Abstract

The novel coronavirus (COVID-19) is challenging the world. With no vaccine and limited medical capacity to treat the disease, nonpharmaceutical interventions (NPI) are the main strategy to contain the pandemic. Unprecedented global travel restrictions and stay-at-home orders are causing the most severe disruption of the global economy since World War II. With international travel bans affecting over 90% of the world population and wide-spread restrictions on public gatherings and community mobility, tourism largely ceased in March 2020. Early evidence on impacts on air travel, cruises, and accommodations have been devastating. While highly uncertain, early projections from UNWTO for 2020 suggest international arrivals could decline by 20 to 30% relative to 2019. Tourism is especially susceptible to measures to counteract pandemics because of restricted mobility and social distancing. The paper compares the impacts of COVID-19 to previous epidemic/pandemics and other types of global crises and explores how the pandemic may change society, the economy, and tourism. It discusses why COVID-19 is an analogue to the ongoing climate crisis, and why there is a need to question the volume growth tourism model advocated by UNWTO, ICAO, CLIA, WTTC and other tourism organizations.

Introduction

A pneumonia of unknown cause detected in Wuhan, China, was first reported to the WHO Country Office in China on 31 December 2019. In early January 2020, 41 patients with confirmed infections by a novel coronavirus (COVID-19) had been admitted to hospitals in China (Huang et al., Citation2020). Even though the virus spread rapidly in the country’s Wuhan region, it was initially largely disregarded by political leaders in other parts of the world (although intelligence services issued warnings of a potentially cataclysmic event; Washington Post, Citation2020). To contain the virus, Wuhan was put into lockdown (a combination of regional and individual quarantine measures), and case numbers in China stabilized at around 80,000 by mid-February (ECDC 2020). By then, global air transport had already carried the virus to all continents and, by mid-March, it had been established in 146 countries. The number of confirmed infections worldwide quickly doubled, linked to a number of super-spreading events, such as the ski destination Ischgl in Austria (Anderson et al., Citation2020; Johns Hopkins, Citation2020). From here, the infection rate accelerated through community transmission and, by 15 April, confirmed cases approached 2 million (with over 125,000 deaths) in over 200 countries (ECDC 2020). The real total number of cases remains unknown as testing is limited in most countries. With no vaccine to prevent the disease and limited medical interventions available to treat it, most countries responded with various forms of nonpharmaceutical interventions (NPI), including lockdown (home isolation, voluntary/required quarantine), social distancing (vulnerable or entire populations), closure of schools/universities and non-essential businesses/workplaces, cancelling or postponing events (i.e. major conferences and tradeshows, concerts and festivals, political debates and elections, sports seasons and the summer Olympics), and bans on gatherings of people over certain numbers.

International, regional and local travel restrictions immediately affected national economies, including tourism systems, i.e. international travel, domestic tourism, day visits and segments as diverse as air transport, cruises, public transport, accommodation, cafés and restaurants, conventions, festivals, meetings, or sports events. With international air travel rapidly slowing as a result of the crisis, and many countries imposing travel bans, closing borders, or introducing quarantine periods, international and domestic tourism declined precipitously over a period of weeks. Countries scrambled to return travelers home, which in the case of important outbound markets involved hundreds of thousands of citizens in all parts of the world. As an example, on 23 March, the British Foreign Secretary urged British tourists to return home, “advising against all but essential international travel”, and highlighting that “[…] international travel is becoming more difficult with the closure of borders, airlines suspending flights, airports closing, exit bans and further restrictions being introduced daily” (FCO (The Foreign & Commonwealth Office), Citation2020). Cruise ships soon became the worst-case scenario for anyone stuck in the global tourism system. Starting with the Diamond Princess on 1 February 2020, at least 25 cruise ships had confirmed COVID-19 infections by 26 March 2020 (Mallapaty, Citation2020) and at the end of March ten ships remained at sea unable to find a port that would allow them to dock. Idealized safe environments (Cordesmeyer & Papathanassis, Citation2011) at sea turned into traps, with thousands of passengers held in cabin quarantine and facing the challenge of returning home.

Within countries, the virus affected virtually all parts of the hospitality value chain. The impact of cancelled events, closed accommodations, and shut down attractions became immediately felt in other parts of the supply chain, such as catering and laundry services. Restaurants had to close as well, though in some countries, a switch to take-away/delivery sales allowed some to continue operations. Reports on lay-offs and bankruptcies followed, with British airline FlyBe succumbing first to market pressure, declaring bankruptcy on 5 March 2020 (Business Insider, Citation2020). Major airlines including Scandinavian Airlines (17 March 2020), Singapore Airlines (27 March 2020) and Virgin (30 March 2020), as well as tour operators including German TUI (27 March 2020) have already requested tens of billions of US$ in state aid.

The situation is unprecedented. Within the space of months, the framing of the global tourism system moved from overtourism (e.g. Dodds & Butler, Citation2019; Seraphin et al., Citation2018) to non-tourism, vividly illustrated by blogs and newspaper articles depicting popular tourism sites in ‘before’ and ‘after’ photographs (Condé Nast Traveller, Citation2020). While some commentators already speculate on “What will travel be like after the Coronavirus”, with some unrealistically optimistic perspectives already having proven wrong (Forbes, Citation2020), the general belief is that tourism will rebound as it has from previous crises (CNN, Citation2020). However, there is much evidence that COVID-19 will be different and transformative for the tourism sector. Governments only begin to understand that, unlike other business sectors, tourism revenue is permanently lost because unsold capacity – for instance in accommodation – cannot be marketed in subsequent years, with corresponding implications for employment in the sector.

Against this background of a rapidly evolving global pandemic, this paper has four interrelated goals. First, to critically review the literature on the impact of previous epidemic/pandemics on global tourism and compares these events to other types of global crises. This section also examines whether the COVID-19 pandemic was an unknowable risk. Second, the paper provides a rapid assessment of the reported impacts of COVID-19 on global tourism through to the end of March 2020, including documented travel restrictions by each country and declines in air travel and accommodations. The differential regional impacts and implications for development are also examined. Recognizing that the impact to global tourism has only just begun, the third goal is to summarize early estimates of the damage to the tourism economy over 2020 and beyond. Because of the tremendous uncertainty, these early estimates are critically assessed against available epidemiological modelling and public health scenarios for restrictions on travel and public gatherings. Finally, the paper considers how the COVID-19 pandemic may change society, the economy, and tourism, and some of the key research needs to understand these changes and contribute to a more sustainable post-pandemic tourism sector. As soon as the virus is under control, there will be an urge by many to go back to business as usual, perhaps to overcompensate for losses by even more aggressive growth. Yet, the crisis holds important messages regarding the resilience of the tourism system, also in regard to other ongoing crises that are not as immediate, but potentially even more devastating than COVID-19, such as climate change.

Pandemics, tourism and global change

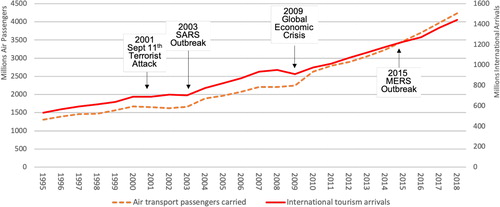

It is important to note that global tourism has been exposed to a wide range of crises in the past (). Between 2000 and 2015, major disruptive events include the September 11 terrorist attacks (2001), the severe acute respiratory syndrome (SARS) outbreak (2003), the global economic crisis unfolding in 2008/2009, and the 2015 Middle East Respiratory Syndrome (MERS) outbreak. None of them led to a longer-term decline in the global development of tourism, and some of them are not even notable in , with only SARS (-0.4%) and the global economic crisis (-4.0%) leading to declines in international arrivals (World Bank 2020a, 2020b). This would suggest that tourism as a system has been resilient to external shocks. However, there is much evidence that the impact and recovery from the COVID-19 pandemic will be unprecedented.

Figure 1. Impact of major crisis events on global tourism. Data source: World Bank (2020a, 2020b).

The relationships between pandemics and travel are central to understanding health security and global change (Burkle, Citation2006). Although tourism research has developed at least a cursory realization of the potential systemic effects of global climate change, there has not been the same appreciation of the systemic effects of pandemics, with studies tending to focus on individual country impacts, rather than the system level challenges and vulnerability. Several studies have demonstrated the important role of air travel in accelerating and amplifying propagating influenza and coronaviruses (see Brown et al., Citation2016 for a review). However, to an extent the rise and fall of academic interest in the relationship between tourism and pandemics is reflective of that of the wider industry and also governments, given that tourism has been affected by disease outbreaks numerous times since the turn of the millennium. Most importantly, there have been several warnings that pandemics posed a major threat to society and tourism from both tourism (Gössling, Citation2002; Hall, Citation2006, Citation2020; Page & Yeoman, Citation2007; Scott & Gössling, Citation2015) and health researchers (Bloom & Cadarette, Citation2019; Fauci & Morens, Citation2012), as well as government agencies (National Academies of Sciences, Engineering, and Medicine, Citation2017, Citation2018) and institutions (Jonas, Citation2014; World Bank, Citation2012).

The main reasons for the increasing pandemic threat in the 21st century are: a rapidly growing and mobile world population; urbanization trends and the concentration of people; industrialized food production in global value chains ; increased consumption of higher-order foods including meat; and, the development of global transport networks acting as vectors in the spread of pathogens (Pongsiri et al., Citation2009; Labonte et al., Citation2011). Disease outbreaks such as SARS, Ebola, Marburg, hantavirus, Zika and avian influenza are all outcomes of anthropogenic impacts on ecosystems and biodiversity (Petersen et al., Citation2016; Schmidt, Citation2016; World Bank, Citation2012). As Wu et al. (Citation2017, p.18) noted, “High-risk areas for the emergence and spread of infectious disease are where […] wild disease reservoirs, agricultural practices that increase contact between wildlife and livestock, and cultural practices that increase contact between humans, wildlife, and livestock [intersect]”.

As a result of global change, the rate at which major epidemics and pandemics occur has been increasing. It is generally recognised that the twentieth century experienced three pandemics. The so called ‘Spanish’ flu or influenza of 1918-19: the ‘Asian’ flu (H2N2) of 1957 and the ‘Hong Kong’ flu of 1968. The twenty-first century has already experienced four pandemics: SARS in 2002, ‘Bird flu’ in 2009, MERS in 2012, and Ebola which peaked in 2013-14, with the increase in pandemic outbreaks since 2000 believed to be strongly related to the global change factors noted above (Coker et al., Citation2011; Greger, Citation2007; Wu et al., Citation2017).

The SARS outbreak in 2003 was defined as an epidemic by the WHO, with most cases in China and Hong Kong and with clusters of cases in Taiwan and Canada as well. SARS has been studied from a tourism context. Siu and Wong (Citation2004) reported that the overall economic impact for Hong Kong was not as severe as expected, but that travel, tourism and retail were substantially affected as a result of the short-term decline in visitation. SARS had an overall estimated global economic cost of US$100 billion, and US$48 billion in China alone (McKercher & Chon, Citation2004; Siu & Wong, Citation2004).

In 2009, swine flu was defined a pandemic, but was a relatively mild event. Nevertheless, the 2009 swine flu pandemic resulted in approximately 284,000 deaths worldwide (Viboud & Simonsen, Citation2012). Russy and Smith (Citation2013) examined the effects of the pandemic on tourism in Mexico, suggesting that losing almost a million overseas visitors over a five‐month period translated into losses of around US$2.8 billion, with European markets being the slowest to return. Keogh-Brown et al. (Citation2010a, p.453), observed, “the current pandemic has not removed the threat of a more virulent avian flu pandemic in the near future. […] the importance of pandemic planning is plain”.

Two other pandemics were active at the time of the emergence of COVID-19. The first is the highly lethal MERS, a viral respiratory disease caused by a coronavirus (MERS‐CoV), identified in Egypt in 2012 (Berry et al., Citation2015). MERS has received significant attention in the travel medicine literature because of the large number of people who engage in the annual hajj pilgrimage to Saudi Arabia (Al-Tawfiqef et al., Citation2014). The second is Ebola, which has an average fatality rate of approximately 50% across the different waves of the disease (Chowell & Nishiura, Citation2014). The first outbreak occurred in the Democratic Republic of Congo (DRC) and Sudan in 1976 with subsequent outbreaks occurring in West Africa in 2014-16 and the DRC in 2018-19. The Ebola outbreak has been recognized as creating wider uncertainty and negative perceptions for African destinations that were unaffected by Ebola (Maphanga & Henama, Citation2019; Novelli et al., Citation2018). The Ebola and MERS outbreaks were significant in raising awareness as to the threat of global pandemics, even if that threat was not recognized or acted upon outside of those concerned with health security. As Fan et al. (Citation2018, p.129) observed, “Few doubt that major epidemics and pandemics will strike again and few would argue that the world is adequately prepared”, and, since the Ebola outbreak, “the United States National Academy of Medicine and several other groups have pointed to gaps, and the need for greater investment, in preparation against epidemics and pandemics”.

One of the central realizations of research on pandemics is that travel is absolutely central to epidemiology and disease surveillance (Hon, Citation2013; Khan et al., Citation2009). This also means recognizing that travel and tourism is both a contributor to disease spread and its economic consequences and is dramatically affected by it because of NPIs (Nicolaides et al., Citation2019). As Baldwin and Weder di Mauro (Citation2020, p.11) suggest, “The harsh reality is that we have no 21st century tools to fight COVID-19. There is no vaccine or treatment. All we have is the methods that were used to control epidemics in the early 20th century. Those, as we shall see, tend to be very economically disruptive”. It is for this reason that special attention is often given to the impacts of the 1918-1919 influenza pandemic (the Spanish Flu), which was ‘one of the worst pandemics in human history’ (Holtenius & Gillman, Citation2014), for understanding the potential impacts of contemporary pandemics (Garrett, Citation2008).

Although its origins were likely in the United States (Barry, Citation2004a; Byerly, Citation2010), the Spanish influenza is referred to as the Spanish Flu as Spain was the first country in which the outbreak was widely reported because wartime restrictions on the media were still in place in many countries. The 1918-19 pandemic infected up to 500 million people (approximately one-third of the then global population), and resulted in an estimate of between 21 to 100 million deaths (approximately 1%–5% of the world’s then population) (Jeffery & David, Citation2006; Johnson & Mueller, Citation2002). The pandemic travelled around the world in three waves and could therefore be described as the first “modern” pandemic characterised by rapid movement via global transport system (shipping and railways) (Killingray, Citation2003; Taubenberger & Morens, Citation2006).

The Spanish Flu is an important analogue for COVID-19 not only because of its similar virulence but also because many of the NPIs that were applied then are being used to mitigate COVID-19 (e.g. quarantine, travel restrictions) (Ferguson et al., Citation2006). Research suggests that the application of such measures in the case of the 1918-19 pandemic reduced death rates by approximately 50% (Hatchett et al., Citation2007) and, if NPI interventions were maintained then mortality was significantly reduced (Markel et al., Citation2006, Citation2007). However, as Hatchett et al. (Citation2007) noted, interventions were rarely maintained for longer than six weeks with the virus continuing to spread once restrictions were relaxed, which then led to public questioning as to the NPIs effectiveness.

Given their recognized massive impacts, there is surprisingly limited assessment of the economic effects of pandemics (Fan et al., Citation2018), with the majority of studies conducted at a national level (Keogh-Brown et al., Citation2010a, Citation2010b; Prager et al., Citation2017). The majority of economic studies of influenza are also generally undertaken in high income OECD countries (Peasah et al., Citation2013). In a widely cited report McKibbin and Sidorenko (Citation2006) estimated that the global economic cost of a Spanish Flu type pandemic would be close to 12.6% of GDP, with the greatest impact on non-OECD countries. In a more recent assessment, Fan et al. (Citation2018) found that at a global scale, a moderately severe influenza pandemic would result in 720,000 deaths and a cost of 0.6% of global income (due to income loss and mortality). compares the economic consequences of three different pandemic scenarios (Burns et al., Citation2006; McKibbin & Sidorenko, Citation2006), as well as a worse-case scenario at the upper end of the severity of the Spanish Flu. A recent update by McKibbin and Fernando (Citation2020) suggested that even a Hong Kong Flu type pandemic would reduce global GDP by around US$2.4 trillion and a Spanish flu type outbreak reduces global GDP by over US$9 trillion in 2020.

Table 1. Pandemic scenarios and their human and economic consequences.

Nevertheless, such scenarios provide only rough estimates of the impact of the COVID-19 pandemic. Despite the considerable uncertainty of the COVID-19 pandemic, in early April 2020 the UN Department of Economic and Social Affairs (2020) estimated that a scenario that assumes wide-ranging restrictions on economic activities in many OECD countries extend until the middle of the second quarter, the global economy is projected to shrink by approximately 0.9% in 2020, down from the forecast of 2.5% growth. They warn the pandemic is likely to undermine efforts to achieve the 2030 sustainable development goals, with highly differentiated impacts on lower income countries.

A salient question emerging from this literature is whether global leaders should have foreseen a pandemic like COVID-19, specifically since a range of health and economic agencies and institutions have been warning of the increased risks arising from the increased likelihood of a harmful global pandemic. For instance, the World Economic Forum (WEF) engaged political, business and other global experts/leaders in assessing key risks to the global economy in its annual Global Risks Report. In 2006 when the first Global Risk Report (WEF 2006) was conducted, a pandemic was one of four key risk scenarios. However, in the 2020 Global Risk Report, infectious disease ranked third last in likelihood (behind only weapons of mass destruction and unimaginable inflation) and tenth in potential impact. Surprisingly, it was also regarded as one of the least inter-connected risks. Similarly, in tourism, warnings of pandemics have been sounded over the years (e.g. Gössling, Citation2002; Hall, Citation2006, Citation2020; Page & Yeoman, Citation2007), cautioning about the need to more thoroughly examine the scenario of “[…] a persistent virulent pandemic that makes international travel a personal risk and is highly regulated to prevent the spread of the biohazard” (Scott & Gössling, Citation2015: 278).

COVID-19 and tourism

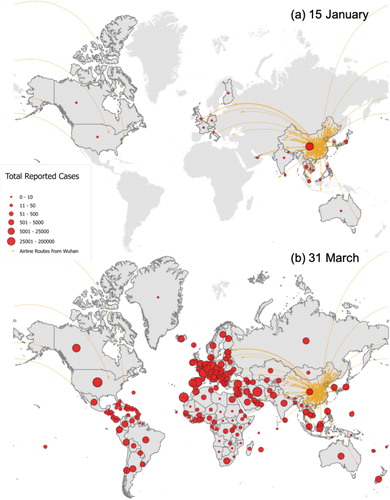

The world has experienced a number of major epidemics/pandemics in the last 40 years, yet none had similar implications for the global economy as the COVID-19 pandemic. COVID-19 is not as contagious as measles and not as likely to kill an infected person as Ebola, but people can start shedding the virus several days in advance of symptoms (Bai et al., Citation2020; Rothe et al., Citation2020). As a result, asymptomatic people transmit COVID-19 before they know to self-isolate or take other measure like physical distancing in public or wearing mouth/nose coverings to prevent spread of the virus through speaking, coughing, or sneezing. With very limited testing in many countries, also due to the unavailability of tests, unknowingly asymptomatic transmission is thought to be substantive (Li et al., Citation2020). reveals the rapid increase in and spread of confirmed COVID-19 cases from its epicenter (ECDC 2020).

Figure 2. Global distribution of COVID-19 Cases (Jan-March 2020). Data Source: ECDC (2020).

Observed impacts

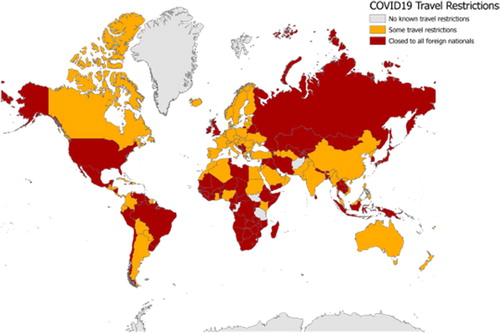

As the number of COVID-19 cases exploded and spread globally, travel restrictions spread out from the Wuhan region epicenter (local lockdown beginning 23 January) to most countries by the end of March. shows countries with borders closed to movement of non-citizens and non-residents as of 31 March 2020 and partial border closures, including restrictions of people arriving from certain other countries or where not all types of borders are closed (air, land, sea). Using country population data, it can be estimated that over 90% of the world’s population are in countries with some level of international travel restrictions and many of these countries also have some degree of restrictions on internal movement, including limited air travel and stay at home orders. This unprecedented response closed borders in a wide range of industrialized countries to all foreign nationals, and virtually all other countries have implemented at least some travel restrictions, including travel bans from selective countries, arrival quarantines, and/or health certificate requirements.

Figure 3. COVID-19 related global travel restrictions (as of 31 March). Data sources: Authors compiled from IATA (2020), International SOS Security Services (Citation2020), and country travel advisory/restriction websites on 31 March.

The rapid emergence, scientific understanding, and NPI responses to COVID-19 evolved over approximately eight weeks, and tourism organizations struggled to comprehend the scope of what was happening: The uncertainty and dynamics of the pandemic and policy responses is exemplified in estimates of COVID-19 impacts on the sector by the United Nations World Tourism Organization (UNWTO), which were significantly revised between early and late March. A 6 March 2020 press release from UNWTO (Citation2020a) estimated the pandemic would cause international tourist arrivals to decline 1-3% (compared to 2019) rather than the forecasted 3-4% growth. Three weeks later, on 26 March, a press release updated this assessment to a 20-30% loss in international arrivals (UNWTO 2020b). These major modifications demonstrate the difficulty of projections at this time, so that all estimates of eventual consequences for tourism must be interpreted with extreme caution, and are at best indicative at present.

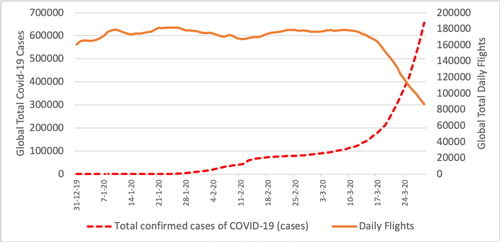

As a result of travel restrictions and lockdowns, global tourism has slowed down significantly, with the number of global flights dropping by more than half (): as case numbers rose, travel bans grounded a growing number of carriers. Passenger numbers are likely to have declined even more steeply, as many airlines adopted specific seating policies to maintain a distance between customers. As an example, Air New Zealand’s seating restrictions to meet government requirements of social distancing imply that the airline is flying at less than 50% capacity even when “full” (Air New Zealand, Citation2020).

Figure 4. Daily global COVID-19 cases and global flights. Data sources: ECDC (2020), FlightRadarCitation24 (Citation2020).

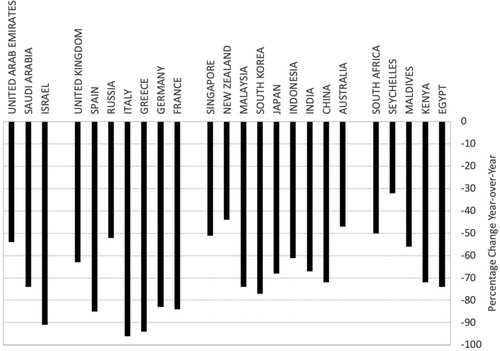

The impact of the crisis on the accommodation sector is illustrated in for the week of 21 March, in comparison to the same week in 2019. In all countries, guest numbers have declined significantly, by 50% or more. The hardest hit were countries heavily exposed to the crisis with large case numbers causing dramatic newspaper headlines (Italy) as well as countries imposing drastic measures to restrict movement in the population (Greece, Germany). Countries that appear to have fared better (Seychelles, Sweden, New Zealand) may still have had large visitor numbers in March, with tourists considering to ride out the crisis in countries perceived as safer. However, even in those situations, tourists are being asked by many countries to return home.

Figure 5. Accommodation occupancy rate change for the week of 21 March (year over year). Data source: STR (2020a)

In one of the fastest reports on the impact of the COVID-19 crisis on national tourism, the Norwegian tourism organization NHO Reiseliv (Citation2020) published longitudinal (weekly) survey data on 31 March 2020. By 5 March 2020, 41% of member businesses had registered cancellations, including hotels, camp sites, gastronomy, car rental, activities, and destination marketing organizations. By 26 March 2020, 90% of member businesses had temporarily laid off staff, with 78% of businesses reducing at least three quarters of the workforce. Hotels and gastronomy, as well as attractions reported the largest decline in their staff numbers, while car rental and camping sites were less exposed. With regard to the latter, the structure of Norwegian camp sites – offering more space – as well as the fact that the season has not started yet help explaining the comparably better situation for these subsectors. However, on 26 March 2020, 65% of tourism businesses already reported difficulties in paying invoices. Liquidity problems were most relevant for cafés and restaurants (72%) as well as hotels (63%); in comparison, DMOs reported the best liquidity (55% still in a position to pay). The report also shows that tourism was hit particularly hard in comparison to other economic sectors in Norway, where seafood, oil and gas, shipping and other industries did not report major impacts. Following tourism, services and retail reported the greatest pressure, temporarily laying off half of their workforce.

In the United States, consultancies such as McKinsey and Company (Citation2020c) have reported that jobs in the accommodation and food services sector account for over 20% of all vulnerable positions, i.e. jobs that are subject to furlough, layoffs, or being unable to work as a result of social distancing. In terms of actual numbers this definition accounts for a lower estimate of 10.5 million sector workers and a higher estimate of 12.6 million in the accommodation and food services sector (McKinsey and Company, Citation2020c). Among the overall estimated 13.4 million jobs that McKinsey and Company (Citation2020c) suggest could be affected in the restaurant industry, 3.6 million involve food preparation and serving (includes fast food businesses), 2.6 million restaurant servers and 1.3 million restaurant cooks are vulnerable. While these represent industry figures, they do illustrate the dire situation of many service workers. Significantly, workers in the accommodation and food services sector have the lowest annual earnings and the lowest levels of education of all sectors indicating the way in which the pandemic may serve to reinforce already substantial disparities in income. Indirectly, the pandemic shines a light on social welfare and job security in tourism, with differences in service employment models underlining vulnerabilities in North America in comparison to for example Europe (Gössling et al., Citation2020).

Projected impacts

Various industry organizations have already published estimates of the consequences of COVID-19 for the global tourism industry in 2020. As indicated, these estimates need to be treated with extensive caution, as it remains fundamentally unclear how the pandemic will develop until September, and how travel restrictions and massive job losses will impact tourist demand during the important northern hemisphere summer season and beyond. While no organization has a crystal ball, the anticipated magnitude of the impact is vital to understand COVID-19 is no ordinary shock to global tourism and has no analogue since the massive expansion of international tourism began in the 1950s.

As highlighted, UNWTO (2020b) has projected a 20-30% decline in 2020 international arrivals that would translate into losses of tourism receipts of US$300-450 billion. Much higher is the estimate by WTTC (2020), anticipating a loss of up to US$2.1 trillion in 2020. Though very significant fiscal and monetary programs have already been implemented, it is currently unclear how these will profit the tourism sector, or whether they will stimulate tourism demand. The following sections discuss industry expectations and provide an outlook for major tourism subsectors, including aviation; accommodation; meetings, incentives, conferencing & exhibitions (MICE) and sporting events; restaurants; and cruises. For anyone employed in global tourism, the current crisis will also have become a personal one, as many businesses have already laid off most of their staff. A key question for all tourism subsectors is thus when travel – international as well as domestic -, or when tourism and hospitality businesses such as accommodation, cafés, or restaurants can reopen.

Airlines

The IATA estimate that revenue passenger kilometers (RPK) will be -38% lower in 2020 than in 2019, with a resulting revenue loss of US$252 billion (IATA, 2020), which can be compared to the expectation of a net profit of US$29 billion in 2020 (IATA, Citation2019). As outlined, at least three airlines (Scandinavian Airlines, Singapore Airlines, Virgin) and German tour operator TUI have already received in excess of US$15 billion in state aid, while US$50 billion have been awarded to US passenger airlines (Reuters, Citation2020). As IATA explained, most airlines have less than three months liquidity, and will not survive an extended period of air transport restrictions (IATA, 2020). illustrates expectations under the assumption that travel restrictions will be lifted by July. Airports, just like airlines, are also facing a financial crisis, with estimated losses of US$76.6 billion in 2020 (Airports Council International, 2020). In light of the very substantial state aid contributions, and industry pressure to postpone decarbonization efforts (Carbon Brief, Citation2020), climate campaigners have already called on governments to bail out airlines only on conditions, including a focus on workers, emission reductions, carbon pricing, or levies on frequent flying (Stay Grounded 2020).

Table 2. Estimated impact of three-month lockdown on 2020 air travel capacity.

Accommodation

With most hotels being closed or experiencing vastly lower tourism numbers, 2020 industry revenue forecasts point to a significant decline (e.g., US hotel revenue per available room is forecast to decline 50.6% STR, 2020b). Domestic markets can be anticipated to recover first. It is currently unclear how accommodation businesses can make sure that rooms are safe for newly arriving guests, or how individual COVID-19 cases occurring in accommodation establishments would be handled. In particular large chains will also have to reconsider their global supply chains, and the dependency structures these have created.

MICE and sport events

As most countries plan to avoid a peaking in COVID-19 cases that would exceed hospital capacity, social distancing will remain a major part of NPI strategies to limit the speed of the pandemic for several months. This will mean that all forms of events in which larger groups of people meet will be restricted, including events as diverse as concerts, meetings, conferences, sports, or large family gatherings (e.g., weddings). Major sports leagues across Europe and North America and other countries have all ended their seasons with the opening of others including the 2020 Summer Olympic Games or the UEFA EURO 2020 postponed. The combined economic impact is not yet known but will be in the hundreds of billions of US dollars. This will also have repercussions for associated businesses such as caterers. The MICE and sports tourism markets could thus be one of the hardest hit tourism subsectors.

Restaurants

With restaurant closures in most countries, and an expectation that social distancing will have to remain a key strategy to manage COVID-19 in many countries for several months, it can be expected that restaurants will face problems recovering, specifically as they usually have limited liquidity and small profit margins. Where restaurants are allowed to stay open for take-away customers, this is an operational alternative, also requiring fewer staff. Many smaller places, including cafés, may however have decided to stay closed, as diminished customer flows do not make it possible to operate at a plus. The initial easing of social distancing is likely to advantage fast food over fine-dining restaurants.

Cruises

No other tourism sub-sector has been in the global news as often as cruises, and it is unlikely that cruise ships can sail again before a vaccine is found or unless passengers can be tested before boarding. Rapid tests will not necessary detect early COVID-19 infections, however. Tests are likely to also affect and potentially reinforce risk perceptions. As Moriarty et al. (2020, p. 347) affirm: “Cruise ships are often settings for outbreaks of infectious diseases because of their closed environment, contact between travelers from many countries, and crew transfers between ships”. Prospective travelers are likely to remember the images of passengers quarantined over weeks, and ports unwilling to let them disembark. Discounted prices for cruise trips are likely to make this sector’s economic recovery much more difficult.

A critical uncertainty related to the severity of these impacts is when physical distancing and travel restrictions can be eased and eliminated. The American Enterprise Institute (Citation2020) has outlined four phases of the COVID-19 response and roadmap of measurable milestones or conditions to achieve to move to each phase of restarting the economy. Much of the world is currently in phase one (slow the spread). To move to phase two (initial state/country level reopening) four conditions should be achieved: (1) sustained reduction in new cases for at least 14 days, (2) hospitals are able to treat all patients requiring hospitalization without resorting to crisis standards of care, (3) able to test all people with COVID-19 symptoms, and (4) able to conduct active monitoring of confirmed cases and contact tracing. In phase 2 it is suggested the majority of schools, universities, and businesses can reopen, but that home working should continue where convenient, social gatherings should remain limited to less than 50 people, and those over age 60 and with underlying health conditions should continue to limit contact within their community. Achieving phase two is critical to restarting the tourism economy at local, national and perhaps limited international scales (e.g., intra-European Union travel). Some countries like South Korea are arguably in this phase, but for many major domestic tourism markets, these conditions are not anticipated to be met for 3-8 months. Once a vaccine is developed and received authorization for use, phase three (establish immune protection and life physical distancing) physical distancing restrictions and other NPIs can be lifted. Once phase three and widespread vaccination is completed, global tourism will be safe to recommence. Tremendous research is being done to fast-track the development and testing of vaccines, but the estimated timeline remains 12-18 months. The final phase (rebuild readiness for next pandemic) needs to invest in research and disease monitoring, health care infrastructure and workforce, and improve governance and communication structures. Tourism, in particular air travel and airports, must be part of new international monitoring and rapid response plans. This would also include a better understanding of tourism’s role in pandemics: Air travel and transport more generally support the spread of pathogens, while the sector also contributes to growing pressure on remaining forest ecosystems (through land use or industrial food sourcing), i.e. developments that are seen to increase the likelihood of future pandemics.

Implications for the future of tourism

At the time of writing, the number of COVID-19 infections worldwide exceeded 1.2 million and deaths has surpassed 69,000 (6 April 2020; ECDC 2020) and unemployment figures have risen steeply in many countries (e.g., US Bureau of Labor Statistics, Citation2020), illustrating the grave consequences the pandemic already has for economies. Given the prospect of future pandemics, there is reason to reconsider global economic value chains, and the specific role of tourism as vector and victim in the occurrence of pandemics.

As outlined earlier, tourism is about movement, and transport does act as a vector for the distribution of pathogens at regional and global scales (Gössling, Citation2002; Hall, Citation2020). However, tourism also supports pandemics indirectly. As noted above, there is much evidence that food production patterns are responsible for repeated outbreaks of the corona virus, including SARS, MERS and COVID-19 (Pongsiri et al., Citation2009; Labonte et al., Citation2011). While these originated in Asia, the case can be made against industrialized food production more generally, which has been linked to animal disease outbreaks (OECD, Citation2012). As many tourism businesses source their food from global markets, preferably at the lowest possible cost, and as there are high volumes of food waste involved in tourism operations, the sector supports industrialized food production (Hall & Gössling, Citation2013). Another factor in virus outbreaks are humans interfering with wildlife as a result of deforestation and conversion of remaining wilderness habitat (Barlow et al., 2016; Lade et al., Citation2020). Again, this is linked to industrialized food production, for instance to produce palm oil (Schouten et al., Citation2012). Notably, climate change also exacerbates the risk of pathogen outbreaks, because climate change will lead to human migration and displacement, for example as a result of drought or flooding events (VSF, Citation2018). Tourism is a major source of emissions of greenhouse gases, and thus a factor increasing the risk of pandemics both directly and indirectly.

The COVID-19 pandemic should lead to a critical reconsideration of the global volume growth model for tourism, for interrelated reasons of risks incurred in global travel as well as the sector’s contribution to climate change. Tourism ‘success’ has been historically defined by virtually all tourism organizations - UNWTO, ICAO, CLIA, or WTTC - as growth in tourism numbers. This perspective has already been questioned in the context of the global financial crisis (Hall, Citation2009) and as the challenges of over tourism, climate change and COVID-19 pandemic further illustrate, this perspective is outdated. Even though growth lobbyists regularly pay lip service to climate change and the SDGs, there is no evidence-based strategy for climate change mitigation, and an overall silence regarding pandemic and other risks the global tourism system imposes on itself and the global economy (Scott et al., Citation2019). Volume growth agendas appear to be driven by individuals and large businesses profiting from such growth models. Specifically, this includes industries represented by ICAO, CLIA, or WTTC, the platform economy (e.g. Booking and AirBnB), aircraft manufacturers such as Boeing and Airbus, national DMOs, and individual large tourism corporations. The UNWTO is a notable case of a supranational organization that is responsible for advancing the SDGs in their entirety, yet in its current form represents a growth advocacy platform (Gössling et al., Citation2016; Hall, Citation2019).

The COVID-19 crisis should thus be seen as an opportunity to critically reconsider tourism’s growth trajectory, and to question the logic of more arrivals implying greater benefits. This may begin with a review of the positive outcomes of the COVID-19 pandemic. For example, as a result of the significant decline in demand, airlines have begun to phase out old and inefficient aircraft (Simple Flying, Citation2020). Video-conferences, a missed opportunity to reduce transport demand (Banister & Stead, Citation2004) for years, has become widely adopted by home office workers, including students forced into distance learning, and business travelers avoiding non-essential air travel. As affirmed by Cohen et al. (Citation2018), many business travelers will welcome opportunities to fly less. Importantly, even high-level exchanges, such as the G20 Leader’s meeting on 26 March 2020, have for the first time been organized through videoconference (European Council, Citation2020). After months of these new work arrangements, for how many organizations and workers will perceive benefits of continued or partial adoption? More generally, views on mobility may also have changed in everyday contexts, as countries without full lockdown responses appear to have seen a significant rise in cycling and outdoor activities.

These ongoing positive changes may be seen as precursors for change on a broader level that will lead the global tourism system reoriented towards the SDGs, rather than “growth” as an abstract notion benefitting the few (Piketty, Citation2015). To this end, resilience research in tourism has highlighted the need to consider the zero-carbon imperative in combination with destination models seeking to reduce leakage, and to better capture and distribute tourism value (Hall, Citation2009; Gössling et al., Citation2016). There may be an insight that tourism in its current form is not resilient, as profitability and liquidity are often marginal; a situation owed to overcapacity in air transport and accommodation, which again can be linked to subsidies, market deregulation, and the apparent disinterest of policy makers to address disruptive developments such as the global rise of AirBnB.

These general findings regarding the need for economic change can be contrasted with business expectations to get “back to normal”, and to possibly overcompensate for lost revenue. It can also be expected that in a situation of global recession (possibly depression), austerity will prompt for calls to cancel existing attempts to introduce even modest carbon-pricing. Calls in this regard have already been heard from directions as diverse as the Global Warming Policy Forum to German car makers (Euractiv, Citation2020; GWPF, Citation2020). Adding to this pressure is an historically low oil price (US$23 at the end of March 2020; Bloomberg, Citation2020), which may, exacerbated by competition in slowly recovering tourism markets, lead to price-driven competition specifically in the most energy-intense tourism subsectors, aviation and cruises. Notably, the price of air transport has declined by 60% over the past 20 years (IATA, 2018). Yet, if there is one message that should be heeded by global policy makers, it is that the pandemic is an analogue to unmitigated climate change. Climate change risks have begun to be tangible, will build up over time, and include the added risk of tipping points (Lenton et al., Citation2019).

Complementing these business and policy perspectives is the question of changes in consumer behaviour and travel demand. Behaviour is influenced by a number of factors that include personal economic wellbeing and disposable income, changes in cost, perceived health risks, and changed capacities for consumption as a result of pandemic restrictions (Lee & Chen, Citation2011). As Fan et al. (Citation2018, p.132) commented, ‘Intense media coverage may lead populations to overreact to mild pandemics’, affirming that behaviors are strongly influenced by the communication of information from news and social media (Kantar, Citation2020; Kristiansen et al., Citation2007).

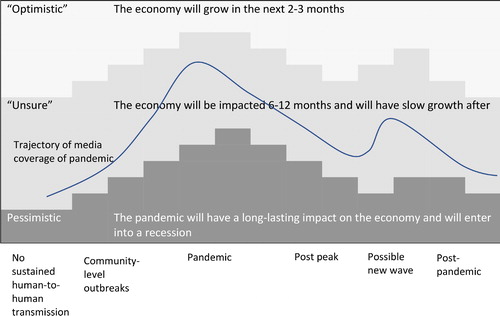

After conducting consumer sentiment surveys across China, Italy, Spain, UK and the US McKinsey and Company (Citation2020a) suggest that consumer optimism will be higher at the start/end of the pandemic, and vary between countries. In the case of China, the first country to go through the various stages of the COVID-19 pandemic, McKinsey and Company (Citation2020b) found consumers were regaining confidence, and interestingly, a greater interest in environmentally friendly products. The pattern identified in consumer surveys is to be expected as it closely follows the notion of an issue-attention cycle across the different stages of an issue, problem or perception of risk (see ; Hall, Citation2002). According to Downs (Citation1972), modern publics attend to many issues in a cyclical fashion. A problem “leaps into prominence, remains there for a short time, and then, though still largely unresolved, gradually fades from the center of public attention” (1972, p.38). The 2003 SARS outbreak illustrates this well, as tourism growth to Asia picked up very quickly once the perceived threat diminished (McKercher & Chon, Citation2004).

Figure 6. Changes in consumer sentiment over the stages of a pandemic. Source: Authors.

Conclusions

This rapid assessment has provided an overview of the ongoing crises up to the end of March 2020, and discussed how it compares to earlier crises. With the magnitude of the COVID-19 pandemic, there is an urgent need not to return to business-as-usual when the crisis over, rather than an opportunity to reconsider a transformation of the global tourism system more aligned to the SDGs. This raises a considerable number of related questions and research needs, i.e. whether the pandemic will support nationalism and tighter borders even in the longer-term; the role of domestic tourism in the recovery and the longer-term transformation to more resilient destinations; the behavioral demand responses of tourists in the short- and longer-term, including business travel and widespread adoption of videoconferencing; the financial stimulus and its consequences for austerity and climate change mitigation; as well as the world’s perspectives on the SDGs. Specifically, with regard to the latter, the pandemic raises questions of vulnerability, as low-paid jobs in tourism have been disproportionately affected by the crisis and early indications are the tourism impacts in lower income countries will be disproportionately considerably greater. COVID-19 provides striking lessons to the tourism industry, policy makers and tourism researchers about the effects of global change. The challenge is now to collectively learn from this global tragedy to accelerate the transformation of sustainable tourism.

Acknowledgement

The authors gratefully acknowledge the cartography of Jaydeep Mistry (Department of Geography and Environmental Management, University of Waterloo, Canada) for and . We are also grateful for fast and insightful comments by four anonymous reviewers.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Air New Zealand. (2020). COVID-19 FAQs. Retrieved April 6, 2020, from https://www.airnewzealand.co.nz/covid19-faqs

- Airports Council International. (2020). The impact of COVID-19 on the airport business. Retrieved April 6, 2020, from https://aci.aero/wp-content/uploads/2020/03/200401-COVID19-Economic-Impact-Bulletin-FINAL-1.pdf

- Al-Tawfiqef, J. A., Zumlaad, A., & Memis, Z. A. (2014). Travel implications of emerging coronaviruses: SARS and MERS-CoV. Travel Medicine and Infectious Disease, 12(5), 422–428. https://doi.org/10.1016/j.tmaid.2014.06.007

- American Enterprise Institute. (2020). National coronavirus response: A road map to reopening. Retrieved April 6, 2020, from https://www.aei.org/wp-content/uploads/2020/03/National-Coronavirus-Response-a-Road-Map-to-Recovering-2.pdf

- Anderson, R. M., Heesterbeek, H., Klinkenberg, D., & Hollingsworth, T. D. (2020). How will country-based mitigation measures influence the course of the COVID-19 epidemic? The Lancet, 395(10228), 931–934. https://doi.org/10.1016/S0140-6736(20)30567-5

- Bai, Y., Yao, L., Wei, T., Tian, F., Jin, D.-Y., Chen, L., & Wang, M. (2020). Presumed asymptomatic carrier transmission of COVID-19. JAMA, 323(14), 1406. https://doi.org/10.1001/jama.2020.2565

- Baldwin, R., & Weder di Mauro, B. (2020). Introduction. In R. Baldwin & B. Weder di Mauro (Eds.), Economics in the time of COVID-19 (pp. 1–30). CEPR Press.

- Banister, D., & Stead, D. (2004). Impact of information and communications technology on transport. Transport Reviews, 24(5), 611–632. https://doi.org/10.1080/0144164042000206060

- Barlow, J., Lennox, G. D., Ferreira, J., Berenguer, E., Lees, A. C., Nally, R. M., Thomson, J. R., Ferraz, S. F. d B., Louzada, J., Oliveira, V. H. F., Parry, L., Ribeiro de Castro Solar, R., Vieira, I. C. G., Aragão, L. E. O. C., Begotti, R. A., Braga, R. F., Cardoso, T. M., de Oliveira, Jr, R. C., Souza Jr, C. M., … Gardner, T. A. (2016). Anthropogenic disturbance in tropical forests can double biodiversity loss from deforestation. Nature, 535(7610), 144–147. https://doi.org/10.1038/nature18326

- Barry, J. M. (2004a). The site of origin of the 1918 influenza pandemic and its public health implications. Journal of Translational Medicine, 2(1), 3.

- Berry, B., Gamieldien, J., & Fielding, B. C. (2015). Identification of new respiratory viruses in the new millennium. Viruses, 7(3), 996–1019. https://doi.org/10.3390/v7030996

- Bloom, D. E., & Cadarette, D. (2019). Infectious disease threats in the 21st Century: Strengthening the global response. Frontiers in Immunology, 10, 549. https://doi.org/10.3389/fimmu.2019.00549

- Bloomberg. (2020). Brent crude. Retrieved April 4, 2020, from https://www.bloomberg.com

- Brown, A., Ahmad, S., Beck, C., & Nguyen-Van-Tam, J. (2016). The roles of transportation and transportation hubs in the propagation of influenza and coronaviruses: A systematic review. Journal of Travel Medicine, 23(1), tav002. https://doi.org/10.1093/jtm/tav002

- Burkle, F. M. Jr, (2006). Globalization and disasters: Issues of public health, state capacity and political action. Journal of International Affairs, 59(2), 231–265.

- Burns, A., van der Mensbrugghe, D., & Timmer, H. (2006). Evaluating the economic consequences of avian influenza. World Bank.

- Business Insider. (2020). UK airline Flybe declares bankruptcy as coronavirus dooms the already struggling carrier. Retrieved March 31, 2020, from https://www.businessinsider.de/international/uk-airline-flybe-declares-bankruptcy-flights-grounded-2020-3/?r=US&IR=T

- Byerly, C. R. (2010). The U.S. military and the influenza pandemic of 1918–1919. Public Health Reports, 125(3_suppl), 81–91. https://doi.org/10.1177/00333549101250S311

- Carbon Brief. (2020). Airlines lobby to rewrite carbon deal in light of coronavirus. Retrieved April 14, 2020, from https://www.carbonbrief.org/daily-brief/airlines-lobby-to-rewrite-carbon-deal-in-light-of-coronavirus

- Chowell, G., & Nishiura, H. (2014). Transmission dynamics and control of Ebola virus disease (EVD): A review. BMC Medicine, 12(1), 196. https://doi.org/10.1186/s12916-014-0196-0

- CNN. (2020). What will travel look like after coronavirus? Retrieved March 31, 2020, from https://www.cnn.com/travel/article/coronavirus-travel-industry-changes/index.html

- Cohen, S. A., Hanna, P., & Gössling, S. (2018). The dark side of business travel: A media comments analysis. Transportation Research Part D: Transport and Environment, 61, 406–419. https://doi.org/10.1016/j.trd.2017.01.004

- Coker, R. J., Hunter, B. M., Rudge, J. W., Liverani, M., & Hanvoravongchai, P. (2011). Emerging infectious diseases in southeast Asia: regional challenges to control. The Lancet, 377(9765), 599–609. https://doi.org/10.1016/S0140-6736(10)62004-1

- Condé Nast Traveller. (2020). Before and after: How coronavirus has emptied tourist attractions around the world. Retrieved March 31, 2020, from https://www.cntravellerme.com/before-and-after-photos-tourist-attractions-during-coronavirus

- Cordesmeyer, M., & Papathanassis, A. (2011). Safety perceptions in the cruise sector: A grounded theory approach. In P. Gibson, A. Papathanassis, & P. Milde (Eds.) Cruise sector challenges (pp. 127–146). Gabler Verlag.

- Dodds, R., & Butler, R. (Eds.). (2019). Overtourism: Issues, realities and solutions. De Gruyter.

- Downs, A. (1972). Up and down with ecology – the issue attention cycle. Public Interest, 28, 38–50.

- Euractiv. (2020). Coronavirus-hit carmakers urge EU to pull legislative handbrake. Retrieved April 4, 2020 from https://www.euractiv.com/section/transport/news/coronavirus-hit-carmakers-urge-eu-to-pull-legislative-handbrake

- European Centre for Disease Prevention and Control (ECDC). (2020). COVID-19 Situation update worldwide. Retrieved April 4, 2020, from https://www.ecdc.europa.eu/en/geographical-distribution-2019-ncov-cases

- European Council. (2020). Statement by President Michael and President von der Leyen after the extraordinary G20 video conference on COVID-19. Retrieved April 4, 2020, from https://www.consilium.europa.eu/en/press/press-releases/2020/03/26/statement-by-president-michel-and-president-von-der-leyen-after-the-g20-video-conference-on-covid-19/

- Fan, Y. Y., Jamison, D. T., & Summers, L. H. (2018). Pandemic risk: how large are the expected losses? Bulletin of the World Health Organization, 96(2), 129–134. https://doi.org/10.2471/BLT.17.199588

- Fauci, A. S., & Morens, D. M. (2012). The perpetual challenge of infectious diseases. New England Journal of Medicine, 366(5), 454–461. https://doi.org/10.1056/NEJMra1108296

- FCO (The Foreign & Commonwealth Office). (2020). Foreign Secretary advises all British travelers to return to the UK now. Retrieved March 31, 2020, from https://www.gov.uk/government/news/foreign-secretary-advises-all-british-travellers-to-return-to-the-uk-now

- Ferguson, N. M., Cummings, D. A., Fraser, C., Cajka, J. C., Cooley, P. C., & Burke, D. S. (2006). Strategies for mitigating an influenza pandemic. Nature, 442(7101), 448–452.

- FlightRadar24. (2020). Total number of flights tracked by Flightradar24, per day, last 90 days. https://www.flightradar24.com/data/statistics

- Forbes. (2020). What will travel be like after the coronavirus? Retrieved March 31, 2020, https://www.forbes.com/sites/christopherelliott/2020/03/18/what-will-travel-be-like-after-the-coronavirus/#4febdd623329

- Garrett, T. A. (2008). Economic effects of the 1918 influenza pandemic: Implications for a modern-day pandemic. Federal Reserve of St. Louis. https://doi.org/10.20955/r.90.74-94

- Gössling, S. (2002). Global environmental consequences of tourism. Global Environmental Change, 12(4), 283–302. https://doi.org/10.1016/S0959-3780(02)00044-4

- Gössling, S., Fernandez, S., Martin-Rios, C., Pasamar, S., Fointiat, V., Isaac, R. K., & Lunde, M. (2020). Restaurant tipping in Europe. A comparative assessment. Current Issues in Tourism, https://doi.org/10.1080/13683500.2020.1749244

- Gössling, S., Ring, A., Dwyer, L., Andersson, A. C., & Hall, C. M. (2016). Optimizing or maximizing growth? A challenge for sustainable tourism. Journal of Sustainable Tourism, 24(4), 527–548. https://doi.org/10.1080/09669582.2015.1085869

- Greger, M. (2007). The human/animal interface: Emergence and resurgence of zoonotic infectious diseases. Critical Reviews in Microbiology, 33(4), 243–299. https://doi.org/10.1080/10408410701647594

- GWPF. (2020). SOS: EU urged to put economic survival ahead of Green Deal. Retrieved April 4, 2020, from https://www.thegwpf.com/sos-eu-urged-to-put-economic-survival-ahead-of-green-deal/

- Hall, C. M. (2009). Degrowing tourism: Décroissance, sustainable consumption and steady-state tourism. Anatolia, 20(1), 46–61. https://doi.org/10.1080/13032917.2009.10518894

- Hall, C. M. (2019). Constructing sustainable tourism development: The 2030 agenda and the managerial ecology of sustainable tourism. Journal of Sustainable Tourism, 27(7), 1044–1060. https://doi.org/10.1080/09669582.2018.1560456

- Hall, C. M. (2020). Biological invasion, biosecurity, tourism, and globalisation. In D. Timothy (Ed.), Handbook of globalisation and tourism (pp. 114–125). Edward Elgar.

- Hall, C. M. (2002). Travel safety, terrorism and the media: The significance of the issue-attention cycle. Current Issues in Tourism, 5(5), 458–466. https://doi.org/10.1080/13683500208667935

- Hall, C. M. (2006). Tourism, biodiversity and global environmental change. In S. Gössling & C. M. Hall (Eds.), Tourism and global environmental change: Ecological, economic, social and political interrelationships (pp. 142–156). Routledge.

- Hall, C.M. and Gössling, S. (Eds). (2013). Sustainable culinary systems. local foods, innovation, and tourism & hospitality. Routledge.

- Hatchett, R. J., Mecher, C. E., & Lipsitch, M. (2007). Public health interventions and epidemic intensity during the 1918 influenza pandemic. Proceedings of the National Academy of Sciences, 104(18), 7582–7587. https://doi.org/10.1073/pnas.0610941104

- Holtenius, J., & Gillman, A. (2014). The Spanish flu in Uppsala, clinical and epidemiological impact of the influenza pandemic 1918–1919 on a Swedish county. Infection Ecology & Epidemiology, 4(1), Art. 21528. https://doi.org/10.3402/iee.v4.21528

- Hon, K. L. (2013). Severe respiratory syndromes: Travel history matters. Travel Medicine and Infectious Disease, 11(5), 285–287. https://www.internationalsos.com/pandemic-sites/pandemic/home/2019-ncov/ncov-travel-restrictions-flight-operations-and-screeninghttps://doi.org/10.1016/j.tmaid.2013.06.005

- Huang, C., Wang, Y., Li, X., Ren, L., Zhao, J., Hu, Y., Zhang, L., Fan, G., Xu, J., Gu, X., Cheng, Z., Yu, T., Xia, J., Wei, Y., Wu, W., Xie, X., Yin, W., Li, H., Liu, M., … Cao, B. (2020). Clinical features of patients infected with 2019 novel coronavirus in Wuhan. The Lancet, 395(10223), 497–506. https://doi.org/10.1016/S0140-6736(20)30183-5

- IATA. (2018). Economic Performance of the Airline Industry. Retrieved April 4, 2020, from https://www.iata.org/contentassets/f88f0ceb28b64b7e9b46de44b917b98f/iata-economic-performance-of-the-industry-end-year-2018-report.pdf

- IATA. (2019). After challenging year, improvement expected for 2020. Retrieved April 5, 2020, from https://www.iata.org/en/pressroom/pr/2019-12-11-01/

- IATA Economics. (2020, March 24). COVID-19 updated impact assessment. https://www.iata.org/en/iata-repository/publications/economic-reports/third-impact-assessment/

- International SOS Security Services. (2020). Coronavirus disease (COVID-19) pandemic. https://www.internationalsos.com/client-magazines/novel-coronavirus

- International SOS Security Services. (2020). Travel restrictions, flight operations and screening.

- Jeffery, K. T., & David, M. M. (2006). 1918 influenza: The mother of all pandemics. Emerging Infectious Diseases, 12(1), 15–22.

- Hopkins, J. (2020). Coronavirus COVID-19 global cases by Johns Hopkins CSSE. https://www.arcgis.com/apps/opsdashboard/index.html

- Johnson, N. P., & Mueller, J. (2002). Updating the accounts: global mortality of the ‘Spanish’ 1918–1920 influenza pandemic. Bulletin of the History of Medicine, 76(1), 105–115. https://doi.org/10.1353/bhm.2002.0022

- Jonas, O. (2014). Pandemic risk. World Bank.

- Kantar. (2020). Global study of 25,000 consumers gives brands clearest direction on how to stay connected in a pandemic world. Press Release. http://www.millwardbrown.com/global-navigation/news/press-releases/full-release/2020/03/25/global-study-of-25000-consumers-gives-brands-clearest-direction-on-how-to-stay-connected-in-a-pandemic-world

- Keogh-Brown, M. R., Smith, R. D., Edmunds, J. W., & Beutels, P. (2010a). The macroeconomic impact of pandemic influenza: Estimates from models of the United Kingdom, France, Belgium and The Netherlands. The European Journal of Health Economics, 11(6), 543–554. https://doi.org/10.1007/s10198-009-0210-1

- Keogh-Brown, M. R., Wren-Lewis, S., Edmunds, W. J., Beutels, P., & Smith, R. D. (2010b). The possible macroeconomic impact on the UK of an influenza pandemic. Health Economics, 19(11), 1345–1360. https://doi.org/10.1002/hec.1554

- Khan, K., Arino, J., Hu, W., Raposo, P., Sears, J., Calderon, F., Heidebrecht, C., Macdonald, M., Liauw, J., Chan, A., & Gardam, M. (2009). Spread of a novel influenza A (H1N1) virus via global airline transportation. New England Journal of Medicine, 361(2), 212–214. https://doi.org/10.1056/NEJMc0904559

- Killingray, D. (2003). A new ‘imperial disease’: The influenza pandemic of 1918–9 and its impact on the British Empire. Caribbean Quarterly, 49(4), 30–49. https://doi.org/10.1080/00086495.2003.11829645

- Kristiansen, I. S., Halvorsen, P. A., & Gyrd-Hansen, D. (2007). Influenza pandemic: perception of risk and individual precautions in a general population. Cross sectional study. BMC Public Health, 7(1), 48. https://doi.org/10.1186/1471-2458-7-48

- Labonte, R., Mohindra, K., & Schrecker, T. (2011). The growing impact of globalization for health and public health practice. Annual Review of Public Health, 32(1), 263–283. https://doi.org/10.1146/annurev-publhealth-031210-101225

- Lade, S. J., Steffen, W., de Vries, W., Carpenter, S. R., Donges, J. F., Gerten, D., Hoff, H., Newbold, T., Richardson, K., & Rockström, J. (2020). Human impacts on planetary boundaries amplified by Earth system interactions. Nature Sustainability, 3(2), 119–128.

- Lee, C.-C., & Chen, C.-J. (2011). The reaction of elderly Asian tourists to avian influenza and SARS. Tourism Management, 32(6), 1421–1422. https://doi.org/10.1016/j.tourman.2010.12.009

- Lenton, T. M., Rockström, J., Gaffney, O., Rahmstorf, S., Richardson, K., Steffen, W., & Schellnhuber, H. J. (2019). Climate tipping points—too risky to bet against. Nature, 575(7784), 592–595. https://doi.org/10.1038/d41586-019-03595-0

- Li, R., Pei, S., Chen, B., Song, Y., Zhang, T., Yang, W., & Shaman, J. (2020). Substantial undocumented infection facilitates the rapid dissemination of novel coronavirus (SARS-CoV2). Science, doi: 10.1126/science.abb3221

- Mallapaty, S. (2020). What the cruise-ship outbreaks reveal about COVID-19. Nature, 580(7801), 18–18. doi: 10.1038/d41586-020-00885-w

- Maphanga, P. M., & Henama, U. S. (2019). The tourism impact of Ebola in Africa: Lessons on crisis management. African Journal of Hospitality, Tourism and Leisure, 8(3). https://www.ajhtl.com/uploads/7/1/6/3/7163688/article_59_vol_8_3__2019.pdf.

- Markel, H., Lipman, H. B., Navarro, J. A., Sloan, A., Michalsen, J. R., Stern, A. M., & Cetron, M. S. (2007). Nonpharmaceutical interventions implemented by US cities during the 1918-1919 influenza pandemic. JAMA, 298(6), 644–654. https://doi.org/10.1001/jama.298.6.644

- Markel, H., Stern, A. M., Navarro, J. A., Michalsen, J. R., Monto, A. S., & DiGiovanni, C. (2006). Nonpharmaceutical influenza mitigation strategies, US communities, 1918–1920 pandemic. Emerging Infectious Diseases, 12(12), 1961–1964. https://doi.org/10.3201/eid1212.060506

- McKercher, B., & Chon, K. (2004). The over-reaction to SARS and the collapse of Asian tourism. Annals of Tourism Research, 31(3), 716–719. https://doi.org/10.1016/j.annals.2003.11.002

- McKibbin, W., & Fernando, R. (2020). The global macroeconomic impacts of COVID-19: Seven scenarios (CAMA Working paper 19/2020). Australian National University.

- McKibbin, W. S., & Sidorenko, A. A. (2006). Global macroeconomic consequences of pandemic influenza. Crawford School of Public Policy, Centre for Applied Macroeconomic Analysis, Australian National University, and Lowy Institute for Foreign Policy.

- McKinsey and Company. (2020a). Global surveys of consumer sentiment during the coronavirus crisis. Retrieved April 6, 2020, form https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/global-surveys-of-consumer-sentiment-during-the-coronavirus-crisis

- McKinsey and Company. (2020b). Cautiously optimistic: Chinese consumer behavior post-COVID-19. Retrieved April 6, 2020, from https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/global-surveys-of-consumer-sentiment-during-the-coronavirus-crisis.

- McKinsey and Company. (2020c). The near-term impact of coronavirus on workers. Retrieved April 6, 2020, from https://www.mckinsey.com/industries/public-sector/our-insights/lives-and-livelihoods-assessing-the-near-term-impact-of-covid-19-on-us-workers?

- Moriarty, L. F., Plucinski, M. M., Marston, B. J., Kurbatova, E. V., Knust, B., Murray, E. L., Pesik, N., Rose, D., Fitter, D., Kobayashi, M., Toda, M., Canty, P. T., Scheuer, T., Halsey, E. S., Cohen, N. J., Stockman, L., Wadford, D. A., Medley, A. M., Green, G., Regan, J. J., Tardivel, K., & Richards, J. (2020). Public health responses to COVID-19 outbreaks on cruise ships — worldwide, February–March 2020. MMWR. Morbidity and Mortality Weekly Report, 69(12), 347–352.

- National Academies of Sciences, Engineering, and Medicine. (2017). Global health and the future role of the United States. The National Academies Press.

- National Academies of Sciences, Engineering, and Medicine. (2018). Understanding the economics of microbial threats: proceedings of a workshop. National Academies Press.

- NHO Reiseliv. (2020). Korona-Analyse for reiselivet. Retrieved April 1, 2020, from https://www.nhoreiseliv.no/tall-og-fakta/reiselivets-status-korona/

- Nicolaides, C., Avraam, D., Cueto‐Felgueroso, L., González, M. C., & Juanes, R. (2019). Hand‐hygiene mitigation strategies against global disease spreading through the air transportation network. Risk Analysis, 40(4): 723–740. https://doi.org/10.1111/risa.13438

- Novelli, M., Burgess, L. G., Jones, A., Ritchie, B. W. (2018). No Ebola… still doomed’–The Ebola-induced tourism crisis. Annals of Tourism Research, 70, 76–87. https://doi.org/10.1016/j.annals.2018.03.006

- OECD. (2012). Livestock diseases: Prevention, control and compensation schemes. Organisation for Economic Cooperation and Development (OECD). http://dx.doi.org/10.1787/9789264178762-en

- Osterholm, M. T. (2005). Preparing for the next pandemic. New England Journal of Medicine, 352(18), 1839–1842. https://doi.org/10.1056/NEJMp058068

- Page, S., & Yeoman, I. (2007). How VisitScotland prepared for a flu pandemic. Journal of Business Continuity & Emergency Planning, 1(2), 167–182.

- Peasah, S. K., Azziz-Baumgartner, E., Breese, J., Meltzer, M. I., & Widdowson, M. A. (2013). Influenza cost and cost-effectiveness studies globally–a review. Vaccine, 31(46), 5339–5348. https://doi.org/10.1016/j.vaccine.2013.09.013

- Petersen, E., Wilson, M. E., Touch, S., McCloskey, B., Mwaba, P., Bates, M., Dar, O., Mattes, F., Kidd, M., Ippolito, G., Azhar, E. I., & Zumla, A. (2016). Rapid spread of Zika virus in the Americas – implications for public health preparedness for mass gatherings at the 2016 Brazil Olympic Games. International Journal of Infectious Diseases, 44, 11–15. https://doi.org/10.1016/j.ijid.2016.02.001

- Piketty, T. (2015). About capital in the twenty-first century. American Economic Review, 105(5), 48–53. https://doi.org/10.1257/aer.p20151060

- Pongsiri, M. J., Roman, J., Ezenwa, V. O., Goldberg, T. L., Koren, H. S., Newbold, S. C., Ostfeld, R. S., Pattanayak, S. K., & Salkeld, D. J. (2009). Biodiversity loss affects global disease ecology. BioScience, 59(11), 945–954. https://doi.org/10.1525/bio.2009.59.11.6

- Prager, F., Wei, D., & Rose, A. (2017). Total economic consequences of an influenza outbreak in the United States. Risk Analysis, 37(1), 4–19. https://doi.org/10.1111/risa.12625

- Reuters. (2020). U.S. Senate approves big rescue for struggling aviation sector. Retrieved April 5, 2020, from https://www.reuters.com/article/us-health-coronavirus-usa-bill/u-s-senate-approves-big-rescue-for-struggling-aviation-sector-idUSKBN21C24T

- Rothe, C., Schunk, M., Sothmann, P., Bretzel, G., Froeschl, G., Wallrauch, C., Zimmer, T., Thiel, V., Janke, C., Guggemos, W., Seilmaier, M., Drosten, C., Vollmar, P., Zwirglmaier, K., Zange, S., Wölfel, R., & Hoelscher, M. (2020). Transmission of 2019-nCoV Infection from an Asymptomatic Contact in Germany. New England Journal of Medicine, 382(10), 970–971. https://doi.org/10.1056/NEJMc2001468

- Russy, D. & Smith, R. (2013) The economic impact of H1N1 on Mexico’s tourist and pork sectors. Health Economics, 22(7), 824–834. doi: 10.1002/hec.2862

- Schmidt, C.W. (2016). Zika in the United States: How are we preparing? Environmental Health Perspectives, 124(9), A157–A165.

- Schouten, G., Leroy, P., & Glasbergen, P. (2012). On the deliberative capacity of private multi-stakeholder governance: The roundtables on responsible soy and sustainable palm oil. Ecological Economics, 83, 42–50. https://doi.org/10.1016/j.ecolecon.2012.08.007

- Scott, D., & Gössling, S. (2015). What could the next 40 years hold for global tourism? Tourism Recreation Research, 40(3), 269–285. https://doi.org/10.1080/02508281.2015.1075739

- Scott, D., Hall, C. M., & Gössling, S. (2019). Global tourism vulnerability to climate change. Annals of Tourism Research, 77, 49–61. https://doi.org/10.1016/j.annals.2019.05.007

- Seraphin, H., Sheeran, P., & Pilato, M. (2018). Over-tourism and the fall of Venice as a destination. Journal of Destination Marketing & Management, 9, 374–376. https://doi.org/10.1016/j.jdmm.2018.01.011

- Simple Flying. (2020). United could follow American with early 757 & 767 retirement. Retrieved April 7, 2020, from https://simpleflying.com/united-757-767-early-retirement/

- Siu, A., & Wong, Y. R. (2004). Economic impact of SARS: The case of Hong Kong. Asian Economic Papers, 3(1), 62–83. https://doi.org/10.1162/1535351041747996

- Stay Grounded. (2020). No unconditional airline bailouts -taking care of people, not airlines. Retrieved April 4, 2020, from https://stay-grounded.org/wp-content/uploads/2020/03/Open_Letter_EU_Transport_Ministers.pdf ECDC

- Stay Grounded. (2020). #SavePeopleNotPlanes: Red lines for aviation bail-outs. Retrieved April 8, 2020, from: https://stay-grounded.org

- STR. (2020a) COVID-19: Hotel industry impact. Retrieved April 5, 2020, from. https://str.com/data-insights-blog/coronavirus-hotel-industry-data-news

- STR. (2020b). U.S. hotel RevPAR forecasted to drop 50.6% for 2020. Retrieved April 5, 2020, from https://str.com/press-release/us-hotel-revpar-forecasted-drop-50-point-6-2020

- Taubenberger, J. K., & Morens, D. M. (2006). 1918 Influenza: the mother of all pandemics. Emerging Infectious Diseases, 12(1), 15–22. https://doi.org/10.3201/eid1209.05-0979

- UNWTO. (2020a). COVID-19: UNWTO calls on tourism to be part of recovery plans. https://www.unwto.org/news/covid-19-unwto-calls-on-tourism-to-be-part-of-recovery-plans.

- UNWTO. (2020b). International tourist arrivals could fall by 20-30% in 2020. Retrieved April 5, 2020, from https://www.unwto.org/news/international-tourism-arrivals-could-fall-in-2020

- US Bureau of Labor Statistics. (2020). Nonfarm payroll employment falls by 701,000 in March; unemployment rate rises to 4.4% (3 April 2020). Retrieved April 3, 2020, from https://www.bls.gov

- Viboud, C., & Simonsen, L. (2012). Global mortality of 2009 pandemic influenza A H1N1. The Lancet Infectious Diseases, 12(9), 651–653. https://doi.org/10.1016/S1473-3099(12)70152-4

- Vétérinaires sans Frontières (VSF) Suisse. (2018). Livestock diseases. Surveillance & early warning systems guidelines Handbook. Retrieved April 5, 2020, from http://www.vsf-suisse.org/vsf/files/web/handbooks/VSF-Suisse-Livestock-Disease-Surveillance-and-Early-Warning-Systems-Guidelines-Handbook.pdf

- Washington Post. (2020). US intelligence reports from January and February warned about a likely pandemic. Retrieved April 14, 2020. https://www.washingtonpost.com/national-security/us-intelligence-reports-from-january-and-february-warned-about-a-likely-pandemic/2020/03/20/299d8cda-6ad5-11ea-b5f1-a5a804158597_story.html

- World Bank. (2012). People, pathogens and our planet: Volume 2 – the economics of One Health. World Bank.

- World Bank. (2020a). Air transport, passengers carried. Retrieved April 4, 2020, from https://data.worldbank.org/indicator/is.air.psgr

- World Bank. (2020b). International tourism, number of arrivals. Retrieved April 4, 2020, from https://data.worldbank.org/indicator/ST.INT.ARVL

- Wu, T., Perrings, C., Kinzig, A., Collins, J. P., Minteer, B. A., & Daszak, P. (2017). Economic growth, urbanization, globalization, and the risks of emerging infectious diseases in China: a review. Ambio, 46(1), 18–29. https://doi.org/10.1007/s13280-016-0809-2