Abstract

Tuberculosis continues to be a major global health problem. Lack of accurate, rapid and cost-effective diagnostic tests poses a huge obstacle to global TB control. While several new diagnostic tools are being developed and evaluated for TB, it is important that new tools are introduced for widespread use only after careful validation of accuracy, impact as well as cost–effectiveness in real-world settings. While there are large numbers of studies on the accuracy of TB diagnostic tests, there are few studies that are focused on cost and cost–effectiveness. There are currently no widely accepted standards on how to evaluate costs of a TB test. In this review, we describe the basic approach for computing the costs of TB diagnostic tests, and provide templates for various data elements and parameters that go into the costing analysis. We hope this will pave the way for a standardized methodology for costing of TB diagnostic tests. Such a tool would enable improved and more generalizable costing analyses that can provide a strong foundation for more sophisticated economic analyses that evaluate the full economic and epidemiological impact resulting from the implementation and routine use of performance-verified new and innovative diagnostic tools. This, in turn, will facilitate evidence-based adoption and use of new diagnostics, especially in resource-limited settings.

Keywords::

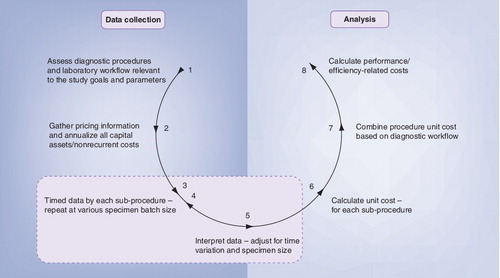

This diagram provides a step by step plan for cost analysis in evaluating TB diagnostic tests in various study settings. Steps 3, 4 and 5 should be undertaken for all the methods evaluated and relevant sub-procedures and repeated to capture data variations caused by specimen loads (and/or specimen batch size). In step 7, the investigator should consult laboratory experts regarding diagnostic workflow to reflect local laboratory practice in combining procedure unit costs.

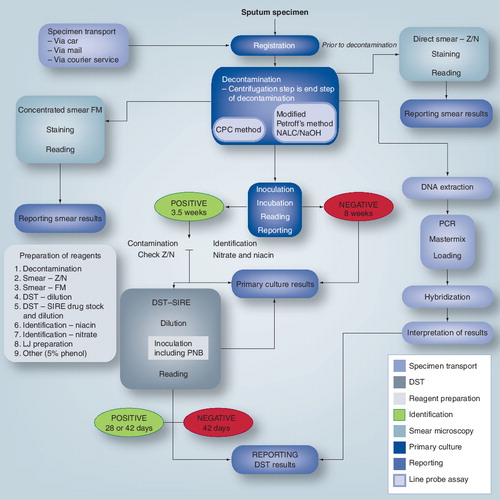

When first planning for a costing study, evaluating diagnostic workflow is essential in capturing all aspects of laboratory activities that need to be evaluated for costs. Shown is a generalized workflow observed in a laboratory where molecular testing for MDR-TB using a line probe assay is being evaluated against the conventional culture method using LJ in a demonstration study. Actual workflow at different laboratories may vary.

CPC: Cetylpyridinium chloride; DST: Drug susceptibility testing; FM: Fluorescent microscopy; LJ: Löwenstein Jensen; MDR: Multidrug resistance; NALC: N-acetyl-L-cysteine; Z/N: Ziehl-Neelsen.

Costs associated with training/QA/QC are assessed independently as per activity cost and allocated into average unit cost based on staff timing associated with the relevant laboratory procedure. For example, test specific training/QA/QC (e.g., culture and molecular testing hands-on training) should be allocated only into test specific unit cost, where as period QA/QC for general laboratory activities should be allocated into all of the laboratory procedures/activities calculated for unit cost.

QA: Quality assurance; QC: Quality control.

Tuberculosis is a major global health problem with more than 9 million new cases and nearly 2 million deaths (including 465,000 deaths in HIV-coinfected patients) caused by TB reported in 2007 alone Citation[1]. Of the TB-associated deaths, the majority are from low- and middle-income countries Citation[2], where there are significant resource constraints for the diagnosis and treatment of TB. The relatively poor performance of existing TB diagnostic tests and the lack of appropriate tools for both diagnosis and susceptibility testing in developing and high disease-burden countries leaves large numbers of patients undetected or mismanaged. Consequently, more than 400,000 new cases of multidrug-resistant TB (MDR-TB) are being reported annually, and the situation has become worse with the emergence of extensively drug-resistant TB (XDR-TB) Citation[3]. Furthermore, a poorly functioning system for TB diagnosis ultimately leads to the erosion of faith in public-health services, increased diagnostic delays and hence transmission of TB, morbidity and mortality, and impedes TB control efforts.

New diagnostics offer great promise and are essential in the fight against TB Citation[4,5]. Therefore, many new diagnostic tools are being evaluated for performance, feasibility of implementation, and sustainability in resource-limited settings Citation[6,7]. The WHO’s recent endorsement of the use of advanced diagnostic technologies (liquid culture and molecular line probe assay) for laboratory diagnosis of TB and MDR-TB in developing countries Citation[8,9] has marked the beginning of a push for the use of new diagnostic tools in high disease burden, resource-poor countries. Furthermore, with the launch of the Global Laboratory Initiative Citation[101] by the WHO in 2007, laboratory capacity strengthening and modernization of TB laboratories in developing countries has become one of the priorities of global TB control.

However, technological advancement does not come cheap and their perceived high cost and logistical difficulties in implementation in resource limited countries are the main obstacles in sustainable introduction of improved TB diagnostic capacity and infrastructure. Now with more than US$1 billion spent per year on diagnostics for TB globally Citation[10], such expenditures must be backed not just by sound evidence on test accuracy and impact on patient-important outcomes, but also with careful and more stringent approaches towards assessing their costs. This must include focusing beyond the simple boundaries of recurrent consumable costs and simple comparisons of equipment costs. Unfortunately, at the moment, there is no definite agreement nor guidelines as to what defines and constitutes the cost of a diagnostic test. Guidelines have been developed by the WHO for the purposes of enabling national TB programs to develop plans and budgets for TB control activities to meet the Global Plan 2006–2015 targets Citation[102]. However, this tool is limited to assessing financial costs. Furthermore, various guidelines published specifically for TB control activities Citation[103] or health technologies Citation[11] offer good overviews of cost and cost–effectiveness concepts, but are too broad and generalized to provide a plan for cost analysis specific for TB diagnostics.

Consequently, analyses parameters for cost and cost–effectiveness studies are left at the discretion of the study investigators and this creates problems with interpreting and assessing one study’s findings in the context of alternative but similar settings. Moreover, the outcomes of the analyses may vary depending on how one evaluates and defines the cost of a diagnostic test and can considerably alter the estimates of full socioeconomic impact. Adopting a common methodology in assessing the cost of a TB diagnostic can allow for more straightforward comparisons among diagnostic alternatives and also provide a strong common platform for cost–effectiveness analysis in TB diagnostics. Thus, the focus of our paper is to:

• Describe costing methodologies used in various cost and cost–effectiveness studies in TB diagnostics

• Propose an approach for costing any TB diagnostic that can be standardized and used as a foundation for further analysis evaluating health and socioeconomic impact

• Provide expert opinion on areas beyond standardized costing of TB diagnostics when moving toward cost–effectiveness analysis

Recent published studies evaluating costs of TB diagnostics: varied methodologies

There are a large number of publications on performance characteristics of TB diagnostic systems in various settings but only a very limited number of studies report on cost or cost–effectiveness of those TB diagnostics Citation[12–19]. A list of selected example studies on costs and cost–effectiveness of TB diagnostics and their methodologies are shown in . The diagnostic tools evaluated range from microscopic examination methods to molecular diagnostic tests and in vitro latent TB infection (LTBI) tests. One of the frequently debated technologies with respect to cost, cost–effectiveness and cost–sustainability is sputum smear microscopy and the use of fluorescent or conventional bright-field microscopes Citation[20]. While most studies claim that cost is a major barrier for introducing the better performing fluorescent microscopy (FM) compared with conventional Ziehl-Neelsen (ZN)-based microscopy, only a small number of studies report the full economic cost to the health service provider in diagnosing patients with the respective technologies Citation[12,13]. Interestingly, a detailed cost analysis performed by Sohn and colleagues contradicts the commonly accepted perception of FM being more expensive than light-microscopy techniques Citation[13].

For most of the studies reviewed in , the ultimate focus extends beyond laboratory costs associated with relevant diagnostic systems. Owing to the broad spectrum of analyses for cost, some of the studies bypass the more accurate methodology of active assessment of laboratory costs, and instead estimate key laboratory cost data elements from information provided by a third party (accounting office or manufacturer and distributor quotes). In the three studies evaluating cost–effectiveness of IFN-γ release assays for LTBI in various settings Citation[14–16] and a study evaluating rapid molecular diagnostic test for TB (nucleic acid amplification tests) Citation[17], costs of diagnostics are simplified as accounting cost or ‘market price’ of the essential consumables for the diagnostic system and estimated labor cost.

By contrast, cost–effectiveness analyses performed by Mueller et al.Citation[18] and Acuna-Villaorduna et al.Citation[19] are based upon the most complete form of cost analysis of diagnostic tests assessed among the studies reviewed in this paper. Crude per test cost of each diagnostic was calculated based on economic costing (see following section) and includes all types of resource elements (overhead, building, staff, chemicals and consumables), where amount usage of these resources are evaluated based on direct observation and time analysis (evaluating duration of laboratory procedures against volume of specimen processed during the observation) of relevant laboratory procedures. Despite their thorough assessment, these two studies, as well as all of the studies evaluated in this paper, did not evaluate costs associated with quality assurance (QA) and quality control (QC) or costs related to laboratory training (with the exception of Acuna-Villaorduna et al. where training costs were evaluated in their analysis, but it was not clear what constituted as training relevant for each test and how these costs were assessed and incorporated into the test cost Citation[19]). Without specific guidelines in place as to what should constitute the cost of a diagnostic test, evaluation of training and QA/QC costs as part of a diagnostic test cost remains variable in cost analysis methodologies.

One of the key methodological differences among all of the studies reviewed here was how capital assets, particularly overhead costs, are evaluated as part of the cost of a diagnostic test. These are important cost factors that are often ignored or not included as part of a test because overhead/infrastructure costs are not specific to a single diagnostic procedure or test. Three studies Citation[13,18,19] provide good examples in how to evaluate these costs where overall overhead costs are allocated based on measurements of utilization (building space usage, staff time and specimen volume levels). Yet, despite similarities in the global concepts in assessing these costs, actual methodologies of calculating the overhead component of a test cost depends on the logistics of data collection and data interpretation (calculating a test’s cost as an overall laboratory procedure as opposed to assessment of per test costs for each sublaboratory procedure pertinent to the diagnostic test).

Regardless of similarities or variations in costing methodologies, it is critical to have a complete and detailed understanding of each study’s methodologies to make appropriate judgments on the cost and cost–effectiveness of the diagnostic tests evaluated. This is particularly more important in the case where one would want to make relevant assessments of the cost and cost–effectiveness of a diagnostic test in different settings (i.e., similar circumstances, different country or region). One must also note the fact that test manufacturers often have divergent pricing policies for high- versus low-income countries, and prices of test kits often vary within each country depending on the negotiating abilities of buyers and healthcare providers. While some studies Citation[18,19] include pricing and other factors as part of their sensitivity analysis (and there are tools such as purchasing power parties/comparative price levels Citation[104] to adjust for differences in price levels between countries), there are several underlying factors such as situational differences (e.g., laboratories with difference capacity and biosafety levels), differences in perspectives and test-specific differences (differences in laboratory workflow and diagnostic algorithm) that make it difficult to utilize other study’s findings as evidence for policy implementation. Nonetheless, reducing the variability in cost analyses for TB diagnostics can aid in the comprehension of results, lead to better utilization of these figures, and allow for more complicated analyses evaluating socioeconomic impacts. In the following section, we attempt to discuss basic concepts and methodologies that can become a foundation for standardizing cost analysis in TB diagnostics.

Steps towards reducing variation in cost analysis methodologies: key concepts

Decision making at the most basic level: laboratory perspective of cost analysis

The manager of a TB culture laboratory may be frequently asked the following question: ‘Is home-made (i.e., laboratory-developed) Lowenstein Jensen (LJ) medium a cost-effective alternative to ready-made, commercially available LJ?’ Assuming that the overall quality of both home-made and commercial LJ media are the same, what other ‘cost’ factors should a laboratory manager consider? The list becomes quite elaborate and goes beyond the simple issue of the cost of chemicals and consumables. Rather, it is an issue that requires evaluation of the laboratory’s culture capacity, staff workload and utilization, and availability of laboratory space and equipment required for producing home-made LJ slants. Likewise, this will apply to other types of TB diagnostics whether they be the century-old light microscopy or newer rapid molecular diagnostics. Now the question becomes more specific as to how we can capture all types of resources needed for a TB diagnostic test and how to value these resources in terms of a monetary value. These issues can be addressed via economic cost analysis.

What are the steps in planning a costing study in TB diagnostics?

Why economic cost analysis?

Cost analysis is a method of partial economic evaluation that focuses on assessing the cost of providing a service, program or intervention Citation[21,22]. While cost analysis does not directly include the effectiveness aspect of an intervention/program, its main advantage lies in the relative ease in interpreting the results (often calculated as cost per specified action or specified unit), the ability to directly compare costs between interventions being considered, with little or no requirements for complicated modeling nor assumptions that may have significant influences on the results of an analysis. Furthermore, despite its limitations, cost analysis results can be used successfully in decision-making processes when relative effectiveness data (which is usually part of field demonstration studies) of compared interventions are available to cross-examine. However, the concept of ‘cost’ in cost analysis varies by how one views it and can largely be defined in two ways: financial or economic cost. Financial cost is often referred to as the accounting cost where costs are the monetary value of expenditures. Economic cost concerns all costs associated with decisions or choices made and is expressed in terms of the alternative choices and the forgone benefits (opportunity cost).

Choosing the right costing concept

In public-health interventions, including evaluations of diagnostic tests for TB, cost analysis should be based on economic costing rather than financial. This is because in public-health programs in developing countries:

• A large number of goods are donated and time is often volunteered

• ‘Price’ often fails to accurately reflect the true value of goods or services provided

These issues effect the opportunity cost Citation[23,24], and are important ingredients in the comparative assessment of costs and benefits of alternative interventions. Likewise, economic costing can provide a clear picture of the complete costs of providing particular goods or services (in this case, TB diagnostic services using various technologies and methods) whereas financial costing only emphasizes the actual flow of money associated with the goods and services purchased Citation[24]. A healthcare provider’s perspective is usually taken when performing a cost analysis of a diagnostic test. However, this approach may fail to take into account other important differences in various diagnostic algorithms where a test that can give results within 1 h may reduce the number of patient visits to the clinic (and thus reduce both direct and indirect patient costs) in order to complete the diagnostic work-up and initiate treatment.

Evaluation of laboratory workflow

provides an example of the overall processes and steps in completing the cost analysis component of studies evaluating laboratory diagnostics. In planning for a cost analysis study of TB diagnostics, one should keep in mind that the overall focus is to express laboratory performance of the new test compared with the current or reference standard(s) – including improvements in time to detection, staff workload, changes in direct and indirect costs in terms of a monetary value – as a unit cost in terms of the number of tests performed or specimens screened. Likewise, it is imperative to have a good understanding of performance characteristics (not only for cost analysis purposes), procedural logistics, and laboratory workflow associated with each relevant diagnostic system evaluated. provides an example of the diagnostic workflow at a culture laboratory (solid culture only) with newly implemented molecular testing capacity for ‘demonstration’ study purposes and all laboratory processes and steps that should be considered for cost analysis. Careful examination of the diagnostic workflow for a TB laboratory allows the investigator to capture all aspects of laboratory activities that need to be evaluated for costs. It also provides a good roadmap for a cost analysis study, where costs can be broken down by procedures and stratified to identify the major drivers of costs for a particular diagnostic method being evaluated. Likewise, evaluation of costs QA/QC and training activities can be calculated (expressed as per activity cost) by utilizing the concepts laid out above and first identifying key activities, resources utilized and estimation or actual measures of utilization of various resources.

Determining data parameters & units, annualization of capital assets & analysis

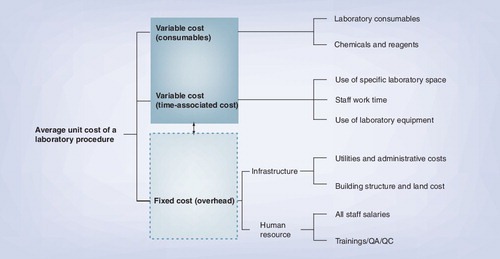

and depict all of the components included in the unit cost of a particular diagnostic procedure. In order to coordinate calculation of overall unit costs for a diagnostic test, simple consumables’ costs need to be calculated based on the ‘ingredients’ approach where the quantity of inputs are multiplied by unit prices of each respective item. In this approach, time analysis (evaluation of the duration of laboratory procedures by direct observation) of laboratory procedures allows for quantification of the usage of capital assets (building space and equipments) in terms of ‘time’ – minutes used and minutes used per square meter of the space – and expressed based on overall capacity and the number of specimens processed during the assessment (point evaluation of laboratory procedures). Laboratory consumables and chemicals are quantified based on relevant units (units, pieces, meters, grams or milliliters).

There are two reasons for assessing use of capital assets in terms of time-specified units. The first is to reflect the opportunity cost of the use of capital assets of a particular procedure over another laboratory task, and the second is to reflect general preference for future spending, known as time preference Citation[24]. Hence, all capital costs (mainly laboratory space and building and laboratory equipment, inclusive of all costs related to maintenance) will need to be annualized based on their estimated expected life-years and discount rate that reflects their rate of return (real rate in private sector or social rate of time preference). For a discussion of the methodology of annunalization of capital assets, see a review by Walker and Kumaranayake Citation[25]. Likewise, assessing costs based on a time analysis of each relevant laboratory procedure in a TB diagnostic system allows for accurate allocation of overhead costs, where overhead costs for each respective laboratory procedure is calculated based on the number of staff, staff time and utilization of the physical space.

The year of pricing & currency that costs are valued

In order to avoid variations and minimize estimations, all pricing on overhead costs, laboratory equipments, chemicals and reagents, consumables and staff salaries ought to be expressed and evaluated in the year when the study was undertaken. This is to avoid any discordance caused by the year in which costs are valued when costs of alternative diagnostic tests are compared. In the case of evaluating capital assets, annualizing (explained previously) their value is based on the life expectancy of ‘new’ capital. Pricings for all recurrent costs such as reagents and chemicals, consumables required for relevant diagnostic systems, staff salaries and overhead costs (maintenance costs and cost of building space) should be averaged as there often are multiple manufacturers and distributors offering the same or similar type of product at different prices, and staff salaries may vary based on the level of experience and seniority.

In most of the laboratories where the cost and cost–effectiveness of TB diagnostics are being evaluated, much of the laboratory equipment and particularly the building space are at least several years old and the pricing available in the laboratory records may be outdated compared with the study year (usually pricing information available within 1–2 years of the study year is acceptable). The simplest way of unifying pricing is to take equipment prices as if purchased new with all costs associated with procurement. Furthermore, assessment of the cost of building infrastructure can be done by thoroughly reviewing current real estate markets in the area/country and adding costs associated with special structural adjustments that are needed to meet biosafety requirements of a TB laboratory. Alternatively, it is also possible to make inflationary adjustments to all pricings and cost data from various years into standardized year US$2000 prices by utilizing a conversion table Citation[26].

It is possible to use the currency most relevant to the study setting (e.g., US$, €, UK£, South African Rand, and so on). However, if conversion to an alternative currency is needed, conversions should be based on annual (current or previous year) exchange rates against the converting currency (e.g., US$). Various currency exchange rates are available, but for health interventions, it is recommended to use the official UN exchange rate, which is available online Citation[105].

Beyond cost analyses

Cost–effectiveness analysis is appropriate when the aim of an evaluation is to compare alternative strategies that are associated with both different costs and different effectiveness. A cost-effective test does not generally mean the cheapest test. The goal of cost–effectiveness analysis is to identify intervention(s) that provide the greatest health impact with the lowest cost per unit of output. In a way, the detailed cost analysis described in previous sections provides a good cost–effectiveness analysis from a laboratory services perspective. However, to capture the potential cost and benefit obtained from newer innovative diagnostic tests beyond the laboratory, full cost–effectiveness/benefit/utility analysis ought to be considered.

In analyses beyond cost analysis, outcome measurements can range from laboratory performance characteristics to health impact indicators (e.g., reduction in mortality, proportion of patients who get cured), but these indicators must remain the same for each type of intervention compared in the study. Furthermore, both cost and effectiveness parameters are determined based on the perspective taken by the study. A summary of types of cost and examples to be considered based on study perspective is shown in . In studies that evaluate changes in diagnostic algorithms, detailed costs of all diagnostic alternatives as well as patient impact data must be evaluated to accurately evaluate changes in costs associated with the introduction of the new diagnostic algorithm. In certain cases (i.e., demonstration studies) the evaluation period may not provide adequate time to evaluate all types of health and societal impact indicators. In such cases, it is possible to use estimated figures from relevant literature or expert opinion and perform sensitivity analyses to evaluate these uncertain parameters.

In TB diagnostic studies, a major limitation is that most of the available studies are focused on test accuracy (i.e., sensitivity and specificity), and even these studies are often poorly designed and reported Citation[27]. Existing systematic reviews on TB tests are all focused on sensitivity and specificity Citation[6]. A caveat in using these effectiveness indicators is that they are dependent on what one views as the ‘gold standard’ to the diagnostic tests being evaluated. With no ultimate ‘gold standard’ test in TB, readers (policy makers) as well as study investigators must be always cautious in declaring one test as ‘cost-effective’ against another. Moreover, there are few data on the impact of new diagnostic tests on patient-important outcomes, such as missed diagnoses, mortality and treatment completion. This will, naturally, diminish the scope of cost–effectiveness analyses on TB diagnostic studies. However, there still remain significant challenges in including important health outcome measurements (such as reduced transmission) in analyses owing to the difficulty in obtaining actual data and the large variability in interpretation of outcome measurements.

Expert commentary & five-year view

In this review, we have highlighted the importance of conducting costing studies on TB diagnostic tests, and have described the key elements of a costing analysis. In evaluating costing study results, it is important for policy makers to clearly understand the methodology and perspective used in the study. Furthermore, it is imperative to recognize that overevaluation/analysis can often lead to indecisive conclusions and provide no directional guidance. As demonstrated by the studies reviewed in this paper, there are currently no standards for how to evaluate costs of a laboratory test, even to the simplest perspective – the laboratory – despite the fact that there are TB-specific (albeit not specific for TB diagnostics) guidelines for cost and cost–effectiveness analysis. For instance, costs of laboratory support activities such as training, technical support and QA are of critical importance in ensuring quality of laboratory procedures, and yet are often poorly accounted for in costing, leading to shortfalls in funding for these activities. A wide variation in laboratory costs reported in these various studies can cause confusion and may lead to inadequate decisions when policy makers are considering implementing similar technology in different countries with similar disease and economic settings. Therefore, with the variations in methodology, each study evaluating laboratory diagnostics must clearly outline study parameters and key factors evaluated in calculating the ‘costs.’ Likewise, because the idea of cost varies based on one’s viewpoint, policy and decision makers should not have a pre-determined mind set that a more expensive test is automatically unaffordable or impractical for sustained and/or widespread implementation.

In the context of modernizing TB laboratories in resource-poor settings, there is growing interest in improving the overall capacity of TB laboratories. It is important to realize that introduction and implementation of more types of new tests alone is not the solution to improving laboratory capacity. In resource-poor settings, every penny invested is significant. Laboratories provided with technological and structural improvements (including technical training) may struggle to adjust to their new diagnostic capacity and ultimately fail to optimize utilization of that capacity. This may result in wastage of very expensive reagents and ultimately lead to failure in sound laboratory practice. In such cases, cost and cost–effectiveness analysis studies of diagnostic systems have little or no meaning and sustainability of the newly improved diagnostic capacity will not be realized. Therefore, partners and organizations working on capacity improvement projects must also consider the important aspects of proper management (inventory, human resources and infrastructure) of the upgraded laboratory capacity that are based on periodic review of costs and performance figures.

In summary, cost analyses are critical for TB control and TB policies. While there are large numbers of studies on accuracy of TB diagnostic tests, there are few studies that are focused on cost and cost–effectiveness. There are currently no widely accepted standards on how to evaluate costs of a TB test. In the next few years, we hope to develop a standardized tool for costing of any TB diagnostic. Such a tool would enable improved and more generalizable costing analyses to be undertaken and the full economic costs to be determined. This, in turn, will facilitate evidence-based adoption and use of new diagnostics, especially in resource-limited settings.

Table 1. Summary of costing methodology utilized in various cost and cost–effectiveness studies evaluating TB diagnostics.

Table 2. Cost data elements for cost analysis of TB diagnostics and suggested data sources.

Table 3. Cost parameters (and examples) based on cost and cost–effectiveness analysis in TB diagnostics.

Key issues

• TB is a major global health problem, and limited diagnostic capacity in high TB burden resource-poor areas is a significant obstacle to global TB control.

• Several new diagnostic tools are being developed and evaluated for TB.

• While new diagnostics offer great promise, limited resources and the movement towards evidence-based guidelines and policies require careful validation of new tools and their cost–effectiveness prior to their introduction for routine use.

• Policy and decision makers are often required to assess accurate costs associated with relevant technology being considered for implementation.

• Cost analysis is one type of economic evaluation that focuses on assessing the cost of providing services, programs or interventions.

• While cost analysis does not directly include the effectiveness aspect of an intervention/program, its main advantage lies in the relative ease of interpreting the results, ability to directly compare costs between/among interventions being considered, with little or no requirement for complicated modeling or assumptions that may have significant influence on the results of an analysis.

• In public-health interventions, particularly when evaluating diagnostic tests for TB, cost analysis should be based on economic rather than financial costing.

• The goal of cost–effectiveness analysis is to identify intervention(s) that provide the greatest health impact with the lowest cost per unit of output.

• While there are large numbers of studies on the accuracy of TB diagnostic tests, there are few studies that are focused on cost and cost–effectiveness. There are currently no standards on how to evaluate the costs of a TB test, even to the simplest perspective – the laboratory.

• A standardized tool for costing of TB diagnostics would enable improved and more generalizable costing analyses to be undertaken and the full economic costs to be determined.

Acknowledgements

The authors are grateful to Heather Alexander Konopka for useful input and suggestions.

Financial & competing interests disclosure

Hojoon Sohn, Heidi Albert and Madhukar Pai are affiliated with the Foundation for Innovative New Diagnostics (FIND), Geneva. FIND is a nonprofit agency that works with several industry partners in developing and evaluating new diagnostics for neglected infectious diseases. This work was supported in part by Canadian Institutes for Health Research (CIHR) grant MOP-89918, and European Commission grant TBSusgent (FP7-HEALTH-2007-B). Madhukar Pai is supported by a CIHR New Investigator Award. Keertan Dheda is supported by a SARChI award and MRC Career Development Award. These funding agencies had no role in the development of this manuscript. The authors have no other financial involvement with any organization or entity with a financial interest in or financial conflict with the subject matter or materials discussed in the manuscript apart from those disclosed.

No writing assistance was utilized in the production of this manuscript.

References

- WHO. Global tuberculosis control: epidemiology, strategy, financing: WHO Report 2009. WHO/HTM/TB/2009.411. WHO, Geneva, Switzerland, 1–303 (2009).

- Lopez AD, Mathers CD (Eds.) Global Burden of Disease and Risk Factors. Oxford University Press, NY, USA (2006).

- WHO. The Global MDR-TB and XDR-TB Response Plan, 2007–2008. WHO/HTM/TB/2007.387. WHO. Geneva, Switzerland (2007).

- Young DB, Perkins MD, Duncan K et al. Confronting the scientific obstacles to global control of tuberculosis. J. Clin. Invest.118(4), 1255–1265 (2008).

- Keeler E, Perkins MD, Small P et al. Reducing the global burden of tuberculosis: the contribution of improved diagnostics. Nature.444(Suppl. 1), 49–57 (2006).

- Pai M, Ramsay A, O’Brien R. Evidence based tuberculosis diagnosis. PLoS Med.5(7), e156 (2008).

- Pai M, O’Brien R. New diagnostics for latent and active tuberculosis: state of the art and future prospects. Semin. Respir. Crit. Care Med.29(5), 560–568 (2008).

- WHO. New WHO policies. The use of liquid medium for culture and DST. Policy statement (2007).

- WHO. Molecular line probe assays for rapid screening of patients at risk of multidrug-resistant tuberculosis (MDR-TB). Policy statement (2008).

- WHO and Foundation for Innovative New Diagnostics. Diagnostics for tuberculosis: global demand and market potential. WHO, Geneva, Switzerland (2006).

- Canadian Agency for Drugs and Technologies in Health. Guidelines for the Economic Evaluation of Health Technologies: Canada (3rd Edition). Ottawa, Canada (2006).

- Kivihya-Ndugga LEA, van Cleeff MRA, Githui WA et al. A comprehensive comparison of Ziehl-Neelsen and fluorescence microscopy for the diagnosis of tuberculosis in a resource-poor urban setting. Int. J. Tuberc. Lung Dis.7, 1163–1171 (2003).

- Sohn H, Sinthuwattanawibool C, Rienthong S et al. Fluorescence microscopy is less expensive than Ziehl-Neelsen microscopy in Thailand. Int. J. Tuberc. Lung Dis.13(2), 266–269 (2009).

- de Perio MA, Tsevat J, Roselle GA et al. Cost–effectiveness of interferon-g release assays vs tuberculin skin tests in health care workers. Arch. Intern. Med.169(2), 179–187 (2009).

- Marra F, Marra CA, Sadatsafavi M et al. Cost–effectiveness of a new interferon-based blood assay, QuantiFERON®-TB Gold, in screening tuberculosis contacts. Int. J. Tuberc. Lung Dis.12(12), 1414–1424 (2009).

- Oxlade O, Schwartzman K, Menzies D. Interferon-g release assays and TB screening in high-income countries: a cost–effectiveness analysis. Int. J. Tuberc. Lung Dis.11(1), 16–25 (2007).

- Dowdy DW, Maters A, Parrish N et al. Cost–effectiveness analysis of the gen-probe amplified Mycobacterium tuberculosis direct test as used routinely on smear-positive respiratory specimens. J. Clin. Microbiol.41(3), 948–953 (2003).

- Mueller DH, Mwenge L, Muyoyeta M et al. Costs and cost–effectiveness of tuberculosis cultures using solid and liquid media in a developing country. Int. J. Tuberc. Lung Dis.12(10), 1196–1202 (2008).

- Acuna-Villaorduna C, Vassall A, Henostroza G et al. Cost–effectiveness analysis of introduction of rapid, alternative methods to identify multidrug-resistant tuberculosis in middle-income countries. Clin. Infect. Dis.47(4), 487–495 (2008).

- Mitchison DA. Bacteriology of tuberculosis. Trop. Doct.4(4), 147–153 (1974).

- Drummond MF, O’Brien B, Stoddart GL et al.Methods for the Economic Evaluation of Health Care Programmes (2nd Edition). Oxford University Press, Oxford, UK (1997).

- Adam T, Baltussen R, Tan-Torres T et al. Making choices in health: WHO guide to cost–effectiveness analysis. WHO, Geneva, Switzerland (2003).

- Buchanan JM. Opportunity cost. In: The New Palgrave: A Dictionary of Economics, (Volume 3) Durlauf SN, Blume LE (Eds.) Palgrave Macmillan, UK 718–721 (1987).

- Creese A, Parker D. Cost analysis in primary health care: a training manual for programme managers. WHO, Geneva, Switzerland (1994).

- Walker D, Kumaranayake L. Allowing for differential timing in cost analyses: discounting and annualization. Health Policy and Planning17(1), 112–118 (2002).

- Kumaranayake L. The real and the nominal? Making inflationary adjustments to cost and other economic data. Health Policy and Planning15, 230–234 (2000).

- Pai M, O’Brien R. Tuberculosis diagnostics trials: do they lack methodological rigor? Expert Rev. Mol. Diagn.6(4), 509–514 (2006).

Websites

- WHO. Global Laboratory Initiative. WHO, Geneva, Switzerland (2007) www.who.int/tb/dots/laboratory/gli/en/index.html

- WHO. Planning and Budgeting for TB control activities. WHO, Geneva, Switzerland www.who.int/tb/dots/planning_budgeting_tool/en/index.html

- WHO. Guidelines for cost and cost–effectiveness analysis of tuberculosis control. WHO, Geneva, Switzerland http://whqlibdoc.who.int/hq/2002/who_cds_tb_2002.305a.pdf

- Organisation for Economic Co-operation and Development. Purchasing power parities/comparative price levels www.oecd.org/std/ppp

- United Nations Statistics Division. Exchange rate, US$ per national currency, period average http://data.un.org/data.aspx?d=cdb&f=srID%3A6080