Abstract

This paper presents an innovative model for property portfolio assessment based on the concept of a growth-share matrix. The proposed real estate portfolio matrix uses two primary qualities of properties: their potential to accrue value over the holding period and their ability to generate stable positive cash flows. The aim of the model is to utilise these two dimensions in the assessment of the qualities of individual properties and to identify their subsets to meet preferences of different groups of real estate investors. The concept was developed to provide companies with strategic advice on how to optimise the sales strategy of their non-core property assets. This method can be applied successfully to both commercial and residential properties. The concept is subsequently utilised for the purpose of post-hoc structural analysis of the Polish commercial real estate market. Transaction analysis accentuates the prevalence of core assets in terms of both transaction volume and value. Value-added assets constitute a much smaller market segment but may nevertheless present a good opportunity for portfolio diversification. Speculative assets appear to be scarce, which is characteristic of the current phase of real estate market conjuncture.

1. Introduction

In today’s turbulent economies and dynamically changing real estate market conditions, making effective and strategically viable property investment decisions has become very difficult. Analysts and executives are seeking ways to optimise a company’s investment or divestment strategies in accordance with predefined strategic requirements and preferences. This is particularly challenging for corporate entities that have a large property portfolio but do not ordinarily invest in real estate as part of their core business activity. Typically, such portfolios consist of properties that may be substantially heterogeneous in terms of value, quality, and synergy. For non-specialised owners, the specificity of real estate appraisal and analysis may be difficult to grasp. Only professional capital investors or developers can understand the drivers and intricacies of property investment to effectively manage this group of assets and properly determine their full market value (Baum, Citation2015). In this situation, the utility maximising approach suggests that properties should be distributed among professional real estate market players that target different asset classes and are specialised in either real estate management or development.

The broad group of market professionals comprises large institutional capital investors who are mainly interested in high-value core properties that generate stable cash flows, whose value can be maintained or improved over a long period, and for which effective debt financing strategies and cost effectiveness are the heart of the business (Ooi, Citation2007). Typical examples of such properties include office buildings in central business districts, industrial properties, and retail centres. Other entities such as real estate developers seek properties that require major redevelopment to extract their full value by utilising the existing or potential zoning conditions for site redevelopment. Finally, there is a pool of small individual investors searching for small properties that could either be cash flow generating assets and/or be treated as speculative investments based on the overall value growth potential. An example would be acquisition for rental purposes of a portfolio of investment apartments that combine both qualities, as they are expected to provide the owner with relatively stable cash flows coupled with the possibility of capturing additional capital value during favourable market conditions. In contrast, an exclusive villa in a resort can be more difficult to rent, but the investor may be placing a bigger bet on the market demand for luxury commodities. The list of different and diverse types of potential investors could be much larger depending on, for instance, their targeted investment size or preferred real estate sector. However, they can be divided into three basic categories: long term-capital investors, developers, and small individual buyers seeking alternative ways of allocating their savings (Baum, Citation2015).

Considering the variety of requirements and specialisations of property buyers and sellers, there is a need to craft aiding tools customised for the management of the existing or potential portfolio by both transacting parties and consultants, who help buyers/sellers design customised strategies for investment/divestment processes. At the same time, the specificity of the real estate market elucidated in the following section warrants the application of non-conventional approaches to appraise real estate assets.

This paper introduces a novel tool—the real estate portfolio matrix (REPO-M)—designed to facilitate the structural analysis of real estate portfolios and, subsequently, tailor investment strategies suitable for various types of investors. The proposed analytical framework overcomes the limitations of purely quantitative algorithms of real estate appraisal by allowing a comprehensive evaluation of real estate assets based on ordinal classification. Exemplifying the application of REPO-M, we perform transactional analysis of the Polish commercial real estate market and demonstrate how REPO-M may be used as an analytical instrument for market research.

2. Literature review

Inherent features of the real estate market make the elaboration and implementation of an investment strategy a challenging task. Multiple decision aids have been designed (e.g., Trippi, Citation1989) to help investors select the assets most suitable for their portfolios and tailor portfolio characteristics to their individual risk preferences and return expectations. Plurality of opinions may persist regarding what constitutes the objective function of the real estate portfolio and which criteria should underlie the process of real estate asset selection. Ultimately, the real estate management strategy has the primordial goal of balancing the risk and returns of the assets in question to meet the investment needs of the owner.

The specificity of information flow within the real estate market may significantly influence the decisions of market participants (Garmaise & Moskowitz, Citation2004). Kummerow and Lun (Citation2005) state that information asymmetry is one of the key factors influencing investment strategies of real estate investors. The impeded information transfer may become further complicated by the heterogeneity and low liquidity of assets, excessive market segmentation, and inability of market participants to arrange an arbitrage due to imperfect information and high transaction costs (Evans, Citation1995; Buitelaar, Citation2007). Therefore, it has been argued frequently (e.g., Shilton & Tandy, Citation1993; Berrens & McKee, Citation2004) that the real estate market may manifest informational inefficiency and high information variance.

Inefficiency of the real estate market aggravates the problem of asset selection and portfolio management, particularly accentuating the trade-off between diversification and specialisation. The presence of pricing anomalies and general market disequilibrium may potentially engender attractive investment opportunities or prompt market participants to explore risk-mitigating alternatives and hedging strategies (Lyons, Citation2015; Brzezicka et al., Citation2018). The possibility of diversification may be largely dependent on the amount of disposable capital to be allocated among real estate assets. Large portfolios may undoubtedly benefit from cross-sector and global diversification. Hastings and Nordby (Citation2007) argue that the specificity of the real estate market makes it a perfect target for cross-border diversification. It has been evidenced that institutional investors tend to diversify their portfolios based on sectoral and geographical factors (Webb, Citation1984; De Witt, Citation1996), with the latter being a major driver of returns of the real estate portfolio (Lee & Devaney, Citation2007). Since local real estate markets are influenced by a multitude of geography-specific factors, such as the fiscal and monetary policy, demography, and political and geopolitical factors, rates of returns from local real estate markets may have very low correlation, which makes international diversification particularly beneficial (Eichholtz, Citation1996). Renigier-Bilozor et al. (Citation2014) use a rating methodology to elaborate an appraisal system applicable to local real estate markets, which would facilitate the decisions by market participants. The attractiveness of a particular real estate market is viewed as a complex combination of technical, social, economic, political, and behavioural factors.

Small real estate portfolios have limited potential for diversification. Therefore, asset selection becomes a predominant concern. When choosing an asset for inclusion in a real estate portfolio, investors have to decide the desired risk-return characteristics of the property, the asset management strategy aimed at maximising the return, and the holding period. Several studies have tried to elucidate the determinants and interrelations shaping the rate of return from real estate assets (Sivitanidou & Sivitanides, Citation1999; Brooks & Tsolacos, Citation2000). Dipasquale and Wheaton (Citation1996) stipulate that rates of return are greatly influenced by demand-side factors and general economic conjuncture. Amédée-Manesme et al. (Citation2016) argue that portfolio allocation decisions are dictated largely by the motivation to maximise investors’ utility function, which depends on the free cash flows generated by assets and the residual value at the end of the envisaged holding period. With respect to that, it would be consistent to argue that when selecting assets for their portfolios, real estate investors seek to either maximise the cash flows generated by the asset through the holding period or boost the property’s terminal value at the end of the holding period. In turn, the holding period, which may significantly differ between various groups of investors, is influenced by the market conditions and performance of a particular asset (Cheng et al., Citation2010). The holding period may be relatively longer for highly specialised illiquid properties, whose potential sale may also generate overwhelming transaction costs and require a significant discount on the intrinsic value. At the same time, Cheng et al. (Citation2010) postulate that investors may be prone to holding properties with relatively more volatile rates of return for a shorter time period.

There have been several attempts to classify real estate for the purposes of asset management, portfolio selection, and performance appraisal. Jackson and White (Citation2005) highlight that traditional classification models for real estate are based on geographical location and level of economic activity within the sector where the real estate is located. According to Jackson and White (Citation2005) and Louargand (1992), these classifications do not fully consider the asset-specific characteristics of real estate and, therefore, are not suitable for the purpose of portfolio optimisation. Tackling the problems of commercial real estate classification, Nelson and Nelson (Citation2003) use discriminant analysis to segregate the real estate market into segments reflecting the fundamental characteristics of the properties. Graham and Bible (Citation1992) propose a classification based on the following four factors: 1) rental rates and occupancy rates, 2) age and condition, 3) construction quality, and 4) location. Sehgal et al. (Citation2015) suggest that real estate assets should be selected based on the goodwill of the developer, location, and construction quality.

This study accentuates the importance of proper classification of real estate assets for optimising investment decisions of particular groups of investors by analysing market trends and developments as well as understanding factors that may fuel or impede the development of the real estate sector. In contrast with the geography – or sector – centred models of real estate market appraisal, we propose a classification based on the assets’ fundamental characteristics. The approach advocated in this paper should help real estate investors assess the real estate portfolio they currently own and, if necessary, adjust its structure to their risk-return profile

3. Concept of the REPO-M

The main goal of the paper is to introduce an analytical framework allowing comprehensive evaluation of the attractiveness of real estate portfolios. The model draws from the growth-share matrix originally developed by the Boston Consulting Group (BCG), which, since the 1960s, has been one of the most notable tools designed to help companies reassess the positioning of their products or services and devise alternative solutions for optimising their portfolios (Krühler et al., Citation2011; Kumar, Citation2012; Winona & Wandebori, Citation2012). By ordinally classifying the firms’ products and services within the growth-share matrix, the model recognises the need for a balanced portfolio composed of products with different potentials to generate positive cash flows both now and in the future. Such an approach allows one to further identify product/service-related challenges and opportunities and devise necessary strategic and tactical responses in accordance with the shareholder wealth maximisation principle.

Despite criticism of the model (Armstrong & Brodie, Citation1994), recent studies (Shuv-Ami, Citation2009; Amatulli et al., Citation2011; Ionescu, Citation2011; Krühler et al., Citation2011) show that 18% of companies still employ the original BCG growth-share matrix, with another 45% using it in a customised form. However, there is no evidence of similar usage of the two-dimensional matrix concept in the context of property portfolio assessment and management.

The proposed REPO-M concept is focused exclusively on the real estate market as it recognises the need of corporate entities and individuals to optimise their real estate portfolios in line with their generic business strategies.

The core idea behind the model is to measure the potential of the product (asset) to generate positive cash flows over a specified holding period. In the property market, this typically means that investors would look at a 5–10-year horizon to assess the size and riskiness of the cash proceeds, ignoring the terminal value of the asset, which would largely depend on the state of the market at the exit. The potential for generating cash is the primary factor considered by capital property investors, and thus a detailed assessment is required during the decision-making process.

In addition, the presented model recognises that some investors may be willing to place riskier bets on uncertain proceeds from positive changes in the overall capital value of the property, rather than focusing exclusively on the long-term stability of the cash flow. The risk-seeking investor would wish to grasp the additional property value growth arising from various sources such as identified property development potential, effective management, and expected favourable changes in market conditions. Compared with the classical BCG matrix, REPO-M proposes to replace the market share with the asset’s value growth potential as a better proxy for measuring the existing market opportunities.

Depending on the property’s characteristics, both measures can be assessed using multiple criteria, which can be further grouped into two basic categories: one related to the property’s inherent qualities and characteristics (internal factors) and the other reflecting changes in the external economic environment (external factors). presents a non-exhaustive list of these criteria. The list is not complete and can vary depending on the property’s intrinsic qualities and type (residential or commercial).

Table 1. A non-exhaustive list of the real estate portfolio matrix property assessment criteria.

It is worth noting that there have been multiple attempts to operationalise these criteria for quantitative appraisal of real estate assets. To the best of our knowledge, none succeeded in including all the relevant factors due to inherent limitations of the quantitative research methodology. Take, for example, the weighted average unexpired lease term (WAULT), which is undoubtedly a key factor influencing an asset’s attractiveness. For a typical commercial property, such as a fully leased office building, the quality and duration of the lease are major internal factors based on which the financial rationality of the project is examined. Legal and technical due diligence should ensure that potential investors’ future operating incomes are sufficiently secured with relevant covenants or guarantees, and that the building’s technical status would not deter the tenant from continuing the lease. In contrast, external factors influencing the property’s ability to generate a long-term positive cash flow, coupled with an expiring lease, would leverage the risk of an increase in vacant space, thereby potentially reducing cash flows generated in the future. The complexity of interrelations between the key characteristics of the property makes the quantification and analysis of the key value drivers extremely challenging.

An extensive list of factors, such as the one presented in , provides the overall picture of the security level and value-generating potential of a particular property for the investor. The asset’s attractiveness can be assessed either qualitatively or quantitatively depending on available data and individual preferences. The analyst should decide on the list of factors that would be adequate for the property type and characteristics. Fully leased office buildings would require a completely different set of assessment criteria compared with a land property or retail unit. Advanced multiscoring approaches may be applied, but the inherent element of subjectivity appears to be impossible to eliminate.

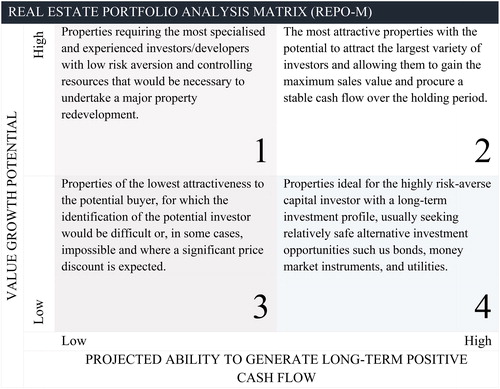

The chosen set of assessment criteria should allow the analyst to allocate the property into one of the four numbered fields of the analytical space of the REPO-M (). Each field represents a combination of two factors (projected ability to generate stable cash flows and value growth potential) corresponding to the risk-return profile of a particular group of investors.

Figure 1. Typology of the real estate assets in the real estate portfolio analysis matrix analytical space.

Source: Own elaboration.

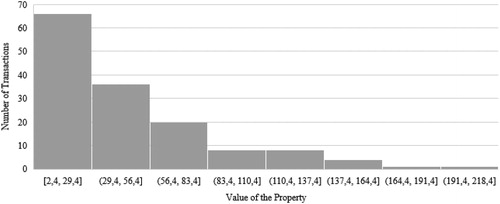

Figure 2. Sample structure by the value of the property (in million euros).

Source: Own elaboration.

The complementary assessment criteria involve presenting the position of properties in the form of circles of different diameters, whose sizes correspond to the properties’ values. This allows classification of the portfolio based on the investors’ buying potential, i.e., small individual investors vs. large institutional buyers. Considering the usual specialisation of the investors in specific real estate assets, such analysis should be performed separately for different segments (e.g., commercial and residential real estate).

The inherent heterogeneity of real estate assets makes their classification along the proposed dimensions difficult. The multitude of factors that determine the assets’ ability to generate stable long-term cash flows and increase their residual value limits the possible applications of quantitative methods that allow for a limited number of standardised explanatory variables. Most of the key factors enumerated in are difficult to operationalise due to their qualitative nature. Hence, expert appraisal may appear to be a valid option.

The resulting matrix establishes a foundation for making specific investment decisions such as acquisition/disposal of real estate assets, overhaul of asset management strategies, and further development of chosen properties already in the portfolio or to be acquired in the future.

Nonetheless, it must be noted that actual investment decisions are frequently contingent upon market-specific circumstances, such as taxation, regulatory framework, and project planning, and the investor’s tactical goals. For example, despite frequently being the most financially rewarding option, real estate development may be constrained (as in case of some real estate investment trusts) by tax qualification issues or statutory limitations on the permissible level of engagement in real estate development. In the presence of such regulatory constraints, channelling the underperforming real estate assets to other specialised investors may represent the most rational decision.

REPO-M may serve as a complementary analytical tool in real estate valuation, which is commonly performed by relying on the discounted cash flow (DCF) methodology. While DCF analysis allows for an explicit stand-alone quantitative appraisal of the asset in question, REPO-M ordinally positions and ranks real estate assets within the investor’s portfolio. REPO-M presents a unified and consistent approach that allows blending of asset evaluation criteria across property types and geographies. Thus, it is intended primarily as a decision-making tool facilitating the analysis and optimisation of real estate portfolios through the synthesis of qualitative and quantitative information.

4. REPO-M in practice: Structural analysis of the Polish commercial real estate market

Application of the REPO-M concept is demonstrated on the sampled transaction data from the Polish commercial real estate market for a 10-year period. The model is expected to reveal the relative preferences of the real estate investors and salient features of the structure of the real estate market in terms of the number and value of the transactions. The model may help investors assess whether the real estate market offers investments that may be of interest to them in view of their risk-return profile. In some cases, properties may change their relative position within the matrix over time, which may be attributable to the evolving real estate market conjuncture or changes in the preferences of real estate investors. In other words, the revealed patterns allow further analysis of demand- and supply-side factors that may have contributed to the observed dynamics.

We claim that using our matrix, real estate investors should be able to optimise their portfolios by channelling their resources to real estate assets that are the most suited to their risk-return expectations, while selling non-complementary assets to investors that specialise in managing them. Therefore, application of the proposed framework may contribute to improvement of the allocation efficiency of the real estate market.

The proposed methodological framework can be tested reliably on empirical data from a particular market. It can also be applied to individual real estate portfolios to assess the investor’s profile and preferences, thereby allowing one to develop an investment strategy that is most suitable for a particular risk-return profile. The proposed model should help discover the investment patterns anchored in the decision making of the market participants and allow for an in-depth analysis of the prevailing market trends. The structural analysis of transactional data may demonstrate the investors’ preferences with regard to the risk-return trade-off—the choice between value-added and core properties—and investors’ propensity to diversify their real estate portfolios across different asset types. On an aggregate level, this information is essential for real estate market research as it may pinpoint the crucial development patterns and presage future market dynamics.

The sample chosen for analysis includes 144 transactions involving commercial real estate properties in the Polish market for the period between 2009 and 2016. The total value of the transactions is 6552 billion euros. For clarity, the data pool was cleaned of portfolio transactions, which constituted a mix of different asset classes and thus could not be properly classified. The timing and geography of the transactions are summarised in . The sample structure in terms of transaction value is presented in .

Table 2. Timing and geography of the sampled transactions.

Each property from the research sample was assessed along two dimensions: 1) sustainability of the cash flows and 2) value growth potential. Considering the heterogeneity of the assets, which precluded the application of the quantitative techniques of analysis, we decided to revert to expert appraisal. A team of four experts was put together, and the Delphi methodology was used to arrive at a consensus. The panel comprised employees of a major Polish real estate broker. The experts were provided with full access to the available basic transaction data (i.e., property name, location, size, initial yield, list of major tenants, WAULT, etc.) and were asked to assign values for the analysed criteria on two separate scales from 0 to 10 (wherein 0 meant that the property had the lowest income sustainability and lowest value growth potential, while 10 meant that, in the experts’ opinion, the property had highly sustainable income and high value growth potential).

At the initial stage of assessment, the experts worked independently to minimise the risk of bias. They were informed that the assessment was not performed for commercial use. This allowed us to alleviate the potential distortionary impact of the brokers’ internal operational processes on the assessment results. Surprisingly, the experts were mostly in agreement regarding their opinions, provided that the necessary transactional data and property-related information were available. Ensuring availability of such data allows us to advocate expert appraisal as an efficient tool for screening and evaluating real estate assets. It is worth noting that the appraisal’s accuracy may be contingent on the efficacy of precautionary risk-mitigating measures taken by the broker, including the enforcement of firewall policies and appropriate ethical standards advocated by industry associations (e.g., Royal Institution of Chartered Surveyors). Thanks to their experience and expertise, real estate analysts appear to be positioned better to assess the attractiveness of real estate properties using a combination of qualitative and quantitative criteria. Information availability seems to play a crucial role in reducing the divergence in analysts’ assessment of real estate assets.

The same panel of experts categorised the sampled assets in accordance with a well-known classification into core, value-added, and opportunistic investments (McDonald & Stiver, Citation2004). The classification was based on the following criteria:

Core: These are modern and well-located assets leased to quality tenants. The objective of these investments is to provide investors with secure cash flows and modest capital appreciation. The income component typically represents a major part (above 70%) of the expected total return. Examples of core investments include central business districts, office buildings, retail centres, and industrial warehouses. The ability to enhance the value of core real estate significantly is limited compared with value-added and opportunistic investments. Core assets generally require little or no short-term capital expenditure other than normal repairs and maintenance (McDonald & Stiver, Citation2004).

Value-added: These are assets with upside potential realised through value-added asset management, refurbishment, redevelopment, or leasing-up of vacant space. These assets typically include ‘secondary’ properties, which, for various reasons, have depressed levels of cash flows. In addition, their value may have deteriorated over time relative to the broader market. Through hands-on ‘active management’, the investor focuses on increasing the asset’s income and terminal value (high capital value growth potential). Value-added investments appeal to knowledgeable institutional or individual investors seeking an enhanced return in exchange for somewhat higher levels of operational risk (McDonald & Stiver, Citation2004), as these risks can often be substantially mitigated. Value added investments can be generalised as corresponding to box 1 of the REPO-M.

Opportunistic: These assets tend to be growth and development oriented or centred on a repositioning or redevelopment strategy. These properties involve a range of high-risk strategies such as real estate development, highly leveraged financing, or transactions involving ‘turnaround’ potential (often known as distressed investing). This group may also include investments with complicated financial structures (including mezzanine debt), emerging market investments, or niche property sectors. Often, they include raw land or purchase of mortgage notes. The focus is on capital appreciation, and the returns are typically back-ended and achieved through a sale or completion of a development, often with little income along the way. Opportunistic strategies require specialised investment and management expertise due to their complexity and higher risk. Investors tend to be sophisticated and well capitalised with higher risk appetites than core or value-added investors. Opportunistic investment considers relatively short-term holding periods (less than three years in many cases). The key to success is to exit the investment expeditiously as the strategy is executed and the property’s value is maximised. Opportunistic investments require careful analysis of the real estate cycle and market trends to take advantage of dislocations and mispricing in the market.

Although opportunistic and value-added real estate may potentially generate returns higher than those of core investments, it has been shown that superior performance may commonly be derived from favourable market conditions, particularly from access to low-cost external financing, which may fuel the real estate market price (Shilling & Wurtzebach, Citation2012).

It is worth noting that while this classification is frequently used in practice, it may appear subjective as it allows the categories to overlap. The categorisation was done independently from the previously prepared assessment of the projected property’s ability to generate stable positive cash flow and value growth potential. We wanted to check whether income sustainability and value growth potential were valid predictors of the property’s categorisation as core, value-added, or opportunistic.

After the panel of experts independently assigned the markings for income sustainability and value growth potential as well as categorised the properties into three broad classes, we ran a probit regression to check whether the two factors underlying REPO-M were valid predictors of the categorisation. Results of the regression are presented in . Due to a small number of observations in the ‘opportunistic’ category (eight), this category was merged with the ‘value-added’ category and compared with the ‘core’ category (encoded as zero). Results of the tests demonstrate that the proposed parameters may be perceived as valid predictors of the categorisation of the sampled properties as ‘core’ and ‘value-added’, with the latter having significantly higher growth potential and lower income sustainability. The test also suggests that expert appraisal (Delphi method) may be perceived as a valid alternative for purely quantitative appraisal techniques. Thus, REPO-M may prove to be a useful instrument supplementing the conventional DCF analysis with a portfolio perspective. Acquisition/divestment decisions should be envisaged from the standpoint of optimisation of the overall portfolio performance, which is possible only through elaboration of a common analytical framework allowing comprehensive synthesis of the qualitative and quantitative appraisal criteria.

Table 3. Results of the probit regression checking the accuracy of expert appraisal of the sampled assets.

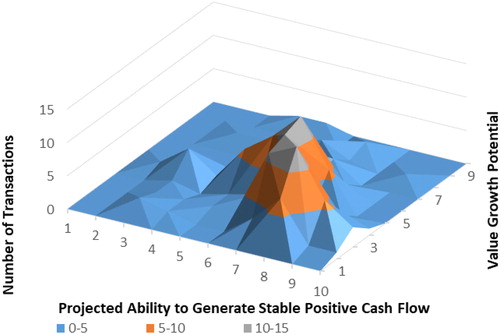

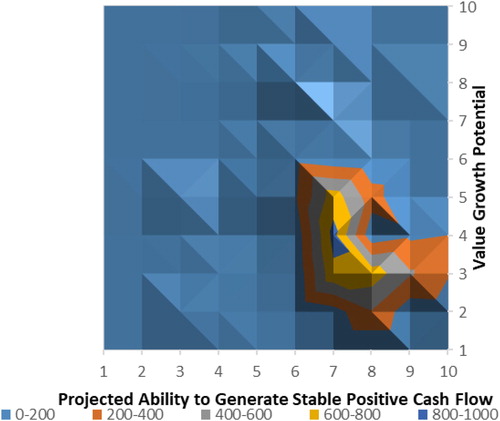

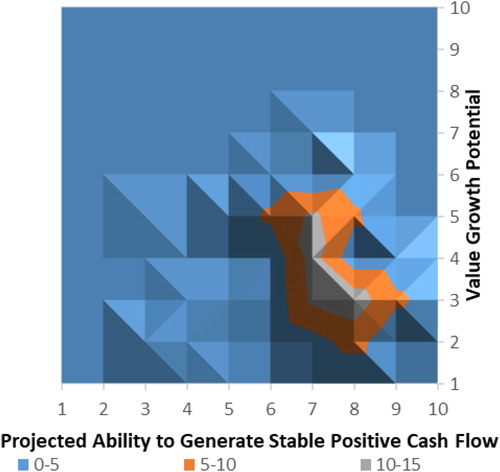

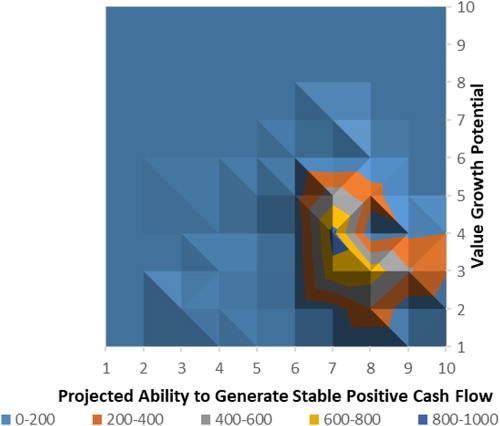

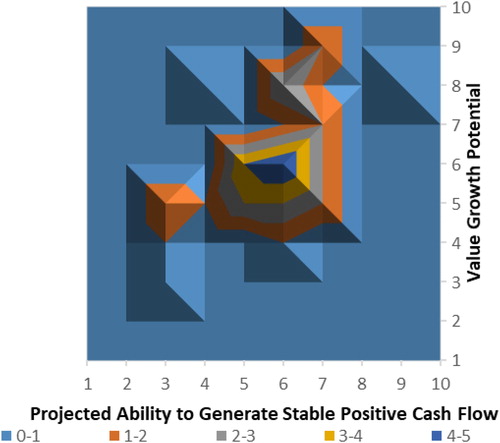

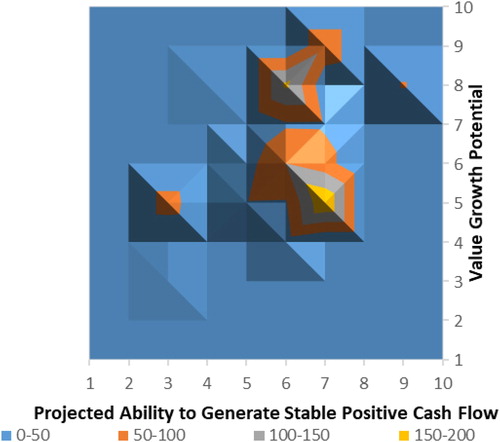

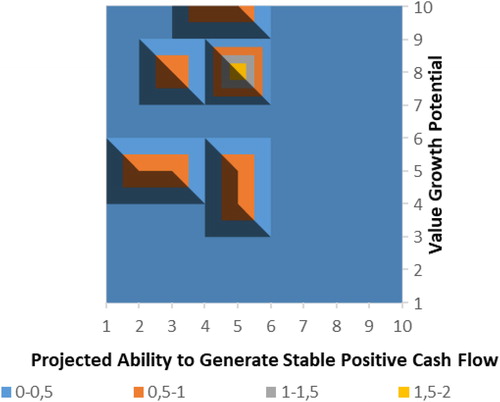

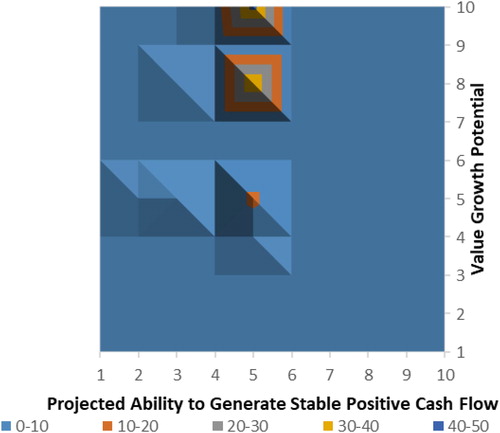

In the next step, we used REPO-M to analyse the structure of the sample. Analysis of the sampled commercial real estate transactions on the Polish market demonstrates the prevalence of core investments in terms of both the number and value of the transactions (). Value-added investments remain a viable option for diversification and boosting of portfolio returns despite constituting a much smaller part of the market and having considerably lower transaction value ( and ). Speculative opportunistic assets constitute a minor part of the sampled transactions ( and ); however, since the market for opportunistic real estate is highly sensitive to interest rates, future developments may cause a rapid shift of a significant part of available capital to the speculative segment. Transactions involving opportunistic assets are much less numerous and have a significantly lower average transaction value. As evidenced by the REPO-M, investments with high sustainability of cash flows and significant potential of value appreciation are rare and represent modest figures in terms of both number of transactions and transaction volume.

Figure 3. Real estate portfolio analysis matrix depicting the sample structure by number of transactions.

Source: Own elaboration.

Figure 4. Real estate portfolio analysis matrix depicting the value structure of the sampled transactions.

Source: Own elaboration.

Figure 5. Real estate portfolio analysis matrix depicting the number of transactions with assets classified as ‘core’ by the panel of experts.

Source: Own elaboration.

Figure 6. Real estate portfolio analysis matrix depicting the value of transactions with assets classified as ‘core’ by the panel of experts.

Source: Own elaboration.

Figure 7. Real estate portfolio analysis matrix depicting the number of transactions with assets classified as ‘value-added’ by the panel of experts.

Source: Own elaboration.

Figure 8. Real estate portfolio analysis matrix depicting the value of transactions with assets classified as ‘value-added’ by the panel of experts.

Source: Own elaboration.

Figure 9. Real estate portfolio analysis matrix depicting the number of transactions with assets classified as ‘opportunistic’ by the panel of experts.

Source: Own elaboration.

Figure 10. Real estate portfolio analysis matrix depicting the value of transactions with assets classified as ‘opportunistic’ by the panel of experts.

Source: Own elaboration.

5. Target users and potential applications

As the real estate market expands, so does the diversity of investment vehicles and number of potential users of REPO-M. However, applications of REPO-M may vary depending on the strategic approach of the stakeholders. In many instances, evaluation of real estate investments (especially speculative investments) may require a significant level of specialisation and expertise. In general, however, we argue that the application of REPO-M is not constrained to a particular user type. Yet, investment decisions made by relying on REPO-M may vary depending on the business environment, tax regime, legal and regulatory constraints, and political or societal considerations. The design of the proposed analytical framework generally favours its application by the less specialised or otherwise more diversified investors.

By ‘specialised investors’, we refer to corporate entities or individuals for whom real estate investments constitute a core business activity. They may be long-term capital investors or developers who take risks associated with the initial commercialisation of the project. In contrast, non-specialised property owners include holders of real estate assets whose core business activities are not associated with real estate.

Large institutional real estate investors, such as life insurance companies and pension funds, may exhibit a tendency to diversify their real estate portfolios by property type. Diversification is shown to potentially enhance portfolio efficiency (Leone & Ravishankar, Citation2018) and increase returns (Moss et al., Citation2017). The need to exploit the benefits of diversification by exploring a wider range of alternative investment options makes institutional real estate investors the key target users of the proposed analytical technique.

In contrast, real estate investment trusts (REITs) tend to be more specialised and are therefore less likely to seek portfolio diversification (Ro & Ziobrowski, Citation2012). The FTSE EPRA/NAREIT Developed Sector Indices published by FTSE Russel demonstrate that 72% of all listed REITs focus on one property type, such as industrial, industrial/office mixed, office, residential, retail, self-storage, healthcare, and lodging/resorts.

Regardless of their long-term strategy, both institutional capital investors and REITs are likely to engage in capital recycling by channelling resources from the older to the newer assets, which generates lower maintenance costs and have higher cash flow generating potential. This investment approach favours the application of REPO-M as an aid for managers in tracking the balance between risk and return on the real estate portfolio.

REPO-M may also be applied to identify the highest and best use of underperforming assets or assets approaching the end of their commercial life cycle. This application may be especially attractive to capital investors whose core activity has switched from management to development of real estate assets due to shortage of acquisition opportunities. Their development activities include new construction on raw land or redevelopment/expansion of properties already in the portfolio with the aim of maximising their value.

REPO-M may also be useful to companies that own real estate but are not specialised investors. These may include industrial companies owning manufacturing/storage facilities or using their properties as a freehold means of production. REPO-M complemented with conventional valuation methods should help such firms manage their real estate portfolios and identify opportunities of divestment whenever their assets start underperforming. An anecdotal example would be of a telecommunication company that, over the years, accumulated various types of properties hosting network installations. With technological advancements, the properties became redundant. The company initiated the disposal of numerous properties scattered across the country with value potential spread across different sectors. In this case, the application of REPO-M should allow effective identification of prospective buyers, thereby potentially maximising sales revenue. As the freehold is expected to gain popularity following changes to the International Financial Reporting Standards and Generally Accepted Accounting Principles, we believe that REPO-M may prove especially useful for this category of users.

6. Concluding remarks

This paper presents a new approach for the assessment of commercial real estate assets based on the two-dimensional growth-share matrix. The paper clearly explains the steps necessary to assess a portfolio of real estate assets from the perspective of various real-estate investors. The described approach could be used in all segments of the real estate market, provided that the assessment criteria are tailored to the property’s type and characteristics. One should be aware of the model’s basic form limitations. The asset appraisal was conducted with repeated expert assessment (Delphi method). Therefore, the distinction between core, value-added, and opportunistic assets may appear highly subjective. At the same time, the specificity of the real estate market, imperfection of the information flow, and prevalence of non-specialised investors allow us to advocate expert appraisal as a valid alternative for purely quantitative analysis. Qualitative assessment allows the consideration of complex interrelations between a plethora of legal, economic, and engineering factors to arrive at a compound score reflecting the property’s potential to generate stable cash flows and accrue value over the holding period. The basic property parameters chosen for REPO-M have been shown to be significant predictors of a property’s classification as core, value-added, or opportunistic.

Due to its novelty, the concept of the proposed approach has not yet been explored well. Therefore, only general principles and applicability have been outlined in the paper. Nevertheless, this paper opens the possibility for further in-depth studies in this field. It is worth focusing on the development of multiscoring assessment tools similar to that proposed in the GE/McKinsey matrices. Developing extensive lists of evaluation criteria tailored to the specific market segment may constitute another interesting direction for future research.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Amatulli, C., Caputo, T., & Guido, G. (2011). Strategic analysis through the general electric/mcKinsey matrix: An application to the italian fashion industry. International Journal of Business and Management, 6(5),61–75.

- Amédée-Manesme, C., Barthélémy, F., & Prigent, J. (2016). Real estate investment: Market volatility and optimal holding period under risk aversion. Economic Modelling, 58, 543–555. doi: 10.1016/j.econmod.2015.10.033

- Armstrong, S., & Brodie, R. (1994). Effects of portfolio planning methods on decision making: Experimental results. International Journal of Research in Marketing, 11(1), 73–84. doi: 10.1016/0167-8116(94)90035-3

- Baum, A. (2015). Real Estate Investment: A Strategic Approach (3rd ed.). Oxford: Routledge.

- Berrens, R., & McKee, M. (2004). What price nondisclosure? the effects of nondisclosure of real estate sales prices. Social Science Quarterly, 85(2), 509–520. doi: 10.1111/j.0038-4941.2004.08502017.x

- Brooks, C., & Tsolakos, S. (2000). Forecasting Models of Retail Rents. Environment and Planning A: Economy and Space, 32(10), 1825–1839.

- Brzezicka, J., Wisniewski, R., & Figurska, M. (2018). Disequilibrium in the real estate market: Evidence from poland. Land Use Policy, 78, 515–531. doi: 10.1016/j.landusepol.2018.06.013

- Buitelaar, E. (2007). The Cost of Land Use Decisions; applying transaction cost economics to planning & development. Oxford/Malden/Carlton: Blackwell Publishing.

- Cheng, P., Lin, Z., & Liu, Y. (2010). Illiquidity, transaction cost, and optimal holding period for real estate: Theory and application. Journal of Housing Economics, 19(2), 109–118. doi: 10.1016/j.jhe.2010.03.002

- De Witt, D. (1996). Real estate portfolio management practices of pension funds and insurance companies in the netherlands: A survey. Journal of Real Estate Research, 11(2), 131–148.

- Dipasquale, D., & Wheaton, W. (1996). Urban economics and real estate markets. Englewood Cliffs: Prentice Hall.

- Eichholtz, P. (1996). Does international diversification work better for real estate than for stocks and bonds?. Financial Analysts Journal, 52(1), 56–62. doi: 10.2469/faj.v52.n1.1967

- Evans, A. (1995). The property market: Ninety percent efficient?. Urban Studies, 32(1), 5–30. doi: 10.1080/00420989550013194

- Garmaise, M., & Moskowitz, T. (2004). Confronting information asymmetries: Evidence from real estate markets. Review of Financial Studies, 17(2), 405–437. doi: 10.1093/rfs/hhg037

- Graham, M., & Bible, D. (1992). Classifications for commercial real estate. The Appraisal Journal, 60(2), 237–246.

- Hastings, A., & Nordby, H. (2007). Benefits of global diversification on a real estate portfolio. The Journal of Portfolio Management, 33(5), 53–62. doi: 10.3905/jpm.2007.698905

- Ionescu, F. (2011). Boston consulting group II – a business portfolio analysis matrix. International Journal of Economic Practices and Theories, 1, 2247– 7225.

- Jackson, C., & White, M. (2005). Challenging traditional real estate market classifications for investment diversification. Journal of Real Estate Portfolio Management, 11(3), 307–321.

- Krühler, M., Nippa, M., Pidun, U., & Rubner, H. (2011). Corporate portfolio management: Theory and practice. Journal of Applied Corporate Finance, 23(1), 63–76. doi: 10.1111/j.1745-6622.2011.00315.x

- Kumar, A. (2012). Nestle india – on BCG matrix. Research Expo International Multidisciplinary Research Journal, 2(2), 2250– 1630.

- Kummerow, M., & Lun, J. (2005). Information and communication technology in the real estate industry: Productivity, industry structure and market efficiency. Telecommunications Policy, 29(2-3), 173–190. doi: 10.1016/j.telpol.2004.12.003

- Lee, S., & Devaney, S. (2007). The changing importance of sector and regional factors in real estate returns: 1987–2002. Journal of Property Research, 24(1), 55–69. doi: 10.1080/09599910701297671

- Leone, V., & Ravishankar, G. (2018). Frontiers of commercial real estate portfolio performance: Are sector-region-efficient diversification strategies a myth or reality?. Journal of Property Research, 35(2), 95–116. doi: 10.1080/09599916.2017.1410851

- Louargand, M. (1992). A survey of pension fund real estate portfolio risk management practices. Journal of Real Estate Research, 7(4), 361–373.

- Lyons, R. (2015). East, west, boom and bust: The spread of house prices and rents in ireland, 2007–2012. Journal of Property Research, 32(1), 77–101. doi: 10.1080/09599916.2013.870922

- McDonald, L., & Stiver, B. (2004). Institutional Real Estate – Investment Style Categories. New York, USA: CRA RogersCasey LLC.

- Moss, A., Clare, A., Thomas, S., & Seaton, J. (2017). Can sector specific REIT strategies outperform a diversified benchmark?. Journal of European Real Estate Research, 10(3), 366–383. doi:10.1108/JERER-11-2016-0042

- Nelson, T., & Nelson, S. (2003). Regional models for portfolio diversification. Journal of Real Estate Portfolio Management, 9(1), 71–88.

- Ooi, J. (2007). The handbook of commercial real estate investing. Journal of Property Investment & Finance, 25(2), 212–213. doi: 10.1108/14635780710733870

- Renigier-Bilozor, M., Wisniewski, R., Kaklauskas, A., & Bilozor, A. (2014). Rating methodology for real estate markets - poland case study. International Journal of Strategic Property Management, 18(2), 198. doi: 10.3846/1648715X.2014.927401

- Ro, S., & Ziobrowski, A. (2012). Wealth effects of REIT property-type focus changes: Evidence from property transactions and joint ventures. Journal of Property Research, 29(3), 177–199. doi: 10.1080/09599916.2012.703222

- Sehgal, S., Upreti, M., Pandey, P., & Bhatia, A. (2015). Real estate investment selection and empirical analysis of property prices: Study of select residential projects in gurgaon, india. International Real Estate Review, 18(4), 523– 566.

- Shilling, J., & Wurtzebach, C. (2012). Is value-added and opportunisitc real estate investing beneficial? if so, why?. Journal of Real Estate Finance and Economics, 34(4), 429–462.

- Shilton, L., & Tandy, J. (1993). The information precision of CBD office vacancy rates. Journal of Real Estate Research, 8(3), 421–444.

- Shuv-Ami, A. (2009). Adjusting the BCG Matrix for the Recession. Proceedings of the ANZMAC Conference in Melbourne.

- Sivitanidou, R., & Sivitanides, P. (1999). Office capitalization rates: Real estate and capital market influences. The Journal of Real Estate Finance and Economics, 18(3), 297–322. doi: 10.1023/A:1007780917146

- Trippi, R. (1989). A decision support system for real estate investment portfolio management. Information & Management, 16(1), 47–54. doi: 10.1016/0378-7206(89)90026-8

- Webb, J. (1984). Real estate investment acquisition rules for life insurance companies and pension funds: A survey. Real Estate Economics, 12(4), 495–520. doi: 10.1111/1540-6229.00335

- Winona, V., & Wandebori, H. (2012). Portfolio strategy of pangeran group using BCG matrix. Journal of Business and Management, 1(3), 170–176.