?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We analyze how direct and indirect effects (spatial spillovers) matter when estimating price effects for a property located in a flood zone. Using a spatial Durbin error model, we show the importance of indirect effects which amount to -6.5% for houses and -4.8% for condominiums in the flood-prone city of Dresden (Germany). Direct effects diminish when controlling for spatial spillovers. Our results are generally robust across different model specifications, urban areas, and risk-adjusted prices that include insurance costs. Thus, ignoring indirect flood effects can lead to flood management that is inefficient and cost-ineffective, as the economic consequences are underestimated.

Floods are the most prevalent natural hazard worldwide in terms of fatalities and financial losses; around one-third of all reported natural catastrophes and implied economic losses result from flooding. Although the effects of global warming and climate change are leading to a higher frequency and severity of flood events, floodplains still provide attractive building land for urban and industrial development, resulting in an increased concentration of values. As a result, higher economic losses occur from flood damage, which poses a challenge not only for the real estate sector but the economy as a whole, and also gives rise to the question of how to adequately price flood risk.

Besides the obvious relevance to urban development, flood risk typically reduces property values due to the potential for structural damage or even the total loss of a property. When estimating flood risk price discounts, the existing literature already considers spatial spillovers to control for unobserved spatial correlation resulting from neighboring properties. However, unobserved spatial dependence in the dependent and explanatory variables leads to biased and inconsistent estimates of price effects, whereas an unobserved spatial lag in the error terms results in a loss of efficiency (Anselin & Bera, Citation1998). Though it controls for spatial dependence, the previous research mostly focuses on the interpretation of direct effects for theoretical flood zones (FZs) and actual floodplains. Direct effects can be compared to coefficients from linear models: They stem from a change in the property itself and mostly result in discounts for locations with an increased risk (Bin et al., Citation2008; Bin & Landry, Citation2013; Rambaldi et al., Citation2013). Conversely, our measurement of flood price effects aims to underline the relevance of indirect effects, which capture spatial spillovers from the neighborhood.

FZ status is only directly reflected in property prices when it is evident to buyers and sellers. Information costs for observing direct flood risk are high for buyers, therefore, they neglect to search for information, especially when the prevailing risk is of high consequence and low probability (Browne et al., Citation2015; Bin & Kruse, Citation2006; Bin & Polasky, Citation2004). Although some studies suggest that the acquisition of insurance may serve as an indicator of flood risk, Kunreuther and Pauly (Citation2004) find that insurance is often not purchased due to the high transaction costs for obtaining information about prevailing risk, a low expected return from financial efforts, and anticipated excessive costs for sufficient insurance. Chivers and Flores (Citation2002) confirm that many buyers are unaware of a property’s floodplain location and flood insurance costs when purchasing a property. Consequently, buyers have less information about direct flood risk than sellers and may accept price discounts to compensate for risks that fall far below the potential statistical economic losses. Thus, the question arises whether the interpretation of direct effects is sufficient for understanding flood price effects under asymmetric information. In situations where decisions are made under conditions of uncertainty, Tversky and Kahneman (Citation1974) suggest that individuals use simplified heuristics based on representativeness or availability, without considering the explicit trade-offs between costs and benefits for different alternatives. Regarding flood risk, we assume that these heuristics may include the immediate neighborhood as an easily observable indicator of FZs. For example, when neighbors are interviewed, recent flood damage may still be visible on buildings or the media may report on flooding in the local area. Spatial regressions include these neighborhood effects as spatially lagged variables (indirect effects) that need to be interpreted in the context of flooding. Ortega and Taṣpınar (Citation2018) analyze changes in the direct effect from damage due to a flood event at the property itself while controlling for the damage suffered by properties in the same city block. Using a standard regression model with fixed effects, they find evidence of an impact from damaged neighboring properties that leads to significantly reduced direct effects.

If studies include indirect effects, they are mostly inadequate in determining the type of spatial spillovers. Spatial dependence can induce either local or global spillover effects. Local spillovers relate to characteristics of the immediate neighborhood that influence price setting for the property in question; however, global spillovers also arise from properties that do not belong to the immediate neighborhood. LeSage (Citation2014b) states that “most spatial spillovers are local” and postulates that global spillovers arise only when there are endogenous interaction and feedback effects. Endogenous interaction induces a sequence of adjustments in (potentially) all properties in the sample, which in turn causes feedback effects and leads to a new long-run steady-state equilibrium. In the context of properties, indirect effects are mostly limited to the immediate neighborhood, due to the shared characteristics of structure and location, such that endogenous interaction and feedback effects are unlikely to occur. Flood risk is particularly variable at a local level based on topographic and development characteristics. Therefore, we assume that local spillovers are predominant in measuring flood price effects.

In this study, we shed new light on the importance of including indirect effects for FZs when interpreting flood price effects, and we aim to increase sensitivity in order to select a correct spatial model. Therefore, we use recent developments in spatial econometrics to control for spillovers and for unobserved spatial dependence. The type of spatial dependence is assessed by a Bayesian model comparison approach (see, e.g., LeSage, Citation2014a), and we find strong evidence for a spatial Durbin error model that controls for local spillover effects. We apply this model to the flood-prone city of Dresden, Germany, which experienced severe flooding from the River Elbe in 2002 and 2013. Indirect effects amount to -6.5% for houses and -4.8% for condominiums, whereas direct effects are not statistically significant. We also compare price effects with insurance costs to determine whether sellers accept price discounts that correspond to the economic loss covered by the insurance contract. Although such price discounts compensate buyers for the costs of covering economic losses in most FZs, sellers anticipate a higher willingness to pay in a high-risk FZ. Finally, we incorporate insurance costs in order to obtain risk-adjusted property prices that confirm the existence of indirect discounts for all FZs.

Theoretical Flood Impact on Property Pricing

Flooding is the prevailing natural risk to urban areas in Germany and can result in significant damage. Many regions have already been subject to severe flood events; therefore many property sellers and buyers have already directly experienced the consequences of flooding. Flood experience typically induces increased risk awareness due to information campaigns or flood protection measures that are implemented in the aftermath of an event (Browne & Hoyt, Citation2000; Michel‐Kerjan & Kousky, 2010; Kriesel & Landry, Citation2004). In general, the literature identifies significant price discounts directly following flood events (Bin & Polasky, Citation2004; Morgan, Citation2007; Shultz & Fridgen, Citation2001). Daniel et al. (Citation2007) conclude that price reductions persist after these events if there is a clear official communication of flood risks; however, without clear communication, price effects typically diminish as more time passes since the most recent flood event (Atreya et al., Citation2013; Lamond & Proverbs, Citation2006). Bin and Landry (Citation2013) find a continuous decline in price discounts until they completely disappear after a period of six years. In addition, spatial spillover effects for flood risk can vary with the information source, including information effects (theoretical zones) and visualization effects (actual floodplains). Merging both effects would overestimate price effects from theoretical zones (Atreya & Ferreira, Citation2015). However, regions with an increased risk status have typically experienced flooding, so price effects are affected positively or negatively and need to be interpreted in the context of flooding history to gain comparable estimates. We focus on theoretical zones in our main analysis but also conduct a robustness check and analyze whether properties in the actual floodplains of the 2002 and 2013 events are still subject to price discounting.

Another bias can stem from a link between FZs and the positive aspects of a waterside location that must be addressed in empirical models (Bin et al., Citation2008). This is important since despite high flood risks there is an increased demand for properties close to water due to the benefits associated with a waterside location (water views, water sports facilities, etc.), resulting in a positive bias in FZ estimates.

If damage occurs despite flood protection measures, flood insurance functions as a risk transfer mechanism, especially for economic losses. Thus, the discounted sum of flood insurance premiums can provide a reasonable basis for comparison for the size of price effects. Atreya et al. (Citation2013) report significantly higher flood discounts than expected based on insurance premiums, due to uninsurable costs (such as inconvenience or psychological costs). Shultz and Fridgen (Citation2001) obtain similar results and are able to explain only 80% of price discounts as compensation for future insurance costs. Although Bin and Kruse (Citation2006) find discounts that nearly correspond to discounted insurance premiums, Harrison et al. (Citation2001) identify a discount of less than the discounted insurance premiums, which therefore does not reflect overall risk.

In contrast to insurance in the studies cited here, flood insurance in Germany is voluntary and privately offered.1 Voluntary insurance systems can suffer from behavioral bias, resulting in comparably low insurance take-up rates and a loss in information value when comparing price effects with insurance premiums. However, compared with the national average take-up rate of 40%, the rate in our area of study, Saxony, is higher, at 46%. Furthermore, Bin et al. (Citation2008) find price discounts that are equivalent to flood insurance costs even when buyers neglect to insure against flooding. This supports the assumption that FZs reflect risk information and have an impact on property pricing even if insurance is not obtained.

When insurance take-up rates are low, homeowners typically rely on government relief programs when facing losses. Government relief is not guaranteed, but the government paid high levels of compensation after major flooding along the River Elbe in 2002 and 2013. Buyers and sellers may anticipate this response and rely on future government relief for flood damage, therefore neglecting to provide or obtain information about flood risk and insurance regarding their property.

Study Area and Data

We analyze inland river flooding in the city of Dresden, the capital of the German federal state of Saxony. We assume that indirect pricing of flood zones especially applies to urban areas where housing density is high and the immediate neighborhood may have a high impact when setting prices of neighboring properties. Dresden is one of the largest cities in Germany, with 547,172 inhabitants as of 2016,2 and has enjoyed tremendous popularity as an investment opportunity and residential location in recent years. Demand for owner-occupied homes is high; the value of home purchases amounted to €512 million in 2014, with increases in property prices of 17.6% between 2007 and 2014. However, the city is exposed to urban flood risk due to its location by the River Elbe and smaller tributaries, especially the River Weißeritz. Dresden’s topography is almost entirely flat, with a steep slope in the hinterland such that there is insufficient space for floodwater to be redirected. This basin location, in combination with the city’s proximity to low mountain ranges that frequently have high levels of precipitation and an increased risk of snow-melt, results in a consistently high flood risk. Nevertheless, investors and urban planners see high potential for building land across the city area, resulting in a noticeable upturn in construction activity even in exposed areas.

Dresden was hit by severe flooding events in 2002 and 2013. The flood event in 2002 was the result of intense summer rainfall leading to high discharges and record-high river water levels followed by high groundwater levels; it caused total losses of €6 billion in Saxony, €1.3 billion of that within the city of Dresden. The River Elbe rose to 940 cm on August 17, 2002, compared with its average level of 165 cm and average flood level of 481 cm in the city of Dresden.3 The flood event in 2013 was again caused by widespread and intense rainfall at a time the soil was already wet due to exceptionally high rainfall in the preceding month. The River Elbe level reached 878 cm on June 6, 2013—the second-highest level for the city of Dresden. The last time the river surpassed the 7-meter level was in 1940, so city authorities and citizens might not have been fully prepared for such high water levels. After the flood of 2002, various measures were implemented to improve flood risk management, which went into effect in 2013. The city of Dresden completed 770 different flood prevention and protection measures by 2010; for example, the city center is now protected by walls and mobile flood protection systems such as flood protection gates, and the River Weißeritz bed was partially expanded (for more details regarding our data sample, see “Flood Characteristics”). Thus, the mitigation of potential losses from new protection measures should have theoretically resulted in an adaption of flood price effects.

Pricing Data and Structural Characteristics

Housing prices and structural characteristics are provided by the private online platform ImmobilienScout24 and include all property listed using this service during the sample period from 2008 to 2016. A general overview of this dataset is given by Boelmann and Schaffner (Citation2018). The dataset contains 6,371 valid observations for houses and 12,358 for condominiums. Asking prices are adjusted for inflation at the level of the first quarter of 2016 using the German Construction Cost Index.4 We control for duplicates based on geographic coordinates, living area, number of rooms, and age of properties. For condominiums, we also use floor numbers. The interpretation of asking prices can be biased when sellers intentionally over- or underestimate achievable prices. Since sellers usually attempt to achieve a high price in a short offering time and inflated prices may lead to a significant increase in the offering time, we include the offering time in our models to control for possible distortion. However, the average asking price per square meter in our dataset amounts to €2,090 compared with an average transaction price of €1,990,5 thus, we assume that asking prices listed in advertisements are almost equal to transaction prices in the sale contract. Furthermore, Harrison et al. (Citation2001) state that even transaction prices underlie bias in terms of flood risk and do not represent intrinsic property value in cases where a property’s location in a flood zone becomes transparent after the housing contract is signed. Because of high information costs and a lack of awareness, buyers typically inform themselves about insurance coverage and flood zone status after purchasing a property, as they can then focus on the FZ classification of one specific property.

The dataset includes structural characteristics such as property type, living area, number of rooms, age, and quality. presents the summary statistics of all locations and higher-flood-risk locations separately for houses and condominiums. The mean values for properties with a higher-flood-risk status, however, do not vary significantly from those for all locations. Thus, properties in flood-prone areas are not substantially different in terms of price and structural characteristics from those located elsewhere.

Table 1. Descriptive statistics.

Neighborhood and Location Attributes

We merge the previous dataset based on geographic coordinates of a property location with neighborhood characteristics containing information on the respective sociodemographic and housing structure at the postcode level. Neighborhood characteristics are obtained from GfK Geomarketing and include attributes such as number of households, household size, migration rate, population age, and number of residential or partly residential buildings. The improvement in the goodness of fit by using detailed neighborhood characteristics in a hedonic analysis is also underlined in other studies (see e.g., Gibbons, Citation2004; Hilber, Citation2005). Additionally, we measure the availability of amenities by calculating the geodesic distance from the nearest park, the city center, and the nearest highway, since these amenities can directly and indirectly affect the valuation of a property (see, e.g., Baranzini & Ramirez, Citation2005; Conway et al., Citation2010). We also include the distance from the nearest body of water and the River Elbe to account for effects related to water proximity.

Flood Characteristics

To identify flood risk, we use both theoretical FZs and actual floodplains. We assign insurance-based FZs to properties at an individual level using the German Insurance Association’s (GDV) ZÜRS Geo tool. This zoning system for flood, backwater, and heavy rain is a geospatial platform with nationwide data for the risk assessment of properties and insurance premium calculation for insurers. Flood risk is classified into four different FZs based on the recurring flooding interval and other locational attributes (see ). FZ 1 includes almost no flood risk. In FZ 2 (100-year floodplain) and 3 (100-year to 10-year floodplain), the risk level increases continuously, and FZ 4 represents the highest risk area (10-year floodplain). FZ 1 includes 87.1% of houses in the dataset with 12.9% located in FZs 2-4. In the condominium sample, 75.4% are located in FZ 1 and 24.6% in FZs 2-4.

Table 2. Flood zone classification.

Table 3. Log-marginal likelihood values and posterior model probability.

We use geographical information from Dresden’s flood events in 2002 and 2013 to identify property locations in inundated areas.6 Whereas 9.2% of houses and 13.4% of condominiums were located in inundation areas in 2002, only 2.5% of houses and 2.2% of condominiums were sited in inundation areas during the event of 2013. presents the floodplains of the respective events in Dresden and the spatial distribution of properties. However, a comparison of properties in our dataset with all existing properties7 indicates that there is no sample selection bias in terms of flood risk and floodplain location.

Figure 1. Inundated properties during the flooding events in 2002 and 2013.

Note. This figure shows affected properties in Dresden during the flooding events in 2002 (left) and 2013 (right). The first row presents properties of our dataset and the second row the general building development in inundation areas obtained by OpenStreetMap.

Empirical Model

With our empirical model, we aim to estimate spatially unbiased price effects caused by a property’s location in an FZ. Our approach is divided into three steps: First, we determine the type of spatial spillovers using a Bayesian model comparison technique (see LeSage & Pace, Citation2009) and calculate price effects for flood zones based on a spatial Durbin error model (SDEM). Second, we calculate the average insurance costs to determine the respective implied discount rate in each FZ; the implied discount rate provides the basis for an assessment of the size of the price effects compared with economic losses. Finally, we add the individual insurance costs to the original property price from step one in order to generate a risk-adjusted property price and then repeat our spatial estimations. Using risk-adjusted prices allows us to observe whether sellers account for insurance costs when setting their asking prices.

Spatial Hedonic Regression for Flood Zones

Since neighboring properties typically share locational, structural, and socioeconomic characteristics, unobserved spatial dependence arises and needs to be addressed in econometric models. There are methods from spatial econometrics that control for different types of spatial dependence to prevent biased and/or inconsistent estimates. These include a spatial lag of the dependent variable, the explanatory variables or the disturbances (Anselin & Bera, Citation1998). Non-spatial approaches that exclude spatial spillovers from the model specification result in estimates that suffer from omitted variable bias. This bias is intensified if the explanatory variables correlate with any omitted spatial effects (LeSage & Pace, Citation2009).

To determine the type of spatial dependence in our dataset, we test three spatial models: the spatially lagged X model (SLX), the spatial Durbin model (SDM), and the spatial Durbin error model (SDEM). For an excellent overview of these, see LeSage and Pace (Citation2009). The SLX model is very similar to a standard linear model but also incorporates all explanatory variables (X) as spatially lagged factors. These local spillovers relate to property characteristics of the immediate neighborhood that can influence price setting for a property.

The SDM includes both spatially lagged dependent and independent variables. From a theoretical perspective, the spatial lag of the dependent variable is added when neighboring properties serve as a benchmark for setting the price of an individual property due to uncertainties in neighborhood characteristics or when spillovers from value appreciation/depreciation arise within the neighborhood (see Osland & Thorsen, Citation2013). The influence of the average of the explanatory variables from neighboring properties is determined using the spatially lagged independent variables. The SDM is an addition to the spatial autoregressive model (SAR), where only the spatially lagged dependent variable is added on the right-hand side. As pointed out by Kim et al. (Citation2003) and Cohen and Coughlin (2008), the SAR is superior if a structural spatial interaction is present in the market and/or if the strength of that relationship is of particular interest for the research question. Even if the former may be present in our data sample—although pricing data of comparable properties are not easy to obtain during the buying process in Germany—the latter is not relevant for us here. From a statistical perspective, the obtainment of consistent coefficients is a major argument in favor of this model, whereby efficient estimators result from the alternative spatial error model. This type of model should be used if spatial interactions are not assumed by theory, so that the focus is more on correcting for the influence of spatial autocorrelation. Even if consistency is a very important property of an estimator, we conclude that the corrections for the influence of spatial autocorrelation is more important for our research question in that it ensures correct inference, which takes precedence over an ability to quantify the strength of the interaction between the price of a property and its neighboring property. Furthermore, the SDM simplifies to the SAR when the parameters of the spatially lagged independent variables take on the value of zero, to the SLX when the scalar parameter of the spatially lagged dependent variables takes on a value of zero, and to a conventional linear regression model when both parameter vectors are equal to zero.

As our third model, we use the SDEM; it captures spatial dependence in the explanatory variables and in the error terms. Although we include a large number of hedonic controls, there might still be unobserved characteristics that vary over space, resulting in spatial correlation of the disturbances. The SDEM combines the SLX model with an error process that accounts for this residual correlation.

In the section on Spatial Hedonic Regressions, we compare all three models using a Bayesian model comparison approach, which shows that the SDEM best describes our dataset. Thus, we focus on a description of the SDEM in this study. Following the method used by Pace and LeSage (Citation2004), the estimation of the SDEM is based on maximum likelihood with Monte Carlo approximate log-determinants8 and is specified as follows:

(1)

(1)

where

is the asking price for property

at time

is a dummy vector indicating whether property

is located in a specific flood zone (FZ 2-4);

is a matrix of explanatory variables including structural, neighborhood, and locational attributes;

represents quarterly time-fixed effects;

is a spatial weight matrix;

indicates the spatial autocorrelation in the error terms; and

is an independent and identically distributed random error term. Regarding the transformation of the dependent variable, we use the log-linear (semi-log) equation form, which is consistent with Rosen (Citation1974) and is preferred over a linear functional form. For the explanatory variables, we use quadratic transformations for structural variables, such as number of rooms and age, thus addressing the declining price effects with an increasing characteristic expression. Locational variables measuring the distance from different amenities are log-transformed in order to capture price effects that decline with distance. Quarterly time-fixed effects control for time variations and seasonal effects in price levels. The adjustment of W captures the geographical area that may share unobserved characteristics. We use a standardized, inverse distance–based spatial weight matrix that identifies properties with their ‘four nearest neighbors’ as a neighborhood cluster.9 The beta coefficients of the SDEM are interpreted as direct effects stemming from a change in the property characteristics averaged over all properties. Thus, the direct effect is the effect of a change in an explanatory variable of property

on the dependent variable of property

The gamma coefficients from spatially lagged variables are interpreted as indirect effects (LeSage & Pace, Citation2009). The indirect effects measure how a change in an explanatory variable of property

affects the dependent variable of property

They should capture all spillover effects from the set of explanatory variables. For example, this effect determines the impact of all neighboring properties being located in a flood zone on the price of an individual property, again averaged over all properties. The total effects measure the sum of both the direct and the indirect effects.

Calculation of Insurance Costs

Insurance costs can provide insights into whether price effects for flood zones are adapted to potential economic losses. Thus, we calculate theoretical insurance costs according to the following equation:

(2)

(2)

where

is the present value of insurance costs,

is the individual insurance premium at the property level, and

is the average real estate return. More precisely, we determine the

s by applying a calculation scheme provided by the German Insurance Association. This scheme is based on a three-step procedure: the specification of the rebuilding value (

), the index-linked adjustment factor (

), and the loss factor (

). First, we calculate the

that covers costs for rebuilding in the case of complete destruction and accounts for various housing attributes (e.g., building type, living area, and quality).10 This value can significantly differ from the current market value and ensures the prevention of underinsurance in the case of value appreciation over time. Second, we adapt the

to the offering year by using an index-linked adjustment factor (

). This factor is provided annually by the German Insurance Association based on economic indicators such as the construction price index and the wage index for the construction sector. Third, we measure an individual loss factor (

) as a function of the flood zone and the

This factor covers marketing and selling expenses, administrative costs, and the profit margin of insurance companies. The insurance premiums for properties located in FZ 4 are not part of this standard calculation scheme and are based on an individual assessment. Thus, we use an extrapolation of the FZ 1 to FZ 3 calculation scheme for the determination of theoretical premiums in FZ 4. For the average real estate return (

), we set 5% as the sum of the risk-free interest rate of 3% (average of 10-year German government bonds over the last 20 years) plus a risk premium of 2% for properties in Dresden. Finally, we compare price discounts for flood zones with annual insurance costs and determine the average implied discount rate. The implied discount rate—the required rate equal to the present value of future insurance costs and the price effect—provides the basis for an assessment of the size of price effects compared with economic losses. Whereas the implied discount rate is lower than the average real estate return (

), sellers compensate potential buyers at an amount equal to more than the costs of insurance coverage. Higher implied discount rates imply that sellers are able to apply price discounts that are lower than the costs of insurance coverage.

Spatial Hedonic Regression Including Insurance Costs

We extend our approach and add the present value of individual insurance costs (), based on a discount rate of 5%, to the original property price (

) in order to simulate a risk-adjusted property price, and then repeat our spatial regressions. Using risk-adjusted prices as the dependent variable allows us to observe whether sellers account for insurance costs when setting their asking prices.11 Note that these risk-adjusted prices arise only when buyers decide in favor of flood insurance; therefore, we adjust the present value of insurance costs to the prevailing insurance take-up rate of 45%. Lastly, we modify the model according to the following equation:

(3)

(3)

where the model specifications and variable descriptions equal those of EquationEquation (1)

(1)

(1) . Adding the insurance costs to the dependent variable, we assume that there would be no cost compensation left for FZs if sellers were to determine their price discounts on the basis of economic losses. Further transaction costs that a buyer may incur during the purchasing process (e.g., tax or brokerage fee) are not conditional to flood risk and consequently are not relevant to this model.

Results

To verify the importance of indirect price effects of a location in different FZs, we divide our empirical analysis into three steps. First, we run spatial regressions on the natural logarithm of property prices to measure direct and indirect price effects for FZs. Second, we determine the average insurance costs in each FZ in order to calculate the respective implied discount rate. Third, we add the individual insurance costs to the original property price in step one in order to gain a risk-adjusted property price and then repeat our spatial regressions.

Spatial Hedonic Regressions

Before estimating flood price effects, we need to determine whether there are structural differences in the results between houses and condominiums; we therefore run a Chow test to determine whether we will need to separate our sample for houses and condominiums (Chow, Citation1960). The resulting test statistics indicate a clear argument for a separation (F = 25.56, p-value < 0.0001). Therefore, we run two separate regressions for these two property types. In line with LeSage and Pace (Citation2009), we also determine the appropriate spatial model (SLX, SDM, or SDEM) and the best specification of the spatial weights matrix using a Bayesian model comparison approach. The log-marginal likelihood and the posterior model probability suggest that SDEM is the most appropriate model because it best describes our dataset (see Panel A in ). For the spatial weight matrix, we choose the ‘four nearest neighbors’ specification, which determines the four nearest properties (immediate neighborhood), as the source of indirect effects (see Panel B in ). For a variation of the spatial weight matrix, see Appendix 1.

According to the Chow test, we split our sample into houses and condominiums, and according to the Bayesian model comparison (), we proceed with an SDEM with a spatial weights matrix of four nearest neighbors. Combining the house and condominium subsamples with three different model specifications (separated zones, water amenities, and combined zones), the coefficients of six different regressions are shown in . The general existence of spatial correlation in all regression models is confirmed by the statistics of likelihood ratio tests and Wald tests on the joint significance of spatial parameters (significant at the 1% level). Our estimation approach fully captures the existing spatial correlation, as indicated by the statistically insignificant and low values of Moran’s I for the residuals. For the calculation of these, we use the classical approach based on Moran (Citation1950) for the serial independence of residuals. An alternative test could be the adjustment of Anselin and Kelejian (Citation1997) encountering regression specifications with instrumental variables or spatially lagged dependent variables. Even if the latter case applies to one of our model specifications (SDM), we adhere to the classical approach since we use for our main analyses SDEM without spatially lagged dependent variables. In addition, the authors point out that their adjusted Moran’s I test is the only acceptable in the presence of spatially lagged dependent variables. Even so, we think that this adjustment is a valuable contribution to models with lagged dependent variables.

Table 4. Price effects for flood zone location.

While assessing the impact of flood risk, we mainly discuss the direct and indirect coefficients for flooding variables (FZs and Spatial Lag FZs). Other estimated coefficients for the structural, neighborhood, and distance variables (see EquationEquation [1](1)

(1) ) are not the main focus of this study, but are mostly statistically significant, have the usual signs, and are robust across model specifications.

First, we discuss the model specification of ‘separated zones,’ which, besides the three FZ dummies (FZ 2-4), includes all hedonic variables and time-fixed effects. The price effects are economically meaningful; for example, a property price increase of 1% has an economic impact of €3,355 for houses and €1,912 for condominiums. Direct effects for houses indicate that, compared with the low-risk reference category FZ 1, prices are reduced by 1.2% in FZ 2, increased by 2.5% in FZ 3, and again reduced by 0.5% in FZ 4. All of these spatially non-lagged FZ coefficients, however, are statistically insignificant at any conventional level. This indicates that there is no price discount for the increased flood-risk status stemming from the property itself and thus sellers do not directly compensate buyers for a property’s location in an FZ. Conversely, indirect effects show statistically significant price effects; prices are reduced by 5.2% in FZ 2, by 6% in FZ 3, and by 26.6% in FZ 4. Thus, only indirect effects from the neighborhood cause discounts for an FZ. This is the case when buyers are only able to inform themselves about housing quality in indirect ways.

As discussed earlier, we assume that high information costs, or even constraints, hinder potential homeowners from obtaining information about a property’s individual FZ status and insurance coverage before signing a contract. Instead, the neighborhood serves as an indicator of flood hazard, for example, if recent flood damage to buildings is still visible or the media report on flooding in the local area. Sellers then adjust their asking prices to flood-related neighborhood effects. The data for condominiums confirm these results: direct effects are again statistically insignificant and indirect effects indicate statistically significant price discounts of 5.6% in FZ 2 and 5.1% in FZ 3. However, the indirect price discount of 13.2% is statistically insignificant in FZ 4. This insignificant coefficient could be a result of the small sample size in this zone. For condominiums, the whole owner community proportionally shares financial losses regarding the building’s structure. Basements, as well as common low-lying spaces, are smaller in relation to houses, so price discounts for FZs are generally smaller.

Furthermore, separating price effects for flood risk location and proximity to water amenities captures a potential positive bias in FZ effects. Controlling for a positive link between water amenities and other water-related factors, we include an interaction term for the land elevation of a property and its distance from the River Elbe in a second model specification (‘water amenities’) in . While property prices are assumed to decrease with increasing distance from the Elbe, this effect is mitigated by controlling for increased land elevation, which is in turn positively linked to a water view. Even in this model specification, indirect effects result in discounts of 5.6% in FZ 2, 7% in FZ 3, and 26.6% in FZ 4. All lagged coefficients are significantly different from zero at a level of 5%. For condominiums, spatially lagged coefficients show statistically significant discounts of 5.4% in FZ 2, 4.7% in FZ 3, and 13.4% in FZ 4. Whereas coefficients in FZ 2 and FZ 3 are statistically significant at a respective level of 1% and 5%, the price effect for FZ 4 is again insignificant. We also use likelihood ratio tests to compare both model specifications and find that the model on ‘water amenities’ is preferred for houses (p-value = 0.0027) and for condominiums (p-value = 0.0144) compared with the ‘separated zones’ model. A comparison of direct and indirect price effects for both housing types based on this model specification is presented in . Overall, price effects are again less negative in the condominium segment. Furthermore, the coefficient for FZ 2 is slightly lower compared with FZ 3 within the condominium segment. Thus, FZ status is considered less essential when setting prices for condominiums compared with houses, and only flood-related neighborhood effects result in statistically significant discounts in both property segments. Results for both model specifications (‘separated zones’ and ‘water amenities’) are comparable, such that a reduction in price effects does not occur after controlling for water view.

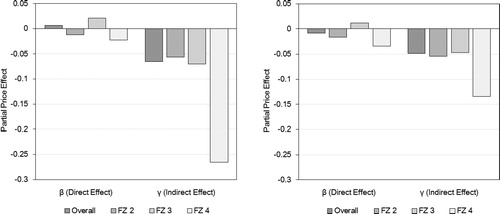

Figure 2. Direct and indirect price effects for flood zone location.

Note. This figure presents direct and indirect price effects for flood zone location of the ‘water amenities’ model in for houses (Panel A) and condominiums (Panel B). While direct effects resulting from the property itself are low and statistically insignificant, indirect effects capturing the influence of the neighborhood determine discounts for flood zones. Note that the indirect effect for FZ 4 in the condominium panel is also statistically insignificant.

For a table with all coefficients from the ‘water amenities’ model, see in Appendix 2.

Table A2-1. Price effects for flood zone location (all variables).

Table A2-2. Log-marginal likelihood values and posterior model probability (condominium).

Table A2-3. Variation of the spatial weight matrix.

Table A2-4. Comparison between price effects and insurance costs (condominium).

In the third model specification in , FZs are combined to measure an aggregated price effect for a general floodplain location (‘combined zones’). Since our previous risk classification is more detailed than in the recent literature, this model specification allows our results to be compared with other studies. Moreover, this literature mostly does not distinguish between direct and indirect flooding effects. For houses, an FZ location results in an indirect effect of -6.5%; for condominiums, the indirect discount is 4.8%. Both effects are statistically significant at a level of 1%.

Taken together, indirect effects are almost in line with the findings from other studies (5–10%) obtained without a differentiation of direct and indirect effects (Bin & Landry, Citation2013; Bin & Polasky, Citation2004; Bin et al., Citation2008). With our results, we are able to show that the indirect effect, and therefore the immediate neighborhood, is the driver of the price discount for FZ location and that this discount is robust to controlling for water amenities. From a theoretical perspective, buyers use the immediate neighborhood as a heuristic for flood risk and assume that it is representative of the flood risk at the property they are considering buying. Furthermore, the information costs for assessing flood risk based on neighboring properties may be lower due to visible structural damage, topographic characteristics, or headlines in local media and the information is therefore more readily available to buyers.

Calculation of Insurance Costs and Implied Discount Rate

We also analyze whether flood price discounts are equal to economic losses, which can be approximated by insurance costs. Thus, we calculate the implied discount rate as the rate that equals the present value of future insurance costs and the flood price effect. Comparing these implied discount rates with the average real estate return of 5% (see also Bin et al., Citation2008), we assume that lower implied discount rates imply that sellers overcompensate potential buyers for direct insurance costs and vice versa.

First, we compute individual insurance premiums for the 25th, 50th, and 75th percentile of the asking price distribution in each FZ. By doing so, we favor the actual distribution of prices for an artificial property with median values for all characteristics. To determine the implied discount rate, we use the predominant type of insurance contract in Germany, which includes a deductible of €1,000. In the next step, we match the present value of these premiums with estimated price effects that are equal to the total effect.12 Our approach for FZ 4 is slightly different. Since the number of observations in FZ 4 is small, we estimate only the implied discount rate for the median price. Furthermore, the insurance premium calculation is based on an extrapolation of the official premium calculation scheme because flooding is not classified as a random event in FZ 4 and the premium calculation is therefore subject to an individual assessment. shows price effects, annual insurance premiums, and the implied discount rates.

Table 5. Comparison between price effects and insurance costs.

For houses, the average implied discount rates amount to 8.7% in FZ 2, 25.6% in FZ 3, and 4.9% in FZ 4. These discount rates are almost stable across the price quartiles within each FZ. Implied discount rates for condominiums are 4.6%, 15.0%, and 4.3%, respectively. For the combined FZ, we find an implied discount rate of 18.4% for flood risk for houses and 5.5% for condominiums. Therefore, the benchmark of 5% almost corresponds to our estimates for condominiums in FZ 2 (4.6%) and for both property types in FZ 4 (4.9% or 4.3%). Equal rates indicate that sellers compensate buyers in an FZ for the costs to cover economic losses. The discount rates for houses in FZ 2 (8.7%) and for both property types in FZ 3 (25.6% or 15.0%) are higher, indicating that sellers anticipate a higher willingness to pay among potential homeowners in these FZs. We are not able to find implied discount rates lower than the average real estate return that would have indicated that sellers accept discounts which are higher than statistical economic losses.

Spatial Hedonic Regression with Insurance Costs

Because flood insurance covers potential economic losses, homeowners could voluntarily decide in favor of acquiring such a protection. Assuming a perfect market, sellers adjust property prices and compensate buyers for future insurance costs. Thus, we sum asking prices and the present value of insurance premiums in order to generate risk-adjusted property prices, and we include these as a new dependent variable in our previous regression EquationEquation (3)(3)

(3) . Using risk-adjusted prices allows us to observe whether sellers account for insurance costs when setting their asking prices—this is a novel approach in our research. The results are presented in .

Table 6. Price effects for flood zone location with insurance costs.

The model specifications with ‘separated zones’ and ‘water amenities’ show almost equal results for direct and indirect effects in comparison with the approach without insurance costs (). The results indicate positive direct effects for houses; for example, in the ‘water amenities’ model, of around 12% in FZ 3 and FZ 4, which are statistically significant at a level of 1% and 10%, respectively. The positive and statistically significant effects imply that sellers assume a willingness to pay for an FZ location that is higher than potential economic losses, for example, due to other beneficial location amenities. Thus, sellers do not compensate buyers for insurance costs. Indirect effects of all FZs are not affected by controlling for insurance costs. This is reasonable, as insurance coverage is independent from the neighborhood since it only covers economic losses at the property itself. Flood damage to neighboring properties can still have a negative price effect. For condominiums, we also find a positive direct effect of 5.8% in FZ 3, which is statistically significant at the 1% level. Indirect effects are again robust while controlling for insurance costs. Results for the ‘combined zones’ model indicate positive direct effects for houses (8.3%) and condominiums (1.6%). Both price effects are statistically significant at a respective level of 1% and 10% and indicate that sellers may assume that the willingness to pay is higher than the potential economic losses expressed by the capitalized insurance premiums. Indirect effects remain unchanged.

Taken together, previous results indicate that local spillovers indicated by indirect price effects from the immediate neighborhood contribute to lower property prices, whereas direct effects for the flood zone location of the property itself mostly diminish when controlling for spatial dependence. These effects are also robust to an analysis with risk-adjusted prices that includes future insurance costs to cover economic loss, providing further evidence of the importance of indirect effects in the analysis of flood zone effects.

Conclusion

In this study, we analyze direct and indirect price effects for the flood zone location of properties. Since the interpretation of indirect effects varies with the type of spatial spillovers (global versus local), and theoretical considerations do not explicitly point towards one of these spillover types, we use the Bayesian model comparison approach to choose the appropriate model (see LeSage, Citation2014a). In our estimation, we find evidence only for local spillover effects stemming from the immediate neighborhood and therefore calculate an SDEM corresponding to the statement by LeSage (Citation2014b) that most spillovers are local. The detailed discussion of indirect effects, the use of the Bayesian model comparison, and the SDEM are unique to our research in comparison with previous flooding research.

Our main results are as follows: Direct effects from the FZ location of the property diminish when controlling for spatial dependence. However, in line with our theoretical considerations, we find strong evidence for indirect price effects. Price effects are generally lower for condominiums compared with houses. These results are mostly robust to flood zone effects measured from risk-adjusted prices that include future insurance costs to cover economic loss. Within various robustness analyses, where we compare a neighboring city with a similar flood risk, a neighboring city without high flood risk, and the entire river basin, we find that the relevance of indirect effects from flood zone or floodplain location persists. Thus, our results provide evidence of the importance of addressing indirect effects in the analysis of flood zone effects.

Since waterside locations are attractive to property buyers, flood-prone areas are increasingly used for urban development. Consequently, the sum of insured losses has also increased in recent decades. Due to the observed relevance of flood price effects for individual sellers and buyers, as well as for the economy as a whole, incorporating indirect effects resulting from the immediate neighborhood in policy interventions is very important and can substantially contribute to an adequate calculation of the economic consequences of flooding. This in turn can stimulate policy formulation for effective flood risk management and cost-efficient, correctly assessed protection measures, such as dikes, retention areas, and the renaturation of former building land.

Acknowledgments

The authors wish to thank Paul Elhorst, Piet Eichholtz, David Ling, and the participants of the 2015 INFER Workshop in Aachen, the 2016 European Real Estate Society (ERES) Annual Conference in Regensburg, and the 2016 American Real Estate and Urban Economics Association (AREUEA) International Conference in Alicante for their insightful comments and suggestions on an earlier version of this paper. Finally, we would like to thank the German Insurance Association (GDV), Westfälische Provinzial AG, and Immobilien Scout GmbH for providing us with raw data and comments on an earlier version of this paper.

Notes

Notes

1 Flood insurance is acquired in a bundle with insurance against other natural disasters including risks from earthquake, land subsidence, landslide, snow pressure, and avalanches. According to the German Insurance Association, the determining factor for the insurance premium calculation is the prevailing risk source. We follow this market approach and completely assign insurance premiums to flood risk, since all other natural hazards have no statistical relevance in our study area.

2 See the Database of the Federal Statistical Office of Germany, GENESIS, https://www-genesis.destatis.de/genesis/online.

3 See https://www.umwelt.sachsen.de/umwelt/infosysteme/hwims/portal/web/wasserstand-pegel-501060 for the water levels.

4 The construction cost index is obtained from the German Federal Statistical Office. This index is preferred over the consumer price index, since it only measures the price trend in construction costs of properties depending on labour and material costs (including equipment, energy, operating, and building supplies).

5 Annual housing market report by the city of Dresden see https://www.dresden.de/media/pdf/wirtschaft/exporeal/2015_Immobilienbroschure_web.pdf. However, those data do not include housing attributes and are not suitable for our analysis.

6 German Federal Office of Cartography and Geodesy (BKG) and German Federal Office of Hydrology (BfG).

7 OpenStreetMap.

8 We use the 3.2.2 (64-bit) version of R for calculating our spatial regressions.

9 We use the k-nearest neighbor approach to account for underlying spatial correlation between observations. A robustness check for the variation of the spatial weights matrix is provided in .

10 As this is the market standard, the rebuilding value is calculated for the year 1914. In 1914, the German currency was on a gold standard and exceptional increases in property prices were inhibited.

11 For endogeneity reasons, we refrain from including insurance costs as an explanatory variable.

12 The total effect is defined as the direct effect + indirect effect (LeSage & Pace, Citation2009).

13 100 meters (m) is the average distance between all houses and half of the average distance between condominiums.

14 A comparison of properties in our dataset with all existing properties from OpenStreetMap is provided in .

15 We note that we do not control for locational characteristics in the ‘Elbe area’ model.

References

- Anselin, L. & Bera, A. (1998). Spatial dependence in linear regression models with an introduction to spatial econometrics. In A. Ullah & D.E. Giles (Eds.). Handbook of applied economic statistics (pp. 237–289). Marcel Dekker.

- Anselin, L., & Kelejian, H. H. (1997). Testing for spatial error autocorrelation in the presence of endogenous regressors. International Regional Science Review, 20(1–2), 153–182.

- Atreya, A., & Ferreira, S. (2015). Seeing is believing? Evidence from property prices in inundated areas. Risk Analysis, 35(5), 828–848.

- Atreya, A., Ferreira, S., & Kriesel, W. (2013). Forgetting the flood? An analysis of the flood risk discount over time. Land Economics, 89(4), 577–596.

- Baranzini, A., & Ramirez, J. V. (2005). Paying for quietness: The impact of noise on Geneva rents. Urban Studies, 42(4), 633–646.

- Bin, O., & Kruse, J. B. (2006). Real estate market response to coastal flood hazards. Natural Hazards Review, 7(4), 137–144.

- Bin, O., & Landry, C. E. (2013). Changes in implicit flood risk premiums: Empirical evidence from the housing market. Journal of Environmental Economics and Management, 65(3), 361–376.

- Bin, O., & Polasky, S. (2004). Effects of flood hazards on property values: Evidence before and after Hurricane Floyd. Land Economics, 80(4), 490–500.

- Bin, O., Kruse, J. B., & Landry, C. E. (2008). Flood hazards, insurance rates, and amenities: Evidence from the coastal housing market. Journal of Risk and Insurance, 75(1), 63–82.

- Boelmann, B., & Schaffner, S. (2018). FDZ data description: Real-estate data for Germany (RWI-GEO-RED). Advertisements on the internet platform ImmobilienScout24. RWI Projektberichte.

- Browne, M. J., & Hoyt, R. E. (2000). The demand for flood insurance: Empirical evidence. Journal of Risk and Uncertainty, 20(3), 291–306.

- Browne, M. J., Knoller, C., & Richter, A. (2015). Behavioral bias and the demand for bicycle and flood insurance. Journal of Risk and Uncertainty, 50(2), 141–160.

- Chivers, J., & Flores, N. E. (2002). Market failure in information: The national flood insurance program. Land Economics, 78(4), 515–521.

- Chow, G. C. (1960). Tests of equality between sets of coefficients in two linear regressions. Econometrica: Journal of the Econometric Society, 591–605.

- Conway, D., Li, C. Q., Wolch, J., Kahle, C., & Jerrett, M. (2010). A spatial autocorrelation approach for examining the effects of urban greenspace on residential property values. The Journal of Real Estate Finance and Economics, 41(2), 150–169.

- Daniel, V. E., Florax, R. J. G. M., & Rietveld, P. (2007). Long term divergence between ex-ante and ex–post hedonic prices of the Meuse River flooding in The Netherlands. In 47th Congress of the European Regional Science Association: Local Governance and Sustainable Development, Paris (pp. 1–20).

- Gibbons, S. (2004). The costs of urban property crime. The Economic Journal, 114(499), F441–F463.

- Greenstone, M., & Gayer, T. (2009). Quasi-experimental and experimental approaches to environmental economics. Journal of Environmental Economics and Management, 57(1), 21–44.

- Harrison, D., T. Smersh, G., & Schwartz, A. (2001). Environmental determinants of housing prices: The impact of flood zone status. Journal of Real Estate Research, 21(1–2), 3–20.

- Hilber, C. A. (2005). Neighborhood externality risk and the homeownership status of properties. Journal of Urban Economics, 57(2), 213–241.

- Kim, C. W., Phipps, T. T., & Anselin, L. (2003). Measuring the benefits of air quality improvement: A spatial hedonic approach. Journal of Environmental Economics and Management, 45(1), 24–39.

- Kriesel, W., & Landry, C. (2004). Participation in the National Flood Insurance Program: An empirical analysis for coastal properties. Journal of Risk and Insurance, 71(3), 405–420.

- Kunreuther, H., & Pauly, M. (2004). Neglecting disaster: Why don't people insure against large losses?. Journal of Risk and Uncertainty, 28(1), 5–21.

- Lamond, J., & Proverbs, D. (2006). Does the price impact of flooding fade away?. Structural survey.

- LeSage, J. P. (2014a). Spatial econometric panel data model specification: A Bayesian approach. Spatial Statistics, 9, 122–145.

- LeSage, J. P. (2014b). What regional scientists need to know about spatial econometrics. https://ssrn.com/abstract=2420725

- LeSage, J., & Pace, R. (2009). Introduction to spatial econometrics. Taylor & Francis. doi:10.1201/9781420064254.

- Michel‐Kerjan, E. O., & Kousky, C. (2010). Come rain or shine: Evidence on flood insurance purchases in Florida. Journal of Risk and Insurance, 77(2), 369–397.

- Moran, P. A. (1950). A test for the serial independence of residuals. Biometrika, 37(1/2), 178–181.

- Morgan, A. (2007). The impact of Hurricane Ivan on expected flood losses, perceived flood risk, and property values. Journal of housing research, 16(1), 47–60.

- Ortega, F., & Taṣpınar, S. (2018). Rising sea levels and sinking property values: Hurricane Sandy and New York’s housing market. Journal of Urban Economics, 106, 81–100.

- Osland, L., & Thorsen, I. (2013). Spatial impacts, local labour market characteristics and housing prices. Urban Studies, 50(10), 2063–2083.

- Pace, R. K., & LeSage, J. P. (2004). Chebyshev approximation of log-determinants of spatial weight matrices. Computational Statistics & Data Analysis, 45(2), 179–196.

- Parmeter, C. F., & Pope, J. C. (2013). Quasi-experiments and hedonic property value methods. In Handbook on experimental economics and the environment. Edward Elgar Publishing.

- Rambaldi, A. N., Fletcher, C. S., Collins, K., & McAllister, R. R. (2013). Housing shadow prices in an inundation-prone suburb. Urban Studies, 50(9), 1889–1905.

- Rosen, S. (1974). Hedonic prices and implicit markets: Product differentiation in pure competition. Journal of Political Economy, 82(1), 34–55.

- Shultz, S.D. & Fridgen, P.M. (2001). Floodplains and housing values: Implications for flood mitigation, Journal of the American Water Resources Association, 37(3), 595–603

- Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124–1131.

Appendix 1

Robustness Analyses

We also analyze whether the relevance of indirect price effects for flood zone location varies with the specific characteristics of our model specification, observation time and study area. Thus, we run three robustness analyses. First, we alternate the spatial weight matrix to test the robustness of flood price effects across these variations. Second, we use our previous dataset for the flood-prone city of Dresden but swap theoretical FZ for actual floodplains. We also test for a variation in these floodplain price effects over time. Third, we analyze theoretical FZs in the neighboring cities of Magdeburg and Leipzig and finally in the whole Elbe area.

Variation of Spatial Weight Matrix

In this step, we test the sensitivity of our results regarding a variation in the spatial weights matrix. We start with an OLS regression as the base model. Then we use an inverse distance ‘five nearest neighbors’ setting, which has the second highest model probability in the Bayesian model comparison (see Panel B of ). Additionally, we use an inverse distance band specification, including properties within a threshold of 100 m as a cluster.13 The new calculated FZ effects are mostly robust to all variations (see ). In general, indirect effects naturally decrease when the threshold of the matrix, and thus the number of affected properties, is lower. For the distance-based approach, there are properties left with zero neighbors, resulting in mostly decreased indirect effects. The significant coefficients of direct effects from the OLS model disappear while controlling for spatial correlation. However, the simple OLS model (λ = 0) is rejected due to a high and statistically significant Moran’s I statistic for OLS residuals and significantly positive λ in all other spatial specifications. For all spatial model specifications, Moran’s I statistics are insignificant and approximately equal to zero, indicating that these models almost completely account for the existing spatial correlation.

Table A1-1. Variation of the spatial weights matrix.

Table A1-2. Event studies.

Table A1-3. Event studies (difference in differences).

Table A1-4. Spatial studies.

Event Studies

The major flooding that Dresden experienced in 2002 and 2013 resulted in significant losses. Thus, we analyze price effects for the location in inundated areas and use dummy variables for both flood events, which are equal to the affected area in 2002 (inundated during the ‘flood 2002’ = 1, zero otherwise) and in 2013 (inundated during the ‘flood 2013’ = 1, zero otherwise). On average, we expect negative direct and indirect price effects for a location in a floodplain due to flood damage at the property or in the neighborhood. However, these negative effects can be offset due to other beneficial location characteristics, reconstruction measures after the flood events, or simply by buyers and sellers being unaware of the flood risk. Results for the dummy variables are presented in . The ‘flood 2002’ model indicates statistically insignificant price effects apart from a positive indirect effect of 4.2% for condominiums, which can stem from a desirable neighborhood location that offsets the floodplain status of these properties. Furthermore, the period between the ‘flood 2002’ and our observation time is rather long, therefore prior floodplain status may not be available to buyers, resulting in insignificant or positive price effects. The location in inundated areas from ‘flood 2013’ results in a direct effect of 8.9% for houses, which is significant at a level of 5%. A positive price effect of houses in inundated areas in 2013 that outweighs negative effects after the flood may be due to either an attractive location or a better building structure after reconstruction due to flooding. The indirect effect for houses within the inundation area is statistically significant at the 10% level and indicates a price discount of 9.1%. This is reasonable in cases where flood damage to neighboring properties is visible and reduces the prices of property nearby. The direct and indirect effects for condominiums, however, are statistically insignificant, indicating that for condominiums, location in a prior floodplain has no remaining price impact. Thus, while interpreting price effects from floodplains, sources of potential biases need to be taken into account in order to understand the pricing of actual flood risk.

The following analysis is based on either actual floodplains (‘memory 2013’) or theoretical flood zones (‘memory zones’). To analyze whether flood price effects change over time, for instance due to changing flood awareness based on the memory effects of buyers and sellers (see “Theoretical Flood Impact on Property Pricing”), we implement a spatial ‘difference in differences’ (DND) model. The DND is a quasi-experimental approach and enables us to determine the observed changes in prices of a treatment group—properties in the inundation area or in FZ 2-4—against prices of a control group—properties outside of the inundation area or in FZ 1—due to an exogenous event, here ‘flood 2013’ (for a general discussion, see Greenstone & Gayer, Citation2009; Parmeter & Pope, Citation2013). Changing price effects are measured by an interaction term that incorporates both a binary variable for the inundation area (or the theoretical insurance-based flood zone) and a time variable counting the months after the flood event occurred in June 2013.

The results are presented in . For the ‘memory 2013’ model, we find a positive and statistically significant direct effect for houses (15.8%) and find a negative coefficient for the interaction term of -0.4%. This indicates that the positive price effect stems from a generally beneficial location associated with the inundation area before the 2013 event occurred. After the event, the locational price effect is reduced due to experienced loss. For condominiums, indirect effects are statistically significant and suggest that prices are reduced by 15% from the location of the neighborhood in inundation areas before the 2013 event occurred. Indirect effects also show a price increase of 0.8% per month after the event, which could be a result of reconstruction in the neighborhood. Thus, prices for condominiums are generally not affected by being located in a floodplain. However, when controlling for the development of price effects after the 2013 event, condominiums are more sensitive to impacts of neighboring properties compared with houses. This is supported by the dense neighborhood structure of condominiums, where a neighboring property might be located in the same building, thus reconstruction measures have a stronger impact on prices for condominiums.

For the ‘zone 2013’ model, we observe a statistically significant direct effect of -14.9% in FZ 4 and an indirect effect in FZ 4 of -34.8% for houses before the 2013 event, which is further reduced by 0.8% per month after the event. For condominiums, there is a statistically significant direct price effect in FZ 2 of -2.7% before the event. Furthermore, spatially lagged coefficients indicate that there are statistically significant price reductions of 9.7%, 10%, and 39.3% in the respective FZs resulting from the neighborhood. However, these indirect price effects were increased by 0.3% and 0.4% per month in FZ 2 and FZ 3 after the event occurred, which confirms the results from the ‘memory 2013’ model for condominiums. Thus, indirect price effects for flood zone status of condominiums are changed due to the 2013 flood event, whereas there is only an adjustment of price effects in FZ 4 for houses. Summing up, price effects from theoretical flood zones and actual floodplains vary widely, so our separated analysis is reasonable in order to gain unbiased comparisons of flood price effects. This is also in line with Atreya and Ferreira (Citation2015).

Spatial Variations in Flood Risk

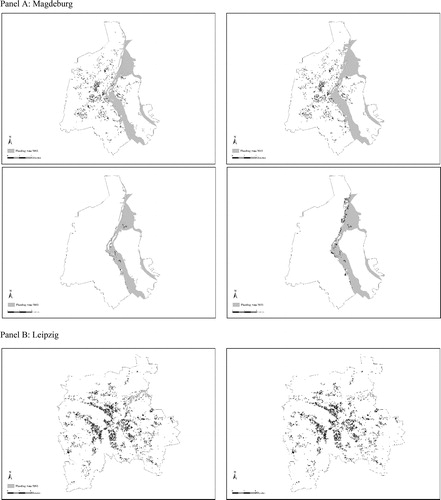

We also extend our study to the neighboring cities of Magdeburg and Leipzig as a spatial test for robustness, comparing price effects from the different locations. We test whether the high relevance of indirect effects is a special case in Dresden and whether these indirect effects depend on specific urban characteristics. Spatially robust indirect effects, however, would provide further evidence for their importance in the context of flood risk. Magdeburg was also affected by flooding events in 2002 and 2013 and is, like Dresden, directly located on the River Elbe. Although Magdeburg is located downstream and the warning time is typically longer, the amount of floodwater is not reduced because it cannot expand into open spaces due to protection measures in upstream cities. Whereas the floodplain in Dresden in 2013 was significantly smaller than in 2002, the amount of floodwater in Magdeburg was significantly higher in 2013. Conversely, Leipzig is located further away from the River Elbe and only indirectly experienced flooding during the events of 2002 and 2013. However, in regional economic importance and population size Leipzig almost equals Dresden, thus providing a comparative basis between mostly theoretical FZs (Leipzig) and a mixture of theoretical FZs and flood experience (Dresden). This allows us to analyze whether the risk awareness of sellers and buyers varies with the type of risk information available across the same region.

The results are presented in . In Magdeburg, property prices are reduced by 21.4% in FZ 3 for houses and increased by 11.8% in FZ 4 for condominiums. Indirect effects indicate a price reduction of only 14.3% in FZ 3 for houses. Since most of the properties in our dataset for Magdeburg are located outside inundation areas and have not experienced structural damage, we find insignificant or even positive price effects. However, average flood damage in Magdeburg was high, so our sample may exhibit a selection bias. In general, a sample selection bias occurs if the dataset is non-randomly collected and therefore is not representative of the whole population. Contrarily, it would be at least representative of a specific period: sellers do not offer properties in these locations in the aftermath of a flood event, as they may assume reduced selling opportunities. A comparison of our dataset with all existing properties in Magdeburg indicates that properties in floodplains are underrepresented, perhaps resulting in positive biased price effects.14 Condominiums in FZ 4 of our dataset may not have experienced flooding, resulting in a positive price adjustment. In Leipzig, we find direct price effects of 12.9% in FZ 3 for houses and 6.6% in FZ 2 for condominiums. Indirect effects indicate price increases of 30.6% in FZ 2 and 30.3% in FZ 3 for houses. For condominiums, indirect effects amount to -6.6% in FZ 2 and -53.4% in FZ 4. Although the indirect effects for condominiums almost correspond to our findings in Dresden, the positive direct and indirect effects for houses indicate a different pricing of FZs. Since Leipzig is not located on the River Elbe, we control for positive amenities correlated with waterside location by including an interaction term between the land elevation and the distance from the nearest body of water. For houses, there may be other positive amenities correlated with FZs, resulting in positive direct and indirect price effects.

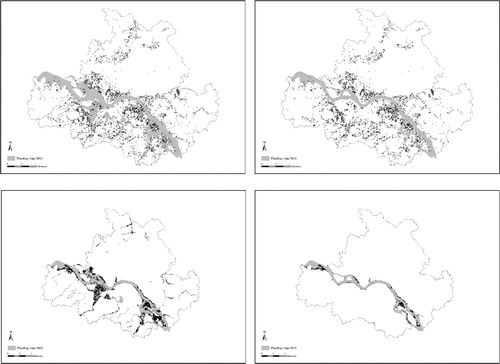

Finally, we analyze direct and indirect flood price effects in the whole ‘Elbe area’ to incorporate all locational differences in study areas along the river and estimate average price effects for the whole river basin. We include in our estimation properties within a distance corridor from the River Elbe of about 10 km to each side of the river and find that for houses, direct effects indicate a statistically significant price reduction of 4.0% in FZ 2 and significant indirect effects of -2.4% and -15.3% in FZ 2 and FZ 4, respectively.15 For condominiums, we find statistically significant direct effects of -2.0% in FZ 2 and -12.5% in FZ 4. Indirect effects are only statistically significant for FZ 2 and amount to -3.8%. These results indicate that there is no substantial variation in flood price effects from those of the city of Dresden. However, direct effects of flood zone location have a slightly higher relevance when analyzing the whole river basin. In areas that are more rural, housing density is less high, so effects from the neighborhood become less important, perhaps resulting in a higher relevance of direct effects.

Taken together, the size and importance of indirect effects vary with the specific characteristics of the study area including flood experience (Leipzig) and urban structures (Elbe area). In Leipzig, four out of six indirect effects become statistically significant and are partly positive. For the Elbe area, we find three statistically significant indirect effects that almost correspond to those in Dresden. The results for Magdeburg must be interpreted carefully, since significantly fewer properties are situated on floodplains. Overall, the spatial variations provide further evidence that indirect effects are generally important in analyzing flood price effects, but they need to be interpreted in the context of the specific study area.

Appendix 2

Further Tables

Figure A1-1. Inundated properties during the flooding events in 2002 and 2013.