Abstract

This special collection examines insurance as an increasingly central mechanism in shaping how the effects of climate change are transforming local economies and ways of life. The papers study a range of exemplary cases, ranging from agricultural micro-insurance in development policy and regional sovereign risk facilities in the Caribbean to public and private insurance in the United States. This framing essay situates these papers in a longer tradition of scholarship on the government of risk and security. It also describes three themes that run through the papers: the economization of climate change; the moral economy of risk and responsibility; and the plasticity of insurance as an abstract technology that may be taken up in various governmental assemblages, in the name of various political projects.

Keywords:

In the last decade, as multilateral political efforts have failed to cap carbon emissions at levels that might prevent massive climate change, experts, officials and activists around the world have turned to the problem of adapting to transformations and upheavals that seem inevitable. Indeed, ongoing climate change is already shaping economic and social life in multiple ways and at multiple scales. Though individual events cannot be readily attributed to climate change, scientific assessments are increasingly confident and specific in anticipating how climate change will play out in particular places (IPCC, Citation2018; US Global Change Research Program, Citation2018). But there is nothing deterministic about the effects of these changes on global economies or local ways of life. Rather, these effects are being channelled by institutional mechanisms and political decision-making.

This special section examines one mechanism through which the effects of climate change are being channelled that promises to be of growing importance in coming years: the financial sector, and within this sector, insurance and reinsurance. In part, the effects of climate change are channelled through existing lines of insurance: more frequent and intense catastrophic events increase pay-outs on various kinds of insurance and threaten the solvency of both individual insurers and broader pools of financial capital. The result may be dramatically increasing premiums or the withdrawal of insurance cover from particular perils and geographical areas (a prospect that was recently discussed in the aftermath of devastating fires in California and other western US states in 2018 and 2020, as well as in bushfire-affected parts of Australia in 2019–2020; see Butler, Citation2020; Kaufman & Roston, Citation2020; Lucas & Booth, Citation2020; Walsh, Citation2018). At the same time, the effects of climate change are being channelled through a range of instruments that both private and public insurers and reinsurers are using to assess catastrophe risks (such as risk mapping and catastrophe modelling), and to manage this risk. Techniques for managing climate risk range from novel financial instruments offered by private insurers and other financial services entities, such as micro-insurance, index insurance, and catastrophe bonds, to public regulation and reinsurance or other governmental backstops.

The papers in this collection take stock of this rapidly changing and still emergent terrain by examining particular geographical locales, institutional settings and technical arrangements of catastrophe insurance as they intersect with climate change: agricultural micro-insurance in development policy, particularly in Africa (Johnson); regional sovereign risk facilities in the Caribbean (Grove); urban resilience initiatives in US cities (Collier and Cox); risk assessment and rate making in public flood insurance (Elliott); and catastrophe modelling of private wind insurance (Gray). These papers investigate the technical issues that are arising and the governmental devices that are being invented and deployed, as both public and private insurers work to assess and distribute catastrophe risk. Thus, on the one hand, they examine how uncertain future catastrophes are rendered knowable and governable in the present; how climate change risks are reflected in existing lines of insurance; and the new insurance and quasi-insurance instruments that are being developed to manage increasingly pervasive and costly catastrophe risk. On the other hand, the papers ask how insurance is shaping the political landscape of risk, vulnerability and responsibility in the Anthropocene today. How does insurance constitute collectivities or publics around climate risks? How does private insurance interact with public security mechanisms, whether through public regulation or public backstops for private insurance, or through private insurance cover for public functions? How does insurance distribute both exposure to climate risks and new forms of security?

Catastrophe insurance and climate change: An emerging assemblage

Discussion of climate change and insurance is not new. The first assessment of the International Panel on Climate Change (IPCC), released in 1990, noted that insurance could serve a double function, both providing signals about risks (that might affect the decisions of businesses or homeowners to locate in a floodplain, for example) and offering an ‘effective means of reducing the economic impact of losses’ (IPCC, Citation1990, p. 184). Five years later, the Citation1995 IPCC Report on the Social and Economic Impacts of Climate Change detailed various ways that private and public insurance mechanisms could interact with climate change. These included incorporating changing risks into insurance premiums, limiting financial exposure of both private and public entities to catastrophe risks, expanding risk pools through cooperation between government and actors in the financial services industry, and advocating for risk mitigation beyond insurance, to limit the exposure of public and private insurers (Bruce et al., Citation1995).

But over the next two decades, despite selective action by a handful of large insurance companies (most notably European reinsurers like Munich Re and Swiss Re), the insurance industry’s response was relatively meagre. A 2012 report by Ceres, a corporate sustainability watchdog, found that few insurers had ‘explicit policies to identify or manage the trends of global climate change’, adding that many did not ‘seem to understand the difference between climate variability and climate change’ (Ceres, Citation2012).

This picture has changed dramatically in the last several years. Initiatives relating to insurance and climate change have rapidly proliferated, often through collaborations between national governments, multilateral organizations, non-profits and foundations, and private insurers. Participants in these initiatives range from the United Nations and the World Bank, which supports a range of national and regional catastrophe insurance programmes, a global index insurance facility, and a host of micro-insurance programmes, to foundations such as the Clinton Foundation and the Rockefeller Foundation, whose 100 Resilient Cities programme defined a central role for private insurers, both as sources of authoritative risk assessment and as providers of new risk transfer arrangements. Pointing to statements emerging from the Paris Climate Change conference, and to the ‘InsurResilience’ initiative launched by the leaders of the G7, which pledged to extend insurance to 400 million people in poor countries by 2020, Surminski, Bouwer and Linnerooth-Bayer (Citation2016) asked whether 2015 was the ‘year of climate insurance’. In these new initiatives, the emphasis has shifted, at least on the level of rhetoric, from the health of the insurance industry to the role of insurance in governing the risks associated with climate change. This new orientation was articulated by UN Environment Chief Erik Solnheim when he introduced a new programme of the UN Environment’s Finance Initiative to partner with global insurers and reinsurers to better manage their own risk in November 2018. ‘An uninsurable world’, Solnheim wrote, ‘is a price that society could not afford. This is why UN Environment is working with leading insurers to understand and reduce risk, to seize unprecedented business opportunities in climate action, and to ensure an insurable, resilient and sustainable world’ (Gallin, Citation2018).

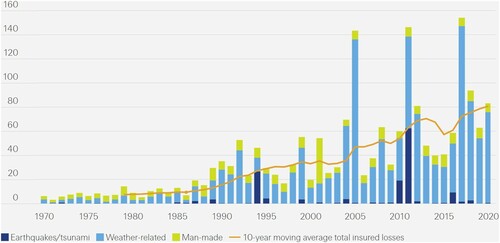

One significant driver of this recent attention to catastrophe insurance and climate change has been the private insurance industry itself. Its motivation is hardly mysterious. Insurers are massively exposed to risks associated with climate change. Such risks to the insurance industry have increasingly drawn the attention of ratings agencies, which conclude that the effects of climate change ‘will magnify the volatility for these firms and result in a number of risk management challenges’ (Moody’s, Citation2018). Pay-outs from existing lines of insurance are increasing dramatically (See ). Swiss Re’s 2018 Sigma study reported that disasters produced a record $144 billion in insured losses and $337 billion in economic losses (versus 10-year averages of $58 billion and $190 billion, respectively) that were largely concentrated in the southeast United States and the Caribbean (Swiss Re Institute, Citation2018). Although not all of these losses are weather-related, insurers link the dramatic increase of loss to climate change, and anticipate that, due to climate change, losses will continue to increase dramatically in the future. Industry groups, consortia of regulators and initiatives of multilateral organizations (such as the UNEP Finance Initiative, mentioned above) also warn that ever-more frequent and intense storms, floods, heat waves and droughts present systemic risks to the insurance industry, and threaten to render certain risks uninsurable.

Figure 1 Insured losses, 1970–2020, in US$ billion at 2020 prices

Source: Swiss Re Institute (Citation2020). News release nr-20201215-sigma-full-year-2020-preliminary-natcat-loss-estimates. Reprinted with permission.

At the same time, private insurance companies and other actors in the financial services industry see climate change as an unprecedented business opportunity and imagine an expansive role for themselves in assessing and managing the risks associated with climate change. Insurance, they argue, can and should act as a financial first responder to the changing climate by estimating and ‘pricing in’ risk, incentivizing mitigation, and unlocking recovery funds in the wake of natural disasters. Reinsurers, meanwhile, are positioning themselves as a backup infrastructure for the rest of the financial sector. In a world of more frequent and severe climate catastrophes, reinsurers claim that their unique tools for ‘pricing’ potential catastrophes, and for defining their likelihood, expected effects and costs, enable them to pool, mitigate and distribute risks associated with climate change, as well as to act as a source of ‘knowledge leadership’ (Collier & Cox, this issue) about emergent threats. In a series of 2010 press releases, Munich Re asserted its own pride-of-place in climate leadership, as a result of its ‘necessary know-how’ and its development of ‘the world’s most comprehensive database on natural catastrophes’. It characterized climate change as ‘a strategic issue for the insurer’ and one about which Munich Re (Citation2010) could offer ‘advice on prevention measures’. Climate change is also ‘opening up new business segments, creating opportunities for the insurance industry’. As Lehtonen (Citation2017, p. 33) observes, the (re)insurance industry acts as ‘a mediating body that gives climate change a shape and presence; it objectifies and commodifies climate change as an uncertain phenomenon, yet presents it as manageable, at least to an extent’.

Some recent reports have viewed the potential role of private insurance in managing the risks of climate change with a kind of breathless optimism, positing that where governmental and inter-governmental processes have failed, insurance can provide both the finance for climate adaptation and instruments to spread risk. ‘While politicians debate, Munich Re innovates’ ran a headline from Forbes Magazine (Baskin, Citation2015), others proclaimed that ‘Insurance gains clout as climate change solution for the poor’ (Rowling, Citation2015), and that a ‘Global insurance plan aims to defuse potential climate damage ‘bombshell’ (Carrington, Citation2017). Critics, meanwhile, have denounced the central role of the private sector in insurance. The activist and author Naomi Klein (Citation2015, p. 9), for example, has charged that ‘global reinsurance companies are making billions in profits, in part by selling new kinds of protection schemes to developing countries that have done almost nothing to create the climate crisis, but whose infrastructure is intensely vulnerable to its impacts’.

There is little doubt that, given their importance in making future risks a matter of governance in the present, private insurance and reinsurance promises to play a central role in shaping how the effects of climate change are assessed and distributed. Yet, it seems much too early to characterize the form of this connection in broad terms, or to render sweeping judgment about its political significance. We are still at the earliest stages of adjustment of existing insurance mechanisms, and of innovation in techniques, in response to changing risks. Moreover, new knowledge practices and techniques for risk mitigation have been put into practice only under highly selective circumstances. It is difficult to predict whether the interest of private insurers in catastrophic risk will be sustained, what kinds of risks will be covered, and, crucially, how private insurance will interact with public mechanisms.

This special section makes two contributions to charting this still emergent and rapidly changing field. First, the papers examine a set of exemplary geographical sites, institutional mechanisms and political issues in this field. These range from micro-insurance and sovereign risk management in Africa and the Caribbean, which have been central focal-points for many international initiatives around insurance, to private and public insurance in the United States, the country with by far the largest catastrophe insurance pools and the largest volume of insured loss. Second, across these diverse institutions and sites, the papers take insurance as a site for inquiring into larger problems of social theory in the context of climate change, each in their own way examining how insurance is reformatting vulnerability and security as objects of governmental management. They address questions such as: How is the role of insurance as high finance related to the old promise of insurance as an instrument for solidarity and for sharing responsibility? How are insurance schemes structured by private and public agents such as municipal governments, private businesses, national authorities, or global financial corporations? What role is insurance playing in constituting climate change as a public problem?

Insurance and risk society: Beyond ‘insurability’ and ‘calculability’

The papers in this issue build on a longstanding critical social scientific inquiry into insurance as a privileged site for understanding the changing politics of risk and security in the face of catastrophic threats. This discussion was initiated 30 years ago by the German sociologist Ulrich Beck in his work on ‘risk society’. Beck (Citation1992 [Citation1986]) observed that the traditional practices of insurance – assessing and distributing risks based on observations about the historical occurrence of loss-making events – corresponded to certain kinds of events. The risks of what Beck called ‘first modernity’, such as accidental death, workplace injuries, or individual disease, exhibited regular patterns of occurrence across geographically-bound populations. Therefore, they could be effectively pooled and distributed over particular groups (of workers, citizens, etc.), thus creating a form of security that corresponded to new forms of solidarity in the emerging welfare states of the late nineteenth and early twentieth centuries (Ewald, Citation2019; Lehtonen & Liukko, Citation2011). But Beck (Citation2002) argued that such actuarial calculations and mechanisms of social solidarity could not function in a ‘second’ modernity dominated by ‘uncontrollable’ and ‘unbounded’ risks such as nuclear war, mass casualty terrorism and ecological disaster. Such risks, he argued, could not be subject to existing forms of expert assessment. Moreover, given their wide geographic spread, they could not be distributed over a population. Consequently, Beck claimed, insurance could be analysed as an ‘autonomic signaling mechanism’ of a new stage of modernity. The limits of insurance cover marked the boundaries of risk society.

In response to Beck’s initial claims about insurance and risk society, a number of scholars pointed out that the line between the insurable risks of ‘first modernity’ and the uninsurable catastrophe risks of ‘second modernity’ did not hold up (Bougen, Citation2003; Collier, Citation2008; Ericson & Doyle, Citation2004a). They documented ways in which private insurers have extended to catastrophe risks employing both calculative and non-calculative techniques of risk assessment (Ericson & Doyle, Citation2004b; Jarzabkowski et al., Citation2015).Footnote1 In response to these arguments, Beck (Citation2009) more recently qualified his claim. Pointing to the example of terrorism insurance after 9/11, which was offered by private insurers only after the creation of a public backstop, Beck (Citation2009) acknowledged that private insurance may be extended to catastrophes. But he anticipated that such coverage would be both ‘selective’ and ‘fragile’, subject to cycles of expansion, collapse and government bailout or other mechanisms to limit private risk. Calling for the abandonment of the ‘unspoken functional premise of private insurance’, Beck (Citation2009, p. 138) argued that critical social science should ‘develop its own critical perspective on the simultaneous collapse and expansion of private insurance coverage’.

Today, particularly in light of rapidly proliferating discussion of climate change and insurance, Beck’s focus on insurance as a privileged site for investigating the changing politics of risk and security seems perspicacious. As we will suggest in the next section, insurance does indeed illuminate key issues of contemporary risk governance, such as the changing forms of expert risk assessment, the interplay between public and private security mechanisms, and the distribution of risk and responsibility in the face of multiplying catastrophic threats. Moreover, Beck’s (Citation2009, p. 138) call to study the ‘simultaneous collapse and expansion’ of private insurance seems particularly apt today. Discussions of catastrophe insurance are characterized equally by urgent calls to dramatically expand insurance cover for climate-related risks and warnings that, unless mitigation or adaptation measures are taken, existing insurance arrangements may collapse, and the risks faced by certain populations in certain geographical areas may become uninsurable.

At the same time, the emphasis in debates around risk society on the limits of insurance in addressing catastrophe risks – and, in particular, their emphasis on the technical calculability of catastrophe risk and the extension of private insurance in particular to cover such risks – do not capture important emerging issues in the field. In part, this is due to significant changes in the insurance industry since the early 1990s that have made private insurers and others in the financial services industry much more willing and able to assess and insure such risks. Furthermore, the emphasis on private insurance in this discussion seems one-sided. Virtually all catastrophe insurance involves the public sector, whether as regulator, as the provider of backstops or reinsurance, or in many cases as the consumer of private insurance products. Thus, to understand the emerging assemblages of catastrophe insurance and climate change we have to devote much more attention to the role of the public sector, including both national and local governments and various inter-governmental and international organizations, and to ‘third sector’ organizations like major foundations, as well as their dynamic relation to private insurance.

Approach and themes

In light of these developments, our strategy is to continue with Beck’s problems, but to capture important emerging issues in the field missed by an overriding emphasis on the limits of private insurance in addressing catastrophe risks. What the collection does as a whole is map a terrain over which the techno-politics of climate change – and, more broadly, the contemporary politics of risk and security – are getting worked out. We identify how political and normative problems are specified through technical mechanisms of government in a field that still has an ‘emergent’ quality to it. Thus, this special section is dedicated less to describing (social and economic) structures, and more to identifying problems and dynamic sites in which things are taking shape. The geography of the papers is necessarily selective, focusing on global sites in which the role of insurance in governing climate change is growing, changing, or most consequential. What the contributions to this special collection share, then, is the premise that the way into larger questions about the politics of climate change starts from specific practices and knowledge infrastructures. At the same time, the papers are not so much ‘case studies’ as studies of situations that exemplify emerging forms of insurance-linked governance of climate risk and of the problems to which they give rise. Three important themes emerge from these studies.

The economization of climate change

In engaging with Beck on the limits to insurability, existing critical insurance scholarship has focused on the commoditization of climate catastrophe risk. It turns out that insurers, who are always confronting the limitations of their own knowledge (Ericson & Doyle, Citation2004b), have indeed found ways to make the threats and fears associated with climate change into marketizable risks, that is, into things that are worth something (Jarzabkowski et al., Citation2015). A suite of new risk assessment tools, most notably catastrophe modelling (Collier, Citation2008; Johnson, Citation2013a), have become increasingly widespread and authoritative (referred to in some cases as the ‘gold standard’ for catastrophe risk assessment). These tools make it possible for insurance to economize climate change in particular ways (Çalişkan & Callon, Citation2009, Citation2010). A range of new risk transfer mechanisms are changing the way that the insurance industry narrowly, and the financial services more broadly, distributes catastrophic risks (Aguiton, Citation2019; Jarzabkowski et al., Citation2015; Johnson, Citation2015). Through reinsurance and various other risk transfer mechanisms, notably what are referred to as ‘alternative risk transfer’ instruments such as catastrophe bonds and other insurance-linked securities, catastrophe risks are now distributed into vastly larger pools of financial capital rather than over relatively small and geographically limited populations of policyholders (Christophers et al., Citation2020; Taylor, Citation2020). As a result of these changes, not only insurers but also other actors in the financial services industry have been increasingly eager to take on catastrophe risks in a drive to develop new markets for primary insurance as well as to meet (and profit from) the growing demand in broader financial markets for investment instruments whose returns are not correlated with other kinds of risk (Johnson, Citation2013b, Citation2015).

But there is more to economization, and to the insurance economization of climate change, than marketization. Economization is also about the constitution and formatting of calculative agencies: the ways in which actors are made to take something into account in their decisions. Examples of this appear across the papers. Collier and Cox, for instance, examine three mechanisms by which the private insurance industry formats contemporary urban resilience initiatives in New York City, New Orleans and Miami: generating knowledge about vulnerability, risk assessments and benefit–cost analysis of resilience interventions for city officials; offering novel risk transfer mechanisms to urban governance actors; and diffusing devices that incorporate future risks into current decisions. Johnson describes the operation of index insurance in Africa, where international development agencies deploy it to make climate change vulnerability manageable for different actors across scales: from individual African farmers and pastoralists, to banks and contract farming operations, to governments and relief organizations. Grove shows how, in the Caribbean, contingency funds, parametric-based catastrophe insurance products, and alternative risk transfer instruments, such as weather derivatives, make it possible for the island nation of Dominica to budgetize disaster management decision-making processes. Through insurance, catastrophes are constituted as events that generate contingent liabilities and that can and should be planned in order to build the state’s financial capacity to meet post-disaster obligations. Elliott examines the efforts of federal and local officials to take climate change into account in the mapping techniques of the US National Flood Insurance Program. Gray investigates how catastrophe modelling firms first assessed climate science in the context of Florida hurricanes in an effort to allow signals about ‘climate risk’ to begin working their way into the market for property and casualty insurance, shifting individual behaviour around decisions about where to build and purchase future homes. Across these sites, we see how insurance renders climate change calculable and, in the process, makes actors accountable for climate change: not only conventional insurance actors, like households buying flood policies, but also public agencies, cities and sovereigns.

Relatedly, the insurance economization of climate change also involves particular work of framing through which, for example, a calculation of risk or model is employed for one purpose rather than another. Gray’s catastrophe modellers in Florida and Elliott’s local officials in New York City both want to account for climate change in and through insurance tools. But how this is ultimately allowed to proceed reflects distinct forms of contestation over which view of risk can be used to govern which types of decision-making; in both cases, views of risk multiply – leading to multiple models for Gray and multiple maps for Elliott. In Grove’s study, insurantializing interventions in Dominica emerge out of development economists’ moral and technical critique of the ‘dependencies’ created by other forms of disaster financing. The critique involves a reconceptualization of the relations between developing states, donors, and markets in which Dominica is made to ‘plan like an insurer’. These papers illustrate that today much of the debate around catastrophe models and other insurance technologies is around how they should be taken up for different political or governmental ends, not about whether it will be possible to assess catastrophe risks for the purposes of insurance. Competing views of problems and their appropriate responses circumscribe the operationalization of insurantial knowledge about climate change.

The moral economy of risk and responsibility

Calculative agencies are also formatted politically and morally. By rendering climate change calculable, insurance renders actors responsible. As an interdisciplinary scholarship has shown, insurance establishes social relations of various kinds: among individuals, among individuals and institutions, and among individuals, states and markets. It ‘define[s] the contours of individual and social responsibility’ (Baker, Citation1996, p. 291) by forging solidarities that include and exclude, and by shaping ideas of membership and mutual obligation (Collier, Citation2014; Elliott, Citation2021; Ericson & Doyle, Citation2003; Ewald, Citation1991, Citation2019; Heimer, Citation2003; Lehtonen & Liukko, Citation2015; Stone, Citation2002). The papers in this collection excavate the stakes of insurance in relation to the moral economy of risk and responsibility as they appear in the context of climate change: issues of who has to take responsibility for climate risk, when, how much and on what terms. Elliott shows that in New York City what is at stake in mapping climate risk is whether or the extent to which homeowners should be made to pay, now, for climate change through their insurance. For Gray, failure to achieve agreement about hurricane model updates in Florida sheds light on the ways that climate change repoliticizes technical issues of risk distribution and raises questions about who should bear the burden of future climate impacts in the present day. These debates over the intertemporal bearing of costs highlight that questions of how to delimit a risk pool, price a risk, or specify an insurance contract are necessarily and simultaneously technical and moral. In addition, the papers show how, in formatting and assigning responsibilities across actors and scales, insurance also specifies how burdens and benefits in a climate-changed world are distributed. For instance, Johnson observes that it is primarily those without other forms of financial security in poor countries who are compelled to experiment with the imperfect coverage offered by index-based contracts, a ‘second best’ option relative to those available to wealthier populations and countries.

An emergent dimension to this moral economy is the relationship between public and private, a distinction which preoccupied Beck but, in our work, does not always seem so clear and operative. Across the landscape we survey, the government of catastrophe risk is taking shape through complex loops of private and public security mechanisms. In the urban resilience policy space mapped by Collier and Cox, a variety of institutional actors are deploying private insurance not as an alternative to public measures, but rather as a mechanism of public intervention. City officials, policymakers and insurance industry experts in New York City, New Orleans and Miami do not seek to displace or privatize public security, but rather are turning to private insurance as a way to advance work on urban resilience as a public problem. Problems of moral hazard, particularly where public insurance underprices catastrophe risk, have led local jurisdictions to seek out ex-ante finance mechanisms in the private insurance industry. Limitations on ex-post disaster finance have led governments, notably in poor countries, to do the same, as Grove’s work in the Caribbean and Johnson’s work in Africa attest. Moreover, private coverage of catastrophe risks is almost universally hemmed in by various kinds of public sector regulations, as is evident from Gray’s discussion of the contentious relationship between catastrophe modelling firms and state-level insurance regulators shows. The papers examine the different ways that private and public mechanisms are articulated with each other, to assess the political and social stakes of these new forms of calculation and mitigation.

The plasticity of the insurance imaginary across scale and space

There is nothing inherent in insurance that indicates the kind of political project in which it is enlisted. As Ewald (Citation1991) observed, the ‘insurance imaginary’ can be put to a variety of uses, in pursuit of different goals. The papers in this special collection examine diverse climate-related problems for which insurance becomes a solution, focusing not only on the technical details of insurance but also on the very different political contexts in which it is taken up. Johnson documents the rapid multiplication of both the insurantial imaginaries harnessed to index insurance and the configurations of risks thereby transferred. As development actors and insurers redesign index insurance to engage risk pools at different scales, the core technology of the index remains alluring as an appropriate ‘solution’ to various humanitarian, welfare and commercial problems, even in the face of consistently low demand and contractual inaccuracy. Grove examines how the developing state government of Dominica takes up ex-ante risk management in response to the contextually-specific problems that climate change impacts pose to its development and disaster management goals. In more affluent contexts in the United States, examined by Elliott, Collier and Cox, and Gray, insurance is more about protecting property investments in a political context in which the politics of land use and social provision are intertwined, as well as financing public infrastructure and investments in resilience measures.

These cases speak to the plasticity of insurance rationality and help to explain why so many different actors are looking to insurance to govern climate change. They also underscore that ‘insurance’ is not one coherent thing, nor does it work in one way only. Taken together, the papers in this special collection show that the precise effects of insurance on lives and landscapes will depend on how it is harnessed to, and how it reconfigures, the various interventions that target individual and collective security as the climate continues to change.

Acknowledgements

Earlier versions of the papers published in the special section ‘Climate change and insurance’ were presented at a workshop, with the same name, at The New School, New York City, in April 2018. We would like to thank all the participants in the discussions and Academy of Finland for having funded the workshop (Decision Numbers 283447 and SRC312624).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Stephen J. Collier

Stephen J. Collier is Professor of City and Regional Planning at the University of California, Berkeley. He is author of Post-Soviet social: Neoliberalism, social modernity, biopolitics (Princeton University Press, 2011) and The government of emergency: Vital systems, expertise, and the politics of security (Princeton University Press, 2021).

Rebecca Elliott

Rebecca Elliott is Assistant Professor in the Department of Sociology at the London School of Economics and Political Science. Her research examines the intersections of environmental change and economic life, as they appear across public policy, administrative institutions, and everyday practice, with a particular focus on the governance of climate change. She is author of Underwater: Loss, flood insurance, and the moral economy of climate change in the United States (Columbia University Press, 2021).

Turo-Kimmo Lehtonen

Turo-Kimmo Lehtonen is Professor of Sociology at Tampere University, Finland. His present work centres on two different topic areas, one of which is insurance and the management of uncertainty, and the other the role of waste in the contemporary way of life. In addition, Lehtonen has written extensively on social theory. His recent publications include papers in the journals Political Theory, Cultural Studies, Distinktion, Theory, Culture & Society and Journal of Cultural Economy.

Notes

1 Moreover, scholars have shown that these practices for assessing catastrophic risk are not new (e.g. Haueter & Jones, Citation2016; James et al., Citation2013).

References

- Aguiton, S. (2019). Fragile transfers: Index insurance and the global circuits of climate risks in Senegal. Nature and Culture, 14(3), 282–298.

- Baker, T. (1996). On the genealogy of moral hazard. Texas Law Review, 75(2), 237–292.

- Baskin, J. S. (2015, September 10). While politicians debate, Munich Re innovates. Forbes Magazine.

- Beck, U. (1992 [1986]). Risk society: Towards a new modernity. Sage.

- Beck, U. (2002). The terrorist threat: World risk society revisited. Theory, Culture & Society, 19(4), 39–55.

- Beck, U. (2009). World at risk. Polity.

- Bruce, J. P., Hoesung, L. & Haites, E. F. (Eds.). (1995). Climate change 1995: Economic and social dimensions of climate change. Cambridge University Press.

- Bougen, P. (2003). Catastrophe risk. Economy and Society, 32(2), 253–274.

- Butler, B. (2020, January 14). Suncorp and IAG temporarily stop selling insurance in fire-affected areas of Victoria and NSW. The Guardian.

- Çalişkan, K. & Callon, M. (2009). Economization, part 1: Shifting attention from the economy towards processes of economization. Economy and Society, 38(3), 369–398.

- Çalişkan, K. & Callon, M. (2010). Economization, part 2: A research programme for the study of markets. Economy and Society, 39(1), 1–32.

- Carrington, D. (2017, November 14). Global insurance plan aims to defuse potential climate damage ‘bombshell’. The Guardian.

- Ceres. (2012). Insurer climate risk disclosure survey. Retrieved from ceres.org

- Christophers, B., Bigger, P. & Johnson, L. (2020). Stretching scales? Risk and sociality in climate finance. Environment and Planning A: Economy and Space, 52(1), 88–110.

- Collier, S. J. (2008). Enacting catastrophe: Preparedness, insurance, budgetary rationalization. Economy and Society, 37(2), 224–250.

- Collier, S. J. (2014). Neoliberalism and natural disaster: Insurance as political technology of catastrophe. Journal of Cultural Economy, 7(3), 273–290.

- Elliott, R. (2021). Underwater: Loss, flood insurance, and the moral economy of climate change in the United States. Columbia University Press.

- Ericson, R. & Doyle, A. (2004a). Catastrophe risk, insurance, and terrorism. Economy and Society, 33(2), 135–173.

- Ericson, R. & Doyle, A. (2004b). Uncertain business: Risk, insurance and the limits of knowledge. University of Toronto Press.

- Ericson, R. V. & Doyle, A. (2003). Risk and morality. University of Toronto Press.

- Ewald, F. (1991). Insurance and risk. In G. Burchell, C. Gordon & P. Miller (Eds.), The Foucault effect: Studies in governmentality (pp. 197–210). University of Chicago Press.

- Ewald, F. (2019). The values of insurance. Grey Room, 74, 120–145.

- Gallin, L. (2018, November 16). UN partners with 16 global re/insurers to develop climate risk assessment tools. Reinsurance News.

- Haueter, N. V. & Jones, G. (2016). Managing risk in reinsurance: From city fires to global warming. Oxford University Press.

- Heimer, C. (2003). Insurers as moral actors. In R. V. Ericson & A. Doyle (Eds.), Risk and morality (pp. 284–316). University of Toronto Press.

- Intergovernmental Panel on Climate Change (IPCC). (1990). Climate change: The IPCC scientific assessment. Cambridge University Press.

- Intergovernmental Panel on Climate Change (IPCC). (1995). Second assessment: Climate change. Cambridge University Press.

- Intergovernmental Panel on Climate Change (IPCC). (2018). Global warming of 1.5° celsius. Cambridge University Press.

- James, H., Borscheid, P., Gugerli, D. & Strauman, T. (2013). The value of risk: Swiss Re and the history of reinsurance. Oxford University Press.

- Jarzabkowski, P., Bednarek, R. & Spee, P. (2015). Making a market for acts of God. Oxford University Press.

- Johnson, L. (2013a). Catastrophe bonds and financial risk: Securing capital and rule through contingency. Geoforum; Journal of Physical, Human, and Regional Geosciences, 45, 30–40.

- Johnson, L. (2013b). Index insurance and the articulation of risk-bearing subjects. Environment & Planning A, 45, 2663–2681.

- Johnson, L. (2015). Catastrophic fixes: Cyclical devaluation and accumulation through climate change impacts. Environment & Planning A, 47, 2503–2521.

- Kaufman, L. & Roston, E. (2020, November 10). Wildfires are close to torching the insurance industry in California. Bloomberg.

- Klein, N. (2015). This changes everything. Simon and Schuster.

- Lehtonen, T-K. (2017). Objectifying climate change: Weather-related catastrophes as risks and opportunities for reinsurance. Political Theory, 45(1), 32–51.

- Lehtonen, T-K. & Liukko, J. (2011). The forms and limits of insurance solidarity. Journal of Business Ethics, 103(1), 33–44.

- Lehtonen, T-K. & Liukko, J. (2015). Producing solidarity, inequality and exclusion through insurance. Res Publica, 21(2), 155–169.

- Lucas, C. & Booth, K. (2020). Privatizing climate adaptation: How insurance weakens solidaristic and collective disaster recovery. WIREs Climate Change, 11(6), e676, 1–14.

- Moody’s. (2018). Climate change risks outweigh opportunities for P&C (re)insurers. Retrieved from https://www.eenews.net/assets/2018/03/15/document_cw_01.pdf

- Munich Re. (2010, June 22). Munich Re climate summit at Shanghai EXPO highlights risks and opportunities of climate change. Press release. Retrieved from munichre.com

- Rowling, M. (2015, June 19). Insurance gains clout as climate change solution for the poor. Reuters.

- Stone, D. (2002). Beyond moral hazard: Insurance as moral opportunity. In T. Baker & J. Simon (Eds.) Embracing risk: The changing culture of insurance and responsibility (pp. 52–79). University of Chicago Press.

- Surminski, S., Bouwer, L. M. & Linnerooth-Bayer, J. (2016). How insurance can support climate resilience. Nature Climate Change, 6, 333–334.

- Swiss Re Institute. (2018). Sigma 4/2018: Profitability in non-life insurance: Mind the gap. Retrieved from swissre.com

- Swiss Re Institute. (2020). Swiss Re Institute estimates USD 83 billion global insured catastrophe losses in 2020, the fifth-costliest on record. Retrieved from https://www.swissre.com/media/news-releases/nr-20201215-sigma-full-year-2020-preliminary-natcat-loss-estimates.html

- Taylor, Z. J. (2020). The real estate risk fix: Residential insurance-linked securitization in the Florida metropolis. Environment and Planning A: Economy and Space, 52(6), 1131–1149.

- US Global Change Research Program. (2018). Impacts, risks, and adaptation in the United States: Fourth national climate assessment, volume II: Report-in-brief. Government Printing Office.

- Walsh, M. W. (2018, November 20). How wildfires are making California homes uninsurable. The New York Times.