ABSTRACT

Britain’s older industrial towns have long been known to face economic problems. However, in the aftermath of the recession triggered by the 2008 financial crisis, recorded unemployment in the towns has fallen to relatively low levels. This paper deploys labour market accounts to measure the contributions of changing levels of employment, population, national and international migration, commuting, and labour market participation to the pattern of change in the towns in the period 2010–16. It also places older industrial towns in their regional context by comparing recent trends in the towns with those in the main regional cities, London and the UK as a whole. The paper concludes that the reduction in recorded unemployment since 2010 paints an overly positive picture of labour market trends in Britain’s older industrial towns.

INTRODUCTION

The recession triggered by the 2008 financial crisis was a profound shock to the global economy, but nearly a decade on it can seem like history. Economic growth returned after a couple of years, and while growth has been unspectacular in most countries, pre-recession levels of output have nearly everywhere been overtaken and unemployment has fallen. In the UK, the focus of the present paper, the growth in productivity has been unusually slow and real wages have fallen, but recorded unemployment is well down on peak levels during the recession.

However, in the UK and elsewhere, the recession and subsequent recovery were overlain on pre-existing regional and local differences in prosperity. The trajectory of Britain’s older industrial towns is of particular interest. They have a long history of economic problems, rooted in the decline of the mining and manufacturing industries that underpinned their original growth, and they entered the 2008 recession with fragile economies, lagging behind the prosperity of London and its hinterland. Recent trends in these towns is an unexplored area, with the commentary having so far progressed little beyond the observation that unemployment has fallen. There has also been little attempt so far to place the trends in older industrial towns within their wider regional context, which is especially important now that labour markets in a physically small country such as the UK spill over from one place to another as a result of large commuting and migration flows. Yet, the economic trajectory of older industrial towns has the potential to shed a light on whether job loss is ultimately self-correcting, through market mechanisms and a modicum of public intervention, or whether it triggers ongoing cycles of local economic decline.

The answer to this question probably matters more than ever because there is clear evidence of a political backlash in Britain and elsewhere from ‘the places that don’t matter’ (Rodriguez-Pose, Citation2017). In the 2016 UK referendum on European Union (EU) membership, for example, the older industrial towns of England and Wales were among the places that voted heavily for Brexit, a development that has been widely interpreted as a symptom of disillusion with globalization and deindustrialization and was one of the reasons why, in spring 2019, the UK government announced the establishment of a ‘Stronger Towns Fund’ targeted specifically at less prosperous local economies beyond the big cities.

Britain is far from alone in having swathes of the country that have lost their original industrial base. Parts of North East France, much of the former East Germany and the ‘rustbelt’ of the United States come to mind. In Britain both the original industrialization and the later deindustrialization generally began earlier and the efforts to rebuild economies have mostly been in place longer, but the scale of the industrial job loss is often not dissimilar to that found elsewhere. The statistical evidence points to the UK as being one of the most regionally unbalanced countries in the industrialized world (McCann, Citation2019), but there may be international pointers in the recent British experience.

AIMS OF THE RESEARCH

The present paper provides an empirical investigation of trends in the labour market in Britain’s older industrial towns between 2010 and 2016, in particular by deploying ‘labour market accounts’ to document the contributions of changing levels of employment, population, migration, commuting and labour market participation to the outcome in terms of unemployment. It seeks to answer four key questions.

Does the reduction in recorded unemployment in Britain’s older industrial towns reflect a resurgence in local job opportunities or have other important labour market adjustments been at work?

How do recent labour market trends in these older industrial towns compare with trends in the main regional cities, including London?

To what extent is there systematic variation in the extent to which the towns have recovered, for example, by region or according to proximity to one of the main regional cities?

How have the recent labour market trends in Britain’s older industrial towns been linked to trends in other places by commuting and migration, including migration from outside the UK?

In the broadest terms, the evidence assembled here is intended to shed a light on whether recent trends suggest there is a viable independent future for the economies of Britain’s older industrial towns and, by inference, for towns in other countries affected by industrial job loss. What is novel in this contribution to economic geography is that it provides new statistical evidence on the contemporary labour market in the advanced industrial economy – and more specifically in its older industrial towns – that has for good or ill probably led the world in deindustrialization.

BRITAIN’S OLDER INDUSTRIAL TOWNS

The distinction between ‘towns’ and ‘cities’ is important because although the UK’s main regional cities nearly all have a strong industrial past, they have always played a wider role in regional and local economies. They have long been service centres for their hinterlands, administrative headquarters, transport hubs for their regions and home to major universities. On the whole, the economies of the big regional cities were therefore never quite as reliant on the older industries that have now shrunk or disappeared.

A further reason for drawing the distinction between ‘towns’ and ‘cities’ is that in recent years towns have tended to be out of favour in policy-making and academic debate. Instead, the focus has been on cities and their potential to lead economic growth. The dominant assumption has been that cities benefit from agglomeration economies that make them better locations for economic activity. If, exploiting this inherent locational advantage, the economy of the cities can be made to grow, the further assumption is that the numerous towns around them will then be carried along in their wake. Prosperity will be spread from the cities to neighbouring areas via commuting flows and through the overspill of businesses to less congested locations, or so the theory goes.

These ideas have academic roots going as far back as Marshall (Citation1890), who argued that industrial clusters raise productivity through easier access to a large and skilled workforce and specialized suppliers and customers. A century later, Porter (Citation1990) deployed much the same arguments to explain competitiveness, Krugman (Citation1991) stressed the agglomeration advantages of cities, and Jacobs (Citation1986) argued that it is cities, not nations, that are the drivers of wealth. In the UK, the State of the English Cities report (Parkinson et al., Citation2006) was important in identifying the reversal of decades of decline in English conurbations and the turnaround in London, in particular, has been underlined by Martin, Gardiner, and Tyler (Citation2014). Unsurprisingly, Britain’s cities have latched on to these ideas to argue that they are now the motors of economic growth and should be prioritized for investment (Core Cities, Citation2013), a view echoed by the Centre for Cities (Citation2015). They have found a receptive audience in central government, which has placed an increasing emphasis on ‘city deals’ and the devolution of powers to city-regions (HM Government, Citation2011; Cabinet Office, Citation2015; Sandford Citation2016).

Yet, the evidence that cities really are leading UK economic growth remains patchy. Fothergill and Houston (Citation2016) argued that whilst cities are potentially good locations for some types of business activity, non-city areas are better for others. In a physically small country such as the UK, the distances are rarely large so the labour market links between towns and cities are very real, as Swinney, McDonald, and Ramuni (Citation2018) have documented. However, whether the UK regional cities have a monopoly on growth and high productivity has been contested in the context of the North of England (Cox & Longlands, Citation2016). It is clear, nevertheless, that UK cities and towns are diverging in terms of their population structure, with all the consequences that may imply for long-term growth (Centre for Towns, Citation2017).

In practice, the employment trends in the big cities beyond London, at least up to 2012, seem not to have been consistently better than elsewhere (Champion & Townsend, Citation2011, Citation2013). Casting the net wider to include smaller cities as well, Pike et al. (Citation2016) also identified a mixed picture, with relative decline in several Northern cities in particular. Martin et al. (Citation2014) found a negative relationship between city size and output growth between 1981 and 2011 – in other words, smaller places fared better. The existing evidence on older industrial Britain since the recession points in the opposite direction: reviewing a range of data up to 2014, the Industrial Communities Alliance (Citation2015) argued that older industrial areas were lagging behind in the recovery.

A WORKING DEFINITION

In this paper we use the term ‘older industrial towns’ to include all Britain’s older industrial areas beyond the main regional cities. There is no official UK government definition of these places, and a definition driven by a single set of statistics is not possible. lists the local authority districts and unitary authorities used here for statistical purposes. Districts and unitary authorities are the smallest building block for which most of the key contemporary data are available.

Table 1. Districts and unitary authorities covering ‘older industrial towns’.

The core of the list comprises the districts and unitary authorities covering the UK’s former coalfields, the location of so much of the UK’s early industrialization. Here we use the labour market-based definition of the coalfields first deployed in Beatty and Fothergill (Citation1996), which covers the places where the coal industry still accounted for 10% or more of men in work in 1981, but the list excludes four small coalfield areas in the Midlands and South where economic recovery is known to have been firmly entrenched by the early 2000s (Beatty, Fothergill, & Powell, Citation2007). The additions to this core cover the locations of job loss from the UK’s main steelworks, shipyards and concentrations of heavy engineering and chemicals (Beatty & Fothergill, Citation2017). The list also includes the former mill towns of Lancashire and West Yorkshire, where the textile industry has all but disappeared. A problem in applying a single statistical indicator at one point in time is the timing of job loss: the main contraction in the UK’s cotton and woollen textile industries occurred in the 1950s and 1960s, and big job losses from shipbuilding also date from this time, whereas the main job losses from steel began in the 1970s and from other industries rather later. A further complication is that much of the historical data are not held on contemporary local authority boundaries. We have also chosen to exclude the main locations of the UK motor industry (where they do not overlap with the location of other older industries) because although the motor industry also experienced substantial job losses it never approached terminal decline, unlike several of the UK’s other industries, and since the 1990s has actually experienced something of a revival. No definition of ‘Britain’s older industrial towns’ can entirely exclude an element of informed judgement and this needs to be kept in mind in interpreting the data presented here.

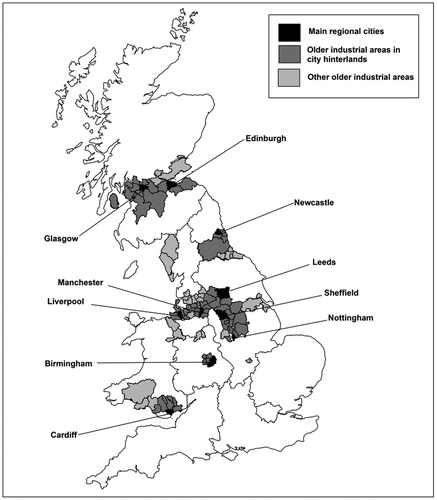

Reflecting Britain’s distinctive industrial geography, the districts and unitary authorities in are all in the Midlands, North, Scotland and Wales, where job losses from older industries have long posed a problem for the regional economy, and the list excludes the main regional cities. In 2016, the local authorities listed in , and mapped in , had a combined population of 16.6 million, or 26% of the Great Britain (GB) total. Three points are worth noting. First, some of these ‘towns’ are actually substantial cities – Sunderland, Hull, Bradford, Stoke and Swansea, for example. Second, several the local authorities cover numerous quite small towns, especially in former mining areas such as County Durham. Third, some of the local authorities stray into rural territory just as some of the obvious omissions (Northumberland is an example) include sub-areas that are clearly older industrial in character.

Figure 1. District and unitary authorities covering Britain's older industrial towns.

THE LABOUR MARKET ACCOUNTING APPROACH

Labour market accounts are a tool that can be used disaggregate overall trends into several constituent flows. Whereas it might be naively assumed that an increase in the number of jobs in a locality will lead to a reduction in local unemployment of the same magnitude, in fact the labour market is a great deal more complex. Alongside changes in labour demand there are simultaneous changes in labour supply, some independent of labour demand, others (commuting, for example) to a significant extent in response to the availability of employment.

The use of labour market accounts to help understand regional and local trends in the UK has a long history. The Cambridge Economic Policy Group (Citation1980, Citation1982) first applied this approach to UK regions, highlighting the interrelationship between employment growth and migration. Begg, Moore, and Rhodes (Citation1986) applied labour market accounts to Britain’s cities over the period 1951–81, illustrating what was, at the time, an outflow of both people and jobs. Turok and Edge (Citation1999) used labour market accounts to expose the serious job shortfall in cities that had accumulated following years of deindustrialization and recession. The approach has also been applied at the sub-regional scale (Owen & Green, Citation1989; Green & Owen, Citation1991).

In the former coalfields, labour market accounts showed how the loss of coal jobs resulted in little or no increase in recorded unemployment, in this instance because of a diversion of working-age men into ‘economic inactivity’ (Beatty & Fothergill, Citation1996; Beatty et al., Citation2007). More recently in the coalfields, labour market accounts have demonstrated how there are growing interactions between the male and female sides of local labour markets (Beatty, Citation2016). In seaside towns, labour market accounts have shown how relatively high unemployment has coexisted with surprisingly resilient employment, the key explanation in this case being sustained in-migration (Beatty & Fothergill Citation2004).

A great advantage of labour market accounts is that the components are all arithmetically related, so it is possible to show how they work together to generate the overall pattern of labour market change. There are several different ways in which the accounts can be presented. The one followed here is as follows:

Increase in the number of jobs

Natural increase in the workforce

Internal net in-migration

International net in-migration

Increase in net in-commuting

Increase in economically active

Reduction in recorded unemployment

Here we assemble labour market accounts for Britain’s older industrial towns for the period from 2010 to 2016. The period begins with the UK economy in deep recession following the financial crisis and from around 2012 onwards covers a period of sustained if unspectacular economic growth. At the time of writing, 2016 is the most recent year for which most of the relevant local economic data is available. Whilst comparisons with the pre-2010 period might have been illuminating, the substantial additional data assembly has precluded this option within the present research.

The principal data source is the UK’s Annual Population Survey (APS), which is a continuous national household survey incorporating the Labour Force Survey (LFS). In 2016/7 the APS had a sample size of around 230,000, of which around four-fifths were of working-age (16–64 years). The changes in the number of jobs, in recorded unemployment and in economic activity rates are all taken directly from this source. The change in net commuting is the changing balance (positive or negative) between the number of jobs in each district and the number of residents in employment, again from the APS. The number of jobs in each area is the number of people who report a primary workplace in the area – this differs a little from the total number of jobs in the area (because some people have more than one job) and more substantially from the number of residents in employment (because of commuting). At the district scale, all APS data are affected by sampling error, but by aggregating into larger groups of towns the bigger sample sizes reduce the confidence intervals and the estimates are broadly reliable. The alternative source of workplace-based employment data, the UK’s Business Register and Employment Survey, provides more reliable figures for individual local areas such as districts, but unlike the APS excludes the self-employed, who these days make up well over 10% of the UK workforce, and therefore cannot be combined in labour market accounts alongside data that covers the workforce as a whole.

The natural increase in the workforce aged 16–64 cannot be measured directly and has been calculated by a cohort survival model based on the age structure of the local population in 2010, the numbers reaching the ages of 16 or 65 by 2016, and deaths of working age. These data are all from the UK’s Office for National Statistics (ONS) or from National Records of Scotland.

In the labour market accounts presented here migration is divided into two components: net migration internal to the UK, and net migration from abroad. This is particularly appropriate given the historically high level of international migration to the UK in recent years (e.g., ONS, Citation2018a). The accounts use the ONS figures on internal migration by local authority, adjusted on the basis of GB data to exclude migrants aged 0–15 and 65 plus. The ONS produces figures on net long-term (i.e., 12 months plus) international migration by local authority, drawing principally on international passenger surveys. However, the ONS notes that the recording of emigration from the UK by international students is problematic (ONS, Citation2017), a view confirmed by the statistics regulator (Office for Statistics Regulation, Citation2017). In university cities and towns, in particular, this is a potentially serious distortion. Additionally, not all international migrants are of working age and not all those of working age are necessarily engaged with the labour market.

The labour market accounts require local-level estimates of net international migration by economically active working-age adults. Bearing in mind that the other elements in the labour market accounts are all either direct measurements from the APS, or the product of a reliable model (natural increase), or longstanding ONS estimates (internal migration), the most robust approach is to estimate net international migration as the residual that arithmetically balances the labour market accounts. For GB as a whole between 2010 and 2016, this points to net international in-migration of economically active working-age adults of 1.1 million. The ONS figure for all net international migration of working age over the same period is 1.4 million. Most, if not all, the difference will be attributable to economically inactive migrants so in practice the two figures are close. The estimation of net international migration of economically active working-age adults as a residual in the labour market accounts is not ideal. However, the local estimates used here are less likely to be distorted by the difficulties in measuring the flows of international students.

OLDER INDUSTRIAL TOWNS, 2010–16

presents labour market accounts for Britain’s older industrial towns for the period 2010–16. The first line shows that the number of jobs in the towns increased by 220,000 over this six-year period. In absolute terms the increase was from 6,170,000 in 2010 to 6,390,000 in 2016. This is the number of jobs located in the towns (more specifically, the number of people recorded by the APS as reporting a primary workplace in these towns), not the number of residents in work.

Table 2. Labour market accounts for older industrial towns, 2010–16.

The second line shows that the natural increase in the workforce in Britain’s older industrial towns was actually negative over these years. In other words, the sum of deaths of working age and people reaching age 65 exceeded the number of young people reaching age 16 – an excess of 190,000. What is noteworthy here is that the period 2010–16 spans the years when the large numbers born immediately after the Second World War finally reached state pension age.

The third line shows that the size of the workforce also declined as a result of internal migration though the reduction, at just 20,000, was not large. By contrast, over this six-year period international migration (the fourth line) increased the economically active working-age population of the towns by 160,000. Both flows here are net, that is, the balance between the numbers moving in and moving out, and they cover just 16–64 year olds.

The negative figure in the accounts for commuting (the fifth line) points to an increase in net out-commuting of 110,000. Commuting between areas has increased over the years as travelling distances have risen, and net commuting is the balance between flows in each direction. In 2010, Britain’s older industrial towns had a net outward flow of nearly 860,000 commuters; by 2016 this had risen to 970,000.

The increase in the economic activity rate among men and women of working age (the sixth line) added a further 120,000 to labour supply in older industrial towns. By 2016, just under 76% of all men and women of working age (16–64) in the towns were ‘economically active’ in that they were either in work or looking for work.

The final line in the accounts shows the reduction in recorded unemployment. The figures here are the number of men and women meeting the International Labour Organisation (ILO) unemployment criteria used by the UK’s LFS. To be ILO unemployed, a person has to be out of work, to have looked for work in the last four weeks, and to be available to start work within the next two weeks. In the UK, the number of ILO unemployed is the government’s preferred measure of unemployment and has for some years substantially exceeded the ‘claimant count’ – the number claiming unemployment-related benefits. In Britain’s older industrial towns, the ILO measure of unemployment fell by 270,000 between 2010 and 2016. In 2016, recorded unemployment in the towns stood at 440,000.

What the labour market accounts indicate is that over this particular period the reduction in recorded unemployment in Britain’s older industrial towns (270,000) was actually 50,000 greater than the growth in local employment (220,000). This was possible primarily because of the excess of retirements over the numbers of young people entering the workforce, and because of an increase in out-commuting. Pushing in the other direction, boosting local labour supply, was rising labour force participation and net migration from abroad.

JOB QUALITY

One of the prominent worries about the recovery from recession in the UK has been that the newly created jobs have been biased towards low-wage, insecure employment. For older industrial towns, the evidence from the APS is mixed. ‘Self-employment’, for example, which can conceal dubious employment practices, accounted for 11% of employed residents in 2017 compared with 14% across Britain as a whole. As a share of all jobs in the towns, self-employment was up just 1 percentage point since 2010. Part-time employment, at 26% of jobs, was also only marginally higher than the GB average and unchanged from the share in 2010.

According to APS data, in 2017, 2.6 million people across the UK as a whole were ‘underemployed’ in that they wanted to work more hours – down on the peak level of around 3.1 million during the recession, but higher than the pre-recession figure of just below 2 million. A government survey of businesses puts the number of employees on zero-hours contracts at 1.8 million, but APS data put the 2017 total lower at 900,000, or 2.8% of all employment (ONS, Citation2018b). The numbers have risen sharply since 2010, but the ONS takes the view that a part of the observed increase is due to increased recognition and awareness of this form of employment. Around one-quarter of those on zero-hours contracts would like more hours, mostly in their current job, and across the UK as a whole APS data show that, in 2017, 4% of workers had second jobs and 5% were in temporary employment.

In the absence of local data, the small national percentages on zero-hours contracts, with second jobs or in temporary employment, suggest that these are likely to be relatively marginal features of the labour market in older industrial towns, though that does not rule out the possibility of increases since the pre-recession years.

However, two indicators do sharply differentiate older industrial towns from other places. One is the continuing reliance on industrial employment. In 2017, 14% of the jobs in Britain’s older industrial towns were still in manufacturing, energy and water – almost twice the proportion in the main regional cities and three times the proportion in London. The other is the proportion of white-collar jobs, which in 2017 accounted for just 39% of all jobs in older industrial towns compared with 50% in the main regional cities and 60% in London. The government’s Annual Survey of Hours and Earnings shows that, in 2017, the median gross weekly pay of employees working in older industrial towns was 9% below the GB average.

DIFFERENCES ACROSS THE COUNTRY

presents labour market accounts for older industrial towns in four parts of Britain: the Midlands, North, Scotland and Wales. What is striking is the similarity of the labour market trends in older industrial towns in each of these parts of the country. Growth in the number of jobs, expressed as a percentage of the base year working-age population, was in the narrow range of 1.1–2.4%. The reduction in recorded unemployment was in an even narrower range between 2.4% and 2.9%. Other labour market flows show only subtle differences across the country. For example, Scotland’s older industrial towns gained rather more from internal UK migration, but rather less from international migration, and Scotland appears to have lagged in terms of rising economic activity rates.

Table 3. Labour market accounts for older industrial towns in different parts of Britain, 2010–16.

Such modest differences should not, however, deflect from the main observation, which is that, on the whole, across the Midlands, North, Scotland and Wales, older industrial towns shared broadly similar labour market trends over this period.

COMPARISONS WITH OTHER AREAS

compares labour market accounts for Britain’s older industrial towns with equivalent figures for the main cities in their regions, for London (defined here as Greater London) and for Britain as a whole. The 10 main regional cities here are the local authorities at the core of larger metropolitan areas that also include several older industrial towns.

Table 4. Labour market accounts for 2010–16: comparisons.

Comparisons between absolute numbers are compromised by differences in population – whereas the older industrial towns have a combined population of 16.6 million, the main regional cities have a total of 5.6 million, London has 8.8 million and the GB as a whole has 63.8 million. The labour market flows are therefore also expressed as a percentage of the working-age population in each area at the start of the period. Several important points emerge from the comparisons:

Between 2010 and 2016, recorded unemployment in older industrial towns fell faster than the average across Britain, at the same rate as in the main regional cities, yet over the same period, the number of jobs in older industrial towns grew substantially more slowly. As a percentage of the resident working-age population, the number of jobs in the main regional cities grew more than three times faster than in older industrial towns, and the job growth in London was nearly seven times faster.

The reduction in the workforce in older industrial towns attributable to a negative natural increase was part of a national GB trend, but not one shared by the main regional cities or in particular by London.

The small loss of the working-age population in older industrial towns attributable to internal migration was less than the equivalent losses from the main regional cities and from London, but the increase attributable to international migration was proportionally less than in the main regional cities or in the GB as a whole, and markedly less than in London.

The increase in out-commuting from older industrial towns (110,000) was not counterbalanced by an equivalent increase in commuting into the main regional cities (just 20,000).

The increase in economic activity rates over this period added proportionally less to the workforce in older industrial towns than to the national average and in particular to London.

In summary, the labour market trends in older industrial towns differ in important ways from trends in the cities and the national average. Despite the above-average reduction in recorded unemployment in older industrial towns, several of the other trends, notably the growth in local employment, are distinctly less positive.

RELATIONSHIP TO REGIONAL CITIES

A large number of older industrial towns are located in the immediate hinterland of the main regional cities, while others are located further afield and therefore less likely to be connected to the cities by commuting flows. On the grouping used here, some 11.9 million of the 16.6 million people in Britain’s older industrial towns live in the hinterlands of the main regional cities. Some of these towns are sufficiently close to the main regional cities to be integral parts of the same labour market (e.g., Salford in relation to Manchester); others are further afield, within commuting distance, but also with a significant degree of physical and economic separation (e.g., Doncaster in relation to Sheffield).

compares labour market accounts for older industrial towns in city hinterlands with equivalent figures for older industrial towns further afield. If proximity to a major city is an important determinant of growth, it should be evident in these figures. In fact, job growth between 2010 and 2016 was virtually the same in towns close to the cities as in towns further afield and there was little difference too in the reduction in recorded unemployment.

Table 5. Labour market accounts for older industrial towns in city hinterlands and more remote locations, 2010–16.

The labour market links between cities and their neighbouring towns are nevertheless very real and powerful. In 2016, net commuting out of the older industrial towns in the cities’ hinterlands totalled 920,000, equivalent to 18% of all residents in employment. Not all this commuting will have been into the main regional cities, of course, but this particular figure is a net flow – the daily flow outwards will be significantly larger, offset in part by in-commuting.

Looking at commuting flows from the other direction, in 2016 the 10 main regional cities covered here had a net in-flow of 910,000 commuters, equivalent to 27% of all the jobs located in these cities. In the cities where the boundary is drawn tightly the proportion is higher still: 37% in Newcastle upon Tyne, 39% in Nottingham and 45% in Manchester. The figures are lower for Leeds (14%) and Sheffield (10%) where the city boundaries are drawn more inclusively.

The experience of individual cities and their hinterlands does, however, seem to have varied. It is difficult to be precise because for individual places the APS data on changes in net commuting is subject to a larger sampling error. However, Manchester, Edinburgh and Cardiff appear to have experienced a marked increase in net in-commuting between 2010 and 2016, balanced by a large increase in net out-commuting from surrounding older industrial towns. Elsewhere, the changes in commuting appear to have been more complex.

THE ROLE OF LONDON

Although London is some distance from nearly all Britain’s older industrial towns, its huge and dynamic labour market might still be expected to exert an important influence. This is less likely to be felt through commuting patterns (though there are unquestionably Monday-to-Friday flows from long distance into London) than through its impact on migration. therefore compares labour market accounts for three parts of Britain: London, the three regions making up the rest of the South (South East, South West and East) and the rest of the country, which includes all the older industrial towns under consideration here.

Table 6. Labour market accounts for London and the rest of Britain, 2010–16.

London’s labour market dynamics over the 2010–16 period are truly astonishing. The number of jobs in London grew by 800,000, at a pace four times faster than in the rest of the South or in the rest of Britain. London also experienced a vast net inflow of economically active adults of working age from abroad (an estimated 530,000), a surge in net in-commuting (up 150,000), a big increase in labour supply from rising economic activity rates (an extra 250,000) and a natural increase in its workforce (80,000) that reflects a population structure skewed towards younger groups.

The relevant question here is whether any of this spectacular growth spilled over into the labour markets of the Midlands, North, Scotland and Wales, where Britain’s older industrial towns are to be found.

Internal migration is the key variable. It might have been expected that London’s employment growth would have attracted workers from the rest of the country. In fact, though London did experience net in-migration, this was entirely attributable to international migration. The internal migration flow (i.e., the flow of UK residents) was actually strongly out of London – a net outflow in excess of 300,000, and the corresponding net inflow was nearly all to the rest of the South of England, which suggests that it was strongly driven by the availability and cost of housing. This meant that, taken as a group, the Midlands, North, Scotland and Wales neither gained nor lost from internal migration. Likewise, but less surprisingly, the increase net in-commuting into London was almost exclusively from the rest of Southern England.

In effect, the figures demonstrate that over the 2010–16 period, London’s impressive job growth was largely detached from the labour market north of a line from the Severn Estuary to the Wash. There was little or no spillover via commuting or migration. This confirms an earlier observation relating to the pre-recession years (Rowthorn, Citation2010) that the net flow of internal migrants into London and the South of England has essentially come to a halt.

THE ROLE OF INTERNATIONAL MIGRATION

Over the 2010–16 period, international migration of working age was a major feature of the UK labour market. The figures in the labour market accounts put the net inflow of economically active working-age migrants to Britain at 1.1 million.

Turning to the impact on older industrial towns, two comparisons stand out. First, though net international migration into the towns provided a substantial boost to labour supply (an estimated 160,000), it failed to offset fully the negative natural increase in the local workforce (190,000) arising from the excess of retirements and deaths over the number of young people reaching working age. Second, at 160,000, the net international migration of economically active working-age adults was equivalent to roughly three-quarters of the net job growth in older industrial towns over the same period (220,000).

It is very unlikely, however, that all the new jobs in older industrial towns would have been created in the absence of international migration. Workers from abroad have probably allowed some firms to expand more than would otherwise have been the case by filling skill shortages or, in at least some cases, by providing a source of cheap labour. On the other hand, in the context of older industrial towns with persistent unemployment, especially during the earlier part of the decade, it is questionable just how much firms’ growth would have been constrained by labour supply.

Britain’s older industrial towns have not, however, been the prime destination for international in-migrants. Rather this has been London, which over the 2010–16 period accounted for almost half of all working-age net international migration to the UK. Again, there are two key statistical observations. First, at 530,000, net international migration by economically active working age adults increased London’s working-age population by almost 10% in just six years. Second, at 530,000, this net international migration was equivalent to two-thirds of the quite spectacular growth in London’s employment over this period (800,000).

Again, it is impossible to tell how much of this job growth in London would have happened in the absence of international migration. However, in London, where labour has generally been in shorter supply than in older industrial towns, it is reasonable to assume that in the absence of international migration more firms would have been constrained by labour supply.

What, then, would have been the knock-on impact on older industrial towns if this huge international inflow to London had not occurred? It is impossible to be certain, but if London had still generated substantial numbers of new jobs, these might have attracted more internal migrants from within the UK, including from older industrial towns. The labour market accounts confirm that London’s rapid job growth since 2010 has not resulted in a net flow of migrants from the North, Midlands, Scotland and Wales, which is consistent with the earlier evidence from Rowthorn (Citation2010) that international migration into London and the South has been the key factor in curtailing internal migration from the rest of the UK.

CONCLUSIONS

The labour market accounts provide a complex picture of recent trends, but four general points emerge from this evidence:

The reduction in recorded unemployment since 2010 paints an overly positive picture of trends in Britain’s older industrial towns. It hides the fact that the number of jobs in older industrial towns has been growing only slowly, that out-commuting from the towns has increased further from an already high base and that the increase in labour force participation has lagged behind the national average. The labour market accounts do not portray the economy of Britain’s older industrial towns as having bounced back strongly from the post-2008 recession, let alone from preceding years of industrial job loss.

The labour market in Britain’s older industrial towns is deeply embedded with neighbouring cities and places further afield. This is evidenced by large commuting flows, but also by other trends that can only be explained by reference to the role that older industrial towns play in the wider UK urban system. For example, the negative natural increase in the workforce in older industrial towns, in contrast to growth in London and the main regional cities, reflects age structures that have been shaped by years of selective migration.

The improvement in the labour market in Britain’s older industrial towns since 2010 does not seem to have been especially dependent on neighbouring cities. Across the towns as a whole there is little evidence that proximity to one of the main regional cities has led to faster growth in employment or bigger reductions in unemployment. As a general rule, Britain’s older industrial towns tend to share similar labour market trends wherever they are located.

There is scant evidence that London’s spectacular employment growth since 2010 has had a positive impact on the labour market in Britain’s older industrial towns. The Exchequer may have gained from London’s growth, and there may therefore have been fiscal and macroeconomic benefits to the Midlands, North, Scotland and Wales, but the labour market accounts show that the direct benefits of job growth in London have been confined to London and surrounding parts of the South.

In effect, labour market trends in Britain’s older industrial towns since the recession confirm neither assumptions of self-correcting economic growth nor fears of ongoing local decline. The best assessment is perhaps that there is persistence in the longer term labour market problems in these places. Just as the 2008 recession was not the underlying cause of their economic weakness, recovery from the recession has not marked a turn-around in their relative position in the UK economy.

It is possible to speculate why the post-recession recovery in Britain’s older industrial towns has been sluggish, though the labour market accounts themselves do not pinpoint why. One likely reason is that the economies of the towns remain strongly reliant on manufacturing whereas the UK’s post-recession upturn once more mirrored the service-led model of earlier years, driven by rising household spending and debt rather than an improvement in the UK’s balance of trade. A second likely reason is the continuing policy emphasis on the big cities, which have continued to draw in public sector investment, especially into London. A third likely reason is simply that the industrial job loss of earlier years has cast a very long shadow, with downward adjustments in local spending power and indeed in population (relative to other areas) that have counteracted positive progress in reviving local economies.

The implication of this assessment – in the UK and elsewhere if this experience offers any guide – is that interventions to support growth and jobs in older industrial towns are likely to remain an important claim on policy-making for some years to come. In principle, an effective approach is likely to require a rebalancing of national economic growth towards the sectors, particularly manufacturing, that remain key components of the economy of older industrial towns, combined with a range of public spending and financial incentives in the towns that make them attractive to potential investors.

Whether the low recorded unemployment in Britain’s older industrial towns, the rapid growth of employment in London and the high level of international in-migration to the UK can be sustained is another matter. Beyond the period covered here, the UK’s departure from the European Union looms large not only over the UK economy as a whole but also over the older industrial towns where so much of what remains of UK manufacturing is located. There is a very good case for revisiting the data presented here in, say, 2022 or 2023, when a different national economic context might have led to different local labour market trends.

DISCLOSURE STATEMENT

No potential conflict of interest was reported by the authors.

Additional information

Funding

REFERENCES

- Beatty, C. (2016). Two become one: The integration of the male and female labour markets in the English and Welsh coalfields. Regional Studies, 50, 823–834. doi: 10.1080/00343404.2014.943713

- Beatty, C., & Fothergill, S. (1996). Labour market adjustment in areas of chronic industrial decline: The case of the UK coalfields. Regional Studies, 30, 627–640. doi: 10.1080/00343409612331349928

- Beatty, C., & Fothergill, S. (2004). Economic change and the labour market in Britain’s seaside towns. Regional Studies, 38, 459–478. doi: 10.1080/0143116042000229258

- Beatty, C., & Fothergill, S. (2017). The impact on welfare and public finances of job loss in industrial Britain. Regional Studies, Regional Science, 4, 161–180. doi: 10.1080/21681376.2017.1346481

- Beatty, C., Fothergill, S., & Powell, R. (2007). Twenty years on: Has the economy of the UK coalfields recovered? Environment and Planning A: Economy and Space, 39, 1654–1675. doi: 10.1068/a38216

- Begg, I., Moore, B. C., & Rhodes, J. (1986). Economic and social change in urban Britain and the inner cities. In V. Hausner (Ed.), Critical Issues in urban economic development: Volume 1. Oxford: Clarendon.

- Cabinet Office. (2015). 2010 to 2015 government policy: City deals and growth deals. London: Cabinet Office.

- Cambridge Economic Policy Group. (1980). Urban and regional policy with provisional regional accounts 1966–1978. Cambridge Economic Policy Review, 6.

- Cambridge Economic Policy Group. (1982). Employment problems in the cities and the regions of the UK: Prospects for the 1980s. Cambridge Economic Policy Review, 8.

- Centre for Cities. (2015). Cities outlook 2015. London: Centre for Cities.

- Centre for Towns. (2017). Launch Briefing.

- Champion, T., & Townsend, A. (2011). The fluctuating record of economic regeneration in England’s second-order city regions 1984–2007. Urban Studies, 48, 1539–1562. doi: 10.1177/0042098010375320

- Champion, T., & Townsend, A. (2013). Great Britain’s second-order city regions in recession. Environment and Planning A: Economy and Space, 45, 362–382. doi: 10.1068/a45100

- Core Cities. (2013). Competitive cities, prosperous people: A core cities prospectus for growth. Manchester: Core Cities.

- Cox, E., & Longlands, S. (2016). City systems: The role of small and medium-sized towns and cities in growing the Northern Powerhouse. Manchester: IPPR North.

- Fothergill, S., & Houston, D. (2016). Are big cities really the motor of UK regional economic growth? Cambridge Journal of Regions, Economy and Society, 9, 319–334. doi: 10.1093/cjres/rsw009

- Green, A., & Owen, D. (1991). Local labour supply and demand interactions in Britain during the 1980s. Regional Studies, 25, 295–314. doi: 10.1080/00343409112331346507

- HM Government. (2011). Unlocking growth in cities. London: HM Government.

- Industrial Communities Alliance. (2015). Whose recovery?: How the upturn in economic growth is leaving older industrial Britain behind. Barnsley: Industrial Communities Alliance.

- Jacobs, J. (1986). Cities and the wealth of nations. Harmondsworth: Penguin.

- Krugman, P. (1991). Geography and trade. Cambridge, MA: MIT Press.

- Marshall, A. (1890). Principles of economics. London: Macmillan.

- Martin, R., Gardiner, B., & Tyler, P. (2014). The evolving economic performance of UK cities: City growth patterns 1981–2011. London: Foresight, Government Office for Science.

- McCann, P. (2019). Perceptions of regional inequality and the geography of discontent: Insights from the UK. Regional Studies. https://doi.org/10.1080/00343404.2019.1619928

- Office for National Statistics (ONS). (2017). International migration data and analysis: Improving the evidence. London: ONS.

- Office for National Statistics (ONS). (2018a). Migration statistics quarterly report: February 2018. London: ONS.

- Office for National Statistics (ONS). (2018b). Contracts that do not guarantee a minimum number of hours: April 2018. London: ONS.

- Office for Statistics Regulation. (2017). The quality of the long-term student migration statistics. London: Office for National Statistics (ONS).

- Owen, D. W., & Green, A. E. (1989). Labour market accounts for travel-to-work areas 1981–84. Regional Studies, 23, 69–72.

- Parkinson, M., Champion, T., Evans, R., Simmie, J., Turok, I., Crookston, M., … Park, A. (2006). State of the English cities. London: Office of the Deputy Prime Minister.

- Pike, A., MacKinnon, D., Coombes, M., Champion, T., Bradley, D., Cumbers, A., … Wymer, C. (2016). Uneven growth: Tackling city decline. York: Joseph Rowntree Foundation.

- Porter, M. (1990). The competitive advantage of nations. New York: Free Press.

- Rodriguez-Pose, A. (2017). The revenge of the places that don’t matter (and what to do about it). London: Centre for Economic Policy Research, London School of Economics (LSE).

- Rowthorn, R. (2010). Combined and uneven development: Reflections on the North–South divide. Spatial Economic Analysis, 5, 363–388. doi: 10.1080/17421772.2010.516445

- Sandford, M. (2016). Devolution to local government in England ( Briefing Paper No. 07029). London: House of Commons Library.

- Swinney, P., McDonald, R., & Ramuni, L. (2018). Talk of the town: The economic links between cities and towns. London: Centre for Cities.

- Turok, I., & Edge, N. (1999). The jobs gap in Britain’s cities. Bristol: Policy Press.