Abstract

Financial systemic risk has an impact on the real economy and may trigger a chain reaction in the whole economic system leading to the financial crisis. Many scholars focus on financial systemic risk, but few of them are bibliometric analyses. Therefore, this paper explores the status quo, emerging trends, and transition trajectory through the above analysis method in the research field from 1990 to 2020. Based on the above analysis, we find the following conclusions: (1) The basic conclusions of the most productive countries, institutions, journals, authors, status quo, and the change of hotspots in this research field are presented. (2) The emerging trends in this research field are ‘credit risk’, ‘capital shortfall’, ‘spill-over’, ‘spread’, ‘financial market’, ‘interconnectedness’, ‘transmission’ in the last three years. (3) The research field of financial systemic risk presents an S-shaped transition trajectory through the local forward, the local backward, the global standard, and the global key-route main path analysis. (4) We find that the most cited authors are not always at the core of the trajectory of financial systemic risk research. The emerging trend ‘credit risk’ is also recently a core research direction in this research field’s transition trajectory.

1. Introduction

Since the outbreak of the 2008 global financial crisis, the financial systemic risk research field is gradually getting a lot of attention, such as bankruptcy and systemic risk (Stolbov & Shchepeleva, Citation2020), the regulation of financial systemic risk (Bitar, Citation2021) and systemic risk of the overlapping portfolio (Jiang & Fan, Citation2021). Although many scholars analysed financial systemic risk research from different angles in recent years, few of them explored the status quo, emerging trends, and transition trajectory of this research field through bibliometric analysis. Bibliometric analysis is a kind of scientific technology identifying the core literature, key information, and future directions of research fields. It has been widely used in many areas, such as sustainable resources (Leong, Citation2021), green infrastructure (Ying et al., Citation2021), financial innovation (Li & Xu, Citation2021) and business research (Alshater et al., Citation2021).

As the number of articles in the financial systemic risk field increases, it becomes necessary to summarise and analyse the status quo, emerging trends, and dynamic development trajectory of the research field. Thus, bibliometric analysis is applied in this paper to mapping research knowledge in the financial systemic risk field from dynamic and visual perspectives. This paper analyzes the published publications of 2,088 financial systemic risk studies retrieved from the economics or business finance section of Web of Science (WoS) from 1990 to 2020 to study the status quo, emerging trends, and transition trajectory of the financial systemic risk research via CiteSpace and Pajek. Furthermore, this article also follows the following goals: (1) To summarise the basic conclusions of the most productive countries, institutions, journals, authors, status quo, and the change of hotspots in this research field. (2) To identify emerging trends in financial systemic risk research. (3) To find the main development trajectory in financial systemic risk research. (4) To conclude the analysis of the financial systemic risk research from an aspect of multiple network to further explore this field and guide future research.

To achieve research goals, the structure of this paper is constructed as follows: Section 2 reviews the relevant literature on financial systemic risk and bibliometric analysis. Section 3 conducts the publication analysis and the co-citation analysis of financial systemic risk research. Section 4 recognises the most productive countries, institutions, journals, authors, status quo, and the change of hotspots through multiple analyses. Section 5 carries out burst detection and keyword analysis to identify the emerging trends. Section 6 reveals the main development trajectory of financial systemic risk by the main path analysis. Besides, Section 6 combines the multiple network analysis in Section 4 and Section 5 to explore features and regular patterns of the financial systemic risk research. Section 7 provides further discussions. Section 8 concludes.

2. Relevant literature review

2.1. Financial systemic risk

Financial systemic risk is defined as the possibility of significant fluctuations in the entire financial system (Lehar, Citation2005), which may cause financial information disruption (Abdymomunov, Citation2013), financial institution malfunction (Yin et al., Citation2021), financial liquidity problem (Davydov et al., Citation2021), and risk contagion (Wu et al., Citation2021).

Considering the severe consequences resulted by financial systemic risk (Patro et al., Citation2013), some scholars began to study the driving forces of the financial systemic risk at the micro-level and macro-level. At the micro-level, financial systemic risk is generated from various aspects, such as the credit of the financing plat-form (He & Chen, Citation2016), the risk exposure of participant (Halili et al., Citation2021) and bank risk shifting (Elliott et al., Citation2021); At the macro-level, financial systemic risk is affected by many factors, such as macroprudential policy (Zhang et al., Citation2020a), macroeconomic activity (Kapinos et al., Citation2020) and a series of main systemic events (Morelli & Vioto, Citation2020).

It is not enough to explore the driving forces of the financial systemic risk, and therefore, various methods are applied to quantify it. The conditional value-at-risk (CoVaR) is the most popular method to quantify financial systemic risk. Many scholars combined it with the GARCH model (Girardi & Ergun, Citation2013), quantile regression (Adrian & Brunnermeier, Citation2014; Xu et al., Citation2021), and Granger causality network (Gong et al., Citation2019) to measure the financial systemic risk. Moreover, some new approaches are also applied to measure the financial systemic risk in recent years, such as economic indicator (Li & Perez-Saiz, Citation2018) and machine learning (Nyman et al., Citation2021).

Although scholars are increasingly paying attention to the financial systemic risk research, there is still a gap between bibliometrics and the field of financial systemic risk research. Accordingly, it is meaningful to explore the financial systemic risk through bibliometric analysis, which can not only summarise the status quo and identify hot topics but also predict future research directions.

2.2. The bibliometric analysis

Bibliometric analysis is a kind of scientific knowledge capture method and analysis technology, which can visually analyse the research field to find the development process, status quo, and emerging trends of the area (Wang et al., Citation2021). Many software can be used for bibliometric analysis, such as CiteSpace, Pajek, Gephi, VOSviewer, and HistCite. Among them, CiteSpace is the most widely used bibliometric analysis software, which can quickly mine and visualise the scientific and technological texts (Chen, Citation2006; Chen et al., Citation2012). Furtherly, CiteSpace also can reveal the potential problems (Feng et al., Citation2015), the major disciplines (Li et al., Citation2017), the relations of cooperation (Ouyang et al., Citation2018), the hotspots (Hu et al., Citation2019), and the emerging trends of the research field (Zhang et al., Citation2020b; Azam et al., Citation2021). Besides, the main path analysis is a unique bibliometric analysis method based on time flow analysis, which can extract the most core citation relationships in the development process and dig out the dynamic development trajectory of the research field (Hummon & Dereian, 1989). This method is widely adopted in the area of text mining (Jung & Lee, Citation2020) and the blockchain domain (Yu & Pan, Citation2021).

Although bibliometric analysis has been applied in many fields, there are few studies exploring the financial systemic risk research field through bibliometric analysis. Therefore, we adopt the method of bibliometric technology to present a more comprehensive analysis in the field of financial systemic risk research.

3. Publication analysis and co-citation analysis

3.1. A database for bibliometrics

To do co-citation analysis and main path analysis of this research field by CiteSpace and Pajek, we should build a database firstly. The first step is to find the data source. Considering that WoS is a huge platform that allows readers to access specific information about articles published in approximately 12,000 leading journals worldwide, we choose WoS as the data source. The second step is to find relevant articles from databases via an appropriate topic. By researching the topic ‘systemic risk’ from the economics or business finance section of Web of Science, 2088 relevant articles published from 1990 to 2020 are found. The following reasons are chosen for the research period from 1990 to 2020: (1) The papers published before are unavailable in WoS data-space. (2) Published articles from 1990 to 2020 reflect a complete research development process in this research field. (3) The latest data of the financial systemic risk research field are included until 2020. Then we will use CiteSpace and Pajek to perform co-citation analysis, main path analysis, and other analysis on the above-mentioned related data.

3.2. Publication analysis of the financial systemic risk research

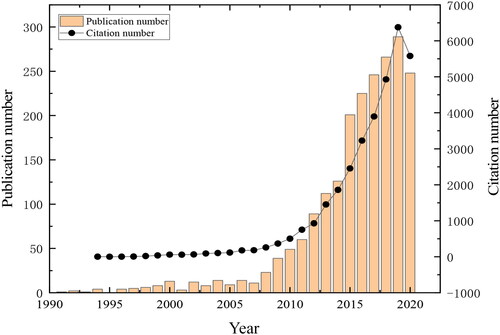

The literature data of financial systemic risk research is collected from the Social Sciences Citation Index, the Conference Proceedings Citation Index-Social Sciences and Humanities, the Book Citation Index-Social Sciences and Humanities, and the Emerging Sources Citation Index, via WoS on Oct 13, 2020. There are 2088 articles published from 1990 to 2020. shows the number of publications and citations per year. As shown in , literature related to financial systemic risk research firstly emerges in 1991, and then there is a low and stable phase in this research field until 2007. After 2008, the literature related to financial systemic risk research is going fast. Thus, this paper divides the whole period into two phases: Phase one (slow development stage: 1990–2007) and Phase two (flouring stage: 2008–2020).

Figure 1. The number of publications and citations per year in financial systemic risk research.

Source: Author.

As shown in , there are few publications and citations in the slow development stage. According to the records on WoS, between 1990 and 2007, the average number of published articles each year is just 6.76, and the average citations per item are 52.88. Although the number of publications is small between 1990 and 2007, some papers published in this phase have far-reaching implications for further research. Berger et al. (Citation1999) devised a structure for evaluating mergers in the financial services industry, which has an enlightening effect on the development of financial systemic risk. Besides, some essential areas related to financial systemic risk are excavated, such as credit problem (Eisenberg & Noe, Citation2001) and financial stability (Nier et al., Citation2007). After 2008, a chain of financial crises has occurred all over the world. Scholars find that the financial fields around the world are a closely connected whole (Elliott et al., Citation2014). Therefore, the importance of financial systemic risk is widely recognised, and a series of publications on financial systemic risk have been published in large numbers. As shown in , the number of publications and citations increases quickly after 2008. The average number of articles published each year rises to 151.77, the average citations per item rise to 2506.23, which also implies the field of financial systemic risk is widely concerned after the 2008 financial crisis. In the flouring stage, some hot and vital topics in the field of financial systemic risk are being studied, such as financial crises (Billio et al., Citation2012), financial institutions' return volatilities (Diebold & Yilmaz, Citation2014) and financial contagion (Acemoglu et al., Citation2015). More significantly, researchers pay attention to the measurement of financial systemic risk, which makes a lot of sense for the safety of the entire financial system. Feinstein et al. (Citation2017) explored the system risk measurement method based on the capital endowment. Gong et al. (Citation2019) constructed a measurement of financial systemic risk, which is based on causal network and connectivity analysis.

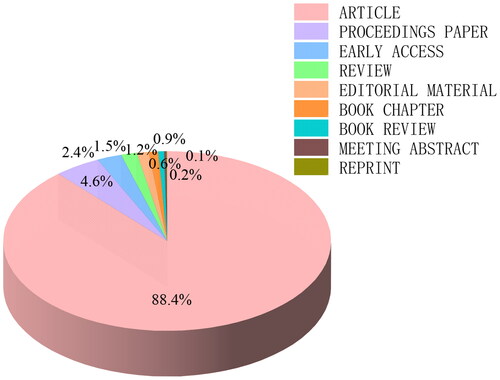

Besides, and respectively show the document type and the top 10 subject categories of financial systemic risk research. As shown in , there are many kinds of literature in financial systemic risk research, such as article, proceeding paper, early access, and review. Among them, the article is the most important form of literature in this research, which accounts for 88.4%. Besides, as shown in , there are many subjects in the financial systemic risk research fields, which means this research field is interdisciplinary and multidisciplinary, covering economics, finance, business, management, mathematics, sociology, and environmental science.

Figure 2. The document type of the financial systemic risk research.

Source: Author.

Table 1. The top 10 subject categories in the financial systemic risk research.

3.3. Co-citation analysis of the financial systemic risk research

To better map the development of the financial systemic risk field, co-citation analysis is applied to explore the dynamic development process and inherent law of this field. Co-citation analysis is a dynamic analysis model describing the development of knowledge, which is formed by the co-citation relationship in the citation network. Besides, different from the static results of the coupled analysis, the results of co-citation are constantly changing with time and research objects, which can better satisfy the needs of the development process of financial systemic risk research.

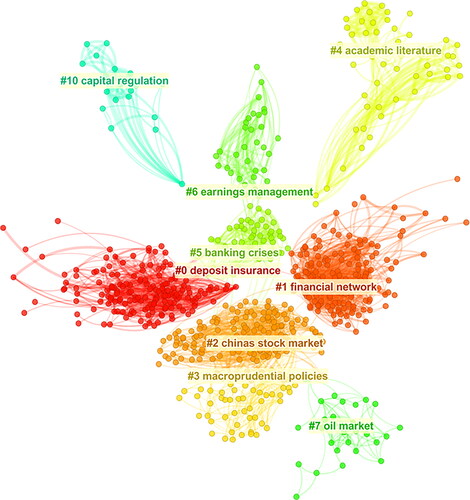

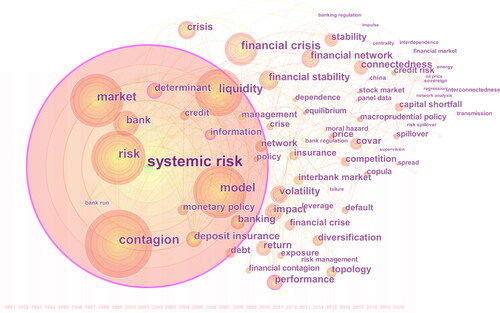

In this paper, the co-citation analysis of financial systemic risk research uses CiteSpace software to process data from WoS. shows the result of the co-citation analysis. As shown in , the co-citation analysis network is aggregated into 9 different coloured areas. Each area of different colours corresponds to a label and a serial number. The smaller the cluster number, the larger the cluster size. Besides, the density of nodes reflects the size of clusters. The larger the cluster, the denser the nodes. The red area represents the largest cluster #0. The areas of orange-red, earthy orange, yellow, yellow-green, grass green, light-green, dark-green, and blue-green respectively represent cluster #1, cluster #2, cluster #3, cluster #4, cluster #5, cluster #6, cluster #7, and cluster #10. shows the details of the largest six clusters. The labels of these six clusters are deposit insurance, financial network, China’s stock market, macroprudential policies, academic literature, and banking crises. Tags are named according to the LLR algorithm. LLR algorithm is used for clustering topic extraction to make the resulting clustering labels consistent with the actual situation and less repeated. Besides, the homogeneity of the cluster is judged by the silhouette score. Generally, clustering is considered reasonable if the silhouette is greater than 0.5, and if the value of the silhouette is closer to 1, the clustering results are more convincing.

Figure 3. Cluster network in the financial systemic risk research.

Source: Generated using CiteSpace on data.

Table 2. Summary of the largest 6 clusters.

Combining , all of the silhouette scores are above 0.6, which means that the generated clusters are all convincing. Cluster #0 is the largest cluster, and its number of references is 167. Besides, all of the largest 6 clusters’ mean years are after 1998. More importantly, the label of the 9 clusters also reveals the most widely studied topic in financial systemic risk research field (Chen, Citation2006). We find that the topics deposit insurance, financial network, banking crises and macroprudential policies are related to the 2008 global financial crisis. It indicates that the 2008 global financial crisis not only has a profound impact on the economic and financial field but also has a massive impact on the research field of financial systemic risk.

shows the most cited articles with co-citation frequency, the top 10 cited articles are all cited more than 100 times, and the most cited paper is from #5 with 275 citations. And the second, third, fourth, the fifth cited paper are from cluster #3, cluster #6, cluster #4, and cluster #2. Furthermore, there are three articles from cluster #5 with 496 citations in the top 10 most cited articles with co-citation frequency, which shows that cluster #5 is an essential component in studying financial systemic risk. Billio et al. (Citation2012) devised several econometric measures on financial systemic risk. Adrian and Brunnermeier (Citation2014) provided out-of-sample forecasts of a countercyclical, forward-looking measure of systemic risk. To assess the ability of financial institutions to respond to financial crises, Acharya et al. (Citation2012) used a method of public information to measure capital shortage, which explores the characteristics of systemic risk and gives a reliable explanation for the financial crisis. Acemoglu et al. (Citation2015) found that a more closely connected financial network will improve financial stability. Acharya et al. (Citation2017), Brunnermeier and Pedersen (Citation2009), Diebold and Yilmaz (Citation2014), Girardi and Ergun (Citation2013), and Elliott et al. (Citation2014) explored the field of systemic risk from the view of the systemic expected shortfall, liquidity model, connectedness, financial distress, and interdependent financial organisations. Those are not only mainstream research directions that are highly concerned and highly recognised in financial systemic risk research but also the cornerstone of this research field.

Table 3. Top 10 most cited articles with co-citation frequency.

Furthermore, shows the result of double figures overlay in financial systemic risk research, the left graph represents the citing disciplines, and the right graph represents the cited disciplines. We find that papers in the financial systemic risk research field are not only cited by many disciplines with high relevance but also cited by other disciplines with weak relevance, which implies that the papers in this field have been widely recognised. For example, the cited disciplines about economics, economic, and politics are not only cited by themselves but also cited by disciplines about Medicine, Medical, Clinical, and disciplines about Mathematics, Systems, Mathematical.

Figure 4. Double figures overlay in the financial systemic risk research.

Source: Generated using CiteSpace on data.

4. The basic factor analysis of the financial systemic risk research

4.1. Basic analysis from the perspective of countries and institutions

Obviously, the more a country & region publishes, the more contributions they made in a certain research field. Furthermore, the most productive institutions are likely to come from the most productive counties & regions in financial systemic risk. In this paper, the record of WoS is chosen to identify the most productive countries, institutions, journals, and authors. Besides, the collaboration network among countries, institutions, and authors is analysed by CiteSpace.

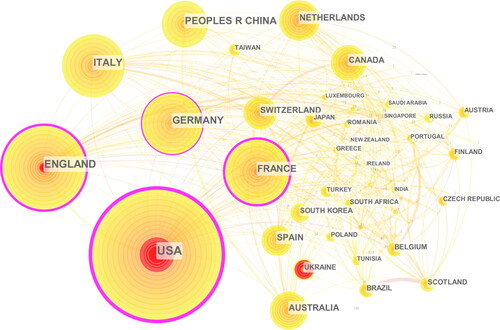

The top 15 countries with the most publications about financial systemic risk research are listed in . And shows the country's collaboration network in financial systemic risk research. Combining with and , the USA is the most productive country, including 635 papers, followed by England (323), Germany (215), Italy (196), the People’s Republic of China (184), France (178), Australia (103), Netherlands (95), Spain (94), Canada (86), Switzerland (79), Ukraine (41), South Korea (40), Scotland (37), Belgium (36). Furthermore, the USA also has the highest total citations, the highest average citations. As can be seen from , these countries have formed a national cooperation network in the financial systemic risk research with a different number of links. The existence of links depends on the cooperation between the countries.

Figure 5. A visualisation of the country’s collaboration network.

Source: Generated using CiteSpace on data.

Table 4. Top 15 productive countries in financial systemic risk research.

Moreover, a node with purple outer rings is of great importance. CiteSpace uses purple circles to mark countries whose betweenness centrality is higher than 0.1 (or authors, journals, institutions, etc.) (Chen, Citation2006; Zhou & Xu, Citation2020). And nodes with red inside rings represent a sudden large number of citations (Chen, Citation2006). Consider the number of links, the USA has the most cooperation with other countries in financial systemic risk research, which is closely related to the number of published articles in the USA. Furthermore, the USA, England, Germany, France have purple outer rings showing their great importance in the national cooperation network. Besides, we find that the prolific countries have more cooperation with other countries in this research. The publications of the USA account for more than 30% of the publications related to financial systemic risk research in the world, and research teams in the USA have more collaboration with other countries in this research. Although the rest of the countries’ publications are relatively less, they also profoundly impact this research area.

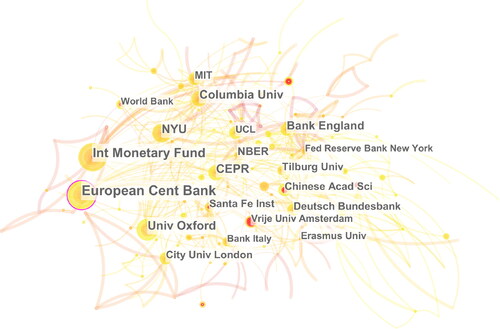

The top 15 institutions which have made significant contributions in the research area are listed in . As shown in , the European Central Bank has published the most paper, but its total citations and average citations are not the most. The following are the International Monetary Fund, University of Oxford, Centre for Economic Policy Research, and New York University. Columbia University is in sixth place with 31 publications, and its H-index is 16, which is the highest. H-index is a mixed quantitative index that can evaluate the amount of academic output and the level of academic output of researchers, which means Columbia University has an important influence in financial systemic risk research. The seventh place is the Bank of England, followed by the National Bureau of Economic Research, Deutsche Bundesbank, Massachusetts Institute of Technology, Tilburg University, University of Pennsylvania. World Bank is in thirteenth place, which has the highest average citation levels, followed by the Chinese Academy of Sciences, University of London.

Table 5. Top 15 productive and influential institutions in the financial systemic risk research.

Among the top 15 most productive and influential institutions, most institutions are from the USA. As a result, the most productive institutions are from the most productive countries. Therefore, the institutions in the USA have significantly influenced financial systemic risk research. Although the institutions in Germany are less, the European Central Bank has the maximum number of research outputs and the second-highest h index value in this research field, meaning Germany has made many contributions in the financial systemic risk research area. Also, shows the collaboration network among institutions in the world between 1990 and 2020. The European Central Bank, the International Monetary Fund, the University of Oxford, and the Centre for Economic Policy Research collaborate with other institutions. As we know, those four institutions are both from prolific countries: The USA, England, and Germany, which indicates the development of academic research depends heavily on cooperation among institutions.

Figure 6. A visualisation of the institution’s collaboration network.

Source: Generated using CiteSpace on data.

4.2. Basic analysis from the perspective of journals and authors

As shown in , the top 15 journals studying financial systemic risk research are identified, according to the statistics from the WoS. Journal of Banking Finance is the most productive journal in this field with 153 publications, and its H-index is 39, which is the highest. The second place is the Journal of Financial Stability, following by Quantitative Finance, Journal of Economic Dynamics Control, Economic Modelling, and Journal of International Financial Markets Institutions Money. Among them, the H-index of the Journal of Financial Stability is the highest, which means this journal also has made many contributions to financial systemic risk research. Besides, the articles published by the Journal of Financial Stability also made contributions to this research area, such as ‘Simulation methods to assess the danger of contagion in interbank markets’ (Upper, Citation2011). Upper (Citation2011) summarised the findings of estimating the simulated risk of contagion due to the risk exposure of the interbank loan market. Furthermore, more than half of the journals are published in the USA and Netherlands, which shows they make many contributions in this field.

Table 6. Top 15 productive journals in financial systemic risk research.

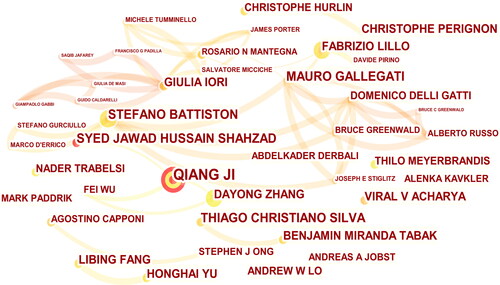

illustrates the top 15 productive authors in this research field. According to the records on WoS, Ji is the most productive author with many contributions. Besides, Demirguc-kunt has the largest total citation number and the highest H-index. Therefore, Demirguc-kunt is a leading scholar in financial systemic risk research. Furthermore, Ji and Acharya also have the highest H-index with a value of 9, which means they also have made significant contributions in this research area. Besides, shows the collaboration network among authors in the world between 1990 and 2020. The loose structure and the few connections between nodes in indicate that there is less cooperation among authors worldwide, which shows that the author’s cooperation network in the field of financial systemic risk research is still in the immature stage.

Figure 7. A visualisation of the author’s collaboration network.

Source: Generated using CiteSpace on data.

Table 7. Top 15 productive authors in the financial systemic risk research.

According to the above analysis of countries, institutions, journals, and authors, we find that the USA is the most significant contributor in the financial systemic risk research field, with the largest number of articles and the most substantial influence in this field of research. Furtherly, the USA is the most important component in the collaboration networks in this field.

5. Emerging trends in the financial systemic risk research field

The emerging trends give researchers future directions and methodologies in the research field. Therefore, keyword analysis and citation burst detection are used in this section to analyse articles that have received rapidly increasing citations and to dig deeper into emerging trends in financial systemic risk research.

Citation bursts represent articles that have received sudden increases in citations, implying that articles received extraordinary attention from their scientific community (Zhou et al., Citation2019). shows the top 10 references with the strongest citation bursts. As shown in , we can also observe the impact duration of each reference with the strongest citation burst. In the sixth column of , each black line represents a year, and the thicker black line represents the period when the citation burst. Between 1990 and 2020, there are top 10 references with the strongest citation burst. In the financial systemic risk research, the first reference citation burst started in 2000 and lasted for 20 years. In that paper, Rochet and Tirole (Citation1996) conducted an empirical study on the domino effect between financial institutions caused by liquidity issues in the interbank clearing network.

Table 8. Top 10 references with the strongest citation bursts.

Furthermore, in the top 10 references with the strongest citation bursts, the highest citation burst strength is 11.94. Besides, the rest of the articles in also profoundly explores the financial systemic risk area and provide scholars with emerging trends in this area. These papers explore the financial systemic risk research field from the view of systemic risk in an interbank market (Freixas et al., Citation2000), interbank payment flows (Furfine, Citation2003), and global financial markets (Acharya et al., Citation2009).

To explore the emerging trends of financial systemic risk research deeply, we should take the top 10 keywords with the strongest citation bursts into consideration to see the fast-growing topics in the research area and analyse the time zone view of keywords. As shown in , between 1990 and 2020, there are top 10 keywords with the strongest citation burst. The first keyword citation burst is ‘bank run’, which has attracted scholar’s attention from 1996 to 2010. The topic ‘regulation’ has the longest citation burst duration and the highest citation burst intensity showing it was fast-growing from 2000 to 2015 in the financial systemic risk research field. Besides, we find that the topic of the citation burst changes over time. shows the time zone view of keywords. Each circular node in the picture represents a keyword, which is located in the year where the analysed data set first appeared centrally. If the keyword appears again in later years, the keyword will increase in frequency where it first appears. As shown in , we can find the recent hot topic are ‘credit risk’, ‘capital shortfall’, ‘spill-over’, ‘spread’, ‘financial market’, ‘interconnectedness’, ‘transmission’, which show the emerging trends in the financial systemic risk research.

Figure 8. The time zone view of keywords between 1990 and 2020.

Source: Generated using CiteSpace on data.

Table 9. Top 10 keywords with the strongest citation bursts.

6. A main path analysis

The main path analysis method is a visualisation method based on time flow analysis of network connectivity to reduce the complexity of the knowledge network and extract key paths, which is a breakthrough development of citation analysis methods. To carry out the main path analysis, the first step is to perform traversal counting. In this paper, the traversal count based on the search path link (SPC) is selected. The traversal weights based on SPC are to calculate the number of node pairs passing through the link under the premise of considering the search path difference, where the starting point must be the source point, and the endpoint must be the sink point. The second step is to perform an appropriate path search strategy to obtain the analysis results. This article uses local forward main path, local backward main path, global standard main path, and global key-route main path strategies for analysis.

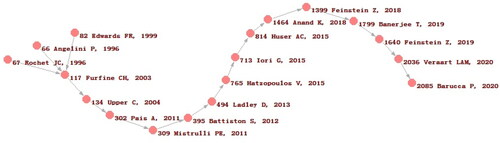

6.1. Local forward main path of financial systemic risk research

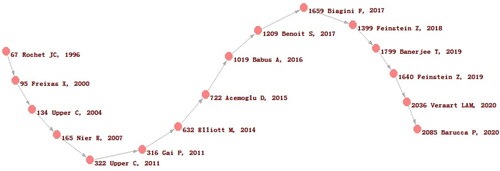

As shown in , the local forward main path is an S-shaped curve without branch points at the beginning and end. There are 16 papers on the local forward main path, half of which have a global citation score (GCS) and local citation score (LCS) with a value of more than 20. Furthermore, the high LCS value of a paper means that it is an important paper in the research field. The path in applies the local forward main path generation method. On the one hand, it reduces the complexity of the knowledge network in the financial systemic risk research and shows the knowledge backbone in the research field. On the other hand, it offers knowledge diffusion in the research field and knowledge path detection.

Figure 9. The local forward main path in the financial systemic risk research.

Source: Generated using Pajek on data.

Rochet and Tirole (Citation1996) studied financial systemic risk from the perspective of liquidity. When considering the inter-bank market, Freixas et al. (Citation2000) discussed the banking system’s ability to withstand risks, the risk chain reaction of the banking system, the coordination role of the central bank, and the justification of the too-big-to-fail policy. Furthermore, Upper and Worms (Citation2004) began to link bank safety nets with risk contagion between banks. They found that the bank’s safety network would reduce the contagiousness of bank failures but would not eliminate the risk of contagion. With the development of science and technology, people pay more and more attention to the connection between the bank's system and financial systemic risks. Nier et al. (Citation2007) concluded that banks with more capital capacity could withstand more contagious defaults. In 2008, the subprime housing credit crisis in the real estate industry caused a global financial crisis, corporate bankruptcy, people lost their jobs, bank failures, and countless fund trust businesses were closed. Many researchers started exploring the relationship between the stability, complexity, and liquidity of the financial industry, especially the financial contagion. Upper (Citation2011) summarised the findings of estimating the simulated risk of contagion due to the risk exposure of the interbank loan market. When it comes to financial networks and contagion, Elliott et al. (Citation2014) illustrated a series of failure models in a financial organization's network. Besides, Acemoglu et al. (Citation2015) argued that financial contagion exhibits a form of phase transition. To study the security issues between banks, Babus (Citation2016) modelled the decision of banks to share this risk through bilateral agreements and proved that there is an equilibrium in which contagion does not occur. In summary, after the 2008 financial crisis, it is not difficult to observe that scholars explored the deeper research areas of systemic risk, and financial contagion has become a mainstream direction of financial systemic risk research that cannot be ignored.

From the perspective of risk management, Benoit et al. (Citation2017) explored the gap between the confidential data method and the market data method to evaluate the achievements of systemic risk deeply. Feinstein et al. (Citation2018) quantified the sensitivity of the Eisenberg-Noe liquidation vector to estimate errors in the bilateral liabilities of the financial system. After applying the method to the European bank's dataset, they found that the perturbation of relative liabilities may lead to huge economic differences, which may underestimate the risk of infection. Banerjee and Feinstein (Citation2019), Feinstein (Citation2019), Veraart (Citation2020), and Barucca et al. (Citation2020) explored financial systemic risk from the aspect of interdependent liabilities, a multilayered financial network, stress testing, and credit risk, respectively.

The local forward main path analysis searches forward from sources to sinks, finding the most cited later papers with important contributions. In this paper, some important papers in the financial systemic risk field are omitted in due to this search strategy. At the same time, the local backward main path and the global main path will provide different search strategies to show the different important bone structures in the field.

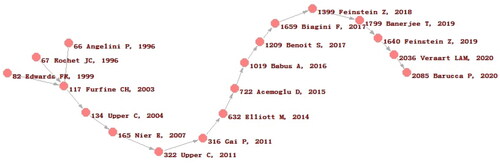

6.2. Local backward main path of financial systemic risk research

As we have known, the local backward main path analysis searches forward from sinks to sources, which means it gives higher weight to papers that have evolved from the widest sources. shows the result of the local backward main path analysis, comparing , which provides different perspectives to analyse the development trajectory of the financial systemic risk research, which can better reflect the source and evolution of knowledge or technology.

Figure 10. The local backward main path in the financial systemic risk research.

Source: Generated using Pajek on data.

As shown in , the local backward main path is also an S-shaped curve, with branch points at the beginning. There are 18 papers on the local backward main path, half of which have a global citation score (GCS) with a value of more than 20. Besides, compared with , the local backward main path overlaps part of the local forward main path. More precisely, the main paths of the two different strategies overlap into one path starting from node 1399 (Feinstein et al., Citation2018). Furthermore, the former traces the development path in the field from the present to the past, so it is not surprising that there are some different paths in the local backward path analysis. From the beginning, the local backward main path gave a diverse perspective to observe the development of financial systemic risk research. Angelini et al. (Citation1996) conducted an empirical study on the domino effect between financial institutions caused by liquidity issues. They found that about 4% of institutional participants in Italy are sufficient to trigger a systemic crisis. Furfine (Citation2003) studied the domino effect of bank failures. By quantifying the scale of fund exposure and simulating the impact of various failure scenarios, it is found that the contagion of bank failures is economically small.

Starting from node 134, the local backward main path provides a unique perspective to explore the development trajectory of financial systemic risk research. The results of the local main backward path show that to study the field of financial systemic risk further, scholars used a variety of econometric and empirical methods. Pais and Stork (Citation2011) used extreme value theory to measure the risk of contagion and found that the risk of contagion increased significantly within and between the banking and real estate sectors. Furthermore, when the negative changes in the financial soundness of institutions tend to continue promptly, the financial network may have the greatest flexibility for the intermediate level of risk diversification (Battiston et al., Citation2012). Besides, the financial systemic risk research also covers the aspect of statistically validated networks (Iori et al., Citation2015) and network reconstruction (Anand et al., Citation2018).

6.3. Global standard main path of financial systemic risk research

The global standard main path is the path with the largest total traversal count, which emphasises the overall importance of knowledge flow rather than promoting the main local path. Comparing , we can find that the global standard main path is also an S-shaped curve, which is composed of a part of the local forward main path and a part of the local backward main path. Before node 134 (Upper & Worms, Citation2004), its result coincides with the local backward main path; after 134 (Upper & Worms, Citation2004), its result coincides with the local forward main path. That shows that in the research of financial systemic risk, the path that emphasises the overall importance of knowledge flow also emphasises the importance of advancing the main local routes.

Figure 11. The global standard main path in financial systemic risk research.

Source: Generated using Pajek on data.

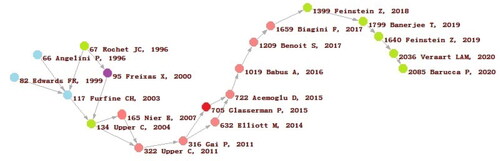

6.4. Global key-route main path of financial systemic risk research

In the analysis of the above main paths, there is a flaw. The link with the highest traversal count may not always be included in the main path. Therefore, the analysis of the global key-route main path becomes important. The search method of the global critical main path analysis ensures that the important top links in the citation network are included in the main path.

shows the result of the global key-route main path analysis, which is also an S-shaped curve. Different colours of nodes represent different meanings. Green represents nodes shared by the four main paths, the blue nodes represent the nodes shared by the local backward, the global standard, and the global key-route main path, the pink nodes represent the nodes shared by the local forward, the global standard, and the global key-route main path, the violet nodes represent the nodes shared by the local forward and the global key-route main path, and the red nodes represent the nodes unique to the global key-route main path. To further compare and contrast the four main path analyses, the global key-route main path is divided into three parts using node 134 (Upper & Worms, Citation2004) and node 1399 (Feinstein et al., Citation2018). The first part of the global key-route main path coincides with the other three main paths, showing liquidity issues (Rochet & Tirole, Citation1996) and interbank market contagion (Upper & Worms, Citation2004) were core and essential directions. In the second part of the global key-route path, there is the unique node of the global key-route main path analysis, node 705 (Glasserman & Young, Citation2015). Glasserman and Young (Citation2015) explored the clear boundaries of the network's potential impact on infection and loss amplification and found that the spillover effect is most significant when the original node is fully utilised and has high financial connectivity under different node sizes. The third part of the global key-route main path also coincides with the other three main paths. That shows that the third part of the global key-route main path not only indicates the mainstream research direction in the last three years but also is an essential link in exploring the development trajectory of financial systemic risk research. In the last three years, scholars have focussed their attention on contagion (Feinstein et al., Citation2018), interdependent liabilities (Banerjee & Feinstein, Citation2019), a multilayered financial network (Feinstein, Citation2019), stress testing (Veraart, Citation2020), and credit risk (Barucca et al., Citation2020).

Figure 12. The global key-route main path in financial systemic risk research.

Source: Generated using Pajek on data.

By analysing these four main paths, we track the development trajectory of the financial systemic risk research, identify critical scholars who have influenced the development of the research field, and investigate recent core research directions in the research field. The main conclusions are as follows: (1) The financial systemic risk research field presents an S-shaped transition trajectory through the above four main path analyses. (2) Nodes 67, 134, 1399, 1640, 1799, 2036, and 2085 are always in the development trajectory of the financial systemic risk research, which indicate those are the key sections in the financial systemic risk research. (3) ‘Contagion’ (Feinstein et al., Citation2018), ‘interdependent liabilities’ (Banerjee & Feinstein, Citation2019), ‘a multilayered financial network’ (Feinstein, Citation2019), ‘stress testing’ (Veraart, Citation2020), and ‘credit risk’ (Barucca et al., Citation2020) are core research directions in recent years. Although the research direction is more diversified, the topics related to the financial crisis, such as ‘credit risk’ and ‘contagion’ are still the mainstream research directions. Furtherly, current research of financial systemic risk field is still influenced by the 2008 global financial crisis.

6.5. The financial systemic risk research under multiple networks analysis

Besides, combined with the above analysis in Section 3, Section 4, and Section 5, we find some meaningful conclusions which might be instructive development of the whole research field. The first thing to note is that the most cited authors mentioned below are the first authors in the most cited articles. Combining the results of the main path analysis and the co-citation analysis, we find that the most cited author is not at the core of the trajectory of financial systemic risk. For example, Billio did not appear on the core track of the development of the financial systemic risk research derived from the main path analysis. However, authors who are highly cited in the field of financial systemic risk research have a greater probability of playing an important role in the development trajectory of the research field. Acemoglu is the fourth most cited author in the research of financial systemic risk. He played an essential role in the development trajectory of this field, whether it is local forward, local backward, the global standard, or the key-route main path analysis. Acemoglu et al. (Citation2015) proposed a new development direction as the convergence point of two bifurcations: contagion and bilateral exposures. Besides, in the early development path in the research field of financial systemic risk, Elliott played a vital role who occupied nodes 632 (Elliott et al., Citation2014). He is also the tenth most-cited author. Elliott et al. (Citation2014) used data on European debt cross-holdings to illustrate a series of failure models in a network of interdependent financial organisations. Besides, when analysing the results of the main path analysis with the output network and collaborative cooperation network, we find the most productive authors are not at the core of the trajectory of financial systemic risk research. For example, Ji did not appear on the core track of the development of the financial systemic risk research derived from the main path analysis. However, in the author's production network, we find that authors with high output are more likely to appear in the main path analysis path. Battiston is the fourth most productive author in the authors’ production network who also appear on the core track of the development of the financial systemic risk research derived from the main path analysis. He occupies node 395 (Battiston et al., Citation2012) as the first author and node 2085 (Barucca et al., Citation2020) as a co-author. Battiston et al. (Citation2012) found that financial networks may have the greatest flexibility for the intermediate level of risk diversification when the negative changes in the financial soundness of institutions tend to continue promptly. Gallegati and Silva also are members of the top 15 productive authors in the financial systemic risk research, and they occupy node 395 (Battiston et al., Citation2012) and node 1464 (Anand et al., Citation2018) as co-authors, respectively. Further, the above three nodes appear on the local backward main path at the same time.

In the journals’ production network, we find that journals with high output may appear more frequently in the main path analysis path in the financial systemic risk research field. Journal of Money Credit and Banking has the twelfth -highest output in the field of financial systemic risk and at the same time occupies the most nodes in the main path analysis: Node 67 (Rochet & Tirole, Citation1996), node 95 (Freixas et al., Citation2000), and node 117 (Furfine, Citation2003). By analysing the three articles published in this journal, we find that those articles’ main ideas changed from focussing on liquidity issues (Rochet & Tirole, Citation1996), the too-big-to-fail policy (Freixas et al., Citation2000) to the interbank payment flows (Furfine, Citation2003). The change of main ideas also shows the development trajectory of the financial systemic risk research. Journal of Financial Stability with second output in the research field of financial systemic risk also occupied two nodes 322 (Upper, Citation2011) and 1464 (Anand et al., Citation2018). Analysing the two articles published in this journal, the focus of articles changed from t the danger of contagion in interbank markets (Upper, Citation2011) to financial network structures (Anand et al., Citation2018). Besides, there are several high-volume journals respectively occupying an important node in the main path analysis, such as the Journal of Network Theory in Finance, Quantitative Finance.

Furthermore, the emerging trend ‘credit risk’ obtained from analysing the emerging trends of financial systemic risk research in section 4 is also recently a core research direction of the main path analysis. The emerging trend appears at node 2085 (Barucca et al., Citation2020), reflecting that the emerging trend ‘credit risk’ is also a core research direction in the financial systemic risk research field’s transition trajectory.

7. Further discussions

In this section, firstly, the previous bibliometric literature on financial systemic risk is reviewed to compare and contrast with our study. Then the status quo of financial systemic risk research is discussed. Finally, the emerging research trends are uncovered to fill in the gaps in current research, which is useful for scholars who are interested in the field of financial systemic risk.

(1) Although little literature explored the financial systemic risk research field through bibliometric analysis, there are some bibliometric studies on related risk research fields. Therefore, we compare and contrast our study with previous bibliometric studies on related risk research fields. Some scholars studied related risk fields through basic literature statistics. Mao et al. (Citation2010), Chun-Hao and Jian-Min (Citation2012) presented a basic bibliometric overview of the risk assessment research field and financial risk research field, respectively. Others explored related risk fields through more sophisticated statistical analysis software, such as CiteSpace (Wang et al., Citation2014), HistCite (Jiménez & Bjorvatn, Citation2018), and Vosviewer (Nobanee et al., Citation2021). Similar to previous studies, this paper carries out basic literature statistics in the financial systemic research field. Different from previous studies, this paper combines CiteSpace and Pajek to dig deep into the field of financial systemic risk research. We not only conduct basic literature statistics but also conduct the co-citation analysis, the cooperation analysis, main path analysis, and multiple networks analysis on the financial systemic risk field, which makes our findings more nutritious and comprehensive.

(2) As for the status quo of financial systemic risk research, ‘deposit insurance’ is the most widely studied topic, and the USA is the most significant contributor in the research field. First, we find that ‘deposit insurance’ is the most widely studied topic after 2008 based on and . Deposit insurance is a financial guarantee system, which aims to ensure the stability of financial markets (Chernykh & Cole, Citation2011). Furthermore, deposit insurance is closely related to the financial systemic risk. On the one hand, financial systemic risk is used to measure the cost of deposit insurance (Staum, Citation2012); On the other hand, deposit insurance may increase the financial system risk and lead to the financial crisis (Anginer et al., Citation2014). Besides, the deposit insurance system of the USA played an important role in disposing financial systemic risk and maintaining financial stability during the 2008 global financial crisis (Demirguç-Kunt et al., Citation2015), which explains the phenomenon that the deposit insurance system was more widely adopted after the 2008. Therefore, there is no doubt that ‘deposit insurance’ is the most widely studied topic in financial systemic risk research fields. Today, there are also many scholars explore the relationship between deposit insurance and financial systemic risk (Ashraf et al., Citation2020; Calomiris & Jaremski, Citation2019). Second, the USA is the most significant contributor in the research field. Since the 2008 global financial crisis first broke out in the USA, which may have led the USA to attach more importance to the development of the financial systemic risk research field. The crisis was brewing in the securities market of the USA from 2001 to 2007, a large number of risky subprime home loans were securitised, which attracted investors from all over the world (Hsu, 2012). However, asset securitisation leads to the accumulation of financial systemic risk, made the subprime mortgage crisis of the USA into a global financial crisis. Although the USA stabilised its financial system from collapse, it is still profoundly affected by the 2008 global financial crisis, along with a decline in employment and economic recession. Today, scholars still explore the financial systemic risk of the USA (Orhan et al., Citation2020). Therefore, undoubtedly the USA pays more attention to the research of financial systemic risk than other countries and regions.

(3) ‘Credit risk’, ‘capital shortfall’, ‘spill-over’, ‘spread’, ‘financial market’, ‘interconnectedness’, and ‘transmission’ are the emerging trends of financial systemic risk research field, which can guide scholars to further explore the field from new perspectives. Besides, all of the emerging trends show a close relationship with the financial crisis, which indicates that financial crisis plays an important role in the development of financial systemic risk research fields. Furthermore, ‘credit risk’ is also recently a core research direction in this research field’s transition trajectory, implying that ‘credit risk’ may be a mainstream trend in financial systemic risk research field.

8. Conclusions

In this paper, we have probed into the status quo, emerging trends, and transition trajectory of financial systemic risk research field through bibliometric analysis. Based on the above analysis, some meaningful conclusions are shown. First, there are 2088 most related articles on the financial systemic risk field from 1990 to 2020. The number of articles in this research field has grown rapidly since 2008, which implies that this research field is attracting more attention after the 2008 financial crisis. We also have identified the most widely studied topics in this field over the past 20 years. Second, the USA, the European Central Bank, the Journal of Banking Finance, and Ji are respectively the most productive country, institution, journal, and author in this field. More specifically, the USA made a significant contribution in this field. Third, the emerging trends of this research field have been presented, and most of those show an intimate relationship with financial crisis. Fourth, we also have recognised that this research field presents an S-shaped transition trajectory through main path analysis. Finally, we have made the following findings under the perspective of multiple networks: (1) The most cited authors and the most productive authors are not always at the core of the trajectory of financial systemic risk. (2) The emerging trend ‘credit risk’ is also recently a core research direction in this research field’s transition trajectory. Besides, we also have provided in-depth discussions about our study, which is aiming to bring more profound and meaningful inspirations for future researchers. Furthermore, our study has some meaningful implications for policy. We have recognised that financial systemic risk has become a global issue that should be paid attention to by countries, institutions, people. Taking the USA into account, we have found a positive correlation between a country’s contribution and returns in this research field. Moreover, ‘credit risk’ is a potential research direction in this research field, which should be focussed on to make up for the deficiency in the current research field of financial systemic risk. In a word, financial systemic risk is a huge challenge for countries, businesses, and individuals from a global view.

The first contribution of our paper is to fill the gap between the bibliometric analysis and financial systemic risk research, which helps researchers to have a deeper understanding of the development of this research field. The second contribution of our paper is to offer a multiple networks analysis of financial systemic risk research through different software, which is different from previous related studies. Combining the advantage of CiteSpace and Pajek, we conduct further analysis of the bibliometric results, reaching more profound conclusions about the authors and emerging trends. Our paper also contributes to explore the close relationship between the financial systemic risk research field and the global financial crises, which motivates researchers to take more efficient and innovative approaches to explore the field of financial systemic risk.

Despite the above contributions, this paper has the following limitations. Firstly, financial systemic risk covers a variety of financial risks, which is a broad concept. We suggest that further studies should narrow down the scope of research to explore more specific financial systemic risk. Second, the literature database is limited to WoS. Though WoS is a vast platform that allows us to acquire most of the key literature we need in financial systemic risk research, there are other databases, such as SpringerLink and ProQuest.

Disclosure statement

There is no economic or non-economic competitive interest between the authors of this article.

Additional information

Funding

References

- Abdymomunov, A. (2013). Regime-switching measure of systemic financial stress. Annals of Finance, 9(3), 455–470. https://doi.org/10.1007/s10436-012-0194-1

- Acemoglu, D., Ozdaglar, A., & Tahbaz-Salehi, A. (2015). Systemic risk and stability in financial networks. American Economic Review, 105(2), 564–608. https://doi.org/10.1257/aer.20130456

- Acharya, V., Engle, R., & Richardson, M. (2012). Capital shortfall: A new approach to ranking and regulating systemic risks. American Economic Review, 102(3), 59–64. https://doi.org/10.1257/aer.102.3.59

- Acharya, V., Philippon, T., Richardson, M., & Roubini, N. (2009). The financial crisis of 2007-2009: Causes and remedies. Financial Markets, Institutions & Instruments, 18(2), 89–137. https://doi.org/10.1111/j.1468-0416.2009.00147_2.x

- Acharya, V. V., Pedersen, L. H., Philippon, T., & Richardson, M. (2017). Measuring systemic risk. Review of Financial Studies, 30(1), 2–47. https://doi.org/10.1093/rfs/hhw088

- Adrian, T., & Brunnermeier, M. K. (2014). Covar. National Bureau of Economic Research, 106(7), 1705–1741.

- Alshater, M. M., Atayah, O. F., & Khan, A. (2021). What do we know about business and economics research during COVID-19: A bibliometric review. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.1927786

- Anand, K., van Lelyveld, I., Banai, Á., Friedrich, S., Garratt, R., Hałaj, G., Fique, J., Hansen, I., Jaramillo, S. M., Lee, H., Molina-Borboa, J. L., Nobili, S., Rajan, S., Salakhova, D., Silva, T. C., Silvestri, L., & de Souza, S. R. S. (2018). The missing links: A global study on uncovering financial network structures from partial data. Journal of Financial Stability, 35, 107–119. https://doi.org/10.1016/j.jfs.2017.05.012

- Angelini, P., Maresca, G., & Russo, D. (1996). Systemic risk in the netting system. Journal of Banking & Finance, 20(5), 853–868. https://doi.org/10.1016/0378-4266(95)00029-1

- Anginer, D., Demirguc-Kunt, A., & Zhu, M. (2014). How does deposit insurance affect bank risk? Evidence from the recent crisis. Journal of Banking & Finance, 48, 312–321. https://doi.org/10.1016/j.jbankfin.2013.09.013

- Ashraf, B. N., Zheng, C., Jiang, C., & Qian, N. (2020). Capital regulation, deposit insurance and bank risk: International evidence from normal and crisis periods. Research in International Business and Finance, 52, 101188. https://doi.org/10.1016/j.ribaf.2020.101188

- Azam, A., Ahmed, A., Wang, H., Wang, Y. N., & Zhang, Z. T. (2021). Knowledge structure and research progress in wind power generation (WPG) from 2005 to 2020 using CiteSpace based scientometric analysis. Journal of Cleaner Production, 295, 126496. https://doi.org/10.1016/j.jclepro.2021.126496

- Babus, A. (2016). The formation of financial networks. The RAND Journal of Economics, 47(2), 239–272. https://doi.org/10.1111/1756-2171.12126

- Banerjee, T., & Feinstein, Z. (2019). Impact of contingent payments on systemic risk in financial networks. Mathematics and Financial Economics, 13(4), 617–636. https://doi.org/10.1007/s11579-019-00239-9

- Barucca, P., Bardoscia, M., Caccioli, F., Errico, M., Visentin, G., Battiston, S., & Caldarelli, G. (2020). Network valuation in financial systems. Mathematical Finance, 30(4), 1181–1204. https://doi.org/10.1111/mafi.12272

- Battiston, S., Gatti, D. D., Gallegati, M., Greenwald, B., & Stiglitz, J. E. (2012). Liaisons dangereuses: Increasing connectivity, risk sharing, and systemic risk. Journal of Economic Dynamics and Control, 36(8), 1121–1141. https://doi.org/10.1016/j.jedc.2012.04.001

- Benoit, S., Colliard, J. E., Hurlin, C., & Perignon, C. (2017). Where the risks lie: A survey on systemic risk. Review of Finance, 21(1), 109–152. https://doi.org/10.1093/rof/rfw026

- Berger, A. N., Strahan, P. E., & Demsetz, R. S. (1999). The consolidation of the financial services industry: Causes, consequences, and implications for the future. Journal of Banking & Finance, 23(2–4), 135–194. https://doi.org/10.1016/S0378-4266(98)00125-3

- Billio, M., Getmansky, M., Lo, A. W., & Pelizzon, L. (2012). Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics, 104(3), 535–559. https://doi.org/10.1016/j.jfineco.2011.12.010

- Bitar, J. (2021). Foreign currency intermediation: Systemic risk and macroprudential regulation. Latin American Journal of Central Banking, 2(2), 100028. https://doi.org/10.1016/j.latcb.2021.100028

- Brunnermeier, M. K., & Pedersen, L. H. (2009). Market liquidity and funding liquidity. Review of Financial Studies, 22(6), 2201–2238. https://doi.org/10.1093/rfs/hhn098

- Calomiris, C. W., & Jaremski, M. (2019). Stealing deposits: Deposit insurance, risk taking, and the removal of market discipline in early 20th century banks. The Journal of Finance, 74(2), 711–754. https://doi.org/10.1111/jofi.12753

- Chen, C. M. (2006). CiteSpace II: Detecting and visualizing emerging trends and transient patterns in scientific literature. Journal of the American Society for Information Science and Technology, 57(3), 359–377. https://doi.org/10.1002/asi.20317

- Chen, C., Hu, Z., Liu, S., & Tseng, H. (2012). Emerging trends in regenerative medicine: A scientometric analysis in CiteSpace. Expert Opinion on Biological Therapy, 12(5), 593–608.

- Chernykh, L., & Cole, R. A. (2011). Does deposit insurance improve financial intermediation? Evidence from the Russian experiment. Journal of Banking & Finance, 35(2), 388–402. https://doi.org/10.1016/j.jbankfin.2010.08.014

- Chun-Hao, C., & Jian-Min, Y. (2012). A bibliometric study of financial risk literature: A historic approach. Applied Economics, 44(22), 2827–2839. https://doi.org/10.1080/00036846.2011.566208

- Davydov, D., Vahamaa, S., & Yasar, S. (2021). Bank liquidity creation and systemic risk. Journal of Banking & Finance, 123, 106031. https://doi.org/10.1016/j.jbankfin.2020.106031

- Demirguç-Kunt, A., Kane, E., & Laeven, L. (2015). Deposit insurance around the world: A comprehensive analysis and database. Journal of Financial Stability, 20, 155–183. https://doi.org/10.1016/j.jfs.2015.08.005

- Diebold, F. X., & Yilmaz, K. (2014). On the network topology of variance decompositions: Measuring the connectedness of financial firms. Journal of Econometrics, 182(1), 119–134. https://doi.org/10.1016/j.jeconom.2014.04.012

- Eisenberg, L., & Noe, T. H. (2001). Systemic risk in financial systems. Management Science, 47(2), 236–249. https://doi.org/10.1287/mnsc.47.2.236.9835

- Elliott, M., Georg, C. P., & Hazell, J. (2021). Systemic risk shifting in financial networks. Journal of Economic Theory, 191, 105157. https://doi.org/10.1016/j.jet.2020.105157

- Elliott, M., Golub, B., & Jackson, M. O. (2014). Financial networks and contagion. American Economic Review, 104(10), 3115–3153. https://doi.org/10.1257/aer.104.10.3115

- Feinstein, Z. (2019). Obligations with physical delivery in a multilayered financial network. SIAM Journal on Financial Mathematics, 10(4), 877–906. https://doi.org/10.1137/18M1194729

- Feinstein, Z., Pang, W., Rudloff, B., Schaanning, E., Sturm, S., & Wildman, M. (2018). Sensitivity of the Eisenberg–Noe clearing vector to individual interbank liabilities. SIAM Journal on Financial Mathematics, 9(4), 1286–1325. https://doi.org/10.1137/18M1171060

- Feinstein, Z., Rudloff, B., & Weber, S. (2017). Measures of systemic risk. SIAM Journal on Financial Mathematics, 8(1), 672–708. https://doi.org/10.1137/16M1066087

- Feng, F., Zhang, L., Du, Y., & Wang, W. (2015). Visualization and quantitative study in bibliographic databases: A case in the field of university–industry cooperation. Journal of Informetrics, 9(1), 118–134. https://doi.org/10.1016/j.joi.2014.11.009

- Freixas, X., Parigi, B. M., & Rochet, J. C. (2000). Systemic risk, interbank relations, and liquidity provision by the central bank. Journal of Money, Credit and Banking, 32(3), 611–638. https://doi.org/10.2307/2601198

- Furfine, C. (2003). Interbank exposures: Quantifying the risk of contagion. Journal of Money, Credit, and Banking, 35(1), 111–128. https://doi.org/10.1353/mcb.2003.0004

- Girardi, G., & Ergun, A. T. (2013). Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance, 37(8), 3169–3180. https://doi.org/10.1016/j.jbankfin.2013.02.027

- Glasserman, P., & Young, B. P. (2015). How likely is contagion in financial networks? Journal of Banking & Finance, 50, 383–399. https://doi.org/10.1016/j.jbankfin.2014.02.006

- Gong, X. L., Liu, X. H., Xiong, X., & Zhang, W. (2019). Financial systemic risk measurement based on causal network connectedness analysis. International Review of Economics & Finance, 64, 290–307. https://doi.org/10.1016/j.iref.2019.07.004

- Halili, A., Fenech, J. P., & Contessi, S. (2021). Credit derivatives and bank systemic risk: Risk enhancing or reducing? Finance Research Letters, 101930. https://doi.org/10.1016/j.frl.2021.101930

- He, F., & Chen, X. (2016). Credit networks and systemic risk of Chinese local financing platforms: Too central or too big to fail? Physica A: Statistical Mechanics and Its Applications, 461, 158–170. https://doi.org/10.1016/j.physa.2016.05.032

- Hu, W., Li, C. H., Ye, C., Wang, J., Wei, W. W., & Deng, Y. (2019). Research progress on ecological models in the field of water eutrophication: CiteSpace analysis based on data from the ISI web of science database. Ecological Modelling, 410, 108779. https://doi.org/10.1016/j.ecolmodel.2019.108779

- Hummon, N. P., & Dereian, P. (1989). Connectivity in a citation network: The development of DNA theory. Social Networks, 11(1), 39–63. https://doi.org/10.1016/0378-8733(89)90017-8

- Iori, G., Mantegna, R. N., Marotta, L., Micciche, S., Porter, J., & Tumminello, M. (2015). Networked relationships in the e-MID interbank market: A trading model with memory. Journal of Economic Dynamics and Control, 50, 98–116. https://doi.org/10.1016/j.jedc.2014.08.016

- Jiang, S., & Fan, H. (2021). Systemic risk in the interbank market with overlapping portfolios and cross-ownership of the subordinated debts. Physica A: Statistical Mechanics and Its Applications, 562, 125355. https://doi.org/10.1016/j.physa.2020.125355

- Jiménez, A., & Bjorvatn, T. (2018). The building blocks of political risk research: A bibliometric co-citation analysis. International Journal of Emerging Markets, 13(4), 631–652. https://doi.org/10.1108/IJoEM-12-2016-0334

- Jung, H., & Lee, B. G. (2020). Research trends in text mining: Semantic network and main path analysis of selected journals. Expert Systems with Applications, 162, 113851. https://doi.org/10.1016/j.eswa.2020.113851

- Kapinos, P., Kishor, N. K., & Ma, J. (2020). Dynamic comovement among banks, systemic risk, and the macroeconomy. Journal of Banking & Finance, 105894. https://doi.org/10.1016/j.jbankfin.2020.105894

- Lehar, A. (2005). Measuring systemic risk: A risk management approach. Journal of Banking & Finance, 29(10), 2577–2603. https://doi.org/10.1016/j.jbankfin.2004.09.007

- Leong, C. (2021). Narratives and water: A bibliometric review. Global Environmental Change, 68, 102267. https://doi.org/10.1016/j.gloenvcha.2021.102267

- Li, B., & Xu, Z. S. (2021). A comprehensive bibliometric analysis of financial innovation. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.1893203

- Li, F., & Perez-Saiz, H. (2018). Measuring systemic risk across financial market infrastructures. Journal of Financial Stability, 34, 1–11. https://doi.org/10.1016/j.jfs.2017.08.003

- Li, X., Ma, E., & Qu, H. (2017). Knowledge mapping of hospitality research − A visual analysis using CiteSpace. International Journal of Hospitality Management, 60, 77–93. https://doi.org/10.1016/j.ijhm.2016.10.006

- Mao, N., Wang, M. H., & Ho, Y. S. (2010). A bibliometric study of the trend in articles related to risk assessment published in Science Citation Index. Human and Ecological Risk Assessment, 16(4), 801–824.

- Morelli, D., & Vioto, D. (2020). Assessing the contribution of China’s financial sectors to systemic risk. Journal of Financial Stability, 50, 100777. https://doi.org/10.1016/j.jfs.2020.100777

- Nier, E., Yang, J., Yorulmazer, T., & Alentorn, A. (2007). Network models and financial stability. Journal of Economic Dynamics and Control, 31(6), 2033–2060. https://doi.org/10.1016/j.jedc.2007.01.014

- Nobanee, H., Al Hamadi, F. Y., Abdulaziz, F. A., Abukarsh, L. S., Alqahtani, A. F., Alsubaey, S. K., Alqahtani, S. M., & Almansoori, H. A. (2021). A bibliometric analysis of sustainability and risk management. Sustainability, 13(6), 3277. https://doi.org/10.3390/su13063277

- Nyman, R., Kapadia, S., & Tuckett, D. (2021). News and narratives in financial systems: Exploiting big data for systemic risk assessment. Journal of Economic Dynamics and Control, 127, 104119. https://doi.org/10.1016/j.jedc.2021.104119

- Orhan, A., Ferhan Benli, V., & Castanho, R. A. (2020). Assessing the systemic risk between American and European financial systems. Prague Economic Papers, 29(6), 649–671. https://doi.org/10.18267/j.pep.756

- Ouyang, W., Wang, Y., Lin, C., He, M., Hao, F., Liu, H., & Zhu, W. (2018). Heavy metal loss from agricultural watershed to aquatic system: A scientometrics review. Science of the Total Environment, 637, 208–220.

- Pais, A., & Stork, P. A. (2011). Contagion risk in the Australian banking and property sectors. Journal of Banking & Finance, 35(3), 681–697. https://doi.org/10.1016/j.jbankfin.2010.05.012

- Patro, D. K., Qi, M., & Sun, X. (2013). A simple indicator of systemic risk. Journal of Financial Stability, 9(1), 105–116. https://doi.org/10.1016/j.jfs.2012.03.002

- Rochet, J. C., & Tirole, J. (1996). Interbank lending and systemic risk. Journal of Money, Credit and Banking, 28(4), 733–762. https://doi.org/10.2307/2077918

- Staum, J. (2012). Systemic risk components and deposit insurance premia. Quantitative Finance, 12(4), 651–662. https://doi.org/10.1080/14697688.2012.664942

- Stolbov, M., & Shchepeleva, M. (2020). Systemic risk, economic policy uncertainty and firm bankruptcies: Evidence from multivariate causal inference. Research in International Business and Finance, 52, 101172. https://doi.org/10.1016/j.ribaf.2019.101172

- Upper, C. (2011). Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability, 7(3), 111–125. https://doi.org/10.1016/j.jfs.2010.12.001

- Upper, C., & Worms, A. (2004). Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? European Economic Review, 48(4), 827–849. https://doi.org/10.1016/j.euroecorev.2003.12.009

- Veraart, L. A. M. (2020). Distress and default contagion in financial networks. Mathematical Finance, 30(3), 705–737. https://doi.org/10.1111/mafi.12247

- Wang, Q., Yang, Z., Yang, Y., Long, C., & Li, H. (2014). A bibliometric analysis of research on the risk of engineering nanomaterials during 1999–2012. Science of the Total Environment, 473, 483–489. https://doi.org/10.1016/j.scitotenv.2013.12.066

- Wang, X. X., Xu, Z. S., Qin, Y., & Skare, M. (2021). Foreign direct investment and economic growth: A dynamic study of measurement approaches and results. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.1952090

- Wu, F., Zhang, D., & Ji, Q. (2021). Systemic risk and financial contagion across top global energy companies. Energy Economics, 97, 105221. https://doi.org/10.1016/j.eneco.2021.105221

- Xu, Q., Jin, B., & Jiang, C. (2021). Measuring systemic risk of the Chinese banking industry: A wavelet-based quantile regression approach. The North American Journal of Economics and Finance, 55, 101354. https://doi.org/10.1016/j.najef.2020.101354

- Yin, L., Feng, J., & Han, L. (2021). Systemic risk in international stock markets: Role of the oil market. International Review of Economics & Finance, 71, 592–619. https://doi.org/10.1016/j.iref.2020.09.024

- Ying, J., Zhang, X., Zhang, Y., & Bilan, S. (2021). Green infrastructure: Systematic literature review. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.1893202

- Yu, D., & Pan, T. (2021). Tracing the main path of interdisciplinary research considering citation preference: A case from blockchain domain. Journal of Informetrics, 15(2), 101136. https://doi.org/10.1016/j.joi.2021.101136

- Zhang, A., Pan, M., Liu, B., & Weng, Y. C. (2020a). Systemic risk: The coordination of macroprudential and monetary policies in China. Economic Modelling, 93, 415–429. https://doi.org/10.1016/j.econmod.2020.08.017

- Zhang, D., Xu, J., Zhang, Y., Wang, J., He, S., & Zhou, X. (2020b). Study on sustainable urbanization literature based on Web of Science, scopus, and China national knowledge infrastructure: A scientometric analysis in CiteSpace. Journal of Cleaner Production, 264, 121537

- Zhou, W., & Xu, Z. S. (2020). An overview of the fuzzy data envelopment analysis research and its successful applications. International Journal of Fuzzy Systems, 22(4), 1037–1055. https://doi.org/10.1007/s40815-020-00853-6

- Zhou, W., Xu, Z. S., & Skačkauskas, P. (2019). Mapping knowledge domain of “TRANSPORT”: A bibliometric study of its status quo and emerging trends. Transport, 34(6), 741–753. https://doi.org/10.3846/transport.2019.11774