ABSTRACT

The private sector has a critical role in terms of countries being able to meet the SDGs. We evaluate the extent to which South Africa’s top 100 listed companies have responded to the SDGs, through a review of their early disclosure of the SDGs in their annual reports. Of these companies, only 6% and 11% in 2016/2017 and 2017/2018 financial year ends respectively have incorporated the SDGs into their business model and strategies as reported. Even though there was an increase between the years, it was noted that only 2% of the companies in 2017 communicated how they incorporated and prioritised the SDGs within their business model and value creation proposition in their Integrated Report specifically. Without a defined business case for the adoption of the SDGs into business, the uptake will continue to be slower than required for the contribution of business in meeting the SDGs to be realised.

1. Introduction

Member countries of the United Nations (UN) adopted the 2030 Agenda for Sustainable Development, including the Sustainable Development Goals (SDGs), in September 2015. The SDGs comprise of 17 goals, 169 targets, as well as indicators, that cover a wide spectrum of global issues including poverty, health, education, climate change and environmental degradation (Szennay et al. Citation2019; Rosati & Faria Citation2019a). The global goals provide practical guidance for development now and into the future (United Nations Citation2015).

Governments are not able to implement these global goals on their own. The private sector is vital towards the achievement of the SDGs, especially considering that business plays a critical role in many of the most pressing environmental stresses and social struggles inherent in the SDGs (Scheyvens et al. Citation2016; Pedersen Citation2018; Thorlakson et al. Citation2018; Szennay et al. Citation2019; Rosati & Faria Citation2019a). Business has the finances, skills and other resources; and well as the ability to be innovative, responsive, and efficient; making them an important partner alongside government and civil society in implementing and achieving the goals (Lucci Citation2012; Porter & Kramer Citation2011; Scheyvens et al. Citation2016; Sullivan et al. Citation2018). Responding to the goals can not only unlock new markets and opportunities, but also secure a company’s long terms prosperity (BSDC Citation2017; UCISL Citation2017; WWF Citation2017). The SDGs provide a framework for a resilient and sustainable growth strategy for business (Scheyvens et al. Citation2016). Adopting the SDGs is thus vital for the private sector (BSDC Citation2017).

Since the adoption of the SDGs, there has been a significant amount of investment into incorporating the goals, targets and indicators into the operations, strategies, management practices and performance reporting of business (Rosati & Faria Citation2019a). The sustainable development agenda is, however, not new to business as companies have has been integrating sustainability principles into corporate social responsibility initiatives and other business practices, such as risk management, for the past two to three decades (Rosati & Faria Citation2019b). This is evident by the growing number of global companies that disclose their environmental and social performances in annual reports (KPMG Citation2017). Literature indicates that sustainability reporting is an important drivers of a company’s sustainability orientation and as such sustainability reporting commitments act as triggers towards the integration of the SDGs into business (Lozano Citation2015; Adams Citation2017; Rosati & Faria Citation2019b). As such, many companies contribution towards the SDGs directly through corporate sustainability goals and practices. This is further supported by target 12.6 of SDG 12 (Responsible Consumption and Production) which specifically encourages companies to adopt sustainability practices and to integrate sustainability information into their reporting cycles.

The intention of this paper is to investigate the early disclosure of the SDGs (by South Africa’s top 100 listed companies on the Johannesburg Stock Exchange (JSE)). Considering that annual reports provide insight into a company’s strategy, governance, performance and prospect towards their value creation these reports provide a wealth of information in which to investigate the current disclosure of the SDGs of companies. We undertook this research by means of a content analysis assessment in which we investigated how and what is disclosured in terms of SDG in the integrated reports and sustainability reports of the top 100 listed companies. South African companies have generally been progressive in their adoption and approach to sustainable development. This is meanly due to the King Commission’s Code for Corporate Governance (King III and King IV) that stipulates that reporting on sustainability activities is mandatory in annual reports (Walker & Meiring Citation2010; Groenewald & Powell Citation2016). This is further supported by the JSE, which requires all listed companies to produce an integrated report in which sustainability is an integral component. We hypothesis that South African companies would over the past two years have embraced the SDGs and disclosured them into their annual reporting. The paper will test this hypothesis.

2. The business case for addressing the SDGs

Over the past 15 years, sustainability has become a ‘megatrend’, comparable to many of the other trends that have shaped the way in which businesses operate. The business case for sustainability has predominantly focused on reconciling environmental protection, social justice, and socio-economic development with the intention of improved business performance (Dyllick & Hockerts Citation2002; Wilson Citation2003; Hahn et al. Citation2015). Nevertheless, global statistics continually remind us that business models based on efficient resource consumption and production have not effectively delivered the fundamental changes that are required, but have rather continued to contribute to unsustainable business practices (Westley et al. Citation2011; Sullivan et al. Citation2018). We have already crossed four of the nine ‘planetary boundaries’; defined as safe operating spaces for humanity with respect to the Earth system; and are on the verge of crossing more in the foreseeable future (Rockström et al. Citation2009). Our consumptive and productive nature is leading to the decline and deterioration of ecosystems, natural resources and biodiversity; further characterised by growing social inequality and persistent poverty (WRI Citation2005; Fiksel Citation2006; Whiteman et al. Citation2013). It is no longer enough for business to be addressing global social and ecological challenges and the interconnected economic issues simply by being ‘less unsustainable’. Rather, there is a need for a transformational change; one that firmly refocuses business operations within the limits of the system in which they operate.

The past few years has seen business engaging with integrated thinking as a systematic approach to overcome global sustainability challenges (Jones Citation2014, UCISL Citation2017). Through integrated thinking, companies are encouraged to recognise and embrace interconnected social, environmental and economic issues relating to sustainability and risk; and to understand how these linkages impact on their ability to create value (Figge and Hahn Citation2004; Waldick Citation2010; Bizikova et al. Citation2011; Gao and Bansal Citation2013). The SDGs are a further driver towards encouraging companies to focus integrated thinking in their business model towards navigating global change. This is because the SDGs are an interconnected platform of goals and targets, with strong interdependencies between the various goals and targets. The intention of the SDGs is to systematically promote growth and development that is consistent with the planet’s carrying capacity, society’s basic needs and priorities, and the capabilities and stability of the economy (United Nations Citation2015). In this regard, integrated thinking needs to be closely aligned with the key concepts of systems dynamics, to enable organisations to understand the effect of their actions on the whole system upon which their operations depend. Specifically, businesses need to capture their sustainability aspirations and risk management in relation to the concept of systems resilience – the ability to persist and adapt in response to external shocks, while retaining original structure and function (Adger Citation2003; Walker and Salt Citation2006). Creating value that builds and maintains positive systems resilience will significantly impact the economic value creation of the business.

The SDGs are changing the business case for sustainability from effective and efficient use of resources for economic progress, towards innovation for sustainable development within the limits of systems resilience and planetary boundaries (UCISL Citation2017). Business has the ability to be a positive agent of change, redirecting consumption and production towards unlocking new markets and opportunities that are firmly aligned with the SDGs (WWF Citation2017). Organisations that continue with a business as usual approach will find themselves under severe environmental and social strain. Businesses that see the SDGs as a compelling new growth strategy for innovation and market development will reap the benefits through new markets and emerging opportunities (Pedersen Citation2018).

Research undertaken by the Business & Sustainable Development Commission (BSDC) shows that the SDGs have the ability to create 380 million jobs and open markets worth up to US$12 for business by 2030 (BSDC Citation2017). However, contributing towards the SDGs will require radical changes and innovation among companies, including aligning their core business with the SDGs, helping to build commitment and ambition on key issues in each sector, and creating space for innovation and leadership in the wider system (UCISL Citation2017). Collaboration and public-private partnerships will be keys to success for business and governments in the coming decades (Pedersen Citation2018).

3. Methodology

The sample of companies used in the study was drawn from the top 100 companies listed on the JSE for the financial years ending 2016/2017 and 2017/2018. The JSE is currently ranked the 19th largest stock exchange in the world by market capitalisation, and the largest on the African continent. All South African companies listed on the JSE are required to produce integrated reports as a listed requirement and practice of the country’s corporate governance code (King III and King IV).

The 2016/2017 and 2017/2018 financial year end annual reports, namely sustainability reports (SR) and integrated reports (IR), from the top 100 listed companies on the JSE were downloaded from their company websites. Content analysis was chosen as the most appropriate method in which to assess SDG disclosure within companies annual reports. The content analysis search was undertaken making use of the terms ‘SDGs’ and ‘sustainable development goals’ to identify (1) whether the company mentioned the SDGs in either of their annual reports; (2) if so, the level of disclosure communicated in either report; and (3) if they communicated SDG disclosure which specific SDG(s) they addressed.

The level at which the SDGs was mentioned in either the SR or IR was rated as follows:

Level 1: Companies acknowledge the SDGs and indicate their commitment to the goals, but they do not report any actions towards the implementation or provide any performance measures towards contributing to the goals.

Level 2: Companies disclosure their commitment to the SDGs by discussing alignment of the goals with the company’s existing initiatives/programmes/priorities.

Level 3: Companies disclosure the how the SDGs are incorporated to their business model, operations, strategies, management, and reporting. They report the specific SDG for which their company is addressing and is aligned with.

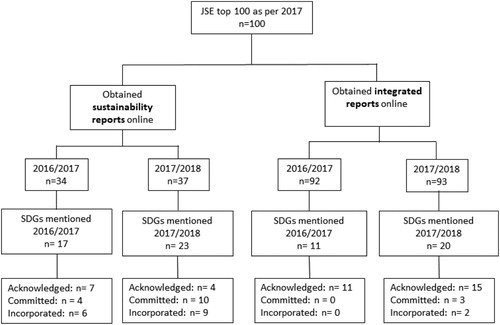

illustrates the steps followed during the data collection process and the screening of each company’s publically-available annual reports, as well as the number of companies included at each of the different screening stages.

Figure 1. Screening and process to access and review companies reports to identify how many mention the SDGs, and the level at which the SDGs are mentioned.

4. Results

There were a few top 100 listed companies in 2016/2017 and 2017/2018 financial year ends for which we were not able to obtain their IR, as they were not available online (). While a separate sustainability report is not necessarily a reporting requirement for South Africa, since sustainability now needs to be firmly captured in the IR, there are still some companies that produce standalone SR’s and make them available online to stakeholders. provides information with regards to the number of SRs and IRs that were publically accessible online. and provide a descriptive finding for each step in , as well as other analysis.

Table 1. Descriptive findings for each of the steps in Figure 1, as well as other characteristics of the companies mentioning the SDGs.

Table 2. A table indicating the level of SDG communication among the JSE top 100 listed companies.

In 2016/2017, of the 92 IRs available online, 11 companies mentioned the SDGs (12%), increasing to 20 companies from the 93 IRs in 2017 (22%). Of the 34 SRs available online in 2016/2017, 17 companies mentioned the SDGs (50%). For 2017/2018 this increased to 23 companies mentioning the SDGs in their SR’s, out of 37 available online (62%) ().

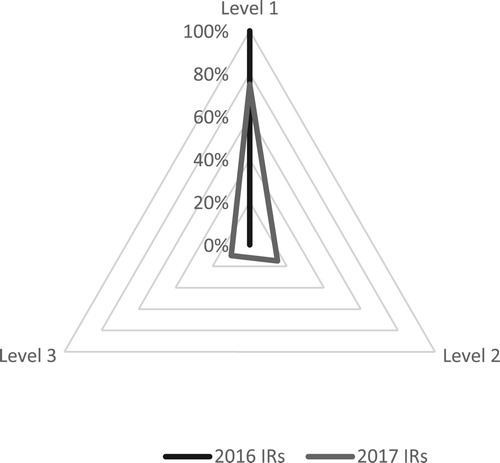

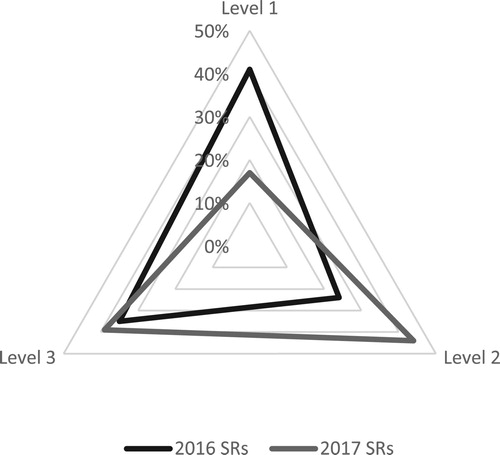

Upon further analysis the majority of companies that mention the SDGs, particularly in the IRs, only acknowledge them (Level 1); this is especially true for 2016/2017. In 2017/2018 we see that a few companies have started to disclosure their commitment to the SDGs (Level 2) and discuss their implementation in their strategies (). For those companies who disclosed the SDGs in their SRs, there appears to be a higher level of committment to the SDGs and even the incorporation of them into companies business models (Level 2 and Level 3) ( and ).

Figure 2. The level at which the SDGs were mentioned in the IRs in 2016/2017 and 2017/2018 financial year end annual reports.

Figure 3. The level at which the SDGs were mentioned in the SRs in 2016/2017 and 2017/2018 financial year end reports.

In total, there were 25 companies that mentioned the SDGs in either their SR or IR (or both) in 2016/2017, and 33 companies in 2017/2018. This is equivalent to 1 in 4 companies on the JSE top 100 that have disclosed the SDGs in their annual reports. This increased to 1 in 3 companies in 2017/2018. Of these companies, 14 disclosured the SDGS only in their SR in 2016/2017, and 13 companies in 2017/2018. Eight of the companies only disclosured the SDGs in their IR in 2016/2017, and this increased to 10 companies in 2017/2018. There were some companies that mentioned the SDGs in both their SR and IR (3 companies in 2016/2017 and 10 companies in 2017/2018) ().

The number of annual reports (either SR or IR) that highlight how a company has incorporated the SDGs into their business strategy, business model and operations was six in 2016/2017 and 11 in 201/20187 (). That is, seventeen of the 71 reports (SR and IR) that mentioned the SDGs disclosured how the companies incorporated the SDGs into their business model and operations. This equated to a total of 24% of the total companies reporting on the SDGs. In the majority of cases, this level of detail was presented in SRs, with only 2 companies disclosing how they have incorporated the SDG’s into their value creation process in their IRs. Ultimately, only 6% of the top 100 have explicitly embedded the SDG into their annual reporting in 2016, and this increased to 11% in 2017/2018. In 2016/2017, this level of reporting was only provided in SRs, whereas in 2017, it was provided in 9 SRs and 2 IRs. Since IRs (unlike SRs) are mandatory, we can conclude that only 2% of the JSE top 100 have incorporated the SDG’s in their mandatory reporting by communicating and disclosuring to stakeholders how their value creation is aligned with the SDGs ().

There were 23 sectors represented in the top 100 JSE listed companies, of which 19 sectors had companies that mentioned the SDGs (in bold in ). It was interesting to note that of the 8 companies from the mining sector, 6 mentioned the SDGs in their annual reporting. Similarly, of the 5 companies in the industrial metal and mining sector, 4 of them mentioned the SDGs in 2016/2017 and 2017/2018. Both these sectors inherently have both positive and negative implications for the environment and society ().

Table 3. The JSE sectors (n=total companies in top 100) with either report (SR or IR) mentioning the SDGs.

The companies that have incorporated the SDGs into their business model and strategies also tend to specify which of the SDGs they address. highlights the number of companies in each sector referring to each of the specific SDGs at this level of detail in their SRs in 2016/2017 (recall that this level of communication was not provided in any IRs in 2016). Similarly shows how many companies in each sector referred to each of the SDGs in either their SRs or IRs in 2017/2018.

Table 4. Number of companies per sector referring to each of the SDGs in 2016 (among companies who have embedded the SDGs in their business model).

Table 5. Number of companies per sector referring to each of the SDGs in 2017 (among companies who have embedded the SDGs in their business model).

5. Discussion

Sustainable development is a philosophy underpinning the King IV Governance Principles, and a reporting requirement of JSE listed companies in South Africa. The SDGs represent a global sustainability agenda and global targets, for which business is an integral stakeholder. It was, therefore, anticipated that more of the top 100 listed companies in South Africa would have aligned their value creation strategies with the SDGs. While it is acknowledged that the SDGs were only launched in September 2015, they had been in discussion long before the Millennium Development Goals expired. Business stakeholders were an integral component of the intergovernmental negotiations that led to the adoption of the 2030 Agenda. An Open Working Group comprising of representatives from the private sector (among others) was established in 2013; in which to coordinate interactions between the UN, civil society and business; leading to the development of the goals and targets (Pedersen Citation2018). The World Business Council for Sustainable Development, the Global Reporting Initiative and the UN Global Compact jointly released a publication entitled ‘SDG Compass: The guide for business action on the SDGs’ in 2015, to give business an early start toward adopting the SDGs. This guide provides insight on how companies can align their strategies, as well as measure and manage their contribution toward the SDGs. There are a number of other similar guidelines that have been released since then, providing business with insight into the value of the SDGs, and how to take them into effect.

The 2016/2017 results can be considered a baseline, as this was the first year that companies could effectively engage with the SDGs in their annual reporting. From this baseline, there has been an increase from 1 in 4 top 100 listed South African companies in 2016/2017 disclosuring the SDGs, to 1 in 3 companies in 2017/2018. A study undertaken by KPMG, published in 2018, highlights that four in ten (40%) of the world’s largest global companies disclosure the SDGs in their annual reporting, suggesting that global business is rapidly engaging with the SDGs (KPMG Citation2018). As business starts to understand how the goals represent future strategies and provide a global framework for transformational change, more and more companies can be expected to incorporate the SDGs into their business models and reporting structures (BSDC Citation2017). Our results suggest that while South African businesses may be aware of the SDGs, they appear to be hesitant to commit or report their actions in contributing towards the targets. There are a number of different reasons for this. Since the business case for engaging with the SDGs has not been clearly articulated for the private sector, there are companies that are not in the position to gain an understanding of how the goals may have a material relationship with their business (PwC Citation2017). Associated with this is the notion that the SDGs can be seen as overwhelming, with their 169 targets; such that many companies have expressed uncertainty as to where and how they can begin to engage with the goals. Larger companies that have a national and international footprint are finding it easier to prioritise the goals and targets, as they can align their company’s value creation with the goals from a global perspective. Small companies that only have a more localised footprint find the goals unachievable and not of relevance to them.

It is, however, not enough to just mention the SDGs by means of a statement that highlights that the company is aware of the global goals. Companies rather need to highlight their commitment to the SDGs through disclosing how their strategies, programmes or initiatives are aligned with certain goals and target, and even better, to show how they have incorporated the goals into their business model, strategies and value creation. Of the top 100 listed companies in SA, only 6% and 11% in 2016/2017 and 2017/2018 respectively have incorporated the SDGs into their business model and strategies and disclosed this in their annual reports. Only 2% do so within their IR, as compared to their SR. This is important because IR’s are mandatory for listed companies in South Africa, and provide information to stakeholders on how companies create value. By 2010, the majority of South African companies had transitioned from separate annual and sustainability reports to integrated reporting as required by King III (Clayton et al. Citation2015). From our results, there are still a number of companies that produce standalone SRs and publish these online. Since the SR is dedicated to the sustainability activities of the organisation specifically, whereas the IR is supposed to be an integrated approach in terms of financial and non-financial reporting, specifically in terms of how the company creates value, it is not surprising to see the SDGs discussed more frequently in SRs. However, considering that the IR is the official report required and the one in which businesses express their ability to create value, there is clearly a need for the SDGs to be incorporated and communicated IRs, in order to reflect how the SDGs are integral to value creation. Specifically, South African companies need to recognise how the SDG provide a framework for transcending beyond traditional models for value creation, towards a more integrated approach between the business, society and the environment.

As per the sector categories described by the JSE, the top 100 companies fall within 23 different sectors. When reviewing the results, it is interesting to note that it is the companies within the primary (extractive) sectors (i.e. mining, oil and gas, forestry, food producers etc.), i.e. sectors that utilise natural resources directly that seem to be engaging and prioritising the SDGs. Some tertiary sectors (e.g. the financial sector – banks, insurance, investment companies etc.) are also engage with the goals, while others (e.g. food and drug retailers) seem to be lagging behind.

It was not possible to conclude from our results which of the specific SDGs are prioritised by companies more than others. Nevertheless, certain trends could be identified. Of the top 100 listed companies that incorporate the SDGs into their business model in South Africa, the results suggest that SDG 3 (good health and well-being) is currently the most considered goal. This is not surprising, as health and safety is a prioritised regulatory requirement in South Africa (Hermanus Citation2007). For example, lack of prioritisation of occupational health and safety in the industrial metals and mining sector has huge social and economic implications for individuals, their families and their communities. There are also direct and indirect socio-economic impacts for society as a whole (Hermanus Citation2007). As such, good health is considered fundamental to advancing all of the SDGs, each of which directly benefits from or contributes to advances in public health (Nugent et al. Citation2018). This was followed by SDG 4 (quality education), SDG 6 (clean water and sanitation), SDG 8 (decent work and economic growth), and SDG 12 (responsible consumption and production). This is in contrast to the results of studies undertaken by PwC, KPMG and the World Council for Sustainable Development which highlight SDG 13 (climate action) as the most frequently identified and prioritised goal (PwC Citation2017; Gomme and Perk Citation2018; KPMG Citation2018). This could be because of companies being more aware of their impact on the environment. There were, however, similarities between our results and the previous studies with regards to two of the other top prioritised SDGs, namely SDG 8 and SDG 12. This prioritisation of SDG 8 and SDG 12 is not surprising, as these are areas where companies have a significant impact (direct and indirect, positive and negative), and are directly linked to businesses (Mhlanga et al. Citation2018).

The comprehensive nature of the SDG framework requires companies to prioritise their areas of engagement. What all these studies suggest is that there is no constant in terms of what and how companies prioritise the goals in terms of their business models. Prioritising a specific goal requires an understanding of the particular issues at a country or local level, combined with an analysis of business operations, sourcing and supply chains (Mhlanga et al. Citation2018). While some of the companies have focused mainly on two or three SDGs; others have either decided to prioritise or engage with most of the goals, or do not provide any information on prioritising specific SDGs. It therefore requires a longer-term vision of, and approach to, business growth strategy and planning than some companies are used to employing. To have that longer term perspective requires an understanding of the risks that companies face if underlying SDG issues are not solved, as well as available opportunities from adapting products and services towards innovations and solutions.

6. Conclusion

Our analysis suggests that South Africa’s 100 listed companies’ engagement with the SDGs must substantially improve if the private sector is to have a meaningful role in contributing towards the achievement of the SDGs. Our results show that while South African top 100 companies are acknowledging and committing to the SDGs as communicated in their annual reporting, few have actually fully integrated the goals and targets into their business models and operations. Not fully understanding the relationship between the objectives of these global goals with material aspects specific to the operations of a business is a potential reason why companies are lagging behind in integrating the SDGs into their business models and strategies. Many companies are merely reinterpreting the SDGs by retrofitting them into their existing sustainability strategies and initiatives (Mhlanga et al. Citation2018). This is in no way a reflection of South African businesses not being leaders in sustainable development. In fact, with the King IV code of conduct and the listed requirements of the JSE, sustainability is a core principle in the governance of business in South Africa. This observation highlights the complicated relationship between the SDGs and a company’s own sustainability objectives (Mhlanga et al. Citation2018).

The role of business in contributing to the SDGs is not straightforward. Embracing 17 goals, 169 targets and approximately 230 indicators is extremely overwhelming. The enormity of the SDGs is leading companies to only focus on small subsets of the SDGs, as seen in our research. This is not ideal, as it promotes companies not fully embracing the notion that all the goals are interconnected and interdependent, exposing companies to unseen risks and unintended consequences (Mhlanga et al. Citation2018). As such, the SDGs in some instances will end up being nothing more than a tool for communication and obtaining a competitive advantage.

While achieving the SDGs relies on contributions from business; companies on the other hand do not currently rely on the SDGs for their success (UCISL Citation2017). Meeting the SDGs will require a significant transformation in business models and strategies, specifically in terms of how businesses embrace the interconnectedness of their operational impacts and value creation on society, the environment and the economy (UCISL Citation2017). In the long term, companies will only succeed once the business case for the SDGs and the role of systems thinking has been specifically defined for business. This will require a shift in thinking from the current economic model to that of a sustainable economy. The SDGs will need to be at the heart of value creation for business. This value creation would not only be measured in terms of profitability, but also in societal value and environmental value. Companies that are able to show this in their business models, and measure their contribution towards achieving the SDGs; will be positive agents of change, driving the future of sustainable business.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Adams, CA, 2017. Conceptualising the contemporary corporate value creation process. Accounting Auditing and Accountability Journal 30(4), 906–31.

- Adger, WN, 2003. Building resilience to promote sustainability: An agenda for coping with globalisation and promoting justice. Newsletter of the International Human Dimensions Programme on Global Environmental Change 2(2003), 1–3.

- Bizikova, L, Swanson, D & Roy, D, 2011. Evaluation of integrated management initiatives. International Institute for Sustainable Development, Winnipeg, Canada.

- Business and Sustainable Development Commission (BSDC), 2017. Better business better world – The report of the Business & Sustainable Development Commission. Business and Sustainable Development Commission, Switzerland. http://report.businesscommission.org/uploads/BetterBiz-BetterWorld_170215_012417.pdf Accessed 5 October 2018.

- Clayton, AF, Rogerson, JM & Rampedi, I, 2015. Integrated reporting vs. sustainability reporting for corporate responsibility in South Africa. Bulletin of Geography 29, 7–17.

- Dyllick, T & Hockerts, K, 2002. Beyond the business case for corporate sustainability. Business Strategy and the Environment 11(2), 130–41.

- Figge, F & Hahn, T, 2004. Sustainable value added – measuring corporate contributions to sustainability beyond eco-efficiency. Ecological Economics 48, 173–87.

- Fiksel, J, 2006. Sustainability and resilience: toward a systems approach. Sustainability: Science. Practice and Policy 2(2), 14–21.

- Gao, J & Bansal, P, 2013. Instrumental and integrative logics in business sustainability. Journal of Business Ethics 112(2), 241–55.

- Gomme, J & Perks, J, 2018. Business and the SDGs: A survey of the WBCSD members and Global Network partners. World Business Council for Sustainable Development, Switzerland. https://docs.wbcsd.org/2018/07/WBCSD_Business_and_the_SDGs.pdf Accessed 5 October 2018.

- Groenewald, D & Powell, J, 2016. Relationship between sustainable development initiatives and improved company financial performance: A South African perspective. Acta Commercii 16(1), 1–14.

- Hahn, T, Pinkse, J, Preuss, L & Figge, F, 2015. Tensions in corporate sustainability: towards an integrative framework. Journal of Business Ethics 127(2), 297–316.

- Hermanus, MA, 2007. Occupational health and safety in mining-status, new developments, and concerns. Journal of the Southern African Institute of Mining and Metallurgy 107(8), 531–8.

- Jones, PH, 2014. Systemic design principles for complex social systems. In GS Metcalf (Ed.), Social systems and design (pp. 91–128). Springer, Tokyo.

- KPMG, 2017. The road ahead. The KPMG survey of corporate social responsibility reporting 2017. KPMG International Cooperative, Switzerland. https://assets.kpmg/content/dam/kpmg/be/pdf/2017/kpmg-survey-of-corporate-responsibility-reporting-2017.pdf Accessed 2 October 2019.

- KPMG, 2018. How to report on the SDGs: What good looks like and why it matters. KPMG International, Switzerland. https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2018/02/how-to-report-on-sdgs.pdf Accessed 10 September 2018.

- Lozano, R, 2015. A holistic perspective on corporate sustainability drivers. Corporate Social Responsibility and Environmental Management 22, 32–44.

- Lucci, P, 2012. Post-2015 MDGs: What role for business. Overseas Development Institute (ODI), London. https://www.odi.org/sites/odi.org.uk/files/odi-assets/publications-opinion-files/7702.pdf Accessed 5 October 2018.

- Mhlanga, R, Gneiting, U & Agarwal, N, 2018. Walking the talk: Assessing companies’ progress from SDG rhetoric to action. Oxfam, London. https://oxfamilibrary.openrepository.com/bitstream/handle/10546/620550/dp-walking-the-talk-business-sdgs-240918-en.pdf Accessed 10 July 2018.

- Nugent, R, Bertram, MY, Jan, S, Niessen, LW, Sassi, F, Jamison, DT, Pier, EG & Beaglehole, R, 2018. Investing in non-communicable disease prevention and management to advance the Sustainable Development Goals. Lancet 391(10134), 2029–35.

- Pedersen, CS, 2018. The UN sustainable development goals (SDGs) are a great gift to business. Procedia CIRP 69, 21–4.

- Porter, ME & Kramer, MR, 2011. The big idea: creating shared value. How to reinvent capitalism – and unleash a wave of innovation and growth. Harvard Business Review 89(1/2), 62–78.

- PwC, 2017. SDG reporting challenge 2017: Exploring business communication on the global goals. PwC, London. https://www.pwc.com/gx/en/sustainability/SDG/pwc-sdg-reporting-challenge-2017-final.pdf Accessed 10 July 2018.

- Rockström, J, Will, S, Noone, K, Persson, A, Chapin, FS, Lambin, E, Lenton, TM, Scheffer, M, Folke, C, Schellnhuber, HJ, Nykvist, B, de Wit, CA, Hughes, T, van der Leeuw, S, Rodhe, H, Sörlin, S, Snyder, PK, Costanza, R, Svedin, U, Falkenmark, M, Karlberg, L, Corell, RW, Fabry, VJ, Hansen, J, Walker, B, Liverman, D, Richardson, K, Crutzen, P & Foley, J, 2009. Planetary boundaries: Exploring the safe operating space for humanity. Ecology and Society 14(2), article no. 32.

- Rosati, F & Faria, LGD, 2019a. Business contribution to the sustainable development agenda: Organizational factors related to early adoption of SDG reporting. Corporate Social Responsibility and Environmental Management 26(26), 588–97.

- Rosati, F & Faria, LGD, 2019b. Addressing the SDGs in sustainanability reports: The relationship with institutial factors. Journal of Cleaner Production 215, 1312–26.

- Scheyvens, R, Banks, G & Hughes, E, 2016. The private sector and the SDGs: The need to move beyond business as usual. Sustainable Development 24(6), 371–82.

- Sullivan, K, Thomas, S & Rosano, M, 2018. Using industrial ecology and strategic management concepts to pursue the sustainable development goals. Journal of Cleaner Production 174, 237–46.

- Szennay, A, Szigeti, C, Kovács, N & Szabó, DR, 2019. Through the blurry looking glass – SDGs in the GRI reports. Resources 8(2), article no. 101.

- Thorlakson, T, de Zegher, JF & Lambin, EF, 2018. Companies’ contribution to sustainability through global supply chains. Proceedings of the National Academy of Sciences 115(9), 2072–7.

- United Nations, 2015. The UN sustainable development goals. United Nations, New York. http://www.un.org/sustainabledevelopment/summit/. Accessed 10 July 2018.

- University of Cambridge Institute for Sustainability Leadership (UCISL), 2017. Towards a sustainable economy: The commercial imperative for business to deliver the UN Sustainable Development Goals. University of Cambridge Institute for Sustainability Leadership, Cambridge. https://www.cisl.cam.ac.uk/resources/publication-pdfs/towards-a-sustainable-economy. Accessed 10 July 2018.

- Waldick, R, 2010. The role of institutions in integrated management. Horizons 10(4), 73–80.

- Walker, B & Salt, D, 2006. Resilience thinking: Sustaining ecosystems and people in a changing world. Island Press, Washington, DC.

- Walker, D & Meiring, I, 2010. King code and developments in corporate governance, vi Legal Brief. King code and governance report, South Africa http://uscdn.creamermedia.co.za/assets/articles/attachments/29922_king_code_and_corporate_governance092010.pdf Accessed 10 July 2018.

- Westley, F, Olsson, P, Folke, C, Homer-Dixon, T, Vredenburg, H, Loorbach, D, Thompson, J, Nilsson, M, Lambin, E, Sendzimir, J & Banerjee, B, 2011. Tipping toward sustainability: emerging pathways of transformation. AMBIO 40(7), 762–80.

- Whiteman, G, Walker, B & Perego, P, 2013. Planetary boundaries: ecological foundations for corporate sustainability. Journal of Management Studies 50(2), 307–36.

- World Resources Institute (WRI), 2005. Millennium Ecosystem assessment: Ecosystems and Human well-being: Synthesis. Island Press, Washington, DC.

- Wilson, M, 2003. Corporate sustainability: what is it and where does it come from. Ivey Business Journal 67(6), 1–5.

- WWF, 2017. ‘SDG’s mean business: How credible standards can help companies deliver the 2030 agenda. WWF, London. https://www.standardsimpacts.org/sites/default/files/WWF_ISEAL_SDG_2017.pdf Accessed 10 July 2018.