ABSTRACT

We explore how digitalization impacts young firms’ growth. A longitudinal panel analysis of the EU’s new ventures during 2010–2018 reveals that digital sectoral capabilities affect young firms’ growth autonomously and via interaction with other sectoral capabilities. Digital sectoral capabilities play an important complementary role in facilitating the upscaling of young firms operating in R&D-intensive contexts as they mature and within environments rich in tangible capital investments. In business contexts characterized by high digital but low human capabilities, young firms struggle to grow, flagging a mismatch of skills’ composition. The effects of digitalization vary depending on the level of competition within each sector. The results on complementarities of sectoral capabilities suggest that horizontal policy solutions favouring specific capabilities in isolation may have limited or counterproductive effects. Instead, policy should target a portfolio of capabilities and consider their complementarities under competitive market structures. Our analysis shows that effective innovation policy should be broadly defined and closely integrated with competition policy.

1. Introduction

Digitalisation has increasingly become a buzzword in discussions on entrepreneurial developments (Audretsch and Belitski Citation2021). Digital transformation enables companies, in particular, young firms, to redefine their business models, allowing for greater experimentation and flexibility by reducing asset specificity, separating previously integrated activities and thus making entrepreneurial outcomes’ intentionally ‘incomplete’ (Yoo, Henfridsson, and Lyytinen Citation2010; Li et al. Citation2016; Autio et al. Citation2018). As a result, offerings’ scope, features, and value continue evolving after products have been introduced to the market.

Digitalisation also facilitates disintermediation, supporting direct interactions between service providers and users, enabling them to bypass intermediaries and reduce transaction costs. It also drives generativity, prompting product ideas and business models to be quickly formed and modified in repeated cycles of experimentation and implementation (Autio et al. Citation2018). Digital networks and platforms and data sharing enable entrepreneurs a quicker opportunity recognition by speeding up the data collection and commercialization process, leading to higher net entry (Nambisan, Wright, and Feldman Citation2019). The proliferation and sophistication of crowdfunding and cryptocurrency platforms ease financing constraints that young firms and SMEs commonly face. Providing alternative finance has made them less dependent on banks and increased their chances of survival and growth (DeYoung et al. Citation2011; Jagtiani and Lemieux Citation2018). E-commerce and multi-segmented platform economies have accelerated young firms’ scalability – both in size and scope – and survival rates (Kenney and Zysman Citation2016; Nambisan et al. Citation2019; Belitski, Korosteleva, and Piscitello Citation2021).

Overall, digital transformation has made entrepreneurship less spatially and sectorally bounded by transforming organizational structures and processes, easing financing constraints and allowing for plenty of scalability opportunities. As a result, its outcomes have become less predefined. These shifts in the external environment are essential for developing a young firm’s resilience to various external shocks (Autio et al. Citation2018; Nambisan et al. Citation2019). For example, while the recent outbreak of the COVID-19 global pandemic has put much strain on young firms and SMEs, it has also offered them opportunities to redefine their business model with more reliance on digital technology and infrastructure (Mason and Hruskova Citation2021).

The process of digitalization and how it shapes entrepreneurial performance is pretty complex. Recent research suggests that human capital deficiencies and changing skills composition may disproportionally affect young firms and SMEs and favour large firms (Criscuolo et al. Citation2021). These bottlenecks are potential impediments to their contribution to European productivity growth (Berlingieri et al. Citation2020). However, new evidence on firm performance suggests that the effect of digitalization manifests itself not so much directly but combined with other sectoral capabilities, underlying the knowledge generation and acquisition process to explain differences in firms’ growth (Bruno, Korosteleva, et al. Citation2021).

Earlier research offering a sectoral system perspective on growth posits that a sectoral knowledge base is critical for shaping sectoral innovation patterns, the rate and direction of technological change, and firm performance (Malerba Citation2002; Malerba and Malerba Citation2004; Malerba Citation2005). However, the focus has been on sector-specific technologies developed via firm R&D investments or acquired via investments in tangible capital. At the same time, digital technologies, exemplifying generic rather than sector-specific technologies, have been shown to have pronounced effects on entrepreneurial dynamics, changing the basis of organizational learning and firm absorptive capacity (Belitski, Korosteleva, and Piscitello Citation2021; Lanzolla et al., Citation2021). Still, the evidence of how digital transformation influences young firms’ growth via complementarities as they mature remains underexplored. Similarly, there is a lack of evidence of how market structure configurations shape the nature of young firms’ growth process.

Drawing on the literature on entrepreneurial growth and industry dynamics, we develop a theoretical framework to explore how digital capabilities, autonomously and interacting with other sectoral capabilities, influence young firms’ growth as they mature. We construct a firm-sector longitudinal dataset for EU countries and the UK during 2010–2018, using Amadeus BvD® data merged with EU-KLEMS sectoral-level indicators and underlying knowledge base sectoral structures. Our findings are twofold: digital capabilities directly affect young firms’ growth; digital capabilities also affect growth via complementarity effects with other sectoral capabilities, benefiting young firms in more competitive environments.

Our study makes several contributions to entrepreneurial performance and industrial dynamics literature.

First, it shows how digitalization and other sectoral capabilities impact young firms’ growth as they mature, thus shedding some light on their resilience. The synergies and trade-offs between digitalization, human capital, innovation, and tangible capital influence young firms’ growth process differently, depending on their maturity.

Second, sectoral capabilities and their interactions are conditional on the market structure. The findings offer evidence of the importance of an interplay between digitalization, human capabilities, innovation capabilities, and tangible capital in influencing entrepreneurial growth in environments with different degrees of competition and the level of firm maturity.

Finally, our study bridges the gap between entrepreneurial growth and industrial dynamics literature. We explore complementarities between sectoral-level knowledge generation and diffusion capabilities and show how market structures influence young firms’ development. Our results carry significant policy implications, which we highlight further below.

This paper is structured as follows. Section 2 discusses the literature on entrepreneurial growth and resilience in a digital context. It also investigates the literature on sectoral capabilities to understand their synergies and trade-offs in shaping young firms’ performance. Finally, we consider the role of industrial structure configurations in these processes. Based on this literature overview, we postulate research hypotheses and conclude this section by presenting our conceptual framework model. Section 3 describes the data, variables and methodology. Section 4 presents the results, and Section 5 discusses the findings, contextualizes them within the literature, and draws policy implications.

2. Theoretical framework and hypotheses

2.1. Sectoral knowledge intense environments, young firms’ growth and resilience in the digital age

The literature on venture performance broadly distinguishes four groups of determinants: (1) founder’s characteristics, (2) firm attributes, (3) entrepreneurial strategies. and (4) contextual environment (for an overview of this literature, see Demir, Wennberg, and McKelvie Citation2017; Parker Citation2018). While the first three factors have been well explored in the literature, the last group remains understudied, particularly sectoral capabilities and their complementarities.

A sectoral system perspective (Malerba Citation2002; Malerba and Malerba Citation2004; Malerba Citation2005) helps us understand how different sectoral patterns shape the entry and performance of firms as they mature and how sector-specific and generic technologies underlie sectoral knowledge base, including stock and flows of knowledge via different channels. With rapid advances in digitalization, the sectoral knowledge base becomes more diverse, leading to a great heterogeneity of firms interacting with each other. Further, digitalization facilitates the broadening of knowledge search. The increasing use of the Internet of Things, Cloud computing, Big Data and business analytics enables more efficient processing of diverse knowledge. The latter redefines firms’ business value creation, augments growth prospects and influences absorptive capacity (Lanzolla et al., Citation2021; Venkitachalam and Schiuma Citation2022).

Young firms engaged in various value-adding economic activities, such as business models and product or process innovation, are more likely to achieve higher growth by gaining temporary competitive advantages (Estrin, Korosteleva, and Mickiewicz 2022). Such benefits are further amplified in more knowledge or digitally intense environments via knowledge spillover (Audretsch and Keilbach Citation2007, Citation2008; Autio et al. Citation2018). In addition, sectoral contexts, facilitating knowledge acquisition and exchange, help strengthen young firms’ ability to become more resilient via their continuous exposure to new ideas and opportunities due to their interactions with peer businesses or customers through digital platforms and capabilities.

Resilience could be thought of as persistence or steady growth rates without fluctuations. Resilience also implies a firm’s capacity to rebound; as long as it is resilient, it will bounce back from temporary disruptions. The latter requires the need for firms to facilitate adaptation and change to be able to embrace new opportunities, reducing thus the detrimental effect of the shocks. While maturing, young firms may experience high and low growth episodes even in a relatively short period. Yet, shocks will be less detrimental to them if they can survive and adapt to constantly evolving market dynamics and embrace new opportunities emerging within different knowledge bases enriched with digital transformation.

2.1.1. Digital sectoral capabilities and new venture growth

Environments rich in digital capabilities will facilitate young firms’ growth autonomously or by interacting with other sectoral capabilities. Moreover, focusing on young firms’ maturity allows an understanding of their growth process. In particular, when young firms get immersed in digital sector capabilities, their growth can be steady or more resilient.

Digitalization has become a significant factor in shaping entrepreneurial ventures, modernizing their organizational structures and business models (Verhoef et al. 2021), and making them recover faster from external shocks. Cirera et al. (Citation2022) show that adopting digital technologies is the critical moderating factor in the relationship between technology readiness and firms’ resilience. Firms that speeded up the introduction of or increased the use of digital technologies in response to the crisis demonstrated higher resilience. Similarly, Abidi, El Herradi, and Sakha (Citation2022) find that digitally-enabled firms faced a lower decline in sales than digitally-constrained firms, suggesting that digitalization acted as a hedge during the pandemic.

New business models allow for greater experimentation and flexibility, making entrepreneurial processes responsive to continuous change (Yoo, Henfridsson, and Lyytinen Citation2010; Li et al. Citation2016; Nambisan et al. Citation2019; Autio et al. Citation2018). Digitalisation facilitates disintermediation, makes location less relevant, and makes entrepreneurs less reliant on intermediaries. Also, it reduces business transaction costs, rendering some efficiency gains and building up a buffer against future shocks (Autio et al. Citation2018).

Digital platforms and data sharing enable entrepreneurs to recognize business opportunities quickly (Nambisan, Wright, and Feldman Citation2019). Platforms facilitate the continuous engagement of young firms in discovering new profitable opportunities, which helps them secure a series of competitive advantages and grow over time (Estrin, Korosteleva, and Mickiewicz Citation2022). Providing alternative finance via digital platforms makes young firms less dependent on banks, raising their chances of survival and growth. It reduces information friction via better data availability and sharing. Also, it improves borrowers’ risk assessment (Jagtiani and Lemieux Citation2018), for example, for young firms traditionally disadvantaged by lenders due to their information opaqueness. Gambacorta et al. (Citation2022) also show that financial digitalization eases the collateral requirements for businesses.

E-commerce and other platform economies have further accelerated the scalability of young firms (Kenney and Zysman Citation2016; Nambisan et al. Citation2019), expanding the growth process beyond the firm’s boundaries (Thomas, Autio, and Gann Citation2014). Thus, digital platforms allow shared value creation by different actors, including individuals and businesses, and for a group of actors with similar interests to pursue entrepreneurial initiatives, as exemplified in the case of crowdfunding platforms (Nambisan et al. Citation2019).

When comparing tangible (physical) and digital technologies, the latter’s effect may spill to other sectors, including mid-tech and low-tech services (Belitski, Korosteleva, and Piscitello Citation2021). Firms intense in digital technologies are asset-light, have lower asset specificity, and their technologies have higher generic (intersectoral) character, enabling adaptability and resilience. This leads us to our first hypothesis:

H1:

Digital sectoral capabilities facilitate young firms’ growth.

2.2. Complementarities between digital and other sectoral knowledge generation & acquisition capabilities

Some recent studies suggest that digitalization accelerates faster than changes in skills, with human capital and skills deficiencies affecting young firms disproportionally (Berlingieri et al. Citation2020). A delay in skill adjustments is a challenge when addressing the growth slowdown in Europe. The evidence on European firms’ performance suggests that the effect of digitalization is less direct but more in combination with other sectoral capabilities (Bruno, Douarin, et al. Citation2022). Similarly, Belitski, Korosteleva, and Piscitello (Citation2021) show that it is an interplay between Digital Technology, Tolerance (cultural diversity), and Talent (high-educated human capital) that jointly explain entrepreneurial dynamics across EU sectors-regions.

Discovery, generation and acquisition of knowledge are critical for new ventures to engage in value-adding activities in dynamic marketplaces (Ketchen, Ireland, and Snow Citation2007). New ventures rely on a set of resources and capabilities and on ‘sectoral platforms’, defined as a combination of complementary capabilities (Breschi and Malerba Citation1997; Andreoni Citation2017), or regional entrepreneurial ecosystems, shown in the literature to strengthen entrepreneurial resilience (Iacobucci and Perugini Citation2021). Therefore, through mutual complementarities and mismatches, digitalization and other sectoral capabilities are critical in determining young firms’ growth. To study how the complementarities between digital and sectoral-level capabilities shape young firms’ growth, we follow other studies suggesting that mezzo-level factors can enhance growth through knowledge generation, acquisition, and transfer. Tangible (fixed capital) and intangible capital, including both R&D intensity and human capital, all play an essential role in accelerating growth via knowledge creation and diffusion (Griffiths et al., Citation2004; Carol, Haskel, and Jona-Lasinio Citation2017; Estrin et al., 2020; Bruno, Korosteleva, et al. Citation2021; Bruno, Douarin, et al. Citation2022). Digitalization via these sectoral capabilities in dynamic markets is expected to enhance firm performance.

Turning to pairwise combinations between sectoral capabilities, we first consider relationships between digital and human capabilities.

As pointed out earlier, there is recent evidence of the gap between digital technology advancements and skill developments (Berlingieri et al. Citation2020). Therefore, digital technology needs to complement human capital to speed up digital technology diffusion. Human capital is a critical conduit for knowledge transfer, but it seems not on its own. With digital technologies, entrepreneurs can solve problems and identify opportunities via open innovation (Belitski, Korosteleva, and Piscitello Citation2021). As argued earlier, digital capabilities enable cost and risk-sharing and collaborative R&D, but this may not work without matching human capital skills and competencies. Hence, our next hypothesis is:

Hypothesis 2a:

Digital and Human Capital complement each other in enhancing young firms’ growth.

Young firms operating in more knowledge-intense environments benefit increasingly from interactions with other firms via knowledge spillovers (Audretsch Citation1995; Audretsch and Keilbach Citation2007, Citation2008). Rapid advances in digitalization have further changed the nature and forms of knowledge assets, redefining businesses’ value drivers and ways of accessing knowledge. For example, businesses are increasingly sourcing strategic knowledge via cloud computing, big data and business analytics (Venkitachalam and Schiuma Citation2022). Without digital technologies, emerging new scientific knowledge, such as bioinformatics and genomics, would not be possible (Dougherty and Dunne Citation2012). Digitalization has enhanced open innovation, particularly crowdsourcing new ideas (Acar Citation2019). Thus, digitalization has significantly transformed the innovation function, opening for businesses new ideas for search and recombination (Lanzolla et al., Citation2021). The emergence of collaborative digital platforms has facilitated interactive innovation between emerging young firms, Big-Tech firms, and customers who play a vital role in influencing firms’ product design and functionality (Nambisan et al. Citation2019). This new perspective shows that an innovation ecosystem rather than new technology-based firms or large firms per se drive innovation. In other words, Big-Tech firms, such as Google or Apple, interact with small technology-based firms (such as software companies developing apps for Apple products), which innovate based on large firms’ technology platforms (Mandel Citation2011). Whether used inside firms, across supply chains or as building blocks of new industrial architectures, the emergence of platforms is a broad recent phenomenon affecting most industries, from products to services (Gawer, Citation2014). For example, E-commerce platforms may enhance upscaling of young firms operating in R&D-intense industries, helping them test novel products on a more extensive set of potential customers (Nambisan Citation2017; Nambisan et al. Citation2019). This may be particularly critical to young firms as they mature, which leads to our next hypothesis.

Hypothesis 2b:

Digital capabilities complement innovation capabilities in stimulating young firms’ growth.

Following Bruno, Korosteleva, et al. (Citation2021), complementarities are expected between digital capabilities and investment in fixed capital (tangibles) to enhance firm growth. Digital capabilities may work as a pre-condition or accelerator for tangible capital to shape firms’ growth in industries with low tangible capital intensity, like services, and high tangible capital intensity sectors like metal manufacturing. Distance matters for the latter, and reaching a broader customer base via a well-developed infrastructure is crucial.

Using firm-level data from the European Investment Survey data, covering 27 EU countries and the UK over the period 2016–2019, Thum-Thysen et al (Citation2017, Citation2021). find that complementarities between tangible capital investments, software (intangible digital investments) and training of employees (intangible human capital investments) played the critical growth-enhancing role. Synergies between investments in fixed capital, intangible assets such as new computer software and human capital enable the development of new organizational structures and business models, facilitating firm-level and macro-economic growth (Thum-Thysen et al. Citation2017; Thum-Thysen, Voigt, and Weiss Citation2021).

As firms develop the necessary physical infrastructure (e.g. ICT hardware) and invest in software and databases, these complementarities generate efficiency gains. Without the latter, it will not be possible to reap further benefits from intangible digital investments (Kim et al. Citation2008). Finally, the digital sector is also expected to have a positive so-called ‘yeast’ growth effect, spreading across other sectors in the longer run (Van Ark, de Vries, and Erumban Citation2021).

Thus, our next hypothesis reads as follows:

Hypothesis 2c:

Digital capabilities reinforce the impact of tangible capital on young firms’ growth.

2.3. Entrepreneurial growth and marketstructure

A market structure may affect entrepreneurial growth through incentives for firms to engage in R&D activities. However, there is no simple relationship between market structure and innovation (Acemoglu, Aghion, and Zilibotti Citation2006; Aghion et al. Citation2009). Aghion and Howitt (Citation2006) show an inverted-U relationship, so only a certain degree of competition positively induces innovative behaviour. Competition may be conducive to growth on the technology frontier but not necessarily behind the frontier (ibid).

On the one hand, concentrated market structures represent barriers to new entrants through economies of scale enjoyed by established incumbents benefitting from lower average costs (due to absolute cost advantages), making them more competitive vis-à-vis new entrants. Incumbents might also enjoy temporally bounded quasi-monopoly power in more concentrated markets via intellectual property protection of products, services, and business models. Digitalisation may help overcome these barriers by reducing young firms’ entry and operating costs (Autio et al. Citation2018) and may allow them to reach out to a broader customer base via e-platforms (Nambisan, Citation2017; Nambisan et al. Citation2017). However, this may not be sufficient to counteract the effect of incumbents’ monopoly rents via their substantial intellectual property assets in concentrated markets.

Conversely -on the other hand- fierce competition in innovation frontier industries can lead to higher innovation rates and faster growth as new innovative entrants challenge the power of incumbents, forcing them to ‘escape competition’ by innovating (Schumpeter Citation2008, Schumpeter 1942, Aghion and Akcigit Citation2017; Aghion, Akcigit, and Howitt Citation2015). Digital capabilities could further reinforce this effect in more competitive industries, increasing the scope for architectural innovation via open innovation platforms (Acar Citation2019; Lanzolla, Citation2021). Hence, our last third hypothesis reads as follows.

Hypothesis 3:

Digitalisation and other sectoral capabilities affect young firms’ growth differently under different market structures:

(H3a)

in a more competitive sectoral environment, digital and other sectoral capabilities are likely to complement each other in facilitating young firms’ growth;

(H3b)

in more concentrated environments, the scope for digital capabilities to enhance/complement the effects of other sectoral knowledge-related capabilities is reduced. In other words, digital capabilities can instead replace/substitute other capabilities to partly mitigate incumbents’ power, but they will not be sufficient to enhance young firms’ growth in more concentrated markets.

Our theoretical framework is summarized in .

Figure 1. A conceptual framework of entrepreneurial growth: Sectoral capabilities, complementarities and market structure.

3. Data and methodology

3.1. Sample and variable description

To address our research questions, we construct a firm-industry longitudinal dataset across the EU countries for 2010–2018, based on the Amadeus database provided by the BvD®, the major commercial source of internationally comparable data on firms. The data on sectoral indicators employed for constructing sectoral capabilities are obtained from the EU KLEMS dataset, which contains rich information on capital formation and employment indicators for all EU member states at the industry level (for the data construction issues and methodology, see Stehrer et al. Citation2019). The EU KLEMS database is run by the Vienna Institute for International Economics Studies (wiiw), and the European Commission funds the data updates.

We limit our sample to entrants, referred to hereafter as young firms, defined following Shan’ et al. (Citation1994) approach. More specifically, we define a firm’s entry the year we observe it for the first time in our sample (i.e. the year of incorporation is equal to the year of a firm’s first observation in our sample). We further mark these young firms throughout the whole period to observe them as they mature. Overall, our final sample of young firms has 13,899 firm-year observations. Their age ranges from zero (i.e. these are young firms that we observe entering for the first time in 2010) to eight years old. More specifically, the age distribution of young firms varies as follows: less or equal to 2 years old: 4,427 firm-year observations; 3 yrs-old: 2,874 firm-year observations; 4 yrs-old: 2,527 firm-year observations; 5-yrs old: 1,990 observations; and greater than 5 yrs old: 2,081 observations. reports descriptive statistics for the whole sample of young firms, whereas reports the correlation matrix.

Table 1. Descriptive statistics and definitions of explanatory factor variables, controls and dependent variables.

Table 2. Correlation matrix.

3.2. Methodology

Our empirical strategy is twofold. First, we identify a set of sectoral-level capabilities supportive of knowledge generation and transfer within sectors, using EU KLEMS sectoral capital structure indicators. More specifically, we propose four pillars of innovation ecosystems at a sectoral level, namely:

digital capabilities, defined by the share of computer software and databases in capital stock netFootnote1;

human capital capabilities, defined as the sum of shares of hours worked by males and females with higher education;

innovation capabilities, defined by the share of Research and Development in Capital stock net;

tangible capital capabilities, defined as a sum of shares of Transport Equipment in Capital stock net and shares of Other Machinery and Equipment in Capital stock net.Footnote2

Second, the regression analysis explores young firms’ growth patterns as they mature, conditional on sectoral capabilities and their interplay. Young firms’ growth is measured as a rate of change in turnover (producer price index adjusted), which is a well-established measure of young firms’ growth in the literature (Nason and Wiklund Citation2018). We employ a standard set of controls in a firm turnover growth model, including a firm’s a lagged level of turnover, expressed in logarithmic form, to control for lagged temporal patterns, firm’s age, size (lagged by one year), and market concentration at a sector-country, and sector-EU levels.

Our model of direct and complementary effects of sectoral capabilities via pairwise interaction channels is specified as follows:

dLN (yit) = α0 + β0LN (yit-1) + β1 (Digital)st + β2 (HumCapital)st +β3 (R&D)st + β4 (TangibleCap)st + β5(Digital)#(R&D)st + β6(Digital)#(HumCapital)st + β7(Digital)#(TangibleCap)st + β8(HumCapital)#(R&D)st + β9(HumCapital)#(TangibleCap)st + β10(R&D)#(TangibleCap)st + ZXit-1 + µZst + Dt + ϕi +εi sct (1)

where dLN (yit) is the dependent variable proxied by a turnover growth rate of change; sectoral capabilities are self-explanatory in the model; ZXit-1 denotes a vector of firm-level controls; Zst stands for industry-level controls; Dt – year controls; and ϕi – firm-level fixed controls, εisct is the idiosyncratic error. Subscripts i,s,c,t stand for i-firm; s-sector; c-country; t- time.

In addition, we extend the analysis further to study the impact of sectoral capabilities and their interactions in a 2-digit sector-country market structure. For this, firstly, we construct a dummy variable to measure market concentration with zero denoting low market concentration, measured as below a mean threshold for every 2-digit sector, and 1 indicating high market concentration (above or equal to a mean threshold for the respective 2-digit industry). In this way, we allow market concentration to vary across industries. Appendix A Table A.1 reports descriptive statistics for market concentration within sector-countries. Second, we split the sample into two sub-samples characterized by low and high levels of market concentration.

4. Empirical results

We summarize our results in , where column 1 reports the direct effects of digitalization and other sectoral capabilities on young firms’ growth. Column 2 shows the results with added pairs of interacted sectoral-level capabilities jointly with the age of young firms. Columns 3 and 4 extend these results further under low and high market concentration structures. All results include a complete set of firm-level and sectoral controls: firm age, size, market concentration within sector-country and sector-EU, and firm and year fixed effects dummies.

Table 3. Direct and complementary effects of sectoral capabilities in interaction with young firms’ age and under different market structures.

Analysing the results, in column (1) of , we first observe that digitalization has a direct positive effect on young firms’ growth which is statistically significant at a 1% significance level. Therefore, we accept Hypothesis 1. Among other sectoral capabilities, human capital capabilities constrain young firms’ growth. Neither innovation capabilities nor tangible capital influence young firms’ performance autonomously.

Next, we consider the complementarities between digitalization and other sectoral capabilities by a young firm’s age (regressions from column (2) ). First, in , we note the lack of significance in the complementarity between digital and human capital capabilities. Thus, we reject Hypothesis 2a.

Figure 2. The impact of Human Capital capabilities conditional on digitalization on turnover growth rate by young firm age.

Digital capabilities have a differential impact on young firms’ growth, conditional on their maturity stage. When firms are at their early stage of maturity (from 2 to 4 years old), there is a lack of complementarity between innovation capabilities and digitalization in sectors of low or moderate R&D capabilities. Still, this relationship reverses as young firms mature, particularly enhancing the impact of innovation (R&D) capabilities for more mature young firms (7- yrs old) operating in more intense R&D environments (). This result shows a dual effect of digitalization. On the one hand, it hampers innovation-led growth prospects for young firms when they are still immature and lack the skills to utilize their digital tools to commercialize their ideas efficiently. On the other hand, it broadens knowledge to search for young firms once they mature and can engage in a more effective process of recombining ideas presented by digital capabilities (see also Lanzolla et al., Citation2021). Overall, these findings support Hypothesis 2b for more mature young firms.

Figure 3. The impact of Innovation Capabilities conditional on digitalization on turnover growth rate by young firm age.

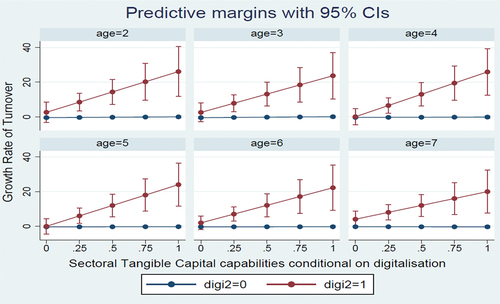

We also find a strong supporting role for Hypothesis 2c, with digitalization enhancing the benefits of more intense tangible capital contexts, allowing young firms to upscale faster. This effect holds for all stages of young firms’ development and strengthens with young firms’ maturity ().

Figure 4. The impact of Tangible Capabilities conditional on digitalization on turnover growth rate by young firm age.

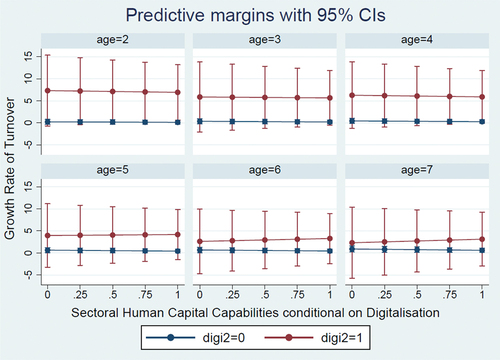

We also observe some interesting patterns of the impact of digital sectoral capabilities and their interplay with other sectoral pillars on entrepreneurial upscaling, depending on market concentration at a sector-country level. We observe a lack of complementarity between human capabilities and digitalization in more competitive environments (). This is the case either at a very young age or at a more mature stage of the firm’s existence (7 yrs old). This lack of complementarity emerges as a bottleneck for entrepreneurs at a crucial stage of their life cycle, i.e. when they bottle for survival or to gain a higher market share, challenging their competitors. Overall, this supports the Berlingieri et al. (Citation2020) argument of the failure of the young firm to benefit from advances in digital technologies due to skills mismatch.

Figure 5. The impact of Human Capabilities, conditional on digitalization, on turnover growth rate by young firm age under low market concentration.

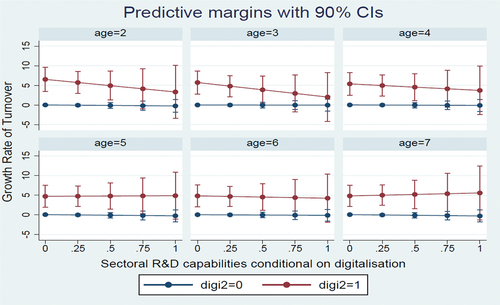

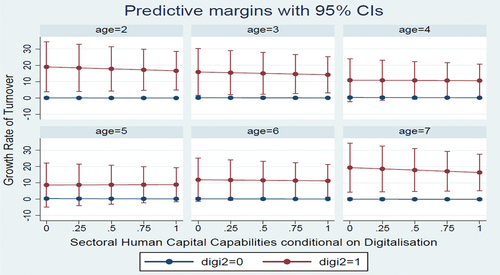

As young firms mature, a positive complementary effect of a rising R&D intensity and digitalization strengthens for young firms operating in more competitive market environments, reinforcing growth-enhancing benefits of a broader search for new opportunities and recombining ideas for younger firms ().

Figure 6. The impact of Innovation Capabilities, conditional on digitalization, on turnover growth rate by young firm age under low market concentration.

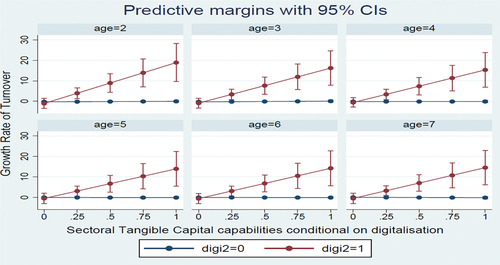

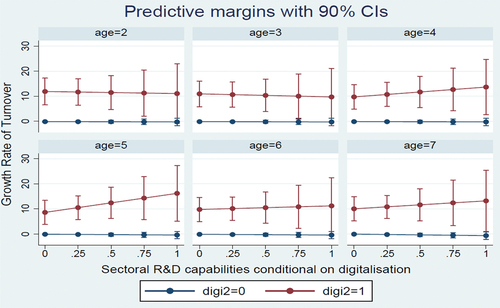

Finally, we find a strong supporting role of digitalization in the environments intense in tangible capital investments, but this only holds in the context of competitive environments, with the magnitude of the effect growing as young firms mature with age (). The complementarity between digital and tangible capital suggests that these are most likely advantages that stem from the digitalization of routinized tasks, leading to higher growth.

Figure 7. The impact of Tangible Capabilities, conditional on digitalization, on turnover growth rate by young firm age under low market concentration.

We find no significant interrelations between digital and other sectoral capabilities under high market concentration, so we support Hypotheses 3a and 3b.

Turning now to the analysis of controls, the negative and significant coefficient of the lagged level of turnover implies faster growth for young firms with a lower initial level of turnover, which is in line with the theoretical expectations. Moreover, we have some evidence of a non-linear (U-shaped) relationship between firm age and turnover growth, indicating their ability to bounce back as they mature beyond three years. Young firms’ first three years of life are the most critical as they are bottling for survival (see Parker Citation2018). This reiterates the importance of the sectoral eco-innovation system and its role in smoothing young firms’ erratic growth. In particular, digitalization creates more persistent companies in the medium and long run. We find a positive association between size, measured by the initial level of employment, and ’ the firm’s growth. Higher firm concentration at the country sectoral level shows a fragmentary marginal positive effect (at a 10% level of significance) on young firms’ growth when examining the direct effect results of sectoral capabilities (Columns (1–2) ). However, this effect disappears once we explore them under different market structures.

5. Discussion and conclusions

This study explored the entrepreneurial growth process and how digitalization and other sectoral capabilities, vital for knowledge generation and diffusion at an industry level, shape this growth process and strengthen young firms’ resilience. This research question also considers different market structures and how they further shape synergies and trade-offs.

We argue that understanding digitalization’s direct impact on young firms’ growth requires focusing on their performance over time. Within each stage of their development, young firms experience both short-lived high growth and a decline (rebounds and slumps), given their vulnerability to potential shocks and changes in the environment, the newness of products, and the competitive environment. Once young firms reach the age of seven, they enter a steadier growth path. This study shows how digitalization alone and combined with other sectoral capabilities helps them adapt to the changes in their vibrant sectoral environment.

Following Nason and Wiklund (Citation2018), we employ a turnover growth rate, regarded as one of the established measures to capture young firms’ scaling process. We assemble a sizable firm-sector level dataset covering EU young firms for 2010–2018 and merge it with EU KLEMS structural indicators of capital to identify sectoral capabilities crucial for knowledge generation, acquisition and exchange. We further employ regression techniques to answer our research questions.

Our results show that digital sectoral capabilities, autonomously and in synergies with other sectoral capabilities, enhance young firms’ growth as they mature. The complementarities between digital and other sectoral capabilities show the critical role digital capabilities play in facilitating the effect of R&D. This is particularly the case as young firms mature, and more so in contexts high in tangible capital investments. Furthermore, we also show that the moderating effect of digitalization varies depending on the level of competition. Its complementary growth-enhancing role is more decisive in more competitive environments, specifically supporting young firms as they mature and counteracting the effect of lower innovative capabilities on their growth at their early stage of operation.

Our study also shows that the mismatch of skills and digital advances impedes young firms’ growth, especially at the early stage of firms’ existence, but also at the later stage of their maturity, when lack of skills appears to hamper young firms’ prospects for upscaling under competitive market structures.

The results on complementarities of sectoral capabilities generate important policy implications. In particular, our results are relevant for digitalization, knowledge diffusion, growth of firms and competition policies. For example, EU growth has slowed over the decade following the global financial crisis, including diminishing technological opportunities and the stagnation of small-scale firms (Castellani et al. Citation2018; Berlingieri et al. Citation2020). Therefore, focusing on the performance of young firms as they mature and conditioning this on digitalization, the intensity of knowledge generation, acquisition and exchange within young firms’ immediate (sectoral) environments may offer potential solutions to reverse the stagnation of small firms and strengthen their resilience. For policy-makers, it would be crucial to provide support tailored to young firms’ needs depending on the stage of their development, the sectors they operate in, and market conditions. While promoting digitalization benefits young firms overall, it has a more pronounced effect in a more competitive environment. This is especially the case for young firms operating in high-intense tangible capital investment environments and mature young firms in more intense R&D contexts.

Our results suggest that general horizontal policy solutions favouring a specific type of capabilities in isolation, be they R&D, digital or tangible investments, may have limited or even counterproductive effects. Instead, policy should target a portfolio of capabilities and consider their complementarities. Moreover, the overall approach should be tailor-made, including understanding different stages of young firms’ development and the market structure features of the individual sectors.

Disclosure statement

No potential conflict of interest was reported by the authors.

Correction Statement

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes

1. Provisionally, we considered both tangible and intangible dimensions of digital capabilities along with other knowledge related sectoral capabilities, exploring interdependences between them, using a factor analysis. Tangible digital capabilities, measured as share of computing equipment in gross fixed capital formation and net capital stock, have not loaded significantly to any of the four knowledge related pillars (Bruno, Korosteleva, et al. Citation2021), so we do not consider computing equipment for further analysis in this study, and we focus only on intangible ICT (Software and Databases). This is also in line with Adarov and Stehrer (Citation2020) who emphasize more important role played by intangible ICT capital in boosting growth in the EU over the period of 2000–2007.

2. For robustness checks we have also used similar indicators but for digital, innovation and tangible capital capabilities, expressed as share of Gross Fixed Capital Formation (GFCF). The results are available upon request from authors.

3. Note, in reported figures digi2 legend stands for Digital.

References

- Abidi, N., M. El Herradi, and S. Sakha, 2022. Digitalisation and Resilience: Firm-Level Evidence During the COVID-19. IMF Working Paper Volume , Issue 34. Publication date 18 February. Publication: Washington D.C. Available from https://www.elibrary.imf.org/view/journals/001/2022/034/001.2022.issue-034-en.xml?rskey=W1zfpA&result=1

- Acar, O. A. 2019. “Motivations and Solution Appropriateness in Crowdsourcing Challenges for Innovation.” Research Policy 48 (8): 103716. https://doi.org/10.1016/j.respol.2018.11.010.

- Acemoglu, D., P. Aghion, and F. Zilibotti. 2006. “Distance to Frontier, Selection, and Economic Growth.” Journal of the European Economic Association 4 (1): 37–74. April 2006. https://doi.org/10.1162/jeea.2006.4.1.37.

- Adarov, A., and R. Stehrer, 2020. New Productivity Drivers: Revisiting the Role of Digital Capital, FDI and Integration at Aggregate and Sectoral Levels (No. 178). Vienna (Austria): Vienna Institute for International Economic Studies (WIIW).

- Aghion, P., and U. Akcigit. 2017. “Innovation and growth: the Schumpeterian perspective.” In ‘Economics without Borders’, Ch.1, edited by P. Aghion and U. Akcigit, 29–72. Cambridge: Cambridge University Press. https://doi.org/10.1017/9781316636404.003

- Aghion, P., U. Akcigit, and P. Howitt. 2015. “Lessons from the Schumpeterian Growth Theory.” The American Economic Review 105 (5): 94–99. https://doi.org/10.1257/aer.p20151067.

- Aghion, P., P. Askenazy, R. Bourlès, G. Cette, and N. Dromel. 2009. “Education, Market Rigidities and Growth.” Economics Letters 102 (1): 62–65. https://doi.org/10.1016/j.econlet.2008.11.025.

- Aghion, P., and P. Howitt. 2006. “Appropriate Growth Policy: A Unifying Framework.” Journal of the European Economic Association 4 (2–3): 269–314. https://doi.org/10.1162/jeea.2006.4.2-3.269.

- Andreoni, A. 2017. Industrial Ecosystems and Policy for Innovative Industrial Renewal: A New Framework and Emerging Trends in Europe. London: SOAS University of London.

- Audretsch, D. B. 1995. Innovation and Industry Evolution. Cambridge, Massachusetts; London, England: MIT Press.

- Audretsch, D. B., and M. Belitski. 2021. “Knowledge Complexity and Firm Performance: Evidence from the European SMEs.” Journal of Knowledge Management 25 (4): 693–713. https://doi.org/10.1108/JKM-03-2020-0178.

- Audretsch, D. B., and M. Keilbach. 2007. “The Theory of Knowledge Spillover Entrepreneurship.” Journal of Management Studies 44 (7): 1242–1254. https://doi.org/10.1111/j.1467-6486.2007.00722.x.

- Audretsch, D. B., and M. Keilbach. 2008. “Resolving the Knowledge Paradox: Knowledge-Spillover Entrepreneurship and Economic Growth.” Research Policy 37 (10): 1697–1705. https://doi.org/10.1016/j.respol.2008.08.008.

- Autio, E., S. Nambisan, L. D. Thomas, and M. Wright. 2018. “Digital Affordances, Spatial Affordances, and the Genesis of Entrepreneurial Ecosystems.” Strategic Entrepreneurship Journal 12 (1): 72–95. https://doi.org/10.1002/sej.1266.

- Belitski, M., J. Korosteleva, and L. Piscitello. 2021. “Digital Affordances and Entrepreneurial Dynamics: New Evidence from European Regions.” Technovation. https://doi.org/10.1016/j.technovation.2021.102442.

- Berlingieri, G. 2020. Laggard Firms, Technology Diffusion and Its Structural and Policy Determinants. OECD Science, Technology and Industry Policy Papers, No. 86, OECD Publishing: Paris. https://doi.org/10.1787/281bd7a9-en

- Breschi, S., and F. Malerba. 1997. “Sectoral Innovation Systems: Technological Regimes, Schumpeterian Dynamics, and Spatial Boundaries.” Chap. 6 In Systems of Innovation: Technologies, edited by C. Edquist, 130–156, Routledge: Milton Park, Abingdon, Oxon, UK: Institutions and Organisations. Routledge.

- Bruno, R.L., Douarin, E., Korosteleva, J. and Radosevic, S., 2022. The two disjointed faces of R&D and the productivity gap in Europe. JCMS: Journal of Common Market Studies. Journal of Common Market Studies, 60(3), pp.580–603.

- Bruno, R., J. Korosteleva, K. Osaulenko, and S. Radosevic, 2021. Sectoral Innovation Systems, Complementarities and Productivity in Europe, GROWINPRO WP 61. Available: http://www.growinpro.eu/sectoral-innovation-systems-complementarities-and-productivity-in-europe/.

- Carol, C., J. Haskel, and C. Jona-Lasinio. 2017. “Knowledge Spillovers, ICT and Productivity Growth,” Oxford Bulletin of Economics and Statistics.” Department of Economics, University of Oxford 79 (4, August): 592–618. https://doi.org/10.1111/obes.12171.

- Castellani, D., M. Piva, T. Schubert, and M. Vivarelli. 2018. “Can European Productivity Make Progress?” Intereconomics 53 (2): 75–78. https://doi.org/10.1007/s10272-018-0725-8.

- Cirera, X., D. A. Comin, M. Cruz, K. Lee, T. Coronado, and Jesica. 2022. Technology and Resilience. Washington, DC: World Bank. https://doi.org/10.1596/1813-9450-9949.

- Criscuolo, C., P. Gal, T. Leidecker, and G. Nicoletti, 2021. The Human Side of Productivity: Uncovering the Role of Skills and Diversity for Firm Productivity, OECD Productivity Working Papers, No. 29, OECD Publishing, Paris, 10.1787/5f391ba9-en.

- Demir, R., K. Wennberg, and A. McKelvie. 2017. “The Strategic Management of High-Growth Firms: A Review and Theoretical Conceptualisation.” Long Range Planning 50 (4): 431–456. https://doi.org/10.1016/j.lrp.2016.09.004.

- DeYoung, R., W. S. Frame, D. Glennon, and P. Nigro. 2011. “The Information Revolution and Small Business Lending: The Missing Evidence.” Journal of Financial Services Research 39 (1–2): 19–33. https://doi.org/10.1007/s10693-010-0087-2.

- Estrin, S., Korosteleva, J. and Mickiewicz, T., 2022. Schumpeterian entry: innovation, exporting, and growth aspirations of entrepreneurs. Entrepreneurship Theory and Practice, 46(2), pp.269–296.

- Gambacorta, L., Y. Huang, Z. Li, H. Qiu, and S. Chen. 2022. “Data versus Collateral.” Review of Finance 27 (2): 369–398. https://doi.org/10.1093/rof/rfac022.

- Gawer, A. 2014. “Bridging Differing Perspectives on Technological Platforms: Toward an Integrative Framework.” Research Policy 43 (7): 1239–1249. https://doi.org/10.1016/j.respol.2014.03.006.

- Griffiths, R., S. Redding, and J. V. Reenen. 2004. “Mapping the Two Faces of R&D: Productivity Growth in a Panel of OECD Industries.” The Review of Economics and Statistics 86 (4): 883–895. https://doi.org/10.1162/0034653043125194.

- Iacobucci, D., and F. Perugini. 2021. “Entrepreneurial Ecosystems and Economic Resilience at Local Level.” Entrepreneurship & Regional Development 33 (9–10): 689–716. https://doi.org/10.1080/08985626.2021.1888318.

- Jagtiani, J., and C. Lemieux. 2018. “Do Fintech Lenders Penetrate Areas That are Underserved by Traditional Banks?” Journal of Economics and Business 100: 43–54. https://doi.org/10.1016/j.jeconbus.2018.03.001.

- Kenney, M., and J. Zysman. 2016. “The Rise of the Platform Economy.” Issues in Science and Technology 32 (3): 61.

- Ketchen, D., R. Ireland, and C. Snow. 2007. “Strategic Entrepreneurship, Collaborative Innovation, and Wealth Creation.” Strategic Entrepreneurship Journal 1 (3–4): 371–385. https://doi.org/10.1002/sej.20.

- Kim, Y. J., H. Kang, G. L. Sanders, and S. Y. T. Lee. 2008. “Differential Effects of IT Investments: Complementarity and Effect of GDP Level.” International Journal of Information Management 28 (6): 508–516. https://doi.org/10.1016/j.ijinfomgt.2008.01.003.

- Lanzolla, G., D. Pesce, and C. L. Tucci. 2021. “The Digital Transformation of Search and Recombination in the Innovation Function: Tensions and an Integrative Framework.” Journal of Product Innovation Management 38 (1): 90–113.

- Li, W., K. Liu, M. Belitski, A. Ghobadian, and N. O’Regan. 2016. “E-Leadership Through Strategic Alignment: An Empirical Study of Small-And Medium-Sized Enterprises in the Digital Age.” Journal of Information Technology 31 (2): 185–206. https://doi.org/10.1057/jit.2016.10.

- Malerba, F. 2002. “Sectoral Systems of Innovation and Production.” Research Policy 31 (2): 247–264. https://doi.org/10.1016/S0048-7333(01)00139-1.

- Malerba, F.2005How Innovation Differs Across Sectors: Sectoral Systems of Innovation Handbook of Innovation FagerbergMowery, NelsonedOxford University Presshttps://doi.org/10.1017/CBO9780511493270.002

- Malerba, F., and F. Malerba. 2004. Sectoral Systems of Innovation. Cambridge University Press. https://doi.org/10.1017/CBO9780511493270.

- Mandel, M., 2011. Scale and Innovation in Today’s Economy, Progressive Policy Institute, Policy Memo, December. Available from: http://progressivepolicy.org/wp-content/uploads/2011/12/12.2011-Mandel_Scale-and-Innovation-in-Todays-Economy.pdf, last accessed September 26, 2014.

- Mason, C., and M. Hruskova2021The Impact of COVID-19 on Entrepreneurial EcosystemsProductivity and the PandemicEdward Elgar Publishinghttps://doi.org/10.4337/9781800374607.00011

- McKelvie, A., A. Brattström, and K. Wennberg. 2017. “How Young Firms Achieve Growth: Reconciling the Roles of Growth Motivation and Innovative Activities.” Small Business Economics 49 (2): 273–293. https://doi.org/10.1007/s11187-017-9847-9.

- Nambisan, S. 2017. “Digital Entrepreneurship: Toward a Digital Technology Perspective of Entrepreneurship.” Entrepreneurship: Theory & Practice 41 (6): 1029–1055. https://doi.org/10.1111/etap.12254.

- Nambisan, S., K. Lyytinen, A. Majchrzak, and M. Song. 2017. “Digital Innovation Management: Reinventing Innovation Management Research in a Digital World.” MIS Quarterly 41 (1): 223–238. https://doi.org/10.25300/MISQ/2017/41:1.03.

- Nambisan, S., M. Wright, and M. Feldman. 2019. “The Digital Transformation of Innovation and Entrepreneurship: Progress, Challenges and Key Themes.” Research Policy 48 (8): 103773. https://doi.org/10.1016/j.respol.2019.03.018.

- Nason, R. S., and J. Wiklund. 2018. “An Assessment of Resource-Based Theorising on Firm Growth and Suggestions for the Future.” Journal of Management 44 (1): 32–60.

- Parker, S. C. 2018. “The Economics of Entrepreneurship“Cambridge University Press.Shanhttps://doi.org/10.1017/9781316756706

- Schumpeter, J. A. 2008[1934]. The Theory of Economic Development. New Brunswick, NJ: Transaction Publishers.

- Shan, W., G. Walker, and B. Kogut. 1994. “Interfirm Cooperation and Startup Innovation in the Biotechnology Industry.” Strategic Management Journal 15 (5): 387–394.

- Stehrer, R., A. Bykova, K. Jäger, O. Reiter, and M. Schwarzhappel, 2019. Industry Level Growth and Productivity Data with Special Focus on Intangible Assets. Report on Methodologies and Data Construction for the EU KLEMS Release 2019. Vienna (Austria): The Vienna Institute for International Economic Studies (WIIW). https://euklems.eu/wp-content/uploads/2019/10/Methodology.pdf

- Thomas, L. D., E. Autio, and D. M. Gann. 2014. “Architectural Leverage: Putting Platforms in Context.” Academy of Management Perspectives 28 (2): 198–219. https://doi.org/10.5465/amp.2011.0105.

- Thum-Thysen, A., P. Voigt, B. Bilbao-Osorio, C. Maier, and D. Ognyanova. 2017. “Unlocking Investment in Intangible Assets.” Quarterly Report on the Euro Area (QREA) 16 (1): 23–35.

- Thum-Thysen, A., P. Voigt, and C. Weiss, 2021. Complementarities in Capital Formation and Production: Tangible and Intangible Assets Across Europe (No. 2021/12). The European Investment Bank.

- Van Ark, B., N. N. de Vries, and A. Erumban. 2021. “How to Not Miss a Productivity Revival Once Again.” National Institute Economic Review 255: 9–24. https://doi.org/10.1017/nie.2020.49.

- Venkitachalam, K., and G. Schiuma. 2022. “Strategic Knowledge Management (SKM) in the Digital Age–Insights and Possible Research Directions.” Journal of Strategy and Management 15 (2): 169–174.

- Yoo, Y., O. Henfridsson, and K. Lyytinen. 2010. “The New Organising Logic of Digital Innovation: An Agenda for Information Systems Research.” Information Systems Research 21 (4): 724–735. https://doi.org/10.1287/isre.1100.0322.

Appendix A

Table A1. Descriptive statistics of Market Concentration index by sector of economic activity (NACE rev.2).