Abstract

Objective:

To investigate the evolving use and expected impact of pay-for-performance (P4P) and risk-based provider reimbursement on patient access to innovative medical technology.

Methods:

Structured interviews with leading private payers representing over 110 million commercially-insured lives exploring current and planned use of P4P provider payment models, evidence requirements for technology assessment and new technology coverage, and the evolving relationship between the two topics.

Results:

Respondents reported rapid increases in the use of P4P and risk-sharing programs, with roughly half of commercial lives affected 3 years ago, just under two-thirds today, and an expected three-quarters in 3 years. All reported well-established systems for evaluating new technology coverage. Five of nine reported becoming more selective in the past 3 years in approving new technologies; four anticipated that in the next 3 years there will be a higher evidence requirement for new technology access. Similarly, four expected it will become more difficult for clinically appropriate but costly technologies to gain coverage. All reported planning to rely more on these types of provider payment incentives to control costs, but didn’t see them as a substitute for payer technology reviews and coverage limitations; they each have a role to play.

Limitations:

Interviews limited to nine leading payers with models in place; self-reported data.

Conclusion:

Likely implications include a more uncertain payment environment for providers, and indirectly for innovative medical technology and future investment, greater reliance on quality and financial metrics, and increased evidence requirements for favorable coverage and utilization decisions. Increasing provider financial risk may challenge the traditional technology adoption paradigm, where payers assumed a ‘gatekeeping’ role and providers a countervailing patient advocacy role with regard to access to new technology. Increased provider financial risk may result in an additional hurdle to the adoption of new technology, rather than substitution of provider- for payer-based gatekeeping.

Introduction

Pay-for-performance (P4P) and various forms of risk-based reimbursement are becoming more established approaches to provider payment in both public and private health insurance programs, yet much is unknown regarding their impacts on the organization, cost, and quality of care. One less-investigated area is their impact on patient access to innovative medical technology.

In the case of Medicare, attention has focused on the payment reform provisions of the Patient Protection and Affordable Care Act (ACA), including those encouraging the development of Accountable Care Organizations (ACOs). As of May 2014, a total of 361 ACOs were enrolled in either the Medicare Shared Savings Program (MSSP) or the Pioneer ACO program, accounting for some 5.6 million assigned beneficiaries, or over 10% of total enrolleesCitation1. In addition, commercial payers are expanding contractual relationships with at-risk provider organizations, which may be defined somewhat differently than those meeting federal ACO definitions. Including both public and private sector models, as of February 2013, the Center for Accountable Care Intelligence estimated that 428 ACOs existed in 49 states, more than double the number at the start of 2011Citation2. Another source estimated that more than half of the US population lives in areas served by ACOs, and that ACOs now cover 37–43 million total Medicare and non-Medicare patientsCitation3.

In addition to ACOs, under the ACA and previously, CMS also is sponsoring a number of other alternative payment and P4P demonstration projects, including, among othersCitation4: hospital-physician gain-sharing; a Hospital Quality Improvement Demonstration Project, which includes inpatient quality of care-based pay-for-performance payments for five clinical conditions; a bundled payment pilot program with four episode-of-care models; Medicare payment penalties to hospitals with high re-admission rates; a hospital value-based purchasing program; Medicare bonuses for physicians who participate in quality reporting; and a shared savings program through the Physician Group Practice (PGP) Demonstration and PGP Transition Demonstration.

Private payers also increasingly include P4P and risk-based reimbursement approaches for providers in their networks. In 2006, it had been estimated that more than half of commercial health plans in the US use P4P incentives of some type in their provider contracts, representing 80% of all enrollees in such plans, and that, of those, 90% had programs for physicians and 38% had programs for hospitalsCitation5. Another source noted in a 2010 survey of payers that 96% of all responding plans reported having incentives either in operation or in development for physicians, and the corresponding figure for hospitals was 40%Citation6.

The design and coverage of these alternative payment programs vary; some involve ‘upside risk’ only, in which provider payment increases with the achievement of certain targets, and others reflect both ‘upside’ and ‘downside’ risk, in which provider payment may also decrease if performance falls short of pre-determined targets. Some affect hospital reimbursement, others affect physician payment, and others affect integrated systems. All, however, reflect experiments in moving from the historical fee-for-service model in which payment is based on volume alone to an approach in which payment is tied to performance against financial metrics, quality of care metrics, or some combination of the two.

The impact, short- and longer-term, of a shift towards P4P or risk-based payment programs is not yet known. Depending on their specific design, P4P reimbursement models may create a range of incentives and potential effects on technology adoption and care. By providing financial incentives for desired outcomes, rather than reimbursing providers solely on the volume of care delivered, P4P programs have the potential to promote higher quality and more efficient care. At the same time, however, in the absence of adequate controls and protections for patient access and carefully defined and monitored metrics for quality, introducing financial risk for providers also has the potential to reduce quality of care by reducing access to needed or globally optimal care that would have a short-term negative financial impact on the affected contracting organization. Others have noted previously that payment reform models have the potential to create unintended negative consequences, such as avoidance of sick, high-risk, or high-cost patients by providers, other barriers to access, and under-use of evidence-based servicesCitation7. As a result, without proper controls and protections, financial incentives have the potential to exacerbate healthcare disparitiesCitation8,Citation9.

In order to reduce these risks, P4P and risk-based provider payment models that include financial incentives that would reduce spending generally also include quality-based incentives and metrics, and payment is generally a result of performance on both sets of measures. Designing and implementing the optimal set of metrics to drive desired care outcomes presents its own challenges, however. Over-reliance on process-based metrics may result in ‘treating to the test’Citation10, or may stifle innovation and inhibit organizations from developing creative solutions that would improve quality of careCitation11. Appropriate outcome-based metrics may be difficult to develop or apply, however.

A shift in provider reimbursement model from the traditional fee-for-service model to P4P and risk-based provider reimbursement may have far-reaching implications on the organization, level, mix, and site of care. To-date, evaluations of such P4P and risk-based reimbursement programs have been limited, and the effects of such programs on outcomes, including quality of patient care, are largely unknownCitation12–17.

Moreover, programs vary in their provider coverage (e.g., acute hospitals, physician groups), the clinical conditions they cover (e.g., acute myocardial infarction, heart failure, joint replacement), and their specific measurement and payment provisions, and may include multiple program components. Having evolved rapidly over a short period of time, firm conclusions may be challenging to draw.

This study investigates one area where evaluations to-date generally have not focused and the impact of changes in provider reimbursement models is largely unexplored—technology assessment and coverage decisions by payers, and payers’ views of their potential impact on selection and adoption of innovative medical technology (such as medical devices, and diagnostic and imaging procedures) by providers. Effects on the assessment and use of medical devices are of particular interest as the population ages to both public and private insurers, to patients, and to manufacturers of innovative technologies. Changes to provider reimbursement may have important effects on patient access, patient outcomes, competition in the medical device market, and incentives for innovation and the future availability of new generations of medical devices over the longer-term.

Patients and methods

Survey design

In order to shed light on the recent evolution of P4P and risk-based reimbursement programs among commercial insurers, the expected direction of such programs in the next 3 years, current approaches to technology assessment and coverage decisions for innovative medical technology, and the potential implications of evolving provider payment models for medical devices and other innovative medical technology, we conducted structured in-depth interviews with nine leading private insurers who have a variety of approaches to P4P and risk-based provider payment in-place. Interviews focused on programs in their commercial lines of business.

We targeted leading insurers who are early adopters of risk-sharing models, and restricted respondents to those having at least one current and significant provider risk-sharing program. Determination of the significance of any risk-sharing program was left to the respondent, but at a minimum the program should contain either quality or financial metrics that affect provider payment, or both.

We targeted respondents from two different categories of private payers. National Payers were defined as payers offering plans across all regions in the US. Respondents from three national payers, representing over 100 million commercially-insured lives, participated in the survey. Regional Payers were defined as payers with a substantial share of enrollees in a single region or geographic market in the US. Because of their strong competitive position in their geographic markets and ability to design their offerings to meet the local needs of employers and members, such payers may be leaders in implementing new payment models. Six of the respondents were regional payers, of which three were Blue Cross Blue Shield organizations. The six regional payers included in the survey represented over 10 million commercially-insured lives.

The respondents were distributed geographically—as noted, three were national payers, one was from the Northeast, one was from the South, one was from the Midwest, and three were from the West. Together, the respondents reported they represent more than 110 million commercial lives (in both insured and self-insured commercial lines of business). The responses were intended to provide insights into the adoption of risk-sharing payment models by different types of likely early adopters, rather than to constitute a nationally representative sample of private payers generally, accounting for the over-weighting of respondents from the west, which may be more likely to have such risk-sharing models in-place.

For each survey respondent, a confidential, in-depth 1-h long telephone interview was conducted with a medical director familiar with both the organization’s provider payment models and medical technology coverage decisions. All respondents were required to be voting members of their plans’ technology assessment committees. The interviews were conducted in November and December of 2013 and were conducted confidentially. Respondents were not informed of the study sponsor, and anonymity was assured to participants. Interviews were audiotaped (respondent-identifying information having been removed) and written transcripts were analyzed by one trained reviewer, with verification by a second reviewer. The survey reflects a mix of questions related to the adoption of risk-sharing models and specific features of those models, and questions related to the process and considerations involved in reviewing new technologies for coverage, as well as views of the current and evolving interaction between the two areas.

In addition to qualitative insights from open-form participant replies, structured information from the survey was compiled for analysis. Such data includes: the characteristics of current risk-sharing payment models at the organization and those anticipated within the coming 3 years; the financial and quality metrics associated with the risk-sharing payment models; the perceived success of the model implementation; and the process for considering new, and potentially more expensive, medical technologies within a risk-sharing payment context. Where selected brief quotations are provided to illustrate representative points, they are drawn directly from confidential interview transcripts.

Limitations

Findings from the survey are limited to nine targeted respondents, and data were self-reported. No means of independently verifying the responses was possible, given the confidential nature of the questions. Views of potential provider behavior are those of payers, and verification with providers was beyond the scope of the research. While response data on both a plan and covered lives basis is presented, and the results from these nine respondents provide insights into the potential future evolution of risk-sharing provider payment models and potential differences among different types of payers and respondents represent over 110 million commercial lives in total, the sample size and approach was not designed or intended to allow for statistical extrapolation to all commercial insurance plans. Given the research design and potential for respondent selection bias, the results should be viewed as hypothesis-generating, highlighting leading high-level trends and identifying potential valuable areas for future research as the use of such provider payment models continues to expand.

Results

Participation in P4P and risk-sharing programs is increasing rapidly

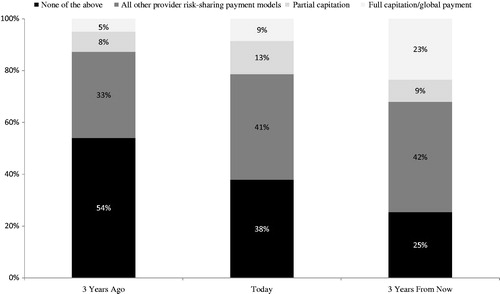

All respondents reported a trend towards greater use of such programs (with the exception of one respondent, who reported that all commercial lives were already subject to such provisions). On average (i.e., the unweighted average of responses across all respondents), the reported percentage of commercial lives subject to any type of P4P or risk-based payment provisions increased from roughly half (46%) 3 years ago to just under two-thirds (62%) today, and was reported as expected to reach three-quarters of commercial lives 3 years from now ().

Figure 1. Percentage of commercial lives in plans with provider risk-based payment models: Unweighted percentage of respondents.

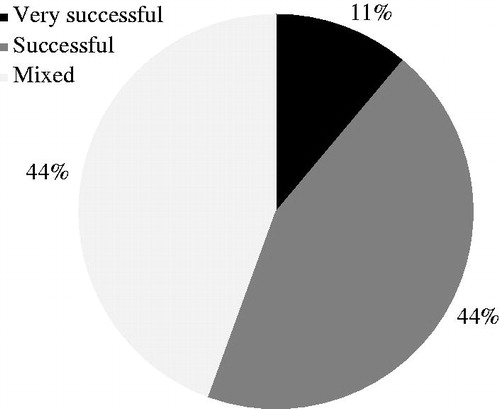

Five respondents (55% of plans, 27% of lives) reported that results were either successful or very successful (the remaining respondents reported that results were mixed) and all respondents reported that these programs were either important or very important to their strategic plans going forward and, therefore, planned to continue or expand their programs (). Eight respondents (89% of plans, 99% of lives) described their organizations as viewing these type of P4P or risk-sharing provider payment programs as ‘pilot programs we fully expect to be “the wave of the future”’ or ‘an established part of how we do business’.

Figure 2. Satisfaction with provider risk-based payment programs: Unweighted percentage of respondents.

The mix of P4P and risk-based payment programs varies, reflecting payer experimentation

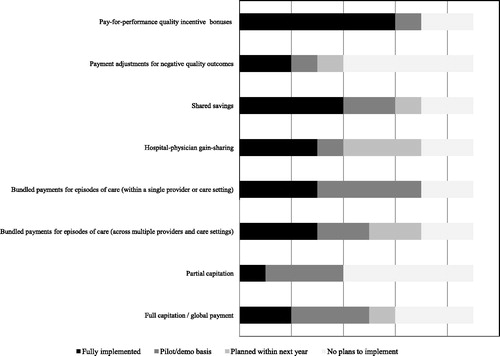

P4P and risk-based payment approaches encompass a wide range of reimbursement program designs and respondents were asked about their current and planned use of eight different provider payment models, divided into four types, generally in order of increasing payer financial risk ():

Pay-for-performance incentives, either in the form of positive quality incentive bonuses or payment adjustments for negative quality outcomes;

Shared performance incentives, either in the form of shared savings programs or hospital-physician gain-sharing;

Bundled payments for episodes of care, either within a single provider or care setting or across multiple providers and care settings; and

Capitation, either partial capitation or full capitation.

Figure 3. Provider risk-sharing payment models in commercial lines of business: Unweighted number of respondents (n = 9).

Respondents differed widely in terms of the number and variety of programs in-place, with three general models emerging based on the level of current development in the use of P4P and provider risk-based reimbursement approaches:

Model A: Established and growing use of capitation and a well-developed risk-based reimbursement program

At one end of the spectrum, two of the respondents reported that full or partial capitation is currently a fully implemented feature of provider payment in their organizations, with the percentage of covered lives growing to an estimated 50–70% 3 years from now, and a reported goal to ‘give as much risk away as possible’. Both respondents described their motivations for such programs as both cost-related and quality-related, and had operated capitation models for some time. Both operated a well-developed P4P and risk-based reimbursement program with multiple components, also including bundled or episode-based reimbursement models (either as standard elements of their reimbursement program or as demonstration projects), as well as shared savings or hospital-physician gain-sharing models.

Model B: Bundled payment and shared savings and gain-sharing models

Three respondents described their organizations as having only pilot or demonstration capitation programs in place, covering a limited number of providers and members, supplemented by bundled or episode-based payment models (either as established provider payment programs or as demonstration projects), and both shared savings and hospital-physician gain-sharing programs. Each of these respondents also had a P4P bonus program in place, but noted a strategy to shift away from ‘upside-only’ programs.

Programs included multiple approaches, and respondents highlighted different programs as being of greatest strategic importance to their organizations. One respondent identified episode-based payment models, including for orthopedic and cardiovascular procedures. Bundles include pre-operative care, operative care, and rehabilitative care, and were described as associated with targeted benefits in improved forecasting, more efficient care, enhanced ability to implement care protocols, reduced variability, and increased economies of purchasing. Another respondent highlighted ACOs and hospital-physician gain-sharing as particularly important, in that they were means by which hospital and physician behavior could be aligned to yield the greatest impacts on cost and quality of care. The third respondent highlighted bundled payment and shared savings as being a focus, in comparison to an earlier focus on P4P quality bonuses.

Model C: More limited but ongoing experimentation with P4P programs

The remaining four respondents reported more limited use or success of P4P and risk-based provider reimbursement, with either only one of the four general types of programs (i.e., capitation, bundled payments for episodes of care, shared performance incentives, or pay-for-performance incentives) today or only demonstration programs in-place. Each of the four noted an emphasis on one or two discrete physician P4P bonus programs in specific areas of clinical or other focus. One respondent noted previous unsuccessful experimentation with a limited scale bundled payment pilot, stalled due to administrative complexity, and ongoing discussions regarding hospital–physician gain-sharing programs.

The payment reform models described by respondents vary with respect to the number and type of programs, the level of provider participation, the specific payment mechanisms and quality metrics employed, and the level of financial risk and reward involved, reflecting ongoing experimentation. Programs ranged from well-established programs covering a high percentage of providers with substantial upside and downside revenue implications for participating providers, to pilot or demonstration programs affecting providers in a single clinical area with upside-only revenue implications. All respondents described their programs as active experiments subject to change.

A variety of financial and quality measures were in use, with preventive care (e.g., flu vaccination), chronic care process of care (e.g., diabetic vision screenings), and chronic care outcomes (e.g., hbA1c levels) in place by seven of the respondents; patient access, patient experience satisfaction, and acute care outcomes (e.g., 30-day re-admissions) cited as in place by six of the respondents; patient safety and efficiency of care (e.g., inpatient admissions, emergency department visits) in place by five; and acute processes of care (e.g., use of ‘clot busters’ within 30 min to emergency department patients with suspected myocardial infarction) and population health (e.g., smokers, BMI) by only two. Multiple sources of metrics were cited, although many reported increasingly relying on HEDIS and Medicare ‘star rating’ metrics in their commercial program designs.

All respondents reported that concerns with cost initially drove their organizations to consider and pursue risk-based provider payment programs, although the importance of financial vs quality metrics varied. Two-thirds of plans (29% of lives) also noted concerns with quality as being important drivers. Both national plans (86% of lives) also noted that employer interest was a factor.

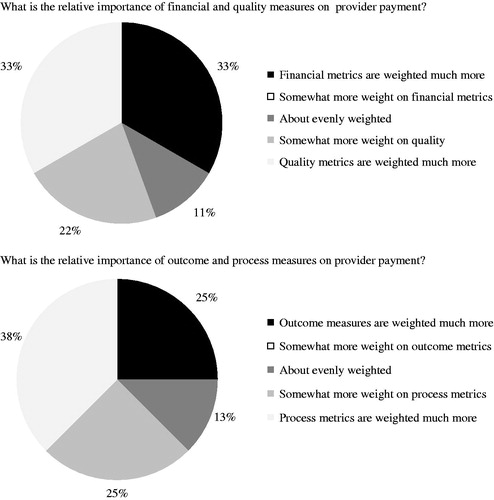

One-third of respondents (6% of lives) reported that financial metrics were weighted much more, one-third of respondents (6% of lives) reported that quality metrics were weighted much more, and there was no obvious relationship between program design or risk-based payment model and metric weighting or selection. Process measures still dominate outcome measures, although several respondents reported a desire to transition to greater use of outcomes measures over time ().

Figure 4. Relative importance of financial, quality, outcome and process measures when determining provider payment: Unweighted percentage of respondents.

All respondents reported not yet having the results of careful evaluations of cost savings results and, when pressed to provide an informal, ballpark estimate of the savings achieved, respondents generally cited financial results ranging from minimal if any savings to 10–20% of total medical expense (TME) for the best performers. To the degree that savings were achieved, they were generally thought to be due to reduced emergency room visits and inpatient admissions. Several also cited purchasing-related efficiencies such as narrowing supplier lists and formularies.

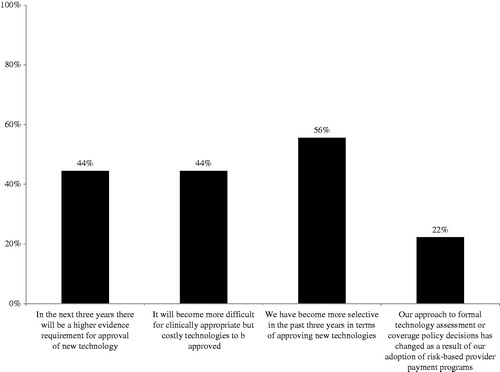

The bar for new medical technology adoption is being raised

Four of the nine respondents (44% of plans, 91% of lives) reported expecting a higher evidence requirement for the approval of new medical technologies in their organizations in the next 3 years. Five payers (56% of plans, 93% of lives) reported having become more selective in the past 3 years with regard to approving new technologies, citing either an increase in the demand for evidence, particularly with regard to comparative effectiveness, or increased cost sensitivity, including by providers who take on risk (‘There’s going to be less coverage of new technology unless there is a demonstration that it really is better than the present standard of care, and that demonstration in most instances will require some measurement of outcomes’) ().

Figure 5. Expectation for technology assessment process: Unweighted percentage of respondents.

Respondents generally described their processes for gathering, presenting, and assessing evidence for coverage as being highly standardized and methodical, and unlikely to change. All described their evidence review process as being supported by internal clinical and scientific staff (rather than outsourced to vendors) and led by a standing technology assessment committee composed of clinical staff. While respondents’ organizations typically review tens to hundreds of new technologies annually (the low cited was ∼40, and the high ∼400) covering a broad range of different technology types and modalities, they describe the evidence review process and the considerations for approving coverage as being essentially the same across different technology types (e.g., new orthopedic devices, implantable cardiovascular devices, new clinical diagnostic tests). For instance, the review process and considerations for devices brought to market under the PMA and 510(k) regulatory approval routes were described as the same by each of the respondents.

The process described typically follows two distinct steps: technology assessment focused on a highly structured scientific review of the available evidence and published literature; and a coverage decision reflecting the results of the technology assessment, as well as other inputs, including the actions of other payers, both public and private, and, in some cases, economic considerations. The stated importance and role of economic considerations in the coverage decision varied across respondents, with two (22% of plans, 23% of lives) reporting that ‘economic considerations never enter into technology coverage policy decisions’, three (33% of plans, 72% of lives) reporting that they ‘always’ do—‘new technologies must demonstrate economic value as well as clinical value’—and four (44% of plans, 5% of lives) reporting that they ‘sometimes’ do, either ‘if the clinical assessment is a “close call”’ or ‘if the economic impact is particularly large’. The coverage decision also typically includes decisions regarding any access and utilization management controls, such as prior authorization requirements.

Increasing levels of provider financial risk may challenge the traditional new technology access and adoption paradigm

Respondents were mixed in their views of the impact of increasing payer financial responsibility on new technology adoption decisions by providers. All but one of the respondents observed that they have seen providers become more selective in adopting new technologies, particularly when they are more costly in terms of their initial acquisition cost. All noted that, as providers become more at-risk financially for at least some of the costs of care, they expect they will become even more selective in the use of new technologies.

While most welcomed providers ‘thinking like payers’, not all respondents viewed this as a universally positive development. Several respondents noted that, in some cases, this could lead to providers not adopting a given new technology because of narrowly-defined cost measures (e.g., because the additional cost would come out of a given provider’s payment budget contract, or ‘silo’, while the savings or other benefits, such as in quality measurement, might not accrue to that provider, but to others in the continuum of care), while payers would want the technology to be used, because it could reduce total costs of care when viewed more globally. Several respondents noted that this development represented a potential reversal of the historical set of interests and behavior, in which providers typically advocated for coverage of a new technology as agents on behalf of patients, and may have been resisted by payers either on the basis of cost considerations, or because sufficient evidence was not yet available to support a universal access determination (‘You could have this kind of perverse thing where the providers, who in the past have been the biggest drivers of new technology because they weren’t paying for it and they liked it because it was easier to do their job, or they felt it was better, are probably now going to be the ones who are going to resist it, and it’s going to be the payers who are going to be pushing so that the quality metrics are better’).

Although several respondents noted that opportunities for competitive pricing on well-established technology was an element of their cost management strategy, only one identified new technology as a major cost driver (when major cost drivers were identified, they were inpatient hospitalizations and emergency department visits). All described the focus of their incentive programs as being the efficiency of the delivery system in general, rather than on controlling the cost of new technology specifically. Several noted that new technologies could be cost-saving when used efficiently to replace older, less efficient technologies (for example, the use of more advanced imaging when it replaced earlier-generation imaging and is used to alter treatment decisions), and when well-matched to the clinical needs of specific populations.

There is some variation in other policies regarding new technology. One-third of respondents reported that ‘new technology carve-outs’ (i.e., payments made separately from per diem or DRG-based reimbursement) were a feature in a significant share of their current hospital contracts; for the remaining two-thirds, they were not. With regard to investigational use, two-thirds of the respondents do not cover investigational use as a matter of policy, and most define investigational either by applying the five-part Blue Cross Blue Shield Association Technology Evaluation Center (TEC) requirements (i.e., has not received final approval for use from the appropriate government regulatory body; published scientific evidence is not yet available demonstrating conclusions with regard to the technology’s effects; published scientific evidence does not demonstrate beneficial effects on health outcomes outweighing harmful effects; published scientific evidence does not yet demonstrate the technology is as beneficial as any established alternatives; or technology is not attainable outside the experimental setting), or by adopting a Medicare determinationCitation18.

However, payers view their technology assessment and coverage determinations as independent from and complementary to providers’ utilization decisions

All respondents reported that ‘we plan to rely more on these types of provider payment incentives to control costs, but don’t see them as a substitute for technology reviews and coverage limitations; they each have a role to play’, finding such provider payment programs to be complements, rather than substitutes, for payer reviews and access limitations.

Although all but one of the respondents noted that they had already seen providers become more selective in their use of new technologies, and several welcomed a trend in which ACOs or other provider organizations are responsible for the total cost of care and for determining access to new technology, allowing payers to focus on underwriting rather than care management, all respondents nevertheless stated that they viewed their responsibility for reviewing the evidence for coverage decisions as unchanged and not reduced as a result (e.g., ‘We are never going to be at a point where we are going to simply rely on provider networks to control our own costs’). Several reasons were cited.

First, respondents noted their legal and contractual responsibility for determining coverage on behalf of their members, consistent with customer plan designs. In some cases, this could mean potential conflict between members, payers, and providers (e.g., when provider organizations accountable for managing the health and care costs of a population have policies and practices that conflict with or do not meet members’ demand for specific procedures, benefits, or technologies that are covered by payers).

Second, respondents noted they are ‘making coverage decisions that are not just solely for the benefit of providers in our risk pool, but for everybody’ and their processes are ‘driving business decisions for the totality’, recognizing that providers accept varying levels of financial risk, and that this likely will be true for some time. In addition, for some the dominant model remains a variant of fee-for-service rather than P4P or provider risk-based payment, so the relative importance of the ‘payer as gate-keeper’ remains high from a cost control point of view. This likely means that technology access and utilization controls will operate at both the payer level (through the process of technology assessment and coverage determination, which will result in some technologies not being covered or considered medically necessary if they are found to be no more clinically effective than alternatives already available, but more expensive) and at the provider level (through the utilization decisions of individual provider groups).

Third, respondents noted that, at least for the time being, and even under an ACO model which integrates hospital(s) and physician group(s) in a given geographic area, they believed individual providers are constrained in their perspective on the total cost of care. (‘They simply don’t have the view of the landscape that we do in terms of the ability to collect data to really understand total episode-of-care costs… our members are accessing care at multiple different sites, and they are mobile as well… patients now seek care all across the country and travel long distances to do so’.)

Discussion

The healthcare system is undergoing historic levels of change. Payers are grappling with the implementation of new mandates affecting fundamental business factors such as coverage, plan design, and medical loss ratios. At the same time, they have been experimenting over the past several years with a wide range of alternative P4P and risk-based payment models that alter their economic relationships with providers.

While not designed to be a statistically robust sample of commercial payers, interviews with leading payers covering a substantial population of commercial lives suggest experimentation with P4P and risk-based provider payment models is ongoing and may be increasing rapidly. Moreover, they depict a complex system in transition, with many unknowns regarding the ultimate implications of changes in economic incentives for payers, providers, employers, and patients. All of the payer representatives interviewed described their approach to provider payment as multi-faceted and evolving, in some cases very rapidly, with a growing emphasis on risk-sharing and P4P models and a substantial increase in the coverage of such programs planned over the next 3 years.

The short and longer-term impacts of shifts in the provider payment model on the organization, mix, quality, patient availability, and cost of care are largely unknown and it will likely be years before definitive findings are available. With regard to innovative medical technology, potential implications include:

Increased reimbursement uncertainty: Respondents described a diverse and evolving provider payment environment, with increasing levels of uncertainty and provider financial risk over time. Provider financial uncertainty may have two types of potential impacts on innovative medical technology: direct impacts on care management and technology choice as a result of increased financial risk and uncertainty (e.g., reduced or increased demand for different types of medical technology); and indirect impacts as a result of increased payment uncertainty and changes in provider demand being translated into greater uncertainty for innovators upstream, with a potential impact on the willingness of investors to deploy capital in investing in new device innovation.

Potential opportunity for certain technologies: At the same time, there may be enhanced opportunities for technologies that have the potential to improve quality performance (as measured by commonly used metrics), reduce measured costs, or both. Several respondents noted that, while payers are ‘going to be pickier about [covering] technology’, they also would have an interest in allowing financially at-risk provider groups to experiment with and access technology that might prove to be more efficient care choices for them. As another example, several respondents noted that technologies that allowed earlier discharge from the hospital or helped avoid hospitalizations altogether (e.g., through home monitoring) might become attractive to provider organizations at-risk financially for inpatient hospital costs.

Greater reliance by payers and providers on quality and financial metrics: The increasing importance of metrics, both financial and quality-related, in provider payment models means that metric selection and quality also will be increasingly important and may have far-reaching implications for care decisions. The metrics used to measure quality of care and patient outcomes and to calculate and allocate financial results in P4P and risk-based provider payment programs vary and are still in flux. Historically, quality metrics have tended to focus on process measures and financial metrics have tended to reflect shorter-term results (e.g., the cost of an inpatient stay). While episode-of-care-based payment may encompass a broader definition of the period of care (e.g., from pre-operative to post-operative rehabilitative care), longer-term results may still be excluded. In the case of many medical interventions, including procedures that involve devices, process quality standards and metrics may be absent, or the link between process standards and longer-term outcomes (e.g., patient quality-of-life, levels of pain, mobility, functional status, and engagement in physical and social activities months following an orthopedic procedure) may not be well-established. As a result, new metrics may need to be developed and validated, including quality metrics which would appropriately measure and ensure optimal patient access to and benefits from such interventionsCitation19.

A potential additional hurdle to the adoption of new technology: A shift towards greater provider financial risk may also entail a shift in the traditional technology ‘gatekeeper’ role, with both payers and risk-bearing providers exercising control over adoption of new technologies, whereas previously, payers typically assumed a gatekeeping role and providers a countervailing patient advocacy role with regard to access to new technology. All payers reported that ‘they planned to rely more on these types of provider payment incentives to control costs, but don’t see them as a substitute for [payers’] technology reviews and coverage limitations; they each have a role to play’. As a result, increased provider financial risk may result in an additional hurdle to the adoption of new technology following FDA clearance and payer coverage, with manufacturers needing to plan for provider group acceptance/coverage prior to individual provider utilization decisions, rather than a substitution of gatekeeping by providers for that of payers. With this development may come the opportunity (or need) for technology manufacturers to increase their interactions with ACOs or other provider risk-assuming groups (in addition to payers) over coverage. At the same time, it may also be the case that such provider groups may have more centralized control over technology adoption co-ordination and demand than has been the case (‘if technology companies feel they have a better mousetrap they may be selling directly to that physician group’).

Increased need for data analytics and evidence, including for coverage and utilization: Respondents noted the increased need and demand for evidence across the spectrum of care management and delivery, including outcomes studies, and analyses and evaluations at a patient and population-level of alternative care pathways. Manufacturers, providers, and payers who can collaborate in developing, evaluating, and applying such evidence will succeed in an increasingly uncertain environment.

Conclusion

The healthcare system faces unprecedented levels of change. A provider payment model shift is underway from ‘volume to value’, with payers actively experimenting with a range of alternative P4P and risk-based provider payment models. This shift holds promise to improve quality of care for patients, but may also have unanticipated effects on provider care delivery choice, patient access, and innovation incentives as economic incentives are altered, and established gatekeeper roles are challenged.

Transparency

Declaration of funding

The authors received financial support from the Advanced Medical Technology Association (AdvaMed) for this research. The analysis presented was designed and executed entirely by the authors, and any errors or misstatements are ours alone.

Declaration of financial/other relationships

GL & RM are employees of Analysis Group, Inc., a consulting company that has provided consulting services to both medical device and diagnostic companies, and commercial payers. GS is a former employee of Analysis Group, Inc. JME peer reviewers on this manuscript have no relevant financial or other relationships to disclose.

References

- CMS. Fast Facts – All Medicare Shared Savings Program and Medicare Pioneer ACOs. Centers for Medicare and Medicaid Services. 2014. http://www.cms.gov/Medicare/Medicare-Fee-for-Service-Payment/sharedsavingsprogram/Downloads/PioneersMSSPCombinedFastFacts.pdf. Accessed June 12, 2014

- Leavitt Partners. (2013, February 20). Accountable Care Organizations have more than doubled since 2011. Leavitt Partners, press release. 2013. http://leavittpartners.com/2013/02/accountable-care-organizations-have-more-thandoubled-since-2011/. Accessed 16 September 2014

- Accountable Care Organizations now serve 14% of Americans. Oliver Wyman, press release. 2013. http://www.oliverwyman.com/media/ACO_press_release(2).pdf. Accessed December 22, 2013

- Centers for Medicare and Medicaid Services, Medicare Demonstrations. http://www.cms.gov/Medicare/Demonstration-Projects/DemoProjectsEvalRpts/Medicare-Demonstrations.html. Accessed December 22, 2013

- Rosenthal MB, Landon BE, Normand SL, et al. Pay for performance in commercial HMOs. N Engl J Med 2006;355:1895-902

- Med-Vantage. 2010 National P4P Survey. 2011. http://www.imshealth.com/deployedfiles/ims/Global/Content/Solutions/Healthcare%20Analytics%20and%20Services/Payer%20Solutions/Survey_Exec_Sum.pdf. Accessed September 7, 2014

- Schneider E, Hussey P, Schnyer C. Payment reform: analysis of models and performance measurement implications. Santa Monica, CA: RAND Health, 2011

- Karve AM, Ou FS, Lytle BL, et al. Potential unintended financial consequences of pay-for-performance on the quality of care for minority patients. Am Heart J 2008;155:571-6

- Wharam JF, Paasche-Orlow MK, Farber JN, et al. High quality care and ethical pay-for-performance: a Society of General Internal Medicine policy analysis. J Gen Intern Med 2009;24:854-9

- Kohn A. Why incentive plans cannot work. Harv Bus Rev 1993;71:54-63

- Porter M, Teisberg E. Redefining health care: creating value-based competition on results. Boston, MA: Harvard Business School Press, 2006

- Mehrotra A, Damberg CL, Sorbero ME, et al. Pay for performance in the hospital setting: what is the state of the evidence? Am J Med Qual 2009;24:19-28

- Greene SE, Nash DB. Pay for performance: an overview of the literature. Am J Med Qual 2009;24:140-63

- Christianson JB, Leatherman S, Sutherland K. Lessons from evaluations of purchaser pay-for-performance programs: a review of the evidence. Med Care Res Rev 2008;65(6 Suppl):5S-35S

- Petersen LA, Woodard LD, Urech T, et al. Does pay-for-performance improve the quality of health care? Ann Intern Med 2006;145:265-72

- Werner W, Kolstad J, Stuart E, et al. The effect of pay-for-performance in hospitals: lessons for quality improvement. Health Aff 2011;30:690-98

- Damberg C, Sorbero M, Lovejoy S, et al. Measuring success in health care value-based purchasing programs. Santa Monica, CA: RAND Health, 2014

- Blue Cross and Blue Shield Association Technology Evaluation Center, Technology Evaluation Center Criteria. http://www.bcbs.com/blueresources/tec/. Accessed December 22, 2013

- Schneider E, Hussey P, and Schnyer C. Payment Reform: Analysis of Models and Performance Measurement Implications. Santa Monica, CA: RAND Health, 2011