?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper explores the viability of the fiscal policy in the reconstruction of the Syrian economy. We use the Structural VAR estimation technique to assess the response of real GDP to shocks in government expenditures and exchange rates in the parallel market. We also control for other variables including money supply and oil prices. We find that government spending is an effective tool for economic recovery in particular under a quasi-fixed exchange rate regime. We also employ the nonlinear ARDL (NARDL) model to detect the existence of asymmetrical effects of government spending on real GDP. The NARDL results show that negative changes in government expenditure have more impact on economic growth compared to positive changes. Additionally, the NARDL model reveals that the post-conflict period was characterized by large government spending’ inefficiencies. Finally, we study three alternative government spending’ rebuilding scenarios. We document that reaching the pre-conflict GDP level is possible under two of the scenarios we investigate. Hence, our results provide strong policy implications according to which fiscal policy can, under specific exchange rate regimes, reverse the adverse effects of civil wars.

I. Introduction

In the last few decades, fiscal policies and monetary policies have been widely used to overcome recessions. However, their effectiveness in rescuing the economy following wars is yet to be proven. In times of civil unrest, local currencies are subject to enormous pressures (inflation, rapid depreciation, and establishment of black markets) limiting significantly the expected benefits of monetary policies. Therefore, most governments would often resort to fiscal policies to boost the economic activity and re-establish social peace.

The assertion that fiscal policies (tax policy, debt policy, government spending policy) aiming at stimulating human capital and productivity can lead to economic growth has attracted substantial debate among economists (Tendengu, Kapingura, and Tsegaye Citation2022; Tilahun Mengistu Citation2022; Twinoburyo and Odhiambo Citation2018; Zagler and Dürnecker Citation2003). Supporters of the Keynesian framework, embodied in the traditional Investment – Saving and Liquidity preference – Money supply (IS-LM) model, advocate that the fiscal policy is persistently effective in closed economy and can significantly improve economic output during recessions (Krugman Citation2015; Romer Citation2012). The new Keynesian model, however, highlights that, due to price rigidities, fiscal policies may have temporary effects on economic growth (Palley Citation2012). Within this framework, the extent of fiscal policy’s impact on the real economy depends on the anticipation of the contemporary and projected government expenditures (Woodford (Citation2007). For an open economy, the Mundell-Fleming model (extension of the IS-LM model) predicts that the final impact on economic growth depends on the foreign exchange rate regime and the level of economic openness (Mishkin Citation2012). Within this context, the exchange rate plays a crucial role in the effectiveness of the fiscal policy (Hlongwane, Mongale, and Lavisa Citation2018).

This paper investigates if the predictions of the above economic theories apply to recessions resulting from civil wars. It is now well-established that the destruction resulting from conflicts negatively affects economic growth and social wellbeing (Koubi Citation2005; De Groot Citation2010). Usually, civil wars lead to casualties among civilians and induce large movements of populations fleeing the conflict zones. Eventually, the dramatic consequences of the unrest would adversely affect the development of a nation imposing severe challenges to any potential recovery by the end of the conflict (Arratibel et al. Citation2011; Bilgel and Karahasan Citation2019).

While there are several currently ongoing civil wars in the world, the Syrian crisis emerges as one of the most complicated conflicts and stands as a candidate for being the largest humanitarian tragedy of the 21st century (Rizkalla and Segal Citation2018). The fact that Syria belongs to the Middle East and North Africa (MENA), a region that is notorious for being the scene of several civil wars, adds to the complexity of this crisis.

During the Syrian conflict, the public institutions, means of production, and channels of trade were highly disrupted. As a result, the use of the fiscal policy in Syria displays specific challenges where policymakers need to rebuild the destroyed capital and find enough funds for regular expenditures. Additionally, they have to determine the optimal distribution of resources between military and social expenditures.

Historically, the fiscal policy in Syria depends mainly on oil and tax revenues (Diwan and Akin Citation2015). However, oil revenues witnessed a dramatic decline during the conflict period where the budget deficit in Syria reached around 30% of GDP in 2013 (Araji, Citation2017). To maintain government expenditure levels, the Syrian authorities had imposed several tax reforms to improve tax administration (Arslanian and Hinnebusch Citation2009) but the externalities of these reforms on economic growth remain unclear to date. Haddad (Citation2004) indicates that the fiscal policy in Syria suffers from many shortcomings such as the large government subsidies. Additionally, the category named ‘other expenditures’, which hovers around 25% of the total Syrian budget, has no obvious effects on economic growth.

In addition to the above limitations, the success of the fiscal policy depends also on the performance of the local foreign exchange market. In Syria, the typical rules governing financial markets do not hold. Indeed, many transactions occur in the black market where people tend to minimize the use of local currency and seek safer investments such as foreign currencies and precious metals (Tony, Chowdhury, and Mansoob Murshed Citation2002). As more transactions occur in unregulated markets, the local currency will depreciate leading potentially to economic contraction. However, exchange rate depreciations may, in some cases, improve growth via an increase in exports. For instance, the ‘export-led growth paradigm’, in which a country may achieve economic development by engaging in international trade, builds on the idea that exchange rate depreciations improve the competitiveness of exports leading to an increase in the steady-state economic growth rate.

Given the scarcity of research on the effects of fiscal policies and exchange rate regimes on the economy during civil wars, our paper adds to the existing literature in several ways. Our first contribution is to assess the current situation of the Syrian economy using the IS – LM model. Within this model, we analyse the dynamics of economic growth in terms of government spending and exchange rates for the period (1990–2017). We also control for the effects of money supply and oil prices. Our second contribution in this paper is to investigate the potential nonlinear response of GDP growth to shocks in government expenditure, exchange rates in the parallel market, money supply and oil prices. The estimation is performed using the Structural Vector Autoregression (SVAR) and the Nonlinear Autoregressive Distributed Lag (NARDL) models. The SVAR model separates government expenditure shocks, exchange rate shocks, money supply shocks, and oil price shocks while the NARDL framework is used to study the influence of such shocks on the real GDP in Syria. The NARDL model has several merits. First, it can be used when variables are not integrated or are integrated of order one. Second, the NARDL model can use different lag orders for all variables. Third, it can be applied for small samples and provides robust results. Finally, this model allows testing for hidden cointegration and differentiating between nonlinear cointegration, linear cointegration, and lack of cointegration.

More importantly, we contribute to the existing literature by exploring three potential scenarios of recovery in the post-conflict period (optimistic, moderate, and pessimistic) using several assumptions of reconstruction based on international aid (i.e. capital inflows) and refugee’s repatriation. These assumptions rely on three possible government expenditure’ growth scenarios under alternative exchange rate regimes. We find that government expenditure is the most effective tool of economic recovery especially under a quasi-fixed exchange rate regime. Moreover, the NARDL results show that negative changes in government expenditure have more impact on economic growth than positive changes. The NARDL model also reveals that government expenditure is more effective in inducing growth when the funds are spent in productive investments. Finally, we find that recovering the 2010 GDP level is possible under two of the scenarios we investigate.

The remainder of the paper proceeds as follows. Section II exposes the literature review. Section III discusses the methodology employed in this paper. Section IV analyses the empirical findings. Finally, section V concludes.

II. Literature review

The exogenous and endogenous economic growth models advocate the importance of real variables. One challenge in using these models to study the impact of civil wars on growth is the unavailability of updated real data. For this reason, the IS – LM model emerges as a suitable alternative to explore economic growth in conflict zones since the variables included in this model can be easily collected even in countries affected by conflicts.

The first variable that is usually included in the IS – LM model is the government expenditure. The Keynesian school of thought advocates the use of fiscal policies to boost economic activity in times of recessions. In this context, using the ARDL model, Tendengu, Kapingura, and Tsegaye (Citation2022) investigate the impact of fiscal instruments such as government investment, consumption and taxation on economic growth in South Africa. Their empirical findings confirm that economic growth responds positively to increases in these variables, particularly when government increases its spending in investment and unproductive sectors. Similar results are found by Tilahun Mengistu (Citation2022) in the context of the Ethiopian economy using the ARDL model. Moreover, Hlongwane, Mongale, and Lavisa (Citation2018) employ the VECM approach to examine the relationship between the fiscal policy and economic growth in South Africa. They argue that tax revenues have a positive impact on economic growth in the long run, while budget deficit adversely affects economic growth.

Yusuf and Mohd (Citation2021) investigate the nonlinear response of economic growth to disaggregated fiscal policy variables (spending, debt, and taxes) in Nigeria using a nonlinear ARDL model. They reveal that these variables have asymmetric impact on economic growth. Hussain, Rafiq, and Khan (Citation2020) study the dynamic relationship between primary fiscal deficit and economic growth in Pakistan using a nonlinear ARDL model. They find that an expansionary fiscal policy which is associated with fiscal deficit has a negative impact on economic growth. In the same context, Ocran (Citation2011) investigates the impact of fiscal policy stance on economic growth in South Africa using Structural VARs approach. His findings reveal that fiscal policy instruments have a small and persistent impact on the level of output. Arratibel et al. (Citation2011) employ the IS-LM framework to assess the impact of fiscal deficit, exchange rate volatility, and trade openness. They find that exchange rate volatility has a negative impact on economic growth whereas fiscal deficit and trade openness have a positive impact. In the same vein, Zagler and Dürnecker (Citation2003) explore the impact of fiscal policy on economic growth in the recent literature. They find that several government spending and tax policies have a direct impact on economic growth.

The second variable that is usually included in the IS – LM model is the exchange rate. While the majority of the research employing this variable concluded that currency depreciation might spur economic growth through its impact on traded sectors, especially in developing countries (Rodrik Citation2008; Belloumi Citation2010), the results of this literature differ depending on the countries’ specific conditions and on the sample-selection (Ha and Hoang Citation2020; Bohl, Michaelis, and Siklos Citation2016; Petreski Citation2009). For example, Ha and Hoang (Citation2020) investigate the impact of the exchange rate regime on economic growth in Asian economies using the GMM approach. Their empirical results emphasize that less flexible or flexible exchange rate regimes are associated with higher economic growth. They argued that Asian countries should avoid fully flexible or fixed currency exchange rate regimes (Husain, Mody, and Rogoff Citation2005; Dubas, Lee, and Mark Citation2005). Moreover, Petreski (Citation2009) finds that the exchange rate regime can affect economic growth via trade and investment channels. Bohl, Michaelis, and Siklos (Citation2016) reveal that fixed or pegged exchange rate regimes are more suitable for emerging economies while crawling or less flexible exchange rate regimes have better effects on economic growth in the G20 countries. They also find that pegged exchange rate regime would have a negative influence on economic growth during financial crises or economic shocks. Other studies find that high exchange rates volatility reduces economic growth through the trade channel (Arratibel et al. Citation2011).

The third variable often used to explain economic growth in the IS – LM context is money supply. While endogenous growth models have praised the role of real variables and ignored the role of monetary variables (Sidrauski Citation1967), a recent literature finds merits to monetary variables in explaining economic growth. This includes the work of Chaitip et al. (Citation2015) who investigate the long and short run relationship between money supply and economic growth using panel ARDL in several Asian countries. They find that the growth in money supply has a positive effect on economic growth in the short run and on its adjustment to the long run equilibrium. Similarly, Tabi and Ondoa (Citation2011) use a VAR approach in Cameron to show that increases in money supply enhance economic growth. Muhammad et al. (Citation2009) investigate the impact of money supply, among other variables, on economic growth in Pakistan. They reveal that money supply positively affects growth in the long run.

The theoretical research on the impact of civil wars on economic growth is mixed. On the one hand, several studies emphasize that conflicts have adverse effects on economic growth via several channels including the scarcity of capital and human resources and the destruction of infrastructure (Collier Citation1999; De Groot Citation2010; Brück and Olaf Citation2013; Ganegodage and Rambaldi Citation2014; Kimbrough, Laughren, and Sheremeta Citation2017). Moreover, civil wars lead to high opportunity costs as they discourage savings, reduce domestic investment and limit foreign direct investment. Collier (Citation1999) advocates that conflicts may lead to the use of government spending in unproductive actions and portfolio substitution. On the other hand, several researchers argue that military spending can have positive effects on aggregate demand similar to the impact of fiscal stimulus in the Keynesian economic theory (Ganegodage and Rambaldi Citation2014). Within this framework, military expenditures increase production and employment and enhance labour and capital productivity.

Our paper contributes to the above literatures by studying the differential effects of the government expenditure, exchange rates, money supply, and oil prices on economic growth resulting from civil wars. In particular, we focus on understanding which one of these macroeconomic variables has the highest impact on GDP in the Syrian economy and whether growth responds symmetrically to positive and negative changes in government expenditure. Once the relevant variables affecting economic growth are identified, this paper suggests several scenarios for recovery based on the SVAR and the nonlinear ARDL results.

III. Data and empirical methodology

Data

To investigate the relationship between real GDP growth, government expenditure, parallel market exchange rates, money supply, and oil prices and in the Syrian economy, we use quarterly data covering the period 1990Q1 up to 2017Q4. The data from 1990 to 2010 corresponds to the pre-conflict period whereas the data from 2011 to 2017 describes the post-conflict period. The data is extracted from Central Bureau of Statistics in Syria and the Central Bank of Syria (CBS). () includes the definition of the dependent and independent variables as well as the source of each variable whereas () reports the descriptive statistics for theses variables. () shows that the average real GDP is 944.8 billion Syrian Lira for the period 1990–2017 in constant 2000 prices. The average real GDP is a good indicator of the average wealth of a country over a specific period. However, the real GDP has a relatively high standard deviation and range reflecting the economic instability of the Syrian economy. The standard deviation of real GDP is a proxy of the variability of yearly real GDPs around the mean, while the range displays the highest difference between the yearly real GDPs observed over the same period. Interestingly, government expenditure is by far the most volatile variable with a standard deviation larger than the mean and median. Moreover, the range of the exchange rate and its standard deviation both point to the large depreciation of the Syrian Lira against the US dollar. The money supply was also extremely volatile where the magnitude of the standard deviation is within the same range as the mean and median. This indicates that Syrian policymakers have an active monetary policy. () also displays the kurtosis (a measure of whether the data are heavy-tailed or light-tailed) and skewness (a measure of the asymmetry) that allow comparison with the normal distribution.

Table 1. Definitions, proxies, and data sources of the dependent and independent variables.

Table 2. Descriptive statistics in Syrian Lira (1990–2017).

All variables are used in their logarithmic form. This log-transformation has three advantages. First, it mitigates the large variability in the data. Second, the coefficient of each variable can be interpreted as elasticity. Third, it helps to deal with the heteroscedasticity problem.

Empirical methodology

We employ two advanced econometric approaches: the Structural Vector Autoregression (SVAR) and the Nonlinear Autoregressive Distributed Lag (NARDL). These methods examine the dynamic response of real GDP growth to the aforementioned macroeconomic variables within the Syrian economy. Moreover, the empirical analysis considers the impact of the conflict period on the relationship between the variables.

The empirical implementation of the NARDL specification is based on the reduced form of the IS – LM model, which explains the interaction between the goods market (IS) and the money market (LM) (see for example Arratibel et al. Citation2011; Bahmani-Oskooee and Kandil Citation2010; Mrabet and Alsamara Citation2018). The conventional IS – LM model, which incorporates both the demand and supply sides of the economy, predicts that the real GDP can be explained by government spending (a proxy for fiscal policy), exchange rate movements, and money supply (a proxy for monetary policy). The effects of government spending and money supply are expected to be positive as they tend to boost the aggregate demand. Additionally, exchange rate appreciations are expected to improve real output through the expansionary effect (Kandil and Mirzaie Citation2002; Bahmani-Oskooee and Kandil Citation2010; Arratibel et al. Citation2011).

The SVAR model is applied to investigate the interactions between the macroeconomic variables and to assess their responsiveness to sudden shocks.

Supply and demand shocks on real GDP growth – SVAR model specification

We use the SVAR model to investigate the channels through which shocks to government expenditure, exchange rates, money supply, and oil prices affect the Syrian real GDP. The SVAR methodology is a variant of the VAR model introduced by Sims (Citation1980). However, the SVAR have some advantages over the typical VAR specification. First, the SVAR is based on a theoretical background to describe the dynamic behaviour of the macroeconomic time-series. Indeed, Blanchard and Quah (Citation1993) introduced the Structural VAR model where the economic theory is used to impose restrictions on the values of estimated residuals and recover the underlying structural disturbances. Second, the SVAR results are straightforward to interpret. Hence, the SVAR model is more suitable to investigate the interactions between macroeconomic shocks when restrictions are implemented.

Within the SVAR context, our empirical analysis uses the impulse response functions (IRFs) and the forecast error variance decomposition (FEVD) techniques to examine the impact of shocks to the variables included in the system.

The SVAR model under investigation can be written as follows:

where is a (5 × 5) matrix,

is a (5 × 1) vector of endogenous variables (

,

is a (5 × 1) structural uncorrelated innovations vector.

The covariance matrix of the structural disturbances has the following form:

, where I is the identity matrix.

Rearranging EquationEquation (1)(1)

(1) , we obtain the reduced form of our structural model given by:

where,

and

. The errors

are linear combinations of errors

, where the covariance matrix is:

.

To solve the system of equation in the SVAR model, it is imperative to tackle the identification problem by imposing specific restrictions on the selected variables. These restrictions are based on intuitions derived from economic theory and summarized as follows:

A positive shock to government expenditure will increase the real GDP (Keynesian theory). Additionally, following the J-curve theory, a positive shock to the parallel market exchange rate (local currency depreciation) will adversely affect the real GDP growth. Moreover, the real GDP growth will increase in response to money supply increases. According to the theoretical Keynesian model of economic growth, the money supply affects the aggregate demand and hence the equilibrium value of real GDP. Similarly, a positive shock to oil prices will result in a higher real GDP growth (given the impact on government revenues in oil exporting countries).

The growth in government expenditure is not affected by shocks to real GDP, exchange rate changes, and money supply. Given that Syria is an oil exporter, any increases in oil price changes may have a positive impact on government revenues and government expenditure.

The parallel market exchange rate changes are not directly affected by shocks to real GDP growth, government expenditure, money supply growth, and oil prices (given that Syria follows a pegged exchange rate regime).

The money supply change is not directly affected by shocks to government expenditure, exchange rates, and oil prices. Alternatively, an increase in real GDP may increase the money supply (the money demand theory).

The oil prices are not affected by the growth in real GDP, government expenditure, exchange rates, and money supply (because it is determined in international oil markets).

By adopting the above theoretical restrictions, we can write:

Nonlinear ARDL methodology

The dynamic error correction model (ECM) is commonly used to investigate the relationship between variables. The ECM is derived from the linear ARDL model. The standard ECM model representation is as follows:

where y is the explained variable and x is the set of explanatory variables. Occasionally, the relationship between y and x may be nonlinear. The motivation of using this model is the possibility to estimate the long-term relationship and the short-term dynamism between all variables. Moreover, this model allows us to identify the adjustment time to the equilibrium after a shock.

The positive and negative sub-variables are derived from the cumulative contribution of positive and negative shocks as follows: ;

. Accordingly, EquationEquation (3)

(3)

(3) can be modified to a nonlinear error correction model as follows:

Where and

In EquationEquation (4)(4)

(4) , p is the number of lags of the dependent variable while q is the number of lags of the independent variables. Δ denotes the difference of the variable. The superscripts (+)and(–)denote the positive and negative effects of x.

An F-test of the joint null hypothesis, is used to control for the presence of asymmetries in the long run relationship between variables. Additionally, the Wald test can be employed to control for the presence of short and long run asymmetries.

IV. Empirical results

The structural VAR estimation

One advantage of the SVAR model is the use of the impulse response functions (IRFs) and the forecast error variance decomposition (FEVD) analysis to examine the impact of any shock to the model variables and identify the main drivers of the dynamics in the system.

The Impulse Response Functions (IRFs) analysis

The IRFs trace the changes in the path of one variable given a shock to another variable. The borderlines in the IRFs figures represent the confidence interval. The middle line that lies between the two borderlines displays the response of real GDP growth to a shock in one of the selected macroeconomic variables. The horizontal line (the zero line) in the IRFs figures shows the time period (or horizon) after the initial shock whereas the vertical line displays the magnitude of response to shocks. When the horizontal line (the zero line) in the IRFs falls between the confidence bands, the impulse responses become statistically insignificant. Therefore, the null hypothesis of no effects of the macroeconomic variable shocks on real GDP growth cannot be rejected.

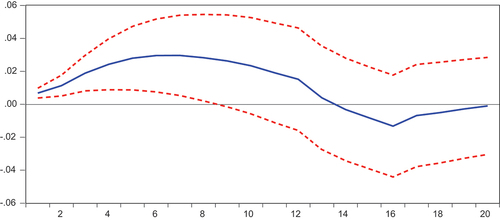

() illustrates the impulse response function of real GDP growth to government expenditure shocks. As can be observed in (), the impact of the government expenditure shock on real GDP growth is positive and statistically significant during the first 8 quarters. This finding is consistent with the Keynesian theory advocating that an increase in government expenditure induces economic growth. Hence, the fiscal policy can be effectively used to induce growth.

Figure 1. Response of real GDP growth to government expenditure changes.

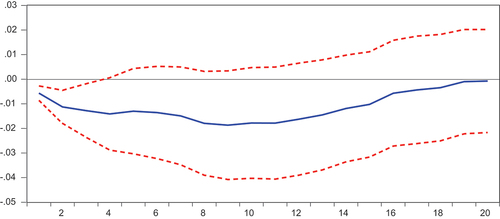

Figure 2. Response of real GDP growth to exchange rate changes.

() shows that the response of real GDP growth to a shock in money supply change is not statistically significant both in the short run and in the long run. This result emphasizes that money is neutral in the long-run and has no impact on real GDP growth in Syria. This result is in line with Moroney (Citation2002) where money explains inflation but not the real GDP growth.

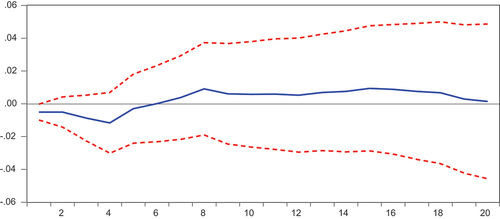

Figure 3. Response of real GDP growth to money supply changes.

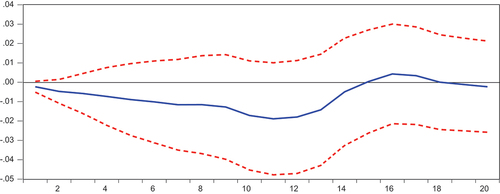

() displays the response of real GDP growth to a shock in oil prices. The results reveal the absence of any significant impact of this variable on real GDP growth in the short run and in the long run.

Figure 4. Response of real GDP growth to oil price changes.

The forecast error variance decomposition analysis

In addition to analysing the IRFs, the SVAR model also enables to study the decomposition of the error variance. The variance decomposition shows the proportion of the forecast error variance that is attributable to a variable’s own innovations and to innovations in other variables in the system. () displays the decomposition of the forecast error variance of the real GDP growth variable. () indicates that the percentage variation in real GDP growth due to a shock in government expenditure is 17% in the short run (the first 10 periods) and 33% in the long run (after 10 periods). () also reveals that the percentage variation in real GDP growth attributable to a shock in money supply is around 12% in the short run and 5% in the long run. Additionally, () shows that the exchange rate change explains 12% of the variations in real GDP growth in the short run and around 15% of the variations in the long run. The oil prices explain the variation of 2% in real GDP growth in the short run and 9% in the long run. Accordingly, government expenditure explains the variations in real GDP growth more than any other variable in the system followed by exchange rate, oil prices, and money supply, respectively.

Table 3. Forecast error variance decomposition of the dependent variable.

In summary, the results of the IRFs and the forecast error variance decomposition clearly show that, among all the policy tools investigated in this paper, the government expenditure avenue appears to be the most promising in inducing economic growth after the Syrian conflict. For this reason, the remainder of the paper implements several scenarios based on government expenditure changes and explores whether this policy tool can be considered as a rescue to the Syrian economy.

The nonlinear ARDL (NARDL) model estimation

The SVAR results emphasize that the government expenditure is the main contributor to real economic growth in Syria compared to money supply. This result is of paramount importance as it suggests that the Syrian government can effectively use government spending to spur growth with the hope of achieving social peace. In this section, we further assess whether government expenditure has an asymmetric effect on real GDP. Indeed, it is usually claimed that decreases in government expenditure would result in larger changes in real GDP compared to increases in government expenditure (Kandil Citation2001; Arratibel et al. Citation2011; Bahmani-Oskooee and Kandil Citation2010). To explore any potential asymmetrical effects, we employ the nonlinear ARDL methodology. Furthermore, we include a dummy variable for 2011 (dum2011 which takes the value of 1 for 2011 onward and 0 otherwise) and two interactive variables equal to the government expenditure (positive and negative changes) multiplied by the year 2011 dummy. These variables will detect any changes in the asymmetrical effects of government expenditure on the real GDP after the start of the uprising. Accordingly, the long run model of real GDP can be specified as follows:

Where is the logarithm of real GDP,

is the logarithm of the exchange rate in the parallel market,

and

are the logarithm of positive and negative changes in government expenditure, respectively. Finally,

is the logarithm of oil prices and

is the error term.

The nonlinear error correction model of real GDP derived from the NARDL can be written as follow:

() reports the estimation results for the asymmetric impact of government expenditure on real GDP when the NARDL model is used. The F-PSS cointegration test within the NARDL model in () shows the existence of a cointegration relationship between positive and negative changes in government expenditure and the real GDP in Syria.

Table 4. The asymmetric impact of government expenditure on real GDP (restricted model).

The estimation results of the unrestricted NARDL in () show that the short run coefficients of positive changes and negative changes in government expenditure are insignificant. The Wald test corroborates this finding and does not reject the null hypothesis of absence of significant effects of government expenditure on real GDP in the short run. Hence, we re-estimate a restricted model where we include the asymmetric long run impact of government expenditure on real GDP. The empirical results of the restricted NARDL model reported in () provide strong evidence that government expenditure (positive and negative changes) explain the long run behaviour of real GDP. Overall, the impact of higher government expenditure on real GDP is positive and statistically significant. More importantly, the results in () reveal that the response of real GDP to negative shocks in government expenditure is larger than its response to positive shocks. Specifically, a one percent increase in government expenditure (positive changes) leads to an increase in real GDP by 0.47% before conflict and 0.05% when we take into consideration the post 2011 civil war period. A plausible explanation of the lower effects of government expenditure, when the conflict period is included, is that most government expenditures after the conflict are not productive due to the large local currency depreciation and the exceptionally high inflation rates in the post conflict period (military expenditure, subsidies, infrastructure reconstruction, higher wages). In contrast, a one percent decrease in government expenditure (negative changes) leads to a decrease in real GDP by 2.3% before conflict and 8.2% when post-conflict period is included. The diagnostic tests reported in () show that the issues of autocorrelation and data normality do not affect the NARDL model results. It is clear from the Jarque-Berra (JB) normality test that the data used were normally distributed. Additionally, the autocorrelation () test confirms that the null hypothesis of no autocorrelation was not rejected.

() below summarizes the long run and short run nonlinear responses of real GDP to government expenditure changes before and after conflict.

Table 5. Summary of the asymmetric impact of government expenditure on real GDP.

In summary, the results of the SVAR model show that government expenditure is the most effective tool of economic recovery. Moreover, the NARDL results reveal that negative changes in government expenditure have more impact on economic growth than positive changes. The NARDL model also confirms that government expenditure was less effective after 2011 as can be seen in from the lower effects of government spending on economic growth when the conflict period is considered.

Scenario forecasts of real GDP growth

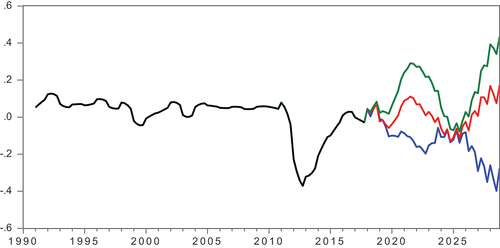

We report below three scenarios to study the viability of government expenditure in achieving economic recovery in Syria and assess whether the real GDP growth rates can converge to their pre-conflict levels by 2028. These scenarios are for illustration purposes only as other assumptions remain possible. To study the alternative scenarios, we employ the estimates of the Structural VAR model.

In the most likely scenario denoted ‘the moderate scenario’, we assume that the government expenditure will increase by 15% annually whereas the foreign exchange rate will increase by 10% yearly.Footnote1 We select these percentages as they represent the average government expenditure growth and increases in exchange rates recorded during the pre-conflict period (1990Q1-2010Q4). () shows that, under this scenario, the real GDP growth rate can reach its pre-conflict level. Thus, the fiscal stimulus can be effective when the monetary authorities adopt a managed flexible exchange rate.

Figure 5. Forecast for the Syrian real GDP growth for different scenarios.

The second scenario builds on the fact that, in recent years, the average growth in government expenditures in Syria was close to 25% per year. Hence, we hypothesize an optimistic scenario where this government expenditure growth rate can be sustained and dedicated to productive sectors rather than military. We also assume that Syria can maintain a depreciation rate of its domestic currency at around 1% annually in case the difference between the parallel market exchange rate and the official exchange rate is minimal. In this case, our forecasts in () show that government expenditure is effective in recovering pre-conflict growth rates under the optimistic scenario.

Finally, the pessimistic scenario conjectures that the current conditions in Syria will persist in the future. Therefore, we assume that the average yearly increase in government expenditure remains at 20% in the range of what has been recorded after the conflict (i.e. 2011–2017). A large share of these expenditures will be unproductive and dedicated to military and security sectors. While the government spending assumption is close to the optimistic scenario, we hypothesize that, under the pessimistic scenario, Syria will not be able to maintain its exchange rate level and will experience a yearly domestic currency depreciation of 34% (which is the average domestic currency depreciation recorded after the conflict i.e. 2011–2017). This large depreciation will hamper any efforts to boost the economy through government spending. () clearly shows that recovering pre-conflict growth rates is not possible under this scenario.

V. Conclusion and policy implications

This study highlights the importance of government expenditure as a viable policy tool to reconstruct the economy in the hope of re-establishing a sustainable peace between different political and ethnic groups in Syria. To this end, we employ two empirical estimation techniques, the SVAR and the NARDL, to investigate how government expenditure, parallel market exchange rates, money supply, and oil prices affect the real GDP growth during the period 1990–2017. Moreover, we include a dummy variable for the year 2011 and two interactive variables equal to government expenditure (positive and negative changes) multiplied by the 2011 dummy to capture any changes in the asymmetrical impact of government expenditure on the real GDP growth after the onset of the conflict.

The results of the SVAR approach show that a sudden increase in government expenditure changes will cause a significant increase in real GDP growth in the short and long run. The variance decomposition technique indicates that government expenditure has the largest percentage contribution to real GDP growth variations. Thus, government expenditure appears as an effective tool to boost economic growth in Syria.

The nonlinear ARDL empirical results show that government expenditure has an asymmetric impact on real GDP. A 1% increase in government expenditure (positive changes) increases the real GDP by 0.47% before the conflict and by 0.05% after conflict. This result highlights that the effectiveness of the government expenditure in boosting growth was greatly reduced after 2011. In contrast, a 1% decrease in government expenditure (negative changes) leads to a decrease in real GDP by 2.3% before the conflict and by 8.2% after the conflict. Interestingly, the results show that the response of real GDP to negative shocks in government expenditure is greater than its response to positive shocks, hence the asymmetrical effect.

Additionally, we provide scenario-based forecasts of the real GDP growth in Syria for the 2018 to 2028 period by changing the government expenditure growth rates under several exchange rate regimes. We find that recovering the 2010 GDP levels is possible under the optimistic and moderate scenarios. Accordingly, our paper provides solid grounds that the fiscal policy along with an appropriate exchange rate regime is capable of restoring economic growth during periods of conflict even when the level of destruction is important like in the Syrian case. Therefore, policymakers can design a possible return to pre-conflict real GDP growth rates by using adequate tax policies and public expenditure schemes. Fiscal policy would be more effective at the microeconomic and macroeconomic levels if the government expenditures are channelled to the most productive sectors. At the macro level, a sound fiscal policy that avoids large deficits creates a stable economic environment that fosters growth. At the micro level, the government can employ the tax policy to promote and facilitate investment, create opportunities for private businesses, and attract international investments. No doubt that designing fiscal reforms and finding public funding resources are more challenging during civil wars. However, the potential economic and social outcomes are so important that the Syrian government should put forward all the resources needed to warrant a safe exit from the conflict. The robustness of our findings can be tested in the context of other conflicts and regions. Additionally, it would of interest to explore which fiscal policy instrument is the most effective in driving growth and whether sector productivity rates affect the speed of the recovery process.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 We make assumptions on government expenditure and exchange rates because these variables are important in determining the real GDP growth according to the IS-LM model employed in this paper.

References

- Araji, S. (2017). Fiscal Policy Considerations for Post War Reconstruction in Iraq, Syria, Yemen and Libya. United Nations Economic and Social Commission for Western Asia.

- Arratibel, O., D. Furceri, R. Martin, and A. Zdzienicka. 2011. “The Effect of Nominal Exchange Rate Volatility on Real Macroeconomic Performance in the CEE Countries.” Economic Systems 35 (2): 261–277. doi:10.1016/j.ecosys.2010.05.003.

- Arslanian, F. 2009. Growth in Transition and Syria’s Economic Performance, edited by R. Hinnebusch, St Andrews, Fife, Scotland: University of St Andrews Centre for Syrian Studies.

- Bahmani-Oskooee, M., and M. Kandil. 2010. “Exchange Rate Fluctuations and Output in Oil-Producing Countries: The Case of Iran.” Emerging Markets Finance and Trade 46 (3): 23–45. doi:10.2753/REE1540-496X460302.

- Belloumi, M. 2010. “The Relationship Between Tourism Receipts, Real Effective Exchange Rate and Economic Growth in Tunisia.” International Journal of Tourism Research 12 (5): 550–560. doi:10.1002/jtr.774.

- Bilgel, F., and B. C. Karahasan. 2019. “Thirty Years of Conflict and Economic Growth in Turkey: A Synthetic Control Approach.” Defence and Peace Economics 30 (5): 609–631. doi:10.1080/10242694.2017.1389582.

- Blanchard, O. J., and D. Quah. 1993. “The Dynamic Effects of Aggregate Demand and Supply Disturbances: Reply.” The American Economic Review 83 (3): 653–658.

- Bohl, M. T., P. Michaelis, and P. L. Siklos. 2016. “Austerity and Recovery: Exchange Rate Regime Choice, Economic Growth, and Financial Crises.” Economic modelling 53: 195–207. doi:10.1016/j.econmod.2015.11.017.

- Brück, T., and J. D. G. Olaf. 2013. “The Economic Impact of Violent Conflict.” Defence and Peace Economics 24 (6): 6, 497–501. doi:10.1080/10242694.2012.723153.

- Chaitip, P., K. Chokethaworn, C. Chaiboonsri, and M. Khounkhalax. 2015. “Money Supply Influencing on Economic Growth-Wide Phenomena of AEC Open Region.” Procedia Economics and Finance 24: 108–115. doi:10.1016/S2212-5671(15)00626-7.

- Collier, P. 1999. “On the Economic Consequences of Civil War.” Oxford economic papers 51 (1): 168–183. doi:10.1093/oep/51.1.168.

- De Groot, O. J. 2010. “The Spillover Effects of Conflict on Economic Growth in Neighbouring Countries in Africa.” Defence and Peace Economics 21 (2): 149–164. doi:10.1080/10242690903570575.

- Diwan, I., and T. Akin. “Fifty Years of Fiscal Policy in the Arab Region.” In Economic Research Forum Working Paper, no. 914. 2015.

- Dubas, J. M., B.J. Lee, and N. C. Mark. 2005. Effective Exchange Rate Classifications and Growth (No. w11272). Cambridge: National Bureau of Economic Research.

- Ganegodage, K. R., and A. N. Rambaldi. 2014. “Economic Consequences of War: Evidence from Sri Lanka.” Journal of Asian Economics 30: 42–53. doi:10.1016/j.asieco.2013.12.001.

- Haddad, B. 2004. “The Formation and Development of Economic Networks in Syria: Implications for Economic and Fiscal Reforms, 1986–2000.” In Networks of Privilege in the Middle East: The Politics of Economic Reform Revisited, edited by Springer, 37–76. New York: Palgrave Macmillan.

- Ha, D. T. T., and N. T. Hoang. 2020. “Exchange Rate Regime and Economic Growth in Asia: Convergence or Divergence.” Journal of Risk and Financial Management 13 (1): 9. doi:10.3390/jrfm13010009.

- Hlongwane, T. M., I. P. Mongale, and T. A. L. A. Lavisa. 2018. “Analysis of the Impact of Fiscal Policy on Economic Growth in South Africa: VECM Approach.” Journal of Economics and Behavioral Studies 10 (2 (J)): 231–238. doi:10.22610/jebs.v10i2(J).2232.

- Husain, A. M., A. Mody, and K. S. Rogoff. 2005. “Exchange Rate Regime Durability and Performance in Developing versus Advanced Economies.” Journal of Monetary Economics 52 (1): 35–64. doi:10.1016/j.jmoneco.2004.07.001.

- Hussain, I., M. Rafiq, and Z. Khan. 2020. “An Analysis of the Asymmetric Effect of Fiscal Policy on Economic Growth in Pakistan: Insights from Non-Linear ARDL.” IBA Business Review 15 (1): 19–49.

- Kandil, M. 2001. “Asymmetry in the Effects of US Government Spending Shocks: Evidence and Implications.” The Quarterly Review of Economics and Finance 41 (2): 137–165. doi:10.1016/S1062-9769(00)00066-1.

- Kandil, M., and A. Mirzaie. 2002. “Exchange Rate Fluctuations and Disaggregated Economic Activity in the US: Theory and Evidence.” Journal of International Money and Finance 21 (1): 1–31. doi:10.1016/S0261-5606(01)00016-X.

- Kimbrough, E. O., K. Laughren, and R. Sheremeta. 2017. “War and Conflict in Economics: Theories, Applications, and Recent Trends.” Journal of Economic Behavior & Organization 178: 998–1013.

- Koubi, V. 2005. “War and Economic Performance.” Journal of Peace Research 42 (1): 67–82. doi:10.1177/0022343305049667.

- Krugman, P. (2015, April 29). The Austerity Delusion. The Guardian. Retrieved October 28, 2015, from http://www.theguardian.com/business/nginteractive/2015/apr/29/theausterity-delusion

- Mishkin, F. S. 2012. The Economics of Money, Banking and Financial Markets. 10th ed. Edinburg Gate: Pearson.

- Moroney, J. R. 2002. “Money Growth, Output Growth, and Inflation: Estimation of a Modern Quantity Theory.” Southern Economic Journal 69 (2): 398–413. doi:10.1002/j.2325-8012.2002.tb00499.x.

- Mrabet, Z., and M. Alsamara. 2018. “The Impact of Parallel Market Exchange Rate Volatility and Oil Exports on Real GDP in Syria: Evidence from the ARDL Approach.” The Journal of International Trade & Economic Development 27 (3): 333–349. doi:10.1080/09638199.2017.1389974.

- Muhammad, S. D., S. K. A. Wasti, A. Hussain, and I. Lal. 2009. “An Empirical Investigation Between Money Supply Government Expenditure, Output & Prices: The Pakistan Evidence.” European Journal of Economics, Finance and Administrative Sciences 17: 60.

- Ocran, M. K. 2011. “Fiscal Policy and Economic Growth in South Africa.” Journal of Economic Studies 38 (5): 604–618.

- Palley, T. I. (2012). Keynesian, Classical and New Keynesian Approaches to Fiscal Policy: Comparison and Critique (IMK Working Paper No. 96). Düsseldorf: Macroeconomic Policy Institute.

- Petreski, M. (2009). Exchange-Rate Regime and Economic Growth: A Review of the Theoretical and Empirical Literature. Economics Discussion Paper, (2009-31).

- Rizkalla, N., and S. P. Segal. 2018. “Well‐being and Posttraumatic Growth Among Syrian Refugees in Jordan.” Journal of Traumatic Stress 31 (2): 213–222. doi:10.1002/jts.22281.

- Rodrik, D. 2008. “The Real Exchange Rate and Economic Growth.” Brookings Papers on Economic Activity 2008 (2): 365–412. doi:10.1353/eca.0.0020.

- Romer, C. D. 2012. Fiscal Policy in the Crisis: Lessons and Policy Implications. Berkley: University of California.

- Sidrauski, M. 1967. “Rational Choice and Patterns of Growth in a Monetary Economy.” The American Economic Review 57 (2): 534–544.

- Sims, C. A. 1980. “Macroeconomics and Reality.” Econometrica: Journal of the Econometric Society 48 (1): 1–48. doi:10.2307/1912017.

- Tabi, H. N., and H. A. Ondoa. 2011. “Inflation, Money and Economic Growth in Cameroon.” International Journal of Financial Research 2 (1): 45–56. doi:10.5430/ijfr.v2n1p45.

- Tendengu, S., F. M. Kapingura, and A. Tsegaye. 2022. “Fiscal Policy and Economic Growth in South Africa.” Economies 10 (9): 204. doi:10.3390/economies10090204.

- Tilahun Mengistu, S. 2022. “Does Fiscal Policy Stimulate Economic Growth in Ethiopia? ARDL Approach.” Cogent Economics & Finance 10 (1): 2104779. doi:10.1080/23322039.2022.2104779.

- Tony, A., A. R. Chowdhury, and S. Mansoob Murshed. By How Much Does Conflict Reduce Financial Development?. No. 2002/48. WIDER Discussion Paper, 2002.

- Twinoburyo, E. N., and N. M. Odhiambo. 2018. “Monetary Policy and Economic Growth: A Review of International Literature.” Journal of Central Banking Theory and Practice 7 (2): 123–137. doi:10.2478/jcbtp-2018-0015.

- Woodford, M. (2007). Globalization and Monetary Control, NBER Working Paper, No. 13329.

- Yusuf, A., and S. Mohd. 2021. “Asymmetric Impact of Fiscal Policy Variables on Economic Growth in Nigeria.” Journal of Sustainable Finance & Investment 1–22. doi:10.1080/20430795.2021.1927388.

- Zagler, M., and G. Dürnecker. 2003. “Fiscal Policy and Economic Growth.” Journal of Economic Surveys 17 (3): 397–418. doi:10.1111/1467-6419.00199.