Abstract

International political economy (IPE) has explained financial globalization as the result of states deciding to open up and liberalize domestic financial systems. Complementing this ‘negative integration’ view, we present a theory of financial globalization during the 1970s that emphasizes the importance of ‘positive integration.’ Credit money systems are characterized by public-private infrastructural entanglements, the management of which require substantial institutional work by monetary technocrats, both at the domestic and at the international level. To illustrate our theory, we trace the expansion of the Eurodollar market during the 1970s. Drawing on archival records from the ‘Standing Committee on the Euro-currency Market’ at the Bank for International Settlements, we show how this group of G-10 central bankers sought to elevate the management of infrastructural entanglements from the domestic to the international level. By ensuring that the Eurodollar market did not interfere with domestic monetary governability, while seeking to provide protection for issuers of Eurodollars, monetary technocrats helped establish the institutional infrastructure for the expansion and globalization of the offshore US dollar system.

1. Introduction

Today, more than ever, we live in a “dollar world” (Gourinchas, Citation2019). The unit of account of one country, the US dollar, serves as an international trade, reserve, and funding currency. The preeminent source of this international currency is the Eurodollar market, in which banks outside of the United States – ‘Euro’ here is a synonym for ‘offshore’ – make loans and accept deposits denominated in US dollars. The Eurodollar market emerged in London in the late 1950s, before it expanded and consolidated during the 1970s. How did that decisive phase of financial globalization come about? The literature offers two main accounts. Economists view financial globalization as the outcome of market forces – at a time of growing international trade, the demand for dollar deposits and loans increased. The market delivered, while states merely stepped out of the way. By contrast, scholars of International Political Economy (IPE) – without denying the existence of market pressures – insist on the causal primacy of states. The US and UK governments, in particular, saw their interests align with the interests of their internationally expanding financial sectors and therefore made the strategic decision to liberalize financial markets. Despite their differences, however, both explanations view negative integration – the removal of restrictions on capital flows – as a sufficient condition for financial globalization. From this perspective, the growth of transnational capital flows follows automatically from financial liberalization and the elimination of capital controls.

The theoretical argument put forward in this paper is that financial globalization requires more than negative integration. We develop a mid-range theory that explains positive integration as the outcome of technocratic agency within a specific structural context. The structure of credit money is “essentially hybrid,” meaning its creation and circulation involve both public and private elements (Mehrling, Citation2013, Citation2015). In this framework, “infrastructural entanglements” between states and private financial actors are a core feature of the monetary system: States depend on financial markets to exercise monetary control, while private financial institutions issuing credit money depend on public backstops (Braun, Citation2018a). At the level of agency, our theory focuses analytical attention on monetary technocrats – primarily central bankers – defined as public servants acting in and through private markets. Monetary technocrats have agency precisely because they are situated at the boundary between the public and private spheres. While acting by transacting in private financial markets, their state-granted privileges make them dominant actors in those markets, allowing them to “govern through financial markets” (Braun et al., Citation2018). They manage public-private infrastructural entanglement through two types of institutional work – they regulate private banking activities to maintain domestic monetary governability, while at the same time providing backstops and other forms of protection to domestic banks in their international operations.

We develop this argument through a historical study of the work of the Standing Committee on the Euro-currency Market, established in 1971 by the G-10 central banks at the Bank for International Settlements (BIS) in Basel. While Helleiner (Citation1994, pp. 16, 18) noted the emergence of a “Basel-based regime” in the 1970s, the lack of archival records meant that the inner workings of this regime remained a black box even in the most insightful accounts of that period (Hawley, Citation1987; Kapstein, Citation1994; Spiro, Citation1999). Newly available archival evidence allows us to paint a much more nuanced picture of the agency of monetary technocrats – including, especially, European ones – in the rise of the Eurodollar market.

Thus, the historical contribution of this paper is to show that the growth of the Eurodollar market during the 1970s was linked to the creation of an institutional infrastructure supporting and stabilizing offshore credit money. We show that the Standing Committee faced significant epistemic uncertainty about the nature and workings of the Eurodollar market and puzzled over its consequences for domestic liquidity and inflation, and thus for monetary governability. Amidst these discussions in Basel, the Bank of England successfully prevented G-10 central banks from imposing restrictive regulations on the Eurodollar market, arguing that governability was not at risk. We also show that from the beginning, central banks sought to mitigate the risks from Eurodollar transactions for their own domestic banks, notably by incorporating official Eurodollar deposits and Eurodollar swaps in their monetary policy toolkits. Following the 1973–74 oil price shock, the Standing Committee members converged on the view that the private banking system should ‘recycle’ petrodollars held by OPEC countries by making Eurodollar loans to oil-importing developing countries. To encourage banks to engage in risky lending on such a massive scale, central banks assured private banks of liquidity support should large losses materialize, providing a lender-of-last-resort infrastructure at the international level.

While our empirical analysis is limited to the Euro-currency markets in the 1970s, the sophistication of the institutional infrastructure underpinning today’s offshore US dollar system suggests that the scope conditions for our theoretical argument are broader (Murau, Citation2018). The infrastructure of protection that monetary technocrats improvised in the 1970s has expanded into a “global financial safety net” (Henning, Citation2015; McDowell, Citation2017): the lending facilities of the International Monetary Fund (IMF) have multiplied, regional financing arrangements have mushroomed, governments have built up their foreign currency reserve assets, and the Federal Reserve maintains currency swap lines with a substantial number of central banks, six of which are unlimited and unconditional (Sahasrabuddhe, Citation2019; Tooze, Citation2018). At the same time, central banks sought to maintain monetary governability in a world in which domestic economic conditions increasingly became subject to a “global financial cycle” (Bauerle Danzman et al., Citation2017; Rey, Citation2015). The development of inflation targeting and macroprudential regulation can both be seen in that light (Krampf, Citation2019; Thiemann, Citation2019).

The remainder of this article is organized as follows. Section two outlines our positive integration theory of financial globalization, based on three conceptual building blocks – the hybridity of money, the unique institutional position of monetary technocrats, and their management of infrastructural entanglement with a view towards governability and protection. Section three applies this framework to reconstruct the expansion of the Eurodollar market during the 1970s, drawing on original archival material from the BIS. We trace how central bankers worked towards maintaining domestic monetary governability, while incentivizing and protecting Eurodollar lending to developed countries, thus underwriting the acceleration of financial globalization. Section four concludes and presents avenues for future research.

2. Toward a positive integration theory of financial globalization

There is broad agreement that the origins of the most recent historical period of financial globalization can be traced to the birth of the Eurodollar market in 1957 – well before the collapse of the Bretton Woods system in the early 1970s (Burn, Citation2006). What has been debated, however, is the explanation for this “resurrection of global finance” (Cohen, Citation1996). The baseline narrative was given by economists, who emphasize the spontaneous, market-driven nature of global banking. According to this view, the growth of the Eurodollar market during the 1960s was driven by banks seeking to evade domestic restrictions, as well as by the growing demand for trade-related credit (Bell, Citation1973; Johnston, Citation1983). IPE scholars have criticized this economic explanation and stressed the active role of states and of monetary power (Andrews, Citation2006). According to this literature governments made active decisions, on the basis of both domestic and international considerations, to liberalize domestic financial markets and eliminate capital controls (Block, Citation1977; Cohen, Citation1978; Helleiner, Citation1994; Kirshner, Citation1997; Strange, Citation1986; Underhill, Citation1991). Scholars have debated whether the US acted defensively (Frieden, Citation1987; Krampf, Citation2019) or whether, operating from a position of strength, it sought to project monetary and financial power (Gowan, Citation1999; Konings, Citation2011; Strange, Citation1987). Still others have emphasized the role of the International Monetary Fund (Abdelal, Citation2007; Copelovitch, Citation2010; Kentikelenis & Babb, Citation2019).

Their differences notwithstanding, the market-led and state-led views of financial globalization share an under-institutionalized conception of (international) money. In essence, both approaches assume a world in which nation states issue and control national currencies,Footnote1 and in which international capital flows occur naturally if governments allow them. From this perspective, liberalizing domestic financial markets and eliminating international capital controls were sufficient measures to unleash financial globalization. This amounts to a theory of “negative integration” (Scharpf, Citation1999), underpinned by the notion that “the unique mobility and fungibility of money” means that unlike goods or people, money moves easily across national borders. As a consequence, the United States and Britain could create a “more open financial order” simply by providing “financial market operators an extra degree of freedom” (Helleiner, Citation1994, p. 18, see also chapter 9).

The central argument of this paper is that theories of negative integration alone cannot explain financial globalization in general and the emergence of a global offshore US dollar system in particular. Rather, we argue that positive integration played an essential role in the process. We show that the “mobility and fungibility” of US-dollar-denominated liabilities of private banks required a sophisticated institutional architecture that comprised infrastructural entanglements between public and private actors. While this argument is widely accepted for the domestic level, the literature on the international financial system has emphasized the absence of global regulators, a global monetary authority, or a global lender of last resort. The remainder of this section develops the theoretical rationale underpinning our argument that financial globalization requires positive institutional integration also at the international level, achieved first and foremost by monetary technocrats. Our theoretical framework consists of three building blocks – the hybridity of money (2.1), monetary technocrats as actors in their own right (2.2), who manage public-private infrastructural entanglements both at the domestic and at the international level (2.3).

2.1. Hybrid international money

To explain why positive integration is needed for the globalization of financial markets, it is essential to understand the hybrid nature of (international) money (Germain, Citation1997, p. 11). In a credit money system, certain actors’ liabilities are other actors’ money. Private banks enjoy a state-granted privilege in that system – they are allowed to create money in the form of bank deposits (Hockett & Omarova, Citation2017; Ricks, Citation2016). When a bank issues a loan to a borrower, it expands its balance sheets simultaneously on both sides. On the liability side of the bank’s balance sheet, a newly created deposit appears. illustrates this process: a borrower incurs a debt (liability) by taking out a loan from the bank (an asset of the bank). Simultaneously, the bank incurs a liability by depositing the loaned amount into the customer’s account – this claim to be paid central bank money is an asset for the customer and a liability for the bank.

Figure 1. Bank deposit creation as a swap of IOUs.

While most of the monetary instruments used in economic transactions are the liabilities of private financial institutions, payment settlement between them (and between them and the central bank) requires public money, issued by the central bank. This entanglement between public and private instruments and institutions makes the monetary system both “essentially hybrid” and inherently hierarchical (Mehrling, Citation2013; Pistor, Citation2013). Central banks sit atop the hierarchy because their liabilities (‘reserves’) serve as settlement money for commercial banks, and thus as the ultimate liquidity backstop of the system. The second layer consists of the liabilities of commercial banks (‘deposits’), which serve as money for the household sector and the non-financial corporate sector. A third layer consists of the liabilities of shadow bank institutions (such as money market funds and repo dealers), which serve as “shadow money” for other financial and non-financial firms (Gabor & Vestergaard, Citation2016; Murau, Citation2017).

The Euro-currency market, in which banks accept deposits and issue loans denominated in foreign currencies, can be understood as a form of shadow banking system at the international level (Ricks, Citation2016). The regulatory tools of the Bretton Woods period – reserve requirements, caps on deposit rates, international exchange controls – were premised on the assumption that money creation occurs onshore: US banks create money by issuing loans to borrowers in the United States using the US dollar as unit of account, UK banks do the same in the United Kingdom using Pound Sterling, etc. In other words, this “embedded liberalism” (Ruggie, Citation1982) rested on the assumption of the “triple coincidence,” an overlap between the GDP area, the political decision-making unit, and the monetary area (Avdjiev et al., Citation2015). From this perspective, there was no need to manage infrastructural entanglements at the international level. It turned out, however, that money could also be created offshore, denominated in a currency different from that of the country hosting the issuing bank (Murau, Citation2018). Thus, banks located in London began to issue US dollar-denominated loans in the late 1950s, thereby creating ‘Eurodollars’ (Burn, Citation2006). As private banks in other developed countries and borrowers in developing countries joined the Eurodollar market, a global dollar area emerged that existed in parallel to many domestic monetary systems.

Whereas the negative integration hypothesis considers liberalization a sufficient condition for the global expansion of the Eurodollar market, the hybridity view of money implies that this expansion could not have occurred without substantial public institution-building at the international level. Consider why the domestic liabilities of commercial banks, trade ‘at par’ – i.e. at a one-to-one exchange rate – with the liabilities of the central bank. This par relationship is underpinned by a sophisticated public backstop infrastructure for bank deposits, notably in the form of public supervision, deposit insurance, and lender-of-last-resort guarantees. Next, consider shadow bank liabilities, such as money market fund shares. Such “shadow money” lacks explicit public backstops but tends to benefit from market actors’ expectations that concerns over “systemic risk” will bring central banks “accommodation” (Murau, Citation2017; Özgöde, Citation2019). The same need for public protection exists at the international level. If anything, the moneyness of Eurodollar deposits is even more institutionally demanding. Even if a central bank decides to backstop the foreign-currency liabilities of its domestic banks, its ability to do so is limited by its own foreign-currency reserves (Awrey, Citation2018). The problem is further exacerbated by the difficulties in assessing counterparty risk that result from depositors, banks, and borrowers often residing on three different continents – as in the paradigmatic case of petrodollar ‘recycling.’ The task of building institutions that could alleviate these problems in the emerging offshore US dollar system was assumed by monetary technocrats.

2.2. Monetary technocrats: public servants in private markets

The hybridity view of international money implies that financial globalization required an institutional infrastructure at the international level. Who are the actors that can bring about such positive integration? In principle, governments (or states) may cooperate, reach agreements, and establish formal international institutions in order to provide this type of global public good. In practice, however, this task requires a degree of mutual trust and a proximity of the regulator to the regulated that are difficult to achieve for governments, but are the bread and butter of international cooperation by technocrats.

The international agency of national technocrats is well established in IPE. Two broad mechanisms explain the international role of technocrats with formally domestic mandates. First, frequent and regular meetings of national technocrats with their foreign peers inspire mutual trust and spur cooperative behavior at the international level (Keohane, Citation2005; Milner, Citation2009). Second, domestic technocrats are often part of international epistemic communities (Adler & Haas, Citation1992; Haas, Citation1992; King, Citation2005) or global networks (Levi-Faur, Citation2005; Marsh & Rhodes, Citation1992; Stone, Citation2004). Within those communities and networks, international cooperation is facilitated by shared intellectual frameworks (Babb, Citation2007; Clift, Citation2018; Major, Citation2014) and professional norms (Abbott et al., Citation2016; Porter, Citation2003; Seabrooke & Tsingou, Citation2014).

Both mechanisms apply to central bankers. Although they are appointed by and receive their mandates from government, they enjoy significant autonomy in their interactions at the international level (Best, Citation2005; Clement & Toniolo, Citation2005; Kapstein, Citation1992).Footnote2 Their capacity to act with relative autonomy is bolstered by their (carefully cultivated) epistemic authority in a notoriously complex field (Braun, Citation2018b).

An important scope condition for central bankers’ international agency is the organization of international monetary cooperation (Block, Citation1977; Cohen, Citation1978; Fioretos, Citation2019). The Great Depression and World War II reduced the world to a “financially underdeveloped state” (Mehrling, Citation2015, p. 313) and decimated the international network of monetary technocrats (Ikenberry, Citation1992, p. 293). Only with the Bretton Woods system was the network gradually revived (Russell, Citation1973). By the 1960s, central bank governors and their deputies had established “a close personal network and high degree of consultation,” institutionalized in the form of monthly meetings at the BIS in Basel (Spero, Citation1980, p. 153). Helleiner (Citation1994, pp. 16, 18) has described the “increasingly sophisticated ‘regime’ based around the Bank for International Settlements” in the 1970s, while Kapstein (Citation1992) has stopped just short of calling international central bank circles in the 1980s an epistemic community. Recent research on international monetary history, spurred by newly available archival material, provides ample new evidence of the international agency of central bankers from the 1960s to the 1980s (Altamura, Citation2017; Green, Citation2016; Kershaw, Citation2018; Mourlon-Druol, Citation2015).

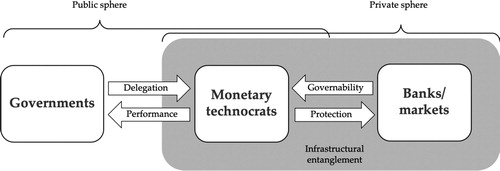

We contribute to the IPE literature by giving an account of the international role of monetary technocrats that also accounts for their special role as intermediaries between the public and the private components of the credit money system. Monetary technocrats are different from other technocrats in that they directly participate in private markets. They govern not only through administrative authority but also (and often primarily) through transactions in financial markets (Braun, Citation2018a; Hockett & Omarova, Citation2015). We capture this special status of monetary technocrats by defining them as publics servants acting in private markets. illustrates the special position monetary technocrats occupy at the interface between states and financial markets.

Figure 2. States, markets, and monetary technocrats in a credit money system.

Source: Authors' own illustration.

2.3. Positive integration through governability and protection

The hallmark of hybrid credit money systems is public-private infrastructural entanglement. Each side provides an indispensable infrastructure to the other – central banks depend on private financial actors to implement monetary policy, while private financial actors depend on central bank liquidity backstops. Regardless of the specifics of their mandates, monetary technocrats therefore pursue two key goals – the governability of the economy, and the protection of private financial institutions from destabilizing losses. Failure to attain these goals hampers financial markets in general, and international markets in particular. We therefore use the concept of “positive integration” to capture that part of central bankers’ institutional work that involves coordination with their foreign peers.

We define governability as the ability to use monetary policy instruments, such as open market operations, to achieve specific policy objectives, such as price stability. Since interest rate signals are propagated via financial markets, the latter are an integral part of the infrastructure of monetary governance (Braun, Citation2018a). To manage this infrastructural entanglement for the purpose of establishing and sustaining monetary governability, central banks have always shaped financial markets – by changing how they transact with private counterparties, by privileging certain types of financial instruments over others, by building up entire market segments, or by lobbying governments for policy changes (Gabor & Ban, Citation2016; Knafo, Citation2013; Krippner, Citation2011; Sissoko, Citation2019; Walter & Wansleben, Citation2019). Abrupt changes on either side of the infrastructural entanglement can put monetary governability in jeopardy. These changes can originate on the public side, as in the case of international monetary regime changes (Krampf, Citation2019), or on the private side. When private actors innovate and financial markets cease to operate according to the central bank’s models and expectations, central banks may reign in innovation and/or adapt their governance techniques. In the case of the Eurodollar market, central banks chose to adapt, notably by entering into Eurodollar transactions with their domestic banks.

The second goal of central bankers is to protect the issuers and users of credit money against losses. This protection, which takes the form of regulatory oversight and liquidity backstops, is an integral part of the infrastructure of private money creation, and is closely intertwined with the notion of “systemic risk” (Özgöde, Citation2019). An important recent contribution has traced the formation of what the authors call the doctrine of “unlimited protection,” which “eliminates the risk of depositor loss […] and prevents any bank of significant size from failing, regardless of whether the bank poses a true systemic risk” (Calomiris et al., Citation2016, p. 50). Whereas Calomiris et al. trace the evolution of this doctrine only at the domestic level, the problem of protection becomes a lot more complicated when domestic financial institutions issue debt instruments denominated in foreign currencies, notably Euro-currency deposits. Since central banks may themselves run out of foreign-currency reserves, offshore credit money raises the question of an international lender of last resort. The long and varied history of the “global financial safety net” offers various examples of attempts to establish emergency lending mechanisms to mitigate the risks associated with cross-border lending and investments (Henning, Citation2015; McDowell, Citation2017). As we will show, important steps in this history were taken by the Standing Committee on the Euro-currency Market.

In sum, governability and protection capture two types of mutual infrastructural entanglements between public and private financial actors – public governance depends on the private issuers of credit money while the private issuance of credit money depends on public backstops. We argue that the expansion of the Eurodollar market in the 1970s required not only liberalization but substantial “positive integration.” This integration was primarily achieved by the monetary technocrats tasked with managing the infrastructural entanglements of the hybrid credit money system. Their institutional work was driven by concerns for monetary governability and protection of private financial actors.

3. Monetary technocrats in action: the BIS standing committee on the euro-currency market, 1971–79

The globalization of the Eurodollar market during the 1970s was a pivotal development in postwar financial history. contextualizes this development in a broader timeline.

Figure 3. Evolution of the Eurodollar market and the rise of financial globalization.

Source: Authors' own illustration.

When the Bretton Woods system was established “there were no functioning private markets” at the international level (Mehrling, Citation2016, p. 26). That is why, when banks in the City of London started dealing in US dollar-denominated bank deposits, this was immediately recognized as a “revolutionary reform of the monetary system” (Einzig, Citation1964, p. x). From the early 1960s, partly driven by the newly introduced Interest Equalization Tax (1963), US banks began to use the Eurodollar market for their own purposes, turning it into an offshore segment of the New York money market (Helleiner, Citation1994, pp. 85–86; Kindleberger, Citation1970, pp. 173–177). During this consolidation period, ‘roundtrip’ transactions, originating and ending in the US, came to dominate the Eurodollar market (He & McCauley, Citation2012).

While Nixon’s closing of the gold window in 1971 thrust the publicly administered monetary system into crisis, the Eurodollar market continued to expand during the 1970s, as it became the dominant channel to recycle petrodollars following the 1973 oil shock (Eichengreen, Citation2019; Kapstein, Citation1994; Spiro, Citation1999). Between 1970 and 1977, the market’s net size increased sevenfold, from USD 60 billion to USD 400 billion (Burn, Citation2006, p. 19). The growth of the private market was accompanied by significant growth of central banks’ ‘official Eurocurrency holdings’ – foreign-currency deposits with Eurobanks used by central banks as substitutes for reserves held in US assets such as treasuries. For US banks, foreign lending became the single largest source of revenue in the 1970s (Guttentag & Herring, Citation1983, p. 2). On the borrower side, developing economies accumulated foreign debt on a massive scale. The foreign interest payments of the twelve largest borrowers increased from $1.1 billion in 1970 (6 percent of their export earnings) to $18.4 billion in 1980 (14 percent of export earnings) (Lipson, Citation1981, p. 603).

While the Euro-currency market included offshore lending denominated in currencies other than the US dollar, Eurodollar deposits dominated, their market share ranging from 72 per cent to 84 per cent between 1964 and 1984 (Battilossi, Citation2010, p. 31). Following the ‘Volcker shock’ in 1979, which helped trigger the debt crisis in Eurodollar-inundated Latin America, the Eurodollar market emerged as the backbone of the international monetary system (Mehrling, Citation2015; Murau, Citation2018).

Our empirical analysis focuses on the Standing Committee on the Euro-currency Market, established in April 1971 by the G-10 central banks under the auspices of the BIS.Footnote3 Our primary sources consist of the archival documents of the Standing Committee, which include background papers and correspondences (henceforth: ‘SCEM’, 1971–79) and the informal records of the conversations taking place in the Committee (henceforth ‘Informal Records’, 1971-1978).Footnote4 The Standing Committee consisted mostly of board-level central bank representatives who met regularly in Basel to discuss and, in some instances, coordinate policies related to the international monetary and financial system. Established at the beginning of the most turbulent period in international monetary affairs since the interwar years, the Standing Committee had no rivals as the effective headquarters of global monetary governance.

At a moment of unprecedented epistemic uncertainty, when even experts had trouble making sense of international monetary developments, much of the Standing Committee’s power derived from its unique position as a high-level forum for collective technocratic puzzling and decision-making. Our analysis reveals a consistent focus on maintaining domestic monetary governability. Central bankers in Basel puzzled over the inflationary impact of the Eurodollar market, negotiated over the appropriate regulatory regime, and built an infrastructure for data collection and dissemination. At the same time, central banks were eager to provide protection for private banks active in the Eurodollar market. Initially they supported the market via their own Eurodollar deposits and swaps with their domestic banks, before providing an implicit backstop guarantee in 1974. With these efforts, central bankers meeting in Basel produced a level of positive integration going well beyond mere liberalization. Monetary technocrats helped globalize the Eurodollar market.

3.1. Maintaining governability

From February 1971 to February 1973, as the Bretton Woods system was disintegrating and inflation rising in advanced economies, the work of the Committee was dominated by concerns of monetary governability. Most committee members worried that “the Euro-currency market has an adverse impact on the effectiveness of domestic monetary policy” (Informal Records, 18 February 1971, Annex I, p. 2). It was this concern that drove the conversion of the Ad hoc Committee on the Euro-currency Market into the Standing Committee, which was tasked to study “the conditions under which the Euro-currency market has an inflationary impact and possible ways and means of reducing or eliminating such impact” (Informal Records, 18 April 1971, p. 1). In other words, the Committee was born from “epistemic uncertainty” (Nelson & Katzenstein, Citation2014, p. 362) and tasked with establishing a shared understanding of the causes and consequences of the Eurodollar market that could serve as new convention to guide the Committee’s work.

3.1.1. Assessing the inflationary impact of the Euro-currency markets

During the first few meetings, the Standing Committee struggled to reconcile the Euro-currency market phenomenon with its then-conventional notions of fractional reserve banking and the money multiplier. This theoretical perspective exaggerated the connection between reserves (liabilities of the Fed), onshore US dollar deposits (liabilities of US banks), and offshore Eurodollar deposits (liabilities of non-US banks). In practice, dramatic changes in bank liability management in the 1960s and 1970s had loosened this connection (Battilossi, Citation2010; Walter & Wansleben, Citation2019). Simply put, banks learned to manage their liabilities with a view towards smoothing payment outflows, thus reducing their need for reserves (or, in the case of Euro-banks, their need for US onshore deposits). The debate over how to reconcile outdated monetary theories with the fast-evolving reality of the Eurodollar market took place both in a series of technical papers (Fratianni & Savona, Citation1971; Friedman, Citation1969; Klopstock, Citation1970; Machlup, Citation1970) and inside the Standing Committee. There, members disagreed on whether autonomous money creation occurred in the Euro-currency markets via “the multiplier effect of the Eurodollar market, which some regard as enabling the Euro-banks to create deposits by granting credits, as national banking systems do” (SCEM, 42-5578 to 42-5587, p. 4). Pointing to epistemic uncertainty, the Banque de France referred to measurement problems and admitted that it had tried to study “the extent of credit creation in the market,” but “without much success” (Informal Records, 17 February 1971, pp. 7–8). In general, Committee members found it “difficult to differentiate between Euro-currency flows and short-term capital flows in general” (Informal Records, 8 January 1972, p. 6).

To settle those questions, the BIS circulated a questionnaire in January 1972 to assess the impact of the offshore Euro-currency markets on the governability of the onshore monetary systems. The central banks’ answers to the questionnaire differed substantially. Germany, France, Italy, Netherlands, Belgium, Switzerland and Canada affirmed that “inflows from or outflows to the Euro-currency market […] have at times interfered with the achievement of the objectives of [our] central bank (a) with respect to domestic monetary management [… and] (b) with respect to the balance of payments” (SCEM, 42-028367). Sweden, the United Kingdom and the United States were agnostic, whereas Japan reported having encountered no problems (Informal Records, 12 February 1972, p. 1). At the same time, Canada, France, Italy, Switzerland and the United States agreed that “flows of Euro-funds had at times helped central banks achieve their objectives,” whereas Belgium, Germany, Japan, Sweden, and the Netherlands disagreed (Informal Records, 12 February 1972, pp. 1-2). Eight central banks believed that the Euro-currency market had “adverse effects on the general inflationary climate,” whereas Canada and the United Kingdom did not. The Federal Reserve argued that the effect was inflationary only if central banks fueled the Euro-currency market “with their own placements” (Informal Records, 12 February 1972, p. 2).

While epistemic uncertainty in the Standing Committee was genuine, the answers to the questionnaire, in particular those of the Bank of England, were conspicuously consistent with national interests (Burn, Citation2006; Helleiner, Citation1994). Where continental Europeans and the Federal Reserve saw potential downsides for governability from the expansion of the Eurodollar market, the Bank of England saw potential upsides. In spite of the inconclusiveness of these results and the ensuing discussions in Basel (Informal Records, 12 February 1972), a report on The Monetary Impact of the Euro-Currency Market listed three areas of agreement: short-term money inflows increased inflationary pressures, thus interfering with domestic monetary governance; international flows were increased by the flow of Euro-funds; and the efficacy of direct controls was “real but limited” (SCEM, 42-6927 to 42-6938, p. 2).

The main effect of the interim report, however, was that the initial assumption guiding the Committee’s work could not be proved. The questionnaire did not yield clear evidence that the Euro-currency markets were inflationary. Instead, central bankers reassured themselves that that Euro-currency markets did not unduly undermine domestic monetary governability.

3.1.2. Negotiating a regulatory regime for the Euro-currency markets

Following the interim report, the Committee was tasked by the G-10 central bank governors with formulating joint regulatory responses to two main questions: First, should the G-10 central banks treat offshore money creation in a given monetary jurisdiction as identical to onshore money creation and therefore introduce international regulations for banks in the Euro-currency markets such as “reserve requirements, guide-lines or ceilings on bank credit” (SCEM, 42-6927 to 42-6938, p. 2); and second, should central banks intervene in the Eurodollar market to restrict the movement of funds and apply policy measures such as controls and open market operations? (SCEM, 42-6927 to 42-6938, p. 3).

From April 1972, a clear conflict emerged that pitted the Bundesbank and the Banca di Italia against the Bank of England, with the Federal Reserve positioned in the middle (Altamura, Citation2017, pp. 89-93). By September 1972, two concrete regulatory proposals were on the table. The Bundesbank suggested that all major countries should impose restrictions such that “the interest rate attraction of the market and its inflationary impact would be considerably reduced” (Informal Records, 9 September 1972, Annex, p. 2). The Bank of Italy proposed that a “regulated area” – the European Common Market member countries in favor of regulation – should be shielded from undesired foreign inflows through reserve requirements and a “Bardepot” (Informal Records, 9 September 1972, Annex, pp. 2–3). Further refined by BIS staff in January 1973 (Informal Records, 10 February 1973, p. 1), these proposals presented – as the Bank of England admitted in an internal memo – “an entirely coherent framework for dealing with problems of monetary flows between the regulated and the outside world” (cited in Altamura, Citation2017, p, 97).

The Committee, however, was unable to reach a consensus. In February 1973, it decided not to implement any of the plans for an international regulatory regime. The Bank of England even requested that the work on Euro-currency market regulation be discontinued (SCEM, 43-33958, p. 1). Was this outcome, which represented a clear victory for the Bank of England, influenced by the deliberations in the Standing Committee? The archival record indicates that the question of monetary governability was at the center of these deliberations. The Bank of England did not ‘win’ by convincing its German and Italian peers that monetary governability was not a problem, which clearly it was in 1970s Britain (Schenk, Citation2010). Instead, the discussions in the Standing Committee continued to be marred by epistemic uncertainty, and the central banks advocating regulation were unable to decide the governability debate in their favor. During the meetings in late 1972 and early 1973, central bankers who initially held strong pro-regulation views accepted the narrative that the Euro-currency markets had some positive and some negative effects on monetary governability (Informal Records, 9 December 1972 & 6 January 1973). In the decisive meeting of February 1973, there was no majority in the Standing Committee to implement international regulations because the case had not been convincingly made that the offshore Eurodollar market impeded the working of the onshore monetary system (Informal Records, 10 February 1973).

3.1.3. Providing technical support for the Euro-currency markets

Once stricter regulation was off the table, the Standing Committee reinforced its efforts to overcome epistemic uncertainty over the nature and dynamics of the Euro-currency markets by collecting and disseminating data about the market. The archival records show that the G-10 central banks decided to collect and publicize data about flows and exposures with the explicit goal of improving private bankers’ ability to assess borrower risk in the Eurodollar market.

The market-facing orientation of the Standing Committee’s data gathering effort was clearly stated in the letter that launched this work. On 7 February 1974, the Secretary General of the OECD wrote to his BIS counterpart that it would be desirable “for the operations of private bankers, if more data could be collected and, if possible, published in a suitable form” (SCEM 44-5070). In a December 1975 meeting of the Standing Committee, Kit McMahon of the Bank of England emphasized the importance of better Euro-currency statistics “so that governments and the banking world would have more to go on in judging how countries’ situations were developing” (Informal Records, 8 December 1975, p. 2, emphasis added). His colleague, John Sangster, defended the idea of publishing data on bank lending to developing countries on the grounds that “the banks that provided these data in the first place would very much like to see the consolidated figures for these countries, from the point of view of their own credit risk management” (Informal Records, 8 December 1975, p. 7, emphasis added).

Beginning in the mid-1970s, banks located in non-G10 financial centers became increasingly important players in the Eurodollar market. Obtaining data from offshore centers such as Singapore, Hong Kong, Bahrain, and Panama therefore turned into a key concern for the Standing Committee. At that point, other international organizations for the first time became interested in the Eurodollar market. The central bankers in the Standing Committee, however, were strictly opposed to any incursions into their Euro-currency jurisdiction. When Kit McMahon of the Bank of England warned that a “number of international institutions – the IMF, the IBRD, the OECD and even the EEC – were becoming increasingly interested in the market, he urged his colleagues to ramp up the BIS’s data operation in order to ward off potential demands from these much larger organizations (Informal Records, 8 December 1975, p. 1). A BIS staff note to Committee Chair René Larre noted a strong preference among Standing Committee members “to have such discussions here in the Standing Committee, rather than leave them to be done by the OECD” (Informal Records, 7 November 1975). René Larre himself was “strongly opposed” to the idea of cooperating with other institutions, “whose presence at meetings would turn the committee into a forum for useless controversies and polemics” (Informal Records, 8 December 1975, p.5).

The controversy highlights the Standing Committee’s self-identification as the technocratic headquarters of the Eurodollar market, distinct from other, more intergovernmental fora of global financial governance. It also shows that central bankers sought to shield the Euro-currency markets from external intervention. In sum, the Standing Committee changed its view of the Euro-currency markets radically between 1971 and 1974. Starting off with grave concerns about their negative consequences for monetary governability, the Committee over time redefined their role from regulators to data infrastructure providers for the Euro-currency markets.

3.2. Protection: towards a lender-of-last-resort infrastructure

A fundamental problem of the international monetary system in the 1970s was – and still is today – the absence of an international lender of last resort (Fischer, Citation1999; Guttentag & Herring, Citation1983; McDowell, Citation2017). When domestic banks accept deposits – and thus incur liabilities – in foreign currencies, the central banks’ ability to backstop the banking system is limited by their own holdings of (or access to) foreign currency reserves. This exacerbates the problem of protection – the backstopping of private credit money by public central banks (Awrey, Citation2018). Our historical analysis reveals that central banks grappled with this problem from the beginning, using official Eurodollar deposits and swaps to stabilize the Eurodollar market. Following the 1973 oil shock, Euro-banks assumed the quasi-public function of ‘recycling’ the large capital surpluses of oil-exporting countries. When the 1974 bank failures exposed the vulnerability of that arrangement, monetary technocrats took the decisive step of providing a coordinated commitment to backstop the market if necessary.

3.2.1. Central bank support, writ small: official deposits and swaps to manage Euro-banks

In the course of their puzzling over the inflationary impact of offshore money, the members of the Standing Committee made a striking discovery – to a considerable extent, they had themselves fueled the growth of the Euro-currency markets. Dating back to at least 1960 (Informal Records, 1 June 1971, p. 18), most central banks in the Standing Committee had conducted sizeable Eurodollar transactions with their domestic banks, in the form of official deposits and swaps. Driven by a desire to stabilize liquidity conditions for the benefit of private banks and of the central bank’s domestic monetary control, these interventions called into question central bankers’ initial view of offshore money as a purely private, market-driven innovation. Official deposits and swaps became a major focus of the Standing Committee’s work in the second half of 1971 (Informal Records, 8 May, 1 June, 10 July and 6 November 1971).

Central bank deposits – which did not, as a rule, require government approval – were part of the institutional infrastructure of the Eurodollar market. Central banks increased the Eurodollar liabilities of their domestic banks by using them as an alternative to conventional foreign exchange assets, such as US government debt. Consider a central bank selling US dollar-denominated assets, such as US government bonds, and transferring the proceeds to a Euro-bank (a non-US commercial bank accepting Eurodollar deposits). In that case, this ‘official deposit’ created both a new Eurodollar liability and a corresponding asset – a deposit with a US bank – for the Euro-bank. Crucially, such central banks deposits “would probably not be placed with foreign commercial banks if there were no Eurodollar market” (SCEM, 42-5578 to 42-5587, p. 4). Official deposits thus increased the net size of the Eurodollar market, with potentially inflationary consequences.

The second type of transaction central banks used for governability purposes were US dollar swaps with commercial banks, whereby central banks sold US dollars spot rate and repurchased them forward. Such swaps could serve a variety of monetary policy purposes: They enabled central banks to control domestic liquidity, slow down increases in their official monetary reserves, repay external debt, facilitate trade finance, and regulate conditions in the exchange market (SCEM, 42-4899 to 42-4910, pp. 2-3). At the same time, swaps provided additional Eurodollar liquidity to Euro-banks. While the Bundesbank thought that swaps expanded the Eurodollar market and wanted to restrict their use, the Banque de France argued that swaps were an important monetary policy instrument and that central banks “should not destroy their existing systems of domestic monetary control for the sake of marginal result” (Informal Records, 10 July 1971, p. 5). While US dollar swaps were used by the majority of central banks, the heaviest users were the Bank of Italy and the Bank of Japan who pursued industrial policy and trade finance goals in addition to monetary policy objectives (Informal Records, 10 July 1971).

Official deposits and swaps were the Eurodollar equivalent of domestic-currency open market operations – a way of managing the infrastructural entanglement between private financial institutions and public monetary policy. By engaging in these transactions, and by using the Eurodollar market to govern domestic monetary and financial conditions, central banks effectively condoned – and bolstered – the Eurodollar market in their jurisdictions. According to estimates of the BIS, 20 percent of the net Euro-currency market consisted of central bank deposits (Informal Records, 8 May 1971, p. 4). The BIS revealed that it had itself made substantial placements (Informal Records, 1 June 1971, p. 4).

Standing Committee members, baffled by these numbers, resolved that G-10 central banks “should not place money directly in the Euro-currency market” except for “exceptional reasons” (Informal Records, 1 June 1971, p. 10). In this case, the Standing Committee was able to reach a consensus over policy measures which were swiftly implemented by all participating central banks. Members felt the need to publicly demonstrate agency. The Bank of England’s Jeremy Morse noted that “there was a lot of agitation going on for something to be done about the Euro-dollar market and it might be a good idea, therefore, to feed those who were calling for action with something” (Informal Records, 1 June 1971, p. 10). The financial press reported that the G10 central banks would “abstain from making further deposits in the market,” possibly even reducing outstanding central bank deposits (Financial Times, 15 June 1971).

The unanimity in the Standing Committee notwithstanding, however, central bank compliance with the informal “standstill agreement” to scale back official deposits proved weak. In early 1972, the Bundesbank’s Otmar Emminger suggested that central banks coordinate their diversification out of dollar assets (such as US government bonds) into Eurodollar deposits, while calling for “a mechanism for shifting central-bank funds, when necessary, out of the Euro-currency market back to the United States” (Informal Records, 6 April 1972, pp. 5, 11). Fears expressed by Committee members in 1978 that their own restraint “would do nothing to stop the growth of other [non-G10] central banks’ Euro-currency deposits” (SCEM, 49-4513, p. 8) suggest that official deposits remained an indispensable component of the Eurodollar market throughout the 1970s.

The failure of central banks to comply with the Standstill Agreement shows that they depended on this tool to both protect their domestic banks in the Eurodollar market and to exercise control over domestic monetary conditions.

3.2.2. Central bank support, writ large: setting up an implicit backstop for Euro-banks

After the Standing Committee had been on the brink of deciding to regulate the Eurodollar market in February 1973, the oil shock in October 1973 brought about an “epochal” shift in its priorities (Altamura, Citation2017, p. 99). Monetary technocrats came to see the Eurodollar market as the solution to the problem of “petrodollar recycling.” The quadrupling of the global oil price between October 1973 and March 1974 created large dollar surpluses in the oil-exporting countries, and deficits for oil-importers. These imbalances created a financial intermediation problem – the surpluses were too large for OPEC countries to spend them entirely on imports, while oil-importing countries needed to borrow in dollars in order to pay for dollar-denominated oil. Although the metaphor of ‘petrodollar recycling’ was apt, it is more instructive to think of the issue as two distinct questions: First, whose liabilities should absorb the oil-exporting countries’ savings in the form of (Euro)dollar credit money balances? And second, who should finance the greatly increased current account deficits of the oil-importing countries?

In principle, the OPEC countries could have done what Japan and China did in the 2000s by investing surpluses directly in US treasuries. In fact, in an agreement that would remain secret for more than two decades, the US encouraged Saudi Arabia to do precisely that (Spiro, Citation1999; Thompson, Citation2017, p. 96). Such direct investments in the liabilities of Western governments and international organizations would have been compatible with a public solution to the second problem: Assuming the role of intermediaries, Western governments and international organizations could have extended loans to developing countries in need of dollars. Such recycling via public balance sheets – the “oil facility” established by the IMF in June 1974 was one example (Kapstein, Citation1994, p. 68) – would have been in line with how international liquidity had been intermediated during the Bretton Woods system. Indeed, most G-10 central banks initially expected this to be the default solution (Kershaw, Citation2018, p. 305). Even private US banks, aware of the risks they would incur in the absence of an international lender-of-last-resort infrastructure, “felt recycling was the proper domain of the government” (Spiro, Citation1999, p. 37).

The key actor pushing for recycling via private financial institutions was the US Treasury, then led by William E. Simon (Kershaw, Citation2018, p. 305).Footnote5 At the time European banks offered higher interest rates than American banks and attracted deposits not only from oil exporting countries but also from US residents. Fearing that a public solution to the recycling problem would further diminish capital inflows to the United States, Simon pushed for recycling via financial markets (ibid.). Bolstered by this US Treasury support, a consensus quickly emerged among bankers and central bankers that petrodollars should be absorbed by private banks (both American and European), and that these banks should make loans to developing countries, as illustrated in (Altamura, Citation2017, p. ch. 3). These loans financed more than oil imports. By mitigating the need for internal adjustment in the Global South, petrodollar recycling also bolstered demand for the exports of fragile developed economies – developing countries became the “borrowers of last resort” of the global economy (Griffith‐Jones, Citation2000, p. 250). This unprecedented expansion of private Eurodollar lending to developing countries could not have occurred without a concomitant expansion of a public infrastructure of protection. One element of that infrastructure was export credit guarantees through which national governments subsidized private bank loans to foreign importers.Footnote6 Another key element was the efforts by monetary technocrats to replicate, at the international level, the semblance of an infrastructure of protection for the Eurodollar market.

Figure 4. Petrodollar recycling via the Eurodollar market.

In the wake of the oil shock, the lender of last resort question featured prominently in Basel. The Standing Committee noted that despite the absence of an international lender of last resort, “the principal central banks could not, in practice, be indifferent to the emergence of major liquidity problems in the market” (SCEM, 45-1137). The problem was aggravated by uncertainty over who would be responsible for foreign branches operating within a central bank’s jurisdiction but in a currency other than its own. In April 1974, Larre circulated a questionnaire (SCEM, 45-0528), submitted by the Dutch central bank, that sought information about each central bank’s interpretation of its “responsibilities as a lender of last resort in relation to Euro-banking operations.” The response of the Bank of Sweden (SCEM, 45-04972) stated particularly clearly that in the unlikely case of a Swedish bank suffering losses on its foreign-currency loans, “it seems unlikely that the central bank would refuse to sell, within limits set by the size of its reserves, the currencies which the commercial bank requires to meet its foreign liabilities.”

The Dutch questionnaire also inquired about “the attitude of the central banks towards their own Euro-market placements.” After the Committee members had agreed, in 1971, to freeze their official placements in the Euro-currency markets, a 1974 paper on “the impact of the oil situation” was ambiguous (SCEM, 44-5651). It noted the need to “avoid adding to the process of ‘reserve creation’ through the Euro-currency market by continuing to abstain from increasing their official Euro-currency deposits.” On the other hand, the paper highlighted that the presence of official central bank deposits during calm periods was likely to create the expectation among commercial banks that central banks would also stand ready to provide liquidity under conditions of market stress. By this logic, abstaining from official placements “could, in the case of a liquidity shortage developing in the Euro-market, conflict with central banks’ responsibilities as lenders of last resort.”

Circulated in April 1974, the lender-of-last-resort questionnaire could not have been timelier. It was followed, in the summer of 1974, by the two most consequential financial events of the 1970s. First, surging interbank lending rates precipitated the first major run on the US interbank money market, the most prominent victim of which was Franklin National Bank, which had moved aggressively into the Eurodollar market (Spero, Citation1980, p. 91). Second, on 26 June 1974, Bankhaus Herstatt, a mid-sized German bank that was active in the Eurodollar market, failed (Schenk, Citation2014). The fallout from Herstatt’s sudden collapse led to the establishment of a second major committee – the Committee on Banking Regulations and Supervisory Practices, subsequently the Basel Committee on Banking Supervision – and had a lasting impact on banking supervision and regulation (Goodhart, Citation2011; Mourlon-Druol, Citation2015).

The Franklin National and Herstatt episodes immediately preceded what could be described as the Eurodollar-market’s “whatever it takes” moment. In meetings of G-6 finance ministers and central bank governors over the weekend of 6-8 September, the pressure on central banks mounted to produce a reassuring announcement regarding lender-of-last-resort support for the Euro-currency markets (Goodhart, Citation2011, pp. 36-40). Following a meeting in Basel on 9 September, the G-10 governors finally published a short joint communiqué on 10 September, the final paragraph of which read:

The Governors also had an exchange of views on the problem of the lender of last resort in the Euro-markets. They recognised that it would not be practical to lay down in advance detailed rules and procedures for the provision of temporary liquidity. But they were satisfied that means are available for that purpose and will be used if and when necessary.

As is usually the case when it comes to the lender-of-last-resort question, the statement is deliberately vague. It is all the more surprising, therefore, that the October edition of Euromoney opened with an editorial that claimed that the actual G10 agreement went above and beyond the official communiqué:

International bankers were profoundly disappointed by the apparent lack of progress at the September Basel meeting of central bankers on support for commercial banks. … In fact, however, not only was there a wider degree of agreement in July then was revealed at the time, but by September this had hardened into a firm commitment by all the countries present (the group of 10 plus Switzerland) on these points: 1. Banks that get into liquidity difficulties with the national boundaries will be supported by the central bank concerned. […] These points were not spelled out in the official communication because of legal constraints on some of the central monetary authorities involved.

The next informal meeting record of the Standing Committee, dating from December 1975, makes no reference to the communiqué. The respective folder in the BIS archive does, however, contain a copy of the Euromoney editorial, followed by a hand-written note in French, signed “RF,” that says (clearly referring to the editorial): “Erroneous interpretation of the ‘Basel Accord’ of 10.9.1974” (“Interpretation erronnée de ‘l’Accord de Bâle’ du 10.9.1974”). We have not been able to determine who wrote the note, nor when.

What had the G-10 central bankers agreed on in Basel? The question was hotly debated among monetary technocrats as well as market participants at the time. Two finance professors and contemporary observers, citing “off-the-record discussions we have had with policy-makers who were directly involved,” speculated that the Euromoney editorial was inaccurate (Guttentag & Herring, Citation1983, p. 20). At a 1977 symposium, however, both Kit McMahon (Executive Director, Bank of England) and Henry C. Wallich (Board of Governors, Federal Reserve) presented papers on the international lender-of-last-resort question, describing the 1974 Basel statement as an expression of the underlying understanding among central bankers that lender of last resort support for Eurodollar banks would be forthcoming if necessary (McMahon, Citation1977; Wallich, Citation1977). Referring specifically to McMahon and Wallich, an IMF paper concluded that “the infrastructure for providing international assistance by lenders of last resort was in place” (Johnson & Abrams, Citation1983, p. 34). The question of the true meaning of the statement notwithstanding, contemporary market participants clearly interpreted it as signaling central bank support for the Eurodollar market. When, in November 1974, Euromoney asked six financial experts whether they expected the “agreement on support for banks in trouble” was “likely to prove of any great practical importance,” one respondent highlighted the positive “psychological effect” of the communiqué, while another expected it would “bolster confidence” (Goodhart, Citation2011, p. 41).

Ultimately, the question of technocratic intent is secondary to our argument, which hinges on market perception. From this perspective, we argue, the message of protection given by the Standing Committee was a necessary condition for rapid expansion and globalization of the offshore US dollar system in the 1970s.

4. Conclusion

This article challenges the view, prevalent in IPE, that the liberalization of financial markets – a form of negative integration, actively pursued by governments – was a sufficient condition for financial globalization during the 1970s. Revisiting the expansion of the Eurodollar market during that pivotal period, we argue that foreign-currency lending by private banks on a global scale required a substantial degree of positive integration.

Our historical analysis focuses on monetary technocrats as the key agents whose institutional work brought about this positive integration. We trace how the Standing Committee on the Euro-currency Market at the BIS in Basel managed the infrastructural entanglements between the public and the private elements of the inherently hybrid Eurodollar system. On one hand, private financial markets serve as the infrastructure through which central banks seek to implement and transmit public monetary policy. The governability of their domestic economies being the principal goal of central banks, they are ready to repress financial innovation – in this case, the Eurodollar market – if it damages the governance infrastructure of monetary policy. On the other hand, central banks sit at the top of a hierarchical monetary and financial system, and therefore serve as the ultimate backstop to the system. This protection constitutes a public infrastructure for the creation of private credit money. Analyzing archival records from the Standing Committee, we show how, by managing these infrastructural entanglements at the international level, monetary technocrats provided the positive integration that underpinned the explosive growth of the Eurodollar market during the 1970s.

Although focused on the 1970s, our analysis yields broader insights for IPE. First, our analysis shows the crucial role that specifically European technocrats, convening in the G-10 setting at the BIS, had in the unfolding of financial globalization (Schelkle and Bohle, forthcoming). The decision reached in 1973 by the Standing Committee not to regulate the Euro-currency markets paved the way for petrodollar recycling on a global scale. At the same time, the intense discussions over the governability implications of financial globalization provided an important impetus for European monetary cooperation and financial integration. The German position in the Standing Committee was generally geared towards preventing international regulatory institutions that would impede monetary union, while the Italian proposal of a ‘regulated area’ would have implied a monetary union of sorts, based on a common offshore currency. These concerns prefigured European monetary technocrats’ aggressive push in the late 1990s to integrate European money markets, as well as their post-crisis push to revive securitization markets. In both cases, central bankers acted in pursuit of monetary governability concerns while actively bolstering the rise and resilience of market-based banking – and thus of financialization – in the euro area (Braun, Citation2018a; Gabor & Ban, Citation2016). The pattern of the pursuit of monetary governability by central banks (and finance ministries) paving the road for financialization has played out repeatedly in various countries, going back to the 1960s (Dutta, Citation2019; Lemoine, Citation2016; Walter & Wansleben, Citation2019). Grasping the unique role of monetary technocrats as public-private intermediaries is key to moving recent debates about technocratic governance in general, and central bank independence in particular, beyond the confines of principal-agent theory (Abbott et al., Citation2019; Jones & Matthijs, Citation2019; Mabbett & Schelkle, Citation2019).

Second, our analysis places the Eurodollar market back at the center of the political economy of financial globalization and financialization. Somewhat paradoxically, little is known about the evolution of the Eurodollar market since the 1980s – the topic all but disappeared from the IPE literature precisely when the Eurodollar market had become the backbone of the international monetary and financial system. Recent research, however, has shown that it is impossible to make sense of financial globalization and US monetary power without a thorough understanding of the offshore dollar system (Binder, Citation2019; Hardie & Maxfield, Citation2016; Hardie and Thompson, forthcoming; Murau, Citation2018; Schwartz, Citation2019).

Closely related, a third question concerns the history of what today is commonly described as the “global financial safety net” (Henning, Citation2015; McDowell, Citation2017). As did the oil crisis of the early 1970s, subsequent episodes of stress in the Eurodollar market – notably the Latin American debt crisis of the early 1980s, the Asian crisis of 1998–99, and the Global Financial Crisis of 2008–09 – spurred monetary technocrats to gradually expand the Eurodollar market’s backstop infrastructure, culminating in the network of (partly unlimited) swap lines between the Fed and a select number of other major central banks (McDowell, Citation2012; Sahasrabuddhe, Citation2019; Tooze, Citation2018). The IPE literature tends to explain the emergence and resilience of this “dollar world” as the result of US monetary power (Andrews, Citation2006). Without denying the importance of state strategy, our analysis points towards the existence of a long-standing, self-reinforcing feedback loop between monetary technocrats’ attempts at bolstering the resilience of the Eurodollar market and their struggle to maintain governability in a world in which domestic monetary conditions have increasingly followed a global financial cycle.

Archival material

Bank for International Settlements, Standing Committee on the Euro-Currency Market (‘SCEM’), 1971-79.

Bank for International Settlements, Informal Records of the G-10 Deputies (‘Informal Records’), 1971-78, 7.15(1), G10 D1-D4.

Euromoney Magazine, 1975-79.

Acknowledgements

We are grateful to Quincy Stemmler for his excellent research assistance. For their constructive comments on earlier drafts we would like to thank Jens Beckert, Andrea Binder, Pierre-Christian Fink, Armin Haas, Iain Hardie, Erik Jones, Seung Woo Kim, Daniel McDowell, Perry Mehrling, Stefano Pagliari, Carolyn Sissoko, Matthias Thiemann, Helen Thompson, Geoffrey Underhill, Leon Wansleben as well as three anonymous reviewers.

Disclosure statement

The authors report no conflicts.

Additional information

Funding

Notes on contributors

Benjamin Braun

Benjamin Braun is a senior researcher at the Max Planck Institute for the Study of Societies in Cologne and a member of the School of Social Science at the Institute for Advanced Study, Princeton (2019–2020). His research focuses on the comparative and international political economy of financial and monetary systems and has been published, among others, in Economy and Society, Review of International Political Economy, and Socio-Economic Review.

Arie Krampf

Arie Krampf is a senior lecturer at the Academic College of Tel Aviv Yaffo. His research focuses on comparative capitalism and on the evolution of the international monetary and financial system. His current research, funded by the Israeli Science Foundation, traces the interaction between Israel’s growth model and its geopolitical factors. Among others, he has published in International Studies Quarterly, the Journal of European Integration and Journal of Institutional Economics.

Steffen Murau

Steffen Murau is a postdoctoral fellow at the Global Development Policy (GDP) Center of Boston University, City Political Economy Research Centre (CITYPERC) of City, University of London, and Institute for Advanced Sustainability Studies (IASS) in Potsdam. His research interests include monetary theory, shadow banking, the international monetary system and the European Monetary Union. Among others, he has published in the Review of International Political Economy and the Journal of Common Market Studies.

Notes

1 See, however, Germain (Citation1997, p. 11), who emphasizes “the growing role of private monetary agents within the IMS.” See also Goodman and Pauly (Citation1993) and Schwartz (Citation2019).

2 Monetary technocrats have been somewhat neglected in the recent debate about the systemic versus the domestic features of the international monetary and financial system (Chaudoin & Milner, Citation2017; Cohen, Citation2017).

3 The G-10 originally comprised the countries that in 1962 agreed to participate in the IMF’s General Agreement to Borrow: Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, the United Kingdom, and the United States. Switzerland joined as the eleventh member in 1964. The Federal Reserve was a member of the Standing Committee even though the United States did not join the BIS until 1994.

4 The archival record is incomplete. In many cases, documents submitted and statements made by Federal Reserve representatives are missing. Although this limits our insights into the positions of US representatives, the contributions of other Standing Committee members most of the time allow us to reconstruct discussions.

5 Prior to his appointment in May 1974, Simon had directed the Federal Energy Administration as Nixon’s ‘Energy Czar,’ managing US oil policy during the height of the oil crisis. As a former senior partner at Salomon Brothers, he was also a Wall Street insider.

6 Efforts to contain the competitive use of these government guarantees led to the establishment, in 1975, of the OECD “Export Credit Arrangement” (Moravcsik, Citation1989).

References

- Abbott, K. W., Genschel, P., Snidal, D., & Zangl, B. (2019). Competence versus control: The governor’s dilemma. Regulation & Governance, Advance Online Publication. https://doi.org/10.1111/rego.12234

- Abbott, K. W., Green, J. F., & Keohane, R. O. (2016). Organizational ecology and institutional change in global governance. International Organization, 70(2), 247–277. https://doi.org/10.1017/S0020818315000338

- Abdelal, R. (2007). Capital rules: The construction of global finance. Harvard University Press.

- Adler, E., & Haas, P. M. (1992). Conclusion: Epistemic Communities, World Order, and the Creation of a Reflective Research Program. International Organization, 46(1), 367–390. https://doi.org/10.1017/S0020818300001533

- Altamura, C. E. (2017). European Banks and the Rise of International Finance: The Post-Bretton Woods Era. Routledge.

- Andrews, D. M. (2006). International monetary power. Cornell University Press.

- Avdjiev, S., McCauley, R., & Shin, H. S. (2015). Breaking free of the triple coincidence in international finance. BIS Working Paper 524. Bank for International Settlements.

- Awrey, D. (2018). Brother, can you spare a dollar? Designing an effective framework for foreign currency liquidity assistance. Columbia Business Law Review, 2017(3), 934–1016.

- Babb, S. (2007). Embeddedness, inflation, and international regimes: The IMF in the early postwar period. American Journal of Sociology, 113(1), 128–164. https://doi.org/10.1086/517896

- Battilossi, S. (2010). The Eurodollar revolution in financial technology: Deregulation, innovation and structural change in Western banking. In A.-A. Kyrtsis (Ed.), Financial Markets and Organizational Technologies. (pp. 29–63). Palgrave Macmillan.

- Bauerle Danzman, S., Winecoff, W. K., & Oatley, T. (2017). All crises are global: Capital cycles in an imbalanced international political economy. International Studies Quarterly, 61(4), 907–923. https://doi.org/10.1093/isq/sqx054

- Bell, G. (1973). The Euro-dollar market and the international financial system. John Wiley.

- Best, J. (2005). The limits of transparency: Ambiguity and the history of international finance. Cornell University Press.

- Binder, A. (2019). All exclusive: The politics of offshore finance in Mexico. Review of International Political Economy, 26(2), 313–336. https://doi.org/10.1080/09692290.2019.1567571

- Block, F. L. (1977). The origins of international economic disorder: A study of United States international monetary policy from World War II to the present. University of California Press. https://doi.org/10.1086/ahr/82.5.1352-a

- Braun, B. (2018a). Central banking and the infrastructural power of finance: The case of ECB support for repo and securitization markets. Socio-Economic Review. Advance Online Publication. https://doi.org/10.1093/ser/mwy008

- Braun, B. (2018b). Central bank planning: Unconventional monetary policy and the price of bending the yield curve. In J. Beckert & R. Bronk (Eds.), Uncertain futures: Imaginaries, narratives, and calculation in the economy (pp. 194–216). Oxford University Press.

- Braun, B., Gabor, D., & Hübner, M. (2018). Governing through financial markets: Towards a critical political economy of Capital Markets Union. Competition & Change, 22(2), 101–116. https://doi.org/10.1177/1024529418759476

- Burn, G. (2006). The re-emergence of global finance. Palgrave Macmillan.

- Calomiris, C. W., Flandreau, M., & Laeven, L. (2016). Political foundations of the lender of last resort: A global historical narrative. Journal of Financial Intermediation, 28, 48–65. https://doi.org/10.1016/j.jfi.2016.09.002

- Chaudoin, S., & Milner, H. V. (2017). Science and the system: IPE and international monetary politics. Review of International Political Economy, 24(4), 681–698. https://doi.org/10.1080/09692290.2017.1302974

- Clement, P., & Toniolo, G. (2005). Central bank cooperation at the Bank for International Settlements, 1930-1973. Cambridge University Press.

- Clift, B. (2018). The IMF and the politics of austerity in the wake of the global financial crisis. Oxford University Press.

- Cohen, B. J. (1978). Organizing the world’s money: The political economy of international monetary relations. Macmillan.

- Cohen, B. J. (1996). Phoenix risen: The resurrection of global finance. World Politics, 48(2), 268–296. https://doi.org/10.1353/wp.1996.0002

- Cohen, B. J. (2017). The IPE of money revisited. Review of International Political Economy, 24(4), 657–680. https://doi.org/10.1080/09692290.2016.1259119

- Copelovitch, M. S. (2010). The International Monetary Fund in the global economy: Banks, bonds, and bailouts. Cambridge University Press.

- Dutta, S. J. (2019). Sovereign debt management and the transformation from Keynesian to neoliberal monetary governance in Britain. New Political Economy, Advance Online Publication.

- Eichengreen, B. (2019). Globalizing capital. A history of the international monetary system (3rd ed.). Princeton University Press.

- Einzig, P. (1964). The Euro-dollar system. Macmillan.

- Fioretos, O. (2019). Minilateralism and informality in international monetary cooperation. Review of International Political Economy, 26(6), 1136–1159. https://doi.org/10.1080/09692290.2019.1616599

- Fischer, S. (1999). On the need for an international lender of last resort. Journal of Economic Perspectives, 13(4), 85–104. https://doi.org/10.1257/jep.13.4.85

- Fratianni, M., & Savona, P. (1971). Eurodollar creation: Comments on Prof. Machlup’s propositions and developments. PSL Quarterly Review, 24(97), 110–127.

- Frieden, J. (1987). Banking on the world: The politics of American international finance. Harper & Row.

- Friedman, M. (1969). The Euro-dollar market: Some first principles. Selected Papers no. 34. University of Chicago: Graduate School of Business.

- Gabor, D., & Ban, C. (2016). Banking on bonds: The new links between states and markets. Jcms: Journal of Common Market Studies, 54(3), 617–635. https://doi.org/10.1111/jcms.12309

- Gabor, D., & Vestergaard, J. (2016). Towards a theory of shadow money. Institute for New Economic Thinking.

- Germain, R. D. (1997). The international organization of credit: States and global finance in the world-economy. Cambridge University Press.

- Goodhart, C. (2011). The Basel Committee on Banking Supervision: A history of the early years 1974–1997. Cambridge University Press.

- Goodman, J. B., & Pauly, L. W. (1993). The obsolescence of capital controls? Economic management in an age of global markets. World Politics, 46(1), 50–82. https://doi.org/10.2307/2950666