Abstract

Corporate Governance (CG) reporting receives increasing attention. This study examines the impact of voluntary CG statement assurance on financial analysts’ and bankers’ decisions. An experiment with a 2 × 2 + 1 between-subject design was conducted. The independent variables comprise the assurance provider (Big Four statutory auditor vs. another Big Four audit firm) and assurance level (limited vs. reasonable). Additionally, a control condition without assurance provision is used. The participants’ reliance on the CG statement, their likelihood to recommend an investment in shares of the fictitious company, their credit risk assessment, and the likelihood to purchase shares of the fictitious company themselves served as dependent variables. Our results indicate that CG statement assurance increases the likelihood for investment recommendation. Moreover, they do not indicate a significant impact of the type of assurance provider. Reasonable assurance predominantly results in decisions of financial professionals which are more favorable for the fictitious company than limited assurance.

1. Introduction

This study examines the impact of voluntary assurance on corporate governance statements on the decision-making behavior of financial professionals. It investigates to what extent the assurance provision itself, the type of assurance provider, and the level of the assurance impact the perceptions and decisions of informed users, such as financial analysts, corporate banking advisors, and private banking advisors.

Corporate governance (CG) is the set of mechanisms through which companies are directed and controlled and by which they are held accountable to their shareholders (Cadbury, Citation1992; Shleifer & Vishny, Citation1997; Sternberg, Citation2004). It involves a set of relationships between a company’s management, its boards, and its stakeholders. It provides the structure through which the company’s objectives are set and determines the means of attaining them and monitoring performance (OECD, Citation2015). Corporate governance provides oversight and accountability mechanisms to ensure that the company is managed effectively and ethically, which protects the interests of capital providers (Gill, Citation2008). CG management is gaining importance in the increasingly complex and fast-paced business world and deficient CG can have far-reaching consequences for both companies and shareholders (HKCGI et al., Citation2022). A prominent example is the recent diesel emission scandal, which triggered a severe crisis in the global automotive industry (Bouzzine & Lueg, Citation2020).Footnote1 Good corporate governance is relevant to a firm’s shareholders (Shank et al., Citation2013), potentially impacting their financial decisions. Hence, there is a demand for related reports.

A principal-agent relationship exists between a company’s management and its shareholders (Jensen & Meckling, Citation1976), i.e. the management has better information on corporate governance. This agency problem could be reduced by CG reporting. Furthermore, shareholders cannot demarcate companies with a high-quality CG, and companies could disclose related information as a signal to market (Spence, Citation1973). Disclosing corporate governance practices enables managers to discharge their accountability to their shareholders (Ling Wei et al., Citation2008). CG reporting provides a clear and concise picture of a company’s corporate governance framework, enhancing transparency and building shareholder confidence (Cheung & Tsui, Citation2010).

In 2006, the European Union introduced mandatory CG statements for listed companies (Directive Citation2006/Citation46/EU, Citation2006). They should provide shareholders with easily accessible essential information about the CG practices applied. Germany implemented the EU Directive in 2009 by adding § 289a (now § 289f) to the Handelsgesetzbuch (HGB) (German Commercial Code). CG statements became part of the management report. In terms of content, the CG statement comprises the following components: (i) the declaration of conformity with the German Corporate Governance Code according to § 161 Aktiengesetz (AktG) (Stock Corporation Act); (ii) details on applied CG practices that go beyond legal requirements, such as ethical standards, labor standards, social standards, and guidelines on compliance or sustainability; and (iii) a description of the working methods of the management board and the supervisory board, and the composition and working methods of their committees. In the following years, the CG statement was continuously extended by European and German legislators, and in 2015, the Act on the Equal Participation of Women and Men in Leadership Positions supplemented the CG statement with a description of diversity enhancements. Then, with the CSR Directive (Directive Citation2014/Citation95/EU, Citation2014) and its implementation into German law in 2016, German listed corporations were required to describe the diversity concept concerning the composition of the board of management and the supervisory board. Finally, in conjunction with implementing the Second Shareholder Rights Directive (Directive Citation2017/Citation828/EU, Citation2017) in 2020, the CG statement must include a reference to the compensation report.

The management prepares the CG statement, and providers of capital cannot determine whether the statement is correct. This hidden action problem implies a moral hazard (Arrow, Citation1985); that is, management can use its information advantage to maximize its benefit instead of shareholder benefit by misstatements. Assurance by an external assurance provider could reduce this risk and increase the credibility of the CG statement (Antle, Citation1982). However, in contrast to most components of the management report, the CG statement is not covered by the annual statutory audit. The auditor must check whether the CG statement is provided and published but not audit its content. Nevertheless, auditing standards require the auditor to critically read other information included in a company’s annual report, such as the CG statement, and to check whether there is material inconsistency between other information and the financial statements or the auditor’s knowledge obtained in the audit (ISA 720 (rev.); IAASB, Citation2015). Companies may voluntarily engage in an assurance provider regarding the CG statement. Thus, two research questions may be of interest: (i) Is the assurance on CG statements beneficial to external users? (ii) How should such an assurance be designed?

Against this backdrop, we investigate the effect of voluntary CG statement assurance on financial professionals’ decision making. Moreover, we analyze whether the assurance impact differs according to the type of assurance provider (statutory auditor (SA) vs. another Big 4 audit firm (AA)) and level of assurance (limited (LA) vs. reasonable assurance (RA)). In doing so, we performed an experiment with a 2 × 2 + 1 between-subject design based on two treatment variables (assurance provider and assurance level) and a control condition without assurance provision. As study participants, we focus on financial professionals, i.e. financial analysts and bankers, because they have a high level of experience and decision-making power in the valuation and analysis of companies. The dependent variables are reliance on the CG statement of a fictitious company, the likelihood of giving an investment recommendation regarding the shares of this company, the perceived level of the company’s credit risk, and the likelihood of privately investing in shares of the fictitious company.

We hypothesize and find that voluntary assurance of the CG statement positively impacts financial professionals’ likelihood of advising clients to invest in the respective company. For the other dependent variables, our results also indicate that assurance results in more favorable decisions for the company. However, the mean differences were not statistically significant. Regarding the assurance provider, we mainly do not identify significant differences between the assurance provision by the statutory auditor and another Big 4 audit firm. This may be explained by opposing effects. On one hand, the incumbent auditor knows the client, which may result in knowledge spillovers and positively impact audit quality. On the other hand, the provision of additional services increases financial interest and may threaten the auditor’s independence, with adverse effects on audit quality. However, we observe a significant interaction between the two treatment variables for ADVICE and CREDIT, indicating that financial professionals may prefer assurance provision by another Big 4 audit firm in the case of reasonable assurance. Concerning assurance level, our results show a clear preference for reasonable assurance.

Prior research examined the effects of assurance on ESG, CSR, or sustainability reports (Hay et al., Citation2021). However, the granularity of such studies is low; that is, an impact of ESG assurance could be caused, for example, by a high relevance of assurance on environmental issues and a lack of significance of assurance on corporate governance components of the report. Our study addresses this research gap by investigating the effects of voluntary assurance on CG statements (Seguí-Mas et al., Citation2018), thereby contributing to research on the benefits of assurance on non-financial information. European research (Sierra García et al., Citation2022) regarding assurance on non-financial reporting is still scarce, and findings from the Anglo-American setting (Clarkson et al., Citation2019) are not directly transferable to the Continental European context. In addition, we complement existing research on alternative assurance providers by comparing the assurance provided by the statutory auditor with that provided by another audit firm. Prior research has typically investigated the effects of alternative assurance providers outside the accounting profession (Hay et al., Citation2021). The research findings on the relevance of different assurance levels are mixed. We contribute to this research by revealing that assurance level influences users’ preferences for a specific assurance provider. A further strength of this study is that real-world subjects participated in the experiment instead of proxying business students. Our results excite regulators who consider making assurance on CG statements mandatory. The findings also interest the demand and supply side of voluntary assurance services because they show that such services might benefit reporting companies. Finally, based on our results, users of such reports could strengthen related demands towards reporting entities for demanding assurance on them.

The remainder of the study is structured as follows. Section 2 provides an overview of the theoretical background and prior research and develops the hypotheses. Section 3 describes the research method, including details of the experimental case, dependent and independent variables, and information about the participants. The following section presents and discusses the empirical results. The final section concludes the study’s main findings, provides information on related implications, reveals the study’s limitations, and offers avenues for future research.

2. Background, prior research, and hypothesis development

2.1. Corporate governance reporting

There is no clear definition of the term corporate governance. One widely used definition describes CG as ‘the system by which companies are directed and controlled’ (Cadbury, Citation1992). Multifaceted CG research has led to further additions to this definition. CG definitions can be assigned to behavioral or normative research frameworks. The normative category deals with the formal and informal rules under which a company operates, such as the legal system, financial markets, and factor markets. The behavioral category deals with the actual behavior of corporations in terms of performance, efficiency, growth, financial structure, and relationships between the different stakeholders inside and outside the company. The distinction between these two streams helps insofar as different purposes of CG reporting can be derived. The normative framework includes a formalized description of CG along the legal system and informal claims of various stakeholders. The behavioral framework includes a structured summary and formalization of the relevant relationships and management within the company (Claessens, Citation2006).

Referring to the normative view, the legal context of CG, both EU and German law, must be considered. In recent years, a major change in CG reporting requirements has emerged at the EU level and continues to expand. Based on the globally agreed UN Sustainable Development Goals (Independent Group of Scientists appointed by the Secretary-General, Citation2023) and the Paris Agreement (Paris Agreement to the United Nations Framework Convention on Climate Change, Citation2016), the EU is pushing for fundamental changes in reporting requirements on CG topics with initiatives currently in development, such as the EU Taxonomy Regulation (Regulation (EU) Citation2020/Citation852, Citation2020), Non-Financial Reporting Directive (Directive Citation2014/Citation95/EU, Citation2014), and the Corporate Sustainability Reporting Directive (Directive (EU) Citation2022/Citation2464, Citation2022). Together, these initiatives have pushed for an extensive transformation of non-financial reporting, including CG reporting. Martínez-Ferrero and García-Sánchez (Citation2017) find evidence that these regulatory pressures explain large portions of the rising demand for voluntary assurance.

In this study’s context, the currently applicable legal framework regarding CG statements for German companies is the German Handelsgesetzbuch, which corresponds to current EU law. Under HGB §§ 289f, 315d, listed companies are required to issue a summarized CG statement [Erklärung zur Unternehmensführung]:

The statement includes the declaration of conformity according to § 161 AktG, i.e. it states whether the recommendations of the German Corporate Governance Code are complied with, and which recommendations have not been or are not being applied and why not (comply or explain approach). Moreover, it includes information on significant CG practices and the supervisory and management board’s working methods and composition. Finally, companies need to disclose the diversity concept yearly for the supervisory board and management board, and the statutory requirements for the equal participation of women and men in management positions.

The statement must be published (i) in full as a separate section in the management report, (ii) as a separate section in the management report with references to publicly available information, or (iii) in full on the company’s website for at least ten years.

The statutory auditor of the financial statements must control whether a CG statement has been made and whether the required disclosures have been made in this statement. Therefore, only the completeness of the information, but not its correctness in terms of content, must be audited (§ 317,2 HGB).

If the CG statement is missing in its entirety or if significant parts of its content are missing, then there will be a violation of the completeness of the management report, which generally results in qualification of the audit opinion.

The overarching purpose of the CG statement is to improve CG in EU member states through increased transparency and EU-wide harmonization (Camilleri, Citation2015).

Turning to the second, behavioral-focused view, there have been only a few studies on CG reporting in settings comparable to this examination. However, CSR reporting, a prominent type of non-financial reporting, has been more intensively researched, and corporate governance is often considered an element of CSR. To date, the external and voluntary assurance of non-financial reporting remains a comparatively underrepresented area of investigation (Ballou et al., Citation2018; Fatima & Elbanna, Citation2023; Pollman, Citation2019). However, research on CG statement assurance is lacking. In contrast, research on the reasons and drivers of external assurance on CSR reports has attracted considerable attention over the last few decades (Martínez-Ferrero & García-Sánchez, Citation2017; Simnett et al., Citation2009). Peters and Romi (Citation2015) found that CSR-related organizational bodies with higher levels of related expertise are more likely to adopt external assurance. However, a significant research gap exists regarding the impact of external assurance on CG statements on the decisions of the company’s key stakeholder groups. Our study, therefore, aims to close this gap by obtaining evidence on the effects on the stakeholder group of financial professionals, who are of prime importance to most companies.

2.2. Assurance provision

Signaling theory can be used as a rationale for external assurance on CG statements (Schaltegger & Hörisch, Citation2017). It is defined as the deliberate reduction of information asymmetries in a market through the provision of information through a costly signal by one party (Ross, Citation1977; Spence, Citation1973). Disclosing financial and non-financial information, such as sustainability or corporate governance reports, can signal an organization’s attributes (Connelly et al., Citation2011; Lys et al., Citation2015; Mahoney et al., Citation2013). However, the receiver of these signals cannot entirely observe their correctness. Thus, external assurance can be used as a signal to the providers of capital about the reliability, credibility, and transparency of the information disclosed (Braam & Peeters, Citation2018). From a sender’s perspective, the assurance of information can be interpreted as a beneficial signal to emphasize the importance of the provided information (Cheng et al., Citation2015). By demanding assurance on CG statements, companies can send repetitive signals that are positively perceived by various stakeholders (Six et al., Citation2010). From a recipient’s perspective, sending information signals can be voluntary and actively claimed by other stakeholders (Moroney et al., Citation2012). This behavior of sending and receiving signals can create a partnership relationship between stakeholders. However, this assumes that the signals sent and the provided information are highly valued and complete. Otherwise, signals can potentially harm the partnership between a company and its stakeholders (Velte & Stawinoga, Citation2017). The effectiveness of assurance as a signal depends on the assurer’s credibility, the assurance engagement’s scope, and the assurance process’s rigor.

Existing research considers the impact of external assurance on non-financial reports in terms of factors such as firm performance, report quality, credibility, and investor decisions. External assurance may raise and reinforce the sender and recipient’s information levels. Consequently, prior research has shown that the external assurance of non-financial reports reduces information asymmetries between stakeholders (Cuadrado-Ballesteros et al., Citation2017).

Investigating performance, Reimsbach et al. (Citation2018) show that assurance of sustainability information positively affects investors’ evaluation of firm performance and leads to better investment-related judgments. However, these findings might be driven by a selection bias; that is, better-performing companies are, per se, more willing to demand an external assurance service.

Other studies have examined the impact of external assurance on factual and report users’ perceptions of report quality. For example, in a matched pair study of the top 500 publicly listed companies in Australia, Moroney et al. (Citation2012) demonstrate that external assurance on voluntary environmental disclosures increases the report quality. Clarkson et al. (Citation2019) show similar results for a comparable US sample and disclose a positive impact of external assurance on information quality. Based on an international sample, Luo et al. (Citation2023) reveal a positive association between corporate carbon assurance and the quality of carbon disclosure. An archival study based on an international sample of listed companies shows that the sole provision of non-audited information might compromise the desired disclosure effect (Cuadrado-Ballesteros et al., Citation2017). Using data from South African listed firms, Donkor et al. (Citation2021) find a positive association between assurance quality and sustainability reporting quality. The credibility of non-financial reports increases when the quantitative and qualitative components are externally assured (Hodge et al., Citation2009). Likewise, based on a sample of listed firms in Taiwan, Du and Wu (Citation2019) observe that external assurance can enhance the credibility of CSR reports.

Another aspect is the impact of external CG assurance on investors’ willingness to invest. When assured non-financial reports are designed in alignment with the company strategy, in a 2 × 2 between-subjects design using MBA students as proxies for non-professional investors, evidence was found that external investment propensity is higher for assured than for non-assured reports (Cheng et al., Citation2015; Shen et al., Citation2017). Analyzing data from an international sample, García-Sánchez et al. (Citation2019) reveal that external assurance on CSR reports strengthens access to financial assets. Gerwanski et al. (Citation2019) show by using a sample of 1408 firm-year observations of European and South African firms that the deliberate neglection of external assurance on non-financial information may even trigger a negative investment signal among shareholders.

Signaling theory emphasizes the potentially positive effects of sending signals like assurance on CG statements to providers of capital, which may reduce agency problems. Prior research has shown that the assurance of non-financial information results in shareholder decisions that are more favorable to the reporting firm. Thus, based on theoretical considerations and previous research findings, we formulate our first hypothesis as follows:

H1: Assurance on CG statements positively impacts financial professionals’ decisions.

2.3. Type of assurance provider

The statutory auditor, another audit firm, or an alternative assurance provider could provide assurance on corporate governance statements. There are information asymmetries between the assurance provider and the shareholders regarding the attributes of the assurance provider. Different providers may differ in their characteristics, and such hidden characteristics (Rothschild & Stiglitz, Citation1978; Spremann, Citation1987) could result in an adverse selection problem (Akerlof, Citation1978). Some assurance provider characteristics can be revealed through screening (Stiglitz, Citation1975). Providers of capital could assess the pros and cons of assurance provision by the financial statement auditor or another audit firm to assess the credibility of their services based on presumed characteristics. The effectiveness of signaling depends on the credibility of the assurance provider; that is, the higher the perceived assurance quality, the stronger the signaling effect.

The quality of the assurance service impacts credibility and depends on the assuror’s ability to detect misstatements (competence) and his/her willingness to report revealed misstatements (independence) (DeAngelo, Citation1981). The type of assurance provider may have opposing effects on the perceived quality of the assurance service. Engaging the incumbent financial statement auditor may result in knowledge spillover (Arruñada, Citation1999). The financial statement auditor has a deep and broad insight into the company’s systems and structures and an enhanced understanding of the company, including its business model, business strategies, and objectives (Eilifsen et al., Citation2001; ISA Citation260 (rev.), Citation2016, ISA Citation315 (rev.), Citation2019; Lu et al., Citation2023). Furthermore, when assessing the risks of material misstatement, the financial statement auditor obtains an understanding of the entity’s governance (ISA 315 (rev.).19) and of its system of internal control (ISA 315 (rev.).21–27), including the proper application of policies. Apart from that, the financial statement auditor already knows the client’s management, helping him to assess the correctness of the corporate governance statement. This information might be useful for assuring CG statements, and could contribute to higher assurance quality and/or lower assurance costs. Beyond that, the CG statement is integrated into the management report. Assurance provision by the statutory auditor could help to ensure the connectivity between, and the consistency of, financial and corporate governance information (Directive Citation2022/Citation2464/EU). Thus, the choice of the financial statement auditor may appear more salient to users and demonstrate consistency and integrated thinking (Lu et al., Citation2023). Additionally, applying similar methodologies and procedures could result in economies of scale. Clients reduce transaction costs when engaging with the financial statement auditor and can negotiate discounts for bundled services (Lu et al., Citation2023).

However, the engagement of the financial statement auditor may threaten the factual and perceived independence of the assurance provider. The provision of assurance on CG statements increases the total fees of the auditor generated from one client, and may result in economic bonding. Furthermore, the simultaneous provision of different assurance services intensifies the familiarity between the audit firm and the client. Although the joint provision of audit and other assurance services is less critical than the simultaneous provision of audit and consulting services (Eilifsen et al., Citation2018; Meuwissen & Quick, Citation2019) it may result in negative shareholder perceptions.

Concerning the type of assurance provider, existing research mainly focuses on comparing audit firms and alternative assurance providers such as consultants or engineers (Pflugrath et al., Citation2011). Exceptions are the studies by Lu et al. (Citation2023), who demonstrate that companies with the same assurance provider for financial and non-financial information have less discretionary accruals and higher chances of receiving going concern modifications, indicating higher audit quality, and by Maso et al. (Citation2020) who also observe an increase in audit quality if an audit firm provides both CSR assurance and the financial statement audit. Nevertheless, there is a research gap regarding the potentially different impacts of assurance on non-financial information provided by the statutory auditor of financial statements or another audit firm. This gap is of particular interest, as the recently issued EU Corporate Sustainability Reporting Directive includes a Member States option to allow a statutory auditor or an audit firm other than the one conducting the statutory audit of financial statements to assure sustainability reports (Directive (EU) Citation2022/Citation2464, Citation2022).

The results of a behavioral experiment by Pflugrath et al. (Citation2011) show that financial analysts from Australia, the US, and the UK perceive greater credibility of CSR reports when assured by a professional accountant. In addition, many archival studies have explored the relationship between the type of assurance provider and the (perceived) quality of assurance provided. Assurance provision by professional accountants is often superior, factually and perceived (Peters and Romi using US data (Citation2015); Sierra García et al. (Citation2022) for Spanish listed companies; Casey and Grenier (Citation2015) based on a US sample; Martínez-Ferrero and García-Sánchez (Citation2017); Cuadrado-Ballesteros et al. (Citation2017); Martínez-Ferrero et al. (Citation2018); Carey et al. (Citation2021) all with an international sample). However, some experimental studies Hodge et al. with MBA students from Australia (Citation2009); Shen et al. with non-professional investors from China (Citation2017), and archival studies by Moroney et al. with Australian data (Citation2012); Birkey et al. using a US sample (Citation2016) indicate that the type of assurance provider is irrelevant or that the assurance provided by a public accounting firm is not superior. Hummel et al. (Citation2019) even indicate that assurance providers that are not belonging to the accounting profession are associated with broader assurance statements.

Assurance provision by the statutory auditor is associated with a strong positive effect on auditor competence. There is an opposing effect on auditor independence. However, fees for assurance services on corporate governance statements are much lower than audit fees, and the familiarity threat is reduced due to mandatory audit firm and audit partner rotation. In addition, some prior research indicates the positive effects of assurance provision by the financial statement auditor. Thus, we formulate the following hypothesis:

H2: Assurance provision by the statutory auditor has a greater positive impact on financial professionals’ decisions than assurance provision by another audit firm.

2.4. Level of assurance

Assurance services are credence goods (i.e. essential aspects of the service, including the actual assurance level) that cannot be observed (Causholli & Robert Knechel, Citation2012), and there is a hidden action problem (Arrow, Citation1984; Grossman & Hart, Citation1986; Laffont & Tirole, Citation1993) because the audit effort remains unclear. Consequently, there is a moral hazard risk (Hart & Moore, Citation1990; Jensen & Meckling, Citation1976); that is, the assurance provider could apply less effort than the client and its shareholders assume. Standards and rules that govern the behavior of assurance providers, such as standards on assurance levels, can mitigate the hidden action problem (Jensen, Citation1986).

An assurance on CG statements intends to increase their credibility and to signal commitment to good corporate governance to a firm’s shareholders. This credibility depends on the assurance providers’ stated confidence in their opinion, i.e. the level of assurance. It is the extent to which the assurer feels that the information given in a report is correct and, in turn, reflects how much trust users should place in the content of a report (Ackers & Eccles, Citation2015).

International and national audit frameworks regulating assurance engagements refer to different assurance levels that are most frequently reasonable and limited. (ISAE 3000 (rev.); IAASB, 2013) and ISAE 3410 (rev.); IAASB, Citation2012, dealing with assurance engagements other than audits or reviews of historical financial information and greenhouse gas statements, respectively, as well as the proposed International Standard on Sustainability Assurance 5000 (ED ISSA 5000, Citation2023), differ between reasonable and limited assurance (ISAE 3410.6 (rev.), Citation2012, ISAE 3000.12 (rev.), Citation2013). The level of assurance obtained in a limited assurance engagement is lower than in a reasonable assurance engagement (ED ISSA 5000.7). In a reasonable assurance engagement, the auditor reduces engagement risk to an acceptably low level. In contrast, in a limited assurance engagement, the auditor reduces engagement risk to an acceptable level, where the risk is greater than for reasonable assurance. The nature, timing, and extent of procedures performed in a limited assurance engagement are limited compared with those necessary in a reasonable assurance engagement, but are planned to obtain a level of assurance that is meaningful in the auditor’s professional judgment (ISAE 3000.12 (rev.), Citation2013). In a limited assurance engagement, the assuror identifies disclosures where material misstatements are likely to arise. In contrast, in a reasonable assurance engagement, the assuror identifies and assesses the risks of material misstatements of the disclosures at the assertion level (ED ISSA 5000.17, Citation2023).

In a reasonable assurance engagement, the assurance provider must acquire a more comprehensive understanding of the entity’s relevant internal control system and perform more extensive analytical and substantive procedures (ED ISSA 5000.102, .107, .109, Citation2023). Only in a reasonable assurance engagement, such procedures must be applied at the assertion level. The procedures for estimating or forward-looking information are more detailed in the case of reasonable assurance (ED ISSA 5000.134). Reasonable assurance is expressed in a positive form (e.g. ‘ … the CG statement is prepared, in all material aspects, in accordance with the legal provisions’). In contrast, limited assurance, on the other hand, encompasses a conclusion in a negative form (e.g. ‘ … no matters have come to the attention of the assurance provider that causes her or him to believe that the CG statement is not prepared, in all material aspects, in accordance with the legal provisions’) (ISAE(rev.) 3000.72, Citation2013).

It is possible that financial professionals do not understand the different assurance levels, perceive limited assurance as sufficient, or doubt that audit firms have the necessary competence and capacity to provide reasonable assurance. Research on assurance levels is limited; however, prior studies demonstrate that report addressees principally notice and understand the qualitative difference between the assurance levels (Hasan et al., Citation2003; Schelluch & Gay, Citation2006). In a study of sustainability reports of the world’s largest listed firms, Cuadrado-Ballesteros et al. (Citation2017) show that analysts’ forecasts are more accurate when based on reports with reasonable assurance than those with limited assurance. From a European sample, Fuhrmann et al. (Citation2017) find that sustainability reports with high assurance levels are significantly and negatively related to the bid/ask spread, but other reports do not. Quick and Inwinkl (Citation2020) experimentally show that German bankers make more favorable decisions toward the reporting company when CSR reports are assured. This effect is stronger when the assurance level is reasonable rather than limited. The higher the assurance level, the higher the likelihood that financial analysts recommend buying shares (Rivière-Giordano et al., Citation2018), the higher the firm value (Hoang & Trotman, Citation2021), the higher the credibility of reports (Hodge et al., Citation2009), and the higher the attractiveness of shares (Sheldon & Jenkins, Citation2020). Conversely, Hodge et al. (Citation2009) does not identify a correlation between assurance levels and the perceived reliability of environmental and social information. Other studies reveals that users often do not understand different assurance levels (Hasan et al., Citation2003; Low & Boo, Citation2012; Roebuck et al., Citation2000; Schelluch & Gay, Citation2006).

We postulate that financial professionals are knowledgeable parties and, therefore, change their judgments by assurance level, presuming that they are especially aware of the differences between various assurance levels. Since reasonable assurance is more substantial than limited assurance, it should provide the CG statement with greater credibility. Further, there is more support in the research on the positive impact of reasonable assurance. As a result, we post hypothesis 3 as follows:

H3: Reasonable assurance on CG statement has a greater positive impact on financial professionals’ decisions than limited assurance.

3. Research method

3.1. Experimental design

3.1.1. Case materials and procedures

We opted for a vignette experiment (Rossi, Citation1979; Rossi & Berk, Citation1985) as the most suitable research method. It allows us to present participants with hypothetical scenarios and to manipulate the independent variables systemically, enabling us to control the content (Rungtusanatham et al., Citation2011). We manipulated the assurance provision, the assurance provider, and the assurance level. Our experimental case versions, i.e. the vignettes, are designed to resemble real-life situations, enhancing the validity of our findings. However, they still lack the richness and complexity of reality, constraining the generalizability of findings to real-world situations (Goudriaan & Nieuwbeerta, Citation2007). Compared to direct questions, participants may feel more comfortable providing honest responses to hypothetical scenarios. Thus, the method may help reduce the likelihood of a social desirability bias (Walzenbach, Citation2019). Given that our participants are financial professionals, a subject group challenging to attract for participation, it was, however, impossible to make use of an advantage commonly associated with vignette experiments, namely having all participants participate in the experiment at the same time of the same day.

We utilized a 2 × 2 + 1 between-subjects design to test the hypotheses. The two treatment variables are the assurance level and assurance provider; both are manipulated at two levels. Assurance Level (ALEVEL) is manipulated at (i) a limited assurance level and (ii) a reasonable assurance level. The assurance provider (APROVIDER) is manipulated at (i) the assurance provider corresponds to the audit firm, which also performs audits of the financial statements, and (ii) the assurance provider is another audit firm. Additionally, a control condition was applied, where no assurance of the CG statement was provided.

To ensure a high level of transparency and compliance with the ethical standards of science, the experimental materials were prepared following the ethical guidelines of the authors’ university and were reviewed and approved by its ethical board. The experiment was conducted online via the ‘SoSciSurvey’ platform.

The experimental case described a fictitious automobile manufacturer, Automobil AG, based in Frankfurt am Main, Germany. To ensure a realistic setting, the financial data of a leading automotive manufacturer were multiplied by a factor of 0.4. The participants were first informed about the company’s production sites, product portfolio, main sales markets, sales figures, number of employees, listing on the Frankfurt Stock Exchange, and key financial indicators, such as EBIT, cash flow, and EPS in a 2-year comparison. Furthermore, information was provided on the aspects of CG at Automobil AG, such as the composition of the management and supervisory board, their members’ compensation, and their qualifications.

Further, the experimental case included information about ‘Automobil AG’s annual audit. A Big Four audit firm performed the audit and issued an unqualified audit opinion. Participants were informed about the appointment of the auditor, absence of any disagreements between management and the auditor, audit fees, and non-audit fees.

Next, the experimental case included an aggregated description of the Corporate Governance Statement of ‘Automobil AG’. It includes a reference to the relevant paragraphs of the German Handelsgesetzbuch (§ 289f, 315d HGB), a declaration of conformity with the German Corporate Governance Code, disclosure of effective CG practices and working methods, information on the composition of the supervisory board and executive board including disclosures on the CG of the company, its diversity concept for its boards, and the legal requirements for the equal participation of women and men in management positions.

The information on the treatment variables followed. After the presentation of the experimental case, we asked participants to answer case-related questions assuming their role as a financial professional, including manipulation checks (MC), and to provide demographic information in a post-experimental questionnaire.

Audit opinions were listed according to limited vs. reasonable assurance and statutory auditor vs. another auditing firm. The audit opinion was prepared based on an established standard industry template from a Big Four audit firm following (ISAE 3000 (rev.); IAASB, 2013).

The wording of the limited assurance opinion is:

[…] Based on the audit procedures performed and the audit evidence obtained, nothing has come to our attention that causes us to believe that the corporate governance statement of Automobil AG for the period January 1, 2020–December 31, 2020, is not prepared, in all material respects, was not determined factually and arithmetically and that the requirements and conditions have not been met in all material respects.

[…] In our opinion, the corporate governance statement of Automobil AG for the period January 1, 2020–December 31, 2020, has been properly compiled in all material respects, and the requirements and conditions have been complied with in all material respects.

Before starting the experiment, seven pilot tests were conducted with representative participants, such as certified financial analysts and bankers, to verify the comprehensibility, plausibility, and terminology. These pilot tests led to marginal verbal and technical changes.

The experimental case was made available to the participants in German and English.Footnote2

3.1.2. Dependent variables

It is of interest whether assurance on CG statements impacts the decisions of financial professionals. Consequently, participants were asked the following questions, which relate to the four dependent variables of this study:

To what extent do you rely on the corporate governance statement of ‘Automobil AG’? (RELY),

With what probability would you make an investment recommendation for ‘Automobil AG’? (ADVICE),

How would you assess the credit risk at ‘Automobil AG’? (CREDIT),

How likely would you invest in ‘Automobil AG’ shares yourself? (INVEST).

Hence, the first dependent variable refers to the participants’ reliance on the company’s CG statement (RELY) to measure whether and to what extent voluntary assurance may impact the statement’s perceived reliability. Second, participants are asked about the probability of making an investment recommendation for the fictitious company (ADVICE), aiming to measure whether and to what extent voluntary assurance impacts their decision-making behavior as financial professionals in their distribution and management of debt capital. Third, participants were asked about their perceived credit risk assessment (CREDIT) to test whether and to what extent voluntary assurance of the CG statement impacts the company’s sensed creditworthiness. Finally, financial professionals were asked about the likelihood of personally investing in the company’s shares (INVEST) to measure whether and to what extent voluntary assurance can impact personal risk behavior associated with using personal capital. All dependent variables were measured on a 7-point Likert scale.

3.1.3. Independent variables

Based on the study’s 2 × 2 + 1 design, a binary manipulation per treatment variable was used in addition to the control group, in which no assurance of the CG statement was reported. The first treatment variable refers to the assurance provider (APROVIDER), and is manipulated at two levels: the statutory auditor (SA) and another auditor (AA). In the additional engagement to assure the CG statement, the auditor may assume specific knowledge about the company from the annual report audit. On the other hand, assurance by another auditing firm may radiate higher independence from the annual audit because of the absence of this implicit knowledge.

The second independent variable is the level of assurance provided (ALEVEL), which is also manipulated at two levels: limited assurance (LA) and reasonable assurance (RA). Both assurance reports and their corresponding assurance levels are based on established templates of a Big Four auditing firm. They are also practiced in this form in real-world reports in use for testing, according to (ISAE 3000 (rev.); IAASB, 2013).

In the case versions where the statutory auditor additionally assured the CG statement, the participants were informed about the related fees (49,500 € in case of limited assurance and 89,500 € in case of reasonable assurance). To ensure a realistic amount of fees, we consulted several partners of a Big Four audit firm that regularly perform voluntary assurance services of CG statements. Furthermore, a control condition was applied, in which no assurance on the CG statement was reported.

Thus, the study’s design resulted in five experimental conditions. shows an overview of the different experimental conditions, their independent variables, and the number of participants per cell.

Table 1. Overview of the five experimental conditions and number of participants per cell.

3.2. Participants

For our study, we resort to participants who belong to the group of financial professionals. This comprises participants with established certifications in the financial industry (CFA or similar) or comparatively great professional experience in banks and the financial analysis of companies. We do this deliberately because in this strand of research, the use of (undergraduate) business students is a widespread practice. While the acquisition of students seems to be comparatively more effortless in the university context, the suitability of this group as a proxy for the evaluation of financial contexts is controversial. Considering the task’s complexity compared to the students’ experience level, Elliott et al. (Citation2007) find empirical evidence for the usability of MBA students as proxies. In the context of assurance services, Low and Boo (Citation2012) argue that the basic knowledge of accounting is given because of the students’ curriculum. However, and in particular, for reasons of external validity, it remains an open question whether conclusions can be drawn with this group as a proxy for financial experts.

Therefore, this study focuses on financial professionals as participants. We define financial professionals as a highly knowledgeable group through their profession, related theoretical education, and practical experience. Financial professionals play a key role as information mediators between capital markets, investors, and the concerned companies. Based on their professional training and experience, they have assumed credibility in analyzing and evaluating company-specific information, such as financial and non-financial reports. Hence, their assessment of a company’s reporting system and derived decision-making behavior can have a direct influence on any recommendations for action for investors. Specifically, we subsume three different professional groups under the term financial professionals: (i) financial analysts, (ii) corporate banking advisors, and (iii) private banking advisors.

The first group consists of financial analysts with a highly reputable professional certification (e.g. CFA, CIIA, or comparable). Owing to these professional qualifications, this group is particularly suitable for evaluating CG statements (Manetti & Toccafondi, Citation2012; van Duuren et al., Citation2016). Additionally, financial analysts investigate financial data and use the results to provide informed guidance to companies or individuals in business investment decisions. Thus, their decision-making behavior is highly relevant to companies.

The second group comprises corporate banking advisors. They typically offer loans and credit products to business customers and treasury services, cash management, trade finance services, or asset management.

The third group encompasses private banking advisors, who primarily serve banks’ private customers.

Common features of all three groups are a high degree of financial and analytical expertise, regular execution of evaluation and decision-making regarding capital flows, and a highly responsible intermediary function between capital providers and capital recipients.

Data were collected from November 17, 2021, to July 12, 2022. For participant selection, we conducted the following process:

First, the graduate databases of the CFA (Chartered Financial Analyst) Institute and DVFA (Deutsche Vereinigung für Finanzanalyse und Asset Management) [German Association for Financial Analysis and Asset Management] were examined for officially accredited graduates and their respective contact data. The accreditations of the CFA Institute, especially in the Anglo-American region, and the DVFA, especially in the DACH region, are internationally recognized and highly respected qualifications in the global financial industry. Second, individuals holding one of these accreditations were contacted directly via the professional network LinkedIn. Third, contact information for bankers with analyst roles was collected through Internet research by researching the publicly available investor relations websites of investment funds, publicly listed companies, and corporate websites. These three steps resulted in 4,250 contact data from financial professionals.Footnote3

Six weeks after the financial professionals were asked to participate, we sent individual reminders. This resulted in 157 usable responses before the manipulation checks and an estimated response rate of 3.7%.Footnote4

Based on the assumption that late respondents indicate the perceptions of non-respondents (Armstrong & Overton, Citation1977), we checked for a potential non-response bias by comparing early and late responses using t-tests. The results do not indicate significant differences, which makes a non-response bias unlikely. We also applied t-tests and compared responses with a low completion time with responses with a high completion time (Li et al., Citation2018). Again, the results do not reveal significant differences, suggesting that the non-response bias is not a major concern in our sample. Moreover, informal talks with bank directors gave us reason to believe that the demographic data of our sample are representative of financial professionals.

The experimental questionnaire included three control questions to check whether participants had read and understood the case correctly. The first manipulation check (‘Was the corporate governance statement assured? ’ – ‘yes’ or ‘no’) was applied to all experimental conditions. Incorrect answers led to the exclusion of 55 cases. The second manipulation check asked which audit firm had carried out the assurance of the CG statement (‘Who has assured the corporate governance statement of “Automobil AG”?’ – ‘ABCD’ or ‘XYZ’). Again, incorrect answers led to the exclusion of 9 cases. The third manipulation check deals with the assurance level of the assurance service in the CG statement (‘How do you assess the assurance level’ on a 7-point Likert scale from 1 = very low to 7 = very high). Comparing the mean answers of the participants with reasonable assurance case versions (4.286) with the mean answers of the participants with limited assurance case versions (2.616) shows a significant difference (t-value = −4.346; p-value < 0.001). It indicates that the majority of our participants understand the differences between assurance levels. However, the results are weak without eliminating potential failures regarding the third manipulation check. Thus, for the experimental conditions in which reasonable assurance was provided, responses in the low range of the 7-point Likert scale (1 = very low to 3), and for the experimental conditions with a limited assurance level, responses in the high range (5 to 7 = very high) were eliminated. Incorrect answers led to exclusion of other 27 cases. This resulted in 66 usable responses after manipulation checks.Footnote5

The combined failure rate for the three manipulation checks (57.9%) is relatively high. However, such failure rates are not uncommon in experimental research, e.g. Cheng et al. (Citation2015) with 35% in a 2 × 2 design; Brown-Liburd and Zamora (Citation2015) with 46% in a 2 × 2x2 design; Aschauer and Quick (Citation2018) with 57.6% in a 2 × 2x2 design; Quick and Sayar (Citation2021) with 34% in a 2 × 2 design; Hoang and Trotman (Citation2021) with 49% in a 2 × 3 design. In addition, our passing rate of about 42% is much better than a random passing rate (0.5 ·0.5 ·0.5; about 16%) ().Footnote6

Table 2. Overview of socio-demographic information of participants.

The mean age of the participants is 3.09, which translates into a range of 40–50 years (AGE; mean = 3.09; median = 3; range 1–5). The average level of education is 3.32, which falls within the range of a bachelor’s degree or comparable diploma (EDU; mean = 3.32; median = 4.00; range 1–5); however, the majority of participants have a master degree. Further, to underline the quality of the sample, 50.8% of participants have a master’s degree or an even higher educational level. Expertise regarding assurance services in general averages 3.88 (KNOW_AS; mean = 3.88; median = 4.00; range 1–7). Expertise in corporate governance has a mean of 3.84 (KNOW_CG; mean = 3.84; median = 4.00; range 1–7). General trust in corporate governance reports averages 3.98 (TRUST_CG; mean = 3.98; median = 4.00; range = 2–7). In comparison, general trust in audit firms is, on average, slightly higher at 4.28 (TRUST_AF; mean = 4.28; median = 4.00; range 2–7). Due to ethical study constraints, the sociodemographic questions were optional, accounting for nine missing responses.

4. Results

shows that the means of the dependent variables regarding the assurance provider vary; for the dependent variables RELY and CREDIT, the means are higher for the assurance provided by another audit firm. For the dependent variables ADVICE and INVEST, the means are higher for the assurance provided by the statutory audit firm. Concerning the assurance level, all means across all dependent variables are higher when reasonable assurance is provided.

Table 3. Means and standard deviations of dependent variables by factor levels.

presents the means and standard deviations of the dependent variables according to the experimental conditions. Across all dependent variables, reasonable assurance provided by another audit firm received the highest mean compared to the statutory audit firm. Furthermore, reasonable assurance provided by the statutory audit firm received the second highest means in most cases. It is striking that the control group does not have the lowest means for the dependent variables CREDIT and INVEST, indicating that limited assurance needs not be beneficial.

Table 4. Means and standard deviations of dependent variables by experimental conditions.

To test our first hypothesis, whether assurance of the CG statement, in general, has an impact on the decisions of financial professionals, we performed t-tests for all four dependent variables by comparing the control group (no assurance) to a pooled sample of the conditions with assurance on the CG statement (experimental conditions 2 to 5).Footnote7 As shown in , the means for the control group are lower for all dependent variables. The differences between the two groups are significant for the dependent variable ADVICE but insignificant for the dependent variables RELY, CREDIT, and INVEST. Regarding our first hypothesis, we can conclude that assurance on CG statements significantly affects financial analysts’ willingness to make an investment recommendation. Hence, we can only partially confirm our first hypothesis. We find no support for variables RELY, CREDIT, and INVEST.

Table 5. Difference in means of dependent variables of control group against other experimental conditions.

Regarding the second and third hypotheses, we first performed a MANOVA. The MANOVA results in provide a general overview of the cumulative impact of the type of assurance provider and the assurance level. The results concerning the assurance provider are insignificant (F-value = 1.41; p-value = 0.244); that is, H2 is not supported. However, the results indicate a significant impact of assurance level on financial professionals’ decisions (F-value = 4.23; p-value = 0.005), supporting H3. In addition, there is a significant interaction between the two treatment variables (F-value = 2.91; p-value = 0.031). The MANOVA provides aggregated results. For deeper insights, we perform ANOVAs.

Table 6. Multivariate analysis of variance (MANOVA) results [Wilks’ Lambda].

informs on the ANOVA results for the dependent variable RELY. The means for assurance provided by another audit firm are higher than those provided by the statutory audit firm (Panel A). However, the difference is insignificant (t-value = −0.838; p-value = 0.406). In contrast, the means for limited assurance are significantly lower than the means for reasonable assurance (t-value = −3.366; p-value = 0.001). The ANOVA results (Panel B) also do not support H2 (F-value = 1.26; p-value = 0.267). Hence, the assurance provider does not have a significant effect. In contrast, the ANOVA results for assurance level (F-value = 11.60; p-value = 0.001) are significant and support H3 in conjunction with the means (Panel A). Reasonable assurance results in a significantly stronger reliance on CG statements than limited assurance. There is no significant interaction between the two treatment variables (F-value = 0.18; p-value = 0.675).

Table 7. Analysis of variance (ANOVA) results for dependent variable RELY.

Panel C shows the post hoc test results. As expected, the provision of reasonable assurance by a statutory audit firm results in significantly stronger (t-value = −2.122; p-value = 0.044) reliance (mean = 5.25) than the provision of limited assurance by the same audit firm (mean = 4.19). Similarly, we find a significant difference (t-value = −2.703; p-value = 0.012) between reasonable assurance (mean = 5.80) and limited assurance (mean = 4.44), both provided by another audit firm. Likewise, there is a significant difference (t-value = −3.264; p-value = 0.003) between the reasonable assurance provided by another audit firm and the limited assurance provided by a statutory audit provider. All other pairwise comparisons are insignificant. In summary, reasonable assurance on the CG statements has a more positive impact on financial professionals’ reliance than limited assurance. Contrarily, a significant effect of the assurance provider is not found.

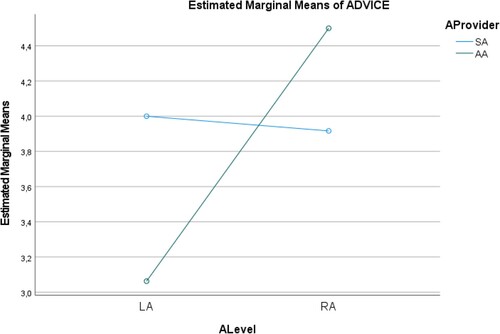

The second dependent variable, ADVICE, refers to the likelihood that financial professionals would issue an investment recommendation for the fictitious company. Univariate tests (, Panel A) do not reveal significant impacts of assurance provider and assurance level. The ANOVA results are presented in Panel B of . We find no support for H2 related to the type of assurance provider (F-value = 0.19; p-value = 0.667) or for H3 related to the assurance level (F-value = 2.74; p-value = 0.104) (, Panel B). However, the interaction between the two treatment variables is significant (F-value = 3.46; p-value = 0.069). Additionally, we performed a contrast test for this dependent variable and compared the provision of limited assurance by another audit firm with the other three conditions (−3, +1, +1, +1). The result is not significant (p-value = 0.107).Footnote8

Table 8. Analysis of variance (ANOVA) results for dependent variable ADVICE.

As shown in and the means in Panel A, reasonable assurance only increases the likelihood of an investment recommendation if provided by another audit firm. Oppositely, limited assurance provided by another audit firm is characterized by an extraordinarily low probability of an investment recommendation. A low assurance level could explain this, in combination with a lack of client-specific knowledge. The post hoc tests (Panel C) reveal a significantly higher recommendation likelihood for reasonable assurance than for limited assurance, both provided by another audit firm (t-value = −2.346; p-value = 0.028). In addition, the limited assurance provided by the statutory auditor results in a significantly higher recommendation likelihood than the limited assurance provided by another audit firm (t-value = 1.925; p-value = 0.064).

Figure 1. ANOVA results for dependent variable ADVICE.

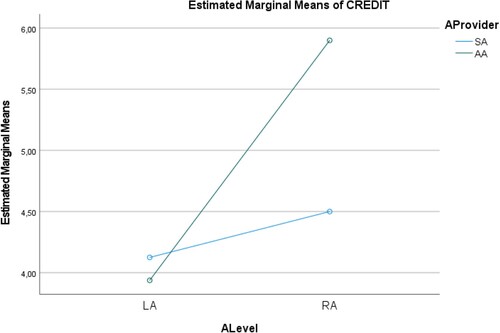

The following dependent variable tested (CREDIT) refers to the assessment of the credit risk of the fictitious company by financial professionals. As shown in Panel A of , the means related to the assurance provider are not significantly different (t-value = −1.030; p-value = 0.308). However, the means for limited assurance are significantly lower than those for reasonable assurance (t-value = −2.943; p-value = 0.005). The ANOVA results are shown in Panel B of . The results for both treatment variables are significant (AProvider: F-value = 2.82; p-value = 0.099; ALevel: F-value = 10.48; p-value = 0.002). In addition, there is a significant interaction between the two treatment variables (F-value = 4.83; p-value = 0.033).

Table 9. Analysis of variance (ANOVA) results for dependent variable CREDIT.

As shown in , the provision of reasonable assurance reduces perceived credit risk. However, this effect is more substantial if another audit firm provides the assurance. The mean values in Panel A confirm this observation. Reasonable assurance results in lower perceived credit risk than limited assurance. Participants prefer the statutory auditor to another audit firm if there is limited assurance (means 4.13 vs. 3.94). However, in the case of reasonable assurance, they assess a lower credit risk if the assurance provider is another audit firm and not the statutory auditor (means 5.90 vs. 4.50).

Figure 2. ANOVA results for dependent variable CREDIT.

The post hoc tests (Panel C) show significant differences between limited and reasonable assurance both provided by another audit firm (t-value = −4.227; p-value = <0.001), between limited assurance provided by the statutory auditor and reasonable assurance provided by another audit firm (t-value = −4.747; p-value = <0.001), and between reasonable assurance provided by the statutory auditor and reasonable assurance provided by another audit firm (t-value = −2.375; p-value = 0.028). Another audit firm has less client-specific knowledge but is potentially more independent. For the limited assurance condition, competence dominates the independence effect, whereas our results indicate that the independence effect is stronger for the reasonable assurance condition. Overall, the findings support H2 and H3.

Our last dependent variable (INVEST) deals with the likelihood that financial professionals will invest their private capital in the fictitious company. Again, t-test results (, Panel A) indicate no significant impact of the assurance provider different (t-value = 0.192; p-value = 0.849) but a significant effect of the assurance level different (t-value = −2.571; p-value = 0.013). The ANOVA results presented in Panel B of indicate that the assurance level significantly affects these investment decisions (F-value = 6.44; p-value = 0.014). By contrast, we find no evidence of a significant influence of the type of assurance provider (F-value = 0.00; p-value = 0.996). The interaction between the two treatment variables was also not significant (F-value = 0.18; p-value = 0.671). Moreover, looking at the means (Panel A), we can see that the means for limited assurance (3.00 and 2.81) are lower than those for reasonable assurance (3.92 and 4.10). Thus, H3 is supported. The post hoc tests in Panel C indicate significant differences between the limited and reasonable assurance provided by another audit firm (t-value = −2.031; p-value = 0.053) and between the limited assurance provided by another audit firm and the reasonable assurance provided by the statutory auditor (t-value = 1.914; p-value = 0.067).

Table 10. Analysis of variance (ANOVA) results for dependent variable INVEST.

In summary, we find some support for H1: external assurance on CG statement positively affects financial professionals’ decisions. In addition, the findings, at best, marginally support the effects regarding the assurance provider. By contrast, financial professionals seem to recognize differences in assurance levels and prefer reasonable assurance over limited assurance. However, we eliminated responses from participants who failed in the third manipulation check. Such failures could either be caused by a lack of attention or by a lack of understanding of assurance levels. Thus, we can only claim that different assurance levels will matter if financial analysts understand the concept of assurance levels.

5. Conclusion

In recent years, corporate governance has attracted significant attention. For example, driving factors are increased stakeholder demands for non-financial management and reporting of companies, scandals such as ‘Dieselgate’ or the legislators, which assign CG a central role in the sustainable development of the economy. In the EU, capital market-oriented entities are obliged to disclose a CG statement. However, the increased relevance of CG and the willingness of companies to strengthen their CG conflicts with the lack of mandatory assurance on CG statements. Further, there are information asymmetries between the management and the addressees of such statements. Therefore, the latter cannot wholly evaluate reporting correctness (hidden action) and management may be tempted to misreport (moral hazard). The lack of generally accepted reporting guidelines exacerbates these risks. The assurance of CG statements could reduce these agency problems.

Against this backdrop, our study focused on three main aspects. First, we examine the decision usefulness of assurance on the CG statement. Second, we analyze the influence of the type of assurance provider, namely, whether the assurance provided by the entity’s statutory auditor or by another Big Four audit firm matters. Third, we investigate the impact of the assurance level, that is, limited or reasonable assurance, on the decision behavior of CG statement users.

Our experimental study used a 2 × 2 + 1 between-subjects design, with financial professionals as participants. The treatment variables were the type of assurance provider and the level of assurance. Additionally, a control group without any assurance on the CG statement was included. Our results indicate that voluntary assurance increases financial professionals’ likelihood of advising to invest in the fictitious company.

Regarding the type of assurance provider, our results mainly fail to identify a significant difference between assurance provision by the Big Four statutory auditor and another Big Four audit firm. Knowledge spillovers may occur in the case of assurance provided by the statutory auditor, which could improve the perceived audit quality. Conversely, additional fees stemming from the assurance service may alleviate concerns about economic dependence and negatively affect audit quality perceptions. These opposing effects could balance each other. However, there is a marginally significant preference for another audit firm concerning the likelihood of credit granting. Reasonable assurance predominantly results in the decisions of financial professionals being more favorable for the fictitious company than limited assurance. Above that, there is a significant interaction between the assurance level and the type of assurance provider for two of our dependent variables: the likelihood of making an investment recommendation and perceived credit risk. Participants seem to prefer assurance provision by another audit firm in conjunction with reasonable assurance.

The results of our study could be of interest to regulators, audit firms, directors, and providers of capital. In light of the current discussions on reforming CG reporting requirements, our results offer essential insights. As part of the recently adopted Corporate Sustainability Reporting Directive (CSRD) (Directive (EU) Citation2022/Citation2464, Citation2022), an assurance requirement, first based on limited assurance, is introduced to improve the reliability of sustainability information. In addition to environmental and social aspects, the CSRD explicitly requires the inclusion of governance-related components. Furthermore, the CSRD includes a Member State options to engage another audit firm than the statutory auditor or even an alternative assurance service provider to express an opinion on sustainability reporting. Our study results slightly support the decision of the European regulator to require CSR assurance. In addition, our findings do not indicate that financial professionals perceive the assurance provision by the statutory auditor as superior. Furthermore, our results confirm the current EU plans to increase the assurance level to a reasonable level in the coming years.

In the same vein, the results also have potential implications for voluntarily reporting companies since our results demonstrate that the demand for assurance may positively affect the reporting company. For audit firms, the identified usefulness of assurance services on CG statements may help market such services. The users of these reports may learn to pay attention to the presence or absence of assurance.

Naturally, our study has limitations. First, we only investigate assurance on CG statements and cannot generalize our findings to assurance on ESG reports. Second, our participants are financial professionals, and other user groups, such as nonprofessional investors, may perceive assurance on CG statements differently. Third, strictly speaking, our findings are only valid for the specifics of our experimental setting. For example, we assume a financially stable company, and the results may differ for financially distressed firms. The automotive industry was chosen because of its economic relevance and shareholders familiarity. However, this industry was affected by the Dieselgate scandal, which may influence the perceptions of assurance on CG statements. Fourth, our study is performed in Germany, a Roman legal country with a two-tier CG-System. Hence, we cannot generalize our findings to companies with different environmental settings. Fifth, the impact of spillover effects on financial statement audits cannot be excluded. For example, the additional fees generated by the provision of CG report assurance services could impair the statutory auditor’s perceived independence, and our participants may have reacted to the reduced credibility of financial statements (Aobdia & Yoon, Citation2023). Sixth, our experiment only considers the potential benefits of CG statement assurance but ignores the related costs. Seventh, we collected data during the COVID-19 pandemic and cannot exclude the possibility that this turbulent period affected our results. Finally, our failure definition regarding the third manipulation check is subjective. However, related sensitivity analyses reveal that our results are relatively stable concerning alternative definitions.

Many of these limitations highlight avenues for future research. For example, future research could analyze the impact of other characteristics of the assurance provider, such as tenure or industry expertise. In addition, it could be of interest to investigate how the new mandatory assurance requirements impact the professional education of public accountants. Further, our study opted for direct questioning over methods like eye-tracking, as our focus is on the financial professionals’ decision-making following information processing. The application of eye-tracking, however, could shed light on the behavioral aspects of information processing (Libby, Citation1981). Finally, with the expanded requirements regarding CSR reporting and related assurance, archival studies on their effects, such as capital markets (earnings response coefficients, abnormal returns, abnormal trading volume, cost of capital, and credit ratings), will become feasible.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 The diesel or exhaust emissions scandal (also known as ‘Dieselgate’) is the term used to describe the combination of a series of primarily illegal manipulations by various car manufacturers to circumvent legally prescribed limits for car exhaust emissions.

2 See the Appendix for the English version of the experimental case.

3 The number of participants can only be estimated due to the acquisition process since the collected and individually contacted email addresses it was called for participation in newsletters of a Financial Analysts Association.

4 We cannot say how many subjects read the DVFA newsletter; therefore it is impossible to calculate a precise response rate.

5 If the unsuccessful participants of this manipulation check are not excluded from the statistical analysis, then the results and significance levels, especially for ‘ALevel’, are significantly weaker. This speaks for the manipulation checks’ effectiveness as these observations are left out for further analysis. We also tested the effects of a stricter or more lenient treatment of the third manipulation check. A stricter treatment increases the significance of our results on the impact of the assurance level for some dependent variables. However, it would have resulted in a loss of a further 13 observations. A more lenient treatment decreases the significance of our results on the impact of the assurance level, which would become insignificant for the dependent variables RELY and ADVICE.

6 AGE includes a 5-point scale with ascending ranks to rank age based on ethical study requirements (1 = under 30 years, 2 = between 30 and 40 years, 3 = between 40 and 50 years, 4 = between 50 and 60 years, 5 = over 60 years). In the same context, EDU includes a 5-point scale to classify educational background (1 = secondary school degree, 2 = high school diploma, 3 = Bachelor’s degree or comparable, 4 = Master’s degree or comparable, 5 = doctoral degree). KNOW_AS and KNOW_CG include the question on general knowledge of audit services and corporate governance, respectively, on a 7-point Likert scale (1 = no knowledge, 7 = very high knowledge). TRUST_CG and TRUST_AF include the question of general trust in corporate governance reports and auditors, respectively, on a 7-point Likert scale (1 = no trust, 7 = very high trust).

7 The use of t-tests is common in research. A t-test by design assumes a normal distribution, which is usually not given for Likert scale data. However, the non-parametric Mann-Whitney-U tests show similar results that both test procedures derive the same results.

8 In a one-tailed interpretation of this contrast test, the p-value is significant. Based on the underlying experimental setting and in combination with the analysis of the overall findings, it can be concluded that the expression AA_LA does not have a stronger influence on decision behavior than all three other comparable expressions.

References

- Ackers, B., & Eccles, N. S. (2015). Mandatory corporate social responsibility assurance practices. Accounting, Auditing & Accountability Journal, 28(4), 515–550. https://doi.org/10.1108/AAAJ-12-2013-1554

- Akerlof, G. A. (1978). The market for “lemons”: Quality uncertainty and the market mechanism. In Uncertainty in economics (pp. 235–251). Elsevier. https://doi.org/10.1016/B978-0-12-214850-7.50022-X

- Antle, R. (1982). The auditor as an economic agent. Journal of Accounting Research, 20(2), 503. https://doi.org/10.2307/2490884

- Aobdia, D., & Yoon, A. (2023). Do auditors understand the implications of ESG issues for their audits? Evidence from financially material negative ESG incidents. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.4549088

- Armstrong, J. S., & Overton, T. S. (1977). Estimating nonresponse bias in mail surveys. Journal of Marketing Research, 14(3), 396–402. https://doi.org/10.1177/002224377701400320

- Arrow, K. J. (1984). The economics of agency. Institute for Mathematical Studies in the Social Sciences, Technical Report (451). https://apps.dtic.mil/sti/pdfs/ADA151436.pdf

- Arrow, K. J. (1985). Informational structure of the firm. American Economic Review, 75(2), 303–307.

- Arruñada, B. (1999). The provision of non-audit services by auditors let the market evolve and decide. International Review of Law and Economics, 19(4), 513–531. https://doi.org/10.1016/S0144-8188(99)00022-8

- Aschauer, E., & Quick, R. (2018). Mandatory audit firm rotation and prohibition of audit firm-provided tax services: Evidence from investment consultants’ perceptions. International Journal of Auditing, 22(2), 131–149. https://doi.org/10.1111/ijau.12109

- Ballou, B., Chen, P.-C., Grenier, J. H., & Heitger, D. L. (2018). Corporate social responsibility assurance and reporting quality: Evidence from restatements. Journal of Accounting and Public Policy, 37(2), 167–188. https://doi.org/10.1016/j.jaccpubpol.2018.02.001

- Birkey, R. N., Michelon, G., Patten, D. M., & Sankara, J. (2016). Does assurance on CSR reporting enhance environmental reputation? An examination in the U.S. context. Accounting Forum, 40(3), 143–152. https://doi.org/10.1016/j.accfor.2016.07.001

- Bouzzine, Y. D., & Lueg, R. (2020). The contagion effect of environmental violations: The case of Dieselgate in Germany. Business Strategy and the Environment, 29(8), 3187–3202. https://doi.org/10.1002/bse.2566

- Braam, G., & Peeters, R. (2018). Corporate sustainability performance and assurance on sustainability reports: Diffusion of accounting practices in the realm of sustainable development. Corporate Social Responsibility and Environmental Management, 25(2), 164–181. https://doi.org/10.1002/csr.1447

- Brown-Liburd, H., & Zamora, V. L. (2015). The role of corporate social responsibility (CSR) assurance in investors’ judgments when managerial pay is explicitly tied to CSR performance. Auditing: A Journal of Practice & Theory, 34(1), 75–96. https://doi.org/10.2308/ajpt-50813

- Cadbury, A. (1992). The financial aspects of corporate governance. London: The Committee on the Financial Aspects of Corporate Governance and Gee and Co. Ltd, 1(3). https://www.ecgi.global/sites/default/files/codes/documents/cadbury.pdf

- Camilleri, M. A. (2015). Environmental, social and governance disclosures in Europe. Sustainability Accounting, Management and Policy Journal, 6(2), 224–242. https://doi.org/10.1108/SAMPJ-10-2014-0065

- Carey, P., Khan, A., Mihret, D. G., & Muttakin, M. B. (2021). Voluntary sustainability assurance, capital constraint and cost of debt: International evidence. International Journal of Auditing, 25(2), 351–372. https://doi.org/10.1111/ijau.12223