Abstract

This study aims to examine the direct and indirect effects of corporate social responsibility (CSR) on organizational performance (OP) through the mediating role of employee engagement (EE) and green innovation (GI) in the Malaysian banking sector. Moreover, this study was conducted to empirically investigate a sample of 550 employees affiliated with eight banks in Kuala Lumpur, Malaysia. The research employed the Partial Least Squares Path Modelling (PLS-SEM) technique to obtain the intended results. The findings of this research demonstrate that CSR has a positive and significant impact on OP, EE, and GI. Furthermore, EE is also significantly correlated with OP, while GI is not significantly correlated with OP. On the other hand, EE mediates the relationship between CSR and OP, while the mediating role of GI was not found. This study highlights the importance of CSR programs in promoting EE and encouraging GI. Ultimately, these initiatives affect organizational performance within the banking sector. This study makes a theoretical contribution by investigating the mediating impacts of EE and GI on the relationship between CSR and OP within the banking sector. Moreover, these findings benefit future researchers interested in exploring the banking sector’s performance.

1. Introduction

Corporate social responsibility (CSR) initiatives enable banks to maintain a positive public image by demonstrating their dedication to addressing societal and environmental issues. Similarly, adopting CSR practices has the potential to alleviate specific risks, such as reputational risks stemming from unethical conduct or environmental obligations. The implementation of responsible banking practices has the potential to bolster the durability of financial institutions. In addition, CSR initiatives play a significant role in fostering a favorable organizational environment, bolstering employee morale and higher employee engagement levels. Employees actively involved and committed to their work tend to exhibit higher productivity levels, contributing to enhanced organizational performance on a broader scale. Furthermore, as Imran et al. (Citation2022) stated, CSR catalysis banks to engage in innovation and embrace sustainable practices. These technological advancements have the potential to result in financial savings and enhance operational effectiveness, thereby positively impacting the bank’s financial performance. The correlation between CSR and organizational performance (OP) has been extensively explored by scholars on a global scale (Shafique & Ahmad, Citation2022). Nevertheless, the results lack consistency and clarity (Platonova et al., Citation2018). Several studies have indicated a positive correlation between CSR and OP (Singh & Misra, Citation2021; Hou, Citation2019), whereas alternative research findings have suggested a negative link (Petrenko et al., Citation2016).

Additionally, several studies indicate a lack of correlation between these variables (Sameer, Citation2021). Despite the considerable scholarly focus on CSR and its influence on OP, as evidenced by the work of Javed et al. (Citation2020), studies examining the direct relationship between these two constructs have produced conflicting findings, as indicated by the research conducted by Platonova et al. (Citation2018) and Martinez-Conesa et al. (Citation2017). Some studies have provided evidence regarding the relationship between CSR and OP. Singh and Misra (Citation2021) have suggested a relationship between CSR and OP, whereas Abbas (Citation2020) has indicated a negative association. Additionally, Sameer (Citation2021) has found no significant correlation between the two variables. Nevertheless, it is important to acknowledge that various research studies have certain limitations, specifically excluding employee engagement and green innovation as potential mediating factors that could influence the relationship between CSR and OP.

It is important to remember that CSR has been investigated in various fields, such as business ethics, marketing, and management research (He & Harris, Citation2020). In addition, the emphasis on CSR in most of the extant studies written has primarily addressed concerns such as performance (Bai & Chang, Citation2015), strategy (Rao & Tilt, Citation2016), and consumer characteristics (Park et al., Citation2017), with little attention given to the relevance of human resource management in this context. Although this lack of work extended toward CSR and human resource management, evidence shows that employee engagement with CSR is a critical aspect when it comes to achieving the desired performance (Ferreira & de Oliveira, Citation2014). Moreover, CSR initiatives are being pursued while research indicates positive relationships between CSR and many individual outcomes, including, but not limited to, employee engagement (Memon et al., Citation2020). This research, therefore, is significant in this regard since employee engagement has been highlighted as the key area of issue for many businesses. Employees who were physically, mentally, and emotionally engaged in their job tasks were considered actively engaged in the organization by the management (Sharma & Kumra, Citation2020).

According to a Gallup poll conducted in the year 2017, only 15% of the employees working around the globe were organically engaged. This, therefore, has frequently led to significant organizational and economic losses due to the loss of productivity due to disengaged employees. The United States performs better than the rest of the world regarding EE, with 34% of the employees believed to be actively engaged. However, this leaves 66% of the residue employees who are not involved. According to the Gallup Organization (Citation2017), disconnected personnel cost the United States economy between $483 billion and $605 billion per year—a time when that has been lost to a lack of productivity. Increased EE, according to the research, can have a positive impact on OP due to more employee engagement is related to significant consequences such as increased efficiency, more customer satisfaction, low level of employee turnover and absence, and fewer safety occurrences and superiority issues (Jiang & Luo, Citation2020).

Researchers have examined financial performance with the help of CSR initiatives for several decades (Bruna & Lahouel, Citation2022). Furthermore, a few studies have also shown that CSR considerably improves OP (Petrenko et al., Citation2016). Regardless, CSR has not been shown to impact OP significantly (Kraus et al., Citation2020). Although different research has established a firm’s performance in corporate social responsibility, scholars have recently concentrated on this association due to the ambiguous findings that have surfaced. According to the extant literature, CSR and OP also have no significant correlation (Gupta & Sharma, Citation2016).

Over the past several years, there has been an increase in the worldwide banking sector’s recognition of the importance of CSR (Belasri et al., Citation2020) and the responsibility that the banking sector plays in society and the environment. Academics have been more interested in banks’ disclosure of CSR information (Xie et al., Citation2019), bringing up many important considerations. It has been affirmed that to evaluate socially conscious efforts, ensure the confidence of stakeholders, and protect CSR and sustainability principles, global research with CSR in the banking industry is now of paramount significance. Numerous research studies in the past have analyzed banks’ CSR efforts. In the same context, according to Aggarwal and Saxena (Citation2023), the banking industry is crucial to the economy. Furthermore, Khan et al. (Citation2020) have argued that despite the benefits to banks from implementing fundamental CSR standards in HR policy and public participation, banks’ contributions to CSR disclosure through regions are not a devastating and uniform concept.

According to Úbeda-García et al. (Citation2021), existing literature highlights the significance of employee engagement and green innovation as crucial factors that mediate the association between CSR and OP. According to Imran et al. (Citation2021), there is a strong association between green innovation and organizational performance. Additionally, Kim and Kim (Citation2020) emphasize the importance of employees in evaluating the relationship between CSR and performance. The implementation of CSR within the banking sector, specifically emphasizing green innovation, holds the potential to exert a positive influence on performance outcomes. Green innovation refers to implementing environmentally conscious practices within the banking sector to minimize costs, waste generation, and pollution. Engaging in CSR initiatives enables banks to introduce environmentally friendly innovations, thereby establishing their environmental credibility and attaining a competitive edge (Achi et al., Citation2022). These are consistent with the theoretical framework of the dynamic capabilities approach, which underscores the importance of the external environment in shaping organizational capabilities and influencing bank performance (Fukuyama & Tan, Citation2022). Prior research has demonstrated the significance of green innovation in ensuring long-term effectiveness, operational efficiency, and sustainability (El-Kassar & Singh, Citation2019). Nevertheless, there is currently a lack of comprehensive attention from scholars toward assessing organizational performance with green innovation.

This study’s primary objective is to evaluate how CSR affects OP in Malaysia’s banking sector. Another objective of this research is to examine how organizational performance is related to CSR, EE, and GI. The primary reason for conducting this survey study is the shortage of prior studies examining the significance of CSR in establishing OP in the Malaysian banking sector. Furthermore, there is a knowledge gap concerning the impacts of EE and GI on CSR and its interaction with OP, even though their mediation functions have been identified. This research aims to fill this gap and add to the existing body of knowledge by investigating the role of EE and GI as mediators in the link between CSR and OP. Uniquely including EE and GI as mediating factors, the proposed model sheds light on the relationship between CSR, EE, and GI and how they affect organizational performance.

2. Literature review and hypothesis development

According to the literature on the banking sector, there has been a clear growth in banks’ focus on CSR and their role in economic development. Fatma and Rahman (Citation2016) state that banks concentrate on CSR for several reasons directly tied to their day-to-day operations. The motivations behind their CSR activities become more transparent when these factors are understood. Concerns and misunderstandings about CSR exist inside the banking sector, such as allegations of hypocrisy and using CSR as a cover for unethical practices (Norberg, Citation2018). In order to dispute misconceptions and shine a light on genuine CSR activities in the banking business, it is important to address these issues and provide supporting references or real-world instances. The relevance and ramifications of CSR in the banking sector can only be fully grasped if all of these factors are considered. Since banks’ activities affect society and the environment, CSR has received more attention recently (Sarfraz et al., Citation2018). They understand the need to contribute to economic growth and sustainable practices; thus, they’ve merged their corporate and social aims. According to Bugandwa et al. (Citation2021), CSR is important to banks for several reasons, including improving their image, luring new clients who share their values, meeting regulatory benchmarks, and satisfying stakeholders. However, other researchers, such as Ahmad et al. (Citation2021), have claimed that certain financial institutions participate in CSR for PR and brand building rather than out of any real concern for the communities in which they operate or the environment. In order to distinguish between actual and superficial projects, addressing these issues and emphasizing genuine CSR efforts is important.

Due to the growing public anxiety regarding the environment, industries have grown sensitive towards implementing eco-friendly ways (e.g., CSR, GI), thus improving the OP. While the institution’s primary purpose is not to maximize profits, it achieves long-term viability through continual development and outstanding achievement. According to Barauskaite and Streimikiene (Citation2021), CSR has been around for more than semi-centennial, although no commonly agreed definition exists. In the authors’ opinion, the core concept of this system is that communally liable businesses take into close consideration of their actions, reunite their preferences through the benefit of stockholders, workforces, and the environment, in addition to their society, then further interested parties, and accept responsibility for their effect upon the environment. They also believe that socially responsible organizations should be transparent about their operations.

Concerns about CSR have now attracted the attention of banks. They function as financial intermediaries, keep track of borrowers, handle financial risk, set up payment systems, price and evaluate financial assets, and greatly impact economic developments, thus making them crucial players in economic development (Forgione et al., Citation2020). In addition, they primarily use social capital to take on this challenge; thus, they must provide the community with more input than the other sectors. Therefore, to describe how they contribute back to society, practically all banks have included a part of CSR in their financial statements. However, the banking sector prioritizes CSR mostly to enhance its image (Shen et al., Citation2016). Such a sector is plagued by pre-existing misconceptions about the banks’ hypocrisy (Hur & Kim, Citation2020), avarice Caruana et al. (Citation2018), and immoral deals tactics of their personnel Tosun (Citation2020). In light of the significance of CSR in the banking sector, we have developed the following hypotheses concerning the banking sector in Malaysia.

2.1. CSR and organizational performance within the banking sector

Previous research on the relationship between CSR and OP shows a weak correlation between financial and non-financial outcomes (Cheffi et al., Citation2021; Safi et al., Citation2023). Several review studies have portrayed this to be the actual situation. Moreover, many studies have demonstrated a positive association between CSR along with financial efficiency, including those of, Siueia et al. (Citation2019), the banking sector of Sub-Sahara Africa, Matuszak and Różańska (Citation2017), the Polish banking sector, Galdeano et al. (Citation2019), and the banking sector of Bahrain. Moreover, the authors have examined several articles studying the correlation between CSR and bank performance. However, regarding the banking sector’s performance, these positive associations have yet to be confirmed (Gangi et al., Citation2018). Specifically, in Malaysia’s banking industry, relationship with CSR and performance is even more unclear than in the other sectors (Platonova et al., Citation2018). Only a few studies have suggested a positive association between CSR and organizational performance, CSR, green innovation (Kraus et al., Citation2020), and CSR with EE (Farrukh et al., Citation2020).

Some academics believe in a positive correlation, particularly with OP (Mehralian et al., Citation2016). However, several scholars argue that this result should be taken with a grain of salt. There are two different views on this issue: one argues that the connection between CSR and OP is weak or nonexistent (Kim & Thapa, Citation2018); the other argues that there is no consensus on how to define CSR and that empirical studies contain measurement errors. Moreover, there has also been a decrease in CSR's positive impact on financial performance in recent years, according to Cho et al. (Citation2019). It must be noted that This might be an actual examination or a result of improved research strategies.

As a result, CSR is predicted to positively impact banking organizations’ performance (Belasri et al., Citation2020). Our study has found that defining OP is a shockingly wide-open subject, with a few findings employing consistent measurements (Cheffi et al., Citation2021). Consequently, researchers use a multi-item concept to assess OP based on research in management control (Kaplan & Norton, Citation1996). Instead of focusing on the non-financial measures, we have resorted to using the multi-item method to evaluate the CSR's impact on the overall organizational performance. Our model’s construct covers all the aspects of organizational performance, from non-financial to environmental. Thus, the study aims to show how CSR influences the banking industry’s efficiency in Malaysia. The CSR and non-financial variables have been studied recently in the banking sector (Tulcanaza-Prieto et al., Citation2020). This study may add to the present CSR literature by giving more in-depth perceptions of the effects of CSR on the performance of Malaysian banking organizations. As a result, the following hypothesis has been suggested:

H1: CSR is positively and significantly related to organizational performance in the banking sector.

2.2. CSR and employee engagement

In-depth research into the relationship between CSR and employee engagement is still developing, but a few studies have shown a positive correlation with these constructs. Following the same context, Glavas (Citation2016) concluded that the significance of CSR to employees increased the influence of better employee opinions of CSR on EE. There was also a positive correlation between CSR and EE found by Tsourvakas and Yfantidou (Citation2018). In another instance, Glavas (Citation2016) argued that the positive association between CSR and engagement could be explained by employees finding more purpose and value unity in their work environments. Additionally, organizations may implement their beliefs by implementing CSR rather than just stating them in a mere statement. According to certain studies, the organization’s values are communicated to employees, thus showing a correlation between CSR and the expected value congruence among potential employees (Im et al., Citation2016). While there has been little research into the link between CSR and EE from the perspective of the Malaysian banking sector, a few empirical studies have been performed in this field in the higher education sector Hossen et al. (Citation2020), SMEs Yeo and Carter (Citation2018), and the telecommunication sector Ramaditya (Citation2019). Furthermore, Other research showed a significant association among CSR with EE (Farrukh et al., Citation2020).

Organizations can also use CSR to navigate outside what is written down in their corporate values and implement these in their business practices. This helps the employees internalize the organization’s fundamental principles, as shown by earlier research, which revealed a statistically significant and positive relationship between CSR and potential employees’ recognition of the organization’s values (Asrar-Ul-Haq et al., Citation2017). Furthermore, CSR initiatives can be utilized as a guideline to assist employees in finding a deeper purpose in their jobs. For example, Flammer and Luo (Citation2017) suggested that organizations could utilize the concept of CSR as a strategy to incentivize employees to work for a level deemed acceptable. Similarly, Lohana et al. (Citation2023) also asserted that when employees believe that they are making a positive contribution to the benefit of the consumer, they feel better, enhancing their self-perception and boosting their understanding of the organization’s distinctiveness.

Despite the limited research that has been performed on the link between CSR with EE, particularly in Malaysia, other studies that share a similar premise could shed light on the relationship that has been mentioned above. Intrinsic motivation and job satisfaction were highly correlated in a study based on EE (Nimon et al., Citation2016). Moreover, CSR and job satisfaction have been shown to have a positive relationship in prior CSR-related research (Jie & Hasan, Citation2018). In addition, the existing CSR research and literature reveal a link between CSR and EE. However, despite conducting studies in the Malaysian banking sector, researchers could not unearth any studies investigating EE mediators of the relationship between CSR and OP. As a result, based on the arguments stated beyond, we have proposed the following research hypothesis.

H2: CSR is positively and significantly related to employee engagement in the banking sector.

2.3. CSR and green innovation

CSR policies and initiatives can affect organizational innovation (Santos‐Jaén et al., Citation2021) by influencing organizations’ core strategies and business models (Szutowski & Ratajczak, Citation2016). The extant literature has statistically indicated a constructive correlation between CSR and innovation (Wu et al., Citation2018). A virtuous loop is therefore generated between CSR and innovation in the banking sector. When CSR is more frequent, banks tend to become more innovative in their approach (Birindelli et al., Citation2015). This gives significant competitive benefits to the banking sector (Zameer et al., Citation2015), allowing them to generate higher revenues by increasing their profitability (Gangi et al., Citation2019). Thus, CSR is recognized as a key driving force that enables businesses to be innovative and efficient (Pathan et al., Citation2021). Zhou et al. (Citation2021) state that organizations prioritizing their CSR initiatives and policies generate more innovative products and processes.

Organizations that engage in CSR must innovate because their conventional ways of operating are no longer effective. Only through innovation will they eventually be able to carry out these activities (Santos‐Jaén et al., Citation2021). Furthermore, stakeholders expect higher social commitment, encouraging corporations to innovate communally responsibly (Ali et al., Citation2022). Chang and Lee (Citation2020) have also described how CSR has reshaped organizational innovation to meet the customers’ changing needs, particularly those more concerned with social ethics. Thus, business innovation is increasingly directed toward socio-environmental advantages (Grayson & Hodges, Citation2017). More importantly, CSR is adopted to meet consumer needs in those organizations that match clients’ preferences with innovation, eventually producing intangible capabilities that allow them to be more technologically adaptive (Raza et al., Citation2020). Furthermore, studies have similarly highlighted the significance of innovation in CSR initiatives and OP (Zhu et al., Citation2019). However, there is currently a paucity of studies on exactly how CSR is implemented intended for environmental preservation, particularly in the employment of GI in developing countries (Shahzad et al., Citation2020). Therefore, researchers can investigate the significance of CSR in association with green innovation as a mediator and OP in the Malaysian banking sector. We postulate the H3 considering the data presented above:

H3: CSR is positively and significantly related to green innovation in the banking sector.

2.4. Employee engagement and organizational performance

The main objective of an EE in the organization is to improve the organization’s overall performance (Ogbonnaya & Valizade, Citation2018). In recent times, the issue of EE has gained popularity in human resource management research, with evidence demonstrating that it is vital for modern cultural organizations to survive in the long term. Some research in this regard has indicated that employee engagement is associated with employee outcomes, productivity, and OP (Bailey et al., Citation2017), with a particular emphasis also on organizational effectiveness (Ali et al., Citation2019) and OP (Tensay & Singh, Citation2020). The extent to which an organization achieves its aim is explained by its performance that is addressed. The performance of a corporation is described at the same time as the ability to predict the attainment of its goals when the organization’s objectives and strategies, organizational structure, processes, and human resources are all in line (Ginter et al., Citation2018). As a result, the findings reveal a significant relationship between EE and OP. Therefore, in conclusion, we have formulated the H4:

H4: EE is positively and significantly related to organizational performance in the banking sector.

2.5. Green innovation and organizational performance

Green innovation is both physical as well as virtual innovation that improves products and processes over time (El-Kassar & Singh, Citation2019) by focusing specifically on the technologies associated with energy saving, pollution control (Begum et al., Citation2022), waste recycling, eco-friendly product design, the use of eco-wrapping, and organizational environmental management (Padilla-Lozano & Collazzo, Citation2022). According to the discussions, there is a distinction between traditional innovation and GI, both motivated by the need to comply with the environmental rules that market ecological concerns (Zhang et al., Citation2020). In this regard, According to Hermundsdottir and Aspelund (Citation2021), the study of green innovation is still in its early stages, with only a certain amount of literature focusing on its definition and concepts. Additionally, as per Charmondusit et al. (Citation2016), GI contributes by focusing on the business’s and customers’ environmental concerns via processes or products. Moreover, green product innovation applies creative concepts to the innovation, production, and strategic communication of innovative products that outpace traditional products regarding originality and their ecological design (Serrano-García et al., Citation2021). Moreover, green process innovation is also associated with energy conservation, toxic waste avoidance, and non-toxicity (Ma et al., Citation2017).

GI is an aspect that affects how well an organization is at being competitive (Li et al., Citation2019). Innovation is expected to add value ultimately, and for that to occur, it needs to reveal the productivity spikes that have contributed towards greater margins, increased profits, more value for participants, more market value, an improved corporate image, better environmental performance, or a combination of the above which will eventually make the organization more competitive (Tu & Wu, Citation2021). Businesses are more likely to participate in GI because they support growing the market and give them the viable benefit of being seen as eco-friendly (Adam et al., Citation2022). A green idea that works well enables organizations to become more efficient and improve their image as an environmentally friendly organization, leading to more profit (Li et al., Citation2017). Organizations that are early adopters of new technology are likely to charge more for green products, enhance their overall image, offer more environmentally friendly products and services, and ultimately find new marketplaces to achieve a competitive edge. We, therefore, formulated our hypothesis based on the above literature:

H5: Green innovation is positively and significantly related to organizational performance in the banking sector.

2.6. The mediating role of EE and GE

Employee engagement refers to employee commitment to the organization. Engaged, committed, and motivated employees are valuable resources for the business wanting to gain a viable edge in the marketplace (Ali et al., Citation2020). In this regard, EE determines an organization’s strength because an engaged employee understands their obligations and performs well beyond the organization’s growth (Bilal et al., Citation2015). According to CSR literature, organizational employees recognize their presence as important in a collectively acknowledged and conscientious organization, thus motivating them to go and achieve beyond their expected responsibilities. CSR activities at the organization tend to recruit competent employees and increase their commitment to the company and the causes that it is involved with (Ahmed et al., Citation2020). Scholars such as Rupp et al. (Citation2018) argued that CSR activities are also positively associated with EE, and employees are more willing to work out for corporations that spend their assets on society’s welfare and for organizational employees (Hosseini et al., Citation2022). CSR initiatives boost the employees’ self-esteem, strengthening their affiliation with the organization they work for, eventually leading to a higher level of engagement (Hur et al., Citation2022).

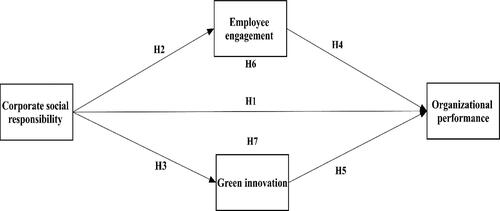

However, EE is a strong indicator of an employee’s organization’s performance, which eventually leads to organizational success (Al-Dalahmeh et al., Citation2018). Research has supported these findings (Ali et al., Citation2020). This is primarily Because actively engaged employees understand the importance of contributing to the organization’s overall performance and maintaining positive relationships with coworkers. Moreover, they are more likely to go the extra mile and put in extra effort, resulting in higher productivity and more employee satisfaction and commitment (Nazir & Islam, Citation2017). It is also noteworthy that EE has previously been linked to CSR (an exogenous variable) and organizational performance, as affirmed according to previous research (endogenous variable). Furthermore, Baron and Kenny (Citation1986) state that mediation will be established if there is a strong association between an exogenous and an endogenous variable. As a result, we have proposed hypotheses H6 and H7. Different empirical studies in this regard have considered green innovation as an exogenous variable, a control variable, or a mediating variable (Padilla-Lozano & Collazzo, Citation2022). A significant portion of the literature that has been written on green innovation is theoretical, essentially aimed at its understanding of the concept and development, largely because the significance and scope of green innovation are undoubtedly still in the process of being clearly defined (Aron & Molina, Citation2020). illustrates the study framework of the current survey research, the hypotheses proposed in the present study, and the need for an empirical investigation. Our research seeks to contribute to the previous literature by investigating the mediating role of green innovation and EE, particularly regarding the relationship between CSR and OP in the Malaysian banking sector. This will be accomplished through the investigation of the subsequent research assumptions:

Figure 1. Research framework.

Source: Created by the author’s based on previous literature.

H6: Employee engagement mediates the relationship between CSR and organizational performance.

H7: Green innovation mediates the relationship between CSR and organizational performance.

3. Research methodology

3.1. Data collection and procedure

This study used structured questionnaires to collect data from the sample representing participants. The questionnaires were collected from the top eight banks in Kuala Lumpur, Malaysia, which included Maybank, CIMB, Public Bank Bhd, RHB Bank, Hong Leong Bank, AmBank, UOB Malaysia, and Bank Rakyat. These banks are considered the leading banks in Malaysia regarding their resources, deposits, finances, market capitalization, number of employees, and the number of divisions, among other factors (Hamid et al., Citation2017). Data has been collected in two waves with a 4-week time frame to minimize the chances of common method bias. In recent years, this approach has been used in several studies (Zhao et al., Citation2020). This method was made smoother and error-free by assigning identifying numbers to different time questionnaires. This allowed the researchers to quickly and readily compare questionnaires after data gathering. Respondents’ demographics and perceptions of CSR-measured items that occurred for the first time in the questionnaire were also determined. However, the second visit included the EE, GI, and OP measurements, which were then collected.

As per Comrey and Lee (Citation1992), there are several sample size ranges in their capacity. For example, a sample size below 50 is regarded as weaker, between 51 and 100 is regarded as weak, and between 101 and 200 is regarded as appropriate. Furthermore, a sample size between 201 and 300 is considered good, while a sample size between 500 and 1000 is considered excellent. As a result, the sample size for this study was 581, which is deemed an excellent sample size. The researcher also distributed 800 questionnaires to the employees in the banking sector via a survey methodology, of which 581 questions received completed answers, and 31 questionnaires were deleted due to incompleteness, leading to a net response rate of around 69% for the study.

3.2. Measures

Ranging from ‘strongly disagree’ to ‘strongly agree’, the researcher has employed a Likert scale with five points Likert in the survey designed. Employee awareness of CSR was assessed by considering a six-item formed by Cheema et al. (Citation2020). The six questions have been designed to assess an employee’s perspective of their organization’s efforts in CSR, primarily by asking whether or not they are content with it and appreciate the organization’s current CSR activities, among several other things (Tsourvakas & Yfantidou, Citation2018). Meanwhile, employee engagement has also been measured by using a nine-item survey that measures three subdimensions: physical, emotional, and cognitive engagement (Rich et al., Citation2010). In this regard, four items from prior research were used to assess the organization’s overall performance (Lin et al., Citation2013). Furthermore, the development in the market standing, sales capacity, profit ratio, as well as reputation have all been measured using these items. A total of eight questions selected and modified from earlier research by El-Kassar and Singh (Citation2019) were also used to assess green innovation. Items that are non-toxic, simple to reuse, with non-polluting have been considered to gauge the organization’s use of environmentally friendly materials. The use of eco-labelling was also tracked down and recorded. comprises a list of the items of CSR, EE, GI, and OP variables.

Table 1. Variables with items.

4. Results

The research model was analyzed using the partial least squares structural equation modeling (PLS-SEM), SmartPLS Version 3.3.7. As per Hair et al. (Citation2017), PLS-SEM is the extensively used statistical software under consideration and used by researchers today. PLS-SEM has been frequently employed in marketing and management research (Imran et al., Citation2021; Imran & Jingzu, Citation2022). Furthermore, the PLS-SEM technique is advised where there is a lack of theoretical foundation for an issue. Furthermore, Hair et al. (Citation2014) indicated that PLS-SEM is a suitable approach to carry out an exploratory analysis, as shown by their research. PLS-SEM is a two-stage technique that includes the following steps: The measurement model is analyzed for the validity and reliability of the proposed variables in the first step. Then, the structural model is evaluated for the path coefficients in the second stage. A further section outlines these two stages in depth.

4.1. Measurement model

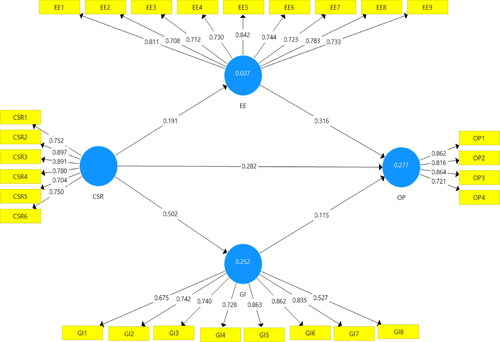

For this research, the SmartPLS 3.3.7 approach was used to test the developed hypotheses with SEM. Furthermore, PLS is useful when the empirical data doesn’t meet normality requirements (Dijkstra & Henseler, Citation2015). It is considered that the results of the PLS model are much more reliable than the results of the ordinary least square (OLS) model, particularly when there are problems with multicollinearity in the data, missing data, or a small sample size. Therefore, the PLS method was employed as a sample size in this study, which was not significantly large. Our study has four reflective variables in it. The PLS-SEM comprises measurement models () and structural models ().

Figure 2. Reliability and validity.

Source: Author's Estimation

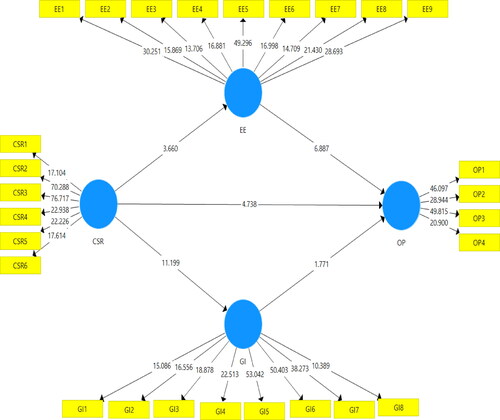

Figure 3. Structural model.

Source: Author's Estimation

Internal consistency reliability, convergent, and discriminant validity are all aspects of the measurement model. This is presented in because the outer loading of every item is more than 0.50 (Hair et al., Citation2014), thus indicating that the items meet this threshold. Moreover, internal consistency reliability was investigated to determine Cronbach’s alpha coefficient and composite reliability (CR) (Chin, Citation2010). In this regard, demonstrates that Cronbach’s alpha and CR for all constructs are more than 0.70, indicating that the internal consistency reliability is acceptable. The degree to which constructs items measure the constructs that are the same as each other is known as convergent validity (Clark & Watson, Citation2019). The convergent validity is calculated using the constructs’ AVE, and research has proven that the AVE of variables should be at least 0.50, as per Hair et al. (Citation2021). explains that the AVE of the constructs is more than the threshold value of 0.50.

Table 2. Reliability and validity of the constructs.

Table 3. Discriminant validity Fornell-Larcker criteria.

When considering the discriminant validity assessment, Fornell and Larcker (Citation1981) recommended a conventional measurement method that could be used in two separate stages. The first stage could evaluate the value of the AVE square root with the values of the measures of the correlational value. The second stage could compare the AVE value to the square correlational values. Also, because the values on the diagonal are greater than any of the values in their respective columns and rows, this is proven in the following table (), shown below. Recently, researchers have introduced a unique way of calculating discriminant validity. Furthermore, the investigators have concluded that the standard metric is inappropriate for calculating discriminant validity in this context. In this regard, Henseler et al. (Citation2015) developed a unique method known as the Heterotrait-Monotrait Ratio (HTMT) of correlation to calculate the discriminant validity.

As a conclusion of this research, according to our findings, both Fornell and Larcker () and HTMT (refer to ) performed adequately. Generally, while each indicator has outer loadings with the least difference, the factor loadings are within 0.65 and 0.85 on the standard deviation scale. Moreover, According to Henseler et al. (Citation2015), the threshold value of HTMT should be less than 0.90 for theoretically similar variables and 0.85 for conceptually dissimilar constructs. While indicates that the variables have an HTMT value lower than 0.85.

Table 4. Discriminant validity HTMT criteria.

4.2 Regression analysis

The assessments of the hypotheses are presented in this section of the study. indicates the β-value, t-value, and p value employed to ascertain whether the hypotheses are accepted or rejected. Moreover, this portion also contains a structural model that can be used to evaluate the study-related proposed hypotheses. The researchers have used the structural model to quantify the p and t-value to examine the hypotheses proposed in the literature. It is possible to accept the hypotheses if the t-value is more than 1.96 or the p value is less than 0.05. The direct and indirect hypothesis relationships are therefore presented in . Moreover, the structural model shown in shows that the p value and t-value of CSR with OP (p value = 0.000; t-value = 4.738), and CSR are positively and significantly associated with Op. Therefore, hypothesis H1 is supported. At the same time, CSR is positively and statistically significant with EE and DI (p value = 0.000; t-value = 3.660, p value = 0.000; t-value = 11.199), where hypotheses H2 and H3 are supported. Furthermore, the association between H4 is positive and statistically significant (p value = 0.000; t-value = 6.887) and supported. Additionally, H5 GI does not have a statistically significant association with OP but does have a positive relationship (p value = 0.077; t-value = 1.771) with OP, and H5 supports the result.

Table 5. Hypothesis direct and indirect effects.

Employee engagement was a significant mediator in the relationship with CSR and OP (p value = 0.000; t-value = 3.729) and was found to have supported hypothesis H6. Moreover, green innovation is also positive but not significantly mediated among CSR and OP (p value = 0.077; t-value = 1.773), and the study findings do not support the conclusions drawn. Further use of the Variance Accounted For (VAF) method was further used to examine the mediating influence of EE and GI on the association between CSR and OP. Moreover, regarding the VAF, with values less than 20% (no mediation), between 20 and 80% (partial mediation), and higher than 80% (full mediation), in that order, H6 is partially mediated, but H7 is not mediated.

The value of f2 specifies whether an exogenous construct influences an endogenous construct (Ramayah et al., Citation2018). As indicated by Cohen (Citation1988), there are three types of f2 value ranges: the smaller effect (0.02), the medium effect (0.15), and the larger effect (0.35). The outcomes of this analysis prove that the empirical value impacts the OP. In fact, to the smaller influence of CSR on OP (f2 = 082), the medium influence of EE on OP (f2 = 0.129). Furthermore, the value of GI also exerts a smaller effect on the OP (f2 = 0.013).

There have only been a Few studies that have adopted an alternative method for determining the predictive accuracy of the model and thus obtaining Q2 value. When utilizing the SmartPLS 3.3.7 tool, the Q2 is calculated using the blindfolding method. In this regard, Chin (Citation1998) indicated that the Q2 value should be larger than 0. Also, as per Cohen et al. (Citation2013), Q2 higher than 0.35, 0.15, and 0.02 implies large, medium, and small predictive significance, respectively. The EE Q2 value (0.013) has a smaller predictive relevance impact. In contrast, the OP Q2 value (0.178) has a medium predictive relevance effect, and the GI (0.136) also has a smaller predictive relevance effect.

4.3. Discussion

According to Suttipun et al. (Citation2021) research on CSR and the financial performance of the listed firms in Thailand, there is a positive association between CSR and financial performance. In addition, some academics have conducted research on the topic of CSR and OP in the banking sector in Asia, such as in India (Deb et al., Citation2022), Pakistan (Szegedi et al., Citation2020), and China (Zhou et al., Citation2021). They found that CSR influences the performance of Banks. The increasing worldwide apprehension over climate change and global warming has underscored the significance of banks in their CSR and environmental initiatives. Nevertheless, it is worth noting that there has been a shortage of academic research examining the correlation between CSR and financial performance in developing countries such as Malaysia, as highlighted by Xu et al. (Citation2022). The results of this study demonstrate a significant association between CSR and OP. This relationship exists directly and indirectly, with the indirect influence being mediated by EE and GI. These findings align with prior research by Ali et al. (Citation2020). The influence of CSR on EE is significant, indicating that CSR programs positively impact employee engagement. Furthermore, our study provides empirical evidence that the construction of EE serves as a crucial mediator in the association between CSR and OP. These findings underscore the significance of EE in facilitating the translation of CSR initiatives into improved performance outcomes. At the same time, the role of green innovation (GI) in facilitating the link between CSR and OP was shown to be statistically insignificant in this research. This suggests that, within the particular context examined, green innovation may not directly impact OP. The comparison of these findings with existing studies in academic literature provides additional evidence for the importance of CSR and EE as crucial factors in mediating the relationship with OP. Moreover, it highlights the contextual variations that can impact the role of GI within diverse banking environments.

5. Conclusion, policy implications, limitation and future study

5.1. Conclusion

The study conducted by Tulcanaza-Prieto et al. (Citation2020) in the banking sector supports the concept that CSR has a positive and statistically significant effect on OP. The observed consistency provides empirical evidence that CSR initiatives positively impact organizational performance. The potential positive impacts of CSR, such as the improvement of reputation, fostering customer loyalty, and strengthening stakeholder relationships, are expected to play a role in the observed enhancements in OP. The findings are additionally supported by the research carried out by Lu et al. (Citation2020) and Khan et al. (Citation2021) in the manufacturing industry of Pakistan, which also demonstrated a significant positive impact of CSR on the performance of SMEs. This finding suggests that the positive correlation between CSR and OP is applicable across various industries and regions, thereby enhancing the generalizability of the results. The inconsistent findings observed in the study conducted by Crisóstomo et al. (Citation2011), which indicated a negative correlation between CSR and OP, may be explained by differences in the specific context of the banking sector, characteristics of the sample used, or variations in the methods employed for measurement. A range of cultural, social, and economic factors specific to different regions and industries can influence the impact of CSR on OP. The results emphasize the significant impact of CSR initiatives on the achievement of banks. Prior studies have established the importance of CSR in attaining enduring sustainability and financial success within the banking industry. Therefore, managers and owners must acknowledge the significance of CSR due to its direct influence on organizational performance and its contribution to the overall success of a bank. The findings of Obeidat (Citation2016) support the hypothesis that CSR and EE constraints play a significant role in shaping a corporation’s business model. This alignment is crucial for improving OP, as evidenced by the inline noted in this study. The integration of CSR and EE limitations has the potential to foster the adoption of more sustainable and responsible business practices, thereby exerting a positive influence on OP.

These findings contribute to the ongoing inconclusive debate surrounding the link between CSR and innovation, especially in the context of developing nations. However, it is important to note that CSR does have a significant impact on overall bank performance. Nevertheless, the literature on the correlation between GI and bank performance is limited (Khan et al., Citation2022). Our study explores this relationship, which has been previously overlooked in research examining the link between CSR and GI. Additionally, EE is shown to substantially impact overall organizational performance, consistent with the findings of Kazimoto (Citation2016) that EE significantly affects organizational performance. On the other hand, Arslan and Roudaki (Citation2019) conclude that EE specifically impacts business performance assessment. Moreover, GI has been proven to enhance organizational performance, aligning with the findings of Tang et al. (Citation2018) and El-Kassar and Singh (Citation2019) that GI contributes to achieving a competitive advantage. Our research further identifies EE and GI as positive mediators in the relationship between CSR and organizational performance. This study provides novel insights into the impact of CSR initiatives on bank efficiency. As banks play a crucial role in the global economic system, policymakers have a valid reason to focus on increasing CSR activities in the banking sector to enhance bank performance and, ultimately, have positive implications for the overall economy. The study’s findings emphasize the importance of understanding the performance factors relevant to banks to support their contribution to economic growth.

5.2. Policy implications

The policy implications of the findings of this study are as follows:

The research emphasizes that CSR exerts a positive and significant influence on the performance of organizations. Hence, policymakers within the banking industry must promote and provide incentives for banks to embrace and execute CSR initiatives. The prioritization of responsible business practices and active engagement in social and environmental contributions can potentially enhance the overall performance of banks.

The research findings suggest that CSR has a significant impact on the level of EE. Policymakers can utilize this insight to formulate policies that promote the development of a work environment conducive to employee engagement within the banking sector. Employees actively involved and invested in their work demonstrate higher commitment and productivity, ultimately leading to improved organizational performance and increased customer satisfaction.

The findings indicate that CSR significantly and positively influences green innovation. This implies that incorporating sustainable practices can result in innovative advancements within the banking sector. It is essential for policymakers to actively endorse and facilitate green innovation initiatives, thereby incentivizing banks to embrace ecologically sustainable practices and technologies that effectively mitigate their environmental impact.

With the positive effect of employee engagement on OP, policymakers may direct their attention toward implementing strategies that augment employee motivation and satisfaction. Implementing employee development initiatives, work-life balance policies, and recognition programs can positively impact performance outcomes within the banking industry.

Policymakers need to recognize the intermediary function of EE in the correlation between CSR and OP. Implementing CSR initiatives can directly affect OP and indirectly influence it by fostering heightened levels of EE. Establishing a workplace culture that prioritizes the well-being of employees and encourages their active participation in CSR initiatives can yield significant enhancements in OP.

The study indicates that green innovation positively affects CSR, but it may not directly impact OP within the specific context being examined. It is recommended that policymakers consider this constraint and investigate supplementary approaches to maximize the performance implications of green innovation, potentially by integrating it with other measures to enhance performance.

5.3. Limitations and future study

The limitations of current research are similar to those of earlier investigations, which emerging researchers in the future can address. In the first part, a cross-sectional strategy has been referred to. Researchers are doubtful that CSR, EE, and green innovation in the banking sector can provide the same results previously. Thus, future researchers can apply the same study paradigm to determine whether results improve over longer durations. Our study obtained data from the Malaysian banking sector, and future researchers can collect data from SME's to observe how the findings have changed. Moreover, future studies can use green capacity as a mediating factor with CSR and OP to determine whether it is statistically substantial. Lastly, since the present research was organized in the Malaysian environment, which has its unique culture, future scholars could perform a parallel study in other nations to discover how progress has been made.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abbas, J. (2020). Impact of total quality management on corporate green performance through the mediating role of corporate social responsibility. Journal of Cleaner Production, 242, 118458. https://doi.org/10.1016/j.jclepro.2019.118458

- Achi, A., Adeola, O., & Achi, F. C. (2022). CSR and green process innovation as antecedents of micro, small, and medium enterprise performance: Moderating role of perceived environmental volatility. Journal of Business Research, 139, 771–781.

- Adam, A., Sam, T. H., Latif, K., Yusof, Y., Khan, Z., Ali Memon, D., Saif, Y., Hatem, N., Iliyas Ahmed, M., & Abdul Kadir, A. Z. (2022). Review on advanced CNC controller for manufacturing in industry 4.0. In Enabling industry 4.0 through advances in manufacturing and materials: Selected articles from iM3F 2021, Malaysia (pp. 261–269). Springer Nature Singapore.

- Aggarwal, A., & Saxena, N. (2023). Examining the relationship between corporate social responsibility, corporate reputation and brand equity in Indian banking industry. Journal of Public Affairs, 23(1), e2838. https://doi.org/10.1002/pa.2838

- Ahmad, N., Naveed, R. T., Scholz, M., Irfan, M., Usman, M., & Ahmad, I. (2021). CSR communication through social media: A litmus test for banking consumers’ loyalty. Sustainability, 13(4), 2319. https://doi.org/10.3390/su13042319

- Ahmed, M., Zehou, S., Raza, S. A., Qureshi, M. A., & Yousufi, S. Q. (2020). Impact of CSR and environmental triggers on employee green behavior: The mediating effect of employee well‐being. Corporate Social Responsibility and Environmental Management, 27(5), 2225–2239. https://doi.org/10.1002/csr.1960

- Al-Dalahmeh, M., Masa’deh, R., Abu Khalaf, R. K., & Obeidat, B. Y. (2018). The effect of employee engagement on organizational performance via the mediating role of job satisfaction: The case of IT employees in Jordanian banking sector. Modern Applied Science, 12(6), 17–43. https://doi.org/10.5539/mas.v12n6p17

- Ali, U., Iqbal, A., Sohail, M., Abdullah, F. A., & Khan, Z. (2022). Compact implicit difference approximation for time-fractional diffusion-wave equation. Alexandria Engineering Journal, 61(5), 4119–4126.

- Ali, H. Y., Asrar‐ul‐Haq, M., Amin, S., Noor, S., Haris‐ul‐Mahasbi, M., & Aslam, M. K. (2020). Corporate social responsibility and employee performance: The mediating role of employee engagement in the manufacturing sector of Pakistan. Corporate Social Responsibility and Environmental Management, 27(6), 2908–2919. https://doi.org/10.1002/csr.2011

- Ali, Z., Bashir, M., & Mehreen, A. (2019). Managing organizational effectiveness through talent management and career development: The mediating role of employee engagement. Journal of Management Sciences, 6(1), 62–78. https://doi.org/10.20547/jms.2014.1906105

- Aron, A. S., & Molina, O. (2020). Green innovation in natural resource industries: The case of local suppliers in the Peruvian mining industry. The Extractive Industries and Society, 7(2), 353–365. https://doi.org/10.1016/j.exis.2019.09.002

- Arslan, M., & Roudaki, J. (2019). Examining the role of employee engagement in the relationship between organizational cynicism and employee performance. International Journal of Sociology and Social Policy, 39(1/2), 118–137. https://doi.org/10.1108/IJSSP-06-2018-0087

- Asrar-Ul-Haq, M., Kuchinke, K. P., & Iqbal, A. (2017). The relationship between corporate social responsibility, job satisfaction, and organizational commitment: Case of Pakistani higher education. Journal of Cleaner Production, 142, 2352–2363. https://doi.org/10.1016/j.jclepro.2016.11.040

- Bai, X., & Chang, J. (2015). Corporate social responsibility and firm performance: The mediating role of marketing competence and the moderating role of market environment. Asia Pacific Journal of Management, 32(2), 505–530. https://doi.org/10.1007/s10490-015-9409-0

- Bailey, C., Madden, A., Alfes, K., & Fletcher, L. (2017). The meaning, antecedents and outcomes of employee engagement: A narrative synthesis. International Journal of Management Reviews, 19(1), 31–53. https://doi.org/10.1111/ijmr.12077

- Barauskaite, G., & Streimikiene, D. (2021). Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corporate Social Responsibility and Environmental Management, 28(1), 278–287. https://doi.org/10.1002/csr.2048

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037//0022-3514.51.6.1173

- Begum, S., Ashfaq, M., Xia, E., & Awan, U. (2022). Does green transformational leadership lead to green innovation? The role of green thinking and creative process engagement. Business Strategy and the Environment, 31(1), 580–597. https://doi.org/10.1002/bse.2911

- Belasri, S., Gomes, M., & Pijourlet, G. (2020). Corporate social responsibility and bank efficiency. Journal of Multinational Financial Management, 54, 100612. https://doi.org/10.1016/j.mulfin.2020.100612

- Bilal, H., Shah, B., Yasir, M., & Mateen, A. (2015). Employee engagement and contextual performance of teaching faculty of private universities. Journal of Managerial Sciences, IX(1), 82.

- Birindelli, G., Ferretti, P., Intonti, M., & Iannuzzi, A. P. (2015). On the drivers of corporate social responsibility in banks: Evidence from an ethical rating model. Journal of Management & Governance, 19(2), 303–340. https://doi.org/10.1007/s10997-013-9262-9

- Bruna, M. G., & Lahouel, B. B. (2022). CSR & financial performance: Facing methodological and modeling issues commentary paper to the eponymous FRL article collection. Finance Research Letters, 44, 102036. https://doi.org/10.1016/j.frl.2021.102036

- Bugandwa, T. C., Kanyurhi, E. B., Bugandwa Mungu Akonkwa, D., & Haguma Mushigo, B. (2021). Linking corporate social responsibility to trust in the banking sector: Exploring disaggregated relations. International Journal of Bank Marketing, 39(4), 592–617. https://doi.org/10.1108/IJBM-04-2020-0209

- Caruana, A., Vella, J., Konietzny, J., & Chircop, S. (2018). Corporate greed: Its effect on customer satisfaction, corporate social responsibility and corporate reputation among bank customers. Journal of Financial Services Marketing, 23(3-4), 226–233. https://doi.org/10.1057/s41264-018-0050-0

- Chang, J. I., & Lee, C. Y. (2020). The effect of service innovation on customer behavioral intention in the Taiwanese insurance sector: The role of word of mouth and corporate social responsibility. Journal of Asia Business Studies, 14(3), 341–360. https://doi.org/10.1108/JABS-06-2018-0168

- Charmondusit, K., Gheewala, S. H., & Mungcharoen, T. (2016). Green and sustainable innovation for cleaner production in the Asia-Pacific region. Journal of Cleaner Production, 134, 443–446. https://doi.org/10.1016/j.jclepro.2016.06.160

- Cheema, S., Afsar, B., Al‐Ghazali, B. M., & Maqsoom, A. (2020). Retracted: How employee’s perceived corporate social responsibility affects employee’s pro‐environmental behaviour? The influence of organizational identification, corporate entrepreneurship, and environmental consciousness. Corporate Social Responsibility and Environmental Management, 27(2), 616–629. https://doi.org/10.1002/csr.1826

- Cheffi, W., Abdel-Maksoud, A., & Farooq, M. O. (2021). CSR initiatives, organizational performance and the mediating role of integrating CSR into management control systems: Testing an inclusive model within SMEs in an emerging economy. Journal of Management Control, 32(3), 333–367. https://doi.org/10.1007/s00187-021-00323-6

- Chin, W. W. (2010). “How to write up and report PLS analyses”, In Esposito Vinzi, V., Chin, W.W., Henseler, J., et al. (Eds), Handbook of Partial Least Squares: Concepts, Methods and Applications (Springer Handbooks of Computational Statistics Series), Springer, Heidelberg, Dordrecht, London, New York, NY, Vol. II, pp. 655–690.

- Chin, W. W. (1998). Commentary: Issues and opinion on structural equation modeling. MIS Quarterly, 22(1), vii–xvi.

- Cho, S. J., Chung, C. Y., & Young, J. (2019). Study on the relationship between CSR and financial performance. Sustainability, 11(2), 343. https://doi.org/10.3390/su11020343

- Clark, L. A., & Watson, D. (2019). Constructing validity: New developments in creating objective measuring instruments. Psychological Assessment, 31(12), 1412–1427. https://doi.org/10.1037/pas0000626

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Erlbaum.

- Cohen, L., Manion, L., & Morrison, K. (2013). Research methods in education. Routledge.

- Comrey, A. L., & Lee, H. B. (1992). Interpretation and application of factor analytic results. Comrey AL, Lee HB. A First Course in Factor Analysis, 2, 1992.

- Crisóstomo, V. L., de Souza Freire, F., & de Vasconcellos, F. C. (2011). Corporate social responsibility, firm value and financial performance in Brazil. Social Responsibility Journal, 7(2), 295–309. https://doi.org/10.1108/17471111111141549

- Deb, D., Gillet, P., Bernard, P., & De, A. (2022). Examining the impact of corporate social responsibility on the financial performance of Indian companies. FIIB Business Review, 231971452210996. https://doi.org/10.1177/23197145221099682

- Dijkstra, T. K., & Henseler, J. (2015). Consistent and asymptotically normal PLS estimators for linear structural equations. Computational Statistics & Data Analysis, 81, 10–23. https://doi.org/10.1016/j.csda.2014.07.008

- El-Kassar, A. N., & Singh, S. K. (2019). Green innovation and organizational performance: The influence of big data and the moderating role of management commitment and HR practices. Technological Forecasting and Social Change, 144, 483–498. https://doi.org/10.1016/j.techfore.2017.12.016

- Farrukh, M., Sajid, M., Lee, J. W. C., & Shahzad, I. A. (2020). The perception of corporate social responsibility and employee engagement: Examining the underlying mechanism. Corporate Social Responsibility and Environmental Management, 27(2), 760–768. https://doi.org/10.1002/csr.1842

- Fatma, M., & Rahman, Z. (2016). The CSR's influence on customer responses in Indian banking sector. Journal of Retailing and Consumer Services, 29, 49–57. https://doi.org/10.1016/j.jretconser.2015.11.008

- Ferreira, P., & de Oliveira, E. R. (2014). Does corporate social responsibility impact on employee engagement? Journal of Workplace Learning, 26(3/4), 232–247. https://doi.org/10.1108/JWL-09-2013-0070

- Flammer, C., & Luo, J. (2017). Corporate social responsibility as an employee governance tool: Evidence from a quasi‐experiment. Strategic Management Journal, 38(2), 163–183. https://doi.org/10.1002/smj.2492

- Forgione, A. F., Laguir, I., & Staglianò, R. (2020). Effect of corporate social responsibility scores on bank efficiency: The moderating role of institutional context. Corporate Social Responsibility and Environmental Management, 27(5), 2094–2106. https://doi.org/10.1002/csr.1950

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.2307/3151312

- Fukuyama, H., & Tan, Y. (2022). Implementing strategic disposability for performance evaluation: Innovation, stability, profitability and corporate social responsibility in Chinese banking. European Journal of Operational Research, 296(2), 652–668. https://doi.org/10.1016/j.ejor.2021.04.022

- Galdeano, D., Ahmed, U., Fati, M., Rehan, R., & Ahmed, A. J. M. S. L. (2019). Financial performance and corporate social responsibility in the banking sector of Bahrain: Can engagement moderate? Management Science Letters, 9(10), 1529–1542. https://doi.org/10.5267/j.msl.2019.5.032

- Gallup Organization. (2017). State of the Global Workplace. Gallup Management Journal. www.gallup.com/workplace/238079/state-global-workplace-2017.aspx

- Gangi, F., Mustilli, M., & Varrone, N. (2019). The impact of corporate social responsibility (CSR) knowledge on corporate financial performance: Evidence from the European banking industry. Journal of Knowledge Management, 23(1), 110–134. https://doi.org/10.1108/JKM-04-2018-0267

- Gangi, F., Mustilli, M., Varrone, N., & Daniele, L. M. (2018). Corporate social responsibility and banks’ financial performance. International Business Research, 11(10), 42–58. https://doi.org/10.5539/ibr.v11n10p42

- Ginter, P. M., Duncan, W. J., & Swayne, L. E. (2018). The strategic management of health care organizations. John Wiley & Sons.

- Glavas, A. (2016). Corporate social responsibility and employee engagement: Enabling employees to employ more of their whole selves at work. Frontiers in Psychology, 7, 796. https://doi.org/10.3389/fpsyg.2016.00796

- Grayson, D., & Hodges, A. (2017). Corporate social opportunity!: Seven steps to make corporate social responsibility work for your business. Routledge.

- Gupta, N., & Sharma, V. (2016). The relationship between corporate social responsibility and employee engagement and its linkage to organizational performance: A conceptual model. IUP Journal of Organizational Behavior, 15(3).

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021). Partial least squares structural equation modeling (PLS-SEM) using R. A Workbook.

- Hair, J., Hollingsworth, C. L., Randolph, A. B., & Chong, A. Y. L. (2017). An updated and expanded assessment of PLS-SEM in information systems research. Industrial Management & Data Systems, 117(3), 442–458. https://doi.org/10.1108/IMDS-04-2016-0130

- Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2014). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications.

- Hamid, B. A., Najibullah, S., & Habibullah, M. S. (2017). Marketing effectiveness of Islamic and conventional banks: Evidence from Malaysia. In Islamic banking (pp. 51–80). Palgrave Macmillan.

- He, H., & Harris, L. (2020). The impact of Covid-19 pandemic on corporate social responsibility and marketing philosophy. Journal of Business Research, 116, 176–182. https://doi.org/10.1016/j.jbusres.2020.05.030

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hermundsdottir, F., & Aspelund, A. (2021). Sustainability innovations and firm competitiveness: A review. Journal of Cleaner Production, 280, 124715. https://doi.org/10.1016/j.jclepro.2020.124715

- Hosseini, S. A., Moghaddam, A., Damganian, H., & Shafiei Nikabadi, M. (2022). The effect of perceived corporate social responsibility and sustainable human resources on employee engagement with the moderating role of the employer brand. Employee Responsibilities and Rights Journal, 34(2), 101–121. https://doi.org/10.1007/s10672-021-09376-0

- Hossen, M. M., Chan, T. J., & Hasan, N. A. M. (2020). Mediating role of job satisfaction on internal corporate social responsibility practices and employee engagement in higher education sector. Contemporary Management Research, 16(3), 207–227. https://doi.org/10.7903/cmr.20334

- Hou, T. C. T. (2019). The relationship between corporate social responsibility and sustainable financial performance: Firm‐level evidence from Taiwan. Corporate Social Responsibility and Environmental Management, 26(1), 19–28. https://doi.org/10.1002/csr.1647

- Hur, W. M., & Kim, Y. (2020). Customer reactions to bank hypocrisy: The moderating role of customer–company identification and brand equity. International Journal of Bank Marketing, 38(7), 1553–1574. https://doi.org/10.1108/IJBM-04-2020-0191

- Hur, W. M., Rhee, S. Y., Lee, E. J., & Park, H. (2022). Corporate social responsibility perceptions and sustainable safety behaviors among frontline employees: The mediating roles of organization‐based self‐esteem and work engagement. Corporate Social Responsibility and Environmental Management, 29(1), 60–70. https://doi.org/10.1002/csr.2173

- Im, S., Chung, Y. W., & Yang, J. Y. (2016). Employees’ participation in corporate social responsibility and organizational outcomes: The moderating role of person–CSR fit. Sustainability, 9(1), 28. https://doi.org/10.3390/su9010028

- Imran, M., & Jingzu, G. (2022). Green organizational culture, organizational performance, green innovation, environmental performance: A mediation-moderation model. Journal of Asia-Pacific Business, 23(2), 161–182. https://doi.org/10.1080/10599231.2022.2072493

- Imran, M., Arshad, I., & Ismail, F. (2021). Green organizational culture and organizational performance: The mediating role of green innovation and environmental performance. Jurnal Pendidikan IPA Indonesia, 10(4), 515–530. https://doi.org/10.15294/jpii.v10i4.32386

- Imran, M., Ismail, F., Arshad, I., Zeb, F., & Zahid, H. (2022). The mediating role of innovation in the relationship between organizational culture and organizational performance in Pakistan’s banking sector. Journal of Public Affairs, 22(S1), e2717. https://doi.org/10.1002/pa.2717

- Javed, M., Rashid, M. A., Hussain, G., & Ali, H. Y. (2020). The effects of corporate social responsibility on corporate reputation and firm financial performance: Moderating role of responsible leadership. Corporate Social Responsibility and Environmental Management, 27(3), 1395–1409. https://doi.org/10.1002/csr.1892

- Jiang, H., & Luo, Y. (2020). Driving employee engagement through CSR communication and employee perceived motives: The role of CSR-related social media engagement and job engagement. International Journal of Business Communication, 232948842096052. https://doi.org/10.1177/2329488420960528

- Jie, C. T., & Hasan, N. A. M. (2018). Predictors of employees’ job satisfaction through corporate social responsibility (CSR) practices in Malaysian Banking Company. Advanced Science Letters, 24(5), 3072–3078. https://doi.org/10.1166/asl.2018.11320

- Kaplan, R. S., & Norton, D. P. (1996). The balanced scorecard: Translating strategy into action. Harvard Business School Press.

- Kazimoto, P. (2016). Employee engagement and organizational performance of retails enterprises. American Journal of Industrial and Business Management, 06(04), 516–525. https://doi.org/10.4236/ajibm.2016.64047

- Khan, H. Z., Bose, S., & Johns, R. (2020). Regulatory influences on CSR practices within banks in an emerging economy: Do banks merely comply? Critical Perspectives on Accounting, 71, 102096. https://doi.org/10.1016/j.cpa.2019.102096

- Khan, P. A., Johl, S. K., & Akhtar, S. (2022). Vinculum of sustainable development goal practices and firms’ financial performance: A moderation role of green innovation. Journal of Risk and Financial Management, 15(3), 96. https://doi.org/10.3390/jrfm15030096

- Khan, Z., Yusof, Y. B., Abass, N. H. B., Ahmed, M. B. I., & Jamali, Q. B. (2021). Recommendations for the Implementation of ISO 9001: 2015 in the Manufacturing Industry of Pakistan. Engineering, Technology & Applied Science Research, 11(3), 7177–7180. https://doi.org/10.48084/etasr.4075

- Kim, M. S., & Thapa, B. (2018). Relationship of ethical leadership, corporate social responsibility and organizational performance. Sustainability, 10(2), 447. https://doi.org/10.3390/su10020447

- Kim, M. J., & Kim, B. J. (2020). Analysis of the importance of job insecurity, psychological safety and job satisfaction in the CSR-performance link. Sustainability, 12(9), 3514.

- Kraus, S., Rehman, S. U., & García, F. J. S. (2020). Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change, 160, 120262. https://doi.org/10.1016/j.techfore.2020.120262

- Li, G., Wang, X., Su, S., & Su, Y. (2019). How green technological innovation ability influences enterprise competitiveness. Technology in Society, 59, 101136. https://doi.org/10.1016/j.techsoc.2019.04.012

- Li, D., Cao, C., Zhang, L., Chen, X., Ren, S., & Zhao, Y. (2017). Effects of corporate environmental responsibility on financial performance: The moderating role of government regulation and organizational slack. Journal of Cleaner Production, 166, 1323–1334.

- Lin, R. J., Tan, K. H., & Geng, Y. (2013). Market demand, green product innovation, and firm performance: Evidence from Vietnam motorcycle industry. Journal of Cleaner Production, 40, 101–107. https://doi.org/10.1016/j.jclepro.2012.01.001

- Lohana, S., Imran, M., Harouache, A., Sadia, A., & Ur Rehman, Z. (2023). Impact of environment, culture, and sports tourism on the economy: A mediation-moderation model. Economic Research-Ekonomska Istraživanja, 36(3), 2222306. https://doi.org/10.1080/1331677X.2023.2222306

- Lu, J., Ren, L., Zhang, C., Rong, D., Ahmed, R. R., & Streimikis, J. (2020). Modified Carroll’s pyramid of corporate social responsibility to enhance organizational performance of SMEs industry. Journal of Cleaner Production, 271, 122456.

- Ma, Y., Hou, G., & Xin, B. (2017). Green process innovation and innovation benefit: The mediating effect of firm image. Sustainability, 9(10), 1778. https://doi.org/10.3390/su9101778

- Martinez-Conesa, I., Soto-Acosta, P., & Palacios-Manzano, M. (2017). Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. Journal of Cleaner Production, 142, 2374–2383. https://doi.org/10.1016/j.jclepro.2016.11.038

- Matuszak,., & Różańska, E., Ł (2017). An examination of the relationship between CSR disclosure and financial performance: The case of Polish banks. Accounting and Management Information Systems, 16(4), 522–533.

- Mehralian, G., Nazari, J. A., Zarei, L., & Rasekh, H. R. (2016). The effects of corporate social responsibility on organizational performance in the Iranian pharmaceutical industry: The mediating role of TQM. Journal of Cleaner Production, 135, 689–698. https://doi.org/10.1016/j.jclepro.2016.06.116

- Memon, K. R., Ghani, B., & Khalid, S. (2020). The relationship between corporate social responsibility and employee engagement-A social exchange perspective. International Journal of Business Science & Applied Management, 15(1), 1–16.

- Nazir, O., & Islam, J. U. (2017). Enhancing organizational commitment and employee performance through employee engagement: An empirical check. South Asian Journal of Business Studies, 6(1), 98–114. https://doi.org/10.1108/SAJBS-04-2016-0036

- Nimon, K., Shuck, B., & Zigarmi, D. (2016). Construct overlap between employee engagement and job satisfaction: A function of semantic equivalence? Journal of Happiness Studies, 17(3), 1149–1171. https://doi.org/10.1007/s10902-015-9636-6

- Norberg, P. (2018). Bankers bashing back: Amoral CSR justifications. Journal of Business Ethics, 147(2), 401–418. https://doi.org/10.1007/s10551-015-2965-x

- Obeidat, B. Y. (2016). Exploring the relationship between corporate social responsibility, employee engagement, and organizational performance: The case of Jordanian mobile telecommunication companies. International Journal of Communications, Network and System Sciences, 09(09), 361–386.), https://doi.org/10.4236/ijcns.2016.99032

- Ogbonnaya, C., & Valizade, D. (2018). High performance work practices, employee outcomes and organizational performance: A 2-1-2 multilevel mediation analysis. The International Journal of Human Resource Management, 29(2), 239–259. https://doi.org/10.1080/09585192.2016.1146320

- Padilla-Lozano, C. P., & Collazzo, P. (2022). Corporate social responsibility, green innovation and competitiveness–causality in manufacturing. Competitiveness Review: An International Business Journal, 32(7), 21–39. https://doi.org/10.1108/CR-12-2020-0160

- Park, E., Kim, K. J., & Kwon, S. J. (2017). Corporate social responsibility as a determinant of consumer loyalty: An examination of ethical standard, satisfaction, and trust. Journal of Business Research, 76, 8–13. https://doi.org/10.1016/j.jbusres.2017.02.017

- Pathan, Z. K., Yusof, Y. B., Abas, N. H. B., Adam, A., & Saif, Y. (2021). Factors affecting implementation of ISO 9001: 2015 in manufacturing sector. Psychology and Education, 58(2), 883–888.

- Petrenko, O. V., Aime, F., Ridge, J., & Hill, A. (2016). Corporate social responsibility or CEO narcissism? CSR motivations and organizational performance. Strategic Management Journal, 37(2), 262–279. https://doi.org/10.1002/smj.2348

- Platonova, E., Asutay, M., Dixon, R., & Mohammad, S. (2018). The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. Journal of Business Ethics, 151(2), 451–471. https://doi.org/10.1007/s10551-016-3229-0

- Ramaditya, M. (2019, February). Examining the impact of corporate social responsibility towards employee engagement (A case study: Telekom Malaysia Berhad in Kedah) [paper presentation]. 5th Annual International Conference on Management Research (AICMaR 2018) (pp. 126–133). Atlantis Press.

- Ramayah, T. J. F. H., Cheah, J., Chuah, F., Ting, H., & Memon, M. A. (2018). Partial least squares structural equation modeling (PLS-SEM) using smartPLS 3.0. An Updated Guide and Practical Guide to Statistical Analysis .

- Rao, K., & Tilt, C. (2016). Board composition and corporate social responsibility: The role of diversity, gender, strategy and decision making. Journal of Business Ethics, 138(2), 327–347. https://doi.org/10.1007/s10551-015-2613-5

- Raza, A., Saeed, A., Iqbal, M. K., Saeed, U., Sadiq, I., & Faraz, N. A. (2020). Linking corporate social responsibility to customer loyalty through co-creation and customer company identification: Exploring sequential mediation mechanism. Sustainability, 12(6), 2525. https://doi.org/10.3390/su12062525

- Rich, B. L., Lepine, J. A., & Crawford, E. R. (2010). Job engagement: Antecedents and effects on job performance. Academy of Management Journal, 53(3), 617–635. https://doi.org/10.5465/amj.2010.51468988