?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This study seeks to analyze the non-linear relationship between a firm’s debt structure and performance based on evidence from Japan through the use of a panel data fixed effects model for a sample of 1,670 listed firms. This is the first study that looks at the effect of the short-term debt threshold on corporate performance, as well as the influence of the 2008 global financial crisis (GFC) on the nonlinear effect of debt structure on corporate performance. Moreover, it represents an initial endeavor that uses cross-industry comparisons to scrutinize the nonlinear effect of debt structure on the performance of Japanese companies. This study’s findings reveal the presence of a nonlinear impact of debt with short-term maturity on corporate performance. In addition, there is a U-shaped relationship between firm performance and short-term debt, suggesting that a firm’s profit decreases at lower levels of short-term debt (below 45.2%) and increases at higher levels of debt with short-term maturity. Moreover, this short-term debt threshold was affected significantly by the financial crisis.

I. Introduction

Investigating the nexus between debt structure and corporate performance has become another important research area of capital structure. Corporate debt as an aggregate of short- and long-term debt has received considerable attention in the literature for capital structure, with most empirical research papers investigating the nexus between firm profitability and capital structure in terms of total debt (e.g. Nenu, Vintilă, and Gherghina Citation2018; Raharja and Mranani Citation2019; Tsuji Citation2019; Rajan and Zingales Citation1995). In contrast, debt structure in itself has yet to be widely investigated. In addition, most previous empirical studies of corporate leverage have examined the determinants of debt and debt maturity (e.g. Ozkan Citation2002; González Citation2015; Yildirima, Masihb, and Ismath Citation2018; among others). Up-to-date empirical research into the impact of debt structure, in terms of maturity, on corporate performance are scarce, despite the crucial decisions that need to be made when dividing a firm’s debt into short- and long-term debt, even though this impacts a firm’s health, solvency, performance, and its future investment plans (Rai and Danilevskaia Citation2005; Rauh and Sufi Citation2010).

Several theories and studies have sought to establish the influence of debt structure on corporate performance by considering that long- and short-term debt have different benefits and costs. For example, it is argued that short-term debt financing is less costly (Titman and Wessels Citation1988; Barclay and Smith Citation1995; Myers Citation1977), but it is riskier and needs to be renewed more regularly (Wang and Chiu Citation2019). However, it also helps to decrease the lender–shareholder agency cost (Myers Citation1977), and in the case of asymmetric information, it helps to reduce the cost of borrowing according to Diamond (Citation1991). In addition, firms that have more access to debt with shorter maturity are more likely to have higher rates of survival and solvency. In contrast, despite its higher cost, long-term debt is more stable and less risky when compared to short-term debt (Rai and Danilevskaia Citation2005; Krivogorsky, Joh, and DeBoskey Citation2018; Nenu, Vintilă, and Gherghina Citation2018). It therefore seems that scrutinizing the relationship between corporate performance and debt in terms of total debt instead of debt structure may result in specious findings, which could affect firms’ performances negatively.

A firm’s decision about the appropriate blend of debt (i.e. short- and long-term) is especially crucial during an economic downturn or a financial crisis. During financial crises, firms may be unable to secure new debt or renew existing debt due to their performance or business activities dwindling. The failure of firms is generally triggered by an inaccessibility to short-term funding, thus creating a risk of bankruptcy and default (Wang and Chiu Citation2019; Nenu, Vintilă, and Gherghina Citation2018). Indeed, a firm’s ability to gain access to short-term debt hinges on its credit channels, debt maturity, and the state of the securities market. In Japan, firms rely heavily on bank loans because, compared to the United States, there is a less-developed short-term instruments market (i.e. securities market), and this limits a firm’s options for financing its short-term needs. Nonetheless, the number of companies issuing short-term debt has increased recently in Japan.

In Japan, despite the crucial effect of capital and debt structures on corporate performance, there is a scarcity of research into it. Few studies have supplied evidence from Japan about the determinants of capital structure (e.g. Nishioka and Baba Citation2004; Zhang and Kanazaki Citation2007; Tsuji Citation2019). In addition, the empirical evidence for the moderating effect of the global financial crisis (GFC) on the significant effect of debt structure, especially short-term debt, on corporate profitability in both emerging and developed markets is lacking (e.g. Dolenc, Grum, and Laporsek Citation2012; Nenu, Vintilă, and Gherghina Citation2018). To the best of our knowledge, no study has yet examined the nonlinear effect of debt structure, combined with the 2008 GFC, on Japanese firms’ performance. Hence, due to the critically important influence of firms’ debt structure and short-term debt on corporate performance, particularly during global financial crises, our study explores the effect that the 2008 GFC had on Japanese firms’ performance.

Our paper contributes to the existing literature for debt maturity as follow. First, this study represents an initial endeavor to scrutinize the nonlinear effect of debt structure on the performance of Japanese companies by applying the panel data fixed-effects approach. It is based on a large sample of 1,670 Japanese firms from eight sectors. Second, our study investigates how the 2008 GFC influenced the effect of debt structure as a determining factor of firm performance in Japan. Third, we sought to measure how the 2008 GFC affected the nonlinear and threshold relationships between firm performance and short-term debt. Studies into the nexus of firm performance and short-term debt are very scarce to the best of our knowledge (Raharja and Mranani Citation2019). Fourth, unlike the previous empirical work on the topic, we also aim to contribute to a better synthesis of the interaction between debt structure and a firm’s performance in two ways. First, we pay close attention to endogeneity issues using lagged firm-specific factors with a static and dynamic panel fixed-effects regression model. Second, this paper aims to investigate the nature of the nonlinear threshold impacts of short-term debt on corporate performance, as well as perform a robustness check for our empirical testing.

Our regression results reveal that short-term debt is significantly and economically crucial for determining corporate performance in Japan. Moreover, our findings confirm the existence of a nonlinear nexus between firm performance and short-term debt. Indeed, the study found a U-shaped correspondence between a firm’s short-term debt and its performance, such that above a certain cut off point, short-term debt strengthens corporate performance, while below a certain level, short-term debt starts to decrease the performance of firms. Moreover, our findings demonstrate that the short-term debt threshold was significantly influenced by the GFC, and firms’ optimal short-term debt clearly increased during the crisis. During the crisis, the threshold for short-term debt was estimated at 44.5%, while outside the crisis period, the threshold was just 32.6%, indicating that short-term debt is more crucial during a crisis due to pressures on liquidity. These findings are crucial for designing policies that will boost firms’ performances.

The remainder of this paper is presented as follows. A review of the relevant literature is presented in Section II, while the data and variables considered are discussed in Section III. The methodology and specified model are presented in Section IV. Next, Section V supplies the statistical analysis and the empirical results. Finally, the last section, Section VI, concludes the paper and discusses the implications for decision-makers.

II. Theoretical background and research hypotheses

The corporate financing literature argues that short-term debt maturity participates in more effectively lessening the agency problem when compared to long-term debt. According to agency theory, a conflict of interest arises between managers and shareholders due to the separation between ownership and management (Jensen and Meckling Citation1976), so a debt policy can aim to minimize agency problems. Indeed, controlling shareholders tend to use debt financing, especially with short-term debt, to monitor and control managers and thus mitigate the agency problem (e.g. Myers Citation1977; Schiantarelli and Sembenelli Citation1997; Thanha, Canh, and Hac Citation2020).

Myers (Citation1977) showed that short-term debt alleviates the shareholder–lender agency problem, finding that firms with high growth opportunities are more likely to use debt with shorter maturities, which in turn enables them to redirect investment and solve underinvestment problems. Leland and Toft (Citation1996) also showed that short-term debt decreases the agency costs related to shareholder risk. Khurana and Wang (Citation2015) and Barclay and Smith (Citation1995) argued that short-term debt decreases the agency costs arising from ‘asymmetric information’, and according to Diamond (Citation1991), it reduces the cost of borrowing in the case of asymmetric information. Likewise, short-term debt is considered more effective compared to long-term debt due to the refinancing pressure and the degree of control imposed on managers (e.g. Hart and Moore Citation1998; Rajan and Zingales Citation1995; Diamond Citation1991). Moreover, it is argued that debt with short-term maturity is less costly (Myers Citation1977; Titman and Wessels Citation1988; Barclay and Smith Citation1995), but it is riskier and needs to be renewed more regularly (Wang and Chiu Citation2019).

Scrutinizing the nexus between debt structure and corporate performance has therefore become another important research area for capital structure, because using total debt rather than debt structure may result in specious findings that may negatively affect firms’ performances if acted upon, because the benefits and costs of short-term debt are opposed.

A negative connection between a firm’s performance and short-term debt maturity has been documented by many empirical studies (e.g. Rajan and Zingales Citation1995; Custódio, Ferreira, and Laureano Citation2013; Nenu, Vintilă, and Gherghina Citation2018; Le and Phan Citation2017; among others). In contrast, a significant positive link between short-term debt and a firm’s profitability has been reported (e.g. Schiantarelli and Sembenelli Citation1997).

In reality, corporate performance is more likely to be affected differently depending on the levels of debt with different maturities. With a high level of short-term debt, a firm’s debt and bankruptcy costs are high (Gordon Citation1971; Mu, Wang, and Yang Citation2017), with it also being more constrained by debt contracts due to the creditor–management agency problem. Creditors may pressure managers to avoid the misuse of debt to ensure their loans are repaid. Managers will thus be placed under greater pressure to invest in highly profitable projects that enhance performance or face the threat of being dismissed. Moreover, using more debt increases tax deductibility (Scott Citation1977; Harris and Raviv Citation1991) and leads to an upsurge in returns on equity for shareholders seeking to reduce the principal–agent problem.

The level of monitoring is higher for short-term debt than debt with long-term maturity, because it must be renewed regularly (Wang and Chiu Citation2019). In addition, managers with superior corporate performance may also prefer to utilize more short-term debt, and this decreases agency problems and the cost of borrowing (Diamond Citation1991). A firm’s cost of borrowing (Scott Citation1977) and distress are relatively low with a low level of short-term debt, so there is less pressure and/or incentive for managers to enhance performance. Low levels of short-term debt therefore negatively affect performance. Sparse empirical studies have documented a nonlinear relationship between corporate performance and debt, such as those of Nguyen and Nguyen (Citation2020), Raharja and Mranani (Citation2019), and Davydov (Citation2016). Interestingly, no study to date has examined the threshold and the nonlinear effect of debt structure on firms’ performances in Japan. Based on the above discussion, we developed our research hypotheses as follows

H1a:

Short-term debt has a significant impact on firm performance.

H1b:

Short-term debt has a significant non-linear (U-shaped) impact on corporate performance.

During economic downturns and financial crises, the credit supply decreases as financial institutions tighten their credit policies as the risk of insolvency increases (Ivashina and Scharfstein Citation2010; Judge and Korzhenitskaya Citation2012; Vithessonthia and Tongurai Citation2015; among others). If the ability of a firm to access external finance during financial crisis, especially through debt with short-term maturity, is decreased (Judge and Korzhenitskaya Citation2012), corporate performance and default risk will likely be affected (Titman and Wessels Citation1988).

Several empirical studies have sought to investigate the effect of the 2008 global financial crisis on debt maturity (e.g. Ivashina and Scharfstein Citation2010; González Citation2015). Other studies have examined the financial crisis’s effect on firms’ performances and investment opportunities in various industrial sectors (e.g. Campello, Graham, and Harvey Citation2010; Dolenc, Grum, and Laporsek Citation2012; Zeitun and Haq Citation2015; among others). For instance, Campello, Graham, and Harvey (Citation2010) found that the financial crisis negatively affected firms’ investment opportunities in Asia, Europe, and the United States. Zeitun and Haq (Citation2015), meanwhile, found that the performances of GCC firms with shorter debt maturity were negatively affected by the crisis. It would therefore seem that financial crises decrease investment opportunities, and this in turn decreases corporate performance and increases liquidity risk, because the credit policies adopted by banks tightened. This in turn limited firms’ ability to borrow, especially through short-term debt, which made it harder to recover from the crisis. Moreover, firms with a higher proportion of short-term debt ratio face greater risk due to the risk of refinancing, especially during a financial crisis or economic downturn (Diamond Citation1991). It therefore seems likely that financial crises influence the nexus between debt structure and firm performance. Our next research hypotheses are therefore as follows

H2a:

Financial crises have a significant negative effect on the connection between debt structure and corporate performance.

H2b:

A stronger (more pronounced) nonlinear relationship between corporate performance and short-term debt is expected during a financial crisis, with there being a higher threshold effect.

III. Data

Data for the firms were collected from the Bloomberg database, while data for macroeconomic and institutional variables were gathered from the International Financial Statistics (IFS) and the World Bank (WB). Our sample comprised 1,670 firms that were listed on the Japanese stock exchange for the study period, which was 2004–2016. Hence, our research is based solely on listed firms. Our data covered eight sectors: Industrial Goods and Services (INDGD), Basic Materials and Chemicals (BASICM), Health Care (HETH), Oil/Gas, Telecommunications (Telecom), Consumer Services (CONSVR), Consumer Goods (CONGD), and Technology Equipment and Hardware, Software and Computer Services (TECHN).

Firms dealing in insurance, banking, financial services, and utilities were excluded from our sample, because these sectors are distinct in the areas of capital structure, debt structure, and other features in terms of their financial sources and their uses. In addition, the firms considered in the study sample needed to have at least six years of financial data to ensure the reliability of the data.

Variables

The existing literature has identified important variables that affect corporate performance (e.g. Rajan and Zingales Citation1995; Davydov Citation2016; Adachi-Sato and Vithessonthi Citation2019; among others). Considering the existing studies, the dependent variable used in this study is firm performance, and this is measured as the earnings before interest and tax (EBIT) to total assets (ROA). The independent variables are debt structure, in terms of the proportion of short-term debt, as well as other firm-specific factors that can influence corporate performance, such as size, risk, growth, and liquidity. We also include two macroeconomic factors and one institutional variable. Appendix A provides definitions of the dependent and independent variables used in our study.

Debt structure variables

Debt structure, in terms of maturity, is measured by short-term debt to total debt (STDTD). Furthermore, a quadratic form of STDTD is used to inspect the nonlinear effect of debt structure on corporate performance. The book values for the debt variables are used because they act as a precise measurement during a financial crisis (see, for example, Adachi-Sato and Vithessonthi Citation2019).

Control variables

Four control variables were used in this study; size (LnTA), growth (Gr_oppt), risk (F_ risk), and liquidity (CUR_R) (e.g. Adachi-Sato and Vithessonthi Citation2019; Custódio, Ferreira, and Laureano Citation2013; Myers and Rajan Citation1995; Nenu, Vintilă, and Gherghina Citation2018). Appendix A provides the definition for the control variables used in our study.

Macroeconomic and institutional variables

Two macroeconomic variables were included, namely GDP growth and inflation. GDP growth (GDP_G) is expected to positively affect firm performance, while inflation (INFL) is expected to negatively affect performance (e.g. Tirapat and Nittayagasetwat Citation1999). Finally, one institutional variable was used, namely the control of corruption, which is a governance aspect. According to the World Bank, a high value indicates that the level of corruption is low. We therefore expect improved institutional quality to have a positive effect on corporate performance (Donadelli, Fasan, and Magnanelli Citation2014).

IV. Model specification

Econometric methodology

In order to study whether the observed variations in firm performance relate to the differences in debt structure for each firm, we estimated the following regression model

Where refers to the return on assets for company i in year t.

is a vector of firm-specific independent regressors, including the debt structure variable (short-term debt (STDTD)) and other firm-specific factors that may affect a firm’s profitability, such as size (LnTA), risk (F-risk), growth (Gr_oppt), and liquidity (CUR_R).

is a vector that includes macroeconomic and institutional variables representing the state of the economy, namely the inflation rate (INFL), GDP growth (GDP_G), and governance in terms of controlling corruption (CORR). Dcrisis is a dummy variable that is equal to 1 for the 2007–2011 sub-period and 0 otherwise, and

is a firm-specific interceptor controlling for all other unobservable firm-level characteristics that may affect a firm’s performance.

We focus on the moderating role of the financial crisis on the nonlinear link between firm performance and short-term debt. To do so, we introduce the Dcrisis variable and an interaction term for this factor with short-term debt. The model therefore adapts into the following:

Hence, on average, the marginal effect of the STDTD on return on assets is as follows:

We followed the example of (González Citation2015) in controlling for potential endogeneity problems by lagging all independent firm-level factors by one year. In addition, to test the sensitivity analysis of the hypothesis for the nonlinear relationship between STDTD and firm performance, Equation (1) was extended to include the lagged value of returns on assets as a determinant of corporate performance in order to capture adjustment delays. Hence, we adopted the nonlinear dynamic model with individual fixed effects that was developed by Hsiao, Pesaran, and Tahmiscioglu (Citation2002), and this can be expressed as follows:

Next, we used a first-differenced model to skip the individual fixed effects, such that:

With

We used the quasi-maximum likelihood (QML) estimators of Kripfganz (Citation2016), which is an alternative to the GMM estimation method in the context of dynamic panel data models. This econometric method is an attractive option for mitigating the problem of biased estimates when the number of cross-sectional units is large and the time horizon is short.Footnote1

We also applied a robustness check analysis to test the sensitivity of the estimation results, thus comparing static and dynamic models of firm performance (Models 1 and 3) and using a different metric for firm performance (Tobin’s Q and ROA).

Threshold effects

Through Equations (1) and (Equation4(4)

(4) ), we empirically tested for a nonlinear relationship between firm performance and short-term debt. Adding a quadratic term for short-term debt in the firm performance model yielded a new model in which the expected response of return on assets to a change in the short-term debt depends upon the short-term debt level. If the coefficients of the linear and quadratic terms of short-term debt were significant and showed opposite signs, we could conclude the presence of a curvilinear nexus between short-term debt and corporate performance with a threshold effect. As mentioned in Section II, we expected that an increase in the short-term debt would decrease firm performance up to a certain point, after which both variables would increase simultaneously. For this U-Shaped curve, we expected

The cutoff point for short-term debt could be identified by solving the equation for the marginal effect of short-term debt, STDTD, on corporate performance as follows:

Using the fixed-effects panel data estimates of and

in (1), and (3), the point estimate of short-term debt was:

To assess the statistical significance of the estimated thresholds, we used the delta method to approximate the variance of a nonlinear function of

such that the approximate variance expression was:

Thus, an approximate 95% interval estimate for the threshold of short-term debt, was:

V. Empirical results

This section provides the descriptive statistics and then discusses our results for the nonlinear effect of debt structure on corporate performance, both for the entire sample and by industry,

Descriptive statistics

shows the variables’ descriptive statistics for the full sample and the sub-samples for during the crisis period (2007–2011) and the out-of-crisis period (2004–2006 and 2012–2016). In addition, we provide details about mean firm-specific factors grouped by economic sector. shows that the average ROA for the full sample was 3.66%, with a low erraticism of 5.13%. The firms’ average performance appears to have been affected by the financial crisis, with the ROA being 3.9% outside the crisis period and 3.3% during the crisis period. Tobin’s Q average was 1.43% outside the crisis period, and 1.25% during the crisis period, confirming that the firms’ average performance was negatively affected by the GFC.

Table 1. Descriptive statistics for dependent (contingent) and independent variables.

The overall average of the STDTD was 19.6%, which was impacted by the financial crisis, with it being 20.8% outside the crisis period and 17.7% within the crisis period. This could be explained by the firms’ inability to increase or renew their short-term debt during the crisis period. The firms’ growth opportunities, additionally, decreased drastically from 8.7% outside the crisis period to 2.6% during the crisis period. The average real GDP per capita also decreased sharply from 1.38% outside the crisis period to −0.12% during the crisis.

reports the average values for the firm-specific variables by industrial sector, both for the full sample period and the sub-sample periods. The mean of the ROA ranged from 3.94% for the technology sector to 3.57% for the consumer goods sector. Firms operating in the technology sector had the largest short-term debt ratio (21.1%), while firms operating in the consumer services sector had the smallest (17.9%).

Table 2. Descriptive statistics (Mean) for dependent (contingent) and independent variables, by industry.

shows the correlation between the dependent variables related to the firm-specific, institutional (control of corruption: CORR), and macroeconomic factors (inflation and GDP_G) for the full sample. The results in reveal no multicollinearity issues between the selected variables.

Table 3. Correlation matrix explanatory variables.

Threshold results for the full sample

shows that the debt structure variable (STDTD) was significant and had a negative effect on corporate performance, which supports our argument that debt structure affects corporate performance. Thus, our hypothesis H1a was accepted. In addition, STDTD had the greatest economic importance of all the firm-specific factors affecting firm performance, which implies that STDTD is crucial for optimizing corporate performance in Japan. This finding is supported by the pecking order theory and is consistent with previous empirical research, including, for example, the studies of Adachi-Sato and Vithessonthi (Citation2019), Nenu, Vintilă, and Gherghina (Citation2018), Le and Phan (Citation2017), and Zeitun and Haq (Citation2015). The validation test performed in validate the results of the fixed-effect estimators.

Table 4. Debt maturity, macroeconomic and institutional determinants of performance ROA. Individual fixed effects model.

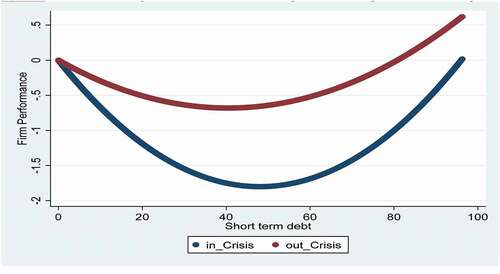

Furthermore, we examined the nonlinear relationship between debt structure and corporate performance with the aim of helping Japanese firms to establish the optimal debt structure for improving their performance. reveals that the nonlinear nexus between STDTD and firm performance is significant, just like in the studies of Nguyen and Nguyen (Citation2020), Raharja and Mranani (Citation2019), and Davydov (Citation2016). Our findings reveal a U-shaped correspondence between STDTD and firm performance. The threshold test in confirms the existence of a threshold impact of debt with short-term maturity on firm performance at an estimated point of 45.2% for Model 1, which supports our argument that a nonlinear correlation between debt structure and corporate performance exists. Thus, we accepted hypothesis H1b about the nonlinear (U-shaped) effect of debt with short-term maturity on corporate performance.

The U-shape for this relationship indicates that below 45.2%, the impact of STDTD on corporate performance is negative. However, once STDTD is above 45.2%, its impact on corporate performance becomes positive. This finding clearly indicates that at a low level of short-term debt (below 45.2%), managers are under less pressure and are less fearful of being dismissed from their positions, so there is less incentive for them to knuckle down and increase their firms’ performances, especially since the costs of borrowing and bankruptcy are low (Scott Citation1977). Managers may also tend to invest in less profitable and riskier projects that may contribute to lower corporate performance. Short-term debt at a low level therefore negatively affects corporate performance. This finding to some extent resembles that of Davydov (Citation2016), who reported a U-shape correlation between a bank’s debt ratio and corporate performance in terms of Tobin’s Q,Footnote2 but differs from the study of Raharja and Mranani (Citation2019), who reported an inverted U-shape relation between debt ratio and performance.

At a high level of debt with short-term maturity (above 45.2%), however, firms’ debt costs increase (Gordon Citation1971; Mu, Wang, and Yang Citation2017), tax deductions increase (Scott Citation1977), and more monitoring by creditors (Rajan and Zingales Citation1995; Hart and Moore Citation1998) due to creditor–manager agency problems. Managers are therefore under more pressure from creditors to guarantee the repayment of loans, and this minimizes the misuse of debt and encourages managers to invest in highly profitable projects that will improve corporate performance, due to the threat of being sacked by the shareholders. Furthermore, short-term debt, at a high level, helps to reduce the principal–agent problem (Diamond Citation1991; Harris and Raviv Citation1991; Myers Citation1977; Thanha, Canh, and Hac Citation2020). Consequently, a high level of short-term debt (over 45.2%) positively affects corporate performance in Japan because managers are under pressure to increase corporate value. Thus, a firm’s optimal debt structure is a pivotal determinant of its performance.

Size was found to have a negative and significant influence on a firm’s performance. Increasing a firm’s size leads to poor corporate performance due to the diseconomies of scale, that result from increases in the average cost. This result is in line with those of other studies (e.g. Goddard, Tavakoli, and Wilson Citation2005; Shehata, Salhin, and El-Helaly Citation2017; among others). A firm’s liquidity negatively and significantly affected its performance. This finding is consistent with the agency theory, the trade-off argument, and previous empirical studies (e.g. Myers and Rajan Citation1995; Jensen and Meckling Citation1976; Adachi-Sato and Vithessonthi Citation2019; Nenu, Vintilă, and Gherghina Citation2018). Growth was found to have a significant positive influence on a firm’s performance, indicating that firms with greater growth opportunities are expected to perform better (Custódio, Ferreira, and Laureano Citation2013). Firm performance was also positively but insignificantly affected by risk.

The effect of the financial crisis

A firms’ access to short-term debt, during a financial crisis, becomes more limited due to tight credit policies, and this may affect their ability to meet their obligations (e.g. Judge and Korzhenitskaya Citation2012; Vithessonthia and Tongurai Citation2015; Adachi-Sato and Vithessonthi Citation2019) and take advantage of investment opportunities that may improve their firm’s performances. As shown in , Models 2–5, the Dcrisis coefficient was significantly negatively affected corporate performance, which agrees with previous studies, such as those of Zeitun and Haq (Citation2015) and other studies. Indeed, the negative coefficient for Dcrisis implies that firms become less profitable during times of financial distress. Thus, we accept hypothesis H2a about the negative and significant impact of the financial crisis on corporate performance in Japan.

To further investigate the effect of the 2008 GFC on the nonlinear nexus of short-term debt and corporate performance, we included cross effects of the Dcrisis dummy on the short-term debt ratio. The first cross effect was STDTD*Dcrisis, and the second was STDTD2*Dcrisis. The results shown in , and Columns 1 and 3 reveal that the respective coefficients of the two cross effects are significant.

Table 5. Debt maturity and firm performance using ROA (Cross effect: crisis with short-term debt).

As shown in , the validity test for the fixed-effects model and the threshold estimates test are significant for the estimated models. In addition, the Fisher test for the cross effect between short-term debt and Dcrisis () is significant for all the specifications selected. This therefore supports the existence of a moderating effect of the financial crisis on the nonlinear nexus between short-term debt and corporate performance. We therefore accepted hypothesis H2b. This finding further indicates that the nonlinear effect of short-term debt is crucial to corporate performance, particularly during financial crises and economic downturns (Wang and Chiu Citation2019). One explanation for this is that firms have a high demand for debt with short-term maturity in order to fund their operations and mitigate the pressure on liquidity during this period (e.g. Ivashina and Scharfstein Citation2010; González Citation2015; Adachi-Sato and Vithessonthi Citation2019). In addition, a firm’s ability to access bank credit during the financial crisis decreased due to the strict, conservative credit policies that were adopted by banks, so firms became more vulnerable to higher borrowing and bankruptcy costs during the GFC (Adachi-Sato and Vithessonthi Citation2019; González Citation2015), and this of course affected firms’ performances negatively. The significant severe negative impact of the GFC on short-term debt and corporate performance has been indicated in some previous studies, including those of Zeitun and Haq (Citation2015) and Wang and Chiu (Citation2019), among others. The estimated coefficients for the firm-level control factors were as expected and similar to the previous results reported in .

show that a U-Shaped relationship existing between firm performance and short-term debt, with there being a higher threshold effect due to the financial crisis. The cutoff point for the ratio of STDTD during the crisis period is 44.5%, compared to 32.6% for the out-of-crisis period. A stronger, more pronounced nonlinear relation between corporate performance and short-term debt due to the financial crisis was found, with there being a higher threshold effect in line with the imposition of a higher recovery cost, which provides extra support for hypothesis H2b.

Figure 1. (a) Non-Linear relationship between short-term debt and firm performance during crisis and out of crisis periods*. (b) Marginal effect of an increase of 1% in STDTD on ROA**.

Figure 1. (b) Marginal effect of an increase of 1% in STDTD on ROA**.

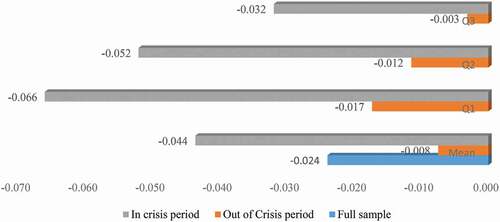

presents the estimated responses of firm performance to changes in short-term debt for the full period, the crisis period, and the out-of-crisis period, according to EquationEquation (3)(3)

(3) . This effect is computed for the sample mean and quartiles of the short-term debt ratio. Since the short-term debt values are below the estimated threshold, the marginal effect of short-term debt on ROA should be negative. The results reveal a significant negative differential influence of the financial crisis on the performance of firms with short-term debt at a low level. For the selected values of short-term debt, an increase of 1% in the STDTD decreased corporate performance by 0.03% and 0.06% during the GFC. This devastating effect is greater than in the out-of-crisis period (i.e. before and after the GFC), by 0.003% and 0.017%, especially at low levels of the short-term ratio.

Threshold analysis by industry

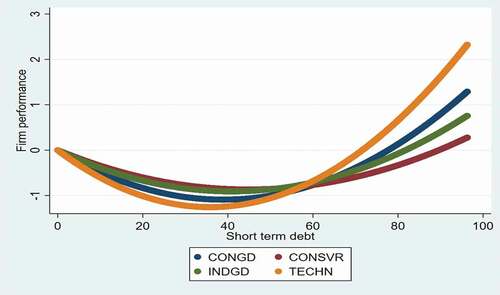

A sectorial analysis was conducted by examining the threshold effects of debt with short-term maturity on corporate performance for the four industrial sectors (CONGD, INDGD, CONSVR and TECHN) to validate our findings. presents the results of the regressions for investigating the nonlinear relation between debt structure and firm performance by industry. Overall, our empirical findings show a significant nonlinear link between STDTD and firm performance for all four sectors.Footnote3

Table 6. Sectorial analysis. Short-term debt and firm performance, by industry.

The significance of the threshold test in confirms the existence of a threshold impact of short-term debt on corporate performance for the four sectors, with a lowest threshold value being for the technology sector (35.8%) and the highest value being for the consumer services sector (44.8%). Firms operating in the technology industry adopted a low short-term debt policy because they had the greatest liquidity and profitability ratios among all the various sectors, thus justifying a lower threshold value for this sector. This finding suggests that these firms had greater cash flow from operations and thus greater access to debt instruments with shorter maturities, leading to it having the lowest threshold ratio. The results also indicate that firms operating in the consumer services sector had the lowest growth rate, which helps explain their higher threshold value compared to other industries, because they have less cash flow from their operations and less access to debt instruments with shorter maturities. The results show that an increase of 1% in the short-term debt reduces corporate performance by 0.023% in the consumer services industry, 0.026% in the consumer goods sector, and 0.029% in the technology industry. The results suggest that size and growth significantly affect firm performance in the four sectors. Liquidity negatively and significantly influences firms’ performances in the INDGD and CONSVR sectors. Inflation, GDP growth, and control of corruption are significantly affect firm performance in the four sectors.

shows a U-shaped relation between firm performance and short-term debt, with there being different cutoff points for short-term debt for INDGD, CONGD, CONSVR, and TECHN. Interestingly, the figure also shows that in the technology sector, when STDTD is below 35.8%, short-term debt’s effect on firm performance is negative. However, once STDTD is above 35.8%, its impact on performance becomes positive for firms operating in this sector. It is interesting that firms operating in the technology sector can shift very quickly to a positive increase in firm performance when extending their short-term debt, compared to other industries, thanks to their high capacity for innovation.

Figure 2. Short-Term debt and firm performance, by industry. A U-Shaped relationship*.

Sensitivity analysis

In this section, we conducted several tests to confirm the robustness of our results in the previous sections. In particular, we examined the sensitivity of our findings to additional control variables and an alternative performance measure, as well as tested a static versus dynamic model to shed light on the nonlinear relationship between short-term debt and corporate performance. Our findings were robust with additional control variables, an alternative performance measure, and other specification models.

Alternative measure of performance

A sensitivity analysis was conducted by testing the robustness of the results of the selected model (1a) utilizing Tobin’s Q as an alternative measure of performance. The objective was to improve our understanding of the nature of the relationship between short-term debt and corporate performance and validate our findings. For all the specifications tested using Tobin’s Q, as a measure of performance, the results shown in confirm the robustness of the nonlinear threshold link between short-term debt and corporate performance. presents the estimated threshold effects for the short-term debt ratio for the whole sample when using the Tobin’s Q performance measure, thus confirming the U-shaped association between short-term debt and corporate performance, which is consistent with the above findings. Our results are therefore robust and allow us to make more-conclusive recommendations. Interestingly, we also observed some important phenomena. First, there is a significant nonlinear nexus between short-term debt and corporate performance (using both ROA and Tobin’s Q). Second, the threshold for short-term debt is lower when using Tobin’s Q (31.6%), compared to 41.4% when using ROA, in Model 4, with there being a higher estimated response of corporate performance to changes in short-term debt when using ROA (e.g. −0.024 in Model 4, ) compared to Tobin’s Q (e.g. −0.0011 in Model 4, ).

Table 7. Sensitivity analysis using Tobin’s Q performance measure for all period (Full sample).

Additional control variables

We added some external factors that affect corporate performance, including country-specific macroeconomic and institutional quality factors, to further test the robustness and validate our empirical findings. The results are shown in (Columns 2–4), (Column 3), and (Columns 2–4), and these are consistent with our findings in Column 1 of , which were presented in previous subsections. Consequently, our findings were deemed valid and robust. The threshold test in the estimated model that includes macroeconomic and institutional quality factors confirms the existence of a highly significant threshold impact of short-term debt on corporate performance.

Interestingly, the threshold value obtained for Model 4 is lower than the one obtained for Model 1 without macroeconomic and institutional quality factors, indicating that the nonlinear link between firm performance and short-term debt depends on GDP growth, inflation, and corporate governance. In all models, inflation has a significant negative effect on performance, while GDP growth has a significant positive impact on firm performance, and inflation has a negative and significant impact on performance. Moreover, the results also indicate that controlling corruption is the most important determinant of corporate performance with a significant positive influence. This finding confirms the importance of good quality governance for boosting firm performance in Japan.

Dynamic model

reports the quasi-maximum likelihood estimation for the dynamic model (4) for robustness check analysis in order to validate our previous findings using alternative estimation method. Our results are consistent with those reported for the static model. There is a U-shaped relationship between firm performance and short-term debt with a significant threshold effect estimated within the 38%–45.5% range, confirming the existence of a nonlinear nexus between short-term debt and company performance.Footnote4 Firm size and liquidity were also significantly associated with corporate performance, while sales growth was only significant for Model 4. In addition, we found a significant positive relation between risk and corporate performance (ROA), which is consistent with the tradeoff theory, which states that as risk increases, the rate of return increases. Our findings also confirm the significant negative effect of the financial crisis on company performance. Moreover, inflation, GDPG, and the control of corruption confirmed their expected effect on corporate performance.

Table 8. Sensitivity analysis. Debt maturity and firm performance using ROA. Dynamic model. Quasi maximum likelihood estimation with fixed effects.

VI. Conclusions and implications

This study has investigated the nonlinear nexus between debt structure and firm performance based on evidence from Japan. It considered a sample of 1,670 companies in Japan from eight industrial sectors. Despite the importance of debt structure in terms of maturity, the vast majority of empirical studies have investigated the relationship between total debt and corporate performance and value, and there is a persistent gap in the empirical research for the influence of debt structure on corporate performance, especially during economic downturns and financial crises, both for emerging and developed countries. No study, to the best of our knowledge, has yet investigated whether a nonlinear relationship exists between corporate performance and debt with short-term maturity, specifically in Japan. In addition, our study investigated the effect of the 2008 GFC on the nonlinear nexus between short-term debt and firm performance.

The findings of this study will be highly relevant for investors, stakeholders, and policymakers in financial institutions by helping them to understand the factors that determine a firm’s performance, as well as the optimal debt structure for maximizing firm performance and value. Moreover, the findings will help stakeholders to pay more attention to the intricate interactions among the different variables, both internally and externally, affecting the relationship between debt structure and performance for a firm, and help them to mitigate the impacts of economic uncertainty and financial crises.

Our empirical results confirm the nonlinear impact of short-term debt on corporate performance. The existence of a short-term debt threshold proves the existence of an optimal debt structure that can contribute significantly to enhancing performance, implying that firms operating in Japan need to identify their optimal debt structure (i.e. mix of short- and long-term debt) for boosting performance. Moreover, we found that the U-shaped relationship between corporate performance and short-term debt differed between the crisis period and the out-of-crisis period, with there being a higher cutoff during the crisis period (44.5%) compared to the out-of-crisis period (32.6%). The financial crisis therefore had a significant detrimental effect on the nexus between corporate performance and short-term debt. The findings clearly indicate that the importance of short-term debt due to pressures on liquidity and the firms’ need for short-term debt increased during the crisis period.

In addition, investigating how the threshold effect for the nexus between short-term debt and firm performance varied by sector revealed many discrepancies between the sectors, which may help decision-makers to predict the patterns and thresholds for the nexus between firm performance and short-term debt based on the industry.

Our study has some limitations and suggestions for future research. First, our sample study only considered listed firms in Japan. Therefore, it would be helpful for a future study to include other countries in order to make cross-country comparisons. In addition, a comparative analysis could be conducted using the fixed effect panel threshold model, Hansen (Citation1999). Furthermore, other institutional variables (e.g. regulatory effectiveness), stock market development, and financial development could be employed in future studies to investigate their impact on corporate performance, specifically during a crisis period.

Acknowledgement

We would like to thank the Editor-in-Chief Prof. Mark Taylor and the anonymous reviewers for their helpful comments and suggestions. Other errors are our own. Open Access funding provided by the Qatar National Library.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Notes

1 In STATA, the QML procedure is available with the command xtdpdml. According to Kripfganz (Citation2016) if all the assumptions are secured and the time horizon is short, QML estimation can provide a gain in effectiveness in dealing with the endogeneity of a lagged dependent variable in the utilized linear dynamic panel data models. For a more recent discussion of dynamic panel modeling using the maximum likelihood technique as an alternative to the GMM-Arelleno-Bond method, see the work of Moral-Benito, Allison, and Williams (Citation2019).

2 In their study, Thanha, Canh, and Hac (Citation2020) reported a U-shaped relation between earnings management and the debt ratio by providing evidence from Vietnam, with a threshold value of 57.142% for total liability to total assets.

3 It is worth mentioning that we also ran the regressions for the basic material, healthcare, telecoms, and oil and gas industries, but we found that there was only an insignificant nonlinear relationship between STDTD and firm performance in these industries.

4 It is worth mentioning that we also ran ordinary least squares (OLS) regressions that further reinforced our previous findings about the existence of a nonlinear nexus between short-term debt and company performance.

References

- Adachi-Sato, M., and C. Vithessonthi. 2019. “Corporate Debt Maturity and Future Firm Performance Volatility.” International Review of Economics and Finance 60: 216–237. doi:10.1016/j.iref.2018.11.001.

- Barclay, M. J., and C. W. Smith. 1995. “The Maturity Structure of Corporate Debt.” The Journal of Finance 50 (2): 609–631. doi:10.1111/j.1540-6261.1995.tb04797.x.

- Campello, M., J. R. Graham, and C. R. Harvey. 2010. “The Real Effects of Financial Constraints: Evidence from a Financial Crisis.” Journal of Financial Economics 97 (3): 470–487. doi:10.1016/j.jfineco.2010.02.009.

- Custódio, C., M. A. Ferreira, and L. Laureano. 2013. “Why are US Firms Using More Short-Term Debt?” Journal of Financial Economics 108 (1): 182–212. doi:10.1016/j.jfineco.2012.10.009.

- Davydov, D. 2016. “Debt Structure and Corporate Performance in Emerging Markets.” Research in International Business and Finance 38: 299–311. doi:10.1016/j.ribaf.2016.04.005.

- Diamond, D. W. 1991. “Debt Maturity and Liquidity Risk.” The Quarterly Journal of Economics 106: 709–737. doi:10.2307/2937924.

- Dolenc, P., A. Grum, and S. Laporsek. 2012. “The Effect of Financial/economic Crisis on Firm Performance in Slovenia–a Micro Level, Difference-in-Differences Approach.” Montenegrin Journal of Economics 8 (2): 207–222.

- Donadelli, M., M. Fasan, and B. S. Magnanelli. 2014. “The Agency Problem, Financial Performance and Corruption: Country, Industry and Firm Level Perspectives.” European Management Review 11: 259–272. doi:10.1111/emre.12038.

- Goddard, J., M. Tavakoli, and J. O. S. Wilson. 2005. “Determinants of Profitability in European Manufacturing and Services: Evidence from a Dynamic Panel Model.” Applied Financial Economics 15 (18): 1269–1282. doi:10.1080/09603100500387139.

- González, V. M. 2015. “The Financial Crisis and Corporate Debt Maturity: The Role of Banking Structure.” Journal of Corporate Finance 35: 310–328. doi:10.1016/j.jcorpfin.2015.10.002.

- Gordon, M. J. 1971. “Towards a Theory of Financial Distress.” The Journal of Finance 26 (2): 347–356. doi:10.1111/j.1540-6261.1971.tb00902.x.

- Hansen, B. E. 1999. “Threshold Effects in Non-Dynamic Panels: Estimation, Testing, and Inference.” Journal of Econometrics 93 (2): 345–368. doi:10.1016/S0304-4076(99)00025-1.

- Harris, M., and A. Raviv. 1991. “The Theory of Capital Structure.” The Journal of Finance 46 (1): 297–355. doi:10.1111/j.1540-6261.1991.tb03753.x.

- Hart, O., and J. Moore. 1998. “Default and Renegotiation: A Dynamic Model of Debt.” The Quarterly Journal of Economics 113 (1): 1–41. doi:10.1162/003355398555496.

- Hsiao, C., M. H. Pesaran, and A. K. Tahmiscioglu. 2002. “Maximum Likelihood Estimation of Fixed Effects Dynamic Panel Data Models Covering Short Time Periods.” Journal of Econometrics 109 (1): 107–150. doi:10.1016/S0304-4076(01)00143-9.

- Ivashina, V., and D. Scharfstein. 2010. “Bank Lending During the Financial Crisis of 2008.” Journal of Financial Economics 97 (3): 319–338. doi:10.1016/j.jfineco.2009.12.001.

- Jensen, M., and W. Meckling. 1976. “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.” Journal of Financial Economics 3 (4): 305–360. doi:10.1016/0304-405X(76)90026-X.

- Judge, A., and A. Korzhenitskaya. 2012. “Credit Market Conditions and the Impact of Access to the Public Debt Market on Corporate Leverage.” International Review of Financial Analysis 25: 28–63. doi:10.1016/j.irfa.2012.09.003.

- Khurana, I. K., and C. Wang. 2015. “Debt Maturity Structure and Accounting Conservatism.” Journal of Business Finance & Accounting 42: 167–203. doi:10.1111/jbfa.12104.

- Kripfganz, S. 2016. “Quasi–maximum Likelihood Estimation of Linear Dynamic Short-T Panel-Data Models.” The Stata Journal 16 (4): 1013–1038. doi:10.1177/1536867X1601600411.

- Krivogorsky, V., G. H. Joh, and D. DeBoskey. 2018. “The in?uence of Supply Side Factors on ?rm’s Borrowing Decisions: European Evidence.” Global Finance Journal 35: 202–222. doi:10.1016/j.gfj.2017.10.008.

- Le, T. P. V., and T. B. N. Phan. 2017. “Capital Structure and Firm Performance: Empirical Evidence from a Small Transition Country.” Research in International Business and Finance 42: 710–726. doi:10.1016/j.ribaf.2017.07.012.

- Leland, H. E., and K. B. Toft. 1996. “Optimal Capital Structure, Endogenous Bankruptcy, and the Term Structure of Credit Spreads.” The Journal of Finance 51 (3): 987–1019. doi:10.1111/j.1540-6261.1996.tb02714.x.

- Moral-Benito, E., P. Allison, and R. Williams. 2019. “Dynamic Panel Data Modelling Using Maximum Likelihood: An Alternative to Arellano-Bond.” Applied Economics 51 (20): 2221–2232. doi:10.1080/00036846.2018.1540854.

- Mu, C., A. Wang, and J. Yang. 2017. “Optimal Capital Structure with Moral Hazard.” International Review of Economics and Finance 48: 326–338. doi:10.1016/j.iref.2016.12.006.

- Myers, S. 1977. “Determinants of Corporate Borrowing.” Journal of Financial Economics 5 (2): 147–175. doi:10.1016/0304-405X(77)90015-0.

- Myers, S., and R. G. Rajan. 1995. “The Paradox of Liquidity.” Working Paper W5143. Cambridge, MA: National Bureau of Economic Research.

- Nenu, E., G. Vintilă, and S. Gherghina. 2018. “The Impact of Capital Structure on Risk and Firm Performance: Empirical Evidence for the Bucharest Stock Exchange Listed Companies.” International Journal of Financial Studies 6 (41): 1–29. doi:10.3390/ijfs6020041.

- Nguyen, L., and C. Nguyen. 2020. “Financial Constraints, Corporate Debt Maturity and Firm Performance: The Case of Firms in Southeast Asian Countries.” Afro-Asian Journal of Finance and Accounting 10 (1): 48–59. doi:10.1504/AAJFA.2020.104404.

- Nishioka, S., and N. Baba. 2004. “Dynamic Capital Structure of Japanese Firms: How Far Has the Reduction of Excess Leverage Progressed in Japan?, Bank of Japan.” Working Paper Series 04-E-16. Bank of Japan.

- Ozkan, A. 2002. “The Determinants of Corporate Debt Maturity: Evidence from UK Firms.” Applied Financial Economics 12 (1): 19–24. doi:10.1080/09603100110102691.

- Raharja, B., and M. Mranani. 2019. “The Nonlinear Effect of Debt on Firm Performance: The Evidence from Indonesia.“ Jurnal Ekonomi Malaysia 53 (3): 3–9.

- Rai, A., and V. Danilevskaia. 2005. “Choice of Short-Term and Long-Term Debt in Five Eastern European Countries.” Journal of International Business Law 4 (1): 34–56.

- Rajan, R., and L. Zingales. 1995. “What Do We Know About Capital Structure? Some Evidence from International Data.” The Journal of Finance 50 (5): 1421–1460. doi:10.1111/j.1540-6261.1995.tb05184.x.

- Rauh, J. D., and A. Sufi. 2010. “Capital Structure and Debt Structure.” The Review of Financial Studies 23 (12): 4242–4280. doi:10.1093/rfs/hhq095.

- Schiantarelli, F., and A. Sembenelli. 1997. “The Maturity Structure of Debt: Determinants and Effects on Firms’ Performance: Evidence from the United Kingdom and Italy.” Working paper. Washington: The World Bank.

- Scott, J. 1977. “Bankruptcy, Secured Debt, and Optimal Capital Structure.” The Journal of Finance 32 (1): 1–19. doi:10.1111/j.1540-6261.1977.tb03237.x.

- Shehata, N., A. Salhin, and M. El-Helaly. 2017. “Board Diversity and Firm Performance: Evidence from the U.K. Smes.” Applied Economics 49 (48): 1–16. doi:10.1080/00036846.2017.1293796.

- Thanha, S. D., N. P. Canh, and N. T. T. Hac. 2020. “Debt Structure and Earnings Management: A Non-Linear Analysis from an Emerging Economy.” Finance Research Letters 35: 1–14.

- Tirapat, S., and A. Nittayagasetwat. 1999. “An Investigation of Thai Listed Firms’ Financial Distress Using Macro and Micro Variables.” Multinational Finance Journal 3 (2): 103–125. doi:10.17578/3-2-2.

- Titman, S., and R. Wessels. 1988. “The Determinants of Capital Structure Choice.” The Journal of Finance 43 (1): 1–19. doi:10.1111/j.1540-6261.1988.tb02585.x.

- Tsuji, C. 2019. “Corporate Profitability and Capital Structure: The Case of the Machinery Industry Firms of the Tokyo Stock Exchange.” International Journal of Business Administration 4 (6): 14–21. doi:10.5430/ijba.v10n6p14.

- Vithessonthia, C., and J. Tongurai. 2015. “The Effect of Firm Size on the Leverage–performance Relationship During the Financial Crisis of 2007–2009.” Journal of Multinational Financial Management 29: 1–29. doi:10.1016/j.mulfin.2014.11.001.

- Wang, C. W., and W. C. Chiu. 2019. “Effect of Short-Term Debt on Default Risk: Evidence from Pacific Basin Countries.” Pacific-Basin Finance Journal 57 (Forthcoming): 101026. doi:10.1016/j.pacfin.2018.05.008.

- Yildirima, R., M. Masihb, and O. Ismath. 2018. “Bacha Determinants of Capital Structure: Evidence from Shari’Ah Compliant and Non-Compliant ?rms.” Pacific-Basin Finance Journal 51: 198–219. doi:10.1016/j.pacfin.2018.06.008.

- Zeitun, R., and G. Haq. 2015. “Debt Maturity, Financial Crisis and Corporate Performance in GCC Countries: A Dynamic-GM Approach.” Afro-Asian Journal of Finance and Accounting 5 (3): 231–247. doi:10.1504/AAJFA.2015.070291.

- Zhang, R., and Y. Kanazaki. 2007. “Testing Static Tradeoff Against Pecking Order Models of Capital Structure in Japanese Firms.” International Journal of Accounting and Information Management 15 (2): 24–36. doi:10.1108/18347640710837335.