?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

We survey the empirical evidence on corporate survival and its determinants in European emerging markets. We demonstrate that (i) institutional quality is a significant preventive factor for firm survival in all sectors of the economy, which holds for small, medium and large firms alike. On the other hand, (ii) the impact of financial performance indicators is lower than one would expect. However, (iii) other firm-level variables play more important roles in firm survival, and the most important preventive factors are the legal form of a limited liability company, the number of large shareholders, and the presence of a foreign owner.

Introduction

Many studies have been conducted to determine what factors influence the performance of firms (Soriano Citation2010; Galbreath and Galvin Citation2008). Since firms are the primary units of wealth creation in any modern economy, such concern is understandable. However, a more basic question should be answered first – what makes firms fail or survive in the first place? Even though one might argue with a Schumpeterian “creative destruction,” by far not all firm failure is productive and beneficial. Hence, determining what factors contribute to firm failure or conversely firm resilience is crucial.

It is almost redundant to stress the vital importance of bank survival, as banks are the key mediators of economic activity, especially in continental Europe with less developed capital markets. Thus, bank failures can cause a disruption in the economy (Gerlach et al., Citation1998), and potential bailouts of troubled banks come at a great cost to taxpayers.

To date, only the internal factors influencing firm survival have been (barely) satisfactorily determined. However, the influence of external factors, such as institutional quality and financial environment, remains largely unknown.

In macroeconomic studies, institutions and their quality have been directly linked by an abundance of evidence to economic growth (Hall and Jones Citation1999; Acemoglu, Johnson, and Robinson Citation2001; Eicher and García-Peñalosa Citation2006; Fagerberg and Srholec Citation2008; Hasan, Wachtel, and Zhou Citation2009). With regard to firms, the influence of institutions on corporate performance has also been ascertained via various mechanisms. High-quality institutions positively affect entrepreneurial behavior (Urbano, Aparicio, and Audretsch Citation2019), risk taking, experimentation and innovation (Boudreaux and Nikolaev Citation2019); protect property rights, which increases firm entry and reduces firm exit (Johnson, McMillan, and Woodruff Citation2002; Desai, Gompers, and Lerner Citation2005); reduce the costs imposed on firms by regulatory burden and uncertainty (Acs and Szerb Citation2007; Acs, Desai, and Hessels Citation2008); and facilitate efficient transactions among firms (North Citation1993).

Financial development, i.e., the maturity of financial markets, can also affect firms’ performance, e.g., by imposing capital market discipline or offering better perceived insurance against expropriation or contract repudiation (LiPuma, Newbert, and Doh Citation2013).

The emerging European economies are quite peculiar. On the one hand, they are obviously less economically and institutionally developed than Western countries; as such, the impact of institutions on firm survival is likely greater than that on their more developed counterparts (Acemoglu et al., Citation2005). On the other hand, the area underwent rapid economic and political transformation in the 1990s in the aftermath of the fall of the Berlin Wall and the dissolution of the former Soviet Union. The transformation was so radical that it was often called “shock therapy.” The reforms accompanied by mass privatization and restructuring were predominantly aimed at creating a competitive free market environment (Aussenegg and Jelic Citation2007; Kočenda and Hanousek Citation2012a), which held doubly so for countries that later joined the European Union (EU) because they had to pass an uneasy rigorous screening process (Estrin et al. Citation2009) scrutinizing their institutions, economic progress and competitiveness. An uneasy transformation way is still echoed in a fact that even after number of years the variability of the GDP growth in most advanced emerging European economies (new EU countries) is larger than that of the old EU economies (Kočenda and Poghosyan Citation2020). Thus, an analysis of the relation between institutional quality and firm survival in this specific region should be enlightening and helpful for further economic research.Footnote1

This paper seeks to fill a double vacancy – the lack of empirical literature on the influence of institutional quality on firm survival in general and the absence of such literature in the region of emerging European economies, specifically. The article is based mainly on recent research on corporate survival in emerging European markets, which will be referred to as core papers (Baumohl, Iwasaki, and Kočenda Citation2019; Iwasaki and Kočenda Citation2020; Baumohl, Iwasaki, and Kočenda Citation2020; Kočenda and Iwasaki Citation2020; Iwasaki, Kočenda, and Shida Citation2022). However, the survey also includes other relevant research. It synthesizes the empirical evidence obtained separately for various firm categories – medium and larger businesses, small businesses, service firms and banks.

The remainder of this paper is organized in the following manner. Section 2 presents a brief literature review on the topic of firm survival, specifically aimed at the already more researched developed markets, to provide a mental starting point for comparison with emerging markets. Section 3 describes the data used in the subsequent analysis and the methodology used for estimation, namely, the Cox proportional hazards model. The results for firm-level variables are comprehensively summarized in Section 4, which is divided into several subsections. Section 5 is the main contribution of this paper. It examines the influence of institutional quality on firms’ survival in emerging European economies, an area not properly researched previously. Finally, Section 6 concludes.

Literature Review

As already mentioned, there is an abundance of literature linking the quality of institutions with the macroeconomic performance of countries (North Citation1990; Hall and Jones Citation1999; Acemoglu, Johnson, and Robinson Citation2001; Eicher and García-Peñalosa Citation2006; Fagerberg and Srholec Citation2008; Hasan, Wachtel, and Zhou Citation2009), as well as with the performance of companies (Porter Citation1998; Yasar, Paul, and Ward Citation2011; Faruq and Weidner Citation2018; Ghoul, Guedhami, and Kim Citation2017). However, there is limited evidence linking institutional quality and financial development with the survival rates of firms. Desai, Gompers, and Lerner (Citation2005) provide evidence from European firms suggesting that greater protection of property rights and greater fairness increase firm entry and reduce firm exit rates. Che, Lu, and Tao (Citation2017) and Zhang et al. (Citation2017) identify a positive linkage between property rights protection and the survival chances of Chinese firms and, conversely, a negative influence of government corruption.

Tsoukas (Citation2011) show in a sample of Asian firms that better financial development is helpful for firm survival in general, especially for medium and larger firms. Schäfer and Talavera (Citation2009) document the negative effects of financial constraints on the survival chances of small German firms. Similar results are obtained by Musso and Schiavo (Citation2008) for the French manufacturing industry, where SMEs play a predominant role. Farinha, Spaliara, and Tsoukas (Citation2019) describe how exposition to bank funding outflows contributes to the failure of Portugal’s small businesses. A positive influence of financial development on firm survival is also suggested by Gagliardi (Citation2009).

Moving on to firm-level variables, Görg and Spaliara (Citation2014) show, unsurprisingly, positive effects of a firm’s good financial health on survival in the case of French and British firms. These results are confirmed by Guariglia, Spaliara, and Tsoukas (Citation2016), who also studied British firms during the GFC, and are also in accordance with the results of Musso and Schiavo (Citation2008) based on French manufacturing data. There is an array of literature concerned with determinants of bank failure for US banks, which is also predominantly focused on financial ratios. Among this literature are Whalen (Citation1991), Wheelock and Wilson (Citation2000), Hwang, Lee, and Liaw (Citation1997), Calomiris and Mason (Citation2003), DeYoung (Citation2003), Cebula (Citation2010), Cole and White (Citation2012) and Carmona, Climent, and Momparler (Citation2019). As expected, these studies generally find that good financial health of banks increases survival chances. Lin and Yang (Citation2016) show that what contributes to the survival probability of banks in East Asia, apart from sound bank fundamentals, are desirable economic conditions measured by GDP growth, inflation, unemployment, etc.

Another set of variables used in the core papers is aimed at investigating the effects of various types of ownership on survival probabilities – foreign ownership, state ownership and large shareholding. Ch and Gelübcke (Citation2015) conclude that foreign ownership is negatively correlated with exit rates for German firms in export markets but positively correlated with those in import markets. Alfaro and Chen (Citation2012) document a higher resilience of multinational subsidiaries compared to local counterparts using worldwide data. Taymaz and Özler (Citation2007) show, in the Turkish manufacturing industry, that foreign plants have higher efficiency and survival probabilities for firms only in the initial phases but not in the long term and that the benefits of foreign direct investment disappear when the industry and other factory characteristics are controlled for. Mata and Portugal (Citation2004) document sharp differences between small domestic and foreign firms in terms of their entry and survival and find that domestic firms have higher exit rates than both newly established and recently acquired foreign firms. Estrin et al. (Citation2009) provide evidence of the positive role of foreign ownership caused not only by the provision of additional investments but also by microlevel reforms of management practices and corporate governance.

With regard to large shareholding, two strands of literature present opposing conclusions. One side argues that large shareholding is connected with increased risk of failure – the expropriation hypothesis (Claessens, Djankov, and Lang Citation2000). The other concludes that large shareholding enhances the survival probabilities of firms – the alignment hypothesis (Shleifer and Vishny Citation1986).

Evidence that the corporate legal form also likely plays a significant role is provided by Harhoff, Stahl, and Woywode (Citation1998), who find that German limited liability companies have higher growth but also higher insolvency rates.

Being listed should be reflected by a better ability of a company to access external funds, which in turn should be positively correlated with growth and survival (Musso and Schiavo Citation2008). Moreover, Mannasoo and Mayes (Citation2009) document that listed banks in Eastern Europe are significantly less prone to distress than are banks that are not listed. One of the channels that could drive this effect is the imposition of market discipline by the disclosure requirements that accompany being listed.

Geroski (Citation1995) prove that firm size and age are both positively correlated with firm survival. Agarwal and Gort (Citation2002) also find evidence that smaller firms are exposed to higher hazard rates. These results are generally confirmed by Klepper and Thompson (Citation2006), who admit that the results might be caused by an omitted variable.

Data and Methodology

Data

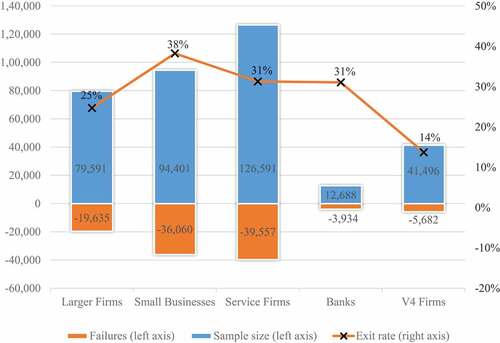

The firm-specific data in all five core papers are obtained from Bureau van Dijk’s Orbis database. The advantage of the Orbis database is that it retains data even for already inactive firms, which makes the analysis possible in the first place. The period being studied spans from the beginning of 2007 until the end of 2015, with the exception of small businesses (Iwasaki, Kočenda, and Shida Citation2022), where the estimation period also includes 2016 and 2017. All firms in the sample satisfy the following conditions: they were active at the end of 2006 and their survival status was known at the end of the estimation period (2015 or 2017). The sample size is on the order of tens of thousands in all cases. Some samples in the core papers overlap to a small degree. A firm is considered to have failed if it is inactive or dormant, in liquidation or bankruptcy and/or dissolved. The precise sample sizes, number of failures, and respective exit rates are shown in . Further, a complete list of both country-level and firm-level factors hypothesized to impact firms’ survival (variables) is provided in , which also contains the definition of the variables and their source. Finally, Appendix offers a comprehensive overview of the specific variables used in each of the core papers.

Figure 1. Number of observations, failed firms, and exit rates.

Table 1. ~TC~

Cox Proportional Hazards Model

The core papers use a survival model, namely, the Cox proportional hazards model (Cox Citation1972). In general, an advantage of survival models over standard logit models is that survival models allow the hazard ratio to vary over time, making it possible to obtain dynamic results. Furthermore, survival models do not need to use proxies for firm failure, which might preclude accurate comparison with other studies. Due to this feature, the Cox model is called a semiparametric model. Another specific advantage of the Cox model is that, in contrast to parametric survival models, there is no need to make assumptions about the baseline hazard function, thereby circumventing the potential risk of inaccuracies stemming from faulty assumptions. Thus, the Cox proportional hazards model is the most commonly used technique in empirical survival studies (Manjón-Antolín and Arauzo-Carod Citation2008).

The description of the model itself begins with the definition of the hazard function (h(t|x)):

The hazard rate h for subject i at time t depends on the set of covariates x. The parameters β are the subject of the estimation. Consider two observations i and i with different values of covariates x, with the following linear representation:

and

Then, the so-called hazard ratio for these two observations is defined as

Note that they are independent of time t because the hazard ratio (hazard proportion) is constant over time in the model, hence the name proportional hazards.

Estimates of parameters β are obtained via maximum-likelihood estimation of the logarithmic transformation of specification (1), which is represented by the following linear model:

Similar to Esteve-Pérez, Sanchis Llopis, and Sanchis Llopis (Citation2004), Taymaz and Özler (Citation2007) and Che, Lu, and Tao (Citation2017), the resulting parameters β are presented as hazard ratios because such form enables a convenient and straightforward interpretation. The value of a hazard ratio of a covariate can be interpreted as a multiplier of the probability of failure resulting from a one-unit change in the covariate. Hence, every covariate with a hazard ratio over 1 increases the firm’s risk of failure, and covariates with values less than 1 enhance the chances of survival. The further the hazard ratio is from 1, the more strongly the covariate influences the survival chances of a firm. For example, if the hazard ratio of covariate A is 0.8 and the hazard ratio of covariate B is 1.3, then a one-unit increase in A results in a 20% improvement in firms’ survival probability and, conversely, a one-unit increase in B increases the firm’s risk failure by 30%.

As Liu (Citation2012) warns, the problem of endogeneity may arise in survival analysis under certain conditions, namely, a) an independent variable is a future variable, b) the estimation period is very short, and c) the dependent variable is continuous. However, the estimations in the core papers should not be endangered by these problems for the following reasons. First, all independent variables are predetermined; thus, the potential problem of endogeneity arising from simultaneity between dependent and independent variables is avoided. Second, the estimation period is almost a full decade, which is a sufficiently long time. Last, the dependent variable is binary (survival/failure) and observed on a yearly basis; therefore, the last potential problem can be ruled out, as the dependent variable is surely not continuous.

Impact of firm-level Variables and Corporate Characteristics

Financial Performance

Of all the characteristics of a firm that could impact firm survival, financial performance would probably come to mind first for most people. Naturally, the assessment of firm-level variables starts with financial performance.

The following indicators have been used as proxies of financial performance to assess its impact on the survival probability of firms and banks: solvency ratio, gross margin (profit margin), and ROA. In addition, the estimation of banks also included the liquidity ratio.

All aforementioned indicators show statistically significant survival-enhancing effects for both small businesses and larger firms, as expected. However, the magnitude of the effect is very modest, approximately 3–5%, with small businesses reaping slightly more benefit. The results are consistent for all country groups based on institutional quality and for all geographic regions, with the sole exception of the V4 countries, where the effect is economically negligible. The effect is almost equal for different economic sectors.

The results are more disappointing in the case of banks. Here, the survival-enhancing effect of financial performance indicators is negligible, and the liquidity ratio even points in the opposite direction (being a hazard factor). Moreover, after a geographic division, statistical significance is retained only for Russia and Ukraine; these aggregate results are not driven by an abnormal event. Rather, the effect is time invariant in the sample. Therefore, financial performance does not influence the survival prospects of banks in emerging European economies.

The positive effects of the financial performance indicators of firms are in accordance with most of the existing evidence. Nevertheless, the literature is by no means unanimous on this matter. Görg and Spaliara (Citation2014) find a positive influence of a higher coverage ratio and lower leverage on the survival prospects of French and British exporting firms. Guariglia, Spaliara, and Tsoukas (Citation2016) show that an increased interest rate burden (which worsens firm solvency) is strongly associated with an increased risk of failure of UK firms; this relationship proved to be especially strong during the GFC. Banerjee and Ćirjaković (Citation2021) find results similar to ours for Slovenian firms. Higher leverage and liquidity are associated with an increased risk of failure in their sample. They attribute the counterintuitive effect of liquidity to the possibility that firms with high liquidity have bleak growth prospects, prompting them to voluntarily decide to exit. However, they find no significant relationship between profitability and risk of failure. Chiaramonte and Casu (Citation2017) also find no significant relationship between the failure of EU banks and the profitability indicators return on average assets (ROAA) and cost-to-income ratio (CIR). Hong, Huang, and Wu (Citation2014) suggest that while systemic liquidity problems contribute to bank failure in the US, there is no significant relationship between a bank’s liquidity on an individual level and its risk of failure.

The evidence suggests that the influence of financial performance is indeed less than one would expect. The following subsections clearly show that other indicators have a much larger impact on the survival prospects of firms and banks, at least in emerging European economies.

Ownership

The variables under the category of ownership are foreign ownership, state ownership and number of large shareholders. This subsection summarizes the results of the factors.

In regard to the survival of medium and large companies, as well as small businesses, foreign ownership is the single most beneficial factor, decreasing the risk of failure by approximately 40% in aggregate. The effect is slightly weaker in countries with high institutional quality and, conversely, even higher for firms in countries with low institutional quality. The sectoral breakdown clearly shows that mining and manufacturing profit the most from foreign ownership.

Foreign ownership also proves to be a factor that considerably enhances the probability of survival of banks in the sample. This effect is especially strong for banks in Russia and Ukraine and most profoundly in the Baltic states. Foreign ownership is most beneficial for banks with worse financial conditions (measured by solvency and ROA).

This finding is supported by the evidence that foreign owners help not only by bringing investments but also microlevel reforms in spheres such as management practices and corporate governance (Estrin et al. Citation2009). This is also in line with the results of Alfaro and Chen (Citation2012), who document a higher resilience of multinational subsidiaries compared to local counterparts using worldwide data. Mata and Portugal (Citation2004) document sharp differences between small domestic and foreign firms in Portugal in terms of their entry and survival and find that domestic firms have higher exit rates than both newly established and recently acquired foreign firms. However, the same authors find no difference in survival between domestic and foreign firms after controlling for various characteristics in larger firms (Mata and Portugal Citation2002). Taymaz and Özler (Citation2007) find that Turkish manufacturing plants with foreign owners perform better and survive longer than domestic plants, but the effect disappears when they control for industry and plant characteristics. Ch and Gelübcke (Citation2015) also arrive at ambiguous results. Their estimation shows that foreign ownership is negatively correlated with exit rates for German firms in export markets but positively correlated with those in import markets. Our finding of positive effects of foreign ownership on banks is in accordance with Grittersova (Citation2014), who show that a good reputation of the parent company is the key mechanism supporting the financial stability of banks in developing economies. These foreign banks are also often viewed as lenders of last resort.

Moving on to state ownership, for medium and large enterprises, being owned by the state is a statistically nonsignificant factor, even after dividing countries into groups by quality of institutions. It is also nonsignificant for most sectors, with the exception of the primary sector, where it is very negative. The Czech Republic is a special case where state ownership (by the central government) is a strong and significantly negative variable, increasing the probability of firm failure. This is in accordance with Kočenda and Hanousek (Citation2012b), who show that state control is connected to lower firm performance in the Czech Republic. Small businesses, in general, are significantly negatively affected by state ownership in terms of firm survival, in fact much more than are larger companies. This holds true especially strongly for the construction sector, where state ownership increases the risk of failure by approximately 35%.

Unlike for firms, state ownership is a very important factor in improving the survival chances of banks. However, the results are ambiguous when taking into account other bank characteristics. State ownership is especially helpful for banks with low solvency. On the other hand, for financially strong banks, state ownership is a negative factor that increases the probability of bank failure.

The relationship between state ownership and bank survival might stem from the ability of state-controlled banks to practice soft budget constraints with state-controlled firms because such practices can be hidden due to multilevel ownership links among the firms and institutions under state control (Kočenda Citation1999; Hanousek and Kočenda Citation2008). Moreover, state-controlled firms may enjoy preferential treatment by the state, which can be considered an unofficial subsidy (Frydman et al. Citation2000). From the perspective of regional breakdown, state ownership is not statistically significant for banks in EU member countries. The last finding reflects the fact that, for example, in Russia, there is a high level of state control in banks (Chernykh Citation2008), whereas states are less involved in the banking sector in EU countries (Hanousek, Kočenda, and Ondko Citation2007; Bonin, Hasan, and Wachtel Citation2015)

Another factor in the category of ownership influencing the probability of firm survival is the number of large shareholders. Generally, it is a survival-enhancing factor with noticeable economic significance. This factor is not statistically significant in countries with low institutional quality. Moreover, this indicator is very dependent on the economic sector. For example, agriculture and construction do not appear to benefit from large shareholding in survival terms. Among service firms, however, the number of large shareholders is actually the single most important failure-preventing factor.

Large shareholding is a measure of dispersion of control. The results suggest that concentrated control is harmful for firm survival, which is in line with Hanousek, Kočenda, and Shamshur (Citation2015) in relation to general firm efficiency. This is in accordance with the so-called alignment hypothesis (e.g., Shleifer and Vishny Citation1986) and contradicts the expropriation hypothesis (Claessens, Djankov, and Lang Citation2000). The impact of large shareholding was not researched in relation to banks and small businesses.

Corporate Governance

Another factor with the ability to influence the survival probability of corporations is the number of board directors. In the case of medium and larger enterprises, larger boards of directors have a helpful effect of enhancing survival probability, although not uniformly. The effect is strong and significant for countries with high institutional quality but only mediocre in countries with mid- and low-quality institutions. On the other hand, the effect is very consistent across economic sectors

However, the boards can become excessively large, as evidenced by the estimation of the squared term of the number of board directors. In other words, very large boards prove to be a slightly negative factor increasing the risk of failure.

For banks, a higher number of board directors is also connected to improved survival probability, and the size of the effect is very meaningful, approximately 15%.

The U-shaped pattern of board size is again visible, shown by the squared term. Thus, not only firms but also banks suffer from overgrown boards. The U-shaped pattern is in accordance with De Andres and Vallelado (Citation2008), who find it in banks from developed countries.

Whether a firm has its audit done by an international audit firm also falls under the scope of corporate governance. Having an international firm doing the audit proves to be a failure-enhancing factor, with the strength of the effect being approximately 20%. Nevertheless, the results are not very consistent across countries and sectors. For countries with high and low institutional quality, the variable is positive and weakly significant, whereas for countries with moderate institutional quality, the indicator is very negative and strongly significant, which drives the aggregate effect.

This finding might be counterintuitive, as international audit firms are considered superior. That seems to be a faulty assumption, as the international auditing market in the Central and Eastern European countries is monopolized by the Big Four” (KPMG, Delloite, PwC and Ernst & Young). Lawrence, Minutti-Meza, and Zhang (Citation2011) show that the quality of international audits depends to a large degree on client characteristics.

Moreover, there might be another more practical explanation for this phenomenon. International auditors perform audits based on International Financial Reporting Standards (IFRS). These standards are very strict and demand to include a broader range of potential risks in the firm’s financial statements. As a result, firms are required to make additional reserves and provisions that may worsen the overall financial performance of the firms and thus increase the risk of failure.

Legal Form

The legal form of an enterprise may also significantly affect its survivability since each form bears differing rights and responsibilities and especially various upper limits to losses. The core papers estimated the effects of four legal forms – joint-stock company, limited liability company, partnership and cooperative – against the default “other legal form.” Limited liability companies emerged as the most survival-enhancing legal form, along with cooperatives. The joint-stock company form is also somewhat positive. These results are in line with previous research by Esteve-Pérez and Mañez-Castillejo (Citation2008), who find that limited liability companies survive longer than their unlimited counterparts. On the other hand, Harhoff, Stahl, and Woywode (Citation1998) find that limited liability companies have a higher insolvency rate than do those with full liability. Importantly, the legal form of joint-stock companies appears to be outright failure inducing in countries with low-quality institutions. No consistent results have been obtained for partnerships. Consequently, it appears that this variable is of lesser importance in determining the survivability of firms and is strongly context dependent.

For the legal form of the bank, both limited liability company and joint-stock company are much more beneficial in terms of survival probability compared to the default other legal forms, with limited liability company faring the best yet again. While the effect of being a limited liability company appears to be uniform across geographical regions, the joint-stock company form is significantly helpful only for banks in the most numerous group – Russia and Ukraine. The fact that the former Soviet Union countries benefit so much from the joint-stock company form likely reflects the historical developments in the region. After the fall of the USSR, the banking sector underwent mass privatization, in which the most important banks were transformed into joint-stock companies. Both joint-stock and limited liability companies are consistently helpful, even after dividing banks into groups based on solvency and ROA.

Linkage with Capital Market

Being listed is generally considered a failure-preventing factor, as firms directly connected to the stock market should have better ability to raise capital. The results are quite consistent for firms in our sample; however, they point in the opposite direction than expected. Being listed proves to be a significant failure-inducing factor for firms in emerging European economies, with the exception of countries with low-quality institutions, where it is a very positive and significant variable. Being listed is the most harmful for firms in services, but the negative effect is present in all sectors. The negative impact holds regardless the size and age of the firms and is largely invariant across time periods

These results highlight the enduring difference between developed stock markets in the West and the relatively young stock markets in the postcommunist states, which are the focus of this study. An earlier work by Johnson, Lopez-de-Silanes, and Shleifer (Citation2000) investigated practices such as asset stripping and expropriation, which were rampant during the period of transformation. Additionally, the recent global financial crisis inflicted serious damage on listed companies through capital crunches and, importantly, from unrealized losses on assets (Iwasaki Citation2014).

Even in more developed countries in the sample, which joined the EU in the big wave in 2004, stock markets have been established via mass privatization of state-owned companies during the fast transformation process at the outset of the reform process (Megginson and Netter Citation2001) and ended with a large number of listed companies lacking in liquidity (Bonin and Wachtel Citation2003; Baumöhl and Lyócsa Citation2014).

Being listed on a stock exchange is an ambiguous factor for banks. It is a statistically insignificant indicator for all country groups, with the exception of non-EU Eastern European countries, for which it is extremely positive and statistically significant. The latter result is in line with Mannasoo and Mayes (Citation2009), who note that listed banks in Eastern Europe are strongly and significantly less prone to distress than their unlisted counterparts, not least because the disclosure requirements that accompany being listed impose market discipline on them.

Size

The estimation fails to reveal any significant relationship between the survival chances of firms and their size. Larger firms face a greater risk of failure than their smaller counterparts, but the effect is negligible, albeit statistically significant. The results are also dependent on economic sector and geographic region. Size is also a negative factor for small businesses as a category. In other words, the larger among the small businesses (defined as firms with up to 50 employees) are at greater risk of failure than the very smallest businesses. However, this effect appears to be driven by former Soviet Union countries, precluding any reliable generalization.

These findings go against expectations, as the majority of earlier research points to positive effects of company size on survival. For example, Banerjee and Ćirjaković (Citation2021) find an L-shaped pattern in Slovenian firms, where size is a risk factor for only micro businesses, but after a very low threshold, it becomes irrelevant. Other examples include Cader and Leatherman (Citation2018), Ebert, Brenner, and Brixy (Citation2019), and Rico, Pandit, and Puig (Citation2020). There are various explanations for this relationship. Geroski, Mata, and Portugal (Citation2010) suggest that this might be due to larger firms having economies of scale and/or better access to financing. They also tend to be more diversified, which increases their resilience. However, the discrepancy might reflect the general immaturity of the markets in emerging European economies when compared to western states, which are typically the subject of survival studies. Moreover, indirect support might be found in Hanousek, Kočenda, and Shamshur (Citation2015), who show that larger EU firms tend to be less efficient, and in Kosová and Lafontaine (Citation2010), who present evidence that the probability of survival of a franchise decreases with increasing chain size.

Although size is considered beneficial even for banks, our estimation again finds a negative but negligible impact of size on banks’ survival chances. The result is yet again driven by Russia and Ukraine, as the effect is actually positive for sample countries that are EU members. The banking sector of Eastern Europe is still different from that of the West, and the historic legacy of those countries is very likely the culprit of the counterintuitive results. In particular, banks in Russia and Ukraine suffer from a larger proportion of low-quality assets, which might be the driver of these results (Brůha and Kocenda Citation2018). Additionally, large banks may consider themselves “too big to fail” and take for granted that they will be bailed out in case of failure. This presumed assurance makes them undertake unnecessary risk they would not have taken otherwise (moral hazard) (Kaufman Citation2014).

Age

The age of a firm is a factor that modestly reduces the risk of failure, that is, that older firms fare better than their younger counterparts, and this holds true for both small and large firms. The results are consistent for all geographic regions and all economic sectors, including subsections of services.

This result is intuitive and might reflect the fact that since firms have already survived for a relatively long time, they likely possess certain characteristics that make them resilient. These findings are also consistent with previous studies (Geroski Citation1995; Klepper and Thompson Citation2006).

The beneficial effect of age is confirmed for banks, where age is a factor that modestly reduces the risk of failure, even though not to such a degree as for firms. This result is consistent across all country groups and across divisions based on solvency and ROA.

Impact of Institutions and Financial Development

Institutional Quality

We now turn to an area that, unlike firm-level factors, has been largely neglected by the firm survival literature – institutional quality. As previously mentioned, there is an abundance of evidence linking the quality of institutions with the economic prosperity of countries (Acemoglu, Johnson, and Robinson Citation2001) or firm performance (Boudreaux and Nikolaev Citation2019). However, in relation to firm survival, the research is sparse in general, and for the region of emerging market economies, it is virtually nonexistent. Thus, this survey of recent research strives to fill this gap.

The core papers have used the following indicators as proxies for measurement of institutional quality: rule of law, democracy, national governance, civil society, corruption control, banking reform and enterprise reform. The research has been conducted for small businesses as well as medium and large enterprises.

National governance and corruption control prove to be the most beneficial of the seven individual indicators for medium and larger businesses. Small businesses benefit the most from the indicators democracy, national governance and civil society. Nonetheless, all measures of institutional quality are highly positively correlated with firm survival and statistically significant. Generally, a one-unit improvement in these indicators leads to a 10% to 30% increase in survival probability by between. This finding corroborates the expected positive linkage between the quality of institutions and the survival chances of firms.

Since all measures of institutional quality are highly correlated among themselves, principal component analysis (PCA) is conducted to ascertain the aggregate impact of institutional quality. The result of the PCA – a comprehensive institutional quality index – is used as a proxy instead of the individual institutional quality indicators. The new estimation shows that the comprehensive IQ index is again linked to increased survival probability, even though to a somewhat smaller degree than the specific indicators individually.

Importantly, institutional quality is a failure-reducing factor for all sectors of the economy. Nonetheless, clear primacy goes to the agricultural sector, where institutional quality has, by far, the largest impact on firm survival. This holds true for small, medium and large enterprises alike.

Dividing the sample into 3 country groups based on institutional quality reveals another very important point. Although the IQ index is a significant positive factor in all groups, firms located in countries with low institutional quality benefit the most from an improvement in their institutions. Conversely, countries with high IQ initially would see only a modest survival-enhancing effect after further improving their institutions. This is also true for small businesses, where the quality of institutions shows the highest benefit for former Soviet Union states, which have the lowest institutional quality from the researched region. Thus, as in many areas of economics, even the quality of institutions shows decreasing marginal returns.

This finding is crucial because it offers a possible explanation for why the literature relating the quality of institutions and firm survival is so sparse. Most of the research is focused on developed countries, which already enjoy relatively high-quality institutions. As such, institutions in those countries are probably not perceived as impacting the firms, and there is less qualitative variation across countries and regions (Che, Lu, and Tao Citation2017). Therefore, when conducting firm survival studies in developed states, they may not come to mind as a possible factor influencing firm survival as naturally as in emerging markets.

Additionally, as the quality of institutions is strongly correlated with membership in the EU, some might argue that the beneficial effect actually stems from EU membership. Such a benefit might, for example, be channeled through improved trade conditions brought about by free access to the EU market. Alternatively, failing firms in EU member states might enjoy more subsidization and state intervention that forestalls their failure. For this reason, both EU membership and the comprehensive IQ index have been included as controls in one model. When compared side by side, EU membership does not show statistically significant results, while the IQ index retains its significance.

In summary, all individual indicators, as well as the combined index of institutional quality, show a survival-enhancing effect for firms across all economic sectors and all country groups based on institutional quality. Firm size does not influence the results in any significant manner. Moreover, all estimations were performed on a very large sample. This extremely robust finding, which is also in line with the literature from other regions, allows for a confident causal inference.

The specific channels through which inadequate institutions might add to firm failure are arguably the same as those that diminish firm performance and economic growth in general. The most prominent is probably the protection of property rights. Che, Lu, and Tao (Citation2017) show that inadequate protection of property rights and expropriation from institutions is harmful to nonstate-owned enterprises in China. Besley and Ghatak (Citation2009) also stress the importance of property rights and show many angles from which their violation may lead to poor economic performance. Additional evidence is provided by North (Citation1990) and Acemoglu, Johnson, and Robinson (Citation2001).

Another well-documented phenomenon is the extent of corruption and its consequences. Doh et al. (Citation2003) list various direct and indirect costs connected with institutional corruption, including bribes, red tape and resources spent as a result of extortion. Moreover, firms may have to bear additional costs for protection against organized crime if the country’s institutions are not able or willing to address it. Moreover, according to North (Citation1993), institutions facilitate efficient transactions between firms and individuals. The core papers did not test the specific transmission channels that lead to the survival enhancing effect. However, there is no indication that those channels should be different in emerging European economies than in the evidence presented above.

Financial Development

The previous subsection presents evidence that institutions associated with a functioning lawful and democratic state are important factors for creating an environment where firms can enjoy a lower risk of failure. This subsection provides an overview of the survival-related impact of the second set of indicators – measures of financial development that are a trademark of modern market economies. The investigation of the impact of financial development on firm survival in emerging European economies has been conducted only for small businesses and banks. However, there is no reason to expect wildly differing results for larger firms.

In this subsection, the analysis starts with the unequivocal case of a financial development (FD) index. Again, a comprehensive (FD) index is created via principal component analysis (for both banks and SMEs separately). The estimation shows that the financial development index is, in both cases, a statistically significant positive factor with a strength close to that of the comprehensive IQ index. The FD index is a positive and significant factor in all geographic regions for banks and firms alike. For banks specifically, the effect is the strongest in Russia and Ukraine, which are considered less financially developed than the EU countries. (Fan, Wei, and Xu Citation2011; Bonin, Hasan, and Wachtel Citation2015). Thus, it is again reasonable to assert that even for banks, there are decreasing marginal returns to be obtained from improvement in the financial development of their domicile countries. In SMEs, this trend is missing. Moreover, the survival of financially weaker banks (especially those with low ROA) depends more on the financial development of their countries than does the survival of sounder banks. Smaller banks are also more reliant on the financial environment are than larger banks. The effect remains strong and significant across all economic sectors.

In regard to specific financial indicators, the literature is more ambiguous. On a theoretical level, the main contention is about the effects of bank intermediation on one hand and financial (mainly stock) market development on the other. Levine (Citation1991) suggests that market-based economies are better at allocating resources to projects with higher returns and thus facilitate more productive long-term investments. Hermes and Lensink (Citation2000) assert that market-based economies are better at reducing asymmetric information. Similarly, according to Tsoukas (Citation2011), firms are better able to hedge, pool risk and access alternative sources of financing in economies with more developed stock markets. Nonetheless, there are also voices critical of stock markets. Singh (Citation1997), for example, criticizes the overly favorable view of stock markets, claiming that managers of joint-stock companies are rewarded for financial engineering rather than genuine wealth creation. He also asserts that stock markets lead to short-termism and less long-term investment, especially in firm-specific capital.

Unlike institutional quality, where all individual indicators are positive, the estimation results of the effect of financial development measures are more varied and they reflect the ambiguity of the theoretical literature. In the case of small businesses, five measures have been used: liquid liabilities, private credit, bank assets, market capitalization and stock trading volume.

Liquid liabilities, private credit and bank assets prove to be positive factors increasing the survival chances of small businesses. Their survival-enhancing effect ranges from 10% to 23%, the highest being achieved by liquid liabilities. These measures roughly represent banking intermediation.

In contrast, the stock market indicators – market capitalization and stock trading volume – are negative factors increasing the risk of failure of small businesses. Notably, in this specific case, there might be a substantial difference between small businesses and larger firms. It can be hypothesized that in economies with a higher proportion of large listed companies, there is less room for small business.

These results contradict the empirical findings of Tsoukas (Citation2011), who find that the development of banking intermediation increases the risk of failure of Asian firms due to more bank-dependent firm management. However, when the sample is divided into market-based and bank-centered countries, a more complicated pattern emerges. Stock market development is a survival-enhancing factor only for market-based countries, whereas it is nonsignificant for the latter. Conversely, increased bank intermediation is a problematic factor only for firms in bank-centered countries, presumably because they have a hard time accessing other sources of financing. Nonetheless, supportive evidence can also be found, e.g., by Bukvič and Bartlett (Citation2003), who show that difficulties with obtaining credit are one of the important setbacks for Slovenian SMEs. Presumably, then, an increase in bank credit should alleviate this problem. Moreover, Mc Namara, Murro, and O’Donohoe (Citation2017) argue that in the strongly bank-based European financial system, the reliance on banks underscores the importance of the state’s lending infrastructure for SMEs.

Similar measures of financial development have been used for banks: liquid liabilities, private credit, bank credit and banking reform. All these measures show a strong positive and statistically significant effect, with the indicator “banking reform” being by far the most beneficial one. A unit change in banking reform level is associated with a 42% increase in survival probability.

The literature supports the positive effects of these aggregate measures of bank and financial sector development on the survival probabilities of banks in both developed and emerging countries, e.g., DeYoung (Citation2003), Cebula (Citation2010) and Lin and Yang (Citation2016).

As already mentioned, the literature is somewhat ambiguous in regard to financial development. There appears to be a consensus about the benefits of general financial development, but there is a rift between proponents of more bank-centered and stock market-based systems of financing. However, the specific effects of financial market development seem to be very context dependent. Stock markets in the emerging European economies are still relatively young and do not meet the standards of their Western counterparts in terms of information processing and as alternative sources of financing. As such, the critique of Singh (Citation1997) probably holds truer for the region compared to the developed countries. Thus, it is reasonable to assume that the relationship between stock market indicators and firm survival is nonlinear and that the potential benefits of financial development can be reaped only after a certain level of maturation of the system. Additionally, the estimation was conducted for smaller firms, which are less likely to reap the benefits of stock markets. For example, the beneficial effects in Tsoukas (Citation2011) are statistically significant only for larger firms.

Time-varying Impact of Individual Factors

The dynamic impact of most factors in the surveyed literature is largely time invariant. Financial performance indicators proved to be by far the most stable variables in terms of their impact on survival. However, some factors change the magnitude of their effect with time. We now summarize those cases. The most important variation is that for firms of all sizes, the institutional quality and financial development of the countries of origin lost the beneficial effect (and statistical significance) during the global financial crisis, and for banks, financial development was outright harmful. The reason for this is quite straightforward. The financial crisis that originated in the USA spilled over to the rest of the world. In general, the more financially and institutionally developed countries were also more interconnected with the Western financial system and/or had a stronger trade balance with Western states and thus were more strongly impacted by the spillover.

However, it is important to note the very positive effect of the financial development of banks during the European sovereign debt crisis. This is in line with broader literature showing the negative impact of the European sovereign debt crisis on European banks’ equity returns (Allegret, Raymond, and Rharrabti Citation2017), their assets due to holding sovereign debt (Gennaioli, Martin, and Rossi Citation2018), or the connection between sovereign risk and the quality of the banking sector in general (Brůha and Kocenda Citation2018).

The survival-enhancing effect of both larger boards of directors and a higher number of large shareholders diminished over time for firms and banks alike. It is plausible that corporate governance and consolidation of control played a more significant role during the global financial crisis, as both factors influenced decision-making. The issue might be even more critical during times when failure is more likely due to external factors.

For small businesses, state ownership lost the initially positive effect and became progressively more harmful as time went on. Similarly, foreign ownership was also most helpful for small businesses during the global financial crisis, and the effect somewhat weakened in the later periods. Alfaro and Chen (Citation2012) also document the weakening of the effect post GFC. However, unlike state ownership, foreign ownership remained a very strong and positive factor throughout all time periods.

Concluding Remarks

In this paper, we review the recent research on the linkage between institutional quality and financial development in the emerging European economies and firm survival in those states. Altogether, over 100000 firms and banks from 17 countries observed between 2006 and 2017 entered the research. For the survival analysis, we used the Cox proportional hazards model, which is considered the gold standard in survival analysis. Many firm-level controls were also used.

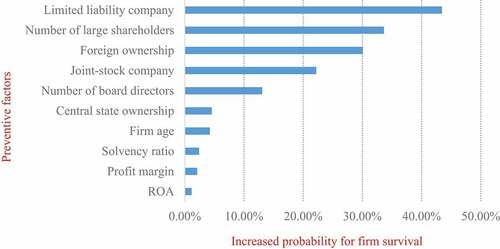

Although the effect of selected firm-specific covariates might differ according to the various model setups and across different samples, some generalized conclusions can be drawn. captures the mean values of estimated hazard ratios for those variables included in all five core papers, averaged throughout their main baseline estimation results. Of course, this approach smears out some noticeable differences, such as the results for different industries, different time periods, and/or for larger/smaller and older/younger firms. However, we have covered these specific estimates above. Here, we provide an overview of the most important preventive factors.

Figure 2. Average impact of selected covariates.

On average, with respect to the firm-specific variables, the three most important preventive factors for firm survival in European emerging markets are the legal form of a limited liability company, the number of large shareholders, and foreign ownership.

Most firm-level variables show the expected effect, at least in direction, if not in magnitude. One notable exception is the linkage with the capital market. This factor is largely considered positive, but our estimation shows opposite results for emerging European economies. This might reflect the specificity of the region. The capital markets are relatively young and have not grown organically but have been created by mass and hasty privatization after the fall of communist regimes, which for approximately 40 years imposed vastly different economic systems on those countries. Moreover, a crucial event that occurred during our estimation period was the global financial crisis, which hit listed companies especially hard through credit crunches and unrealized losses on assets. Another variable with the opposite influence than expected is international audit, which was also a failure-inducing factor. However, the international auditor market in this region is monopolized by the “big four,” and criticism has already been levied by other authors on the quality of such auditing.

The evidence speaks quite unambiguously in the case of institutional quality. All the indicators – rule of law, democracy, national governance, civil society, corruption control, enterprise reform and bank reform – show a positive relationship with firm survival. The first component obtained by principal component analysis confirms this. The results are more complicated for financial development. While the indicators liquid liabilities, private credit and bank credit also show a positive correlation with firm survival, higher market capitalization and stock trading volume have a negative influence on survival rates. This might be because a more developed stock market is associated with tougher competition, which many, especially smaller, firms have trouble facing.

An important thread running through the research is the observation of diminishing marginal returns in institutional quality and financial development. This means that firms located in countries where the quality of institutions is lowest would benefit most from improvements in their institutions. These results can therefore serve as policy recommendations for the countries in the sample.

Acknowledgement

We would like to thank Tomáš Výrost, an anonymous referee, and presentation participants for their constructive comments that helped us to improve our work, and to Martin Slaba for his research assistance. We acknowledge research support from the Slovak Research and Development Agency (Contract No. APVV-18-0310) and the Scientific Grant Agency (VEGA project No. 1/0182/20). The authors report that there are no competing interests to declare. The usual disclaimer applies.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Eduard Baumöhl

Eduard Baumöhl is an associate professor at the Faculty of Commerce, University of Economics in Bratislava, an associate professor at the Faculty of Economics, Technical University of Košice (Slovakia), and an associate professor at the Department of Finance, Faculty of Economics and Administration, Masaryk University (Czechia). His research topics include financial markets, stock market integration, financial contagion, networks, financial econometrics and corporate finance.

Evžen Kočenda

Evžen Kočenda is Full Professor, Head of Department of Finance, and Director of Doctoral Studies at the Institute of Economic Studies, Charles University in Prague. His fields of interest include applied economics and econometrics, international money and finance, transition and European integration, corporate performance and governance, and nonlinear procedures.

Notes

1. For future research, it might be beneficial to comprehensively investigate the relationship between the pandemic crisis and firms’ failure. The global spread of COVID-19 became a new component linked to firms’ external environment (Stef and Bissieux Citation2022) along with pandemic-related non-pharmaceutical interventions imposed in form of the policy responses to mitigate the health crisis.

References

- Acemoglu, D., S. Johnson, and J. A. Robinson. 2001. “The Colonial Origins of Comparative Development: An Empirical Investigation.” American Economic Review 91 (5): 1369–401. 10.1257/aer.91.5.1369.

- Acemoglu, D., S Johnson, and J. A. Robinson. 2005. “Institutions as the Fundamental Cause of Long – Run Growth. ” In Handbook of Economic Growth. Elsevier Press, P. Aghion and S. Durlauf edited by, North Holland: Elsevier Press. 385–472. 10.1016/S1574-0684(05). https://www.sciencedirect.com/science/article/abs/pii/S1574068405010063

- Acs, Z., and L. Szerb. 2007. “Entrepreneurship, Economic Growth and Public Policy.” Small Business Economics 28 (2–3): 109–22. doi:10.1007/s11187-006-9012-3.

- Acs, Z., S. Desai, and J. Hessels. 2008. “Entrepreneurship, Economic Development and Institutions.” Small Business Economics 31 (3): 219–34. doi:10.1007/s11187-008-9135-9.

- Agarwal, R., and M. Gort. 2002. “Firm and Product Life Cycles and Firm Survival.” American Economic Review 92 (2): 184–90. doi:10.1257/000282802320189221.

- Alfaro, L., and M. X. Chen. 2012. “Surviving the Global Financial Crisis: Foreign Ownership and Establishment Performance.” American Economic Journal: Economic Policy 4 (3): 30–55. doi:10.1257/pol.4.3.30.

- Allegret, J. P., H. Raymond, and H. Rharrabti. 2017. “The Impact of the European Sovereign Debt Crisis on Banks Stocks.” Some Evidence of Shift Contagion in Europe. Journal of Banking and Finance 74,24–37. doi:10.1016/j.jbankfin.2016.10.004.

- Aussenegg, W., and R. Jelic. 2007. “The Operating Performance of Newly Privatised Firms in Central European Transition Economies.” European Financial Management 13 (5): 853–79. doi:10.1111/j.1468-036X.2007.00400.x.

- Banerjee, B., and J. Ćirjaković. 2021. “Firm Indebtedness, Deleveraging, and Exit: The Experience of Slovenia during the Financial Crisis, 2008–2014*.” Eastern European Economics 59 (6): 537–70. doi:10.1080/00128775.2021.1966310.

- Baumohl, E., I. Iwasaki, and E. Kočenda. 2019. “Institutions and Determinants of Firm Survival in European Emerging Markets.” Journal of Corporate Finance 58:431–53. doi: 10.1016/j.jcorpfin.2019.05.008

- Baumohl, E., I. Iwasaki, and E. Kočenda. 2020. “Firm Survival in New EU Member States.” Economic Systems 44 (1): 100743. doi:10.1016/j.ecosys.2020.100743.

- Baumöhl, E., and S. Lyócsa, (2014). How Smooth Is the Stock Market Integration of CEE-3? William Davidson Institute Working Papers Series, WP no. 1079. University of Michigan, https://deepblue.lib.umich.edu/bitstream/handle/2027.42/132978/wp1079.pdf?sequence=1

- Besley, T., and M. Ghatak. 2009. “Property Rights and Economic Development.” In Handbook of Development Economics, D. Rodrik and M. Rosenzweig edited by, vol. 5, 4525–95. Amsterdam: North Holland Press. doi:10.1016/B978-0-444-52944-2.00006-9.

- Bonin, J., and P. Wachtel. 2003. “Financial Sector Development in Transition Economies: Lessons from the First Decade. Financial Markets.” Institutions and Instruments 12 (1): 1–66. doi:10.1111/1468-0416.t01-1-00001

- Bonin, J. P., I. Hasan, and P. Wachtel. 2015. “Banking in Transition Countries.” In The Oxford Handbook of Banking, 2nd, Oxford: Oxford University Press. 963–83. 10.1093/oxfordhb/9780199688500.013.0039

- Boudreaux, C. J., and B. Nikolaev. 2019. “Capital Is Not Enough: Opportunity Entrepreneurship and Formal Institutions.” Small Business Economics 53 (3): 709–38. doi:10.1007/s11187-018-0068-7.

- Brůha, J., and E. Kocenda. 2018. “Financial Stability in Europe: Banking and Sovereign Risk.” Journal of Financial Stability 36:305–21. doi: 10.1016/j.jfs.2018.03.001

- Brůha, J, and E Kočenda. 2018. ”Financial Stability in Europe: Banking and Sovereign Risk.” Journal of Financial Stability 36:305–21.

- Bukvič, V., and W. J. Bartlett. 2003. “Financial Barriers to SME Growth in Slovenia.” Economic and Business Review 5 (3): 161–81. http://miha.ef.uni-lj.si/ebr/abstract.asp?ID=71.

- Calomiris, C. W., and J. R. Mason. 2003. “Fundamentals, Panics, and Bank Distress during the Depression.” American Economic Review 93 (5): 1615–47. doi:10.1257/000282803322655473.

- Carmona, P., F. Climent, and A. Momparler. 2019. “Predicting Failure in the US Banking Sector: An Extreme Gradient Boosting Approach.” International Review of Economics and Finance 61:304–23. doi: 10.1016/j.iref.2018.03.008

- Cebula, R. J. 2010. “Determinants of Bank Failures in the US Revisited.” Applied Economics Letters 17(13-15) (13): 1313–17. doi:10.1080/00036840902881884.

- Ch, Franco, and J. P. W. Gelübcke. 2015. “The Death of German Firms: What Role for Foreign Direct Investment?” The World Economy 38 (4): 677–703. doi:10.1111/twec.12227.

- Che, Y., Y. Lu, and Z. Tao. 2017. “Institutional Quality and New Firm Survival.” Economics of Transition 25 (3): 495–525. doi:10.1111/ecot.12119.

- Chernykh, L. 2008. “Ultimate Ownership and Control in Russia.” Journal of Financial Economics 88 (1): 169–92. doi:10.1016/j.jfineco.2007.05.005.

- Chiaramonte, L., and B. Casu. 2017. “Capital and Liquidity Ratios and Financial Distress: Evidence from the European Banking Industry.” The British Accounting Review 49 (2): 138–61. doi:10.1016/j.bar.2016.04.001.

- Claessens, S., S. Djankov, and L. H. P. Lang. 2000. “The Separation of Ownership and Control in East Asian Corporations.” Journal of Financial Economics 58 (1/2): 81–112. doi:10.1016/S0304-405X(00).

- Cole, R. A., and L. J. White. 2012. “Déjà Vu All over Again: The Causes of US Commercial Bank Failures This Time around.” Journal of Financial Services Research 42 (1–2): 5–29. doi:10.1007/s10693-011-0116-9.

- Cox, D. R. 1972. “Regression Models and Life-Tables. Journal of the Royal Statistical Society.” Series B 34 (2): 187–220. doi:10.1111/j.2517-6161.1972.tb00899.x.

- De Andres, P., and E. Vallelado. 2008. “Corporate Governance in Banking: The Role of the Board of Directors.” Journal of Banking and Finance 32 (12): 2570–80. doi:10.1016/j.jbankfin.2008.05.008.

- Desai, M. A., P. A. Gompers, and J. Lerner (2005). Institutions, Capital Constraints and Entrepreneurial Firm Dynamics: Evidence from Europe. NBER Working Paper Series, June 2005, 10.3386/w10165

- DeYoung, R. 2003. “De Novo Bank Exit.” Journal of Money, Credit, and Banking 35 (5): 711–28. doi:10.1353/mcb.2003.0036.

- Doh, J. P., P. Rodriguez, K. Uhlenbruck, J. Collins, and L. Eden. 2003. “Coping with Corruption in Foreign Markets.” Academy of Management Executive 17:114–27. doi: 10.5465/ame.2003.10954775

- Ebert, T., T. Brenner, and U. Brixy. 2019. “New Firm Survival: The Interdependence between Regional Externalities and Innovativeness.” Small Business Economics 53 (1): 287–309. doi:10.1007/s11187-018-0026-4.

- Eicher, T. S., and C. García-Peñalosa. 2006. Institutions, Development, and Economic Growth. Cambridge, MA: The MIT Press.

- Esteve-Pérez, S., A. Sanchis Llopis, and J. A. Sanchis Llopis. 2004. “The Determinants of Survival of Spanish Manufacturing Firms.” Review of Industrial Organization 25 (3): 251–73. doi:10.1007/s11151-004-1972-3.

- Esteve-Pérez, S., and J. A. Mañez-Castillejo. 2008. “The resource-based Theory of the Firm and Firm Survival.” Small Business Economics 30 (3): 231–49. doi:10.1007/s11187-006-9011-4.

- Estrin, S., J. Hanousek, E. Kočenda, and J. Svejnar. 2009. “Effects of Privatization and Ownership in Transition Economies.” Journal of Economic Literature 47 (3): 699–728. doi:10.1257/jel.47.3.699.

- Fagerberg, J., and M. Srholec. 2008. “National Innovation Systems, Capabilities and Economic Development.” Research Policy 37 (9): 1417–35. doi:10.1016/j.respol.2008.06.003.

- Fan, J. P. H., K. C. J. Wei, and X. Xu. 2011. “Corporate Finance and Governance in Emerging Markets: A Selective Review and an Agenda for Future Research.” Journal of Corporate Finance 17 (2): 207–14. doi:10.1016/j.jcorpfin.2010.12.001.

- Farinha, L., M.-E. Spaliara, and S. Tsoukas. 2019. “Bank Shocks and Firm Performance: New Evidence from the Sovereign Debt Crisis.” Journal of Financial Intermediation 40 (Article): 100818. doi:10.1016/j.jfi.2019.01.005.

- Faruq, H. A., and M. L. Weidner. 2018. “Culture, Institutions, and Firm Performance.” Eastern Economic Journal 44 (4): 519–34. doi:10.1016/j.jcorpfin.2010.12.001.

- Frydman, R., C. Gray, M. Hessel, and A. Rapaczynski. 2000. “The Limits of Discipline: And Hard Budget Constraints in the Transition Economies.” The Economics of Transition 8 (3): 577–601. doi:10.1111/1468-0351.00056.

- Gagliardi, F. 2009. “Financial Development and the Growth of Cooperative Firms.” Small Business Economics 32 (2): 439–64. doi:10.1007/s11187-007-9080-z.

- Galbreath, J, and P Galvin. 2008. “Firm Factors, Industry Structure and Performance Variation: New Empirical Evidence to a Classic Debate.” Journal of Business Research 61 (2): 109–17. doi:10.1016/j.jbusres.2007.06.009.

- Gennaioli, N., A. Martin, and S. Rossi. 2018. “Banks, Government Bonds, and Default.” What Do the Data Say? Journal of Monetary Economics 98:98–113. doi: 10.1016/j.jmoneco.2018.04.011

- Gerlach, H. ”Bankruptcy in the Czech Republic, Hungary, and Poland and Section 304 of the United States Bankruptcy Code, Proceedings Ancillary to Foreign Bankruptcy Proceedings.” Md. J. Int'l L. & Trade 22 (1998): 81

- Geroski, P. A. 1995. “What Do We Know about Entry?” International Journal of Industrial Organization 13 (4): 421–40. doi:10.1016/0167-7187(95).

- Geroski, P. A., J. Mata, and P. Portugal. 2010. “Founding Conditions and the Survival of New Firms.” Strategic Management Journal 31 (5): 510–29. doi:10.1002/smj.823.

- Ghoul, S., O. Guedhami, and Y. Kim. 2017. “Country-level Institutions, Firm Value, and the Role of Corporate Social Responsibility Initiatives.” Journal of International Business Studies 48 (3): 360–85. doi:10.1057/jibs.2016.4.

- Görg, H., and M. E. Spaliara. 2014. “Financial Health, Exports and Firm Survival: Evidence from UK and French Firms.” Economica 81 (323): 419–44. doi:10.1111/ecca.12080.

- Görg, H, and M-E. Spaliara. 2014. ”Financial Health, Exports and Firm Survival: Evidence from UK and French Firms.” Economica 81 (323): 419–44. doi:10.1111/ecca.12080.

- Grittersova, J. 2014. “Transfer of Reputation: Multinational Banks and Perceived Creditworthiness of Transition Countries.” Review of International Political Economy 21 (4): 878–912. doi:10.1080/09692290.2013.848373.

- Guariglia, A., M. E. Spaliara, and S. Tsoukas. 2016. “To What Extent Does the Interest Burden Affect Firm Survival? Evidence from a Panel of UK Firms during the Recent Financial Crisis.” Oxford Bulletin of Economics and Statistics 78 (4): 576–94. doi:10.1111/obes.12120.

- Hall, R., and C. I. Jones. 1999. “Why Do Some Countries Produce so Much More Output per Worker than Others?” Quarterly Journal of Economics 114 (1): 83–116. doi:10.1162/003355399555954.

- Hanousek, J., E. Kočenda, and P. Ondko. 2007. “The Banking Sector in New EU Member Countries: A Sectoral, Financial Flows Analysis.” Czech Journal of Economics and Finance 57 (5–6): 200–24. https://www.scopus.com/record/display.uri?eid=2-s2.0-34548082211&origin=inward.

- Hanousek, J., and E. Kočenda. 2008. “Potential of the State to Control Privatized Firms.” Economic Change and Restructuring 41 (2): 167–86. doi:10.1007/s10644-008-9047-3.

- Hanousek, J., E. Kočenda, and A. Shamshur. 2015. “Corporate Efficiency in Europe.” Journal of Corporate Finance 32:24–40. doi: 10.1016/j.jcorpfin.2015.03.003

- Harhoff, D., K Stahl, and M Woywode. 1998. “Legal Form, Growth and Exit of West German Firms –empirical Results for Manufacturing, Construction, Trade and Service Industries. J.” Journal of Industrial Economics 46 (4): 453–88. doi:10.1111/1467-6451.00083.

- Hasan, I., P. Wachtel, and M. Zhou. 2009. “Institutional Development, Financial Deepening and Economic Growth: Evidence from China.” Journal of Banking and Finance 33 (1): 157–70. doi:10.1016/j.jbankfin.2007.11.016.

- Hermes, N., and R. Lensink. 2000. “Financial System Development in Transition Economies.” Journal of Banking and Finance 4 (4): 507–24. doi:10.1016/S0378-4266(99)00078-3.

- Hong, H., J. Z. Huang, and D. Wu. 2014. “The Information Content of Basel III Liquidity Risk Measures.” Journal of Financial Stability 15:91–111. doi: 10.1016/j.jfs.2014.09.003

- Hwang, D. Y., C. F. Lee, and K. T. Liaw. 1997. “Forecasting Bank Failures and Deposit Insurance Premium.” International Review of Economics and Finance 6 (3): 317–34. doi:10.1016/S1059-0560(97).

- Iwasaki, I. 2014. “Global Financial Crisis, Corporate Governance, and Firm Survival: The Russian Experience.” Journal of Comparative Economics 42 (1): 178–211. doi:10.1016/j.jce.2013.03.015.

- Iwasaki, I., and E. Kočenda. 2020. “Survival of Service Firms in European Emerging Economies.” Applied Economics Letters 27 (4): 340–48. doi:10.1080/13504851.2019.1616053.

- Iwasaki, I., E. Kočenda, and Y. Shida. 2022. “Institutions, Financial Development, and Small Business Survival: Evidence from European Emerging Markets.” Small Business Economics 58 (3): 1261–83. doi:10.1007/s11187-021-00470-z.

- Johnson, S., R. Lopez-de-Silanes, and F. Shleifer. 2000. “Tunneling.” American Economic Review 90 (2): 22–27. doi:10.1257/aer.90.2.22.

- Johnson, S., J. McMillan, and C. Woodruff. 2002. “Property Rights and Finance.” American Economic Review 92 (5): 1335–56. doi:10.1257/000282802762024539.

- Kaufman, G. G. 2014. “Too Big to Fail in Banking.” What Does It Mean? Journal of Financial Stability 13:214–23. doi: 10.1016/j.jfs.2014.02.004

- Klepper, S., and P. Thompson. 2006. “Submarkets and the Evolution of Market Structure.” The RAND Journal of Economics 37 (4): 861–86. doi:10.1111/j.1756-2171.2006.tb00061.x.

- Kočenda, E. 1999. “Residual State Property in the Czech Republic.” Eastern European Economics 37 (5): 6–35. doi:10.1080/00128775.1999.11648698.

- Kočenda, E., and J. Hanousek. 2012a. “Firm break-up and Performance.” Economics of Governance 13 (2): 121–43. doi:10.1007/s10101-011-0106-2.

- Kočenda, E., and J. Hanousek. 2012b. “State Ownership and Control in the Czech Republic.” Economic Change and Restructuring 45 (3): 157–91. doi:10.1007/s10644-011-9114-z.

- Kočenda, E., and I. Iwasaki. 2020. “Bank Survival in Central and Eastern Europe.” International Review of Economics and Finance 69:860–78. doi: 10.1016/j.iref.2020.06.020

- Kočenda, E., and K. Poghosyan. 2020. “Nowcasting Real GDP Growth: Comparison between Old and New EU Countries.” Eastern European Economics 58 (3): 197–220. doi:10.1080/00128775.2020.1726185.

- Kosová, R., and F. Lafontaine. 2010. “Survival and Growth in Retail and Service Industries: Evidence from Franchised Chains.” Journal of Industrial Economics 58 (3): 542–78. doi:10.1111/j.1467-6451.2010.00431.x.

- Lawrence, A., M. Minutti-Meza, and P. Zhang. 2011. “Can Big 4 versus non-Big 4 Differences in audit-quality Proxies Be Attributed to Client Characteristics?” The Accounting Review 86 (1): 259–86. doi:10.2308/accr.00000009.

- Levine, R. 1991. “Stock Markets Growth and Tax Policy.” Journal of Finance 46 (4): 1445–65. doi:10.1111/j.1540-6261.1991.tb04625.x.

- Lin, C.-C., and S.-L. Yang. 2016. “Bank Fundamentals, Economic Conditions, and Bank Failures in East Asian Countries.” Economic Modelling 52(B):960–66. doi: 10.1016/j.econmod.2015.10.035

- Lin, Ch-Ch., and S-L. Yang. 2016. ”Bank Fundamentals, Economic Conditions, and Bank Failures in East Asian Countries.” Economic Modelling 52:960–66.

- LiPuma, J. A., S. L. Newbert, and J. P. Doh. 2013. “The Effect of Institutional Quality on Firm Export Performance in Emerging Markets: A Contingency Model of Firm Age and Size.” Small Business Economics 40 (4): 817–41. doi:10.1007/s11187-011-9395-7.

- Liu, X. 2012. ”Survival Analysis: Models and Applications”. Chichester: John Wiley & Sons.

- Manjón-Antolín, M. C., and J. M. Arauzo-Carod. 2008. “Firm Survival: Methods and Evidence.” Empirica 35 (1): 1–24. doi:10.1007/s10663-007-9048-x.

- Mannasoo, K., and D. G. Mayes. 2009. “Explaining Bank Distress in Eastern European Transition Economies.” Journal of Banking and Finance 33 (2): 244–53. doi:10.1016/j.jbankfin.2008.07.016.

- Mata, J., and P. Portugal. 2002. “The Survival of New Domestic and Foreign Owned Firms.” Strategic Management Journal 23 (4): 323–43. doi:10.1002/smj.217.

- Mata, J., and P. Portugal. 2004. “Patterns of Entry, post-entry Growth and Survival: A Comparison between Domestic and Foreign Owned Firms.” Small Business Economics 22 (3–4): 283–98. doi:10.1023/B:SBEJ.0000022219.25772.ca.

- Mc Namara, A., P. Murro, and S. O’Donohoe. 2017. “Countries Lending Infrastructure and Capital Structure Determination: The Case of European SMEs.” Journal of Corporate Finance 43:122–38. doi: 10.1016/j.jcorpfin.2016.12.008

- Megginson, W.L, and J.M Netter. 2001. “From State to Market: A Survey of Empirical Studies on Privatization. J.” Journal of Economic Literature 39 (2): 321–89. doi:10.1257/jel.39.2.321.

- Musso, P., and S. Schiavo. 2008. “The Impact of Financial Constraints on Firm Survival and Growth.” Journal of Evolutionary Economics 18 (2): 135–49. doi:10.1007/s00191-007-0087-z.

- North, D. C. 1990. Institutions, Institutional Change and Economic Performance. Cambridge: Cambridge University Press. doi:10.1257/jep.5.1.97.

- North, D. C. 1993. “Institutions and Credible Commitment.” Journal of Institutional and Theoretical Economics 149 (1): 11–23. https://www.jstor.org/stable/40751576.

- Porter, M. E. 1998. “Clusters and the New Economics of Competition.” Harvard Business Review 76 (6): 77–90.

- Rico, M., N. R. Pandit, and F. Puig. 2020. “SME Insolvency, Bankruptcy, and Survival: An Examination of Retrenchment Strategies.” Small Business Economics 57 (1): 111–26. doi:10.1007/s11187-019-00293-z.

- Schäfer, D., and O. Talavera. 2009. “Small Business Survival and Inheritance: Evidence from Germany.” Small Business Economics 32 (1): 95–109. doi:10.1007/s11187-007-9069-7.

- Shleifer, A., and R. W. Vishny. 1986. “Large Shareholders and Corporate Control.” Journal of Political Economy 94 (3): 461–88. doi:10.1086/261385.

- Singh, A. 1997. “Financial Liberalisation, Stockmarkets and Economic Development.” Economic Jounal 107:771–82. doi: 10.1111/j.1468-0297.1997.tb00042.x

- Soriano, D.R. 2010. “Management Factors Affecting the Performance of Technology Firms.” Journal of Business Research 63 (5): 463–70. doi:10.1016/j.jbusres.2009.04.003.

- Stef, N., and J. J. Bissieux. 2022. “Resolution of Corporate Insolvency during COVID-19 Pandemic.” Evidence from France. International Review of Law and Economics 70:106063. doi: 10.1016/j.irle.2022.106063

- Taymaz, E., and S. Özler. 2007. “Foreign Ownership, Competition, and Survival Dynamics.” Review of Industrial Organization 31 (1): 23–42. doi:10.1007/s11151-007-9144-x.

- Tsoukas, S. 2011. “Firm Survival and Financial Development: Evidence from a Panel of Emerging Asian Economies.” Journal of Banking and Finance 35 (7): 1736–52. doi:10.1016/j.jbankfin.2010.12.008.