?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We study the temporal evolution of going-concern reporting from 2004 to 2013 and test whether sanction risk is related to the likelihood of a going-concern opinion using samples of privately held firms. In 2009, the Supervisory Board of Public Accountants (SBPA) in Sweden started to issue significantly more going-concern-related disciplinary sanctions, and we test whether and how auditors at different audit firms adjust their reporting practices (Type I and Type II errors) in response to the increased sanction risk. Our findings reveal that auditors are more likely to issue going-concern opinions to bankrupt and non-bankrupt firms when the sanction risk is higher, suggesting that sanction risk is positively associated with conservatism in auditors’ reporting. Furthermore, we find that auditors at Big 4 firms alter their reporting to conservative more than non-Top 7 firms when sanction risk increases. Finally, results on the informativeness of going-concern opinions indicate that a going-concern opinion increases the bankruptcy probability during both the lower and higher sanction risk periods, but the impact is higher under the higher sanction risk period.

1. Introduction

The auditor’s abilities to warn the public (i.e. users of audited financial statements) about future financial problems by including the going-concern opinion is a fundamental part of auditing. This requirement is specified in the International Standards of Auditing (ISA 570). The inability to include a going-concern opinion when warranted (i.e. Type II error) has economic consequences for users (Barnes Citation2004) and clients but may also lead to disciplinary sanctions for auditors if such failure is considered to reflect sub-standard auditor reporting.Footnote1 Given the importance of an adequate application of auditing standards to ensure audit quality, surprisingly little is known about how the sanction risk impacts reporting practices. A deeper understanding of how going-concern reporting practices develop under different levels of sanction risk is valuable to find ways of assessing the efficiency and effectiveness of regulatory interventions. The application of ISA 570 is especially interesting to investigate because it involves a high degree of subjectivity, controversy, and complexity.

The first purpose of this study is to examine going concern-reporting practices under both low(er) and high(er) sanction risk by using samples of bankrupt and non-bankrupt privately held Swedish firms. We conduct a large-scale study focusing on going-concern reporting practices in Sweden from the introduction of the going-concern standard in 2004 until 2013 and analyse whether and how an upward shift in sanction risk impacts reporting behaviour. Specifically, we examine whether the propensity to issue going-concern opinions for companies that subsequently enter into bankruptcy (i.e. related to Type II errors) and for those that do not (i.e. related to Type I errors) changes when sanction risk increases.[1] From 2009 and onwards, the Supervisory Board of Public Accountants (SBPA) issued significantly more going-concern-related disciplinary sanctions to auditors than in the period 2004–2008 (see appendix for details). An increase in the issuing of going-concern opinions for bankrupt and non-bankrupt firms would reflect more conservative reporting.

In Sweden, the litigation risk for auditors is low (Choi et al. Citation2008),Footnote2 and furthermore, the litigation risk is lower in private firms than in public firms (Hope and Langli Citation2010). Therefore, the cost of erroneous going-concern reporting is closely related to the risk of disciplinary sanctions in our setting. Hope and Langli (Citation2010) study the association between (abnormal) audit and non-audit fees and the propensity to issue going concern opinions in the low litigation setting of Norway. They find no evidence of an association between the fee measures and going concern reporting. We expand the study by Hope and Langli (Citation2010) by analysing how going concern reporting in a low litigation risk environment is impacted over time by changes in the sanction risk. The Supervisory Board of Public Accountants (SBPA)Footnote3 oversees auditors, issues reprimands (less severe) and warnings (more severe) and may ultimately withdraw their licences (most severe). We assume that auditors consider (new) information about the risk of being caught employing sub-standard going-concern reporting practices and that reporting practices reflect the sanction risk.

Because sanction costs are different for various types of audit firms because of differences in reputation concerns (DeFond and Zhang Citation2014, Sundgren and Svanström Citation2017), auditors in large audit firms may report differently from small audit firms under both low and high sanction risk. They may also respond differently to changes in sanction risk. Our second purpose is, therefore, to analyse going-concern reporting practices of different sized audit firms when considering the sanction risk.

An extensive body of research has examined how audit quality is related to reputation and litigation concerns (see DeFond and Zhang Citation2014 for a review). However, most studies examining auditors’ responses to the risk of litigation or regulatory sanctions focus on audit fees, and few attempts have been made to understand how regulatory sanction risk influences reporting behaviour. Important exceptions are Carson et al. (Citation2019) who identify changes in going-concern reporting in Australia under increased regulatory scrutiny and DeFond et al. (Citation2018) who conclude that non-Big 4 audit offices in the US are more likely to issue a first-time going-concern opinion when they have a greater awareness of SEC enforcement actions. Furthermore, Firth et al. (Citation2014) examined whether sanctioned auditors in China change their going-concern reporting practices in the post-sanctioned period and find support for more conservative reporting after the sanction for the sample of risky clients.

There are three important differences between these studies and our study. First, we study going-concern reporting practices in privately held firms. Overall, there is limited knowledge about auditor reporting practices in private firms, and our study contributes with new evidence. The Swedish setting allows us to contribute to this area of research because audits are performed in many private firms following the statutory audit requirement and data (from the audit report) is publicly accessible. Second, we specifically study (changes in) the impact of going-concern-related sanction risk on going-concern reporting. This is because this sanction risk may cause a stronger impact on going-concern-reporting practices than the risk of receiving any type of enforcement or sanction. Finally, the consequences of a sanction may vary with audit firm size, and we, therefore, analyse whether and how Big 4, the next tier of auditors (i.e. Grant Thornton, BDO, and Mazars) and non-Top 7 audit firms adjust their reporting practices when the sanction risk changes. Overall, the findings in our study have implications for the effectiveness and relevance of regulatory sanctions to change auditor behaviour. The fact that auditors revise their reporting behaviour when the sanction risk increases imply that auditor oversight is relevant and effective in impacting audit practice (at least to a degree).

This study proceeds as follows. Section 2 presents the Swedish institutional setting, and in Section 3, we review related literature, and develop our hypotheses. In Section 4, we present the model and our sample. Section 5 contains the main empirical results of the study, and Section 6 concludes.

2. Institutional setting

National auditing standards (Revisionsstandard, RS) that were mainly based on ISA were first introduced in Sweden in 2004,Footnote4 which meant that a going-concern standard similar to ISA 570 in all relevant respects was adopted at that time. The standard requires an auditor to consider the appropriateness of the management’s use of the going-concern assumption and to evaluate whether material uncertainties exist as to the entity’s ability to continue as a going-concern. If there are significant doubts on this point, appropriate reporting will depend on the circumstances and range from an explanatory paragraph to an adverse opinion. However, regardless of what the management reports, in the audit report, an auditor should draw attention to going-concern uncertainty (RS 570 §§33–34, ISA 570 §§21–24).Footnote5 The normal period for the auditor to consider is the same as that for the management, typically 12 months from the end of the accounting year (RS 570 §18, ISA 570 §13).

Before 2004 and the implementation of ISA based standards in Sweden, auditors had to follow the guidelines published by the Institute of Public Accountants. The most important recommendation at this time was the so-called ‘audit process’ (Sw. revisionsprocessen). By and large, these guidelines were in line with IFAC standards (FAR Citation1999, p.80). However, despite the section on audit reporting (Section 2.5) being the most extensive, it did not include anything about the reporting of going-concern uncertainty, even though a company’s management needed to prepare its financial statement following the going-concern assumption. In principle, though, the financial reporting requirement suggested that if an auditor were unable to agree on the going-concern assumption, this difficulty would then be included in the audit report. This step was, however, not done in practice.Footnote6 Auditors were required, and still are required to, report deviations from the Company Act related to liquidation rules—such as the management’s failure to present a balance sheet for liquidation purposes when half of the shareholders’ equity had been consumed (Ch. 25 §13).

In Sweden, the risk of litigation against auditors is low (Choi et al. Citation2008), and the risk is furthermore lower in the private client segment than for audits in public clients (Hope and Langli Citation2010). However, the SBPA regularly issues disciplinary sanctions against certified auditors who perform below the standards.Footnote7 Importantly, the SBPA does not issue guidelines. SBPA is a governmental authority under the Ministry of Justice, which performs quality control investigations, both on its initiative but also after having received complaints, to ensure the level of audit quality. Its investigations are regular quality inspections and inspections directed at high-risk groups. For practical reasons, the inspection of auditors without public assignments has partly been delegated to the professional institute, FAR. FAR advises auditors on reporting standards and practices, while SBPA has a limited capacity to assist with guidance. The formal tasks of the SBPA and the procedures for inspections in Sweden have remained similar during the study period.Footnote8 The current oversight system with independent national audit regulators supervising auditors and issuing disciplinary sanctions against auditors has been the global norm for about 15 years (IFIAR Citation2019, p. 3, Accountancy Europe Citation2018).Footnote9 The European Commission (EC) introduced independent oversight over financial reporting and auditing in its revised Eighth Directive of 2006 (Citation2006/Citation43/EC).

The possible sanctions based on the degree of seriousness are (i) a reprimand, (ii) a warning, and (iii) the withdrawal of licence. In the period 2004–2013, 522 sanctions were issued against about 13% of certified auditors. The total number of disciplinary cases opened and sanctions issued have been (relatively) constant during the study period (see ). The same stable trend can be noted for the total number of quality control inspections performed by SBPA. While the annual number of inspections performed by FAR varies substantially between the individual years, the figures for a 2-year period were more stable.Footnote10 It should be noted that until 2016, no fine was related to these sanctions. However, Sundgren and Svanström (Citation2017) show that reprimands and warnings are associated with salary reductions in Big 4 audit firms, thus suggesting that (Big 4) auditors are motivated to avoid sanctions.

Table 1. Disciplinary sanctions issued by the Supervisory Board of Public Accountants, 2004–2013.

While the total number of sanctions has remained relatively stable during the study period (2004–2013), very few going-concern-related sanctions were issued up until 2009, after which they started to be issued relatively frequently (see and Appendix 1). Only one disciplinary sanction relating to going-concern-reporting was issued in the 2004–2008 period. This number increased to 37 in the 2009–2013 period.Footnote11 The average number of going-concern-related sanctions per year in the latter period is 7.2, with a minimum of 3 (in 2011) and a maximum of 12 (in 2013) (see Appendix 1). Noticeable is also that only two of the 37 going-concern-related sanctions are reprimands, which indicates that SBPA considers the failure to include a going-concern opinion to be serious misconduct.

The number of sanctions issued relating to going-concern reporting indicates a clear shift in the sanction risk and suggests that from 2009 and onwards SBPA paid close attention to this issue. Auditors, at least in the larger audit firms, are well aware of the content of a disciplinary sanction. They arrange meetings to discuss the outcome of disciplinary cases and to decide how to improve and harmonise procedures, routines and second opinion procedures to minimise the risk of sanctions being issued.Footnote12

Up until November 2010, all limited liability companies in Sweden had to be audited.Footnote13 Consequently, the vast majority of all audit assignments were conducted in private companies and, typically, in small ones. In supplementary analyses, we test if going-concern practices were impacted by the abolished statutory audit requirement. The Swedish audit market consists of over 900 audit firms and includes distinct categories of audit firms. The Big 4 audit firms dominate the market and employ about 50% of all certified auditors. Grant Thornton, BDO, and MazarsFootnote14 follow in rank order after the Big 4 audit firms. The group of non-Top seven audit firms includes a wide range of firms, including many sole proprietors and firms with only a few certified auditors, as well as some larger firms.Footnote15

3. Literature and development of hypotheses

The assessment of whether a company is a going-concern involves judgment and has been described as one of the most complex tasks in auditing (Louwers Citation1998). In only the most extreme cases can the auditor be certain. In all other cases, there will be a cut-off or threshold to represent ‘reasonable belief’ (Barnes Citation2004). Therefore, the translation of the ISA 570-based reporting standard into day-to-day audit activities was probably not a straightforward process, but involved various initial interpretive problems regarding how the standard should be applied in existing practice.

Auditors have incentives not to include language in the audit report that may negatively impact the relationship with a client, such as a going-concern opinion (Carson et al. Citation2019). For example, it has been argued that a going-concern opinion may become a self-fulfilling prophecy (e.g. Gaeremynck and Willekens Citation2003). Also, there is an increased risk that a going-concern opinion leads to the client switching to another auditor (Lennox Citation2000, Lu Citation2006). Therefore, auditors are likely to be indulgent with their clients and apply a high threshold for material uncertainties to avoid client losses (from bankruptcies and/or auditor switching). On the other hand, auditors face the risk of litigation or disciplinary sanctions for failing to include a going-concern opinion when warranted.

The threshold for when there is substantial doubt about the ability for the entity to continue its operations, thereby warranting the inclusion of the going-concern paragraph, can be expected to be closely related to the cost associated with erroneous reporting (i.e. Type 1 and Type II errors). While there are costs associated with both types of errors, the Type II error is the principal concern of regulators and Supervisory Bodies (Geiger and Raghunandan Citation2002, Read Citation2015).

3.1. Going-concern reporting and sanction risk

In a low litigation risk setting like Sweden (Choi et al. Citation2008), the risk of regulatory sanction (i.e. level of enforcement) is the main factor impacting the cost associated with failing to report following the standard. Sanctions are likely to impact auditor’s reputation negatively (DeFond and Zhang Citation2014), and the most severe cost or consequence of sanctions are losing the certification. Auditors are, therefore, expected to apply strategies to minimise the risk of receiving a sanction. This procedure would involve paying close attention to the actions taken by the SBPA related to the ISA 570 standard, that is, carefully analysing the frequency and type of going-concern-related disciplinary sanctions being issued. If the risk of receiving a sanction is assessed low (high), auditors are likely to apply a high (low) threshold for inclusion of the going-concern opinion.

During 2005–2008, auditors receive some, but limited, information about the sanction risk from the SBPA. The available information at hand would suggest a low sanction risk in this period. In 2009, when there is an increase in the frequency of ISA 570-related sanctions issued by the SBPA (see and Appendix 1 for details), the sanction risk increases, and consequently, auditors may need to adjust their reporting practices accordingly. When more sanctions are published, auditors can no longer underestimate the sanction risk and rely on previous practices because the cost of such behaviour is then simply (too) high.

Auditors can be expected to modify going-concern reporting practices in response to the increased sanction risk starting in 2009. Ceteris paribus, a general increase in the frequency of going-concern opinions (both for companies that subsequently enter bankruptcy and those that can continue the operations) reflects conservative reporting, and such a reporting change is expected to lower the risk of receiving a disciplinary sanction (Carson et al. Citation2019) and can be considered an efficient response when the sanction risk increases.Footnote16 We, therefore, formulate the following two hypotheses:

H1a: The propensity to correctly include a going-concern opinion increases with sanction risk.

H1b: The propensity to incorrectly include a going-concern opinion increases with sanction risk.

3.1.1. Related empirical evidence

A review of the existing research on public oversight provides some but limited guidance on the impact of sanctions on auditor reporting. Sundgren and Svanström (Citation2017) found no evidence to suggest that receiving a disciplinary sanction had an impact on the sanctioned auditors’ subsequent reporting behaviour. Three different samples were used in Sundgren and Svanström (Citation2017) to study any potential post-sanction effect on auditors’ salary, loss of clients, and auditor reporting.Footnote17

It could well be that the risk of sanctions has a general impact on auditors’ reporting behaviour even if there is not ‘a sanctioned auditor effect’. Prior evidence shows, however, a salary effect, in that sanctioned auditors at Big 4 audit firms earn less after the sanction than before it, which suggests that there are mechanisms in place in those firms that penalise audit failures (Sundgren and Svanström Citation2017). Carson et al. (Citation2019) studied a sample of financially distressed Australian publicly listed companies from 2012 to 2014 and found an increase in the going-concern opinions issued. The increase could not be explained solely by changes in client risks but was instead attributed to increased regulatory scrutiny (i.e. inspection risk). DeFond et al. (Citation2018) document that non-Big 4 audit offices in the US are more likely to issue a first-time going-concern opinion when they have a greater awareness of SEC enforcement actions thus indicating that auditor adjust to more conservative reporting when they are more aware of inspection (and sanction) risks. Firth et al. (Citation2014) find that Chinese auditors who are sanctioned (for failure to detect financial statement fraud) during the 1996–2007 period, report more conservatively for risky listed clients after the sanction. However, they find no such effect for non-risky listed clients. In a related study, Kaplan and Williams’ (Citation2013) investigate the impact of litigation risk on auditors’ going-concern reporting in a sample of US-listed firms. They find a significant positive association between auditors’ ex-ante litigation risk and the propensity to issue a going-concern report.

There is a related literature that studies the impact of sanctions or deficient oversight reports on client losses. Sundgren and Svanström (Citation2017) study the effect of disciplinary sanctions on loss of clients in a Swedish private firm setting. The analyses did not reveal any significant association between receiving a disciplinary sanction and the loss of clients thus indicating that clients are either unaware about sanctions or do not regard this information to motivate an auditor change. This result does not however imply that auditors do not need to care about sanctions since sanction can risk impacting their salary development (Sundgren and Svanström Citation2017) and in a worse could case lead to the withdrawal of her license. While Sundgren and Svanström (Citation2017) focus on different effects for the auditor (i.e. salary, loss of client, reporting) of actually receiving a sanction, this study instead tests whether and how a general increase in the going concern sanction risk impacts the going concern reporting of auditors at small and large audit firms respectively. The two studies are performed in the same institutional setting and uses (to a minor extent) the same data on going-concern reporting, but the aim and focus of the studies are (very) different, i.e. ‘sanctioned auditor effect’ versus ‘going concern reporting practices when sanction risk increases’.

Abbott et al. (Citation2013) use PCAOB inspection reports and find that clients of GAAP-deficient auditors are likely to change to non-deficient auditors to signal (high) audit quality. Daugherty et al. (Citation2011) examine PCAOB inspected auditors’ involuntary and voluntary client losses in the period following a deficient PCAOB report. They document that auditors with deficiency reports are involuntarily dismissed by clients and replaced by inspected auditors without deficiencies. Furthermore, auditors with deficiency reports voluntarily resign from their publicly listed clients and cease to be registered with the PCAOB. These results indicate that negative inspection outcomes matter for publicly listed audit clients in the US.

3.2. Audit firm size, sanction risk, and going-concern reporting

The environment in which the audit takes place is part of the context that shapes auditors’ incentives and reasoning for interpreting and applying auditing standards and deciding on reporting behaviour (Nobes and Parker Citation2010, Knechel et al. Citation2013). Large audit firms (typically measured by Big 4 firms) differ in many respects from small audit firms (typically measured by non-Big 4 firms) (see DeFond and Zhang Citation2014, Knechel et al. Citation2013, Francis Citation2011 for reviews). Evidence indicates that there are differences regarding incentives to preserve reputation (Khurana and Raman Citation2004), client characteristics (Ramirez Citation2009), access to networks (Lander et al. Citation2013), and use of audit procedures (Blokdijk et al. Citation2006). Consistent with systematic differences between the firm types and by using data from private firms in Sweden, Sundgren and Svanström (Citation2013) find that the likelihood of receiving a disciplinary sanction is significantly lower if being employed by one of the six largest audit firms in Sweden than a non-Top 6 audit firm.Footnote18 Furthermore, both Sundgren and Svanström (Citation2014) and Tagesson and Öhman (Citation2015) report that Big 4 auditors are more likely to issue going-concern opinions for samples of bankrupt companies (i.e. fewer Type II errors). These findings support quality and reporting differences between large and small audit firms also in the private firm segment of the Swedish audit market.

An increase in sanction risk may (or may not) differently impact reporting behaviour of auditors in large and small audit firms. The arguments for expecting a stronger sanction effect for auditor reporting in large audit firms are primarily that an increased sanction risk is more expensive, in terms of reputational loss, for large audit firms compared to small audit firms (Palmrose Citation1988, Callaway Dee et al. Citation2011, Lawrence et al. Citation2011). The cost related to Type II errors in particular can be expected to be higher for large audit firms compared with small audit firms, due to differences in reputational loss. Footnote19

On the other hand, auditors at larger audit firms can already under low sanction risk be expected to apply a lower threshold for inclusion of the going-concern opinion. They may, therefore, need a relatively smaller adjustment of their reporting practices than auditors at small audit firms when sanction risk increases.Footnote20 As long as the sanction risk is assessed to be low, low costs are expected for Type II errors, and auditors at small firms have few incentives to include the going-concern opinion.Footnote21 However, these incentives will increase when erroneous reporting becomes costlier, thus resulting in the possibility of finding even a greater sanction effect in smaller audit firms than in larger audit firms. Based on the different arguments presented in the above, we formulate the following non-directional hypothesis:

H2: The impact of sanction risk on the (magnitude of the) adjustment in the propensity to issue going-concern opinions is unaffected by audit firm size.

4. Model and sample selection

4.1. Empirical models

We use the following regressions to test the hypotheses:

(1)

(1)

(2)

(2)

All variables are defined in . The models are estimated separately for bankrupt and non-bankrupt firms to measure how sanction risk influences Type I and Type II errors respectively. A Type I error is defined as a situation when a firm receives a going-concern opinion but survives.Footnote22 A Type II error occurs when a firm enters into bankruptcy without receiving a going-concern opinion. We use the audit report in the last financial statements before bankruptcy (prepared more than three months and less than twelve months before bankruptcy). The dependent variable GCD takes the value one if the audit report includes a going-concern opinion; otherwise, it is zero.

Table 2. Variable definitions.

There is no well-accepted measure of sanction risk. In the previous literature, some studies use the term inspection risk scrutiny (Glover and Prawitt Citation2013, Carson et al. Citation2019). It has been described as auditors’ additional effort, attention, and procedures that are driven by anticipated inspection. Inspection risk is fundamentally similar to the risk we investigate. Carson et al. (Citation2019) use a time-specific indicator to identify periods with a high quantity of regulatory inspection activity and the number of inspections as measures. Inspired by this research, we measure the sanction risk with a variable taking the value one for the year 2009 and afterwards (SBPA2009) and with the number of going-concern-related sanctions issued by SBPA in the corresponding year (SANCTIONS). The difference from Carson et al. (Citation2019) is that we base the measurement on inspections resulting in going-concern-related disciplinary sanctions and not on the total number of inspections performed in the period. We believe that our measure is a more precise indicator of the sanction risk of sub-standard going-concern reporting. The rationale for the use of the indicator variable is that there was only one going-concern-related sanction in 2004–2008, and there is a sharp increase in the number of sanctions starting from 2009 (see and the Appendix).

We include BIG4 (PwC, KPMG, EY, and Deloitte), and NEXT3 (Grant Thornton, BDO, and SET Mazars) to study whether the reporting in Top 7 audit firms differs from that in smaller audit firms (i.e. non-Top 7).Footnote23 Hypothesis 2 focuses on the impact of increased sanction risk on going-concern reporting. To test that hypothesis, we interact BIG4 and NEXT3 with the sanction risk measures in model (2).

The models include the following control variables. We expect the probability of a going-concern opinion to be associated with the financial conditions of the firm. Following Reynolds and Francis (Citation2000) and other studies, we include LOSS and the probability of bankruptcy to control for the financial conditions (PROBZ). We measure the probability of bankruptcy by using Shumway’s (Citation2001) estimate of Zmijewski’s (Citation1984) model.Footnote24 Prior studies also suggest that the time between the balance sheet date and the bankruptcy filing is negatively associated with the likelihood of a going-concern opinion (e.g. Li Citation2009). We include DELAY as the measure in regressions estimated on the sample with bankrupt firms.

Slightly less than half of the firms in the sample were using the balance sheet date of 31st December. As studies suggest that a busy-season effect might emerge from this concentration in auditees’ balance sheet dates (e.g. Knechel and Payne Citation2001, Sweeney and Summers Citation2002), we include the indicator variable BUSYSEASON. Furthermore, it has been found that the likelihood of a going-concern opinion depends on the size of the company (e.g. Li Citation2009, Geiger et al. Citation2014, Carson et al. Citation2019). The association is typically assumed to be negative because large companies have more resources to avoid bankruptcy (Mutchler et al. Citation1997), or because large companies have more negotiation power with auditors in the opinion decision process (McKeown et al. Citation1991). On the other hand, auditors have more reputation at stake when auditing larger companies and may therefore be more willing to include a going concern opinion for these companies. We include LNASSETS to control for this effect. Studies suggest that the agency conflict between the firm and debt holders creates a demand for auditing in privately owned firms (Knechel et al. Citation2008). We use an indicator variable, taking the value one if the firm has bank debt as the measure (BANKDEBT).

There are macroeconomic conditions that may influence auditor reporting. Prior studies suggest that audit risk increased with the onset of the global financial crisis that started in 2009. Auditors would, therefore, be more likely to issue a going-concern opinion under the financial crisis, and Xu et al. (Citation2013) and Geiger et al. (Citation2014) present empirical evidence consistent with this prediction. The financial crisis hit the Swedish economy relatively hard in 2009, although the economy recovered very quickly. The real GDP growth rate in the years 2008, 2009, and 2010 were 0.6%, −5.0%, and +6.6% respectively. To control for the possibility that the financial crisis increased the propensity to issue going-concern opinions, we include the indicator variable CRISIS in the model. This variable takes the value one if the balance sheet date of the company ends in the second half of 2008 or 2009.Footnote25

Furthermore, firms that are members of a group may receive support from other group firms, which positively influences the likelihood of survival (Beaver et al., Citation2019). It is possible that parent companies signal the ambition to financially assist a subsidiary in financial distress (or vice versa), thus decreasing the likelihood that the auditor issues a going concern opinion.Footnote26 We include indicator variables for SUBSIDIARIES and PARENTS to control for this. The former takes the value one if the firm is a subsidiary to a Swedish or foreign firm and the latter if the firm is a parent in a group. Firms that do not belong to a group are in the comparison category. Finally, we include industry indicator variables as controls for the effects of industry since the auditor’s going concern assessment may be more (or less) difficult in certain industries. The industry variables are measured at the two-digit level, and there are twelve (eleven) industry indicators in regressions run on bankrupt (non-bankrupt) firms.

4.2. Sample

To test our predictions, we use a sample of 7,143 privately held firms that filed for bankruptcy within 12 months of the balance sheet date and a matched sample with 7,143 non-bankrupt private firms. Both samples span the 2004 to 2013 period. The financial data is from the Serrano database, which also includes an indicator for unclean audit reports. From the Retriever database, we retrieved PDF versions of the audit reports for firms that had received unclean reports and checked manually whether those reports included a going-concern opinion.

We first identified all firms in Serrano that filed for bankruptcy three to twelve months after the balance sheet date.Footnote27 We next excluded firms with publicly traded parents, firms that filed for bankruptcy or liquidation before the date when the audit report was signed, and firms for which any of the explanatory variables were missing. We also excluded 108 firms for which no pair could be found, leaving 7,143 firms to analyse further.

The sample of non-bankrupt firms is composed as follows. Firstly, for each bankrupt firm we searched for a privately held non-bankrupt firm of the same size,Footnote28 from the same industry, for the same year and with the same type of financial statements (i.e. consolidated if the parent in a group and separate financial statements if not a parent).Footnote29 Secondly, among the possible pairs, we choose the non-bankrupt firm with the closest to the same bankruptcy probability (PROBZ).Footnote30 We do not allow the same firm to be the pair for two or more bankrupt firms. The non-bankrupt firms were identified from the Serrano database. Most of the matched pairs have virtually identical bankruptcy probabilities: the absolute value of the difference in PROBZ between the bankrupt and non-bankrupt firm is smaller than 1.28% for 95% of the firms in the sample.Footnote31

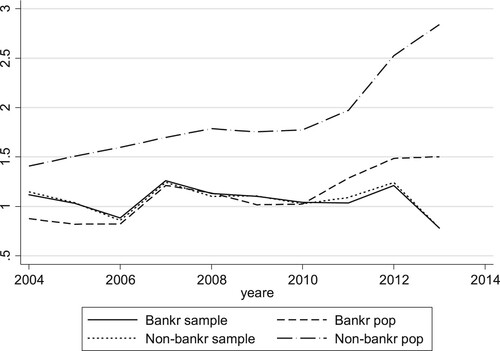

compares the size and number of firms in the sample with all firms in Serrano.Footnote32 It shows that our sample includes two-thirds (7,143 / 10,611) of the bankrupt firms with a balance sheet date three to twelve months before the bankruptcy filing.Footnote33 Furthermore, the table shows the mean (median) assets of the bankrupt firms are SEK 7.448 (1.079) million. The corresponding numbers for all bankrupt firms are SEK 10.030 million and SEK 1.100 million respectively (EUR 1 = SEK 8.85 as of 12/31/2013). shows that the mean (median) assets of the non-bankrupt firms are SEK 12.092 (1.087) million, that is, they are on average slightly larger than the bankrupt firms in the sample. shows median assets of bankrupt and non-bankrupt firms in the sample and population by year. It shows that the bankrupt and non-bankrupt firms in the sample are of similar sizes and that the bankrupt firms in the sample are of a similar size as bankrupt firms in the population. Thus, the overall conclusion that can be made from and is that the sample mirrors the population fairly well.

Figure 1. Median assets of bankrupt and non-bankrupt firms in the sample and the population. Notes: The scale of the y-axis is assets in Million Swedish krona. The median assets for the population (Bankr pop, Non-bankr pop) is for all firms in Serrano database after the exclusion of publicly traded firms and firms with no audit report data. The median assets of bankrupt firms are from financial reports 3 to12 months before the firm went bankrupt.

Table 3. Size of firms in the sample in comparison with all firms in the database.

5. Results

5.1. Descriptive statistics

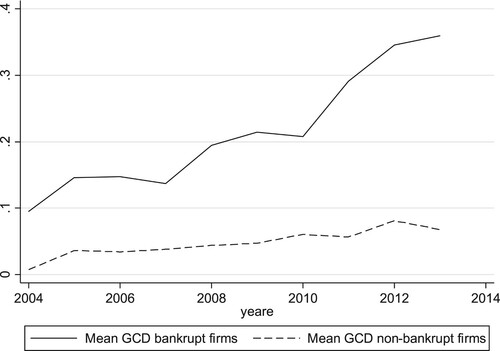

presents the proportion of going-concern opinions by year. It shows that the proportion of going-concern opinions are low in the first years after the introduction of the ISA 570 equivalent going-concern standard but increases with time passed since the effective date. The proportions of firms with a going-concern opinion prior to bankruptcy are 9.54% in 2004, 14.60% in 2005, and 14.73% in 2006. In 2009 and 2010, the proportions are 21.48% and 20.78% respectively. In 2012 and 2013, the proportions are significantly higher at 34.58%, and 36.00 shows that the proportions of firms with a going-concern opinion before bankruptcy are considerably higher among firms with a Big 4 or Next 3 auditor than among firms with a non-Top 7 auditor. graphically displays the increase in going-concern opinions for bankrupt and non-bankrupt firms.

Figure 2. Average proportion of bankrupt and non-bankrupt firms with a going concern opinion 2004–2013. Note: The scale of the y-axis is the fraction of firms with a going-concern opinion.

Table 4. Proportion of going-concern opinions by year.

We continue with a few observations related to the proportion of firms with a going-concern opinion before 2009 and from 2009 to 2013. The overall averages before and after 2009 are 21.21% and 33.71% for firms with a Big 4 auditor. The corresponding averages are 20.44% and 28.80% for firms with a Next 3 and 11.15% and 20.63% for firms with a non-Top 7 auditor. These numbers show that the proportions of bankrupt firms with a going-concern opinion is lower before 2009 irrespective of audit-firm size. The absolute increase in the proportion of firms with a going-concern opinion is 12.50% for Big 4 (33.71% minus 21.21%). The corresponding percentages are 7.96% and 9.48% for Next 3 and non-Top 7 respectively. Thus, in absolute terms the proportion of firms with a going-concern opinion increased more for firms with Big 4 auditors than non-Big 4 auditors. However, the relative increase for non-Top 7 firms, calculated as the proportion of firms with a going-concern opinion after 2009 (20.63%) divided by the proportion of firms with a going-concern opinion before 2009 (11.15%) is 85.02%. The corresponding percentages for firms with a Big 4 and Next 3 are 58.96% and 40.90% respectively. Thus, in absolute terms the impact of increased sanction risk is highest for firms with a Big 4 but in relative terms the impact is highest for firms with a non-Top 7 auditor.

can also be used to learn about the number of bankruptcies per year and the auditors of failing firms. First, it shows that the number of bankruptcies peak in the financial crisis years 2008 and 2009. However, the number is high still in 2010 but is after that lower.Footnote34 Around 31.56% (2,257 / 7,143) of the bankrupt firms in the sample are audited by a Big 4 auditor. The corresponding percentages for Next 3 and non-Top 7 are 13.06% and 55.34% respectively. For comparison, Big 4 firms audit 36.16% of all firms in the 2005 to 2013 period. The corresponding percentages for Next 3 and non-Top 7 are 12.37% and 51.47% respectively, suggesting that Big 4 firms audit a proportionally smaller fraction and non-Top 7 audit a proportionally larger fraction of bankrupt firms. This indicates Big 4 firms emphasise clients’ distress risk more than non-Top 7 firms when they consider which clients to accept. Alternatively, it is possible that firms switch to non-Top 7 firms when they become financially distressed.

, Panel B, presents figures for non-bankrupt firms. A first observation that can be made is that the ratio of firms with a going-concern opinion is considerably lower than for the bankrupt firms. While the overall average for the bankrupt firms is 20.41%, it is only 4.75% for non-bankrupt firms. This result indicates that auditors use client-specific information beyond what is incorporated in bankruptcy probabilities as they decide whether to issue a going-concern opinion or not. Furthermore, the figures suggest the proportion of non-bankrupt firms with a going-concern opinion has increased over time, indicating that Type 1 errors have increased and that auditors have become more conservative in their going-concern reporting.

The formulation of auditors’ going-concern reporting depends on the adequacy of the disclosures in the financial statements of matters that may cast doubt on the ability to continue operations. The auditor issues an emphasis of matter opinion if the disclosures are adequate. 90.88% (1325 / 1458) of the bankrupt firms with a going-concern opinion received an emphasis of matter opinion (not reported in tables). Furthermore, 6.04% received a qualified opinion and 3.09% an adverse opinion or disclaimer. The corresponding percentages for the non-bankrupt firms are 87.61% (297 / 339), 7.67%, and 4.72% respectively.

, Panel A, presents averages of the explanatory variables. It shows that 17.75% of the bankrupt firms without and 19.75% of the bankrupt firms with a going-concern opinion are subsidiaries. Furthermore, 5.54% of the firms without a going-concern opinion and 7.68% of the firms with a going-concern opinion are parent companies. The fraction of subsidiaries is slightly higher in the non-bankrupt sample.

Table 5. Descriptive statistics.

presents Pearson product-moment correlations and Spearman rank correlations. The Pearson correlation between SBPA2009 and SANCTIONS is 0.848. These variables are alternative proxies of sanction risk and are not included simultaneously in the regressions. There are also positive correlations between GCD and SBPA2009, and between GCD and SANCTIONS. The correlations between the control variables are overall low. The most correlated are LNASSETS and PROBZ, and LNASSETS and BANKDEBT and these correlations are below 0.400.

Table 6. Correlations.

5.2. Main results

reports estimates of models (1) and (2). Panel A studies the frequency of Type II errors (i.e. failure to include a going-concern opinion in the most recent audit report before bankruptcy), and Panel B studies the frequency of Type I errors (i.e. a going-concern opinion was issued, but the firm did not file for bankruptcy). The left-hand regressions in both panels report logistic regressions and the right-hand regressions report linear probability model (LPM) results estimated with ordinary-least squares (OLS). The z-values (t-values) of the logistic (OLS) regressions are based on Huber-White robust standard errors (Rogers Citation1994) using conventional maximum likelihood estimates.Footnote35

Table 7. Tests of hypotheses 1 and 2 on the entire samples.

Table 7. Continued.

Consistent with the prediction in hypothesis 1a, SANCTIONS and SBPA2009 have positive coefficients significant at the 0.01 level in the estimates of model (1). Marginal effects can be used to indicate the magnitude (economic significance) of sanction risk. The average marginal effect (defined as the average of the slope coefficients of the covariate patterns observed in the dataset) of SANCTIONS is 1.14% in regression (1), suggesting that the probability of a going-concern opinion before bankruptcy increases by 1.14% for each going-concern-related sanction issued in that year. For example, in 2009, there are 5 sanctions indicating that the probability of a going-concern opinion is 5.70% higher in that year than in a year without sanctions. The average marginal effect of SBPA2009 is 7.98% in regression (3), suggesting that the probability of a going -concern opinion before bankruptcy is around 8% higher in years 2009–2013 than in 2004–2008. The linear probability model results in regressions (5) and (7) indicate marginal effects of similar magnitude.

Panel B studies the likelihood that an auditor reports a going-concern opinion for a non-bankrupt firm. SANCTIONS and SBPA2009 have positively significant coefficients in regressions (9) and (11), suggesting that a higher sanction risk is associated with an increase in Type I errors. Indeed, the coefficient estimates are somewhat lower in Panel B than in Panel A, indicating that a higher sanction risk affects Type II errors more than Type I errors.Footnote36 The average marginal effects of SANCTIONS and SBPA2009 are 0.25% and 1.62% in regressions (9) and (11), respectively. However, the evidence is overall consistent with more conservative going-concern reporting when sanction risk is higher.

Hypothesis 2 focuses on the issue of whether the impact of sanction risk differs between large and small audit firms. To test this hypothesis, we use the interaction between measures of sanction risk and audit firm size. However, the interpretation of the interaction effect in a nonlinear model (e.g. logit) is not itself meaningful (e.g. Ai and Norton, Citation2003, Norton et al., Citation2004, Breen et al., Citation2018). Kohler and Kreuter (Citation2012) point out that there is, to the best of their knowledge, no single best solution to that problem, although the statistical literature offers several techniques. The interpretation of interaction effects in terms of marginal effects is one solution. The marginal effects in a logit model depend on the values of the regressors, and there is, therefore, no single measure of the marginal effect. As one test of hypothesis 2, reports the average marginal effects of sanction risk for BIG4, NEXT3, and non-Top 7 auditors. An alternative to interpreting interactions in a logit model is to use LPM.Footnote37 The appealing feature of LPM is that it provides unique estimates of marginal effects.

The bottom part of Panel A shows that the average marginal effect of SANCTIONS for BIG4 and non-Top 7 are 0.015 and 0.010, respectively. The difference in the average marginal effect between BIG 4 and non-Top 7 is significant at the 0.10 level. The average marginal effect of NEXT 3 is lower than that of BIG4 and non-Top 7 but not significantly so. The coefficient of BIG4*SANCTIONS in the LPM model reported in regression (6) is positively significant, thereby providing further support that sanction risk has a greater impact on Big 4 auditors’ reporting than non-Top 7 auditors’ reporting.

Results with SBPA2009 as the measure of sanction risk are mostly similar. Panel A reveals that the average marginal effects of BIG4, NEXT 3 and non-Top 7 are 0.103, 0.055, and 0.072, respectively. These results indicate that the probability of a BIG 4 auditor issuing a going-concern opinion is around 10% higher during the higher sanction risk period than during the lower sanction risk period. The corresponding likelihoods for NEXT3 and non-Top 7 are 5.5% and 7.2% respectively. Although the magnitude of the differences between the auditors is fairly large, the differences in the average marginal effects are insignificant. However, the LPM results reported in regression (8) suggest that the difference in the effect between BIG4 and non-Top 7 is significant (p-value < 0.05). In conclusion, most of the results based on data for bankrupt firms suggest a higher sanction risk impacts BIG 4 firms’ going-concern reporting more than non-Top 7 firms’ going-concern reporting.

In regressions (10) and (12) we use logit regressions to test hypothesis 2 for non-bankrupt firms. Overall, the average marginal effects are lower than in Panel A, indicating that increased sanction risk has a greater impact on the reporting for bankrupt than non-failing firms. However, consistent with hypothesis 2, the average marginal effect of SBPA2009 is significantly higher for BIG4 than for non-Top 7. The LPM results in regression (16) are qualitatively similar to the logit results in regression (12).

We also estimated regressions (4) and (12) separately for each audit firm type (not reported in tables). The analyses of bankrupt firms show that SBPA2009 has positive coefficients significant at least at the 0.05 irrespective of audit firm type. The odds-ratios of SBPA2009 are 1.80 when the firms are audited by a Big 4 auditor, suggesting that the proportion of firms with a going-concern opinion is 80% higher after than before 2009. The odds-ratios for firms with Next 3 and non-Top 7 auditors are 1.41 and 1.79 respectively. The analyses of non-bankrupt firms suggest SBPA2009 is significant only when firms have a Big 4 auditor. The odds-ratios for firms with a Big 4, Next 3 and non-Top 7 are 1.78, 1.05 and 1.32 respectively. These results correspond with results in Panel B of , suggesting only Big 4 firms report more going-concern opinions for bankrupt firms after 2009.

In sum, considering the tests with both bankrupt and non-failing firms, the results provide partial support for hypothesis 2. Most of the results indicate that auditors at Big 4 firms alter their reporting in response to a higher sanction risk more than auditors at non-Top 7 firms.

5.3. Additional tests of H1 and H2

We conduct the following un-tabulated analyses to gain further insights on the robustness of the results. First, we attempt to alter the time for when to assume that auditors upgrade their sanction risk. In these analyses we follow Defond et al. (Citation2018) and use lagged sanction risk measures, that is, the SBPA dummy assumes the value one in 2010 and thereafter, and SANCTIONS is the number of sanctions issued by SBPA in the previous year. Lagged SANCTIONS and SBPA have positive coefficients significant at the 0.01 level supporting hypotheses 1a and 1b. Furthermore, compared with , the use of lagged variables provides stronger support for the prediction that an increase in sanction risk has a greater impact on the reporting in Big 4 than in non-Top 7 firms.

Second, we study whether the results are sensitive to the classification of audit firms into the categories BIG 4, NEXT 3 and non-Top 7. In years 2004 and 2005, the BIG 4 firms and the firms in the NEXT 3 category (Grant Thornton, BDO, and Mazars) were considerably larger than all non-Top 7 firms: the largest non-Top 7 firm in 2005 was Randby Björklund whose revenues were 100 million, and the smallest Top 7 firm in that year was Mazars with SEK 220 million in revenues. In 2006, Baker Tilly started to grow, and in 2010 its revenues exceeded those of Mazars. Therefore, a ‘Next 4’ classification might better depict the structure of the audit market than a ‘Next 3’ classification in the latter part of the time period studied. To examine the NEXT3 versus NEXT4 effect, we first include BIG4, NEXT3, and a Baker Tilly indicator in model (1). Baker Tilly has insignificant coefficients showing that its reporting does not significantly differ from that of non-Top 8 firms, nor are the coefficients of Baker Tilly significantly different from those of NEXT 3. Second, we re-estimate models (1) and (2) with BIG4, NEXT4, and non-Top 8. SANCTIONS and SBPA2009 have positively significant coefficients in those regressions. Results related to hypothesis 2 are also qualitatively similar. In sum, our results are not sensitive to the choice between a NEXT3 and NEXT4 classification.

Finally, we add several additional control variables to mitigate the concern for omitted variables. Prior studies suggest that the client’s importance for the audit partner (Chi et al., Citation2012), auditor tenure (Knechel and Vanstraelen Citation2007), office size (Francis and Yu Citation2009), busyness (Sundgren and Svanström Citation2014), auditor’s age (Sundgren and Svanström Citation2014), gender (Hardies et al. Citation2016) and the location of the office (Samsonova-Taddei Citation2013) influence audit quality. The main reason why these variables are not included in models (1) and (2) is that the variables are only available for a subset of the firms. Most importantly, the variables are missing for virtually all observations from 2004.

The inclusion of all these variables in models (1) and (2) results in the omission of 333 or 359 firms, leaving 6,810 bankrupt and 6,784 non-bankrupt firms. Un-tabulated results show that SANCTIONS and SBPA2009 have positive coefficients significant at the 0.01 level, also in this extended version of model (1). However, different from and most of the results commented in the above, the regressions with more control variables but smaller sample size generally fail to provide significant support for the prediction that an increased sanction risk has a greater impact on the reporting of BIG 4 auditors than non-Top 7 auditors.Footnote38

Regarding the additional control variables, the regressions show that there is a significant positive association between the logarithm of office size and the likelihood of a going-concern opinion. Firms audited by female auditors are also significantly more likely to receive a going-concern opinion (p-value < 0.05) than firms audited by male auditors. On the other hand, the auditor’s age and the number of assignments have negative and significant coefficients (p-values < 0.01). These findings are in line with the results reported in Sundgren and Svanström (Citation2014). We find no significant association between auditor tenure and the likelihood of a going-concern opinion. Finally, the results show that client importance (measured as the client’s revenues divided by the revenue of all clients of the audit partner) is significantly negatively related to Type II errors. Client importance is not significantly associated with Type I errors. Findings support the argument that client importance may impair auditor independence.Footnote39

6. Supplementary analyses

6.1. Statutory audits

Prior literature suggests that an auditor trades-off between the risk of loss of reputation from issuing an incorrect going-concern opinion and client risk loss when they decide what report to issue (e.g. Knechel and Vanstraelen Citation2007). Until 2011, audits were statutory irrespective of firm size when micro -firms were exempted from this requirement (see Section 2). The option to opt-out of auditing if the auditor would issue a going-concern opinion is arguably a credible threat that may influence the auditor’s propensity to issue a going-concern.Footnote40

To test this prediction, we interact the sanction risk measures with STATUTORY in model (1). As the sanction risk started to increase in 2009 and the statutory auditor requirement was abolished in November 2010, we exclude observations from 2009 and 2010. The LPM results in reveal positive coefficients significant at the 0.01 or 0.05 level on the STATUTORY*SANCTIONS and STATUTORY*SBPA2009 interactions when the samples include bankrupt firms. The logit regressions in columns (1) and (2) also show that the average marginal effects of SANCTIONS and SBPA2009 are significantly higher for firms with a statutory audit than for firms without. However, in the analyses of the non-bankrupt firms, we cannot reject the null hypotheses that the impact of sanction risk is similar for firms with and without a statutory audit requirement. In sum, a higher sanction risk reduces Type II errors more in firms with a statutory audit requirement than without.

Table 8. Regressions examining the impact of sanction risk in firms with and without the statutory auditor requirement.

6.2. Informativeness of going-concern opinions

To examine the effects of sanction risk on the informativeness of going-concern opinions, we combine the bankrupt and non-bankrupt firm samples and examine whether sanction risk impacts the association between going-concern opinions and bankruptcy. The study of informativeness by the use of going-concern opinions’ ability to predict bankruptcy follows prior work (e.g. Hopwood et al. Citation1994, Foster et al. Citation1998, Knechel and Vanstraelen Citation2007).

To be more precise, we study the informativeness by exploring how sanction risk influences the association between going-concern opinions and bankruptcy risk and its impact on the discriminative ability using the area under the receiver operating characteristic curve (ROC-curve) as the measure.

We estimate variants of the following model:

(3)

(3)

The dependent variable BRUPT is an indicator variable taking the value 1 if the firm goes bankrupt. The test variable is the interaction between GCO and SBPA2009 (for brevity, we only tabulate results with SBPA2009). The model includes the following control variables. Following the recommendation by Cram et al. (Citation2009), we include PROBZ and LNASSETS to control for imperfect matching. Furthermore, we include UNCLEAN (an indicator taking the value 1 if the audit report departs from the standard formulation). Consequently, our analyses focus on the incremental explanatory power of GCD over all types of unclean audit reports. Model (3) also includes all control variables in model (1). , Panel B, presents the mean values of the variables for the bankrupt and non-bankrupt firms.

Panel A of presents logit and LPM results for the entire sample and for sub-samples with a BIG4, NEXT3, or non-Top 7 auditors. All models are statistically significant and their pseudo R-squared / R-squared are between 13.8% and 20.0%. Using 0.5 as the cut-off, regression (1) classifies 68.84% of the bankrupt and non-bankrupt firms correctly. Regression (2) includes only firms with a Big 4 auditor and it classifies 70.92% of the firms correctly. When the sample includes firms with a Next 3 and non-Top 7, the logit regressions correctly classify 70.71% and 67.99% respectively.

Table 9. Tests of the information contents of going-concern opinions.

The marginal effects presented in the lower part of the table show that a going-concern opinion increases the bankruptcy probability during the lower and higher sanction risk periods, but the impact is higher under the higher sanction risk period. For example, regression (1) suggests that the average marginal effect of GCD is 17.5% and 23.2% under the lower and higher risk periods, respectively. Furthermore, the table suggests that a GCD is associated with a 2–3% higher bankruptcy risk in the higher sanction risk period than in the lower sanction risk periods for BIG4, the difference is 7–8% for auditors with a NEXT3 or non-Top 7 auditor. These results indicate that an increased sanction risk has a greater effect on the information contents in non-Big 4 firms. This result can, at first glance, be viewed as conflicting results related to hypothesis 2 in . Those results suggest Big 4 firms change their reporting more in response to higher sanction risk than non-Top 7 auditors. However, shows that Big 4 auditors issue more going-concern opinions to non-bankrupt firms as well when the sanction risk is higher, and that may reduce the predictive ability of GCD.

We next compare the discriminative ability of GCD under the lower and higher sanction risk periods by studying the area under the ROC curve using the methods suggested by Cleves (Citation2002). The ROC curve displays the sensitivity (i.e. fraction of correctly predicted bankrupt firms) versus one minus specificity (i.e. one minus fraction correctly predicted non-bankrupt firms) as the cut-off for classifying a firm as bankrupt is varied. Hosmer and Lemeshow (Citation2000) suggest that areas under the ROC curve of 0.70 to 0.80 are acceptable and above 0.80 good or excellent.

The analyses show that the area increases from 0.722 to 0.729 under the lower sanction risk period when GCD is added to the model and that it increases from 0.779 to 0.790 under higher sanction risk period. Although the differences are small, they indicate that GCD significantly increases ROC under the lower as well as higher sanction risk periods.Footnote41 The finding that the area under the ROC curve is significantly higher if the model includes GCD holds irrespective of whether the firms are audited by a Big 4, Next 3, or non-Top 7 auditor. In sum, the results suggest GCD improves the discriminative ability regardless of audit firm size and sanction risk.

Finally, Panel B of compares the ROC of model (3) under the lower and higher sanction risk periods. Overall, these results suggest that ROC is significantly higher under the higher sanction risk period than under the lower sanction risk period. These results are consistent with the view that going-concern opinions are more informative during the higher sanction risk period. Still, we cannot rule out that other factors drive the increase in discriminative ability.

7. Conclusions

We examine how regulatory sanction risk influences auditors’ going-concern reporting using a sample of privately-owned Swedish firms. The sample covers 10 years, starting from the first effective date of an ISA 570-based going-concern reporting standard in 2004. Sanction risk is measured by the frequency of disciplinary sanctions issued against auditors for sub-standard going-concern reporting. Our findings show that auditors’ issue more going-concern opinions to bankrupt and non-bankrupt firms in periods with higher sanction risk, suggesting that a change in sanction risk increases the level of conservatism in the going-concern reporting.

The next set of analyses examine how audit firm size interacts with sanction risk. Generally, the results suggest auditors at Big 4 firms alter their reporting more than non-Top 7 firms when sanction risk increases. A rationale for that result is that a sanction would more severely affect the reputation of a Big 4 auditor than that of a non-Top 7 auditor thus providing Big 4 auditors the incentive to be more conservative in their reporting.

The informativeness of the audit report increases with the reduction in Type II errors but decreases with a similar increase in Type I errors. To examine the net effect, we compare going-concern opinions’ ability to predict bankruptcy in periods with low and high sanction risk. We find a stronger association between going-concern opinions and bankruptcy risk in the higher sanction risk period. Furthermore, results suggest sanction risk impacts the association between GCD and bankruptcy, especially in firms with a non-Top 7 auditor.

The results of this study should be interpreted with some limitations in mind. First, the underlying reasons for the observed going-concern reporting practices could not be directly tested. Second, the data used are from a country where all firms had to undergo an audit regardless of their size until 2010. Thus, the average audit client is small, and generalisations to other settings may not be appropriate. Third, the failure to issue a going-concern opinion for firms entering bankruptcy and the issuance of a going-concern opinion to a non-bankrupt firm is not equivalent to audit quality. For example, it is possible that financial problems of a bankrupt firm became apparent after the issue of the audit report, thus suggesting that a clean report was adequate and contained all the relevant information at the time of signing the audit report.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 It has been suggested that auditors’ issuance of a going-concern opinion could become a self-fulfilling prophecy, i.e., the opinion causes the client to go bankrupt (Mutchler Citation1984, Tucker and Matsumura Citation1998). However, the empirical evidence for the existence of a self-fulfilling prophecy shows conflicting results (Citron and Taffler Citation2001, Pryor and Terza Citation2001).

2 Based on the Wingate Litigation Risk Index, Sweden belong to the group with low litigation risk (i.e., an index below 10) together with Denmark, India, Ireland, Italy, Malaysia, Norway, Pakistan, Singapore and South Africa. Australia, Hong Kong, New Zealand, United Kingdom and United States belong to the group with high litigation risk (i.e., and index greater or equal to 10). The Wingate litigation index is derived from an assessment of litigiousness for doing business as an auditor in each country.

3 In April 2017, the SBPA changed its name to Swedish Inspectorate of Auditors (Sw. Revisorsinspektionen).

4 RS 570 included one national addition to the ISA 570. Paragraph 4SE referred to national accounting guidelines that specified the management’s responsibility to test the going-concern assumption. However, this specification does not in any way reduce the responsibilities of the auditor to assess and report ongoing concern uncertainty. From 2011, an outright translation of the ISA was adopted.

5 There is a degree of flexibility concerning the wording of going-concern opinions. The standard does not specify phrasing but instead offers examples of how to formulate the going-concern opinion, and practice has produced variations in auditors’ choice of words. In the period from 2004 to 2008, there are numerous examples of ambiguous or vague statements related to going concern reporting. Examples of such statements include ‘Actions are required in order to manage the going concern assumption,’ ‘The future of the company is dependent on … , ’ and ‘It is difficult to assess whether the company will be able to turn the negative profit trend in time.’

6 We have discussed audit reporting requirements and practice before 2004 with several experienced auditors in Sweden who signed audit reports long before 2004. They all stated that there was no practice at all to report on going-concern uncertainty before the introduction of RS 570 in 2004.

7 The average number of annual sanctions in the period 2004-2013 was 52 (see for more details).

8 SBPA operates based on governmental regulation (Sw. Förordning). The tasks and resources of SBPA are specified in annual governmental regulation letters (Sw. Regleringsbrev). With regard to auditor oversight, these regulations have remained the same during the entire study period (Förordning Citation1997:Citation666; Förordning Citation2007:Citation1077). The unchanged tasks of the SBPA are to exercise oversight of certified auditors and audit firms to ensure the delivering of audit services of high quality and high ethical standards, and to ii) decide on disciplinary sanctions. The auditor oversight and inspection procedures, as described on the SBPA homepage, has also remained (largely) unchanged during the entire study period.

9 The IFIAR's work is aimed primarily at developing inspections to ensure that the working methods of the international oversight bodies are as coordinated and as effective as possible.

10 The number of inspections performed by the SBPA during the period of 2005-2013 varies from a minimum of 137 (in 2009) to a maximum of 198 (in 2005). The number of quality control inspections performed by FAR were the following (2-years periods): 2005/2006: 1617; 2007/2008: 1425; 2009/2010: 1058; 2011/2012: 1415. Since all certified auditor without engagements in public companies are inspected at least every sixth year (by FAR), this allows for allocating either small or large resources to individual years over this 6 year-period.

11 In most going-concern-related cases, SBPA also identified other deficiencies in audit conduct. In many of these cases, the sanctioned auditor had failed to include going-concern remarks in multiple audit assignments. One should note that the audit reports assessed in the disciplinary sanctions are issued typically a few years back from when the sanction is issued.

12 This conclusion is based on discussions with two certified auditors at large audit firms.

13 Starting in November 2010, companies that did not exceed two of the following three size criteria were exempted from the audit requirement: SEK 3 million in revenue, SEK 1.5 million in balance sheet total, and three employees.

14 The firm is registered under the name Mazars SET.

15 These market shares are based on all joint-stock companies in Serrano for which we know the audit firm affiliation (2.7 million observations for 0.5 million firms). The market shares are measured over the 2004-2013 period and further shows that Big 4 audit 36.2%, Grant Thornton, BDO, and Mazars audit 12.4%, and non-Top 7 audit 51.5% of all firms. Big 4 firms’ market share based on sales of clients is 79.3%, i.e., considerably higher. The corresponding market shares of Grant Thornton, BDO, and Mazars is 7.2%, and it is 13.5% for non-Top 7 firms. The market shares are fairly stable over the sample period. For example, the lowest market share of Big 4 (based on the number of firms audited) is 34.4% in 2011 and the highest market share is 37.4% in 2006. The minimum and maximum market shares for non-Top 7 are 50.1% (in 2006 and 2007) and 53.7% (2011).

16 All going-concern-related sanctions issued are due to a failure to include a going-concern opinion. There are, to the best of our knowledge, no cases of sanctions issued because of the auditor issuing an unwarranted going-concern opinion.

17 Sundgren and Svanström (Citation2017) use a sample with 3,139 (private) companies for the 2006 to 2011 period to test the impact of being sanctioned on the auditor’s going-concern reporting. As mention in Sundgren and Svanström (Citation2017, p.798), the data used in that study is a sub-sample of the (bankrupt) sample used in this study. The non-bankrupt sample used in this study has been collected later and is not used in Sundgren and Svanström (Citation2017).

18 The top 6 audit firms are Big 4, Grant Thornton and BDO.

19 This claim can be supported by evidence suggesting that Big 4 audit firms respond quicker to regulatory changes than non-Big 4 firms by increasing their propensity to issue going concern opinions (e.g., Xu et al. Citation2013). It is unclear whether the cost related to Type I errors is different for large and small audit firms.

20 At large international audit firms, the reporting practices are initially influenced by knowledge from the international network that in this case has prior experience of going-concern reporting from countries already applying the similar standard and internal pre-discussions. Therefore, they may need to make the relatively smaller adjustment to their reporting practices compared with smaller audit firms when sanction risk increases.

21 It is the cost of Type II errors that is affected when the sanction risk increases. The cost of Type I error remains unchanged since there are no cases of sanctions issued against auditors that have issued unwarranted going concern opinion. However, the relative cost of Type I error reporting is affected by whether the cost of Type II errors is high or low. When the cost of Type II errors is low, then the relative cost of Type I errors is high, and few Type I errors occur. When the cost of Type II increases, this provides incentives for the auditor to issue more going concern opinions which is likely to lead to more Type I errors and fewer Type II errors.

22 As previously observed in the literature (e.g., Carson et al. Citation2019), Type 1 errors have to be interpreted with some caution. It is, for example, possible that there were significant doubts about the firm's ability to continue its operations at the audit report date. However, the firm eventually underwent a successful reorganization. Alternatively, a firm with poor prospects may liquidate without filing for bankruptcy.

23 Grant Thornton, BDO, and Mazars all belong to a major international network characterized by quality assurance and internal quality reviews, as well as common methodology and practice rules (Lenz and James Citation2007). Therefore, auditors at these firms should be motivated (reputation concern) to develop similar reporting practices as Big 4 auditors and they are also likely to respond similarly (as Big 4) to shifts in the enforcement level.

24 The model includes net income to total assets, total liabilities to total assets and the current ratio. The ratios include several observations with extreme values, so we winsorized the ratios at the top and bottom 1 per cent .

25 The exact reporting date is not available, but based on the assumption that the report is signed around three months after the balance sheet date, the use of 1st July as the cut-off approximates the definition in Geiger et al. (Citation2014), whose crisis variables take the value one if the report has been issued after 1 September 1 2008.

26 In several disciplinary cases, the SBPA has clarified that the auditor cannot avoid issuing a going-concern opinion by referring to that the subsidiary is likely to receive financial support from the parent company. In that case, a formal letter of intent is required.

27 The requirement that the time between the balance sheet date and bankruptcy is at least three months reduces the risk that the bankruptcy petition was filed before the audit report was signed. The twelve months limit is used to assure that bankruptcy occurred within the time to be covered by the auditor when the firm's ability to continue as a going-concern is assessed (see ISA 570, § 13).

28 We assigned the firms into ten categories based on percentiles of their assets in a first search in which we identified 6,651 pairs. To increase the number of matched pairs, we used five size categories in a second search for pairs.

29 Parents in groups whose sales exceed SEK 80 million, assets SEK 40 million, and 50 employees have to prepare consolidated financial statements. If available, the consolidated reports are used to calculate size and financial ratios for the parent companies. Separate financial statements are used for subsidiaries and firms that do not belong to a group.

30 The Serrano database used for this study includes bankruptcy dates until the end of 2017, i.e. at least four years after the balance sheet date. 15 of the 7,143 non-bankrupt firms filed for bankruptcy more than one year but less than four years after the balance sheet date. The minimum and median time between the balance sheet date and the bankruptcy filing are 1.23 years and 3.28 years respectively. The finding that there are few non-bankrupt firms filing for bankruptcy in subsequent years suggests that the Type 1 measurement error is low in this study.

31 The average PROBZ is 50.0% and the standard deviation is 35.8% showing that a 1.28% difference in PROBZ is small in comparison with the entire variation in the data.

32 To improve comparability, publicly held firms and firms with no audit report information in Serrano are not included in the ‘all’ categories in Panel A of .

33 There are around 12,000 firms with financial statements less than one year prior to bankruptcy and around 36,000 firms with financial statements less than two years prior to bankruptcy, indicating that two-thirds of all bankrupt firms fail to send their financial statements to SCRO the year prior to bankruptcy.

34 Small firms are exempted from the statutory audit starting from 2010. A possible reason for the relatively low number of observations in 2011 to 2013 is that distressed small firms might have opted out of auditing (see footnote 40 for numbers). A further factor influencing the number of observations per year is that we include a firm in the sample only if the firm filed for bankruptcy within one year after the date of the financial statements. Financially distressed firms sometimes overlook the obligation to make their financial statements available in the years prior to bankruptcy, implying that the needed data is not available. The number of firms overlooking the rule may vary between years.

35 There are few observations with a going-concern opinion in, especially, the sub-sample with non-bankrupt firms. Coefficient estimates based on conventional maximum likelihood estimates may be biased if there are few observations on one of the outcomes (e.g., King and Zeng Citation2001). We estimated the logit regressions in using a penalized maximum likelihood estimation using ‘firthlogit’ in Stata (Coveney Citation2015). Those results are qualitatively similar to the ones presented in the tables.

36 Tests of the difference of the coefficients of SANCTIONS regressions (5) and (13) suggest the higher sanction risk has a greater impact on the reporting in bankrupt than in bankrupt firms (p-value < 0.01). The coefficient of SBPA2009 is also significantly higher in regression (7) than in regression (15) (p-value < 0.05). However, the sanction risk measures are not significantly different in the logit regressions.

37 There is an ongoing academic discussion about the strengths and weaknesses with the use of logit, probit or LPM when the outcome variable is binary. See Breen et al. (Citation2018) for a review and references.

38 Indeed, this result may be driven by the smaller sample size. We estimated regressions with the variables in model (2) on the 6,810 bankrupt and 6,784 non-bankrupt firms used in the extended model and those results generally fail to support the prediction that an increased sanction risk has a greater impact on the reporting of BIG 4 auditors than non-Top 7 auditors.

39 Some studies suggest standard implementation is a learning process (e.g., Mennicken Citation2008, Kvaal and Nobes Citation2012). Learning is likely to take place in the first years after the effective date of a standard, and we examine the effect of learning by estimating model (1) on observations from 2007 to 2013. SANCTIONS and SBPA have positive coefficients significant at the 0.01 level in the analyses of the bankrupt firms. The sanction risk measures have positive coefficients significant at the 0.05 or 0.10 level when the sample includes non-bankrupt firms. In conclusion, the association between sanction risk and the going-concern reporting is unlikely to be driven by learning effects.