ABSTRACT

This paper explains the energy mix of China’s overseas electricity investments across Belt and Road Initiative (BRI) recipient countries. We focus on Indonesia and Pakistan. Our research is based on both newly gathered project-level data and in-depth interviews with stakeholders of Chinese-backed power plants in Indonesia and Pakistan. We examine (1) why Chinese actors are involved in renewable power generation in Pakistan and not in Indonesia, and (2) why Chinese-backed coal-fired projects in Pakistan are cleaner than in Indonesia. We argue that variations along the three dimensions – scope, governance regime, and issue linkage – lead to different energy mixes in Chinese-invested power plants across BRI countries. This framework specifies how supply and demand factors interact across multiple levels regarding the formulation and implementation of China’s overseas electricity projects. Our findings shed new light on the environmental implications of BRI projects and the dynamics of renewable energy development in emerging markets.

1. Introduction

China has become the world’s leading source of foreign direct investment (FDI) and other financing for electricity generation (Gopal et al. Citation2018, p. 12). Development finance by Chinese policy banks is a crucial component of such cross-border finance (Li et al. Citation2020a, pp. 1–2). According to the Global Development Policy Center, policy banks ‘have supported similar amounts of power generation capacity overseas’ compared to FDI (Ma Citation2020, p. 2). China’s role in financing power generation is particularly key for developing countries, where most future demand for power generation will occur. For example, in sub-Saharan Africa, China has become the largest investor in the region’s electricity sector (Lema et al. Citation2021). Given that the recent rapid expansion of Chinese overseas electricity investment will contribute to global climate change (Ma Citation2020), this issue has drawn increasing attention from both the academia and policy community (Gallagher et al. Citation2018, Citation2021, Kong and Gallagher Citation2019, Citation2020, Citation2021a, Citation2021b, Liu and Urpelainen Citation2021).

The existing literature often follows a supply and demand framework, looking at both ‘push’ and ‘pull’ factors, to explain the contours of Chinese overseas involvement in the power sector (Kong and Gallagher Citation2021a, Citation2021b). Gallagher et al. (Citation2021) and Kong and Gallagher (Citation2021a) emphasize the key role of demand-side variables. Developing countries have sought coal finance from China because of a variety of domestic factors ranging from their familiarity with coal technology to underdeveloped grid infrastructure (Gallagher et al. Citation2021, p. 7). Recipient countries also exhibit modest demand for Chinese renewable finance because they worry it will not fulfill their development objectives quickly or lack the capacity and enabling frameworks to deploy it rapidly (Kong and Gallagher Citation2021a, p. 3). In terms of the supply side, Chinese policy banks are reluctant to sponsor renewables partly out of their own experiences with China’s problematic domestic renewable power expansion (Kong and Gallagher Citation2020, p. 10). On the other hand, overcapacity in China increases the need for Chinese overseas development finance (Li et al. Citation2022, Niczyporuk and Urpelainen Citation2021), and it also serves as an important push for the globalization of China’s coal-fired power plant industry (Kong and Gallagher Citation2020, pp. 15–16). However, in recent years coal has faced new economic and political obstacles, and many Chinese-financed coal plants have been halted or remain in limbo (Wang and Christoph Citation2021).

Building on the list of drivers identified in the existing literature, we seek to articulate causal mechanisms through which they combine into outcomes by answering the question ‘how, by what intermediate steps, a certain outcome follows from a set of initial conditions’ (Mayntz Citation2004, p. 241). Specifically, we propose a theoretical framework that considers interactive dynamics between domestic and transnational factors to explain why Chinese overseas electricity engagement exhibits varying energy profiles across recipient countries. We focus on the constellations of interests of BRI project participants and other related decision-makers in both China and recipient countries. These transnational constellations are different along three key dimensions: (1) whether a constellation includes or excludes coal interests from the recipient country, (2) the extent to which the governance of Chinese-backed projects in a recipient country has been institutionalized, and (3) whether the host country’s central government is able to leverage China’s strategic considerations to advance the recipient’s renewable energy development. Variations along the three dimensions lead to different energy mixes in Chinese-invested power plants across BRI countries. Our framework thus opens the black box of a complex process by which interactions between push and pull factors influence how China engages in power sectors of BRI countries.

We focus on Indonesia and Pakistan as our cases. Parallels between Indonesia and Pakistan provide a good opportunity to use the method of paired comparison (Tarrow Citation2010). Although both are amongst the largest recipients of Chinese outward electricity investments, they exhibit stark differences regarding the energy profile of Chinese-backed power plant projects: (1) Chinese actors are engaged in solar and wind in Pakistan and not Indonesia, and (2) Chinese-backed coal-fired projects in Pakistan are ‘cleaner’ than those in Indonesia. Our empirical analysis demonstrates how our theoretical framework can provide a coherent account of the cross-country divergence across BRI countries.

Our paper advances the emerging research agenda on China’s overseas energy investment in three ways. First, we develop a multi-level framework to explore variations in Chinese-backed power plants across different BRI countries. More specifically, this perspective highlights how micro-level interest groups, meso-level governance regimes, and macro-level geopolitics collectively influence the dynamics of China’s electricity projects under the BRI. Second, by providing an in-depth analysis of the cases of Indonesia and Pakistan, our research lays out specific mechanisms underlying the complex interplay between Chinese and recipient country actors. Therefore, this paper unpacks the process through which these transnational interactions affect the formulation and implementation of Chinese-backed projects. Third, our research adds empirical details regarding China’s global expansion in the power sector in two key BRI countries.

In the second section, we outline a theoretical framework to explain how varying constellations of the transnational network lead to different portfolios of Chinese outbound power investments. The third section provides a brief description of our case selection and data collection. In the fourth section, we provide a summary of the different technology profiles of Chinese power sector investments in Indonesia and Pakistan. This country-level variation poses an empirical puzzle that is not fully explainable by looking at supply and demand factors in isolation. Then we conduct a detailed comparative analysis of the dynamics in Indonesia and Pakistan and demonstrate how our proposed mechanisms provide a systematic explanation. We conclude with a discussion on both theoretical and policy implications.

2. The analytical framework

2.1 Constellations of interests

In this section, we introduce our theoretical framework - – the constellations of interests – and elaborate on specific mechanisms within this framework. We take the unit of analysis as the cross-country constellation of actors, including both project participants (investors and project developers) and decision-makers and regulators in both China and the recipient country. Following Hale et al. (Citation2020), we conceptualize the decision-making processes of BRI projects as ‘reverse two-level games.’ Accordingly, BRI projects entail two levels of bargaining involving different types of stakeholders. On the one hand, there is a level of transnational bargaining that mainly occurs between business consortia in China and recipient countries. On the other hand, there is also a higher level of interstate bargaining between Chinese and recipient country leaders. We term this ‘reverse’ two-level games because, opposite to Putnam’s framework, bargains between states determine the broad scope of what is possible at the transnational level, which is where (with some exceptions) projects are originated and determined. Between these two levels of negotiations, bureaucratic politics and the transnational interplay between different government agencies in China and recipients play a crucial mediating role.

Therefore, our framework allows us to simultaneously explore micro, meso, and macro-level dynamics of transnational interactions around Chinese-backed projects: (1) how individual interests of business consortia are formed around BRI projects at the micro-level, (2) how these interests are mediated by specific governance arrangements at the meso-level, and (3) goal alignment between the Chinese government and host country governments at the macro-level.

At the micro-level, we focus on whether a specific type of business actor in the host country – coal-interest groups – is excluded or not from the formulation and implementation of BRI power plant projects. At the meso-level, our research examines variation in the degree of institutionalization of the regime regulating Chinese-backed investments, which comprises domestic bureaucratic regulators and liaison offices that are tasked with the responsibilities of monitoring, coordination, and information sharing. Finally, our analytic framework pays attention to macro-level variations, namely whether the Chinese state values a specific BRI country with geopolitical or strategic interests. As will be shown below, variations in the above three levels are associated with different energy mixes of Chinese-backed power plants in BRI recipients.

2.2 Mechanisms: scope, governance regime, and issue linkage

We now articulate specific mechanisms under our framework. The constellations of interests vary across three dimensions: scope, governance regime, and issue linkage. First, in terms of the scope mechanism, we focus on whether a certain type of business interest is included in the formulation and implementation of the recipient country’s BRI power plants. More specially, we pay particular attention to interest groups that represent the domestic coal industry, which has strong incentives to support the expansion of coal power while opposing the development of the RE sector (Cheon and Urpelainen Citation2013). Once this group has access to energy policy formulation, it is more supportive of traditional fossil fuels than renewable energies. In many nascent democracies, coal interest groups can promote their policy objectives by providing campaign funding and other forms of political support to politicians who advocate an increase in coal-fired power in the economies. For recipient countries in which coal business plays an influential role in affecting their energy policies, we should witness a transnational business coalition between Chinese power companies and domestic coal interests. Meanwhile, demand for Chinese-backed coal plants in these countries should be higher.

Second, concerning the governance regime, we focus on the degree to which a regulatory system is institutionalized. Put differently, we examine the extent to which rules or norms become routinized through stable and supportive regulatory apparatuses. An institutionalized governance regime alleviates the enforcement problem (Shimshack Citation2014). An enforcement problem occurs when an individual actor decides not to adhere to ‘a given agreement or set of rules’ (Koremenos et al. Citation2001, p. 776). BRI investments involve a host of subnational and non-state actors from both China and recipients. With both domestic and foreign actors getting involved, it becomes more challenging to monitor their behaviors and punish noncooperation. Under this circumstance, a more institutionalized regime can maintain higher levels of monitoring and thereby encourage compliance since shirkers are more likely to be punished (Koremenos et al. Citation2001, p. 790).

Since BRI projects involve cross-border activities, an institutionalized regime also entails efficient transnational coordination between domestic and Chinese regulators. An institutionalized regime thus allows actors in both countries to better cope with the problem of uncertainty. As Koremenos et al. (Citation2001, p. 778) note, ‘uncertainty refers to the extent to which actors are not fully informed about others’ behavior, the state of the world, and/or others’ preferences.’ An institutionalized governance regime, on the other hand, can mitigate this problem by facilitating the sharing of information between Chinese and domestic regulators and the coordination of their management of BRI projects (Koremenos et al. Citation2001, pp.787–788).

The extent to which a governance regime has been institutionalized has a deep influence on how Chinese developers of coal power plants behave. A more institutionalized governance system allows regulators have a stronger monitoring capacity to enforce local environmental standards. When pollution standards are better enforced, Chinese companies are more likely to develop coal plants with more efficient technology. Additionally, by reducing policy uncertainties, a more institutionalized regulatory system creates a more favorable investment climate for Chinese power companies. As a result, these developers, are more willing to invest in larger-scale projects. As we will see in the case of Pakistan, it is economically sound for Chinese developers to apply environmentally more friendly technologies to coal plants with massive generation capacity.

Our third mechanism is about goal alignment between the Chinese state and host country government. Here, we build on a body of IR literature on issue linkage. Issue linkage means ‘the simultaneous discussion of two or more issues for joint settlement’ (Poast Citation2013, p. 740). It is a common practice that a great power can provide economic side payments to its ally in exchange for the latter’s diplomatic support (Davis Citation2009). As a bargaining strategy, issue linkage allows a powerful state to use economic tools to serve its security interests. From the perspective of the ally, issue linkage brings one-sided economic gains, and it empowers this less powerful state to leverage mutual security cooperation to pursue its own policy goals.

With China’s expanding global economic influence, the Chinese government is increasingly seeking to exploit its growing economic might to advance the state’s geopolitical interests (Norris Citation2016, Hillman Citation2020, Reilly Citation2021). For those countries in which the Chinese government attempts to exert political influence, these target states can receive economic side payments from China as inducements for pro-Beijing policies (Norris Citation2016, Reilly Citation2021). On the other hand, elites in a recipient country can maneuver the Chinese government’s considerations about its security interests and link their own domestic policy goals to China’s economic inducements. In fact, as a recent analysis of China’s state-backed capital in the Philippines indicates, ‘the absence of any direct coercive apparatus and the existence of civil society’ give ‘elites in the host state the opportunity to hijack Chinese capital to pursue their own goals’ (Camba Citation2020, p. 973)

Therefore, for those target states, if domestic elites decide to support the development of the RE sector, they can attract Chinese state-backed investments even though these countries are not necessarily favorable places for developing RE projects. Under this circumstance, the Chinese government views its financial sponsorship of these power plants in target states as a way to enhance political influences in these foreign countries.

3. Case selection and data collection

Indonesia and Pakistan provide a good pairwise comparison in which to investigate Chinese electricity investments under the BRI for three reasons. First, along with Brazil, both countries are amongst the top three countries where the most power generation capacity has been built with Chinese investment and finance (Ma Citation2020, p. 8). Second, the two countries share a set of similar political characteristics including regime type and patterns of center-local relations (Lieven Citation2012, Davidson Citation2015). These similarities allow us to conduct a comparative study that controls for the influences of several confounding variables. Third, as described in detail below, the two BRI countries exhibit considerable differences in how Chinese actors engage in the power sector. However, although Indonesia and Pakistan are key places to explore electricity projects under the BRI, we should be cautious about generalizing the lessons learned here to other contexts. In particular, Pakistan constitutes a relative outlier under the BRI. Appendix G discusses the uniqueness of Pakistan and further probes the generalizability of our findings by providing additional analyses of Chinese electricity projects in several sub-Saharan African countries.

For our case study, we adopt a mixed-method design that uses both quantitative and qualitative data. We conducted dozens of in-person and teleconference-based semi-structured interviews with different types of power sector stakeholders in China, Indonesia, and Pakistan using a snowball technique in 2019, 2020, and 2021. Our interview subjects include international and local NGOs, government officials, researchers from think tanks and institutes, journalists, and managers from Chinese policy banks and power companies (see Appendix A).Footnote1 In addition to interviews, we compile a dataset on power plants in Indonesia and Pakistan. The data are compiled from existing datasets such as Global Energy Monitor, AidData, Water & Power Development Authority, and they are further crosschecked with websites of regulators and major electricity companies, Chinese, Bahasa, English, and Urdu media articles, and CSIS’s Reconnecting Asia data map (see Appendix B and C). The dataset is available from the Harvard Dataverse.Footnote2

4. Chinese investments in power sectors in Indonesia and Pakistan

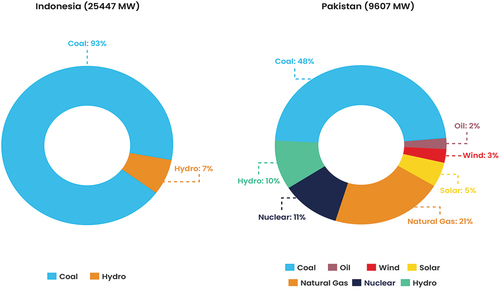

To illustrate how China’s electricity projects in Indonesia are different from those in Pakistan, we compiled different data sources and collected additional information to build a comprehensive dataset on Chinese-backed power plants in the two countries. Appendix B and C present a brief description of our data sources and coding rules about how we compile these data. An examination of the data shows that (1) Chinese actors invested in renewables in Pakistan but not in Indonesia, and (2) Chinese power plants use more efficient technology in Pakistan than in Indonesia.Footnote3

First, Chinese actors engage in solar and wind in Pakistan and not in Indonesia. shows that Chinese investments in Indonesia’s electricity sector are highly concentrated in coal. Between 2000 and 2020, on one hand, over 90% of Chinese-backed power plants in Indonesia are coal-fired. On the other hand, there are no Chinese-invested solar or wind electricity projects in Indonesia during the same period. Indeed, there are no commercial scale solar or wind projects of any kind due to Indonesia’s unfavorable political economy, as we explain below. In contrast, as illustrates, 8% of Chinese-backed power plants in Pakistan during the period 2000 − 2020 are solar or wind.

Figure 1. Technology mix of China’s electricity projects in Indonesia and Pakistan (2000–2020).

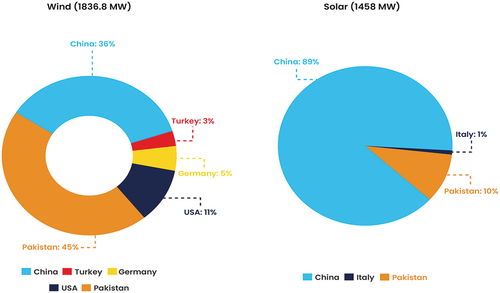

presents the nationality of renewable energy project developers in Pakistan. As both figures demonstrate, Chinese firms play a predominant role in the development of Pakistan’s wind and solar sector. Within the wind sector, China is the largest foreign investor country in Pakistan. Even more strikingly, in terms of generation capacity, Chinese-backed solar plants account for nearly 90% of Pakistan’s entire solar sector.

Figure 2. Nationality of renewable energy developers in Pakistan by capacity (MV) (2000 − 2033).

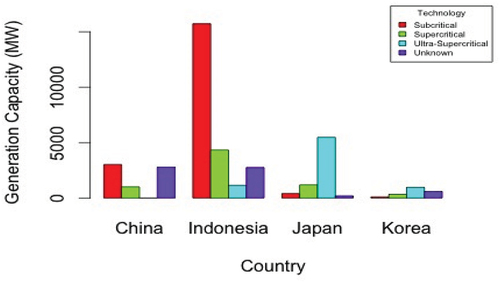

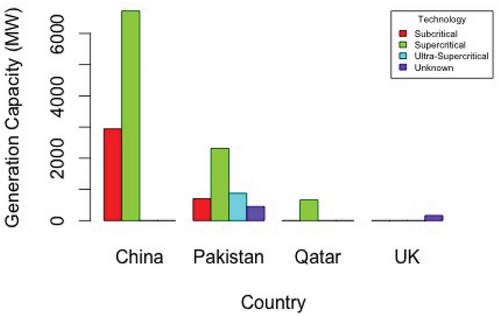

In addition to cross-country distinctions regarding Chinese engagement in RE, Chinese coal power plants are more environmentally damaging in Indonesia than in Pakistan. show the technology of foreign-invested coal-fired plants in Indonesia and Pakistan, respectively. The data demonstrate that Chinese companies bring lower end of technology (i.e., subcritical power plants) to Indonesia compared to other foreign investors. By contrast, Chinese-backed coal power plants tend to employ more advanced technology (i.e., supercritical power plants) in Pakistan.Footnote4

Figure 3. Technology of coal power plants in Indonesia by investors (2008–2018).Footnote5

Figure 4. Technology of coal power plants in Pakistan by investors (2000–2021).

The divergences between Indonesia and Pakistan are puzzling if we only analyze supply or demand dynamics in isolation. Instead, we argue that the revealed cross-country differences between the two countries can be better explained by considering the interactions between supply-side and demand-side factors. Because of space limitations, for a detailed discussion on the insufficiency of focusing on either supply or demand factors in accounting for distinctions between Indonesia and Pakistan, see Appendix D.

5. Mechanism-oriented explanations of differences between Indonesia and Pakistan

To explain divergences in the energy mix of China’s overseas electricity investments, we examine different constellations of interests of BRI stakeholders in Indonesia and Pakistan. More specifically, we argue that three mechanisms – (1) scope, (2) governance regime, and (3) issue linkage – act as key determinants of cross-country differences between Indonesia and Pakistan regarding China’s electricity investments. In the following subsections, we articulate how these mechanisms unfold in Indonesia and Pakistan. Appendix E presents a table and a figure to visualize our mechanisms here. Appendix F suggests the reasons why Indonesia and Pakistan are different in terms of the three mechanisms.

5.1 Chinese-backed projects in indonesia’s power sector

5.1.1 Scope – the inclusion of coal interests

The coal industry is a powerful player in Indonesian politics. The country is the world’s largest exporter of steam coal, and Indonesian coal production experienced a significant increase between 2000 and 2016 (Cornot-Gandolphe Citation2017). With the explosive growth of coal mining and exporting activities, Indonesia’s coal industry has been dominated by a small number of oligarchs (Mori Citation2020, p. 5). The coal industry gains considerable political power as it ‘is tightly connected to political elites in Indonesia, involving several big names in current national political landscape’ (Arinaldo and Adiatma Citation2019, p. 13).

The coal industry’s political clout results in a number of favorable government policies. For instance, in 2014, subsidies to coal production were around USD 946 million while renewables only received roughly USD 36 million (Attwood et al. Citation2017). Partly because of these massive subsidies to coal, the Perusahaan Listrik Negara (PLN)Footnote6 had to pay higher tariffs to buy electricity generated by renewables. While the minimum feed-in tariffs (FITs) for solar PV and wind were USD 14.5 cents/kWh and USD 9.26 cents/kWh in 2015, respectively, PLN’s average generation cost from coal was USD 4.10 cents/kWh in 2014 (Attwood et al. Citation2017, p. 30, Table 30). Since renewables are more expensive than coal power plants, PLN prioritizes the development of coal power over renewables. According to PLN’s long-term plan, the coal share in Indonesia’s electricity mix is expected to reach 60–65% by 2028 (Arinaldo and Adiatma Citation2019, p. 7).

Although both the Indonesian government and PLN actively support the development of the country’s coal industry (Wijaya Citation2021), renewables encounter more policy hurdles in Indonesia’s electricity market. In addition to providing much fewer subsidies to renewables than coal power plants, the Indonesian government also start imposing lower tariffs for RE project developers after 2016 (Halimanjaya Citation2019, p. 51). Moreover, PLN’s monopoly of the national power grid leads to prolonged tariff negotiations between PLN and IPPs. Because of PLN’s recalcitrance, it is not surprising that many potential RE projects ‘have been held up for years due to difficulties in the negotiating PPAs’ (Setyowati Citation2020, p. 7).

Coal domination in Indonesia’s energy mix has profound implications on how Chinese investors engage in the country’s power sector. Because China is one of the largest importers of Indonesian coal (Arinaldo and Adiatma Citation2019, p. 17), many Chinese companies have cultivated close business connections with Indonesia’s major coal miners (Mori Citation2018, p. 183). During the last decade, several Chinese electricity companies and Indonesian coal oligarchs have created joint ventures to develop coal power plants as IPPs (Mori Citation2020, p. 5). For example, PTBA, Indonesia’s third largest coal producer, built a joint venture with China Huadian Hong Kong to develop a large-scale coal-fired plant (Mori Citation2018, p. 183).

On the other hand, coal domination discourages the entry of Chinese RE developers. As noted above, under the strong influence of the coal industry, both the Indonesian government and PLN lack incentives to implement pro-RE energy policies. According to our interviews, many Chinese solar companies are hesitant to invest in Indonesia, and they are still waiting for possible policy changes of the country’s unfavorable regulations on renewables (Interview with a journalist with extensive knowledge of Indonesia’s clean energy development, 12/24/2020; Interview with a manager of an Indonesian company that provides consultancy for Chinese electricity investors, 12/27/2020; Interview with an international NGO manager, 04/21/2021).

5.1.2 The absence of institutionalized governance regimeFootnote7

Although Indonesia’s Ministry of Maritime Affairs is tasked with coordinating BRI projects in the country,Footnote8 the de facto environmental governance regime on these projects is highly decentralized, fragmented, and lacks transnational coordination. Consequently, the whole regulatory system suffers from the weak capacity to monitor Chinese-backed projects and enforce environmental standards. As a result, Chinese investors tend to favor environmentally more damaging technology (i.e., subcritical coal power plants) to save their costs and increase profitability rates.

First, Indonesia’s environmental governance regime is vertically decentralized. Since 2001, both Indonesia’s Environmental Impact Assessment (EIA) system and industrial pollution control have been decentralized (Bedner Citation2010, pp. 43–44). With the decentralized control of AMDAL (EIA in Indonesian) and industrial pollution regulations, local governments play a pivotal role in Indonesia’s environmental management (McCarthy and Zen Citation2010). In many places, Chinese electricity companies act as providers of campaign funds for local Indonesian officials in exchange for local governments’ approval of Chinese-backed coal power plants (Interview with a manager of an Indonesian company that provides consultancy for Chinese electricity investors, 12/27/2020). Since many provincial and district-level governments are vulnerable to the capture of Chinese coal-fired companies, they do not enforce environmental standards and ensure effective compliance of Chinese-backed projects (Interview with an Indonesian researcher, 04/07/2021). For example, in the case of the Celukan Bawang coal plant in Bali, a project invested by China Huadian Engineering, nine local NGOs and international organizations submitted a file to Denpasar Administrative Court (PTUN) against it in late 2018. They accused that the project did not carry out a comprehensive AMDAL regarding its climate change impacts (Interview with an international NGO manager, 04/21/2021).Footnote9

Second, Indonesia’s regulatory system of Chinese-backed power plants is horizontally fragmented. These plants are subjected to a number of central-level Indonesian agencies, often with conflicting policy agendas. The governance regime’s supervisory ability to enforce environmental sustainability is weak and ineffective. Hence, Chinese coal plants enjoy discretion to employ lower-end technology. In particular, although the Ministry of Maritime Affairs is responsible for coordinating BRI projects, PLN, as the major electricity generator and distributor, is another crucial actor in shaping the dynamics of Chinese electricity investment. PLN has strong incentives to increase profitability rather than promote environmental sustainability. This is because the Ministry of State-owned Enterprises (MSOE) supervises PLN, and MSOE overwhelmingly focuses on financial performances when it evaluates Indonesian state-owned enterprises (SOEs) (Maulidia Citation2019, p. 134). Since PLN prioritizes economic considerations, it tries to cut costs as much as possible when building new plants. Therefore, Chinese power companies often win tenders for coal plants as they can propose low bid prices by using lower types of technology (Interview with a European researcher on China’s electricity investment in Indonesia, 04/12/2021).

Third, for Chinese-backed coal plants, the Chinese government has not tried to develop transnational supervisory mechanisms to enforce environmental standards. Although the Chinese side’s regulatory effort becomes critical when the host country’s governance regime is weak, these Chinese consortia in Indonesia rarely provide regular reports or updates about the environmental implications of their projects to Chinese regulators such as NDRC, State-owned Assets Supervision and Administration Commission, or Ministry of Ecology and Environment (Interview with an officer of Asian Development Bank, 12/22/2020). As will be shown below, unlike in the case of Pakistan, the environmental performances of Chinese-backed coal plants are not under heavy scrutiny from both the Chinese and the Indonesian government.

5.1.3 The absence of issue linkage

The Chinese state does not view supporting China’s electricity investments in Indonesia as critical to securing its geopolitical interests. As a result, Chinese electricity companies make investment decisions in Indonesia mainly out of their commercial considerations. Likewise, Chinese policy banks tend to finance economically sound power plants, and they are not willing to bear high business risks. For instance, after the issuance of a 2017 electricity regulation, the Indonesian government requires that PLN holds the majority of the shares of all electricity projects participated by foreign investors in Indonesia. Consequently, Chinese policy banks are reluctant to sponsor many coal-fired power plants in Indonesia. The reason is that the associated bankability risk increases when Chinese companies cannot control their overseas project. As a result, a number of Chinese coal-power project developers cannot find supportive financiers to develop these projects (Interview with a manager of an Indonesian company that provides consultancy for Chinese electricity investors, 12/27/2020; Interview with an international NGO manager, 04/21/2021).

Since high politics is absent regarding Chinese investments in Indonesia’s power sector, the Chinese government lacks strong incentives to employ policy tools to induce Chinese firms to enter Indonesia’s RE market. Therefore, Jakarta’s domestic policy landscape largely determines whether Chinese power generators prefer to engage in Indonesia’s RE sector (Interview with a journalist with extensive knowledge of Indonesia’s clean energy development, 12/24/2020). However, given unfavorable policies enacted by the Indonesian government and PLN, many China’s major power generators such as Huadian and Datang take a wait-and-see attitude regarding potential RE projects (Interview with an international NGO manager, 04/21/2021).

5.2 Chinese-backed projects in pakistan’s power sector

5.2.1 Scope – the exclusion of coal interests

Unlike Indonesia, Pakistan’s coal industry has never occupied an influential role in determining the country’s energy policy. The limited political clout of Pakistan’s coal sector is partially a result of the negligible position of coal in the country’s energy consumption. For example, coal only constituted merely 0.2% of Pakistan’s total electricity generation in 2013–2014 (Mirjat et al. Citation2017, p. 114). Historically, Pakistan’s major coal deposit – the Thar coalfield has been underutilized. One reason is that the quality of the coal in the Thar Desert is not good enough for generating electricity (Interview with a National Electric Power Regulatory Authority (NEPRA) director in Pakistan, 09/27/2020).

Rather than importing coal for domestic energy consumption, Pakistan has heavily relied on imported oils to generate electricity since the 1990s. The dominance of imported oil in Pakistan’s electricity generation mix originated in the mid-1990s when the Pakistani government initiated a partial reform of the then stagnant power sector (Bacon Citation2019, pp. 12–13). To mitigate severe power shortages that emerged in the 1980s, Islamabad turned to an expedient approach to reform the power sector. In particular, the 1994 National Power Policy set up a set of policies to encourage the participation of private investors in the then closed power sector. Among all these policies, the one with the most far-reaching consequence is to allow these new entrants to choose fuel for the power plant (Bacon Citation2019, pp. 12–13, Downs Citation2019, pp. 12–13). Given the low international price of oil in the mid-1990s and ‘the policy favored developers who were willing to build plants that could be brought online first’ (Bacon Citation2019, p. 13), many developers built oil-based plants. This 1994 reform led to an oil-heavy power generation mix that persisted until today. Although increased private investments resulted in almost added 45,00 MV generation capacity, the heavy dependence on imported oil make Pakistan’s electricity generation much more expensive when the oil price increased drastically in the 2000s. During the fiscal year 2014, ‘the average generation cost of electricity produced from residual fuel oil was four times higher than that of coal’ (Downs Citation2019, pp. 18–19).

Given the peripheral position of Pakistan’s coal sector, the formulation of the country’s first RE policy in the late 2000s did not encounter fierce political resistance from domestic energy production groups (Interview with an Alternative Energy Development Board (AEDB) official in Pakistan, 10/09/2020). Instead, the biggest challenge of promoting the RE sector lies in attracting domestic and international investors given the considerable commercial risks associated with RE investments at that time (Interview with a Pakistan environmental NGO manager, 04/16/2021). As shown in detail below, Pakistan eventually turned to China and received the latter’s sponsorship of these RE projects.

5.2.2 An institutionalized governance regime

Chinese project developers have the discretion in choosing which type of technology (i.e., sub-critical versus super-critical) would be used for their coal power plants (Interview with a Pakistan environmental NGO manager, 04/16/2021; Interview with a Chinese expatriate manager who worked for a major Chinese electricity project in Pakistan, 04/16/2021). The choices of these developers are to a certain degree determined by two factors that are closely related to the transnational governance system of Chinese power projects in Pakistan.

First, unlike the case of Indonesia, Beijing makes substantial efforts to enforce environmental standards with regard to Chinese-backed electricity projects. Chinese overseas power companies need to go through the approval processes in both Pakistan and China when it comes to getting environmental impact evaluations for their proposed projects. The Chinese standards are even more stringent than World Bank and IFC (Interview with a Pakistan’s Private Power and Infrastructure Board (PPIB) official, 10/02/2020). Chinese developers in Pakistan thus have a stronger motive to adopt more environmentally friendly technologies since the Chinese government imposes more stringent environmental standards on them (Interview with a Chinese expatriate manager who worked for a major Chinese electricity project in Pakistan, 04/16/2021). In fact, Chinese coal-fired plants are required to install an automatic digital monitoring system on daily air pollution emissions although local environmental regulatory offices in many places often lack the technological capacities to effectively keep track of these data (Interview with a Chinese environmental NGO manager, 12/28/2020).

To improve its capacity of overseeing electricity projects in Pakistan, Beijing also maintains an institutionalized channel to acquire information from the Pakistan side. In particular, there is ‘a joint consultative and planning process between China’s National Development and Reform Commission and Pakistan’s Ministry of Planning, Development, and Reform’ (Markey Citation2020, p. 48). In addition, there are regular meetings between ministry-level officials from both countries to discuss a variety of project-related issues. This routinized cross-national exchange of information strengthens the supervisory capacity of government-level stakeholders (Interview with a Pakistan’s PPIB official, 10/02/2020). Under closer scrutiny of the Chinese government, Chinese companies, therefore, pay more attention to enhancing their environmental performance in Pakistan.

Second, a Chinese coal plant is more likely to apply environmentally less damaging technology when its generation capacity is larger than a certain threshold (Interview with a Chinese expatriate manager who worked for a major Chinese electricity project in Pakistan, 04/16/2021). The employment of these technologies becomes economically sound only for mega-projects. For example, ultra-super-critical technology requires an installed capacity of no less than 600 MW (Personal communication with a Japanese researcher, 04/15/2021). A more institutionalized transnational governance system facilitates the construction of large-scale coal power plants by reducing transaction costs associated with these projects. In particular, the Chinese and the Pakistani government coordinate with each other to streamline the review and approval process of CPEC power plant projects (Interview with an AEDB official in Pakistan, 10/09/2020). Moreover, Islamabad provides a government guarantee to ensure commercial returns of CPEC projects and the Chinese side requires Sinosure to issue state-backed insurances to these CPEC projects (Interview with a Chinese environmental NGO manager, 12/28/2020). As a result, Chinese companies are more willing to invest in massive infrastructure projects in Pakistan. Consequently, these Chinese coal-power developers are also more willing to install more environmentally friendly technologies.

5.2.3 The presence of issue linkage

Although Pakistan is not an official ally of China, the two countries maintain an ‘all-weather friendship’ with each other. From the perspective of the Chinese government, the Sino-Pakistan axis is crucial for achieving three strategic goals: counterbalancing the influence of India (Small Citation2015, pp. 47–65), strengthening China’s control over its restive borderland – Xinjiang (Small Citation2015, pp. 67–91), and ensuring a permanent maritime facility in the Indian Ocean (Miller Citation2019, p. 178, Markey Citation2020, p. 48). Out of these motives for China’s internal and external security, Beijing decides to pour a vast amount of money into a few infrastructure projects in Pakistan even if many of these investments are not economically sound. For the Chinese government, CPEC projects are regarded as the ‘flagship’ of the BRI, and therefore the Chinese side is willing to bear high risks and unanticipated costs associated with these mega-projects. In fact, Chinese SOEs under the purview of the State-owned Assets Supervision and Administration Commission often suffer losses by doing business in Pakistan. However, a common mindset of these SOEs is to minimize these losses, rather than seek a profit, since participation in the CPEC is a mandate imposed by the Chinese state (Interview with a Chinese expatriate official journalist in Pakistan, 12/25/2020). According to Miller (Citation2019, p. 176), ‘government officials working on the Belt and Road project privately admit they expect to lose 80% of their investments in Pakistan.’

Power plants account for the bulk of CPEC’s earlier projects as Pakistan suffers from chronic electricity shortages. In Pakistan, the electricity supply would be turned off for 12–14 hours in cities and load shedding occurs for 16–18 hours in rural areas (Arshad and O’Kelly Citation2018). Consequently, the electricity blackouts result in popular discontent (Bacon Citation2019, p. 17). In the 2013 election, electricity shortage became a key political issue among the contestants for prime minister. Using the slogan ‘Bright Pakistan’, Sharif won the 2013 election by blaming the previous administration failed to overcome the power shortages and promising to resolve the energy crisis. After Sharif’s victory, he immediately turned to China to seek the latter’s investments in Pakistan’s power sector (Downs Citation2019, pp. 13–14). Out of the geopolitical interests, Beijing decided to sponsor the development of Pakistan’s power generation projects (Interview with a Chinese Academy of Social Sciences researcher, 12/21/2020; Interview with a Chinese expatriate official journalist in Pakistan, 12/25/2020). Therefore, during CPEC’s first phase, ‘of the total $46 billion initially projected by Pakistani officials, $34 billion was slated for power projects’ (Markey Citation2020, p. 57).

From Pakistan’s perspective, Islamabad has strong incentives to promote the development of RE sectors because of the country’s severe shortage of foreign exchange reserves (Interview with a Pakistan environmental NGO manager, 04/16/2021). As discussed above, Pakistan’s electricity industry is traditionally mainly fueled by imported oil from the Persian Gulf. For instance, in 2014, oil comprised almost 39% of all electricity fuels in Pakistan and it cost the country US$ 14.7 billion to import oils (Valasai et al. Citation2017, p. 737). The heavy reliance on oil imports causes a chronic underbalance of international payments. Moreover, this trade deficit further exacerbates Pakistan’s foreign debt problem. In fact, ‘Pakistan drew on IMF funds in fourteen of the twenty-one years between 2000 and 2020’ (Wingo Citation2020, p. 395). Different Pakistani governments periodically sought Beijing’s financial support to ‘reduce the scale and urgency of another IMF bailout’ (Markey Citation2020, p. 55).

The development of RE sectors had not been viewed by Pakistan as a way to save the country’s reserve assets until 2010 (Interview with a Pakistan environmental NGO manager, 04/16/2021). Although Pakistan was eager to promote RE to reduce its excess reliance on imported fossil fuels, it still faces daunting barriers to attracting investments in renewables at that time. As shown above, Pakistan does not enjoy a particularly favorable business environment for RE and foreign investors are quite hesitant to enter the country’s RE market. Under this circumstance, Islamabad courted Chinese backers for financing RE projects in Pakistan given that the Chinese state prioritizes its geopolitical influences over concerns about resultant commercial risks (Interview with an AEDB official in Pakistan, 10/09/2020). For example, when Beijing and Islamabad formulated CPEC between 2013 and 2015, several wind farms in Pakistan were re-branded as a part of the CPEC since it is easier for CPEC projects to receive loans and insurance from Chinese financiers than non-CPEC projects (Interview with an AEDB official in Pakistan, 10/09/2020).

6. Conclusion

This paper explores the energy mix in Chinese-backed electricity projects under the BRI. We propose a theory focusing on the constellations of interests of BRI project participants and other related decision-makers in both China and recipient countries. Our theory specifies three mechanisms – scope, the institutionalization of governance regime, and issue linkage – to account for the configuration of Chinese electricity investments in BRI countries, focusing on Indonesia and Pakistan.

Theoretically, this article makes two contributions to the burgeoning research on Chinese overseas energy investments. First, we add a multi-level perspective to the existing literature. At the micro-level, our theory emphasizes the importance of coal-interest business groups in BRI recipients. At the meso-level, we show how the transnational governance regime can structure the behavior of Chinese electricity generators. At the macro-level, we highlight how high politics between China and recipients can affect the dynamics of Chinese renewable investments. This perspective thus provides a more coherent account of Chinese-backed power plants under the BRI.

Second, instead of introducing more causal variables (either ‘push’ or ‘pull’), we theorize how domestic and transnational factors interact with each other and thereby clarifying how these explanatory variables are related to China’s electricity projects through multiple pathways. Therefore, our mechanism-oriented approach unpacks the complex process linking an array of causal factors and outcomes.

These findings also have implications for promoting RE growth in emerging markets. The comparison of Indonesia and Pakistan shows how scope, governance, and issue linkage shape the fortunes of sustainable energy technologies. While the inclusion of powerful coal interests in the scope of decision-making is difficult to change, advocates of RE should at the very least avoid creating and using institutional mechanisms that favor pre-existing interest groups over new interest groups. In governance, coordinated enforcement and monitoring of environmental rules, impact assessment, and social safeguards can remove the built-in advantage that coal and other fossil fuels have when their negative social, environmental, and health impacts are not mitigated. In strategically important countries, savvy advocates, policy entrepreneurs, and decision-makers can use issue linkage to entice China and other global investors to build RE markets.

Of course, there is a good deal of room left for future research. The first weakness of our paper is the limitation of our case selection. Our theoretical framework is based on two cases from South Asia and Southeast Asia. It is possible that the mechanisms cannot be generalized to other regions such as Africa and Latin America. Second, we only investigate Chinese electricity investments in coal and renewables. Future studies should also examine the dynamics of China’s engagement in hydro and nuclear power across BRI countries.

Looking ahead, our framework makes clear that limiting China’s outbound support for coal power is not by itself sufficient to encourage BRI countries to transition to renewables. Making ‘supply’ unattractive is only a partial solution. Though Chinese President Xi Jinping announced a stop to financing coal abroad in September 2021, this announcement does not automatically translate into greater Chinese financing of renewables. In this way, proposals to ‘green BRI’ must account for the interplay of supply and demand mechanisms, not just focus on one factor in isolation.

Supplemental Material

Download MS Word (94.2 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplementary material

Supplemental data for this article can be accessed online at https://doi.org/10.1080/09644016.2022.2087355.

Additional information

Funding

Notes

1. It is important to note the limitations of our qualitative data. Although we interviewed a variety of actors with different backgrounds, policy experts constitute a major type of our interview subjects. Therefore, our data are susceptible to the bias of these experts. Adding more interviews from other types of interview subjects such as project developers would improve our theoretical arguments. Future research is needed to address this issue.

2. The link to access the data is following: https://doi.org/10.7910/DVN/WYGSPW.

3. For a discussion on the origins of these cross-country differences, see Appendix F.

4. According to Gallagher et al. (Citation2021, p. 4), ‘Super and ultra-super-critical power plants need a lower amount of coal to generate the same account of energy compared to subcritical coal-fired power plants. Super-critical plants are able to achieve a higher level of efficiency because their boilers operate at a higher temperature and pressure than subcritical ones.’ For more information about the usage of subcritical technology by Chinese companies in Indonesia, see Tritto (Citation2021).

5. The calculation is based on this source: Tritto Angela, Coal power plants in Indonesia: ownership, investments, and impacts, Harvard Dataverse, https://doi.org/10.7910/DVN/ ETNOQA.

6. In 2016, ‘PLN and its subsidiaries control around 79% of power generation’ in Indonesia (Maulidia et al. Citation2019, p. 243).

7. We address possible alternative explanations for the deployment of particular coal-fired power technology in the Appendix H.

9. State Administrative Lawsuit on Cancellation of Bali Governor’s Decree No. 660.3/ 3985/ IV-A/ DISPMPT About Environmental Permit Development of Steam Power Plant (PLTU) given to PT. PLTU CELUKAN BAWANG ON THE VILLAGE ON THE SUPPORT OF GEROKGAK DISTRICT, REGENCY OF BULELENG.

References

- Arinaldo, D. and Adiatma, J.C., 2019. Indonesia’s coal dynamics: toward a just energy transition. IESR report.

- Arshad, M. and O’Kelly, B.C., 2018. Diagnosis of electricity crisis and scope of wind power in Pakistan. Proceedings of the Institution of Civil Engineers-Energy, 171 (4), 158–170. doi:10.1680/jener.17.00021

- Attwood, C., et al., 2017. Financial supports for coal and renewables in Indonesia. Winnipeg, Canada: International Institute for Sustainable Development.

- Bacon, R.W., 2019. Learning from power sector reform: the case of Pakistan. Washington, DC: The World Bank.

- Bedner, A., 2010. Consequences of decentralization: environmental impact assessment and water pollution control in Indonesia. Law & Policy, 32 (1), 38–60.

- Camba, A., 2020. The Sino‐centric capital export regime: state‐backed and flexible capital in the Philippines. Development and Change, 51 (4), 970–997. doi:10.1111/dech.12604

- Cheon, A. and Urpelainen, J., 2013. How do competing interest groups influence environmental policy? The case of renewable electricity in industrialized democracies, 1989–2007. Political Studies, 61 (4), 874–897. doi:10.1111/1467-9248.12006

- Cornot-Gandolphe, S., 2017. Indonesia’s electricity demand and the coal sector: export or meet domestic demand? OIES paper. Oxford: Oxford Institute for Energy Studies.

- Davidson, J.S., 2015. Indonesia’s changing political economy. New York: Cambridge University Press.

- Davis, C.L., 2009. Linkage diplomacy: economic and security bargaining in the Anglo-Japanese alliance, 1902–23. International Security, 33 (3), 143–179. doi:10.1162/isec.2009.33.3.143

- Downs, E., 2019. China-Pakistan economic corridor power projects: insights into environmental and debt sustainability. New York: Columbia Center on Global Energy Policy.

- Gallagher, K.P., et al., 2018. Energizing development finance? The benefits and risks of China’s development finance in the global energy sector. Energy Policy, 122, 313–321. doi:10.1016/j.enpol.2018.06.009

- Gallagher, K.S., et al., 2021. Banking on coal? Drivers of demand for Chinese overseas investments in coal in Bangladesh, India, Indonesia and Vietnam. Energy Research & Social Science, 71, 101827. doi:10.1016/j.erss.2020.101827

- Gopal, S., et al., 2018. Fueling global energy finance: the emergence of China in global energy investment. Energies, 11 (10), 2804. doi:10.3390/en11102804

- Hale, T., Liu, C., and Urpelainen, J., 2020. Belt and road decision-making in China and recipient countries: how and to what extent does sustainability matter? ISEP, BSG, and ClimateWorks Foundation.

- Halimanjaya, A., 2019. The political economy of Indonesia’s renewable energy sector and its fiscal policy gap. International Journal of Economics, Finance and Management Sciences, 7 (2), 45. doi:10.11648/j.ijefm.20190702.12

- Hillman, J.E., 2020. The emperor’s new road: China and the project of the century. New Haven, CT: Yale University Press.

- Kong, B. and Gallagher, K.P., 2019. Globalization as domestic adjustment: Chinese development finance and the globalization of China’s coal industry. GCI Working Paper 04/2019, Global Development Policy Center, Boston University.

- Kong, B. and Gallagher, K., 2020. Chinese development finance for solar and wind power abroad. GCI Working Paper 01/2020, Global Development Policy Center, Boston University.

- Kong, B. and Gallagher, K.P., 2021a. Inadequate demand and reluctant supply: the limits of Chinese official development finance for foreign renewable power. Energy Research & Social Science, 71, 101838. doi:10.1016/j.erss.2020.101838

- Kong, B. and Gallagher, K.P., 2021b. The new coal champion of the world: the political economy of Chinese overseas development finance for coal-fired power plants. Energy Policy, 155, 112334. doi:10.1016/j.enpol.2021.112334

- Koremenos, B., Lipson, C., and Snidal, D., 2001. The rational design of international institutions. International Organization, 55 (4), 761–799. doi:10.1162/002081801317193592

- Lema, R., et al., 2021. China’s investments in renewable energy in Africa: creating co-benefits or just cashing-in? World Development, 141, 105365. doi:10.1016/j.worlddev.2020.105365

- Li, Z., Gallagher, K.P., and Mauzerall, D.L., 2020a. China’s global power: estimating Chinese foreign direct investment in the electric power sector. Energy Policy, 136, 111056. doi:10.1016/j.enpol.2019.111056

- Li, Z., Gallagher, K., Chen, X., Yuan, J. and Mauzerall, D.L., 2022. Pushing out or pulling in? The determinants of Chinese energy finance in developing countries. Energy Research & Social Science, 86, 102441 .

- Lieven, A., 2012. Pakistan: a hard country. New York: PublicAffairs.

- Liu, C. and Urpelainen, J., 2021. Why the United States should compete with China on global clean energy finance. Washington, DC: Brooking Institute.

- Ma, X., 2020. Understanding China’s global power. GCI Working Paper 10/2020, Global Development Policy Center, Boston University.

- Markey, D., 2020. China’s Western Horizon: Beijing and the New Geopolitics of Eurasia. Oxford: Oxford University Press.

- Maulidia, M., 2019. Enhancing the role of the private sector in achieving transitional renewable energy targets in Indonesia. PhD Dissertation.

- Maulidia, M., et al., 2019. Rethinking renewable energy targets and electricity sector reform in Indonesia: a private sector perspective. Renewable and Sustainable Energy Reviews, 101, 231–247. doi:10.1016/j.rser.2018.11.005

- Mayntz, R., 2004. Mechanisms in the analysis of social macro-phenomena. Philosophy of the Social Sciences, 34 (2), 237–259. doi:10.1177/0048393103262552

- McCarthy, J. and Zen, Z., 2010. Regulating the oil palm boom: assessing the effectiveness of environmental governance approaches to agro‐industrial pollution in Indonesia. Law & Policy, 32 (1), 153–179.

- Miller, T., 2019. China’s Asian dream: empire building along the new silk road. London: Zed Books Ltd.

- Mirjat, N.H., et al., 2017. A review of energy and power planning and policies of Pakistan. Renewable and Sustainable Energy Reviews, 79, 110–127. doi:10.1016/j.rser.2017.05.040

- Mori, A., 2018. Impact of the China-induced coal boom in Indonesia: from a resource governance perspective. In: A. Mori, ed. China’s climate-energy policy: domestic and international impacts. New York: Routledge, 167–197.

- Mori, A., 2020. Foreign actors, faster transitions? Co-evolution of complementarities, perspectives and sociotechnical systems in the case of Indonesia’s electricity supply system. Energy Research & Social Science, 69, 101594. doi:10.1016/j.erss.2020.101594

- Niczyporuk, H. and Urpelainen, J., 2021. Taking a gamble: Chinese overseas energy finance and country risk. Journal of Cleaner Production, 281, 124993. doi:10.1016/j.jclepro.2020.124993

- Norris, W.J., 2016. Chinese economic statecraft: commercial actors, grand strategy, and state control. Ithaca, NY: Cornell University Press.

- Poast, P., 2013. Can issue linkage improve treaty credibility? Buffer state alliances as a “hard case”. Journal of Conflict Resolution, 57 (5), 739–764. doi:10.1177/0022002712449323

- Reilly, J., 2021. Orchestration: China’s economic statecraft across Asia and Europe. Oxford: Oxford University Press.

- Setyowati, A.B., 2020. Mitigating energy poverty: mobilizing climate finance to manage the energy trilemma in Indonesia. Sustainability, 12 (4), 1603. doi:10.3390/su12041603

- Shimshack, J., 2014. The economics of environmental monitoring and enforcement. Annual Review of Resource Economics, 6 (1), 339–360. doi:10.1146/annurev-resource-091912-151821

- Small, A., 2015. The China-Pakistan Axis: Asia’s new geopolitics. Oxford: Oxford University Press.

- Tarrow, S., 2010. The strategy of paired comparison: toward a theory of practice. Comparative Political Studies, 43 (2), 230–259. doi:10.1177/0010414009350044

- Tritto, A., 2021. China’s belt and road initiative: from perceptions to realities in Indonesia’s coal power sector. Energy Strategy Reviews, 34, 100624. doi:10.1016/j.esr.2021.100624

- Valasai, G.D., et al., 2017. Overcoming electricity crisis in Pakistan: a review of sustainable electricity options. Renewable and Sustainable Energy Reviews, 72, 734–745. doi:10.1016/j.rser.2017.01.097

- Wang, N. and Christoph, June 2021. “Coal phase-out in the Belt and Road Initiative (BRI): an analysis of Chinese-backed coal power from 2014-2020”. Beijing: Green BRI Center, International Institute of Green Finance (IIGF.

- Wijaya, T., 2021. Conditioning a stable sustainability fix of ‘ungreen’ infrastructure in Indonesia: transnational alliances, compromise, and state’s strategic selectivity. The Pacific Review, 1–31. doi:10.1080/09512748.2021.1884123

- Wingo, S.C., 2020. New types of financing for a new financier: a theory of Chinese development finance (Doctoral dissertation, University of Pennsylvania).