?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The paper examines the impact of terrorism on economic growth in Pakistan. Channel variables, such as foreign direct investment (FDI), domestic investment, and government spending, through which terrorism influences economic growth, are identified. For empirical analysis, annual data for the period 1972–2014 are used, and a structural model is estimated using the generalised method of moments (GMM) estimation approach. The results reveal that (1) the impact of terrorism on FDI and domestic investment is significantly negative, whereas the impact on government spending is significantly positive and (2) the net effect of terrorism on economic growth is negative. One per cent increase in terrorism reduces FDI by 0.104 per cent, domestic investment by 0.039 per cent and economic growth by 0.002 per cent. To increase economic growth more resources must be allocated to improve law and order. To attract foreign investment, complementary domestic investment must be increased.

1. Introduction

Terrorism is a complex phenomenon without a single agreed upon definition because many authors have defined the term terrorism based on their own understanding of it. The global terrorism database (GTD) defines a terrorist attack as ‘the threatened or actual use of illegal force and violence by a non‐state actor to attain a political, economic, religious, or social goal through fear, coercion, or intimidation.ʼ The attacks on the Twin Towers on September 11, 2001 (9/11), established that terrorism had reached a new dimension. Its roots are as much Middle Eastern as they are European and as much religious as they are secular.

The link between peace and economic growth is indispensable because economic development cannot occur without peace, and peace and security without growth may not be sustainable. Terrorism has both a direct and indirect effect on economic growth. Accumulations of physical and human capital are the main determinants of economic growth. Terrorism, conflicts and violence destroy both physical and human capital and undermine the socio-political institutions that positively affect economic growth. A country with a high level of violence loses the confidence of investors domestically and globally, which decreases domestic and foreign investments. Further, both human and financial resources shift abroad due to terrorist activities, which adversely affect economic growth. Countries affected by terrorism are allocating a considerable amount of financial and human resources to overcome terrorism and are spending less on economic and social infrastructure, which are imperative sources of human and physical capital accumulation. Terrorism is adversely affecting economic growth in these countries.

There are several reasons for terrorism in Pakistan, which include among others, ethnicity, illiteracy, income inequality, inflation, high population growth, high unemployment, political instability, poverty, and injustice (Ismail & Amjad, Citation2014; Khan, Estrada, & Yusof, Citation2016; Syed, Saeed, & Martin, Citation2015). In Pakistan, terrorism primarily increased after 9/11, when Pakistan began playing its role as a front line state against terrorism. Both internal and external forces are promoting terrorism in Pakistan. These terrorist activities have negatively affected economic growth in Pakistan. Some studies have been conducted in Pakistan and have shown that terrorism has deteriorated economic growth in the country (Hyder, Akram, & Padda, Citation2015; Khan et al., Citation2016; Khan & Yusof, Citation2017; Mehmood, Citation2014; Shahbaz et al., Citation2013). But these studies have explored the direct effect of terrorism on economic growth. No study to date has been conducted to investigate the indirect effect of terrorism on economic growth. This study tries to fill this gap using data for the period 1972–2014. Thus, the objective of this study is to examine both direct and indirect impacts of terrorism on economic growth in Pakistan.

The rest of the paper is organised as follows. Section 2 provides literature review. Section 3 describes the economic cost of terrorism in Pakistan. Section 4 discusses the theoretical framework. Section 5 provides the estimated results. The final section concludes the paper and offers policy implications.

2. Literature review

The empirical literature has shown that terrorism is harmful to economic growth (Blomberg, Hess, & Orphanides, Citation2004, Blomberg, Broussard, & Hess, Citation2011; Crain & Crain, Citation2006; Mirza & Verdier, Citation2008; Naor, Citation2006; Tavares, Citation2004; Virgo, Citation2001). Gaibulloev and Sandler (Citation2009) illustrate that transnational terrorist attacks seriously limit economic growth. Aslam, Rafique, Salman, Kang, and Mohti (Citation2018) demonstrate that terrorism has adversely affected Asian stock markets. According to Barth, Li, McCarthy, Phumiwasana, and Yago (Citation2006), terrorism can generate inefficient resource allocation and thus impedes output growth and capital formation. Gupta, Clements, Bhattacharya, and Chakravarti (Citation2004) and Ocal and Yildirim (Citation2010) postulate that terrorist activities are important reasons for low economic growth in less developed countries. In turn, Meierrieks and Gries (Citation2012) document that there is no link between terrorism activities and output growth. Using data for 115 countries for the period 2000 to 2015, Çinar (Citation2017) has found that terrorism has negatively affected the economic growth of the countries, especially in low-income countries. The study has found that terrorism has affected low-income countries about three times more than high-income countries. Choi (Citation2015) has investigated the impact of economic growth on terrorism using data for 127 countries for 1970 to 2007. It is found that countries with high industrial growth are less likely to experience internal and external terrorism.

In Pakistan, some empirical studies are available, but they have investigated the direct impact of terrorism on economic growth and concluded that terrorism has deteriorated economic growth in Pakistan (Hyder et al., Citation2015; Khan et al., Citation2016; Khan & Yusof, Citation2017; Mehmood, Citation2014; Shahbaz et al., Citation2013). Mubashra and Shafi (Citation2018) have shown that counter-terrorism activities have short- and long-run effects on economic growth in Pakistan. In Pakistan, no study to date has analysed the indirect effect of terrorism on economic growth. The present study will try to fill this gap. The objective of the study is to explore the direct and indirect effects of terrorism on economic growth in Pakistan. To explore the indirect effect of terrorism on economic growth some channel variables are identified, and a macro-econometric model is estimated using standard econometric techniques.

The literature has identified various channel variables through which terrorism is expected to affect economic growth (Eckstein & Tsiddon, Citation2004; Frey, Luechinger, & Stutzer, Citation2007; Khan et al., Citation2016; Mirza & Verdier, Citation2008; Sandler & Enders, 2008). For instance, terrorism impedes economic growth by damaging infrastructure, foreign trade, foreign investment, domestic savings, the currency exchange rate, tourism, and domestic capital formation, and by increasing inflation, brain drain, capital flight, debt burden, and government expenditure, among others. However, to explore the indirect effect of terrorism on output growth, we use three channel variables, FDI, domestic investment and government expenditure. We have selected these channel variables because FDI has significantly decreased in Pakistan due to terrorism and travel bans issued by Western countries to their entrepreneurs (Khan et al., Citation2016). In 2005, the FDI (net) inflow was 3.66 per cent of GDP but decreased to 0.36 per cent of GDP in 2015. Terrorism has also destroyed capital accumulation, which is the main input of production. In 2005, capital formation was 17.46 per cent of GDP but decreased to 13.51 per cent of GDP in 2015. It has decreased domestic output, and therefore, it has badly affected economic growth. Further, to overcome terrorism, government expenditures have increased from 7.84 per cent of GDP in 2005 to 11.84 per cent of GDP in 2015. Thus, terrorism has significantly harmfully affected these three sectors of the economy, which has thwarted economic growth.

Terrorism reduces foreign investment because foreign investors can diversify their investment portfolio (Agrawal, Citation2011; Blomberg & Mody, Citation2005; Kang & Lee, Citation2007). Abadie and Gardeazabal (Citation2008) have also documented that terrorism reduces net foreign investment. Abadie and Gardeazabal (Citation2003) document the negative effect of terrorism on capital markets, which adversely affects foreign investment. The risks presented by terrorism elevate the costs of business activity because costly security measures and compensation decrease the returns on FDI. Bandyopadhyay, Sandler, and Younas (Citation2014) highlight that all forms of terrorism discourage FDI. Filer and Stanisic (Citation2016) document that terrorism reduces FDI and that, compared to portfolio investment or external debt, FDI is more susceptible to terrorism. According to Shahzad et al. (Citation2016), terrorism has a deteriorating effect on FDI in Pakistan. Similar to foreign investment, terrorism also negatively influences domestic investment (Blomberg, Hess, & Orphanides, Citation2004; Eckstein & Tsiddon, Citation2004; Gaibulloev & Sandler, Citation2008; Llussá & Tavares, Citation2011; Persitz, Citation2007). Terrorism has crowded-in government expenditures because the government must spend more money to take appropriate security measures, which reduces output growth (Gaibulloev & Sandler, Citation2009).

3. Economic cost of terrorism in Pakistan

Terrorism in Pakistan mainly originated during the Soviet-Afghan war in 1980s. This conflict brought terrorist into south Asia in the name of Jihad. These Mujahideen were trained by American CIA and other western intelligence agencies to carry out insurgencies in Afghanistan and to fight a proxy war against Soviet forces in Afghanistan. Mostly these Mujahideen were not disarmed after the war ended in Afghanistan. Some of these Mujahideen found safe places in tribal areas of Pakistan near the Pakistan-Afghan border. After the event of 9/11 both internal and external funded terrorists started terrorism activities in Pakistan in the name of Islam as Pakistan was playing the role of a front line state against terrorism.

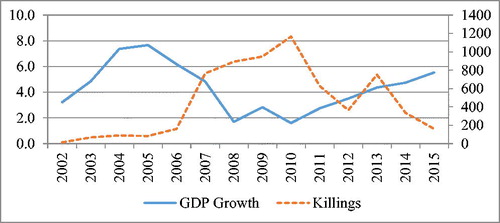

These terrorism activities after the event of 9/11 have adversely affected the economy of Pakistan. First, Pakistan observed an immediate flood of Afghan refugees, which spilled terrorism into Pakistan. Second, the Indian insurgency in Pakistan, particularly in Balochistan province, through Afghanistan has also increased terrorist activities because terrorists obtain financial and military support from India. Terrorism activities have adversely affected economic growth in Pakistan. shows GDP growth and deaths by suicide attacks in Pakistan. clearly indicates an inverse relationship between economic growth and terrorist attacks in Pakistan, i.e., when terrorism is low, economic growth is high, and when terrorism is high, economic growth is low. To overcome terrorism, a significant share of human and financial resources have been allocated for security purposes.

Figure 1. GDP growth and deaths by suicide attacks in Pakistan (2002–2015).

In the last 17 fiscal years since the event of 9/11, Pakistan’s economy has suffered a direct and indirect cost linked to terrorist activities of almost $126.79 billion, which is equal to Rs. 10762.14 billion (see ). Further, normal economic and trading activities have also been disrupted, which has increased the cost of doing business. Terrorism has also adversely affected Pakistan’s international trade. As a result, Pakistan has lost its market share and therefore remains unable to achieve its targeted growth rates. provides the loss to Pakistan’s economy due to terrorist attacks by sector during the fiscal years 2014–15 and 2015–16. It is evident from the table that foreign investment, tax collection and exports have been badly affected due to terrorism. Other than financial and economic losses, Pakistan has also suffered human capital loss. Over last 14 years from 2003 to 2016, 21,485 civilian and 6660 security forces personnel have lost their lives in terrorist attacks in Pakistan (see ).

Table 1. Direct and indirect cost of terrorism (2002–2014).

Table 2. Losses by sector due to terrorist attacks.

Table 3. Fatalities in terrorist violence in Pakistan (2003–2016).

To overcome the threat of terrorism, the government of Pakistan launched a military operation (Zarb-e-Azb) against terrorists without any discrimination in its territory near the Pakistan-Afghan border in June 2014. Subsequently, in December 2014, the government of Pakistan also began the National Action Plan (NAP) to take preventive measures against terrorism. Both the military operation and the NAP have remained successful and have improved security conditions in the country. This improvement has formed a suitable atmosphere for business and investment in the country and has decreased the losses to the economy. However, Pakistan needs to increase productive capacity by restoring damaged infrastructure and to adopt a favorable investment atmosphere. Further, the stability in neighbouring Afghanistan is fundamental to completely revitalise Pakistan’s economy and to sustain stability in the system.

4. Theoretical framework

Terrorism has both direct and indirect effects on economic growth. Terrorism impedes economic growth directly by damaging infrastructure, incurring a loss of human capital, reducing school enrolment, reducing short-run commerce, causing internally displaced persons (IDPs), and reallocating resources, among others. Terrorism also thwarts economic growth indirectly by affecting macroeconomic variables, e.g., by reducing FDI, lessening domestic investment, increasing inflation, increasing non-development government expenditures (law and order), damaging stock markets, and increasing unemployment, among others. Sandler and Enders (Citation2008), Mirza and Verdier (Citation2008), Frey et al. (Citation2007), Eckstein and Tsiddon (Citation2004) and Collier (1999) have explained the channels through which terrorism impedes economic growth. Based on theory, we take three important macroeconomic variables to find the indirect effect of terrorism on output growth. These variables include FDI, domestic investment and government spending because, in Pakistan, terrorism has highly affected these sectors of the economy.

4.1. Effect of terrorism on foreign direct investment

Terrorism affects FDI in many ways. Terrorism increases insecurity and uncertainty in the country, which causes a loss of confidence in foreign investors, causing them to divert their resources from the host country to other, peaceful countries (Abadie & Gardeazabal, Citation2003, Abadie & Gardeazabal, Citation2008; Agrawal, Citation2011; Blomberg & Mody, Citation2005; Enders & Sandler, Citation1996; Kang & Lee, Citation2007; Kinyanjui, Citation2014). Terrorism also makes foreign investors more concerned about their expected returns from their investment. If foreign investors do not see any increase in their expected returns in the presence of high levels of terrorism, then they will shift their resources from the host country to other, safe countries. An uncertain environment makes an investor to deem it an unproductive investment since costly security measures decrease the returns on FDI. Terrorism also damages local infrastructure such as roads, bridges, and telecommunications. It discourages foreign investment by increasing the cost of doing business. Bandyopadhyay et al. (Citation2014) document that all forms of terrorism discourage FDI. Filer and Stanisic (Citation2016) document that terrorism reduces FDI and that, in comparison to portfolio investments and external debt, FDI is more susceptible to terrorism. Thus, foreign investment decreases with the increase in terrorism in the host country.

4.2. Effect of terrorism on domestic investment

Domestic investment is also an important channel through which terrorism affects output growth. Similar to foreign investment, terrorism also decreases domestic investment because it becomes difficult for domestic investors to invest in a terror-stricken environment. Further, public investment is also severely damaged because government projects such as the construction of roads, highways, canals, dams, bridges, highway, hospitals, and schools are also brought to an end in the presence of terrorist activities (Eckstein & Tsiddon, Citation2004; Llussá & Tavares, Citation2011; Persitz, Citation2007). Moreover, terrorism severely damages investment in vulnerable sectors of the economy such as tourism. Terrorist activities induce public expenditures on defence and security issues, which can crowd out public and private investments (Blomberg, Hess, & Orphanides, Citation2004; Gaibulloev & Sandler, Citation2008).

4.3. Effect of terrorism on government spending

Terrorism increases government expenditure because the government must spend more on security issues to maintain law and order in the country (Blomberg, Hess, & Orphanides, Citation2004). This reallocation of government resources decreases expenditure on social sector development such as health and education (Collier et al., Citation2003). It will decrease economic growth. In turn, high government expenditure on security offsets terrorism by improving the law and order situation, which will increase both domestic and foreign investments. It will increase economic growth.

4.4. Recapitulation

This study investigates both the direct and indirect effects of terrorism on economic growth in Pakistan. To observe the direct effect of terrorism on growth, we estimate the following reduced form equation:

(1)

(1)

To examine the indirect effect of terrorism on economic growth, we use a simultaneous equation model containing four equations, including an economic growth rate and three channel variable equations, i.e., FDI, domestic investment and government spending. The mathematical representation of the structural model is as follows:

(2)

(2)

(3)

(3)

(4)

(4)

(5)

(5)

All variables, except growth (), are expressed in natural log form, and the variables are defined as follows:

= Real GDP growth rate

= Foreign direct investment

= Domestic investment

= Government spending

= Human capital index

= Terrorism

= Income level

= Trade openness

= Exchange rate

= Domestic credit to private sector

= Foreign debt

= Foreign aid

provides the summary of the expected effect of terrorism on the channel variables and the effect of the channel variables on economic growth.

Table 4. Effect of terrorism on economic growth.

5. Data overview and estimation of the model

5.1. Data overview

For empirical analysis, annual data is used for the period 1972–2014. Terrorism is the total number of deaths, and its data is taken from the Global Terrorism Database (GTD) and the South Asia Terrorism Portal (SATP). Economic growth is the real GDP growth rate. FDI, domestic investment, government consumption, domestic credit to the private sector, foreign debt, and foreign aid are taken as a percentage of GDP. Trade openness is measured as exports plus imports as a percentage of GDP. The exchange rate is defined as domestic currency per unit of foreign currency. The data for these variables is taken from International Financial Statistics (IFS), World Development Indicators (WDI) and Pakistan Economic Surveys. Human capital is measured by human capital per person, which is related to the average years of schooling and the return on education, and the data is collected from the Penn World Table (PWT). The data for internal and external conflicts is collected from International Country Risk Guide (ICRG). The values of both internal conflict and external conflict scores fall between 0 (very high risk) and 12 (very low risk).

provides the descriptive statistics of the main variables used in this study. All three measures of dispersion, i.e., standard deviation, quartile deviation and inter-quartile range, indicate that terrorism has the highest deviation. Domestic investment, government spending, and external and internal conflicts also have high deviations. The mean value of terrorism shows that, in Pakistan, 135 persons have been killed on average from 1972 to 2014 and that this killing ranges from 1 to 2872 persons. A similar interpretation holds for all other variables.

Table 5. Descriptive statistics of the variables.

5.2. Estimation of a single equation model

To study the direct effect of terrorism on economic growth, EquationEquation (1)(1)

(1) is estimated. An endogeneity problem is likely to arise in the model due to reverse causality between the explanatory variables. To correct the endogeneity issue, the generalised method of moments (GMM) estimation technique is applied to estimate the model. Lagged values of the variables are taken as instruments. The appendix provides the technical details of the GMM method. provides the estimated results. The results in column 1 reveal that terrorism has a negative effect on economic growth and that the coefficient is statistically significant. Economically speaking, a one per cent increase in terrorism will decrease economic growth by 0.002 per cent. This result is in accordance with the existing empirical literature showing that terrorism decreases economic growth (Crain & Crain, Citation2006; Mirza & Verdier, Citation2008; Naor, Citation2006). Other variables have theoretically expected effect on economic growth. Human capital has significant positive effect on growth. A one per cent increase in human capital will increase output growth by 1.299 per cent. Both domestic and foreign investments have statistically significant positive effects on growth. A one per cent increase in domestic (foreign) investment will increase economic growth by 0.072 (0.009) per cent. Economic growth also increases with the increase in government spending as the coefficient of government spending is positive and statistically significant. A one per cent increase in government spending will increase economic growth by 0.074 per cent. The intuition is that government expenditures on security measures improve law and order condition in the country, which boosts economic activity in the country.

Table 6. Effect of terrorism and post-9/11 dummy on economic growth.

In Pakistan, terrorist activities mainly began after the 9/11 attack. For robustness check, we re-estimate our model by using a post-9/11 dummy to examine the impact of terrorism on output growth in Pakistan. The correlation coefficient between the post-9/11 dummy variable and the terrorism variable is 0.65, which is statistically significant at the one per cent level of significance using t-statistics. This finding means that we can use the post-9/11 dummy as a proxy for the terrorism variable. The estimated results are reported in column 2 of , which shows that, similar to terrorism, the post-9/11 dummy has a statistically significant negative effect on economic growth. The estimated value of the coefficient implies that terrorism after the event of 9/11 has decreased economic growth by 0.018. The magnitude of the post-9/11 dummy coefficient is higher than the terrorism variable, which indicates that terrorism after the event of 9/11 has undermined economic growth more than terrorism in column 1. All other variables maintain their signs and significance level.

High R-squared and adjusted R-squared values indicate that the model fits the data well. The R-squared (adjusted R-squared) value implies that 99.1% (98.9%) of the variation in the dependent variable is explained by all independent variables in column 1 and by 99.5% (99.4%) in column 2. The autoregressive (AR) term is used in the model to overcome the problem of autocorrelation. In both equations, Durbin-Watson (DW) statistics are close to 2, it implies that autocorrelation problem has been removed. The high p-values of the J-statistics imply that the instruments used are valid.

5.3. Robustness analysis

The literature has shown that internal and external conflicts affect economic growth (Cervellati & Sunde, Citation2011; Collier et al., Citation2003; Ghobarah, Huth, & Russett, Citation2003). The empirical findings have also shown that external and internal conflicts can have substantial economic ramifications that result in reduced economic growth in a conflict-ridden country (Collier et al., Citation2003; Collier & Hoeffler, Citation2004; Collier & Sambanis, Citation2002; Fielding, Citation2003) and its neighboring countries ( Murdoch & Sandler, Citation2002, Murdoch & Sandler, Citation2004 ). Therefore, for robustness analysis, we use internal and external conflicts as proxy variables for terrorism and estimate their effects on economic growth. The estimated results are given in . Column 1 explains the results for external conflict, whereas column 2 explains the results for internal conflict. Both external and internal conflicts have statistically significant negative impact on economic growth. A one per cent increase in external (internal) conflict will decrease economic growth by 0.048 (0.015) per cent. After comparing the two effects, it is evident that external conflict undermines economic growth more than internal conflict. Human capital, domestic and foreign investments, and government spending have statistically significant positive effect on economic growth, as was theoretically expected. The estimated results are in accordance with the existing literature (Eckstein & Tsiddon, Citation2004; Frey et al., Citation2007; Sandler & Enders, Citation2008).

Table 7. Effect of external and internal conflicts on economic growth.

5.4. Estimation of the structural equations model

To investigate the indirect effect of terrorism on economic growth, we estimate a structural growth model represented by the system of EquationEquations (2–5), which comprises one growth equation and three channel variable equations, i.e., FDI, domestic investment and government expenditures. Simultaneous equation bias is likely to occur in our equations. Therefore, to remove this bias problem, the model is estimated using GMM technique. provides the estimated results of the structural model. The explanatory power of the equation, represented by the R-squared, is above 70 per cent. The autoregressive (AR) process is used to eliminate autocorrelation problem. The Durbin-Watson (DW) values are close to 2, which show that autocorrelation problem does not exist in the model. The high p-value of the J-statistics shows that the instruments used are valid.

Table 8. System estimates for the structural growth model.

The results of growth equation closely resemble the existing findings in the empirical growth literature (see, e.g., Barro, Citation1990, Citation1991; Barro & Sala-i-Martin, Citation2004; Levine & Renelt, Citation1992). All channel variables, i.e., FDI, domestic investment and government spending, have statistically significant positive effect on economic growth. Further, economic growth also increases with the increase in human capital, as the latter has statistically significant positive effect on economic growth. The magnitudes of the coefficients show that human capital increases economic growth more than any other variable. Our estimated results are in accordance with the prevailing literature (Abadie & Gardeazabal, Citation2003; Blomberg, Hess, & Orphanides, Citation2004, Blomberg, Hess, & Weerapana, Citation2004; Mirza & Verdier, Citation2008).

Terrorism has a significant negative effect on FDI. One per cent increase in terrorism decreases FDI by 0.086 per cent. These results are in accordance with previous studies (Bandyopadhyay et al., Citation2014; Fielding, Citation2004; Filer & Stanisic, Citation2016; Kang & Lee, Citation2007; Shahzad et al., Citation2016). Foreign investment increases with the increase in domestic income (GDP) because the coefficient on income is positive and statistically significant. A one per cent increase in domestic income increases FDI by 0.961 per cent. FDI appears to be a complement, rather than substitute for trade openness. Our findings support Singh and Jun (Citation1995) and Zakaria and Ahmed (Citation2013), who show that liberalised economies attract more FDI and promote its more efficient utilisation than closed economies. Foreign investment increases with the depreciation of the domestic currency because it will increase the return/profit of foreign investors. Thus, the depreciation of the local currency appears to be conducive to attract foreign investment. The statistically significant positive coefficient of the exchange rate variable implies that when the domestic currency depreciates by one per cent, foreign investment increases by 0.660 per cent. The effect of domestic investment on foreign investment is not only positive but also statistically significant, which implies that domestic investment complements foreign investment, i.e., foreign investment increases with the increase in domestic investment.

Similar to foreign investment, terrorism has a significant negative effect on domestic investment. A one per cent increase in terrorism will decrease domestic investment by 0.038 per cent. This result is also in accordance with the previous literature (Eckstein & Tsiddon, Citation2004; Llussá & Tavares, Citation2011; Persitz, Citation2007). In terms of magnitude, terrorism decreases foreign investment more than domestic investment, which means that foreign investment is more sensitive to terrorism than domestic investment. Moreover, as expected, a high level of domestic income appears to be conducive for domestic investment. It validates the ‘acceleration principle’ in which investment increases with the increase in income. The statistically significant positive coefficient of income shows that a one per cent increase in income will increase investment by 0.113 per cent. Investment increases when the local currency depreciates. When the domestic currency depreciates by one per cent, domestic investment increases by 0.583 per cent. This result is highly significant. In fact, depreciation of the domestic exchange rate renders exports less expensive, thereby favorably affecting domestic investment. The significant positive coefficient on foreign investment shows that it complements, rather than substitutes for, domestic investment. Finally, as was theoretically expected, domestic credit (to the private sector) has a positive effect on domestic investment. A one per cent increase in domestic credit will increase domestic investment by 0.230 per cent. This finding means that when the private sector has more credit, firms will invest more in business, which will increase investment in the country.

Terrorism has a positive impact on government consumption. The coefficient on terrorism is statistically significant, indicating that a one per cent increase in terrorist activities increases government spending by 0.039 per cent. This result supports the notion that terrorism increases government spending because the government has to take appropriate security measures (Nasir & Shahbaz, Citation2015). These results corroborate previous studies (Arunatilake, Jayasuriya, & Kelegama, Citation2001; Gaibulloev & Sandler, Citation2009; Gupta et al., Citation2004). Income has a positive impact on government spending because, when income increases, government revenues will also increase and, hence, government spending will increase. Trade openness positively affects government spending. This result substantiates the notion of Cameron (Citation1978) and Rodrik (1998) that public spending is higher in more trade liberalised countries because they are vulnerable to external shocks and the government reduces risk. Foreign aid also enables the government to increase its consumption. A one per cent increase in foreign aid will increase government spending by 0.163 per cent. However, high foreign debt decreases government expenditure in Pakistan. Both these variables are statistically significant.

summarises the channel effects of terrorism on economic growth. The impact of terrorism on each channel variable is presented in column-1, whereas the effect of each channel variable on economic growth is presented in column 2. Column 3 is the product of columns 1 and 2, which shows the indirect effect of terrorism on economic growth through the channel variables. Terrorism has statistically significant impact on economic growth through all three channel variables. Terrorism negatively affects growth by decreasing foreign and domestic investments, whereas it positively affects growth by increasing government spending. The indirect net effect of terrorism on economic growth is −0.002, which implies that when terrorism increases by one per cent, economic growth shrinks by 0.002 per cent. These results are in accordance with the previous literature (Abadie & Gardeazabal, Citation2003, Abadie & Gardeazabal, Citation2008; Bandyopadhyay et al., Citation2014; Blomberg, Hess, & Orphanides, Citation2004; Gaibulloev & Sandler, Citation2008). The results show that the indirect effect of terrorism on economic growth (0.002) is equal to the direct effect ().

Table 9. The contribution of effect of terrorism on GDP growth.

6. Conclusion

The paper empirically examines the effect of terrorism on economic growth in Pakistan, using data for the period 1972–2014. The results show that terrorism has a negative effect on output growth in Pakistan. The direct effect shows that a one per cent increase in terrorism will decrease output growth by 0.002 per cent. This result is robust when the post-9/11 dummy is used as a proxy variable for the terrorism variable. Further, when the external and internal conflict variables are used, the results remain the same, i.e., both external and internal conflicts have a negative effect on economic growth in Pakistan. To explore the indirect effect of terrorism on growth, three channel variables—FDI, domestic investment, and government consumption—have been identified. The results show that terrorism decreases both FDI and domestic investment, whereas it increases government spending, and these results are statistically significant. The results reveal that terrorism negatively affects growth through FDI and investment, whereas it positively affects growth through government consumption. The overall effect of terrorism on economic growth is negative. Thus, the indirect effect of terrorism on economic growth is the same as the direct effect.

This paper has some policy implications. The government is taking military action against terrorists in the country to remove internal conflict; however, the government should allocate some budgetary funds for socio-economic development in war-affected areas to remove the root causes of terrorism such as poverty, illiteracy, income inequality, unemployment, and injustice. Doing so will decrease terrorism by increasing the opportunity cost of terrorism (Frey & Luechinger, Citation2003) because military operations, which increase the material costs of terrorism, are not successful in the long run (Feridun & Shahbaz, Citation2010). The government should also formulate foreign policy to end external conflict with neighbouring countries. Further, the government should take appropriate steps at international levels to remove foreign-funded terrorism in Pakistan from neighbouring countries. Not only is terrorism adversely affecting Pakistan’s economy, but the bad image that Pakistan projects to the world is also hurting foreign investment in the country. The government should portray a soft image of the country to attract FDI. Further, the government should provide diversification opportunities to foreign investors with a lower terrorism risk, and a high return and compensation may be provided for high-risk projects. Since terrorism positively affects economic growth through government expenditures, more resources should be allocated to improve levels of law and order in the country because doing so is beneficial for economic growth.

The main limitation of the study is that it has used only three channel variables for the analysis. Some other channel variables like inflation rate, defence expenditure, etc. can also be used for analysis. This is left for future research. Future research can also be carried out using monthly and quarterly data and by formulating any terrorism index.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1. Each equation has some excluded variables, and therefore, the order condition for identification holds. The rank condition is also assumed to be satisfied in a model of this size

References

- Abadie, A., & Gardeazabal, J. (2003). The economic costs of conflict: A case study of the Basque Country. American Economic Review, 93(1), 113–132. doi: 10.1257/000282803321455188

- Abadie, A., & Gardeazabal, J. (2008). Terrorism and the world economy. European Economic Review, 52(1), 1–27. doi: 10.1016/j.euroecorev.2007.08.005

- Agrawal, S. (2011). The impact of terrorism on foreign direct investment: Which sectors are more vulnerable? CMC Senior Thesis Paper 124. https://scholarship.claremont.edu/cmc_theses/124.

- Arunatilake, N., Jayasuriya, S., & Kelegama, S. (2001). The economic cost of the war in Sri Lanka. World Development, 29(9), 1483–1500. doi: 10.1016/S0305-750X(01)00056-0

- Aslam, F., Rafique, A., Salman, A., Kang, H.-G., & Mohti, W. (2018). The impact of terrorism on financial markets: Evidence from asia. The Singapore Economic Review, 63(5), 1183–1204. doi: 10.1142/S0217590815501118

- Bandyopadhyay, S., Sandler, T., & Younas, J. (2014). Foreign direct investment, aid, and terrorism. Oxford Economic Papers, 66(1), 25–50. doi: 10.1093/oep/gpt026

- Barro, R. J. (1990). Government spending in a simple model of endogenous growth. Journal of Political Economy, 98(5, Part 2), s103–s125. doi: 10.1086/261726

- Barro, R. J. (1991). Economic growth in a cross section of countries. Quarterly Journal of Economics, 106(2), 407–433. doi: 10.2307/2937943

- Barro, R. J., & Sala-I-Martin, X. I. (2004). Economic growth. 2nd Edition, Massachusetts: MIT Press Cambridge.

- Barth, J. R., Li, T., McCarthy, D., Phumiwasana, T., & Yago, G. (2006). Economic impacts of global terrorism: From Munich to Bali. Research Report, Milken Institute.

- Blomberg, S. B., & Mody, A. (2005). How severely does violence deter international investment? Working Paper (01), Department of Economics, Claremont McKenna College.

- Blomberg, S. B., Broussard, N. H., & Hess, G. D. (2011). New wine in old wineskins? Growth, terrorism and the resource curse in Sub-Saharan Africa. European Journal of Political Economy, 27(Suppl. 1), S50–S63. doi: 10.1016/j.ejpoleco.2011.06.004

- Blomberg, S. B., Hess, G. D., & Orphanides, A. (2004). The macroeconomic consequences of terrorism. Journal of Monetary Economics, 51(5), 1007–1032. doi: 10.1016/j.jmoneco.2004.04.001

- Blomberg, S. B., Hess, G. D., & Weerapana, A. (2004). Economic conditions and terrorism. European Journal of Political Economy, 20(2), 463–478. doi: 10.1016/j.ejpoleco.2004.02.002

- Cameron, D. R. (1978). The expansion of the public economy: A comparative analysis. American Political Science Review, 72(4), 1243–1261. doi: 10.2307/1954537

- Cervellati, M., & Sunde, U. (2011). Democratization, violent social conflicts and growth. IZA Discussion Paper (5643),

- Choi, S.-W. (2015). Economic growth and terrorism: Domestic, international, and suicide. Oxford Economic Papers, 67(1), 157–181. doi: 10.1093/oep/gpu036

- Çinar, M. (2017). The effects of terrorism on economic growth: Panel data approach. Proceedings of Rijeka School of Economics, 35(1), 97–121.

- Collier, P. (1999). On the economic consequences of civil war. Oxford Economic Papers, 51(1), 168–183. doi: 10.1093/oep/51.1.168

- Collier, P., & Sambanis, N. (2002). Understanding civil war: A New Agenda. The Journal of Conflict Resolution, 46(1), 3–12. doi: 10.1177/0022002702046001001

- Collier, P., Elliott, V. L., Hegre, H., Hoeffler, A., Reynal-Querol, M., & Sambanis, N. (2003). Breaking the conflict trap: Civil war and development policy. Washington, DC: World Bank.

- Collier, P., & Hoeffler, A. (2004). Greed and grievance in civil War. Oxford Economic Papers, 56(4), 563–595. doi: 10.1093/oep/gpf064

- Crain, N. V., & Crain, W. M. (2006). Terrorized economies. Public Choice, 128(1-2), 317–349. doi: 10.1007/s11127-006-9056-6

- Eckstein, Z., & Tsiddon, D. (2004). Macroeconomic consequences of terror: Theory and the case of Israel. Journal of Monetary Economics, 51(5), 971–1002. doi: 10.1016/j.jmoneco.2004.05.001

- Enders, W., & Sandler, T. (1996). Terrorism and foreign direct investment in Spain and Greece. Kyklos, 49(3), 331–352. doi: 10.1111/j.1467-6435.1996.tb01400.x

- Feridun, M., & Shahbaz, M. (2010). Fighting terrorism: Are military measures effective? Empirical evidence from Turkey. Defence and Peace Economics, 21(2), 193–205. doi: 10.1080/10242690903568884

- Fielding, D. (2003). Investment, employment and political conflict in Northern Ireland. Oxford Economic Papers, 55(3), 512–535. doi: 10.1093/oep/55.3.512

- Fielding, D. (2004). How does violent conflict affect investment location decisions? Evidence from Israel during the Intifada. Journal of Peace Research, 41(4), 465–484. doi: 10.1177/0022343304044477

- Filer, R. K., & Stanisic, D. (2016). The effect of terrorist incidents on capital flows. Review of Development Economics, 20(2), 502–513. doi: 10.1111/rode.12246

- Frey, B. S., & Luechinger, S. (2003). Measuring Terrorism. Zurich IEER Working Paper No. 171. Available at SSRN: https://ssrn.com/abstract=468140 or http://dx.doi.org/10.2139/ssrn.468140.

- Frey, B. S., Luechinger, S., & Stutzer, A. (2007). Calculating tragedy: Assessing the costs of terrorism. Journal of Economic Surveys, 21(1), 1–24. doi: 10.1111/j.1467-6419.2007.00505.x

- Gaibulloev, K., & Sandler, T. (2008). Growth consequences of terrorism in Western Europe. Kyklos, 61(3), 411–424. doi: 10.1111/j.1467-6435.2008.00409.x

- Gaibulloev, K., & Sandler, T. (2009). The impact of terrorism and conflicts on growth in Asia. Economics & Politics, 21(3), 359–383. doi: 10.1111/j.1468-0343.2009.00347.x

- Ghobarah, H. A., Huth, P., & Russett, B. (2003). Civil wars kill and maim people - long after the shooting stops. American Political Science Review, 97(02), 189–202. doi: 10.1017/S0003055403000613

- Gupta, S., Clements, B., Bhattacharya, R., & Chakravarti, S. (2004). Fiscal consequences of armed conflict and terrorism in low and middle income countries. European Journal of Political Economy, 20(2), 403–421. doi: 10.1016/j.ejpoleco.2003.12.001

- Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica, 50(4), 1029–1054. doi: 10.2307/1912775

- Hyder, S., Akram, N., & Padda, I. U. (2015). Impact of terrorism on economic development in Pakistan. Pakistan Business Review, 16(4), 704–722.

- Ismail, A., & Amjad, S. (2014). Determinants of terrorism in Pakistan: An empirical investigation. Economic Modelling, 37, 320–331. doi: 10.1016/j.econmod.2013.11.012

- Kang, S. J., & Lee, H. S. (2007). Terrorism and FDI flows: Cross-country dynamic panel estimation. Journal of Economic Theory and Econometrics, 18(1), 57–77.

- Khan, A., & Yusof, Z. (2017). Terrorist Economic Impact Evaluation (TEIE) model: The case of Pakistan. Quality & Quantity, 51(3), 1381–1394. doi: 10.1007/s11135-016-0336-z

- Khan, A., Estrada, M. A. R., & Yusof, Z. (2016). How terrorism affects the economic performance? The case of Pakistan. Quality & Quantity, 50(2), 867–883. doi: 10.1007/s11135-015-0179-z

- Kinyanjui, S. (2014). The impact of terrorism on foreign direct investment in Kenya. International Journal of Business Administration, 5(3), 148–157. doi: 10.5430/ijba.v5n3p148

- Levine, R., & Renelt, D. (1992). A sensitivity analysis of cross-country growth regressions. American Economic Review, 82(4), 942–963.

- Llussá, F., & Tavares, J. (2011). Which terror at which cost? On the economic consequences of terrorist attacks. Economics Letters, 110(1), 52–55. doi: 10.1016/j.econlet.2010.09.011

- Mehmood, S. (2014). Terrorism and the macroeconomy: Evidence from Pakistan. Defence and Peace Economics, 25(5), 509–534. doi: 10.1080/10242694.2013.793529

- Meierrieks, D., & Gries, T. (2012). Economic performance and terrorist activity in Latin America. Defence and Peace Economics, 23(5), 447–470. doi: 10.1080/10242694.2012.656945

- Mirza, D., & Verdier, T. (2008). International trade, security and transnational terrorism: Theory and a survey of empirics. Journal of Comparative Economics, 36(2), 179–194. doi: 10.1016/j.jce.2007.11.005

- Mubashra, S., & Shafi, M. (2018). The impact of counter-terrorism effectiveness on economic growth of Pakistan: An econometric analysis. (MPRA Paper No. 84847).

- Murdoch, J. C., & Sandler, T. (2002). Economic growth, civil wars, and spatial spillovers. Journal of Conflict Resolution, 46(1), 91–110. doi: 10.1177/0022002702046001006

- Murdoch, J. C., & Sandler, T. (2004). Civil wars and economic growth: Spatial dispersion. American Journal of Political Science, 48(1), 138–151. doi: 10.2307/1519902

- Naor, Z. (2006). Untimely death, the value of certain lifetime and macroeconomic dynamics. Defence and Peace Economics, 17(4), 343–359. doi: 10.1080/10242690600688407

- Nasir, M., & Shahbaz, M. (2015). War on terror: Do military measures matter? empirical analysis of post 9/11 period in Pakistan. Quality & Quantity, 49(5), 1969–1984. doi: 10.1007/s11135-014-0084-x

- Ocal, N., & Yildirim, J. (2010). Regional effects of terrorism on economic growth in Turkey: A geographically weighted regression approach. Journal of Peace Research, 47(4), 477–489. doi: 10.1177/0022343310364576

- Persitz, D. (2007). The economic effects of terrorism: Counterfactual analysis of the case of Israel. Department of Economics, Tel Aviv University.

- Rodrik, D. (1998). Why do more open countries have larger governments. Journal of Political Economy, 106(5), 997–1032. doi: 10.1086/250038

- Sandler, T., & Enders, W. (2008). Economic consequences of terrorism in developed and developing countries: An overview. In Terrorism, economic development, and political openness. (pp. 17–47). New York, NY: Cambridge University Press. ISBN: 9780521887588. doi: 10.1017/CBO9780511754388.002

- Shahbaz, M., Shabbir, M. S., Malik, M. N., & Wolters, M. E. (2013). An analysis of a causal relationship between economic growth and terrorism in Pakistan. Economic Modelling, 35, 21–29. doi: 10.1016/j.econmod.2013.06.031

- Shahzad, S. J. H., Zakaria, M., Rehman, M. U., Ahmed, T., & Fida, B. A. (2016). Relationship between FDI, terrorism and economic growth in Pakistan: Pre and post 9/11 analysis. Social Indicators Research, 127(1), 179–194. doi: 10.1007/s11205-015-0950-5

- Singh, H., & Jun, K. W. (1995). Some new evidence on determinants of foreign direct investment in developing countries. (Policy Research Working Paper No. 1531). World Bank 1995.

- Syed, S. H., Saeed, L., & Martin, R. P. (2015). Causes and incentives for terrorism in Pakistan. Journal of Applied Security Research, 10(2), 181–206. doi: 10.1080/19361610.2015.1004606

- Tavares, J. (2004). The open society assesses its enemies: Shocks, disasters and terrorist attacks. Journal of Monetary Economics, 51(5), 1039–1070. doi: 10.1016/j.jmoneco.2004.04.009

- Virgo, J. M. (2001). Economic impact of the terrorist attacks of september 11, 2001. Atlantic Economic Journal, 29(4), 353–357. doi: 10.1007/BF02299323

- Zakaria, M., & Ahmed, E. (2013). Openness–growth nexus in Pakistan: A macro–econometric analysis. Argumenta Oeconomica, 30(1), 47–84.

AppendixGeneralised methods of moment (GMM)

The generalised method of moments (GMM) estimation technique was formalised by Hansen (Citation1982). Consider the following model:

where

is a vector of explanatory variables and

is a vector of the regression coefficients and

is the error term. The moment conditions are

a constant for all

is the key condition in estimating

In the presence of endogeneity,

but

where

is the vector of instruments that is correlated with

but not with the error term. If

is

is

matrices, and

then there are more instruments available than regressors, i.e., the equation is over-identified. The vector of the parameters

is estimated by minimising

where

is an

weighting matrix. If

is replaced, then

Thus, the optimal solution for is

Note that

and if

then higher weights will be given to moment conditions with lower variance. This leads to

Like Two Stage Least Square (2SLS), GMM is also an instrumental variable estimator, which selects parameter estimates such that the correlations between instruments and disturbances are close to zero. However, it is a step further to 2SLS estimators as it uses all moments by minimising their difference from zero. It also utilises variance-covariance matrix of all moments to account for heteroscedasticity and autocorrelation and gives more weight to that moment which possesses small variance. In this way GMM provides consistent and asymptotically efficient estimates.