Abstract

As the Covid-19 crisis deepened in 2020, President Joko Widodo announced that Indonesia should prepare for the ‘new normal’. But when social distancing restrictions were relaxed in June to encourage economic recovery, the virus was not yet contained in Indonesia. Since then, the rate of infection has been rising faster than in many neighbouring countries. The pandemic has hit the economy hard, with a 5.3% reduction in GDP in the second quarter, the worst economic slump since 1998. In this Survey, we look at how Indonesia is preparing for the new normal. We argue that the government is focused on short-term recovery and does not have a clear strategy to address the medium-and longer-term implications of Covid-19. The response to the virus relies on public compliance to public health measures. There is a clear lack of emphasis on reducing the rate of infection through effective testing and tracing and enforcing social distancing and mobility restrictions. The government has developed an economic recovery plan that concentrates on cushioning the short-term impact of the crisis and supporting the poor and near-poor, rather than reducing long-term poverty and preventing structural changes in unemployment. Finally, we find that the pandemic is undermining the long-term financial sustainability of Indonesia’s social health insurance system. The education sector is reasonably prepared for extended school closures and distance learning. Yet there is no strategy to address the accumulated learning losses resulting from this crisis.

Sejalan dengan semakin dalamnya krisis Covid-19, Presiden Joko Widodo mengumumkan agar Indonesia bersiap menyambut kondisi normal baru. Namun ketika pembatasan sosial dilonggarkan di bulan Juni demi mendukung pemulihan ekonomi, penyebaran virus sesungguhnya belum bisa dikendalikan di Indonesia. Sejak saat itu, tingkat infeksi terus naik, lebih cepat dari banyak negara tetangga lainnya. Pandemi Covid-19 telah memukul ekonomi dengan keras, dengan kontraksi 5,3% pada PDB Indonesia di Triwulan II, kondisi ekonomi terparah sejak 1998. Dalam survei ini, kami melihat bagaimana Indonesia mempersiapkan diri menuju kondisi normal baru. Kami berpendapat bahwa respon pemerintah berfokus pada pemulihan jangka pendek, namun tidak memiliki strategi yang jelas untuk menyasar dampak jangka menengah dan panjang dari Covid-19. Respon terhadap virus bergantung pada kepatuhan publik terhadap aturan-aturan kesehatan. Terdapat kelemahan penekanan dalam mengurangi tingkat infeksi melalui uji efektif dan pengecekan (testing and tracing) atau dalam memberlakukan pembatasan sosial dan restriksi mobilitas. Pemerintah telah membangun rencana pemulihan ekonomi yang lebih berkonsentrasi kepada upaya mengatasi dampak jangka pendek dari krisis serta mendukung orang miskin dan rentan miskin, dibandingkan upaya penanggulangan kemiskinan jangka panjang dan potensi pergeseran dalam komposisi pengangguran. Akhirnya, kami menemukan bahwa Covid-19 juga melemahkan keberlanjutan finansial jangka panjang dari sistem jaminan sosial kesehatan. Sektor pendidikan cenderung lebih siap untuk perpanjangan penutupan sekolah dan penerapan sistem Pendidikan Jarak Jauh (PJJ). Namun demikian, tidak ada strategi untuk mengganti akumulasi pendidikan yang hilang sepanjang krisis ini berlangsung.

INTRODUCTION

Facing the worst economic slump in 20 years and an ever-accelerating rate of Covid-19 infection, Indonesia is struggling to deal with the pandemic. In June 2020, the government relaxed some of the country’s social distancing restrictions (PSBBs) and opened up some sectors of the economy. These measures were presented by President Joko Widodo as ‘preparing for the new normal’. Yet, at the time, the spread of Covid-19 was not under control and critics argued that the government was recklessly prioritising economic recovery over containing the pandemic.

The government’s economic recovery package aims to support domestic consumption and address rapidly worsening poverty and unemployment. However, disbursement of support funding has been slow and the social protection programs that are the foundation of the recovery strategy were not designed to reach those most affected by the pandemic.

In this Survey, we consider how Indonesia is preparing for the new normal. In the next section, we look back at how Indonesia has managed Covid-19, and the policy options for controlling the crisis in the months ahead. In September–October 2020, the government had no clear strategy for containing the virus in the medium-to-longer term, with public health policy focused on managing current infections rather than decelerating the rate of infection. In the third section, we assess the economic fallout of the crisis and the government’s strategy for dealing with the immediate socio-economic impacts. Again, the government’s focus is largely on the short-term impact of the crisis, relying mainly on existing social protection programs to shield the welfare of the poor and near-poor. However, the crisis response package offers little to address potential long-term poverty through the impact on labour markets. To make matters worse, the government’s long-awaited omnibus reform bill aimed at stimulating investment, output and jobs was passed by the House of Representatives on 5 October but was met with a fiery response from workers and students who led angry demonstrations across the country, calling for the bill to be withdrawn. Finally, we look at the long-term implications of the Covid-19 crisis for two crucial public sectors, health and education, and some challenges these will face under a continued Covid-19 presence.

COVID-19 IN INDONESIA: STILL NO SIGN OF DECELERATION

Indonesia in Global and Regional Comparison

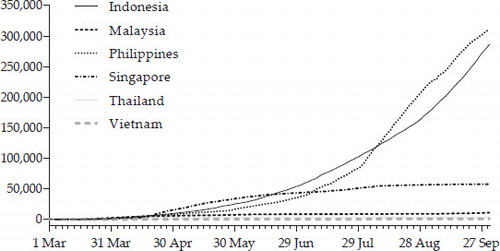

While many countries in Asia and Western Europe are tightening measures to avoid a second wave of Covid-19, Indonesia still finds itself in the midst of the first wave, struggling to contain case numbers that have been rising faster than in many neighbouring countries. Singapore, for example, which identified spread of the virus early, also responded early with monitoring of incoming travellers, travel restrictions and elaborate contact tracing starting as early as January 2020. While these measures were effective initially, by April infections had started to increase, prompting Singapore to enter into a lockdown, closing schools, universities and workplaces to reduce daily case numbers. Thailand, Vietnam and Malaysia also introduced lockdown measures early and have been able to ‘flatten the curve’ and minimise new infections, despite some temporary setbacks.

Indonesia and the Philippines, in contrast, are still struggling to contain the virus. Both are experiencing an acceleration in case numbers (). While Indonesia has seen a gradual acceleration, the Philippines experienced a surge in July 2020, and is now matching Indonesia’s pace in detecting new cases. Local observers have attributed the recent rise in the Philippines to the government’s decision to end the initial stay-home orders too early and people subsequently finding it difficult to practise social distancing—a concern also voiced in Indonesia. Indonesia also stands out in Southeast Asia in terms of the number of Covid-19-related deaths.

FIGURE 1 Number of Covid-19 Cases in Indonesia and Neighbouring Countries, March–October 2020

The mortality rates are contested and many assume that the number of deaths is greatly underestimated in Indonesia (for example, Susan Olivia, John Gibson and Rus’an Nasrudin in the August Survey of Recent Developments).Footnote1 Nevertheless, the case fatality rate in Indonesia is still fairly high, at 3.7%, with 40.5 deaths reported per one million people. Late testing and treatment are some of the reasons put forward for the high case fatality rate in Indonesia compared with its neighbours (Ariawan and Jusril Citation2020).

The Spread of Covid-19 within Indonesia

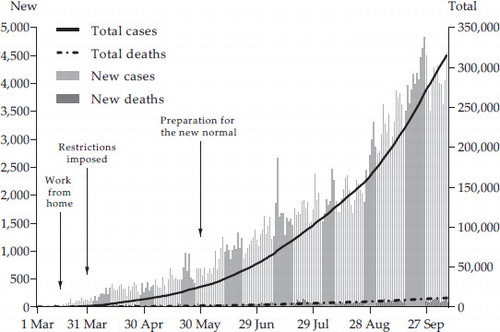

According to official figures, daily cases in Indonesia have risen gradually since March (). The government introduced a work-from-home order for public servants in mid-March. In early April, when Indonesia’s neighbouring countries entered into lockdowns, the government tightened the work-from-home orders by imposing large-scale social and mobility restrictions (PSBBs) and announced an international travel ban a few weeks later, yet the country did not enter into a full lockdown.Footnote2 Epidemiological analyses suggest that the social distancing measures were effective in reducing transmission rates by almost 50% from April to June (Ariawan and Jusril Citation2020). With the economic situation worsening as a result of the mobility restrictions, the government relaxed some of the PSBBs in June. However, despite the initial positive effects of the PSBBs, as of September 2020 Indonesia had not yet managed to ‘flatten the curve’. That is, the earlier PSBBs reduced the rate of acceleration but were not able to turn this into a deceleration. When the PSBBs were imposed, daily infections had just passed 100 cases, and when the restrictions were relaxed, these had increased to about 600. The reproductive rate (the average number of new infections caused by one existing infection) was still estimated to be as high as 1.2 when the PSBBs were relaxed—whereas, according to the World Health Organization (WHO), the reproductive rate needed to remain below one for a period of two weeks before infection rates could be considered to be under control. As a result, infection numbers have accelerated sharply. By the end of August and following several public holidays that involved spikes in domestic travel, daily reported new cases passed the 3,000 mark for the first time, with daily infections reaching 4,000 by late September and reproductive rates still above one in all provinces (Ariawan et al. Citation2020).

FIGURE 2 Number of Confirmed Covid-19 Cases and Deaths in Indonesia, March–October 2020

Looking at the age profile of Covid-19 mortality, we see that the reported Covid-19 fatalities were largely concentrated among adults aged over 40 years, although some deaths were found in younger cohorts. About 55% of deaths occurred in people aged 55 and over, about 25% in those aged 45–55, and about 20% in those under 45 (Ministry of Health Citation2020a). Infections are spread more evenly across age groups than fatalities, with the bulk occurring among 20–59-year olds, the most economically productive age group.

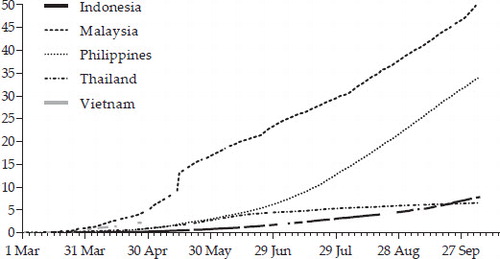

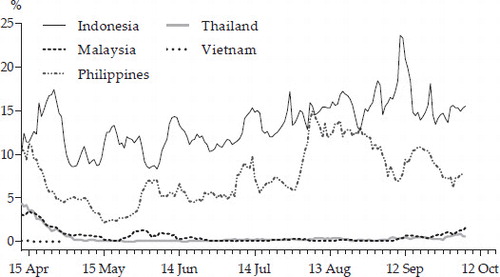

Health experts have urged increased testing as one of the most important instruments for containing the spread of the virus. Testing for Covid-19 serves two purposes. The first is to confirm a diagnosis so that medical treatment can be appropriately rendered. The second is to facilitate surveillance for tracking and disease suppression, including finding people who are asymptomatic or have only mild symptoms but may still be able to spread the infection. This information is crucial to help individuals and public health officials take appropriate action to slow the spread of the virus. Yet testing in Indonesia has remained worryingly low. shows this by comparing testing rates in Indonesia with those in neighbouring countries. Despite its high caseload, Indonesia still has the lowest testing rate in Southeast Asia, well below the WHO-recommended target of one test per 1,000 people per week (Satgas Covid-19 2020). The testing regime in Indonesia is still too focused on patients with symptoms. This is further illustrated by the very high rate of positive tests in Indonesia (). WHO recommends that countries adopt a broad testing strategy, to the extent of having a positive rate of 5% or lower, in order to test broadly enough to capture asymptomatic cases. However, Indonesia’s positive rate is far above this target, currently fluctuating at around 18% and with most of the testing concentrated in Jakarta.

FIGURE 3 Total Number of Covid-19 Tests per 1,000 People in Indonesia and Neighbouring Countries, March–October 2020

FIGURE 4 Daily Positive Test Rates in Indonesia and Neighbouring Countries, April–October 2020

Indonesia’s struggle to increase testing seems to be due to a limited testing capacity as well as to poor Ministry of Health leadership that is frustrating a broad testing policy. The testing capacity is limited by a shortage of testing facilities and weak public health infrastructure. This is a problem throughout Indonesia but capacity also varies by region (Hendarwan et al. Citation2020; Sucahya Citation2020). The ministry has also not been able to effectively coordinate and regulate procurement of testing materials. It has been slow to scale up polymerase chain reaction (PCR) tests, with public facilities also having to rely on a cheaper antibody test that is less effective in detecting active infections. The PCR tests are freely available at public facilities for cases with observable symptoms, not for asymptomatic cases, in effect imposing a narrow testing strategy. In addition, PCR testing can be subject to delays, as the tests are processed only in large batches for reasons of cost effectiveness. Finally, the health ministry has not formulated monitoring indicators for contact tracing or communicated policy targets to districts, reducing the incentive for local governments to prioritise broad testing.

Contact tracing remains extremely limited, mainly owing to inadequate disease surveillance and health information systems (Ariawan and Jusril Citation2020). There are no clear and consistent procedures for gathering contact information (for example, keeping records of visitors at restaurants or shops). In practice, public health measures focus on sanitation, detecting visible symptoms, and social distancing, not on gathering contact information. Contact tracing therefore relies mostly on retrospective information provided by infected individuals. Contact tracing tends to be initiated only when a positive test is reported, while test results take about 5–7 days on average to be processed and reported. Such delays increase the potential for positive cases to spread infection, especially if voluntary quarantining after testing is not practised.

Regional Challenges and Responses

Jakarta is still the epicentre of the virus in Indonesia and has been leading in the acceleration of daily infections. This is in part due to the higher testing rates in Jakarta, which make it more likely that infections will be identified. Data on daily cases and deaths are therefore likely to be more accurate in Jakarta than in rural areas and outer islands, which contributes to a Jakarta-centric view of the pandemic. Nevertheless, the data that are available suggest considerable regional variation in the spread of the disease. Along with Jakarta, East Java (especially Surabaya) has been hit hard in terms of recorded cases, seeing strong increases in daily cases until July. However, the region has so far managed to avoid the surge in cases experienced in Jakarta. Large municipalities are also a more conducive environment for the virus to thrive. International evidence suggests that this is due not so much to population density as to mobility, connectivity and economic activity in large cities (Hsu Citation2020).

Some regions have introduced their own PSBBs in response to rising infection rates. The health ministry has sole authority to impose PSBBs, but local governments, as well as the Covid-19 Task Force, can submit proposals for local PSBBs to the ministry. For example, the Jakarta governor imposed transitional PSBBs when the national restrictions were eased. These transitional restrictions mainly involved reducing work activities in certain sectors, limiting the number of employees allowed in a workplace, instituting a work-from-home policy for civil servants, and restricting public transport. Recently, the restrictions have been tightened further in response to the acceleration of infections in Jakarta in August and September. However, these restrictions are at odds with national policy and have attracted criticism from government officials who fear the economic repercussions of the local restrictions. Such tensions between the policy priorities of national and subnational jurisdictions are not unique to Indonesia; they fit a pattern observed especially in some other geographically dispersed and more populous countries (for example, Brazil and the United States). The continuing acceleration of infections in Jakarta, despite its transitional PSBBs, also points to a key limitation of local restrictions. The high degree of connectivity and economic integration within the Greater Jakarta region (Jabodetabek) makes it near impossible to isolate Jakarta from its surrounding provinces. A lack of coordination between the national and provincial governments therefore undermines the effectiveness of any local efforts to control the virus.

Policy Options with the Rapid Spread of Covid-19

By September 2020, it had become clear that the Indonesian government had painted itself into a corner by rejecting most of the more difficult and less popular but potentially workable options for reducing the rate of spread of the virus. Covid-19 infections began to accelerate out of control after the government called for ‘preparation’ for the new normal, and then relaxed the PSBBs in June 2020. Since then, the government has ruled out a lockdown in fear of the economic repercussions, even though in other countries this measure has proved the most effective way to curtail infections. Testing and contact tracing have also been held back by the narrow testing strategy of the health ministry, the country’s limited testing capacity and a lack of clear government directives to the regions. Indonesia is unlikely to develop a stronger capacity for testing and contact tracing in the short term. That leaves social distancing and public health measures as the main tools for containing the virus. Yet relying on the voluntary compliance of the public in the absence of strict enforcement has its limitations, as other countries have experienced when relaxing restrictions. Two high-frequency surveys of Covid-19 impacts suggest weak compliance with public health measures: while personal sanitation measures (such as regular hand washing) are common practice, social distancing in public spaces and adequate health protocol in workplaces are less commonly practised (Hanna and Olken Citation2020; World Bank Citation2020). Observers further criticise the communications strategy of the government in raising awareness of the risks associated with contracting Covid-19, given that the current level of risk awareness in the population is low.Footnote3 The government seems to be placing all its bets on a vaccine, with the president even suggesting that a vaccine will be available as soon as January 2021. However, even in the most optimistic scenarios for the development of a vaccine, one is unlikely to be rolled out before the second quarter of 2021.Footnote4

ECONOMIC DEVELOPMENTS

Economic Growth

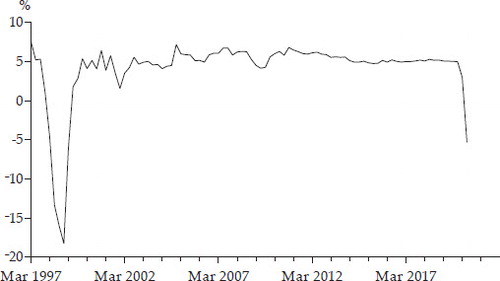

The Covid-19 crisis and the subsequent social distancing and mobility restrictions have had a severe impact on economic growth. In the second quarter of this year, GDP fell by 5.3% compared with the same quarter last year. Indonesia has not seen such an economic contraction since 1998, during the Asian financial crisis ().

FIGURE 5 Quarterly GDP Growth, 1997–2020 (year on year)

After a decade of rather stable economic growth of about 5.4% per year, growth fell to 3.0% year on year in the first quarter of 2020, as Indonesia felt the first effects of the pandemic (see Olivia, Gibson and Nasrudin’s August Survey in BIES).

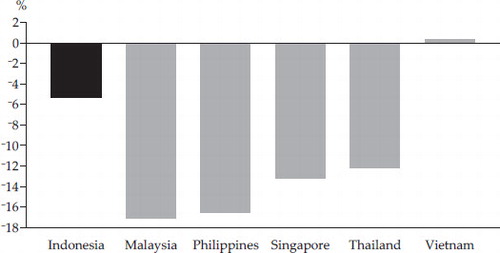

Nevertheless, Indonesia’s reduction in GDP has been modest compared with that of neighbouring countries. For example, Malaysia, the Philippines, Singapore and Thailand all experienced double-digit contractions in the second quarter of 2020 (), with some countries seeing a reduction in GDP as early as the first quarter. Presumably, this was due to stricter measures to contain Covid-19 and also differences in economic sensitivity to reduced international trade. The exception in Southeast Asia was Vietnam, which saw slower economic growth but managed to avoid a contraction.

FIGURE 6 GDP Growth in Indonesia and Neighbouring Countries, Q2 2020 (year on year)

As in other countries, the economic impacts in Indonesia have varied greatly across sectors. The sectors most affected by the pandemic are those that are more vulnerable to mobility restrictions, falling international trade and disruptions to supply chains. In addition, many of these sectors tend to be labour-intensive, employing both informal sector workers and formal sector (wage) workers. shows quarterly GDP growth (year on year) for 2019 and 2020, disaggregated by sector and expenditure. Particularly hard hit were transport and storage (falling by over 30% in June 2020, year on year), accommodation and restaurants (falling 22%) and, to a lesser extent, business services, wholesale and retail trade, and manufacturing. The contraction in the transport and storage sector is not surprising, as transport was immediately disrupted by reduced commuting resulting from work-from-home orders, and overall reduced mobility resulting from the largescale social distancing and travel restrictions (BPS 2020b). All subsectors contracted, but air and rail transport saw the largest declines (80% and 64%, respectively), followed by warehousing and transport support services. Although the transport sector constitutes less than 4.0% of overall GDP, it accounts for a quarter of the 5.3% contraction in GDP, the largest contribution of all sectors.

Table 1. Components of GDP Growth (2010 prices; % year on year)

Manufacturing, the economy’s largest sector, with a 20% share of GDP, provided an almost equal contribution to overall economic decline. Within this sector, the production of transport equipment saw the largest decline, over 30%, as one would expect given the contraction in the transport sector. The textiles and clothing subsector saw a decline of almost 15% due to supply-side and value chain disruptions, as well as falling domestic retail sales and exports (Pane and Pasaribu Citation2020). On the other hand, the increased demand for modern and traditional medicines boosted growth in the chemical and pharmaceutical subsector to 9% in the second quarter. Wholesale and retail trade, another large sector (which contributes 13% of GDP and is a much larger provider of jobs) contracted by 8%. The shutdown of international tourism and near collapse of domestic tourism led to a massive decline of the hotel and accommodation subsector of almost 50%.

In contrast, some sectors have thrived during the Covid-19 crisis, especially information and communications, and health care and social work (). Working-from-home and social distancing restrictions increased Indonesia’s reliance on information and communications technology (ICT), such as mobile technology, contributing to double-digit growth in the ICT sector year on year. This had a positive effect on employment in the sector. However, as the sector had less than a 5% share of GDP, the increase in employment was dwarfed by the contractions in other sectors and likely benefited mainly the formal sector and more-educated workers.

Agriculture, forestry and fisheries is a relatively large sector (with a 16% GDP share) and saw low but positive growth (2.2% year on year) in the second quarter. A delay in the rice harvest was behind most of the restrained growth stemming from crop production. Nevertheless, all other agricultural subsectors also saw year-on-year growth, except for livestock and fisheries, which experienced modest declines. One explanation for the outperformance of agriculture could be that many agricultural supply chains did not face mobility restrictions.

From an expenditure point of view, the economic contraction was caused mostly by reduced household consumption and a fall in investment, along with reduced government consumption. Household consumption declined by 5.5%, which translates to a 3.0% reduction in overall GDP, more than half of the total contraction. This decline was mainly in the consumption of clothing, transport, communications, leisure and travel. The reduction in household consumption was also reflected in a declining inflation rate and falling consumer prices in the second quarter.Footnote5 More worrying for the longer term, investment fell by nearly 10%, with a decline in expenditure on all types of capital goods.

A fall was also recorded in government consumption, although it did increase by over 20% compared with the first quarter. The reductions were most pronounced for personnel (11%) and goods (21%) (Ministry of Finance Citation2020). This decline in government consumption is unexpected, given that the government developed a national economic recovery package to curb the rise in poverty, stimulate consumption and support business. There could be several reasons why government spending has been sluggish. First, establishing the recovery package requires some reallocation of funds within the relevant ministries, which could lead to both disruptions and reductions in spending. Second, the disbursement of the recovery package has been slow (see below). Third, reduced local government spending in response to the decline in national revenue could explain part of the reduction in overall government consumption (Lewis and Nikijuluw, forthcoming). In addition, there are anecdotal reports that the work-from-home policy and mobility restrictions have disrupted local government bureaucracies.

The Covid-19 crisis has brought about a big slump in global trade, which has affected Indonesia. Exports and imports were down by 12% and 17% year on year, respectively, in the second quarter of 2020. Services exports (including tourism) were more severely affected than commodity exports: between the first and second quarters of 2020, goods exports fell by 17%, whereas services exports fell by more than half. Services imports also fell steeply, by 40%.

The balance of payments returned a surplus of about $9 billion in the second quarters of 2020, following a first-quarter deficit of about $8 billion (). This change was underpinned by a reduction in the current account deficit. As imports declined more than exports, the trade balance moved into surplus in the second quarter. The exchange rate has been fairly steady since the initial Covid-19 shock. This has been good for price stability and real incomes during the crisis. Portfolio investment inflows rebounded strongly, after a decline in the first quarter, bringing the financial account back into positive territory.

Table 2. Balance of Payments ($ billion per quarter)

Response Package

In response to the pandemic, the government developed the National Economic Recovery (PEN) program. The program was first announced in February, with a value of Rp 8.5 trillion. As infection rates accelerated and the economic crisis deepened, the value of the package increased to Rp 405 trillion in March and Rp 695 trillion in June (). This amounts to 4.2% of GDP.

Table 3. National Economic Recovery (PEN) Program for 2020 and 2021

As a share of GDP, Indonesia’s response package is much smaller than the packages of most high-income countries. For example, Japan’s response is 21% of GDP, the United States’ is 12% and Australia’s is 10%. Within the region, Indonesia’s response is modest compared with that of Thailand (9.6% of GDP), but comparable to the responses of Vietnam (3.6%) and the Philippines (3.9%).Footnote6 We need to be careful in comparing the sizes of fiscal response packages across countries, since the extent of Covid-19 infections, social mobility restrictions and economic impacts varies greatly. Nevertheless, the difference in size between high-income and low-income countries is unambiguous and can partly be explained by differences in borrowing capacity and domestic resource mobilisation. Indonesia’s tax base is relatively small; the country has annual tax revenues of about 12% of GDP, expected to decline to below 10% this year (Kacaribu Citation2020).

The largest component of Indonesia’s recovery package is social protection, amounting to almost Rp 204 trillion for boosting consumption and reducing the poverty impacts of economic contraction. The PEN program aims to support the private sector through Rp 124 trillion in business incentives (mainly tax deductions) and Rp 54 trillion for corporate financing. The support for micro, small and medium-sized enterprises (MSMEs) amounts to Rp 121 trillion, mainly for working capital guarantees and interest rate subsidies. Sectoral and regional governments are supported with a budget of Rp 106 trillion, of which Rp 18 trillion is allocated for job creation and public works schemes.

The main policy instruments for channelling the social protection package are existing programs such as the Hopeful Families Program (PKH); the food assistance programs, Kartu Sembako and Bansos Sembako; and the village cash support program, BLT. In addition, the government has added the new pre-employment card, Kartu Prakerja, and is offering electricity bill discounts.Footnote7 While the scope of this set of programs is certainly comprehensive, the package is designed for poverty alleviation in pre-Covid-19 times and not for a pandemic. First, most programs are geared towards supporting rural areas and the poor, not urban and middle-income households affected by the Covid-19 crisis. Second, targeting relies on a social welfare database (DTKS) developed over the past decade. This database has been an effective instrument for improving the targeting of social protection programs, but it is not equipped to deal with large shocks and related poverty dynamics; that is, it is not designed to identify short-term welfare changes among individual households (such as unemployment or sudden severe illness) and movements in and out of poverty. In addition, the database has not been updated since 2015 (see Olivia, Gibson and Nasrudin’s August Survey).

A recent World Bank (Citation2020) survey found that many lower–middle-income households are vulnerable to income shocks due to Covid-19, as 24% of bread-winners in households have stopped working. Job losses have been especially pronounced in Java, in urban areas, among people with a senior secondary education or less, and in the industry and services sectors. A large share (about 64%) of people with jobs also experienced reduced income. As many as 55% of respondents declared that government assistance was an important consumption-smoothing strategy, since they had experienced reduced non-food and food expenditure. The database for targeting social protection programs is not able to capture rapid changes in welfare status, leading to increased exclusion errors in targeting. The Covid-19 crisis has brought to light an urgent need to increase the flexibility of the social protection targeting system; for example, by introducing innovative information systems. These could include a social registry that covers the poorest 60% of the population, social assistance programs that can be applied for when the demand arises (as in the case of the Kartu Prakerja program), or community-based targeting (as in the case of the BLT program) (Sumarto Citation2020).

We further observe that the PEN program lacks a clear focus on long-term unemployment and business sustainability, as it is mostly focused on mitigating the short-term impact of Covid-19 on the economy. Recently, the government has been trying to design new programs to mitigate long-term unemployment. One of these is a productive social assistance package that is expected to sustain business operations and employment for 12 million micro enterprises. In addition, social security contributions for work-related accidents and death have been reduced to near-zero. However, the PEN program does not include wage subsidies to help firms retain workers during the crisis, unlike programs in countries such as Malaysia, Singapore and Australia, as well as several European countries. Instead, Indonesia offers wage subsidies directly to workers. These payments boost household real incomes and avoid implementation and accountability issues, but they leave firms and jobs vulnerable.

Another problem is that various PEN programs providing business incentives to MSMEs are not fully aligned with the needs of these enterprises. A survey conducted by Statistics Indonesia (BPS) in July 2020 covering 25,300 micro and small enterprises (MSEs) and 6,800 medium–large enterprises (MLEs) shows that the assistance needs of the two types of entity are different (BPS 2020c): 70% of MSEs indicated that working capital assistance should be a priority for government during the pandemic, while 40% of MLEs said that electricity subsidies, relaxation of loan payments, and postponement of tax payments should be a priority. Both MSEs and MLEs requested a temporary electricity subsidy, but this package is not in place yet. Using PEN funding to provide electricity subsidies would ease the financial burden on businesses during the crisis and is administratively convenient to implement owing to the existing database held by Indonesia’s state electricity company (PLN). A serious challenge facing the implementation of the PEN package is the low rate of disbursements. As of 7 October, just 48% of the allocated budget had been disbursed (Ministry of Finance Citation2020). Disbursements accelerated in September, especially for the social protection programs and the support packages for MSMEs, which have realisation rates of 78% and 73%, respectively (). But for the other components, the rates are much lower: 30% for the health package, 26% for sectoral and regional government support and 24% for the business incentives, while no funding has yet been released for corporate financing.

Low disbursements will certainly delay the economic recovery and there is an urgent need to accelerate them. The delays are partly due to the government bureaucracy’s being overwhelmed by the spending increase, especially in the first months of PEN. The bureaucracy tended to be overly careful in allocating funds, compelled to focus on procedure and accountability, and apprehensive of a watchful Corruption Eradication Commission (KPK) and the Supreme Audit Agency (BPK). However, the large variations between sectors also suggest structural barriers to a swift Covid-19 response. For example, the social protection programs that were most effectively scaled up were those with already-established institutions and accountability, and clearly identified beneficiaries.

As the impact of Covid-19 on the economy is likely to persist for some time, the government has also budgeted a PEN package for 2021 of about Rp 356 trillion. Unlike the 2020 PEN program, the 2021 package has its largest component allocated to sectoral programs and regional governments. A total of Rp 137 trillion has been allocated to economic recovery through tourism, ICT development and industrial zones. The social protection program is supported with Rp 110 trillion for five main areas: conditional cash transfers, basic food support, the pre-employment program, village fund cash transfers and unconditional cash transfers. Private sector support includes Rp 20 trillion for business incentives, Rp 15 trillion for corporate financing and Rp 49 trillion for small and medium-sized enterprises.

National Budget

The Covid-19 crisis has had a profound impact on the budget, reducing revenues, increasing expenditures and increasing the budget deficit. Since the onset of the crisis, the government has revised the budget for 2020 twice, first in April and again in June (see Presidential Decrees 54/2020 and 72/2020). The latest budget revision reflects a bleak economic outlook, with domestic revenues expected to fall from about Rp 1,955 trillion in 2019 to Rp 1,699 trillion in 2020, and expenditure expected to increase by 11% from about Rp 2,309 trillion in 2019 to Rp 2,739 trillion in 2020 (). Tax revenues are expected to fall to 9% of GDP, mainly owing to a decrease in both personal and corporate income tax. Non-tax revenues will decrease by almost one-third compared with the 2019 budget, owing to lower oil and gas prices as well as a fall in other commodity prices. As of August 2020, about 57% of the total budgeted tax revenue had been collected (Ministry of Finance Citation2020). The proposed budget for 2021 places much hope in positive growth projections and a rebound in domestic revenues. In the expectation of economic recovery, the government intends to spend less on social assistance and subsidies, although its planned social assistance spending for 2021 is still higher than the 2019 level. With total expenditure remaining at a similar level to that of 2020, the government aims to bring the deficit down to 5.5%. However, the macroeconomic assumptions and development targets in the 2021 budget appear very optimistic, with the government looking for economic growth in the range of 4.5% to 5.5% and a poverty rate below 10%. The economic growth prediction is in line with those made by the ADB and the OECD (5.3%) but higher than the World Bank’s prediction (2.0%–4.4%). The government’s poverty predictions, however, seem unrealistic given that Indonesia recorded a poverty rate of 10% in March, before the country bore the full brunt of the crisis (see the next subsection).

Table 4. Budgets for 2019, 2020 and 2021 (Rp trillion)

Largely because of increased spending, reduced revenues and automatic stabilisers, and partly because of the planned recovery packages, the government’s expected deficit has increased to 6.3% of GDP. As this exceeds the 3% limit imposed by Law 17/2003 on State Finance, the president has passed a decree to allow deficits to exceed this threshold until the end of the 2022 fiscal year. The burden of the budget deficit will be shared by the finance ministry through borrowing, and Bank Indonesia (BI) through quantitative easing. The possibility of revisions to the BI law was flagged by the House of Representatives in August. The proposed revision of the law would almost certainly curtail the independence of the central bank and could have far-reaching implications for BI’s credibility in financial markets (see the box).

Poverty

There are early signs of a significant rise in poverty. BPS (2020d) observed an increase in poverty in March 2020 compared with September 2019, based on the National Socio-economic Survey (Susenas). This showed an increase in the poverty rate from 9.2% to 9.8%. This 0.6-percentage-point increase corresponds to a 6.1% increase in poverty relative to the September 2019 level, or about 1.6 million people falling below the poverty line. At the national level, such an increase could be considered modest. However, when we examine rates across provinces, we see that the hike in the poverty rate is mainly concentrated in Java, especially in DKI Jakarta, West Java and Banten, where we see increases of about one percentage point. The relative increase is greatest in Jakarta, at 32% compared with the level in September 2019 (an increase from 3.4% to 4.5%), and 15% in West Java (from 6.8% to 7.9%). In urban areas, the poverty rate increased by 13% (from 6.6% to 7.4%), while rural areas saw a relative increase of only 2% (from 12.6% to 12.8%).

The poverty rates are certain to have changed by September 2020, following the economic contraction in the second quarter. Nevertheless, the March poverty increase already matches the best-case scenario predicted by Suryahadi, Al Izzati and Suryadarma (Citation2020), based on annual GDP growth of 4.2%. Based on 1% growth or a 3.5% contraction in GDP, their predictions are poverty rates of 12.4% and 16.6%, respectively, or an additional 8.5 million and 19.7 million people in poverty. These short-term poverty effects mainly reflect the immediate mobility effects of the work-from-home policy announced mid-March, in addition to the impact of the slowdown in global investment and trade on jobs and incomes in Indonesia. These mobility restrictions were still largely voluntary, as the mandatory large-scale social distancing restrictions were not in effect until early April. Several studies have shown that work-related mobility declined sharply in the second half of March (BPS 2020d, 2020e). The first income effects from this reduction would most likely have been felt by the near-poor and informal sector workers in urban areas of Java, such as low-wage workers involved in transport, restaurants and retail. Existing social protection programs equipped to reach the poor and near-poor can play a role in alleviating the immediate income effects of the mobility restrictions on this vulnerable section of the population.

Central banks around the world have moved into unconventional territory in response to the Covid-19 pandemic. Bank Indonesia (BI) is no exception. In addition to low-ering interest rates and providing extra liquidity to the financial system, BI is now financing a large share of the government budget deficit, with more finance to come. Such unorthodox policy is well justified as a one-off response to the severe economic crisis.Footnote1 However, some parliamentarians want to normalise these arrangements in problematic ways. A draft revision to the 1999 BI law produced by the parliament legislative committee would in particular allow for deficit monetisation beyond the current crisis; it would also create a monetary board, led by the finance minister, sitting atop the central bank.Footnote2

Indonesia experienced the dangers of ‘money printing’ and hyperinflation in the final years of Sukarno’s presidency. The Soeharto government reined this in with a strict balanced budget rule. A further safeguard was introduced with the 1999 BI law giving BI clear independence and barring it from directly financing the deficit. But with the arrival of Covid-19, some of these strictures have been loosened. BI first intervened heavily in the secondary market for rupiah bonds during the violent investor sell-off in March and April of this year. It also quickly agreed in April to directly purchase bonds from the government as a buyer of last resort. By mid-year, BI had gone much further, agreeing to a ‘burden sharing’ scheme to help finance up to Rp 574.59 trillion (about 3.5% of GDP) of the significantly enlarged 2020 budget deficit of 6.3% of GDP at heavily subsidised interest rates.Footnote3

In normal times, Indonesia relies on foreign investors to finance a large part of its budget deficit by purchasing government rupiah bonds. Before the pandemic struck, non-residents typically held about 40% of these bonds. This share has now dropped to just over 30%. While capital outflows have abated, inflows are yet to return in a sizeable way. At the same time, the government’s borrowing requirements have greatly expanded, threatening a debilitating financing gap.

With few alternative funding sources, BI stepped in to help finance the budget deficit. This is unlikely to trigger a surge in inflation if it remains a limited emergency measure. BI purchases government bonds with newly created central bank ‘base money’, which circulates through the economy and ultimately winds up being deposited with the banking system. Depressed economic conditions mean that rapid credit growth is unlikely. The extra money created will more likely end up parked with the central bank—sitting in BI’s deposit facility as excess reserves or being actively mopped up by BI as part of open market operations. There is, however, no free lunch. BI must still pay interest on the excess liquidity it absorbs.

The main danger of deficit monetisation is the longer-term risk that seemingly cheap central bank financing will prove difficult to give up and ultimately give way to fiscal profligacy. If BI continued sterilising the increased liquidity, this would crowd out the private sector via higher interest rates and financial repression. If BI did not, it would eventually lead to a surge in inflation or even currency debasement.

The burden-sharing scheme was billed as a one-off. But given the allure of seemingly cheap central bank funding, it is perhaps unsurprising that some parliamentarians now propose to enshrine this as an ongoing capability available at any time of economic uncertainty. Combined with the proposal for BI to be overseen by a monetary board led by the finance minister, such changes would cast the independence of the central bank, and its ability to resist unwarranted pressures to fund the budget deficit, in serious doubt. Ironically, if these changes were passed, the erosion of BI’s credibility with financial markets would likely make it harder, not easier, for the central bank to support the government budget through the current crisis, without triggering destabilising capital outflows.

Recent media reports suggest that these specific proposals do not have serious support within the legislature or the executive, with the latter reportedly being more focused on restructuring the coordinating mechanisms for banking system stability.Footnote4 That is just as well. Nonetheless, the signs are that burden sharing could continue for the duration of the Covid-19 crisis. BI governor Perry Warjiyo has said that the central bank will continue to serve as the standby buyer for government bonds into 2021.Footnote5 President Widodo has indicated that burden sharing might continue for some time if growth remains depressed.Footnote6

BI still enjoys a high degree of credibility with the markets. That, however, could dissipate quickly if there are signs that Indonesia intends to engage in repeated largescale deficit monetisation. It would be better to define a more targeted approach, with less concern about the government’s rising interest bill and greater focus on protecting the credibility of BI and its ability to intervene if truly needed. If alternative deficit funding sources are available from the market at a broadly reasonable cost, they should be taken up. Any BI support should be structured to ensure that the bonds purchased are anchored to the market price during ‘normal’ times. These should also be easily tradeable, in order to aid BI liquidity management. Most important, an exit strategy is needed to make clear that this is a temporary emergency measure, and not the new normal.

Roland Rajah and Stephen Grenville, Lowy Institute

More concerning are the potential long-term poverty effects driven by structural damage to the economy from a persistent Covid-19 presence and a prolonged economic recession due to firm closures and unemployment. First, if economic growth does not recover, unemployment is likely to increase among formal sector wage workers and lower–middle-income earners who are not covered by the social protection programs. Recent employment and poverty statistics are not yet available, but high-frequency surveys provide some evidence of new pockets of unemployment. A World Bank (Citation2020) survey of wage workers in manufacturing and construction finds that 24% of breadwinners had stopped working in May, falling to 10% in August.Footnote8 Second, unemployment among low-skilled workers may lead to structural unemployment if the recession is followed by a skill-biased recovery; that is, if low-skilled workers in low-wage jobs are replaced by a younger and better educated cohort (Manning, forthcoming). Both of these scenarios are beyond the scope of the current set of programs in the economic recovery plan and highlight the importance of protecting private sector workers from the Covid-19 economic fallout.

PREPARING HEALTH AND EDUCATION FOR THE NEW NORMAL

What are the main challenges ahead for the health and education sectors under the new normal? These sectors are crucial for human capital development and poverty reduction, yet government policy seems focused on current practical concerns of Covid-19 rather than the repercussions of the pandemic in the medium-to-long term. As the vanguard in the fight against Covid-19, the health sector faces challenges that are both daunting and complex. We focus here on the implications of Covid-19 for the functioning and sustainability of the National Health Insurance (JKN) scheme, which forms the financial foundation of Indonesia’s public health system. For the education sector, we look at all levels of education (primary, secondary and tertiary) going into the current academic year, and how institutions have been preparing for and delivering education, faced with the uncertainties of the new normal and the escalating pandemic.

National Social Health Insurance

The social security system in Indonesia is not equipped to deal with the health and economic shocks associated with a pandemic. The system is designed to manage shocks such as sickness, work accidents, retirement and death. But it is biased towards the formal sector and still does not include unemployment insurance. Without this insurance, the government is struggling to protect those who have become unemployed because of the Covid-19 shock.

The Covid-19 pandemic undermines Indonesia’s social health insurance system through two channels: by increasing unemployment (or reducing hours worked and earnings) in the labour market, and by crowding out non-Covid-19-related care in the health care sector. As of 31 July, active JKN memberships had fallen by 5.4 million as premium contributions were withdrawn for many workers; this is equivalent to 2.7% of the total active JKN membership (BPJS Kesehatan 2020). To a large extent, this is the result of an estimated 3.5 million formal and informal workers losing their jobs since March 2020.Footnote9 The drop in the active JKN membership was especially large in the informal sector, falling by 2.4 million (or 16%) from January to September 2020. The formal sector membership also experienced a decline, especially in the second quarter: between March and June, the active membership fell by 0.5 million (or 2%). Since JKN membership includes the worker’s family, the whole family will drop out of the JKN system if a formal sector worker loses JKN coverage through unemployment.

Finally, memberships subsidised by local governments also dropped significantly, by about 1.8 million, suggesting that some local governments stopped their subsidy programs.Footnote10 An active JKN membership provides insurance for treatments in all public and most private health facilities; without JKN membership, a patient is required to pay out of pocket. However, treatment for Covid-19 is free for all Covid-19-confirmed patients, with the cost of treatment borne not by the JKN but by the central government.

As active JKN memberships decreased, the utilisation of health care declined, especially for non-Covid-19-related issues. Monthly referrals from primary to secondary or tertiary care dropped by more than 60%, from just under nine million in January to just over three million in May. We see a similar trend for hospitalisations, which declined from 1.1 million to less than 0.5 million per month. One reason is that Covid-19 treatment crowds out other health care, as resources are diverted and some health care services are limited or even put on hold. Fear of contracting Covid-19 at health care facilities is also known to prevent utilisation of primary care. The lack of an active JKN membership may further reduce the incentive to seek health care.

The decline in non-Covid-19-related health care has been observed worldwide and may have severe long-term health implications, as crucial diagnoses and treatments are postponed or forgone. In the long term, health care utilisation is expected to rebound as waiting lists are reduced, while, for some patients, more intensive treatment may be required if essential treatment has been delayed.

These developments may undermine the financial sustainability of Indonesia’s social health insurance system, as a result of revenue losses due to reduced premium payments combined with the increased costs of health care in the long term. In the short term, JKN membership rates are sufficient to cover health care costs, as utilisation is suppressed by Covid-19.Footnote11 But as the health care system recovers and health care services are resumed, the JKN will need financial support to make up for its lost revenues.Footnote12

The national recovery package includes bolstering contribution assistance to the JKN by Rp 3 trillion. The aim is to subsidise the premium contributions of 34 million self-enrolled members and non-employees who are registered for classthree insurance from July to December 2020. This support is designed to prevent further loss of self-enrolled members until the end of the year.

However, the subsidy does not cover all lost memberships and is not sufficient to return active JKN participation to the levels before Covid-19. First, the subsidy is based on the membership level in June and does not cover people who dropped out before then. Second, it does not cover formal sector workers who have dropped out or members who have lost local government funding for their memberships. Central government support should therefore aim to not only halt declining membership but also extend contribution assistance to members who were previously covered by local governments.

In 2021, JKN membership activity will depend on economic recovery. The key policy priorities will be to (1) expand the target group of informal sector workers whose premiums are subsided by the central government, as the Covid-19 crisis has revealed that this group is very exposed to macro shocks; (2) to address membership loss in the local government-subsidised group through cofinancing or by replacing local government subsidies with central government subsidies; and (3) to develop an on-demand application system for transitional subsidies to support formal sector workers who become unemployed.

The Education Sector

One of the earliest measures taken to slow the spread of the virus in Indonesia was to close schools, in some regions as early as mid-March. While potentially effective in limiting the spread of the virus, school closures can disrupt education, with potentially harmful long-term human capital implications. There seems to be consensus among education specialists that the disruptions to education due to school closures are likely to lead to persistent learning losses. A number of studies suggest that even temporary disruptions have long-run implications, such as reduced future earnings for the affected students (Azevedo et al. Citation2020; Andrabi, Daniels and Das Citation2020; Kaffenberger Citation2020).

The disruptions are likely to have heterogeneous effects. Students from poorer backgrounds or with adverse learning conditions at home are expected to be affected more severely. To prevent a widening education gap, a policy focus on recovering and remedying the learning losses, especially among the most affected groups, will be key when schools reopen. A number of different teaching practices— in particular, expansion of teaching hours and tailoring of teaching to specific learning needs—have been proposed and are being implemented in Indonesia as a means to recovery (Beatty et al. Citation2020).

In the following subsections, we provide an overview of the main challenges that schools have faced during the Covid-19 pandemic and discuss how they can address these challenges and prepare going forward. We provide insights from all levels of education, from primary to tertiary. Our findings are based on two sets of primary data that we collected in September and October 2020. First, we conducted a telephone survey with school principals of 50 randomly sampled primary and secondary schools in the Greater Jakarta area, the hot spot for Covid-19 (see the earlier section on ‘Covid-19 in Indonesia’).Footnote13 Second, as a proxy for tertiary education, we conducted an online survey of administrators of all economics departments at Indonesian public universities. We collected responses for 47 departments with an undergraduate program (the response rate was 100%) and 26 departments with a graduate program (the response rate was 90%).Footnote14

Primary and Secondary Education

In late June 2020, the government enacted a set of regulations for reopening schools. The directive envisaged that schools would reopen as early as July 2020 in a staggered fashion. Junior and senior secondary schools were allowed to reopen at the start of the school year (July), primary schools in October and early childhood education centres in December 2020 at the earliest. To date, there is no schedule for tertiary education institutions to reopen. The directive dictates further criteria for reopening, most notably that a district can only reopen schools if the district has zero current Covid-19 cases. As soon as a positive case is recorded, schools must close again (Arsendy et al. Citation2020). In practice, this means that only a minority of schools are authorised to reopen. At the time of writing, only 48 of the 514 districts and cities in Indonesia were without Covid-19 (Satgas Covid-19 2020). The staggered reopening of education facilities, together with the zero tolerance for the Covid-19 caseload, creates uncertainties for schools and students. Linking school openings to the Covid-19 caseload will likely create ongoing disruptions, and it remains to be seen how schools and students will respond to this in the short-to-medium term.

All the schools in our sample have been closed since March and were still closed at the time of the survey interviews. Principals expect to reopen in January 2021 at the earliest, with 40% expecting to reopen only after March 2021. All the schools have moved to provide education via distance learning. The main challenges to distance learning, irrespective of school type, are internet costs and access, while over half the sample also mentioned a lack of hardware (). In addition, schools find it challenging to monitor their students’ progress through distance learning. Such monitoring is crucial for identifying the students who are most subject to learning losses due to the crisis and who require additional support.

Table 5. Perceived Barriers to Distance Learning in Primary and Secondary Schools in DKI Jakarta, September–October 2020 (%)

At the moment, only four of the interviewed schools (three primary; one secondary) expect students to drop out of school because of the school closures. Yet principals from primary schools report that they have not been able to get in touch with about 10% of their students, and secondary schools cannot contact about 12%. The Jakarta school principals’ perceptions echo some of the earlier findings for the whole of the country (see Arsendy et al. Citation2020). Students most at risk of losing out because of the crisis are those from lowerand lower–middle-income households, who face considerable difficulty accessing the internet and other means of communication.

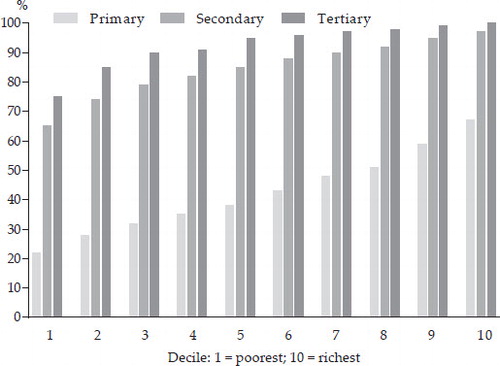

Prior to the Covid-19 crisis, internet access varied greatly across Indonesian provinces: average access in 2019 was about 40%, ranging from 20% in Papua to 66% in Jakarta (Arsendy et al. Citation2020). Looking specifically at internet access for students at the onset of the pandemic, based on the March 2020 Susenas, shows that access increases with age and household income. On average, 40% of primary school students but 84% of secondary school students, and nearly all students in tertiary education, have access to the internet.

FIGURE 7 Student Access to Internet by Education Level and Income Decile

There is also a strong correlation between students’ access to the internet and household income. At the primary school level, internet access increases from about 22% of students in the poorest decile to about 67% of students in the wealthiest decile. For secondary education, we see a less steep gradient by income, with internet access for the wealthiest students almost 50% higher than for the poorest (97% and 65%, respectively). At the tertiary level, almost all students from the wealthiest decile have access to internet, while about 25% of the poorest group still does not. Although school principals do not expect to return to face-to-face schooling before January 2021, they have already prepared for reopening, in particular with regard to preventive health measures. All report having health protocol as well as sufficient sanitation facilities. Furthermore, both teachers and students will be required to wear face masks in class. However, schools seem less prepared to address the potential learning losses of students who cannot be reached or sufficiently monitored through distance learning. Just over 69% of primary schools and 71% of secondary schools have considered offering additional teaching to students who cannot be reached (). Additional teaching during holidays is being considered by just over 33% of primary schools but 50% of secondary schools. Finally, about 30% of primary schools and 50% of secondary schools are prepared to reduce the curriculum content for this academic year.

Table 6. Plans for Complementary Teaching in Primary and Secondary Schools in DKI Jakarta, September–October 2020 (%)

Principals do not see teacher quality per se as a concern. Across the board, about 67% of primary school principals claim that their teachers have received adequate professional development and training to deliver distance learning. The percentage is even higher, at 79%, among secondary school principals. The results for our Jakarta sample, however, contrast with broader nationwide concerns that Indonesian teachers are ill-equipped to deliver schooling from home. For example, the World Bank (Citation2016) estimated that only 5% of primary school teachers in Indonesia are capable of significantly improving the learning levels among their students.

In response to the Covid-19 crisis, the education ministry has removed constraints on the use of School Operational Assistance (BOS) funds. Before schools were closed, up to half of the BOS funds could be used to pay for contract teachers who were already registered with the ministry. When schools started to close, the ministry removed this restriction, enabling more flexible use of the funds. BOS funds can now be used to purchase health and sanitation supplies, internet data credit and subscriptions to online learning platforms, which had previously not been mandated. While teachers have continued to receive salaries during school closures, all schools in our sample have reduced other benefits for teachers. All schools report having used BOS funds to help teachers and students pay for internet quotas. However, only 64% of primary schools report having taken advantage of the government’s internet subsidy quota program, while all junior and senior secondary schools have done so.

Satisfaction with the support received varies by school type. Among primary schools, about 53% are satisfied with the support received from the government; at the secondary level, the percentage is 71%. Schools would appreciate additional support for improved internet access and further support for internet quotas, as well as general support for school budgets and facilities.

In conclusion, schools expect the closures to continue longer than the government has planned, and these closures may increase learning losses. Despite this uncertainty, most schools seem to be prepared for extended closures and distance learning. However, they are still largely preoccupied with maintaining day-to-day teaching and applying preventive health measures to allow reopening. To date, there has been little focus on developing and implementing strategies to reduce learning losses. Schools will need clear directives and support to increase teaching hours and introduce ways to recover learning losses.

Higher Education

As of October 2020, it was still unclear if and when there would be a return to in-class teaching at the tertiary level in the 2020–21 academic year. Enrolment rates in tertiary education remained stable overall and even increased significantly for bachelor programs for the teaching term following the introduction of Covid-19 restrictions. The positive trend in student numbers was also reflected in the finding that only 8% of administrators reported difficulties in enrolling new students in bachelor programs. In contrast, almost half (45%) of the administrators for master courses reported that maintaining student numbers was challenging, and almost all program administrators (95%) reported that they had reduced tuition fees because of Covid-19.

All programs had shifted their classes to online platforms and started online teaching by April 2020 at the latest. The number of courses offered online has increased gradually. For the winter term, all the master and higher-level programs have shifted 80%–100% of their courses online. Among the bachelor programs, 82% are now offering 80%–100% of their courses online.

Online courses require adequate supporting infrastructure. Unsurprisingly, internet costs and internet access are identified as the main challenges faced by program administrators (). The same holds for students. Most bachelor (84%) and master (85%) students report that internet costs and internet access are their main problems. About 84% of the bachelor programs and 90% of the master programs report having taken action to address these challenges, mostly by providing financial aid and internet quotas for students (in about 40% of programs) or by offering flexible lecture and assignment times.

Table 7. Main Challenges Perceived for Adjusting Teaching to the New Normal, September–October 2020 (%)

Changes in teaching modes have also had some positive aspects. A stronger reliance on the internet has led students to become more engaged in technology for learning and more active in looking for information and materials, while teaching has become more interactive. The main positive aspects of online teaching identified by respondents, irrespective of the program degree, are that schedules can be managed more flexibly (30%) and that time and money can be saved, as the respondents no longer need to commute to and from campus (14%).

Most universities have been providing training and professional development to their lecturers during the Covid-19 crisis: 82% of program administrators for bachelor programs, and nearly 80% for master programs, report providing training for their teaching staff.

Overall, administrators have not seen a large drop in teaching quality as a result of moving to online courses. If anything, there seems to be a tendency to report improved quality, indicating at least a perception of improved teaching quality. This is also reflected in student feedback. Master programs that have collected student feedback report that it was satisfactory in all cases. For the bachelor programs, 14% of students rated teaching performance as satisfactory, 67% as good to very good and only 17% as not satisfactory. The overall objective for almost all program administrators for the coming term and beyond is to further improve the quality of e-learning.

The current plans of the education ministry for a phased reintroduction of face-to-face learning meet the approval of most administrators (73%). While about 25% expect that a return to face-to-face teaching is likely by January 2021, 28% think February is more realistic, with the remainder anticipating a return by March 2021 or later.

So far, the disruptions to higher education do not seem to have been severe. Most universities have been able to make a swift transition to online teaching, and internet access is not a key obstacle for the majority of students. However, for a substantial group of students, especially those from low-income households, the cost of distance learning remains significant and adapting to the new normal is less straightforward. To avoid a widening gap in access to higher education, the government should consider further general support to facilitate distance and online learning. A welcome start is the decision of the education ministry to allocate Rp 7.2 trillion for subsidised phone credit and internet data packages for university students, school students and teachers. However, the success of this program will depend on improving the stability and coverage of internet networks in remote areas and particularly in many of the eastern regions of Indonesia. A lack of access to communication devices is another obstacle, especially for students from lower-income households.

Supplemental Material

Download PDF (120.7 KB)ACKNOWLEDGMENTS

We thank Canyon Keanu Can, Fauzi Estiko and Khalida Fauzia for their excellent research assistance. We are grateful to Hal Hill, Budy Resosudarmo and the reviewers for their valuable feedback, and to Chris Manning for his support throughout the development of this Survey.

Notes

17 https://www.thejakartapost.com/news/2020/09/28/bi-buys-15-7b-in-govt-bonds-to-support-economy.html

1 Reliable alternative data on death rates are not available. However, information on funerals in Jakarta indicate the extent of underestimated fatalities. Jakarta’s Agency of Parks and Cemeteries reports a total of 6,388 funerals involving the Covid-19 protocol (up to 27 September), about 21% of all burials in 2020. The involvement of the Covid-19 protocol implies that the deceased was a suspected Covid-19 case, even if this had not been confirmed by a test. The formal number of confirmed Covid-19 deaths for Jakarta up to 27 September was 1,692, only a quarter of the number of suspected cases (Paat and Bisara Citation2020).

2 For example, Indonesia did not impose shop closures, curfews, stay-at-home orders or a shutdown of domestic travel. The Government Response Stringency Index, measuring the number and strictness of government policies, also reveals that the stringency of Indonesia’s response to Covid-19 trailed that of other countries (Hale et al. Citation2020).

3 For example, a survey by Statistics Indonesia (BPS 2020a) found that 17% of respondents believe it very unlikely or even impossible that they will be infected with Covid-19. A third of respondents with a primary education or less take this position, compared with 13% who have a tertiary education. This suggests that the perceived risk of Covid-19 is strongly correlated with level of education.

4 Bio Farma, a state-owned enterprise (SOE) for vaccine production, has completed a third round of clinical trials of a vaccine. It hopes to obtain approval from the National Agency of Drug and Food Control (BPOM) to start preparing for mass production in the first quarter of 2021 (Danareksa Research Institute Citation2020). The government has assigned SOEs to participate in multilateral cooperation to develop Covid-19 vaccines. Bio Farma is collaborating with Sinovac (China), Kimia Farma with Sinopharm (China), and Kalbe Farma with Genexine (South Korea) (Ministry of Health Citation2020b). See also Gesuri (Citation2020).

5 The core inflation rate per annum dropped from 2.7% in May to 1.9% in September. In August and September, the consumer price index decreased by 0.05% compared with the previous month.

6 Based on data from the IMF’s ‘Policy Responses to Covid-19’ web page: https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-Covid-19.

7 See Olivia, Gibson and Nasrudin’s August Survey in BIES for a discussion of social protection programs. The online appendix table compares the details of programs in the pre-and post-Covid periods to show how they have been expanded to accommodate the PEN package. The table is available here: http://dx.doi.org/10.1080/00074918.2020.1854079.

8 An online survey by Hanna and Olken (Citation2020) finds higher unemployment rates for August, of around 60%, among respondents who reported that they were working in February (down from about 70% in June). However, the authors’ online survey methods may lead to overstated unemployment rates.

9 Coordinating Ministry for Economic Affairs presentation, 26 August 2020. Formal sector workers are enrolled through employers, so active membership relies on employers’ paying the premiums. Informal sector workers are required to self-enrol and pay premiums.

10 The reduced membership support by local governments was most prominent in Greater Jakarta, Central Java, Yogyakarta, Sulawesi and Banten. An interview with the Social Security Agency for Health (BPJS Kesehatan) revealed two possible reasons: an increase in the insurance premium in January 2020, and reduced fiscal capacity of local governments to subsidise premiums due to Covid-19.

11 Based on the JKN’s utilisation, claims and membership contribution data, BPJS Kesehatan estimates it will have a surplus of Rp 0.3 trillion to Rp 0.8 trillion (Dartanto, Wahyono et al. 2020).

12 The main financial risk for the JKN is that self-enrolled informal sector will drop out of the JKN. Only 40%–50% of self-enrolled informal sector members actually pay premiums (they remain registered but cannot access services). Yet the claim ratio for this group is almost 312% (that is, the cost of care for this group is three times higher than the revenue obtained from this group) (Dartanto, Halimatussadiah et al. 2020). The JKN relies on a broad and near-universal active membership to cover these claims.

13 Our sample comprised 36 primary schools, seven junior secondary schools and seven senior secondary schools. The schools were selected randomly from a database of public schools provided by the education ministry.

14 The survey was conducted in cooperation with the Indonesian Association of Economics Study Programs (APSEPI).

REFERENCES

- Andrabi, Tahir, Benjamin Daniels and Jishnu Das. 2020. ‘Human Capital Accumulation and Disasters: Evidence from the Pakistan Earthquake of 2005’. RISE Working Paper 20/039, RISE Programme, Oxford.

- Ariawan, Iwan and Hafizah Jusril. 2020. ‘Covid-19 in Indonesia: Where Are We?’ Indonesian Journal of Internal Medicine 52 (3): 193–5.

- Ariawan, Iwan, Pandu Riono, Muhammad N. Farid, Hafizah Jusril and Wiji Wahyuningsih. 2020. ‘Covid-19 Epidemic in Indonesia’. ADB presentation, 9 October.

- Arsendy, Senza, C. Jazzlyne Gunawan, Niken Rarasati and Daniel Suryadarma. 2020. ‘Teaching and Learning during School Closure: Lessons from Indonesia’. In Vol. 89 of ISEAS Perspectives. Singapore: ISEAS–Yusof Ishak Institute. https://www.iseas.edu.sg/wp-con-tent/uploads/2020/09/ISEAS_Perspective_2020_89.pdf

- Azevedo, João Pedro, Amer Hasan, Diana Goldemberg, Syedah Aroob Iqbal and Koen Geven. 2020. Simulating the Potential Impact of Covid-19 School Closures on Schooling and Learning Outcomes: A set of Global Estimates. Washington, DC: World Bank. http://pubdocs.world-bank.org/en/798061592482682799/covid-and-education-June17-r6.pdf

- Beatty, Amanda, Menno Pradhan, Daniel Suryadarma, Florischa Ayu Tresnatri and Goldy Fariz Dharmawan. 2020. Recovering Learning Losses as Schools Reopen in Indonesia: Guidance for Policymakers. Policy Brief. Oxford: RISE.

- BPJS Kesehatan (Social Security Agency for Health). 2020. Data Kepesertaan dan Utilisasi Rawat Inap dan Rawat Jalan Rujukan [Data on membership and utilisation of inpatient and outpatient referrals]. Jakarta: BPJS Kesehatan.

- BPS (Statistics Indonesia). 2020a. Perilaku Masyarakat di Masa Pandemi Covid-19 [Public behaviour in the time of the Covid-19 pandemic]. Jakarta: BPS. https://www.bps.go.id/ publication/2020/09/28/f376dc33cfcdeec4a514f09c/perilaku-masyarakat-di-masa-pan-demi-covid-19.html

- BPS (Statistics Indonesia). 2020b. Pertumbuhan Ekonomi Indonesia Triwulan II-2020 [Indonesian economic growth, Q2 2020]. Berita Resmi Statistik [Official statistics news] No. 64/08/ Th. XXIII. Jakarta: BPS. https://www.bps.go.id/pressrelease/2020/08/05/1737/-ekonomi-indonesia-triwulan-ii-2020-turun-5-32-persen.html

- BPS (Statistics Indonesia). 2020c. Analisis Hasil Survei Dampak Covid-19 terhadap Pelaku Usaha [Analysis of survey results on the impact of Covid-19 on businesses]. Jakarta: BPS. https://www.bps.go.id/publication/2020/09/15/9efe2fbda7d674c09ffd0978/analisis-hasil-survei-dampak-covid-19-terhadap-pelaku-usaha.html

- BPS (Statistics Indonesia). 2020d. Profil Kemiskinan di Indonesia Maret 2020 [Poverty profile in Indonesia March 2020]. Berita Resmi Statistik [Official statistics news] No.56/07/Th.XXIII. Jakarta: BPS. https://www.bps.go.id/pressrelease/2020/07/15/1744/persentase-penduduk-miskin-maret-2020-naik-menjadi-9-78-persen.html

- BPS (Statistics Indonesia). 2020e. Tinjauan Big Data terhadap Dampak Covid-19 [Big data overview on the impact of Covid-19]. Jakarta: BPS. https://www.bps.go.id/ publication/2020/06/01/effd7bb05be2884fa460f160/tinjauan-big-data-terhadap-dampak-covid-19-2020.html

- Danareksa Research Institute. 2020. Meredam Dampak Covid-19 [Mitigating the impact of Covid-19]. DRI’s Pulse Check 09/20. Jakarta. https://www.danareksa.co.id/publikasi/ riset/dris-pulse-check-meredam-dampak-covid-19/

- Dartanto, Teguh, Alin Halimatussadiah, Jahen Fachrul Rezki, Renny Nurhasana Chairina Hanum Siregar, Hamdan Bintara, Usman, Wahyu Pramono, Nia Kurnia Sholihah, Edith Zheng Wen Yuan and Rooswanti Soeharno. 2020. ‘Why Do Informal Sector Workers Not Pay the Premium Regularly? Evidence from the National Health Insurance System in Indonesia’. Applied Health Economics and Health Policy 18 (1): 81–96. doi: 10.1007/s40258-019-00518-y

- Dartanto, Teguh, Tri Yunis Miko Wahyono, Mundiharno, Benjamin Saut PS, Ocke Kurniandi, Citra Jaya, Mizmara Alan F. and Muthmainnah. 2020. Dampak Covid-19 terhadap Program JKN [The impact of Covid-19 on the JKN program]. BPJS Kesehatan Policy Brief.

- Gesuri, Ardian Taufik. 2020. ‘Presiden Jokowi memastikan, mulai Januari 2021 Indonesia vak-sinasi massal Covid-19’ [President Jokowi confirms, mass vaccination for Covid-19 will start in Indonesia in January 2021]. Kontan, 31 August. https://nasional.kontan.co.id/news/ presiden-jokowi-memastikan-mulai-januari-2021-indonesia-vaksinasi-massal-covid-19

- Hale, Thomas, Sam Webster, Anna Petherick, Toby Phillips and Beatriz Kira. 2020. COVID-19 Government Response Tracker, Blavatnik School of Government, University of Oxford. https://ourworldindata.org/grapher/covid-stringency-index?time=2020-01-22.

- Hanna, Rema and Ben Olken. 2020. ‘Online Survey on Economic Impact of COVID 19 in Indonesia’. Results from week 22. J-PAL Southeast Asia.