,

(A16)

(A16) and when

,

(A17)

(A17) Applying the operator

to both sides of (EquationA15

(A15)

(A15) ), (EquationA16

(A16)

(A16) ) and (EquationA17

(A17)

(A17) ), together with a number of algebraic manipulations, yields to the following second order ODEs,

and

(A18)

(A18) Hence, for

,

satisfies the nonhomogeneous differential Equation (EquationA18

(A18)

(A18) ), when the extreme poverty rate function

(constant value) and the penalty function

. The particular solution of

is

Therefore, the general solution of

is given by

where

is the homogeneous solution of (EquationA18

(A18)

(A18) ). Then, following a similar procedure to that of Proposition 3.1, letting

, such that

is associated with the change of variable

, the homogeneous part of Equation (EquationA18

(A18)

(A18) ) reduces to Equation (EquationA7

(A7)

(A7) ) for

,

and

, with regular singular points at

(corresponding to x = 0, B and ∞). A general solution of (EquationA7

(A7)

(A7) ) in the neighbourhood of the singular point

is given by

(A19)

(A19) for arbitrary constants

(see for example, equations (15.5.3) and (15.5.4) of Abramowitz & Stegun (Citation1972)). Due to the fact that

is finite, we can then conclude that

, as the second term of (EquationA19

(A19)

(A19) ) is unbounded when

for

. Thus, the solution of

is given by

Then, following the proof of Proposition 3.1, one can easily obtain the solutions for

and

, when

and

, respectively.

Considering the continuity of and

at the critical capital

and the capital barrier level B, that is, using (Equation15

(15)

(15) ), (Equation16

(16)

(16) ), (Equation20

(20)

(20) ) and (Equation21

(21)

(21) ), one can derive a system of equations from which the unknown coefficients

,

,

and

, can be determined to obtain an explicit solution for

.

A.5. Proof of Proposition 4.2

Following a similar procedure to that in Appendix A.4, for , one can derive from (Equation22

(22)

(22) ) the following nonhomogeneous second order ODE for

, when the extreme poverty rate function

(exponential extreme poverty rate), the penalty function

and the force of interest

,

(A20)

(A20) Clearly,

is always a particular solution of Equation (EquationA20

(A20)

(A20) ), so that one can write

where

is the homogeneous solution of (EquationA20

(A20)

(A20) ). Now, making the substitution

, Equation (EquationA20

(A20)

(A20) ) yields to the following second order ODE

A second substitution,

, such that

, produces Equation (EquationA7

(A7)

(A7) ) for

,

and

, with regular singular points at

(corresponding to x = 0, B and ∞). Thus, knowing that a general solution of (EquationA7

(A7)

(A7) ) in the neighbourhood of the singular point

is of the form (EquationA19

(A19)

(A19) ) and that

one obtains the homogenous solution

(A21)

(A21) for arbitrary constants

. Due to the fact that

is finite, we can then conclude that

, as the first term of (EquationA21

(A21)

(A21) ) is unbounded when

for

. Hence, the solution of

is given by

As in Appendix A.4, following the proof of Proposition 3.1 for

, one can easily obtain the solutions for

and

, when

and

, respectively.

Finally, due to the continuity of and

at the critical capital

and the capital barrier level B, that is, using (Equation15

(15)

(15) ), (Equation16

(16)

(16) ), (Equation20

(20)

(20) ) and (Equation21

(21)

(21) ) for

and

, one can derive a system of equations from which the unknown coefficients

,

,

and

, can be determined to derive a closed-form expression for

.

Appendix 2.

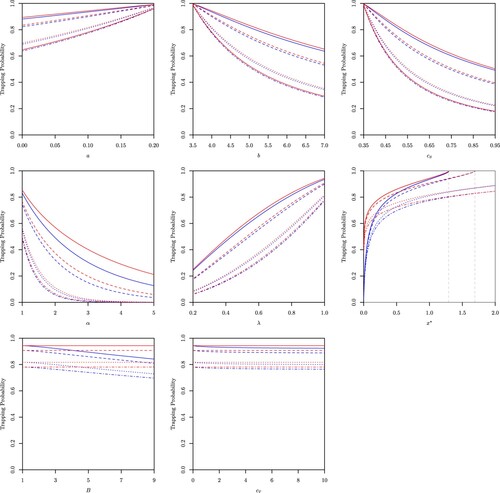

Effects of underlying factors on the trapping probability

We consider the influence of the parameters on the trapping probability by varying them in a reasonable range, keeping all other parameters constant. The reference setup is given below.

Reference setup: a = 0.1, b = 4, ,

,

,

, B = 2 and

.

Appendix 3.

Effects of underlying factors on the probability of extreme poverty

We consider the influence of the parameters on the probability of extreme poverty by varying them in a reasonable range, keeping all other parameters constant. The reference setup is given below.

Reference setup: a = 0.1, b = 4, ,

,

,

, B = 2,

,

and

.

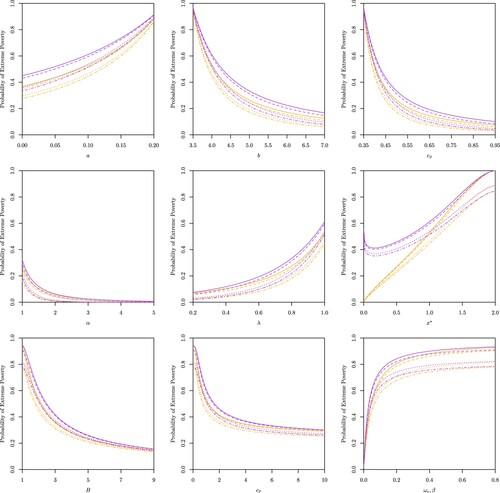

Figure A1. Effects of the rate of consumption , income generation

, investment or savings

, the parameter of the Beta distribution

(i.e. expected remaining proportion of capital), the expected capital loss frequency

, the critical capital

, the capital barrier level

and the capital transfer rate

on the trapping probability of the original model obtained in Henshaw et al. (Citation2023) (in red) and on the trapping probability of the model with capital cash transfers (in blue) for initial capital

.

Figure A2. Effects of the rate of consumption , income generation

, investment or savings

, the parameter of the Beta distribution

(i.e. expected remaining proportion of capital), the expected capital loss frequency

, the critical capital

, the capital barrier level

, the capital transfer rate

and the extreme poverty rate function on the probability of extreme poverty for a constant extreme poverty rate function (in orange) and an exponential extreme poverty rate function (in purple) for initial capital

.