Abstract

The article presents an original stock-flow consistent macroeconomic agent-based model with the aim to reexamine Harrod’s instability principle as an explanatory element of macroeconomic dynamics. The main findings are that bottom-up economic models can be subject to Harrodian instability and can produce endogenous cycles without introducing innovation waves, monetary wage spirals, or financial instability. Upward instability is stopped by the ceiling of full employment, and downward instability can be tamed by introducing an autonomous expenditure that feeds aggregate demand.

Appendix

Markup shocks during expansion

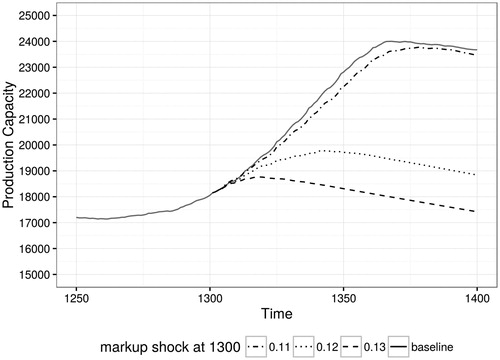

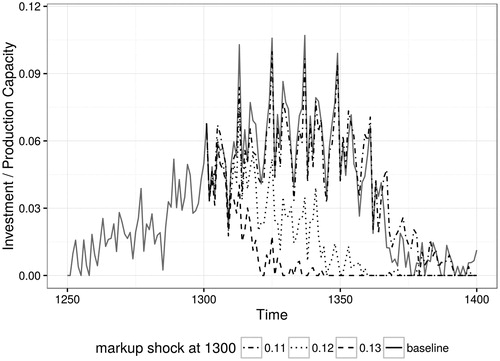

The size of the markup shock considerably affects accumulation dynamics. The higher the shock, the lower the accumulation rate gets, as shown in and . This is the well-known paradox of cost: increasing markup reduces real wages and decreases the accumulation rate.

Figure 6. Markup shocks during expansion.

Figure 7. Markup shocks during expansion.

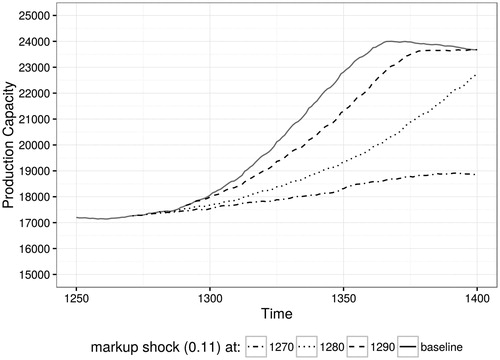

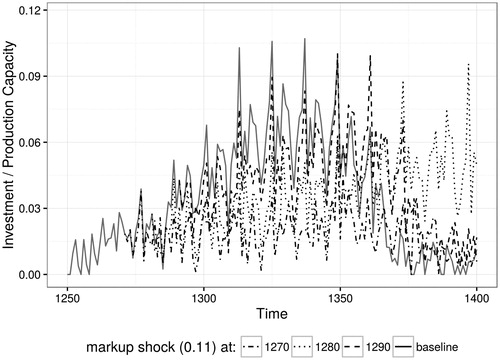

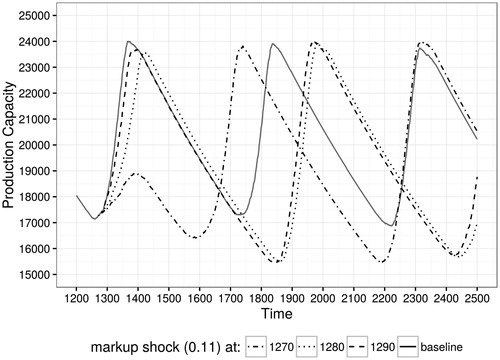

Figure 8. Markup shocks: the importance of timing.

Markup shocks: the importance of timing

In the short run, the effect of a markup shock on accumulation dynamics depends, to a large extent, on the timing of the shock. and show different progressions in productive capacity following the same shock (markup switch set to 0.11), but applied at different times at the beginning of the expansion phase. The earlier the shock is set up at the beginning of the exogenous expenditures-led phase, the greater its effect on dynamics will be. In the short run, growth and investment rates are lower when the shock on markup is set earlier in the exogenous expenditures-led phase. This decrease occurs because a higher markup increases the entire system’s propensity to save and reduces the efficiency of the autonomous component of demand. During the upward instability phase, the Harrodian instability becomes increasingly important, and the relative importance of the autonomous component of demand decreases. Consequently, the impact of the markup shock is reduced. In the medium term, the timing of the shock has little impact on the cycle, as illustrated in . A higher markup produces deeper recessions because the lower bound decreases due to a higher markup reducing the efficiency of autonomous expenditures. The upper bound remains restricted by full employment and therefore stays at the same level.

Figure 9. Markup shocks: the importance of timing.

Figure 10. Markup shocks: the importance of timing.

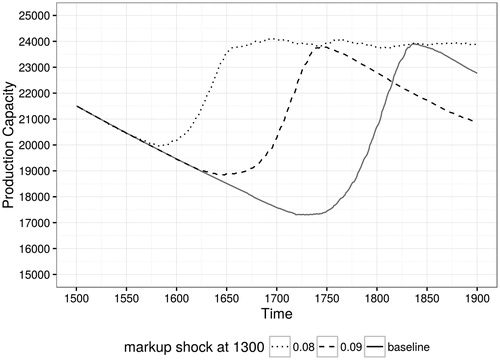

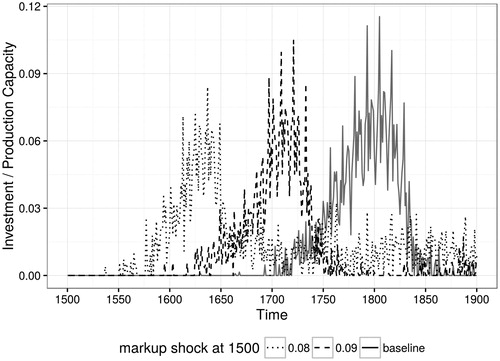

Markup shocks during recession

and show the effects of a lower markup shock at step 1500. Reducing the markup to 0.09 or 0.08 allows a faster economic recovery and decreases the depth of the recession. A lower markup implies a reduced propensity to save of the system, which reinforces the effect of the autonomous component of demand. Figure 12 shows that, besides the temporal lag, the accumulation rate decreases with a lower markup. Although this may seem counterintuitive, this decrease occurs because recovery takes place earlier, and depreciation of the productive capacity has had a lower impact because it is of shorter duration. This reduces the distance to full employment and shortens the upward instability phase because the Harrodian instability is an exhilarationist dynamic: the longer it lasts, the higher it will become.

Figure 11. Markup shocks during recession.

Figure 12. Markup shocks during recession.

Table A1. Notations of variables and parameters.

Table A2. Initial values and parameters.

Table A3. Transactions-flow matrix.

Notes

1 Keynesian and Harrrodian instability rely both on the combination of the accelerator principle and the accelerator effect (i.e., the two-way feedbacks between aggregate demand and investment). In both case, the multiplier is a central component of the model because it is the investment that determine the level of production. The difference lies in the way the accelerator principle plays (i.e., how aggregate demand affects investment decisions). The Keynesian instability is described as a short/medium run phenomenon, where the utilization rate (as a proxy of aggregate demand) affects the accumulation rate and the utilization rate is determined by the accumulation rate. This is, respectively, the accelerator principle and the multiplier effect. The Harrodian instability takes place in a longer time scale but the mechanisms are basically the same. When there is a discrepancy between the utilization rate and its normal value, firms adapt their expectations relative to the trend growth rate of sales. These expectations are a component of the Kaleckian investment function, and their adjustment acts as the accelerator. If the distinction is relevant in the Kaleckian model, it is not the case in the present model because it does not converge to fully adjusted position and because firms do not produce long-run expectations about the trend growth rate of sales.

2 By plausibility, Dallery (Citation2010) means the ability of the model to produce results consistent with historical reality.

3 Decentralized decision-making produces uncertainty that prevents decentralized agents from making decisions.

4 Transaction-flow matrix is provided in the .

5 Lavoie (Citation2012) considered this to be the most realistic mechanism to deal with adjustments to supply and demand.

6 Seppecher (Citation2014) explained that the minimum inventory level seems to correspond to one-month production at full capacity utilization.

7 Cordonnier and Van De Velde (Citation2009) made a theoretical distinction between investment to improve efficiency and investment for the purpose of increasing capacity.

8 See Cottin-Euziol and Rochon (Citation2013) for an analysis of the effects of bank credit repayments.

9 The model is implemented under Netlogo (v5.2.0).

10 In this article, as in post Keynesian literature, potential GDP is the production of full employment.

11 See Allain (Citation2015) for a contribution concerning the effect of autonomous expenditures on Harrodian instability in a Kaleckian framework.

12 See Krishna Dutt et al. (Citation2015) for a contribution on the effect of labor market flexibility in a Kaleckian framework.