?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Increasing numbers of economists and policymakers consider that reindustrialisation is a key factor in enhancing economic growth and a better standard of living in post-crisis Europe. Therefore, a new European Union industrial policy focuses on increasing manufacturing share in gross domestic product (G.D.P.). The assumption of recently developed theoretical models states that development of the financial sector is essential for economic growth and therefore for the growth of the manufacturing industry. The aim of this research is to examine the importance of the financial conditions in the process of industrialisation in Central and Eastern European countries. The results of a macro panel model that examines which factors influence the manufacturing value added as a percentage of G.D.P. suggest that the role of the financial sector is very important for the level of industrialisation in the analysed countries. The research is based on data collected from the World Development Indicators database published by the World Bank for the period from 2005 to 2015.

1. Introduction

Deindustrialisation is usually defined as an absolute or relative decrease of employment in industry, or as a decrease in the share of industry in gross domestic product (G.D.P.). Today, the term deindustrialisation mainly refers to the experience of the advanced economies of the world. Most of these economies have been deindustrialising from the beginning of the second half of the twentieth century. This trend was particularly obvious in the employment share of manufacturing. Employment deindustrialisation was associated with the loss of good jobs, rising inequality, and a potential decline in innovation capacity (Rodrik, Citation2016). Clark (Citation1940) proposed the theory of a reversed U-shaped relationship between economic development and manufacturing employment. He claimed that, as an economy develops, prices of agricultural products and relative demand for them decreases, while manufacturing prices and relative demand for them increases. The result is an increase in manufacturing employment. In the later stage of development, demand for manufacturing products decreases. This shifts the employment from manufacturing to the service sector.

In terms of output, deindustrialisation has been less remarkable and uniform. This pattern was obscured by the frequent reliance on value-added measures at current rather than at constant prices. However, the trend of deindustrialisation has been spread to developing countries and was more striking in low and middle-income industries. According to Rodrik (Citation2016), these countries have experienced premature deindustrialisation. The author expects that premature deindustrialisation can have potentially significant economic and political consequences, including lower economic growth and democratic failure. Namely, in most of these countries manufacturing has started to shrink at lower levels of income compared with the levels of income in developed countries when the process of deindustrialisation started. Therefore, developing countries are becoming service economies without experiencing a whole process of industrialisation.

Recently, literature trends have been based on examining the importance of reindustrialisation. The first wave of literature on reindustrialisation appeared in the 1980s in Europe and the U.S.A. The reindustrialisation literature in Europe was focusing on the creation of new innovative industries, activities and products, with high priority for the environmental protection industry, and was associated with political changes in Central and East Europe. These changes were associated with the crisis and decline of state-owned industries, leading to some deindustrialisation. This subject became important again after the latest economic crisis (Camarinha-Matos, Citation2013).

As mentioned above, before the 2008 crisis, the dominant opinion was that deindustrialisation was a prerequisite for the successful economic development. However, after the crisis, this opinion has been changed, and a much greater appreciation of the importance of industry has become evident. Increasing numbers of economists and policymakers consider that reindustrialisation is a key process for enhancing economic growth and a better standard of living in post-crisis Europe. Therefore, a new industrial policy in the European Union (E.U.) focuses on increasing manufacturing share in G.D.P. This is particularly important for new E.U. member states from Central and Eastern Europe. In these countries, the decline of state-owned industry had initiated a wide deindustrialisation process – the increasing role of services and the relative marginalisation of industry. In this process, post-socialist states have been transformed into service-dominated economies. Although the deindustrialisation process has been stopped in a few Central and Eastern European countries (C.E.E.C.s), such as the Czech Republic and Poland, in countries such as Croatia the deindustrialisation process has caused significant reallocation of resources from the industrial sector to the service sector. Due to this reallocation, the level of industrial production in Croatia is at a lower level than before the transition.

In the last few decades, the process of financial liberalisation has changed the economic structure worldwide. Even though the assumption of recently developed theoretical models implies that development of the financial sector is important for economic growth, and therefore for the growth of the manufacturing industry (Gourinchas & Jeanne, Citation2006), empirical evidence of the link between financial sector development and industrialisation is inconclusive. Some authors found strong support for the growth-enhancing hypothesis, and some other found only weak or mixed evidence of positive growth. Strong support for growth-enhancing financial liberalisation was documented in the work of Bekaert, Harvey, and Lundblad (Citation2005), Quinn and Toyoda (Citation2008) and Gehringer (Citation2013), while Rodrik (Citation1998) and Edison, Levine, Ricci, and Sløk (Citation2002) found only a weak growth effect. In addition, the negative influence of financial globalisation has been found in enhanced financial instability (Rodrik Citation1998; Stiglitz Citation2004) and increased volatility of industrial production (Levchenko, Rancière, & Thoenig, Citation2009). In C.E.E.C.s, reforming the banking sector was the first crucial step towards financial development. In the transition process, from the 1990s, foreign banks were allowed to enter the market, and within a decade they held a majority share in most C.E.E.C.s’ banks. As a result, a heavily regulated industry turned into a highly competitive one, stimulating economic growth to some extent (Caporale, Rault, & Sova, Citation2009).

Due to the transition process in C.E.E.C.s, these countries have experienced the process of deindustrialisation and financial development at the same time. However, despite the widely recognised importance of financial sector development and reindustrialisation on economic growth, little research has been conducted on the relationship between the financial sector and industrialisation. This is particularly true when one considers this issue in C.E.E.C.s that, to the best of our knowledge, has not been addressed in empirical literature. Our research seeks to fill this gap in the literature. Therefore, the aim of this research is to examine the role of the financial conditions in the process of industrialisation in C.E.E.C.s (Bulgaria, Croatia, the Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia and Slovenia) for the period 2005–2015. The panel model is applied in order to examine the importance of the financial sector in the process of deindustrialisation in C.E.E.C.s.

The article is structured as follows. The next section gives an overview of existing literature on the relationship among analysed variables. The stylised facts and descriptive statistics about industrialisation and variables of interest analysis in C.E.E.C.s are presented in Section 3. Model specification and results are presented in Section 4. Concluding remarks are in the last section of the article.

2. Empirical literature

In most previous empirical works, deindustrialisation was defined as decline of manufacturing employment in total employment. Clark (Citation1940) attributed the shift of employment from manufacturing to services to the normal structural change of all economies on their development path. With economic development, as real income per capita rises, the relative demand for agricultural products falls and relative demand for manufacturing first rises, and then falls in favour of services. This occurs as a consequence of the higher rate of relative productivity in the industrial sector and of the systematic changes in consumption patterns in different development stages. The theory was adopted by many economists who state that deindustrialisation emerges with the higher rate of productivity growth in manufacturing relative to services, consequently lowering the employment growth in manufacturing relative to services, even if output increases at the same rate (Rowthorn & Wells, Citation1987; Krugman & Lawrence, Citation1993; Rowthorn & Ramaswamy, Citation1997; Rowthorn & Coutts, Citation2004; Tregenna, Citation2011).

According to Rowthorn and Wells (Citation1987) this is positive form of deindustrialisation. They argue that deindustrialisation can also occur as negative process, as result of a structural disequilibrium in the economy that prevents a nation from reaching its growth potential or employment of its resources. It is manifested in poor performance in the manufacturing sector, and is accompanied by a slowdown in manufacturing output and productivity (Alderson, Citation1999). Finally, it will result in poor performance of the economy in general, a decline in competitiveness and growth in unemployment, since the labour shed is not absorbed by the service sector. Rowthorn and Wells (Citation1987) also identified ‘trade-related deindustrialisation’. They concluded that nations that run a manufacturing trade surplus, ceteris paribus, will devote more resources and labour to this sector than nations that run deficits.

Following Rowthorn’s earlier explanation of deindustrialisation as the consequence of higher productivity growth in manufacturing and the reallocation of labour from manufacturing to services, Palma (Citation2005, Citation2014) adds that it results from a reduction in income elasticity for manufacturers and a new international division of labour (including ‘outsourcing’). He develops a new concept of the ‘Dutch disease’, pointing to an additional form of deindustrialisation in cases where a country discovered significant natural resources, developed export service activities, mainly finance or tourism, or as a result of changes in economic policy. In addition, Palma (Citation2014) emphasises a case of ‘reverse’ reindustrialisation, a reduction in manufacturing employment associated with a fall in income per capita, typical for countries of the former Soviet Union and Eastern Europe.

Felipe, Mehta, and Rhee (Citation2014) raise the question whether today’s developing economies can achieve high-income status without first building large manufacturing sectors, and how difficult it is to sustain high levels of manufacturing activity. They found that practically every economy that enjoys a high income today experienced a manufacturing employment share in excess of 18–20%, and that the maximum expected employment share for a typical developing economy has fallen to around 13–15%. That is why the authors conclude that the path to prosperity through industrialisation may have become more difficult.

Rodrik (Citation2016) documents a significant deindustrialisation trend in recent decades. He notices that countries are running out of industrialisation opportunities sooner and at much lower levels of income compared with the experience of early industrialisers. The author emphasises the differences between countries, and underlines that Asian countries and manufacturing exporters have been largely insulated from those trends, while Latin American countries have been especially hard hit. The author finds that advanced economies have lost considerable employment, but they have done very well in terms of manufacturing output shares at constant prices. The evidence suggests that both globalisation and labour-saving technological progress in manufacturing have been behind these developments.

On analysing the literature dealing with the importance of (re)industrialisation, it can be concluded that it has been always actualised in crisis and post-crisis periods. Industrial policies in C.E.E.C.s have had a pattern similar to the developed European countries, which evolved from a vertical towards a horizontal and ‘fresh’ approach. After the end of the Second World War, most governments in the U.S.A. and Western Europe applied the Keynesian vertical approach. Active direct state support was directed towards selected key industrial sectors and less developed regions to stimulate post-war economic recovery and preserve employment in large firms. In the late 1980s, with the creation of the E.U. Single Market, this ‘vertical’ industrial policy lost favour as the Reagan–Thatcher economic policies emphasised the withdrawal of the state from economic management, the privatisation of state-owned enterprises, a greater reliance on market forces and the creation of a business-friendly ‘investment climate’ in which the spontaneous forces of the market would decide which industries or sectors would prosper, and which would fall by the wayside (Bartlett, Citation2014). Under the new pro-competition ‘horizontal’ approach to industrial policy, the role of the government was to enable a growth-enhancing environment, ensuring the quality of institutions which will create a competitive market. These new industrial policies have been designed to support privatisation and small-to-medium enterprises (S.M.E.s), develop technology parks and local industrial clusters, and promote the transfer of knowledge from universities and research institutes to the business sector (Bartlett, Citation2014). The recent global financial crises, and the shift of economic power to new emerging economies in East Asia and the rise of the B.R.I.C. economies led by China, stimulated the European Commission (E.C.) to rethink the E.U. industrial development approach with the aim to increase its global competition. Consequently, in 2010 the E.C. introduced a ‘fresh’ industrial policy. Although the horizontal approach to industry policy is still relevant and its aim is to prevent unfair competition within the E.U., the Commission identified specific sectors for development at a European level, such as space technology, clean and energy efficient motor vehicles, transport equipment, healthcare, environmental goods, energy supply industries, security industries, chemicals, engineering, transport equipment, agro-food and business services (European Commission, Citation2010). The new industrial policy draws on the provisions of the Lisbon Treaty, in particular Article 173 T.F.E.U. on industrial policy. As part of the Europe 2020 strategy the Commission will now regularly report on the E.U.’s and Member States’ industrial policies, organised through the Competitiveness Council and the European Parliament (Bartlett, Citation2014).

The deindustrialisation process in each particular country is the result of a mix of positive and negative factors that have changed over time. Many socio-economic, financial and institutional factors could promote or hinder the industrialisation process. A country’s size, its natural resources, the skills of its people, the stability of its government and institutions and their ability to implement the fiscal, monetary, and exchange rate policies all influence sustainable industrial development. Research literature that clarifies the understanding of the role of the financial sector in the process of de(re)industrialisation is scarce. The weaknesses of existing work could be overcome if the literature on the connections between the financial sector and economic growth is taken into consideration (e.g., King & Levine, Citation1993; Levine, Citation1997, 2005; Rajan & Zingales, Citation1998). This literature has focused on the role of financial intermediaries in facilitating exchange and providing liquidity (Bencivenga & Smith, Citation1991) and in diversifying risks (Acemoglu & Zilibotti, Citation1997). Recently, attention has been paid to the impact of the financialisation process, financial liberalisation policies and financial development on economic growth.

Svilokos and Burin (Citation2017) highlight that although financial development is usually perceived as a positive process with positive effects on economic growth (Bekaert et al., Citation2005; Quinn & Toyoda, Citation2008; Gehringer, Citation2013), the real effects may be opposite. In the scientific literature financialisation has usually been proved to have negative effects on economic growth and development (Yeldan, Citation2000; Epstein, Citation2001; Stockhammer, Citation2004; Palley, Citation2007; Freeman, Citation2010). The rise of the financial sector as a dominant force in many developed economies over the last two decades has been accompanied by widespread deindustrialisation, and has left these economies vulnerable to destructive financial bubbles (Bellamy-Foster & Magdoff, Citation2009).

The roots of analysis of the impact of interest rate changes on the economy can be found in the neoclassical growth framework (Jorgenson, Rational, & Patterns, Citation1967; Jorgenson & Hall, Citation1971, McKinnon–Shaw complementarity hypothesis). According to the neoclassical (or marginalist) approach, which is nowadays still dominant among economists, the negative dependence of investment on the interest rate is necessary for establishing a stable full-employment general equilibrium. Expected inflation rates are an integral part of determining whether or not an interest rate impacts investment. The real interest rate represents a fundamental valuation of the influence between inflation and nominal interest rates, and therefore is used in broader economic analyses of consumption/saving and investment decisions. An increase in the real interest rate creates an incentive to postpone consumption and increase saving, which can negatively impact economic activity. It is argued that a reduction in interest rates increases liquidity, lowers the cost of consumption and increases aggregate demand. This demand expansion should lead to secondary effects such as accelerated investment and employment growth, so inducing a multiplier process in the economy (La Roux and Ismail, Citation2004). Conventional economic analysis suggests that lower interest rates will directly increase investment spending by lowering the cost of capital, which should raise production capacity and thus potential future output growth. The size of this effect depends on the financial conditions of firms and on economic structures, such as the capital intensity of production (Peersman & Smets, Citation2002). The European Commission (Citation2009a, Citation2009b) conducted an analysis on a sample of 25 E.U. countries, and the findings imply that real interest rates have a robust negative correlation with manufacturing output growth.

Interest rate uncertainty has obvious effects on investment (Ingersoll & Ross, Citation1992; Alvarez & Koskela, Citation2004; Alvarez, Citation2010). Unlike the traditional theory, some scholars have concluded that there was a positive correlation between interest rate and investment. McKinnon (Citation1973) and Shaw (1973) found out that real interest rates and growth rates are positively related. They concluded that financial restrictions and letting market forces determine real interest rates lead to higher real interest rates and higher levels of savings, which in turn induce economic growth. Lanyi and Saracoglu (Citation1983) found positive correlation between investment and interest rate in an uncertain environment and Beccarini (Citation2007) concluded that the higher volatility the interest rate had, the more positive the correlation would be. There are also some scholars who believe that the rates may have no impact on investment. Dore, Makken, and Eastman (Citation2013) found that investment depended on the level of demand in the macroeconomic, rather than interest rates. Real interest rate could be negative if inflation is higher than the interest rate. It could cause depreciation in the exchange rate and investment reallocation to some other countries where governments are able to maintain inflation. The McKinnon–Shaw hypothesis (1973) states that a low or negative real rate of interest discourages savings and hence reduces the availability of loanable funds, constrains investment, and in turn lowers the rate of economic growth.

Exchange rate fluctuations are important for industry, especially for exporting sectors. There is a relatively large body of literature suggesting a correlation between the real exchange rate and G.D.P. growth (Levy-Yeyati & Sturzenegger, Citation2002; Petreski Citation2009). Rodrik (Citation2008) concluded that a weak real exchange rate could compensate for institutional weaknesses and market failures which lead to underinvestment in the traded goods sector in developing countries. Greenwald and Stiglitz (Citation2006) stated that, in developing countries, favourable exchange rates help export sectors like manufacturing to compete. Aizenman and Lee (Citation2010), Benigno, Converse, and Fornaro (Citation2015) and McLeod and Mileva (Citation2011) concluded that exchange rate undervaluation acts like a subsidy to the tradable sector. Glüzmann, Levy-Yeyati, and Sturzenegger (Citation2012) find that undervaluation does not affect the tradable sector, but does lead to higher savings, investment and employment through lower labour costs and income redistribution in developing countries.

Di Nino, Eichengreen, and Sbracia (Citation2011) and Hausmann, Pritchett, and Rodrik (Citation2005) demonstrate that rapid growth accelerations are often correlated with real exchange rate depreciations. Rodrik (Citation2008) finds that the growth acceleration occurs, on average, after 10 years of steady increase in undervaluation in developing countries. Habib, Mileva, and Stracca (Citation2016) concluded that a real appreciation (depreciation) significantly reduces (raises) the annual real G.D.P. growth, more than in previous estimates in the literature. Their overall conclusion is that the exchange rates do matter for growth in developing economies, but substantially less so in advanced ones, which confirms and strengthens the conclusions of Rodrik (Citation2008). Kappler, Reisen, Schularick, and Turkisch (Citation2012) find limited effect of 25 episodes of large nominal and real appreciations on economic growth. Nouira and Sekkat (Citation2012) find no evidence that undervaluation promotes growth for developing countries, after excluding overvaluation episodes. Although most empirical papers confirm a positive relation between weak real exchange rates and growth, Dollar (Citation1992) shows that overvaluation harms growth, whereas Razin and Collins (Citation1997) and Aguirre and Calderon (Citation2005) find that large (over)undervaluation hurts growth, while modest undervaluation enhances growth. Rose (Citation2014) emphasised that the exchange rate regime was not an important determinant of growth during the global financial crisis.

Industrial export-oriented countries have access to large markets. Moreover, trade liberalisation allows access to imported inputs, technology and capital as well as a more competitive exchange rate which could boost industry growth. Jamison, Lau, and Wang (Citation2003) point out that trade openness has a strong impact on economic growth. Rodrik (Citation1998) considers that trade openness increases the risk of fluctuations in the output of the economy caused by fluctuations in trade conditions.

Foreign direct investment (F.D.I.) may initiate industrialisation through the provision of financial resources and links to export markets. F.D.I. may contribute to the host country through technology and knowledge transfer, improved competition and human capital, upgrading its technological, operational and managerial effectiveness. In this way F.D.I. may trigger industrialisation in developing countries (Søreide, Citation2001). Many economists consider F.D.I. as an important contributor to the development process of developing and emerging economies (Kudina & Pitelis, Citation2014). Adopting new technologies has proved to be a precondition for industrial development. Host countries free-ride on expensive research investment usually paid for by multinational corporations. The welfare effects of F.D.I. are not necessarily beneficial. Dependency theorists argue that F.D.I. in developing countries creates investment dependence and delays development in these countries (Boswell & Dixon, Citation1990), and that dependence on foreign capital impedes their development (Bornschier & Chase-Dunn, Citation1985; London & Smith, Citation1988; Boswell & Dixon, Citation1990). Although it is crucial to acknowledge that dependency scholars have mainly focused on economic growth and development, perhaps it is reasonable to expect that F.D.I. and long-term dependence on foreign capital in developing countries negatively influence industrialisation. Bornschier and Chase-Dunn (Citation1985) argue that while F.D.I. flows might enhance economic growth in developing countries in the short run, the long-term dependence on foreign capital, indicated by F.D.I. stock, hurts economic growth.

3. Some stylised facts and descriptive analysis

After the 2008 crisis, the E.C. set the target to increase the contribution of manufacturing to G.D.P. from 16% to 20% by 2020 in the European economy. The details of common industrial policy are stated in the document named ‘Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions for a European Industrial Renaissance’ (European Commission, Citation2014). This document points out the need for modernisation and reindustrialisation of the E.U.’s industry through highly adaptive, productive and technologically advanced industries.

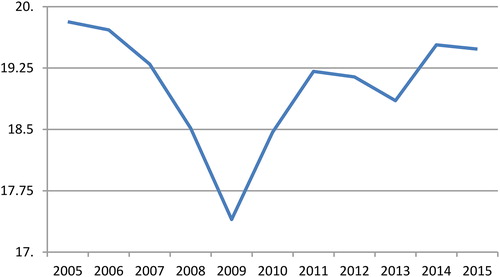

shows average manufacturing value added share of G.D.P. for C.E.E.C.s. It is evident that this share fell in all C.E.E.C.s in the period 2005–2008. The exceptions were Bulgaria and Poland. In Bulgaria the share was higher in 2008 compared with that in 2005, and in Poland this share remained approximately the same. This declining trend may be explained by the deindustrialisation process, in which these countries have been transformed into service-oriented economies. In this period, the industry share in the Czech Republic, Hungary, the Slovak Republic and Slovenia accounted for more than 20% of G.D.P., while in other countries this share was lower. Latvia had the lowest share.

Figure 1. Manufacturing value-added average as a percentage of G.D.P. in C.E.E.C.s. Source: World Bank Data.

After the 2008 crisis, as mentioned above, the general opinion was to strengthen the industrial sector. This process, measured as an increase in manufacturing value added as a percentage of G.D.P., was successful in almost all countries. The only exception was Croatia ( in Appendix). However, the manufacturing value added as a percentage of G.D.P. in C.E.E.C.s is higher than the E.U. average (16%). The exceptions are Croatia and Latvia. The high share of industry may be explained by the fact that in transition countries the deindustrialisation process was shorter compared with Western economies.

For comparison purposes, the manufacturing sector’s share of gross value added has decreased in all western European economies since 2005. The exception is Germany, where this share has remained almost unchanged. Still, there are large differences in industry share within these countries in 2015 – Ireland (36.9%) and Portugal (13.8%) (World Bank Data). Even though the decrease in industry share may be explained by the stronger growth of the service sector, in some of these countries this decline can be explained by worsening international competitiveness. This decline in competitiveness is related to price-related factors and efficiency of institutions, financial, product and labour markets (Heymann & Vetter, Citation2013).

According to the review of previous literature, it seems that the process of industrialisation is determined by various factors, such as real effective exchange rate (R.E.E.R.), interest rate, household final consumption (H.F.C.), F.D.I.s and trade openness. The data for analysing variables of interest for the period 2005–2015 were obtained from the World Development Indicators (W.D.I.) database published by World Bank. Variables included in our research are defined and analysed in the following section.

R.E.E.R. is the weighted average of a country’s currency relative to an index or basket of other major currencies, adjusted for the effects of inflation. For calculating R.E.E.R. the weights are determined by comparing the relative trade balance of a country’s currency against each country within the index. This exchange rate is used to determine an individual country’s currency value relative to the other major currencies. The trend of the R.E.E.R. in all C.E.E.C.s was positive in the period before crises. This finding indicates that currencies of the analysed countries have been strengthened in that period. However, after the crisis the R.E.E.R. has been relatively stable in all countries ( in Appendix).

The real interest rate ratio is calculated as the real interest rate in specific country divided by average real interest rate in the Economic and Monetary Union (E.M.U.). The real interest rate is an interest rate that has been adjusted to remove the effects of inflation to reflect the real cost of funds to the borrower and the real yield to the lender or to an investor. The real interest rate of an investment is calculated as the amount by which the nominal interest rate is higher than the inflation rate. In the period 2005–2015 the real interest rate has significantly varied within and among the analysed countries. However, according to the real interest rate ratio indicator, it is evident that this ratio for Croatia and the Slovak Republic was higher than 1 for almost the whole analysed period (2005–2015).1 This indicates that in Croatia and the Slovak Republic the credit costs were worse than in the E.M.U. member countries. In other analysed countries this ratio was declining in the period 2005–2008, and indicates that credit conditions were improved in comparison to those in the E.M.U. After the crisis, by 2013 the real interest rate ratio indicator started to rise, and this trend suggests the inferior position of these countries. However, after 2013 the trend of the real interest rate ratio indicator has been declining, and indicates the improvement regarding financial conditions in Bulgaria, Poland, Romania, the Slovak Republic and Slovenia ( in Appendix).

H.F.C. expenditure (formerly private consumption) is the market value of all goods and services, including durable products (such as cars, washing machines and home computers), purchased by households. It includes the expenditures of nonprofit institutions serving households, even when reported separately by the country. Data are in constant local currency. H.F.C. was relatively stable in all analysed countries for the observed period.

F.D.I. is the net inflows of investment to acquire a lasting management interest (10% or more of voting stock) in an enterprise operating in an economy other than that of the investor. It is the sum of equity capital, reinvestment of earnings, other long-term capital, and short-term capital as shown in the balance of payments. This series shows net inflows (new investment inflows less disinvestment) from foreign investors and is divided by G.D.P. In the observed period, F.D.I. net inflows had a slightly positive trend before the crisis and negative trend after the crisis. In Hungary, Bulgaria and Estonia this trend was significant ( in Appendix).

The analysis of the trade openness indicator, measured as the sum of import (as a percentage of G.D.P.) and export (as a percentage of G.D.P.), shows that in all C.E.E.C.s trade openness had a positive trend for the whole observed period, with the exception in the time of crisis when this indicator sharply decreased ( in Appendix).

4. Model specification and results

This study investigates a panel of 11 C.E.E.C.s for the period 2005–2015 and comprises 121 observations. We included: Bulgaria, Croatia, the Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia and Slovenia. Our explained variable is the industrialisation in C.E.E.C.s measured as the manufacturing value added as a percentage of G.D.P. in constant prices (MAN) that is regressed against these independent variables: REER, real interest rate ratio (INT_R), HFC, FDI and openness (OPEN). The data were obtained from the W.D.I. database published by the World Bank.

In order to examine the influence of financial conditions on the process of deindustrialisation, a fixed-effect panel regression model can be employed. Hsiao (Citation2003) and Klevmarken (Citation1989) list several benefits from using panel models – controlling for individual heterogeneity, more variability, less collinearity among the variables, more degrees of freedom and more efficiency of the data, the effects that are simply not detectable in pure cross-section or pure time-series data can be better detected and measured, etc.

The basic class of models that can be estimated using panel techniques may be written as (1):

(1)

(1)

where i denotes cross-section dimension (in our case countries), t denotes the time-series dimension (in our case years), α is a scalar (constant term), β is K × 1 vector of coefficients, Xi,t is the i,t-th observation on K explanatory variables, ui,t is error component. This error component consists of the time-invariant unobservable individual-specific effect that is not included in the regression (µi), and the reminder of the disturbance that varies within cross-section and time-series dimension (νi,t):

(2)

(2)

In fixed-effects model µi are assumed to be fixed parameters to be estimated, and νi,t are independent and identically distributed with mean 0, and variance σ2ν. The Xi,t are assumed to be independent of the νi,t for all i and t.

Because we are focusing on the specific set of countries (C.E.E.C.s) and our inference is restricted to this set, according to Baltagi (Citation2008) the fixed-effects model is an appropriate specification. Using a fixed-effects model, the ‘individuality’ of each country is taken into account by letting the intercept vary for each country, but it is still assumed that the slope coefficients are constant across countries. The adequacy of fixed effect can be tested by employing Cross-section F and Cross-section Chi-square tests with the null hypothesis that the cross-section effects are redundant.

The fixed-effects model, by the substitution of (2) into (1), can be written as (3):

(3)

(3)

Now, Generalised Method of Moments (G.M.M.) and Instrumental Variable (I.V.) estimator can be performed on (3) to get estimates of α, β and µ. Namely, the G.M.M./I.V. estimator should be used if the error distribution cannot be considered independent of the regressors’ distribution. Hansen (Citation1982) proposed to use the G.M.M. approach in situations when we have heteroskedasticity of unknown form. Since then, G.M.M. has become a very popular tool that is used in empirical research. The standard I.V. estimator is a special case of G.M.M. estimator.

We estimate a model of the form:

(4)

(4)

contains the results of our model and the results of tests. All statistical tests confirm the statistical validity of the proposed model.

Table 1. Model and diagnostics.

The results of the model indicate that REER, INT_R and OPEN are statistically significant variables, while HFC, FDI are not. The sign of REER is negative, and that means that appreciation of domestic currency will have negative effect on manufacturing production. This is in line with Greenwald and Stiglitz (Citation2006), who argued that favourable exchange rates help export sectors, like manufacturing, to compete. This sector is a tradable sector, and in this case exchange rate undervaluation can act like a subsidy (Aizenman and Lee, Citation2010, Benigno et al., Citation2015, McLeod and Mileva, Citation2011). Furthermore, our research results suggest that the negative impact of decreased foreign competitiveness due to stronger domestic currency is higher than the gains that manufacturing industry receives due to lower prices of imported raw materials.

As expected, INT_R has negative sign. This is in line with the analysis of the European Commission (Citation2009a; Citation2009b) that was conducted on the sample of 25 E.U. countries, and which shows that real interest rates have a robust negative correlation with manufacturing output growth. According to our finding, the higher real interest rate in a specific C.E.E.C. compared with the interest rate in the E.M.U. will negatively influence the manufacturing production in that country. This finding is also in accordance with La Roux and Ismail (2004).

The variable OPEN is significant and has a positive sign. This indicates that industrial production is international trade oriented through exporting final products and importing the raw materials. This supports the findings of Jamison et al. (Citation2003), whose paper shows that trade openness has a strong impact on economic growth, and Rodrik’s (1998) conclusions of positive relationship between openness and output of the economy. Grossman and Elhanan Helpman (Citation1991) explained connections by the flow of knowledge and new technologies.

We also included FDI in our model because some papers suggest that there may be some connections between manufacturing production and this variable. We did not find this connection in our sample of C.E.E.C.s, and this could be explained by the fact that most of the F.D.I.s were directed to the service sector rather than manufacturing.

Furthermore, we included the HFC variable in our model in order to find out whether H.F.C. is important for manufacturing production. We find that it does not directly influence MAN, but because of endogeneity of this variable (negative relation between HFC and INT_R) we used it with lags as excluded instruments which improve our model characteristics.

5. Concluding remarks

For a long time, deindustrialisation was considered as a prerequisite for successful economic development. However, after the crisis of 2008, this opinion has changed, and a much greater appreciation of the importance of industry has become evident. Increasing numbers of economists and policymakers consider that reindustrialisation is a key factor for enhancing economic growth and a better living standard in the post-crisis Europe. A new industrial policy in the E.U. focuses on increasing manufacturing share in G.D.P. This is particularly important for new E.U. member states from C.E.E.C.s. In these countries the deindustrialisation process has caused reallocation of resources and employment from the industrial sector to the service sector. Due to this reallocation, the level of industrial production in several C.E.E.C. economies is at a lower level than before the transition.

In this paper we examine the role of the financial conditions for industrialisation level in C.E.E.C.s in the period 2005–2015. To the best of our knowledge, this issue has not been addressed in the existing empirical literature. The analysis of the results in this research suggests that real interest rate ratio, R.E.E.R. and trade openness are very important for the level of industrialisation. Even though the deindustrialisation process resulted in decreased manufacturing share in G.D.P. in all C.E.E.C.s, this share is still above the E.U. average. This finding implies that policy makers in C.E.E.C.s should provide additional incentives in order to stimulate modernisation and reindustrialisation of the E.U.’s industry through highly adaptive, productive and technologically advanced industries. Furthermore, the results highlight the necessity of expanding the analysis of this issue and of conducting additional study of micro-level data to verify these findings. Also, it could be very useful to analyse the composition of industry in each country in order to determine its influence on the relationship between industrialisation and financial conditions.

Discloser statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 If the indicator is greater than 1 that means that the real interest rate in specific country is higher than the average real interest rate in EMU.

References

- Acemoglu, D., & Zilibotti, F. (1997). Was Prometheus unbound by chance? Risk, diversification and growth. The Journal of Political Economy, 105(4), 709–751.

- Aguirre, A., & Calderon, C. (2005). Real exchange rate misalignments and economic performance. Central Bank of Chile Working Papers No. 315. Retrieved from: https://core.ac.uk/download/pdf/6642514.pdf

- Aizenman, J., & Lee, J. (2010). Real exchange rate, mercantilism and the learning by doing externality. Pacific Economic Review, 15(3), 324–335.

- Alderson, A. (1999). Explaining deindustrialization: Globalization, failure, or success? American Sociological Review, 64(5), 701–721.

- Alvarez, L. H. R., & Koskela, E. (2004). Irreversible Investment under Interest Rate Variability: New Results. Bank of Financial Discussion Papers, EconWPA 0404007 Retrieved from: https://ideas.repec.org/p/wpa/wuwpot/0404007.html

- Alvarez, L. H. R. (2010). Irreversible capital accumulation under interest rate uncertainty. Mathematical Methods of Operations Research, 72(2), 249–271.

- Baltagi, B. (2008). Econometric analysis of panel data. Chichester: Wiley.

- Bartlett, W. (2014). Shut Out? South East Europe and the EU's New Industrial Policy, LEQS Paper No. 84. Retrieved from: http://dx.doi.org/10.2139/ssrn.2534513

- Beccarini, A. (2007). Investment sensitivity to interest rates in an uncertain context: Is a positive relationship possible?. Economic Change and Restructuring, 40(3), 223–234.

- Bekaert, G., Harvey, C. R., & Lundblad, C. (2005). Does financial liberalization spur growth?. Journal of Financial Economics, 77(1), 3–56.

- Bellamy-Foster, J., & Magdoff, F. (2009). The Great Financial Crisis, New York: Monthly Review Press. Retrieved from https://monthlyreview.org/product/great_financial_crisis/

- Bencivenga, V. R., & Smith, B. D. (1991). Financial intermediation and endogenous growth. Review of Economic Studies, 58(2), 195–209.

- Benigno, G., Converse, N., & Fornaro, L. (2015). Large Capital Inflows, Sectoral Allocation, and Economic Performance. International Finance Discussion Papers 1132. Retrieved from: http://dx.doi.org/10.17016/IFDP.2015.1132

- Bornschier, V., & Chase-Dunn, C. (1985). Transnational corporations and underdevelopment. New York: Praeger.

- Boswell, T., & Dixon, W. J. (1990). Dependency and rebellion: A cross-national analysis. American Sociological Review, 55(4), 540–559.

- Camarinha-Matos, L.M., (Ed.). (2013). Collaborative Business Ecosystems and Virtual Enterprises: IFIP TC5/WG5. 5 Third Working Conference on Infrastructures for Virtual Enterprises (PRO-VE’02) May 1–3, 2002, Sesimbra, Portugal. Vol. 85. Springer, 2013.

- Caporale, G., Rault, C., & Sova, R. (2009). Financial development and economic growth: Evidence from ten new EU members. Deutsches Institut fur Wirtschaftsforschung, Discussion Paper 940. Retrieved from https://www.econstor.eu/bitstream/10419/29733/1/611469170.pdf

- Clark, C. (1940). The conditions of economic progress. London: Macmillan.

- Di Nino, V., Eichengreen, B., & Sbracia, M. (2011). Real Exchange Rates, Trade, and Growth: Italy 1861-2011, Banca díItalia, Economic History Working Papers No. 10. Retrieved from: https://www.bancaditalia.it/pubblicazioni/quaderni-storia/2011-0010/index.html/com.dotmarketing.htmlpage.language=1

- Dollar, D. (1992). Outward-oriented developing economies really do grow more rapidly: Evidence from 95 LDCs, 1976-1985. Economic Development and Cultural Change, 40(3), 523–544.

- Dore, M., Makken, R., & Eastman, E. (2013). The monetary transmission mechanism, non-residential fixed investment and housing. Atlantic Economic Journal, 41(3), 215–224.

- Edison, H. J., Levine, R., Ricci, L. A., & Sløk, T. M. (2002). International financial integration and economic growth. Journal of International Money Finance, 21(6), 749–776.

- Epstein, G. (2001). Financialization, rentier interests and central bank policy. PERI Conference on Financialization of the World Economy (pp. 1–43), December 7–8, 2001, Department of Economics, University of Massachusetts, Amherst, MA.

- European Commission. (2014). Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions for a European Industrial Renaissance. Brussels: European Commission Retrieved from: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52014DC0014&from=EN

- European Commission. (2010)., An integrated industrial policy for the globalisation era: Putting competitiveness and sustainability at centre stage, COM(2010) 614. Brussels: Commission of the European Communities. Retrieved from: https://www.kowi.de/Portaldata/2/Resources/fp7/2010-com-industrial-policy.pdf

- European Commission. (2009a). European Competitiveness Report 2008. Luxembourg: European Commission. Retrieved from: file:///C:/Users/Korisnik/Downloads/cr-2008-final_4058.pdf

- European Commission. (2009b). Sectoral Growth Drivers and Competitiveness in the European Union. Luxembourg: European Commission. [Retrieved from: file:///C:/Users/Korisnik/Downloads/2009_sectoral_growth_drivers_3318%20(1).pdf

- Felipe, J., Mehta, A., & Rhee, C. (2014). Manufacturing Matters… but It’s the Jobs That Count, ADB Economics Working Paper Series, No. 420. Retrieved from https://www.adb.org/sites/default/files/publication/149984/ewp-420.pdf

- Freeman, R. B. (2010). It’s financialization!. International Labour Review, 149(2), 163–183.

- Gehringer, A. (2013). Growth, productivity and capital accumulation: The effects of financial liberalization in the case of European Integration. International Review of Economics and Finance, 25, 291–309.

- Glüzmann, P. A., Levy-Yeyati, E., & Sturzenegger, F. (2012). Exchange rate undervaluation and economic growth: DÌaz Alejandro (1965) revisited. Economics Letters, 117(3), 666–672.

- Gourinchas, P.-O., & Jeanne, O. (2006). The elusive gains from international financial integration. Review of Economic Studies, 73(3), 715–741.

- Greenwald, B., & Stiglitz, J. E. (2006). Helping infant economies grow: Foundations of trade policies for developing countries. American Economic Review, 96(2), 141–146.

- Grossman, G., & Elhanan Helpman, E. (1991). Trade, knowledge spillovers, and growth. European Economic Review, 35(2–3), 517–526.

- Habib, M. M., Mileva, E., & Stracca, L. (2016). The real exchange rate and economic growth: revisiting the case using external instruments. European Central Bank, Working Paper No 1921. [Retrieved from https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1921.en.pdf

- Hansen, L. (1982). Large sample properties of generalized method of moments estimators. Econometrica, 50(4), 1029–1054.

- Hausmann, R., Pritchett, L., & Rodrik, D. (2005). Growth accelerations. Journal of Economic Growth, 10(4), 303–329.

- Heymann, E., & Vetter, S. (2013). Europe’s re-industrialisation. The gulf between aspiration and reality. EU Monitor European Integration Deutschebank Research, Retrieved from https://www.dbresearch.com/PROD/DBR_INTERNET_ENROD/PROD0000000000323902.pdf

- Hsiao, C. (2003). Analysis of panel data. Cambridge: Cambridge University Press.

- Ingersoll, J. E., & Ross, S. (1992). Waiting to invest. Investment and uncertainty. The Journal of Business, 65(1), 129.

- Jamison, D. T., Lau, L. J., & Wang, J. (2003). Health’s contribution to economic growth in an environment of partially endogenous technical progress, Disease Control Priorities Project, Working Paper no.10. Retrieved from: https://www.researchgate.net/publication/228354905_3_Health's_Contribution_to_Economic_Growth_in_an_Environment_of_Partially_Endogenous_Technical_Progress

- Jorgenson, D., Rational, C., & Patterns, O. (1967). Growth in a monetary economy: Discussion. American Economic Review, 57(2), 557–559.

- Jorgenson, D., & Hall, R. E. (1971). Application of the theory of optimum capital accumulation. In G. Fromm (Ed.) Tax incentives and capital spending (pp. 9–60, Investment 2, ch. 2, pp. 27–76). Washington: The Brookings Institution,.

- Kappler, M., Reisen, H., Schularick, M., & Turkisch, E. (2012). The macroeconomic effects of large exchange rate appreciations. Open Economies Review, 24(3), 471–494.

- King, R. G., & Levine, R. (1993). Finance, entrepreneurship and growth. Journal of Monetary Economics, 32(3), 513–542.

- Klevmarken, N. A. (1989). Panel studies: What can we learn from them? Introduction. European Economic Review, 33, 523–529.

- Krugman, P., & Lawrence, R. (1993). Trade, jobs, and wages. National Bureau of Economic Research Working Paper Series, Working paper No. 4478. Retrieved from: http://www.nber.org/papers/w4478.pdf

- Kudina, A., & Pitelis, C. (2014). De-industrialisation, comparative economic performance and FDI inflows in emerging economies. International Business Review, 23(5), 887–896.

- Lanyi, A., & Saracoglu, R. (1983). Interest Rate Policies in Developing Countries. Occasional Paper 22, Washington, DC: International Monetary Fund.

- Le Roux, P., & Ismail, B. (2004). Modelling the impact of changes in the interest rates on the economy: An Austrian Perspective. South African Journal of Economic and Management Sciences, 7(1), 132–150.

- Levchenko, A. A., Rancière, R., & Thoenig, M. (2009). Growth and risk at the industry level: The real effects of financial liberalization. Journal of Development Economics, 89(2), 210–222.

- Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35, 688–726.

- Levy-Yeyati, E., & Sturzenegger, F. (2002). To float or to fix: evidence on the impact of exchange rate regimes on growth. American Economic Review, 12(2), 1–49.

- London, B., & Smith, D. A. (1988). Urban bias, dependence and economic stagnation in noncore nation. American Sociological Review, 53(3), 454–463.

- McKinnon, R. I. (1973). Money and capital in economic development. Washington, DC: Brookings Institution.

- McLeod, D., & Mileva, E. (2011). Real exchange rates and growth surges. Fordham Economics Discussion Paper Series, 2011-04. Retrieved from: https://www.researchgate.net/publication/267236373_Real_Exchange_Rates_and_Productivity_Growth

- Nouira, R., & Sekkat, K. (2012). Desperately seeking the positive impact of undervaluation on growth. Journal of Macroeconomics, 34(2), 537–552.

- Palley, T. I. (2007). Financialization: what it is and why it matters. The Levy Economics Institute and Economics for Democratic and Open Societies, Working Paper No. 525, 1–31. Retrieved from: https://scholarworks.umass.edu/cgi/viewcontent.cgi/referer=https://www.google.hr/&httpsredir=1&article=1124&context=peri_workingpapers

- Palma, J. G. (2005). Four sources of de-industrialisation and a new concept of the ‘Dutch Disease’. In J.A. Ocampo (Ed.), Beyond Reforms: Structural dynamic and macroeconomic vulnerability. Palo Alto, CA: Stanford University Press and the World Bank.

- Palma, J. G. (2014). Industrialization, ‘premature’. Deindustrialization and the Dutch Disease. Revista NECAT, 3(5), 7–23.

- Peersman, G., & Smets, F. (2002). The industry effects of monetary policy in the Euro area. European Central Bank, Working paper no. 165. Retrieved from: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp165.pdf?615e8f2c92db7cb856cc31eee5c7007c

- Petreski, M. (2009). Exchange-rate regime and economic growth: a review of the theoretical and empirical literature. Kiel Institute for the World Economy, Discussion Paper No. 2009-31. Retrieved from: https://www.econstor.eu/bitstream/10419/27729/1/604541589.PDF

- Quinn, D. P., & Toyoda, A. M. (2008). Does capital account liberalization lead to economic growth? An empirical investigation. Review of Financial Studies, 21(3), 1403–1449.

- Rajan, R. G., & Zingales, L. (1998). Financial dependence and growth. The American Economic Review, 88(3), 559–586.

- Razin, O., & Collins, S. M. (1997). Real exchange rate misalignments and growth. NBER Working Paper No. 6174. Retrieved from: http://www.nber.org/papers/w6174.pdf

- Rodrik, D. (1998). Who needs capital account convertibility? In Should the IMF pursue capital account convertibility? Essays in International Finance (vol. 207, pp. 55–65. Princeton: Princeton University Press.

- Rodrik, D. (2008). In D. W. Elmendorf, N. G. Mankiw, & L. H. Summers (Eds.), The real exchange rate and economic growth. Brookings Papers On Economic Activity, Fall 2008. (pp. 365–412). Washington, DC: Brookings Institution.

- Rodrik, D. (2016). Premature deindustrialisation. Journal of Economic Growth, 21(1), 1–33.

- Rose, A. K. (2014). Surprising similarities: Recent monetary regimes of small economies. Journal of International Money and Finance, 49(A), 5–27.

- Rowthorn, R., & Coutts, K. (2004). De-industrialisation and the balance of payments in advanced economies. Cambridge Journal of Economics, 28(5), 767–790.

- Rowthorn, R. E., & Ramaswamy, R. (1997). Deindustrialisation: Causes and implications. The World Bank Economic Review, 10(2), 323–339.

- Rowthorn, R. E., & Wells, J. R. (1987). Deindustrialisation and foreign trade. Cambridge: Cambridge University Press.

- Shaw, E. (1973). Financial deepening in economic development. New York: Oxford University Press.

- Søreide, T. (2001). FDI and Industrialisation; Why technology transfer and new industrial structures may accelerate economic development?. Chr. Michelsen Institute working papers 3. [Retrieved from: https://www.cmi.no/publications/file/942-why-technology-transfer-and-new-industrial.pdf]

- Stiglitz, J. E. (2004). Capital-market liberalization, globalization, and the IMF. Oxford Review of Economic Policy, 20(1), 57–71.

- Stockhammer, E. (2004). Financialisation and the slowdown of accumulation. Cambridge Journal of Economics, 28(5), 719–741. doi:10.1093/cje/beh032

- Svilokos, T., & Burin, I. (2017). Financialization and its impact on process of deindustrialization in the EU. Zbornik Radova Ekonomskog Fakulteta u Rijeci: Časopis za Ekonomsku Teoriju i Praksu / Proceedings of Rijeka Faculty of Economics: Journal of Economics and Business, 35(2), 583–610.

- Tregenna, F. (2011). Deindustrialisation, structural change and sustainable economic growth. MERIT Working Papers 032, United Nations University - Maastricht Economic and Social Research Institute on Innovation and Technology (MERIT).

- Yeldan, A. (2000). The Impact of Financial Liberalization and the Rise of Financial Rents on Income Inequality The Case of Turkey. UNU/WIDER Working Paper No. 206, doi:10.1093/0199271410.003.0014.

Appendix

Table A1. Manufacturing value added as a percentage of G.D.P. in C.E.E.C.s.

Table A2. Real effective exchange rate in C.E.E.C.s.

Table A3. Real interest rate ratio in C.E.E.C.s.

Table A4. Foreign direct investment in C.E.E.C.s.

Table A5. Trade openness in C.E.E.C.s.