ABSTRACT

Financial technology (FinTech) is widely recognised as important in addressing financial inclusion. However, limited research theorises how new entrants and incumbents work together in FinTech ecosystems to shape financial inclusion. We undertake a theory-generating case study with multilevel interacting organisations in Ghana, where, like many other African countries, the growth in FinTech has led to new opportunities for financial inclusion. We conceptualise three practices, as building blocks at the ecosystem level, through which incumbents and new entrants shape financial inclusion: (1) innovative and collaborative practices, (2) protectionist and equitable practices, and (3) legitimising and sustaining practices. We articulate a theoretical model that explains how the practices shape financial inclusion and propose three theoretical propositions of how financial inclusion in developing countries is being scaled and shaped in terms of actors, relationships, and practices.

SPECIAL ISSUE EDITORS:

1. Introduction

Globally, nearly a quarter of adults do not have access to a basic bank account (Demirgüç-Kunt et al., Citation2018) due to the high cost of services, lack of access and trust in banks, distance to a financial institution, and challenges in obtaining identification documentation (Senyo et al., Citation2020). The lack of access to formal instruments for savings or borrowing compounds poverty, because the ability to save, borrow and exchange money is key in helping to escape poverty. However, access to financial services gives individuals the opportunity to be paid and to pay and improve their quality of life (Demirgüç-Kunt et al., Citation2018). Thus, financial inclusion, defined as where “individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit and insurance – delivered in a responsible and sustainable way” (World Bank, Citation2018), is fundamental to alleviating poverty (Demirgüç-Kunt et al., Citation2018).

In the last 15 years, there has been a move to examine “how banks can translate the potential of mobile phones into greater financial access for poor people” (CGAP, Citation2008: 1). This has shifted from the role of banks, to include a wider network of technology, entrepreneurial and start-up financial technology firms (known as “FinTech firms”) that offer novel digital financial services as alternatives to traditional banking services. FinTech describes the application of technology to provide new and improved financial services (Gomber et al., Citation2018). In developing countries, mobile money, a FinTech innovation that enables financial transactions without a bank account, is improving financial inclusion (Senyo & Osabutey, Citation2020).

Mobile money solutions, such as M-Pesa in Kenya (e.g., Oborn et al., Citation2019), have reduced the number of households in poverty. Other solutions, such as Oi Paggo in Brazil and TCASH in Indonesia (e.g., Iman, Citation2018), demonstrate how contextually relevant solutions provide customers newer, cheaper, easier, faster and more efficient ways of storing and transferring value. Complex relationships between “old” firms such as banks and “new” firms such as telecommunication companies (telcos) and FinTech firms (Gozman et al., Citation2018) are required to co-create these innovative services.

However, these examples have proven difficult to replicate in other developing countries and many people remain financially excluded (Demirgüç-Kunt et al., Citation2018). Despite the growing research on FinTech, and in particular mobile money, the majority of the studies focus on individual adoption issues such as antecedents, drivers and inhibitors (e.g., Senyo & Osabutey, Citation2020), users’ perception and cultural barriers (e.g., Bongomin et al., Citation2019). Studies at the organisational level tend to examine FinTech firms as a phenomenon (e.g., Gozman et al., Citation2018; Leong et al., Citation2017; Oshodin et al., Citation2019) or how banks respond to disruption by FinTech firms (e.g., Gomber et al., Citation2018), rather than how these actors resolve the tensions behind financial exclusion. An area that remains under-theorised is how meso-level actors and macro-level institutions (Walsham & Sahay, Citation2006) combine to shape financial sector practices to address financial inclusion. We address the research question: How does the interplay between “new” and “old” actors shape financial sector practices to address financial inclusion? We undertake a multilevel qualitative theory-generating case study with interacting organisations in Ghana.

In the ensuing sections, we first present the theoretical background, then our methodology. We then present the research findings, followed by a discussion of the theoretical and practical contributions, limitations and research directions.

2. Theoretical background

2.1. FinTech as a new ecosystem

FinTech innovations, such as mobile money, operate in an ecosystem of heterogenous actors that compete and cooperate to achieve a common goal (Lagna & Ravishankar, Citation2021; Lee & Shin, Citation2018; Muthukannan et al., Citation2020). Innovation ecosystems typically have one, or several, focal entities that help to define boundaries and coordinate between autonomous organisations (Jacobides et al., Citation2018; Senyo et al., Citation2019). Jacobides et al. (Citation2018) suggest that innovation ecosystems have multilateral non-generic complementarities which are the unique capabilities of actors and are not unilaterally hierarchically controlled.

In a FinTech ecosystem, new and old actors combine to offer unique capabilities that complement one another and contribute to innovation (Lagna & Ravishankar, Citation2021; Lee & Shin, Citation2018; Muthukannan et al., Citation2020). Lee and Shin (Citation2018) identify five interacting actors in the FinTech ecosystem: FinTech firms, offering technology mediated payments, wealth management, lending, crowdfunding, capital market and insurance services; technology developers such as big data analytics, cloud computing, blockchain and social media developers creating digital solutions; government actors including financial regulators and legislature creating a stable regulatory environment; financial customers, who use and benefit from the services; and traditional financial institutions such as large commercial banks acting as the trusted custodians of money.

FinTech-driven business models challenge established financial sector incumbents and institutions in relationships, governance mechanisms, products, services and markets (Gozman et al., Citation2018). Incumbent financial institutions respond to protect their interests by reinventing their products, processes and business models (Drummer et al., Citation2017). As many incumbents are limited by legacy technologies and struggle to compete with the agility of FinTech firms, they must collaborate with them to access new technical capabilities or new markets and customers (Drummer et al., Citation2017). FinTech firms, in turn, rely on banks to access regulated markets and financial expertise and capital (Senyo & Karanasios, Citation2020).

These symbiotic relationships help overcome challenges of delivering services to the unbanked, such as the high levels of investment amidst long payback periods, challenges of scaling-up, inadequate financial infrastructure to allow interoperability between services and a proportionate regulatory framework that attracts investments from banks and other actors. The interplay between the new and old actors not only defines the boundaries of activity (Jacobides et al., Citation2018), but also shapes the direction of financial inclusion (Leong et al., Citation2017).

2.2. The Ghanaian FinTech ecosystem

The FinTech ecosystem in Ghana is complex and dynamic (Disrupt Africa, Citation2019) with interdependencies between actors that are more dynamic than outside of Africa. The actors include government actors such as telecommunication sector regulators and the central bank; traditional financial institutions; telcos; merchants; FinTech firms; agents; think tanks and development organisations; and users. shows the connections between the incumbents (solid line arrows) and new actors (broken line arrows).

Figure 1. The Ghanaian FinTech ecosystem.

An established actor is the Ghanaian central bank, referred to as the Bank of Ghana (BoG). The BoG regulates financial activities by providing policy and regulatory directions to mitigate systemic risk and provide consumer outcomes including financial inclusion (Senyo & Osabutey, Citation2020). The BoG views FinTech as a key enabler of financial inclusion and has set up a FinTech and innovation department, formulated e-money and digital financial services policies, introduced a payment system and services law (Act 987, 2019), and a FinTech licencing regime to regulate the ecosystem (Senyo et al., Citation2020).

Traditional financial institutions, including micro-savings and loans services organisations, were previously the sole providers of banking services to Ghanaians and were regulated by the BoG (Senyo et al., Citation2020). Now, they play the fundamental role of custodians of monies transacted on mobile money networks in addition to their core banking services since telcos are not licenced as independent financial institutions and cannot hold funds in the same way. For instance, each telco needs to have a partner bank to whom deposits in eFunds are transferred and held for safekeeping.

Telcos provide mobile money services through their mobile network platform. In Ghana, like much of Africa, telcos play a critical bridging role by providing the platform for citizens to access financial services. They often directly develop and provide the financial service (Iman, Citation2018) and are central in mobile money services (see ). To deliver mobile money-based financial services, FinTech firms and banks partner with the telcos. Likewise, although telcos also have limited brick and mortar offices, their partnerships with mobile money agents provide more access points. There are about 30 unique mobile money services in Ghana such as Qwikloan, Zeepay, G-money, Slydepay, and eTranzact.

Merchants are firms that accept mobile money payment for goods and services while FinTech firms develop digital financial services. FinTech firms enable electronic payment and seamless interoperability between actors and integration of electronic payments through mobile phones into many products and services. As a result, users are able to conduct financial transactions digitally.

Agents are actors contextually specific to developing countries in the delivery of financial services. In Ghana, agents are small firms, mostly one person, acting as “shadow bank branches” or “cash-in, cash-out” points and providing digital financial services such as cash deposit and withdrawals, mobile money transfer, airtime sales and mobile money registrations. Agents have helped increase financial inclusion in developing countries and support most communities with daily financial activities (Oborn et al., Citation2019). Other actors, such as think tanks, develop programmes to support financial and technology literacy and may help develop specific innovations and policies for the unbanked. Finally, individuals and businesses use mobile money to facilitate financial transactions such as money transfer, pay bills and school fees, purchase phone credit, data bundles, insurance services and electricity credits, make deposits and secure micro-loans. Hence, mobile money is gradually becoming a substitute for cash transactions.

3. Methodology

3.1. Research setting and design

To explain the complex interactions between technology, firms, structures, people, and contextually specific issues, we adopted a qualitative methodological orientation (Klein & Myers, Citation1999) and a case study design. Ghana, a middle-income African country, is ideal for our theorising in three ways. First, only 58 percent of the population has a bank account (Demirgüç-Kunt et al., Citation2018), meaning there is scope for mobile money to improve financial inclusion. Second, there is growing diffusion of mobile money services. Third, the number of actors such as banks, telcos, think tanks, FinTech firms and regulators suggests a complex environment offering new opportunities for financial inclusion (Disrupt Africa, Citation2019). In line with our qualitative inductive study design and our goal of developing new theory, we applied some grounded theory tenets, particularly those related to coding and theoretical sampling, which we describe in the next subsections.

3.2. Data collection

We conducted 29 semi-structured interviews across 17 organisations between 2019 and 2020. While most studies focus on a specific technology offering, such as M-Pesa (e.g., Oborn et al., Citation2019), the diversity of activity in Ghana demanded that we reflect on a range of technologies and actors. Our sampling included incumbent and new actors. As we conducted interviews, we shifted from purposive sampling to a more theoretical sampling (Glaser & Strauss, Citation1967) to build our ongoing theorising. For instance, as our coverage of large established actors grew, we focused more on organisations delivering innovation in financial inclusion. Data was collected with one or two researchers present and the research team frequently met for debriefings. We adopted an insider–outsider approach where the researchers reviewed the main themes emerging from the data to ensure rigour, trustworthiness and contextually specific understanding (Davison & Martinsons, Citation2016).

All interviews were semi-structured, tailored to each participant, conducted in English and lasted on average 50 minutes. Most interviews were conducted face-to-face, audio-recorded with interviewees’ permission, or comprehensive notes taken by the researchers, although some were by phone due to COVID-19 requirements. The interviews were structured around innovation, connections between organisations and how financial inclusion was being addressed. In line with inductive research, the questions changed to align with our emerging theorising. summarises the type of firms, focus for the study, years in operation, and interviewees role, providing breadth and depth across the Ghanaian FinTech ecosystem. Our sample is limited to organisations and institutions that develop, offer, promote or regulate FinTech services rather than users, agents or merchants who are beneficiaries.

Table 1. Details of study participants

3.3. Data analysis

Data was analysed in parallel with data collection to confidently reach theoretical saturation and adapt our theoretical sampling approach. This approach is valuable in generating theory in novel technology and organisational settings (e.g., Urquhart, Citation2016). While IS scholars outline overlapping approaches to a grounded theory analysis (see Urquhart, Citation2016), we follow the process (see Appendix A) of open, axial and selective coding (Corbin & Strauss, Citation1990), as is common where analysis and theorising is grounded in the data.

First, we conducted open coding by reviewing interview transcripts to elicit initial codes. Open coding helps become immersed in the data and understand the range of concepts discussed by interviewees. We also followed the principle of the constant comparative method whereby we compared and contrasted codes, interview transcripts and actor perspectives (Charmaz & Mitchell, Citation2001; Corbin & Strauss, Citation1990; Urquhart, Citation2016). Multiple rounds of open coding were undertaken with frequent debriefings, discussions and negotiation of the codes (Glaser & Strauss, Citation1967).

Second, we performed axial coding through clustering and integrating of the open codes to derive interesting theoretical and empirical categories. This helped manage the volume of data and create a coherent structure that captured umbrella concepts (Charmaz & Mitchell, Citation2001) and the emerging story. Lastly, we conducted selective coding by aggregating the axial codes into overarching dimensions. Selective coding helped explore how our axial codes fit into broader theoretical categories. As noted in , this led to the theoretical concepts of innovative and collaborative practices, protectionist and equitable practices, and legitimising and sustaining practices.

Figure 2. Data structure.

During this process, we engaged with existing theory, concepts and content categorisation schemes (Urquhart, Citation2016). This led to concepts and theories on innovation ecosystems, financial inclusion and ICT for development (e.g., Karanasios & Slavova, Citation2019; Lagna & Ravishankar, Citation2021). The research process transitioned from pure inductive to integrating and building concepts from the literature. We established a framework () that captures the richness of the data and traces emerging theoretical constructs.

4. Findings

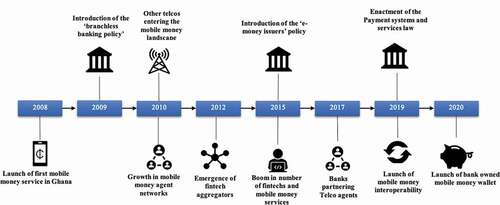

Our findings reveal three interwoven practices which shape financial inclusion: innovative and collaborative practices, protectionist and equitable practices, and legitimising and sustaining practices. summarises the interactions between the multilevel actors and the three practices. We also present a timeline of major events in Ghana’s FinTech ecosystem (see Appendix B) and yearly mobile money transactions statistics to support our findings (see Appendix C).

Table 2. Multilevel practices and interactions for financial inclusion

4.1. Innovative and collaborative practices

Our analysis reveals two dominant and interwoven practices that shape financial inclusion. First, FinTech firms, telcos and banks provide innovative financial services which substitute for, and/or refine, traditional offerings. Second, in doing so, actors reconfigure their relationships and adopt new collaborative models to deliver their innovations.

4.1.1. Substituting and refining established financial products and services

illustrates traditional financial services (column 1) and barriers to their use (column 2) which contribute to financial exclusion. Column 3 shows how mobile money addresses these barriers through technology and collaboration between new (e.g., FinTech firms and telcos) and old actors (banks) to develop substitute services or refine existing ones and their use (column 4). For example, people can use mobile money to easily transfer money to others in remote parts of the country in under a minute, without needing a bank account, or can purchase electricity credits, pay school fees and secure micro-loans.

Table 3. Traditional vs. substitute/refined approaches to financial inclusion

Mobile money services are substitutes for traditional banking services tailored to the unbanked; the mobile money account becomes the bank account, and the mobile phone becomes the means of transaction. Depositing money is replaced by converting cash to eFundsFootnote2 stored in a mobile money account. Banking services, such as transferring funds, are replaced by peer-to-peer mobile money transfers. FinTech firms build on the successful substitution by “move[ing] from just enabling sending and receiving of money and buying airtime and goods” (FinTech Firm 2), to offering other innovative financial services such as international remittance, direct debit, payment aggregation, hire-purchase, investment management and pension contributions through mobile money platforms. A FinTech firm outlined how their start-up allowed the unbanked to participate

“Previously, people [unbanked] could not access small loans from banks because banks are not in most villages and people could not fulfil strict documentation requirements. However, with our services [mobile micro-loans], a user can request a loan with their mobile phone and within a few minutes, they will have the money in their mobile money account […] no need for collateral as compared to banks.” (FinTech Firm 6)

4.1.2. Blending products and services development through new collaborative models

Both old and new actors are collaborating to blend their own offerings and capabilities with other actors and provide more “joined-up” holistic services to the unbanked. The actors recognised that developing and delivering services to the unbanked requires new interactions and interdependencies amongst multiple actors, and thus new combinations of technological capabilities, resources and relationships. Some incumbents like banks do not have in-house technical competencies to develop their own solutions and therefore rely on FinTech firms. Though telcos can technically develop mobile money solutions, they also sometimes rely on FinTech firms to overcome technical challenges such as interoperability issues and their ability to be more agile and respond rapidly to the market. For instance, if a telco wishes to launch a new service to all Ghanaians, it is easier to use FinTech firms already connected to their competitors’ mobile money platform than for the telco to negotiate directly with its competitor for access.

shows the collaborative models for the new services. FinTech firms use telcos’ mobile money platforms and infrastructure to provide innovative solutions, viewing them as “strategic partners” (FinTech Firm 2). FinTech firms also work with banks to deliver services specifically to financially excluded groups, and incumbent banks also partner with FinTech firms and telcos to expand their services. Through these collaborative practices, the actors improve financial inclusion by co-joining and blending their capabilities. A FinTech articulated their symbiotic relationship with banks:

“[we] enable banks to build a relationship with traditional SusuFootnote3 groups, using mobile money these Susu groups can build a credit history which the banks can rely on to offer them micro-loans.” (FinTech Firm 3)

Table 4. Examples of financial inclusion services

Despite the quid-pro-quo, the relationships are delicate and based on clear separation of each actor’s activity and role. A FinTech explained they do not pursue banks’ customers:

“The partnership with banks is not a simple conversation, but banks are accepting that there is some value in a relationship. Our bank partners are happy with us as the eFunds are kept with them. But, for the banks who are not our partners, we are seeing some acceptance with some wanting to switch to our solutions. (FinTech Firm 3)

4.2. Protectionist and equitable practices

New actors entering the market and new pathways to manage previously unserved markets triggered new forms of collaboration. This also generated rivalry and competition between actors, which resulted in protectionary practices being lobbied for and introduced. BoG intervention was rationalised as necessary to protect the unbanked (e.g., preventing risky or predatory financial products), and to hasten financial inclusion. Yet, many related policies further preserve the relative advantage of incumbents. Such policies have been well received by telcos and banks as necessary to ensure benefits are appropriately disseminated and that each actor is incentivised to facilitate innovative and collaborative practices. This is in contrast to approaches by Western policymakers, which have focused on increasing competition and reducing barriers to entry, rather than protecting established banks’ position as gateway organisations, seeking “rent” for access to customers and infrastructure (Gozman et al., Citation2018). Such policies have been rationalised in Ghana:

“The banks think the financial sector is their baby so when the FinTech firms and telcos wanted to enter the industry, there was lots of resistance and this led to slow uptake of FinTech innovations […] the BoG had to introduce a policy that banks become the custodian of deposited funds before things took off.” (FinTech Firm 5)

4.2.1. Interventionary policies favouring established actors and institutions

When telcos first launched mobile money in 2008, incumbent banks were not supportive initially. While banks were not able to reach the majority of unbanked people, they viewed them as an untapped market, and considered telcos’ mobile money services as a threat. The absence of regulation on mobile money compounded tension among actors. In response, the BoG regulated mobile money under the “branchless banking law”, so that telcos could operate as agents for banks. This raised new tensions, as telcos criticised the law as a barrier to their independence and the growth of mobile money. Banks also resisted this arrangement, viewing it as a forced marriage between competitors. As the BoG viewed mobile money as important for financial inclusion, there was a need to address this impasse.

In 2015, the BoG introduced the “E-money Issuers” policy to recognise telcos as “independent financial institutions”. The policy also recognised banks as custodians of eFunds transacted over mobile telecommunication networks and, in so doing, protected their position in the FinTech ecosystem. Consequently, telcos need to partner with a bank to hold eFunds. This policy aimed to reduce tension between the incumbent banks and telcos, allowing telcos to roll out mobile money as “semi-autonomous” financial institutions.

After launching the E-money Issuers policy in 2015 (see timeline in Appendix B), the registered number of mobile money accounts doubled from about 7 million in 2014 to 13 million in 2015 (Bank of Ghana, Citation2019), and active (in use) mobile money accounts also doubled from about 2.5 million in 2014 to 4.8 million in 2015. These policy actions, which favoured banks and telcos, protected the integrity of the financial sector, and strategically fostered a sustainable financial sector that can address financial inclusion.

4.2.2. Controlling access to key infrastructure, functions and customers

Under the protectionist policy, incumbents retain ownership and control of key infrastructure, such as mobile money platforms, banking licences and deposit-taking functions, as well as customer relationships. This separation between the digital infrastructure enabled mobile money and the underpinning currency:

“All the monies collected on the wallets are kept in banks and also when developing products like savings and loans products as well as investment products, regulation demands you have a banking partner to carry some of the risk. You can’t do without the bank if you really want to do financial inclusion.” (Telco 2)

Protectionist practices should not be interpreted as a restricting force, whereby telcos and banks control access to mobile money infrastructure and deposit-taking. Rather, this stability and centralisation creates “a win–win situation where they [FinTech firms] have access to us to increase their customer base and we have access to them to increase our services and revenue” (Telco 1).

On the one hand, FinTech firms and telcos need banks as custodians of eFunds so they can operate. On the other hand, banks and telcos need FinTech firms to develop innovative solutions to address financial inclusion. For example, FinTech firms offering mobile money-based university admissions rely on telcos for access to mobile money platforms. At the same time, custodian banks are needed to hold the money transacted via the mobile money platform. Through this collaborative arrangement, multilevel actors benefit from the mutually beneficial relationship, propelling them towards improving financial inclusion.

4.3. Legitimising and sustaining practices

Legitimising and sustaining practices address and nurture financial inclusion by embedding the outcomes of practices to improve financial inclusion. The practices described here refer to purposive structuring of institutional arrangements (top-down) and engagement of individuals (bottom-up) to scale up financial inclusion in Ghana.

Top-down restructuring of institutional arrangements to accommodate new entrants is consistent with Western practices on revising established approaches to licencing regulated financial activities and the degree to which new entrants are regulated and supervised (Gozman et al., Citation2018). However, the granularity of the practices we identify are distinct to the Ghanaian context, by the ways in which individual agents, at the grassroots level, and already known to their communities, have been engaged in trust building, becoming pivotal in improving financial inclusion.

4.3.1. Top-down revision of institutional arrangements for trust building

Our study reveals the ways in which policies and related mandates are enacted, performed and reconstituted to improve financial inclusion. Key actors such as the BoG, telcos and banks are simultaneously adjusting, adapting and compromising to ensure institutional arrangements can sustain financial inclusion. One example is the “E-money Issuers” policy. However, other examples illustrate how institutional arrangements were changed to accommodate not just new entrants such as large established telcos, but also FinTech firms such as the introduction of legislation to allow the licencing of FinTech firms to operate in the new FinTech ecosystem. Policymakers aimed to build trust in new products and services for the unbanked by addressing malpractice, protecting consumers and mitigating systemic risk to Ghana’s economy. Such outcomes were legislated through Ghana’s Payment Systems and Services law (Act 987 of 2019).

When FinTech firms began providing mobile money-based solutions in 2012 (see Appendix B), there was no specific law guiding their operations. With the growth of FinTech firms, the BoG enacted the payments and systems law so that FinTech firms could seek their own licence rather than having to partner with licenced banks. The BoG also formulated the National Financial Inclusion and Development Strategy (NFIDS). The importance of these three institutional arrangements in improving financial inclusion is emphasised as:

“ … right now, when it comes to that [financial inclusion], it’s more important to implement what we [Ghana] have set out in the national financial document policy [the NFIDS]. … there’s supposed to be access, equity, education. Government has to ensure that all government payments are digitised and are targeted at the right places. … for now, it’s just picking the actions in there. (Think Tank 1)

Internal reorganisation in actors was also needed. Previously, financial inclusion and its potential for development and growth was not prioritised by the BoG and other banks. However, with the potential of mobile money, BoG revised their institutional practices. Previously, the BoG’s main focus was on banks, reflected in how its departments were organised and resourced. The BoG revised its internal structures and relationship with the new and old actors. The quote from the BoG shows a mindset shift to embracing digital technology for financial inclusion:

“Financial inclusion is bigger than Bank of Ghana, we have evolved to have providers, infrastructure providers and consumers. The Payment Systems Department (PSD) is just an aspect of the drive for financial inclusion … We have Ghana interbank payment and settlement systems (GhIPSS) supporting us with the infrastructure, we have banks, providers, deposit taking institutions and we have the FinTech firms who deal with payment systems. … the Bank of Ghana decided to join the Alliance for Financial inclusion and then proceeded to set up the Payment Systems Department”. (BoG)

4.3.2. Bottom-up trust building through empowerment of localised agents

As part of transforming the financial landscape, prevailing cultural-historical norms were combined with new financial practices to ensure contextually relevant innovation at the community level. New roles were developed to facilitate such bridging and build trust. Our findings show how the banks, telcos and FinTech firms worked together to innovate and collaborate to develop new products and services for the unbanked. While the blending of each organisation’s distinct capabilities with the BoG’s careful restructuring of institutions and policies offered new ways to reach the unbanked through the design and legitimation of new products and services delivered digitally, one key component was still missing. Agents, as intermediaries between users and telcos, were needed at the grassroots level to offer direct access to services and support. Consequently, localised agents were crucial. These agents built and maintained trust in technology-enabled ways of managing personal finances, in a significant change from usual practices. A think tank added:

“The success of M-Pesa [in Kenya] is largely attributed to mobile money agents, so we really advocated for more flexibility in having many agents if mobile money was to work in Ghana and now you can see the results, … .very impressive.” (Think Tank 2)

In Ghana, cash is common and social ties are critical in building trust, as is the use of intermediaries such as drivers who operate between cities and villages moving money between parties. These cultural norms are embedded in the new financial landscape. For instance, “mobile money agents” act as intermediaries between telcos and individuals. As intermediaries, agents receive commission for transactions, a lucrative source of income. While agents may be like shadow bank branches, limited capital is required for establishment, leading to wide availability in many villages and communities compared to bank branches. Agents are people who live and operate within communities, creating a high level of trust in mobile money to drive financial inclusion. This was critical for telcos, as support services were needed for people in remote areas, building on the strength of local social ties, as the unbanked considered traditional banking services to be for the middle class and city dwellers. Agents use cultural ties to legitimise a market solution.

With time, the agent network grew and surpassed bank branch reach. Agents also allowed people without mobile money accounts to make financial transactions. For instance, people could use a “token”, a unique number with details of a money transfer to receive money through agents. Agents were pillars of mobile money:

“With the banks, even with the biggest banks they do not have up to 1,000 branches. We work with agents and today our agent base is around 16,000 so we are able to reach a lot more people and give them access to a financial wallet to be able to send and receive money, have access to credit and all that sort of things which the banks are not able to meet.” (Telco 2)

Despite these benefits, banks did not initially see the value of using agents, considering them simply as another channel to deliver financial services, and no different from automated teller machines. However, recently banks have recognised the important cultural role of agents, and have begun partnering with them to reach unbanked people:

“We launched an agency banking network which also allowed us to reach the unbanked in their communities directly by converting mobile money agents, converting shops into [Bank 2’s] agents, so that people could just go there and do their deposits and withdrawals, without coming all the way to us in the branch.” (Bank 2)

One bank respondent explained, “[customers] used to come in buses [to branches]; at times, they would move together and it’s like a festival”. The emergence of agents is the final element in delivering meaningful services to the unbanked. The combination of mobile money and agents means that people can access their accounts through their mobile phones and “move the funds from their accounts onto their mobile wallets and go to the nearest agent and go and cash out” (Bank 3).

5. Discussion and conclusion

Our study examined how the interplay between new and old actors shapes financial sector practices to address financial inclusion. Our multilevel data allows us to develop contextually relevant theory by articulating how the interconnections, dynamics and interplay between actors shape financial inclusion through their products and services for the unbanked.

5.1. Theoretical contributions: ecosystem perspective on financial inclusion

Our findings included three interwoven practices at the FinTech ecosystem level as building blocks for financial inclusion: innovative and collaborative practices, protectionist and equitable practices, and legitimising and sustaining practices. These practices and their relationship are illustrated in as our theoretical model of FinTech ecosystem practices shaping financial inclusion. The model shows that innovative and collaborative practices result in new FinTech products and services while protectionist and equitable practices lead to new regulations, relationships and roles. The new FinTech products and services and the new regulations, relationships and roles influence each other. On the other hand, legitimising and sustaining practices provide a conducive environment for the new FinTech products and services and new regulations, relationships and roles to thrive. What makes these practices unique is how they are connected and reinforce one another. Focusing on the interaction between the practices rather than considering them in isolation is more holistic in understanding how FinTech ecosystem practices shape financial inclusion. The practices are further expanded with propositions that lay the foundation for future research and infer general theoretical insights.

Figure 3. Model of FinTech ecosystem practices shaping financial inclusion.

Innovative and collaborative practices involve new collaborative models of blended product and services development to create substitutes and refinements of established financial products and services. These solutions are more accessible, and targeted to the unbanked. Innovative and collaborative practices were largely embodied by the interdependencies between FinTech firms, banks, and telcos. Their collaborative practices and unique capabilities developed innovative FinTech services (Jacobides et al., Citation2018). FinTech firms are largely responsible for the technical development of FinTech services (Senyo & Karanasios, Citation2020), while telcos provided their mobile money platform for users to access the services (Iman, Citation2018). Banks act as custodians of eFunds transacted on mobile money (Senyo & Osabutey, Citation2020). By identifying this symbiotic relationship between actors we address how FinTech firms deliver pro-poor financial services (Lagna & Ravishankar, Citation2021). For instance, previously, the unbanked could not access small loans from traditional banks because of documentary and collateral requirements and inaccessible bank branches. However, with mobile money, people in remote communities can use their mobile phones to request micro loans in under five minutes without visiting a physical branch or providing any collateral.

The dynamic interplay between old and new firms (Gozman et al., Citation2018) also leads to tensions, as organisations must navigate pluralistic and often conflicting logics: financial services for the poor vs. financial services for profit; co-creating innovation vs. protecting market share. The longevity of these arrangements requires careful value co-creation, sharing of rewards and careful macro-level intervention to ensure such equity is created and persists (Jacobides et al., Citation2018). Our study setting is a FinTech ecosystem where incumbents and new actors pull together complementary capabilities, and new products and services are mutually constituted and co-delivered by competing, yet mutually dependent organisations (Senyo & Karanasios, Citation2020). We advance the following proposition:

Proposition 1: Innovative and collaborative practices, inclusive of varying configurations of actors, shape financial inclusion through the co-creation of relevant new FinTech services.

The emergence of new actors in FinTech demands the building block of protectionist and equitable practices to cater to the new and old actors’ pressures, while meeting the needs of the unbanked. Such practices were mostly embodied by the BoG, with support from think tanks. In addition to regulating the financial sector, the BoG is tasked with increasing financial inclusion in Ghana. Recognising the value of FinTech solutions like mobile money for financial inclusion, it was imperative to create an environment for the technology to thrive (Senyo & Osabutey, Citation2020).

At the same time, there was a need to balance the drive for greater financial inclusion through mobile money and the need for a stable traditional financial sector, while protecting people from predatory financial services. The BoG introduced new regulations to protect incumbent banks and telcos by ring-fencing some of their activities, while also encouraging innovation such as holding funds, while at the same time licencing new FinTech firms, which could then compete with some banking incumbents offering similar products and services. In this way, new products and services are mutually constituted and co-delivered by organisations with different or competing agendas (Jacobides et al., Citation2018; Senyo & Karanasios, Citation2020). Thus, the Ghanaian context also reveals tensions in competitive practices emerging from the introduction of new regulations. We therefore propose

Proposition 2: Protectionist and equitable practices enable control of resources between old and new actors that is necessary to encourage new relationships and roles to shape financial inclusion.

The third building block is legitimising and sustaining practices to address and nurture financial inclusion by embedding the outcomes of the previously described practices. Legitimising and sustaining practices are represented by activities of actors such as agents, merchants, think tanks and the regulator (BoG) who build trust and normalise new mobile money solutions and the relationships formed in the new FinTech ecosystem. These practices can be viewed from macro and micro levels. Macro level practices are embodied in actors such as the regulator (the BoG), and think tanks through their public support and legislative backing of new FinTech solutions and relationships (Senyo & Osabutey, Citation2020). For instance, the BoG’s new FinTech department is a way to support and sustain the FinTech ecosystem.

In turn, at the micro level, legitimising and sustaining practices are embodied in the activities of agents and merchants who offer supporting services for FinTech innovations. This is important in explaining the sustainability of mobile money services for the unbanked (Lagna & Ravishankar, Citation2021). While agents act as intermediaries between users and telcos, merchants accept mobile money payment for goods and services (Senyo et al., Citation2020). These actions create user trust and legitimise FinTech solutions and sustain their use, thereby shaping financial inclusion. These actors are known by users, ensuring bottom-up trust building to legitimise and sustain the use of FinTech innovations. Therefore, users are comfortable in using services provided by agents as there is some level of surety that problems can be easily resolved. The interplay between the macro and micro level practices and actors not only defines the boundaries of activity (Jacobides et al., Citation2018), but also shapes the direction of financial inclusion. We propose:

Proposition 3: Legitimising and sustaining practices shape financial inclusion by encouraging and normalising new mobile money solutions and relationships formed in the new FinTech ecosystem.

In sum, our model asserts that financial inclusion requires collective orchestration of the three practices and a symbiotic relationship between old and new actors. Through a combination of widely distributed agent-networks in communities, access to mobile networks, cheaper transaction costs, innovative financial services and a restructured financial landscape backed by strong regulation, mobile money contributes to financial inclusion in Ghana. At the end of 2020, there were about 36 million registered mobile money accounts, representing seven-fold growth since 2013 (see Appendix C), and increasing financial inclusion.

However, our findings reveal tensions embedded in the ecosystem. Information asymmetries and moral hazards may be introduced into the financial system as the network and interactions of players become increasingly diverse and complex, in turn reducing the transparency of the financial system for users. The intermediary role of localised agents may simultaneously mitigate and exacerbate these issues, depending on the agent’s knowledge, motivations and moral compass (e.g., some agents commit fraud (Senyo & Osabutey, Citation2020)). These complex arrangements may also prove challenging to supervise. The introduction of new systems and technologies alongside legacy technologies, and the need for both manual and automated interoperability between networks of systems, is also likely to reduce the transparency of Ghana’s financial system at the technical level.

Our findings, model and subsequent propositions contribute to theory in three ways. First, our findings show that development of FinTech services for financial inclusion requires pulling together capabilities between independent yet complementary competitors from three different traditional sectors: information technology (for FinTech firms), telecommunication (for telcos) and banking (for banks). To improve financial inclusion, competing actors need to work together to develop FinTech services that are contextually sound because of environmental constraints. The literature has predominantly conceptualised co-creation of digital innovation to occur between IT-producing firms. Our study offers an alternative perspective from the developing country context and extends the literature by demonstrating how competitors can work together to shape financial inclusion. Our findings underscore the conceptualisation that only alliances between IT-producing firms can co-create digital innovations and, in our case, FinTech services.

Second, the study contributes by theorising how regulators can use regulations to strike a balance between triple competing interests of incumbents, new actors and citizens to shape financial inclusion (Lagna & Ravishankar, Citation2021). This study demonstrates that to understand institutional responses to financial inclusion, it is important to distinguish between regulations designed to protect incumbents and those designed to legitimise new actors. While some regulations might be suitable for traditional financial institutions, they might not work for new actors. Our findings suggest regulations that are both protectionist and equitable to incumbent and new actors can help balance the regulation of FinTech ecosystems.

Lastly, we extend the existing FinTech and innovation ecosystem literature by articulating how accounting for and enabling localised trust building can normalise practices to shape financial inclusion. We established the instrumental role of bottom-up trust building in the form of legitimising local mobile money agents and merchants to operate in the FinTech ecosystem. As these agents largely operate in communities, they create trust and drive adoption and use of FinTech services (Senyo et al., Citation2020). This insight also explains why some FinTech initiatives from incumbents like branchless and mobile banking have not reduced financial exclusion (Iman, Citation2018). To successfully use FinTech services for financial inclusion, it is important to normalise bottom-up trust building and build users’ trust.

5.2. Practical contributions

Governments and practitioners may use our findings to inform their own strategies to balance government interventions to both protect critical players and the roles they play while simultaneously encouraging new players to enter markets and compete. This is important where there is a rapidly evolving financial sector with a range of multilevel actors pursuing new opportunities for financial inclusion. A related challenge is how to supervise new actors to prevent malpractice and build trust in a new ecosystem, while not stifling innovation, ensuring that regulatory obligations are not an insurmountable barrier to entry. This challenge is faced by regulators across financial services globally, as new FinTech firms enter established markets.

Likewise, challenges faced by practitioners running telcos, banks and FinTech firms include managing an increasingly complex network of relationships and the fine line between maximising returns and sharing value to ensure the new model of financial inclusion remains viable. Where the gap between the needs of new actors and regulatory interventions is high, it may mean financial inclusion services do not meet the needs of the unbanked. Where the gap between the needs of old actors and regulatory interventions is high, it can also mean innovation may be high but the necessary incentives for old and new actors to collaborate are weak, resulting in a weak outcome. This may help understand why some efforts at improving financial inclusion are more successful than others.

5.3. Limitations and future research

The financial sector is not uniform across the world. While a strength of our study is the breadth of data collected in one setting (Davison & Martinsons, Citation2016), the financial sector in Ghana is not replicated across Africa and has its own nuances. However, there are commonalities with other countries in the challenge of delivering financial services and the interplay and tension between innovative and collaborative, protectionist and equitable, and legitimising and sustaining practices in shaping financial inclusion.

Further research could examine the ecosystem in other countries, including where FinTech has reduced financial exclusion, or has failed to address it. Mobile money is only part of financial inclusion. Scholars should not neglect the broader financial needs of the unbanked. With the rise of multiple mobile money services in Ghana, an important direction of research is to examine how multiple competing services interoperate and form a complex ecosystem that improves financial inclusion, or alternatively how disparate and competitive digital solutions fragment the market.

Studies could also examine how mobile money services adapt and evolve as they meet the market: how do the services and practices in our model transform as they are appropriated by individual users. Our study did not include users, merchants, and mobile money agents as our sample was limited to actors that develop, offer, promote or regulate FinTech services rather than beneficiaries. Future research may focus on the role of agents, not only as cash-in and cash-out points, but also as important enablers of financial inclusion. Similarly, the role of merchants who receive mobile money payment for their goods and services in shaping financial inclusion could be investigated. Future research could examine the distinction between firms that focus on the unbanked and those that focus on the banked as a more profitable sector.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1. Unstructured Supplementary Service Data (USSD) is a communications protocol used by GSM cellular phones to communicate with mobile network operators’ platforms. It is the base technology for mobile money.

2. An eFund is digital money used for mobile money transactions.

3. An informal savings club arrangement between a small group of people.

References

- Bank of Ghana. (2019). Payment systems statistics-first half 2019. https://www.bog.gov.gh/wp-content/uploads/2019/10/Payment-Systems-Statistics-First-Half-2019-Table.pdf

- Bongomin, G. O. C., Munene, J. C., Ntayi, J. M., & Malinga, C. A. (2019). Collective action among rural poor: Does it enhance financial intermediation by banks for financial inclusion in developing economies? International Journal of Bank Marketing, 37(1), 20–43. https://doi.org/https://doi.org/10.1108/IJBM-08-2017-0174

- CGAP. (2008). Banking on mobiles: Why, how, for whom? In Focus note no.48. Consultative Group to Assist the Poor, 1—28.

- Charmaz, K., & Mitchell, R. (2001). Grounded theory in ethnography. In P. A. Atkinson, A. Coffey, S. Delamont, J. Lofland, & L. Lofland (Eds.), Handbook of ethnography (pp. 60–174). Sage Publications.

- Corbin, J., & Strauss, A. (1990). Grounded theory research: Procedures, canons, and evaluative criteria. Qualitative Sociology, 13(1), 3–21. https://doi.org/https://doi.org/10.1007/BF00988593

- Davison, R. M., & Martinsons, M. G. (2016). Context is king! Considering particularism in research design and reporting. Journal of Information Technology, 31(3), 241–249. https://doi.org/https://doi.org/10.1057/jit.2015.19

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The global findex database 2017: Measuring financial inclusion and the FinTech revolution. World Bank.

- Disrupt Africa. (2019). Finnovating for Africa 2019: Reimagining the African financial services landscape. Disrupt Africa.

- Drummer, D., Feuerriegel, S., & Neumann, D. (2017). Crossing the next frontier: The role of ICT in driving the financialization of credit. Journal of Information Technology, 32(3), 218–233. https://doi.org/https://doi.org/10.1057/s41265-017-0035-9

- Glaser, B. G., & Strauss, A. (1967). The discovery of grounded theory: Strategies for qualitative research. Aldine Publishing.

- Gomber, P., Kauffman, R. J., Parker, C., & Weber, B. W. (2018). On the FinTech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), 220–265. https://doi.org/https://doi.org/10.1080/07421222.2018.1440766

- Gozman, D., Liebenau, J., & Mangan, J. (2018). The innovation mechanisms of FinTech start-ups: Insights from SWIFT’s innotribe competition. Journal of Management Information Systems, 35(1), 145–179. https://doi.org/https://doi.org/10.1080/07421222.2018.1440768

- Iman, N. (2018). Is mobile payment still relevant in the FinTech era? Electronic Commerce Research and Applications, 30, 72–82. https://doi.org/https://doi.org/10.1016/j.elerap.2018.05.009

- Jacobides, M. G., Cennamo, C., & Gawer, A. (2018). Towards a theory of ecosystems. Strategic Management Journal, 39(8), 2255–2276. https://doi.org/https://doi.org/10.1002/smj.2904

- Karanasios, S., & Slavova, M. (2019). How do development actors do “ICT for development”? A strategy-as-practice perspective on emerging practices in Ghanaian agriculture. Information Systems Journal, 29(4), 888–913. https://doi.org/https://doi.org/10.1111/isj.12214

- Klein, H., & Myers, M. (1999). A set of principles for conducting and evaluating interpretive field studies in information systems. MIS Quarterly, 23(1), 67–93. https://doi.org/https://doi.org/10.2307/249410

- Lagna, A., & Ravishankar, M. N. (2021). Making the world a better place with FinTech research. Information Systems Journal, 1–42. https://doi.org/https://doi.org/10.1111/isj.12333

- Lee, I., & Shin, Y. J. (2018). FinTech: Ecosystem, business models, investment decisions, and challenges. Business Horizons, 61(1), 35–46. https://doi.org/https://doi.org/10.1016/j.bushor.2017.09.003

- Leong, C., Tan, B., Xiao, X., Tan, F., & Sun, Y. (2017). Nurturing a FinTech ecosystem: The case of a youth microloan startup in China. International Journal of Information Management, 37(2), 92–97. https://doi.org/https://doi.org/10.1016/j.ijinfomgt.2016.11.006

- Muthukannan, P., Tan, B., Gozman, D., & Johnson, L. (2020). The emergence of a FinTech ecosystem: A case study of the Vizag FinTech valley in India. Information and Management, 57(8), 103385. https://doi.org/https://doi.org/10.1016/j.im.2020.103385

- Oborn, E., Barrett, M., Orlikowski, W., & Kim, A. (2019). Trajectory dynamics in innovation: Developing and transforming a mobile money service across time and place. Organization Science, 30(5), 1097–1123. https://doi.org/https://doi.org/10.1287/orsc.2018.1281

- Oshodin, Osemwonyemwen; Molla, Alemayehu; Karanasios, Stan; and Ong, Chin Eang, “How do FinTech Start-ups Develop Capabilities? Towards a FinTech Capability Model” (2019). Pacific Asis Confernece on Information Systems (PACIS) 2019 Proceedings. 59. https://aisel.aisnet.org/pacis2019/59

- Senyo, P. K., & Karanasios, S. (2020). How do FinTech firms address financial inclusion? International Conference on Information Systems. https://aisel.aisnet.org/icis2020/societal_impact/societal_impact/7

- Senyo, P. K., Liu, K., & Effah, J. (2019). Digital business ecosystem: Literature review and a framework for future research. International Journal of Information Management, 47, 52–64. https://doi.org/https://doi.org/10.1016/j.ijinfomgt.2019.01.002

- Senyo, P. K., & Osabutey, E. L. C. (2020). Unearthing antecedents to financial inclusion through FinTech innovations. Technovation, 98, 102155. https://doi.org/https://doi.org/10.1016/j.technovation.2020.102155

- Senyo, P. K., Osabutey, E. L. C., & Seny Kan, A. K. (2020). Pathways to improving financial inclusion through mobile money: A fuzzy set qualitative comparative analysis. In Information Technology & People. https://doi.org/https://doi.org/10.1108/ITP-06-2020-0418

- Urquhart, C. (2016). Grounded theory. The International Encyclopedia of Communication Theory and Philosophy 4, (pp. 781—794). John Wiley & Sons. Chicago.

- Walsham, G., & Sahay, S. (2006). Research on information systems in developing countries: Current landscape and future prospects. Information Technology for Development, 12(1), 7–24. https://doi.org/https://doi.org/10.1002/itdj.20020

- World Bank. (2018). Financial inclusion: Financial inclusion is a key enabler to reducing poverty and boosting prosperity. https://www.worldbank.org/en/topic/financialinclusion/overview