?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to examine the influence of banks’ credit to SMEs on non-performing loans. Many studies find that access to financial sources has become an obstacle to the growth and sustainability of SMEs. This study uses theoretical and empirical approaches to support the study’s hypothesis. Data are presented for 15 banks in Palestine, covering the period 2006 to 2016.The study uses empirical techniques regarding to examine the relationship between the variables. Evidence shows that encouraging banks to lend more money to SMEs through the use of a guarantee fund could decrease their risk. Thus, enhancing credit to SMEs could improve the growth and sustainability of these firms. The study recommending policymakers and bank’s managers could develop their strategies according to SME’s needing. Therefore, enhancing the growth in these firms and reducing the bank’s risk. Furthermore, adopting the guarantee funds in developing countries could decrease the bank’s risk, thus lending more to SME. The value of this paper comes from the importance of SME in the economic growth and development sustainability. Therefore, there is a need to convince banks to enhance SME credit through a guarantee fund and that extending this type of credit would positively influence banks’ activities.

1. Introduction

Banks play a critical role in enhancing the sustainability of small- and medium-sized enterprises (SMEs) through offering financial services, technology, and business solutions (Berger & Udell, Citation2006; De la Torre, Pería, & Schmukler, Citation2010). Banks attract deposits and offer direct and indirect financial services, such as loans, mortgages, and other services, (Beck, Senbet, & Simbanegavi, Citation2015, Shihadeh, Hannon, Guan, Ul Haq, & Wang, Citation2018; Werner, Citation2016). Banks, as financial intermediation institutions, have the main targets of earning profits, maximising stockholder value and minimising risk (Pilloff, Citation1996; Shihadeh et al., Citation2018). Therefore, banks that aim to achieve these targets on the supply side of their financial services depend on providing banking services to companies, SMEs, and retails on the demand side (Shihadeh, Citation2018). Further, the main issue for these demand-side entities is the investment and trading process that takes place when they seek the services financial institutions offer which, therefore, reflect on a country’s economic and development sustainability.

Most large firms start out as small firms. SMEs constitute the majority of firms in an economy and create the newest jobs, thus making a vital contribution to employment regarding both the number employed and the employment rate (De la Torre et al., Citation2010; Kumar & Rao, Citation2015). Further, in emerging economies, SMEs in the formal economy contribute to around 40% of GDP and hire approximately 60% of the total work force, (World Bank, Citation2014). In Palestine, SMEs’ contribute to approximately 55% of GDP, and hire around 91% of the total labour force, (Wang & Shihadeh, Citation2015). In the MENA region, SMEs represent about 90% of total firms and hire around 30% of the labour force, (Nasr & Pearce, Citation2012). Furthermore, SMEs could help in poverty alleviation though employment, investment, and the market cycle, (Bauchet & Morduch, Citation2013). Therefore, encouraging the sustainability of SMEs, through enhancing their access to sources of finance is vital to supporting comprehensive economic sustainability, (Batrancea, Morar, Masca, Catalin, & Bechis, Citation2018).

Researchers, policymakers, and economists have examined the factors that influence SME performance and growth and, thus, their contribution to the economy. They find that access to financial sources poses the main obstacle to SME growth, (Duygan-Bump, Levkov, & Montoriol-Garriga, Citation2015; International Monetary Fund, Citation2014; Shinozaki, Citation2012, Gozzi & Schmukler, Citation2015; Wellalage & Locke, Citation2017); they also find that this obstacle comes from SMEs’ lack of adequate collateral; the absence of special financial services directed towards SMEs; rules and regulations that pose difficulties to SMEs, such as providing a legal definition of a firm and registering a firm, (Beck & Demirgüç-Kunt, Citation2006). Further, SMEs lack skilled management, technology, and employees with training and experience, limitations that reflect on their continuity, innovation, and growth. On the one hand, the above factors stand as barriers to the access of the financial sources that are necessary to the continuity and growth of SMEs, (Erdogan, Citation2018). On the other hand, banks consider SMEs as sources of financial risk. Meanwhile, banks look to decrease their operational risks by balancing their income sources and loan portfolios, which means providing services to retail, SMEs, and corporations or making other kinds of investments, such as making deposits with other larger financial institutions or entering into partnerships with other companies.

This study examines the link between SMEs’ importance to economic growth, innovation and employment and their need for financial resources and banks’ risk. The approach of this study is to examine the causal relationship between credit to SMEs (as the main factor of their sustainability, and banks’ risk as measured by non-performing loans (NPLs) and loans in Palestine, in particular. The motivation of this study comes from (i) the importance of SMEs in the economy and development as addressed by previous studies and global institutions; (ii) the Palestinian case as a developing country that faces high unemployment and unstable economic growth; and (iii) adopting the European Palestinian Credit Guarantee Fund (EPCGF) to guarantee the credit banks grant to SMEs. The EPCGF was introduced in May 2005. Initially, two banks took advantage of the credit guarantee program. Several other banks followed so that 10 banks, in total, were involved in 2017, (EPCGF, 2018). These factors motivated us to test the causal relationship between SME sustainability (through credit to SMEs) and non-performing loans in Palestine. The results of this study contribute to the literature on SMEs and banks from the point of view of the importance of a fund that provides credit guarantees and, thereby, enhances SMEs’ access to financial resources and decreases banks’ risk. Therefore, the study will try to answer research question: whether there is relationship between credits to SMEs and bank’s risk.

The findings of this paper will contribute to the sustainability literature as a new academic research field. Also, policymakers can use these results to develop rules and regulations to enhance SMEs’ sustainability by providing access to financing in developing countries. Furthermore, bank managers can benefit from this study to enhance their banks’ performance, reduce credit risk, develop their investment strategies, and also implement their bank’s strategy in line with their government’s sustainable-development agenda. Furthermore, the governments of the developing countries can adopt the guarantee funds to enhance the SMEs growth through accessing to the formal financial sources.

This paper is organised as follows: the next section provides a review of the previous literature and develops the hypothesis, and SME-bank credit connection and the problem of bank risk. Section 3, provides the data and methodology. Section 4 provides an empirical analysis and discusses the results. Section 5 presents the conclusions and some policy implications

2. Literature review and hypothesis development

2.1. Literature review

Most of the previous studies on SMEs point out weaknesses in their access to financial resources and provide several reasons for this phenomenon, including a lack of collateral, weakness in management and financial systems, and unstable profitability (Al-Hyari, Al-Weshah, & Alnsour, Citation2012; Badaj & Radi, Citation2017; Beck, Demirguc-Kunt, & Maksimovic, Citation2008; Beck & Demirgüç-Kunt, Citation2006; Bruns & Fletcher, Citation2008; Petersen & Rajan, Citation1994). It is notable that, in 2017, SMEs in the Middle East, North Africa (MENA) with access to loans or lines of credit constituted around 28% of the total number of firms with access to financing, while, the same percentage for SMEs in Palestine was 6% for the same year (World Bank Enterprise Survey, Citation2017). The reasons for this low percentage are collateral issues, bank risk, and the absence of government regulations that enhance SMEs’ access to financial resources (Beck & Demirgüç-Kunt, Citation2006; Berger & Udell, Citation1998; International Monetary Fund, Citation2014). Here, we include credit to SMEs as a key proxy factor that could affect the sustainability of these firms (Shihadeh et al., Citation2018; Walsh, Przychodzen, & Przychodzen, Citation2017).

A study by (De la Torre et al., Citation2010) points out some important facts about banks’ lending practices in relation to SMEs, including the following: (i) banks are very interested in lending to SMEs; banks find that profitable SMEs offer opportunities to increase their earnings; (ii) banks can invest in SMEs in several ways and not just through credit, as they can develop more services which meet SMEs’ needs; (iii) banks can serve SMEs through technology, risk rating, and training. Further, (Jacobson, Lindé, & Roszbach, Citation2005) examine the credit risk among corporations, SMEs, and retail. They conclude that it is less risky for banks to provide credit to SMEs and retail than to corporations. (Erdogan, Citation2018) uses a qualitative method to examine the factors that influence SMEs’ access to financing through bank loans from Turkish banks. The study concludes that several factors influence the level of SMEs’ access to financial resources, such as real financial information, adequate working capital and revenue generation.

Further, (Gill & Biger, Citation2012) examine the barriers to growth among Canadian SMEs and find that access to financing, the market situation, regulations and environmental factors could influence SME growth. The study recommends that governments could review their regulations with a view to enhancing SME growth. (Lee, Sameen, & Cowling, Citation2015) use the financial crisis as their study period, and analyse its influence on SME innovation. The study covers a large sample set of SMEs in the UK and divides the sample into two groups: before the crisis (2007–2008) and after the crisis (2010 and 2012). The results indicate that innovative firms find it more difficult to access financial services than other kinds of firms. The study confirms the need for additional financial resources for innovative SMEs. (Quartey, Turkson, Abor, & Iddrisu, Citation2017) use the World Bank’s Enterprise Survey to test the factors that influence SMEs’ access to financing within selected countries in Africa. The results indicate that inadequate collateral, high risk and a limited credit history are considered barriers to access to financial resources. (Wonglimpiyarat, Citation2015) note that government policies and regulations enhance bank financing to SMEs in Shanghai and Beijing as financial centers in China. The study finds that, despite developments in the Chinese regulations in terms of enhancing sustainability in SMEs, these regulations and rules needs further development to increase innovation and rapid growth in the SME sector.

Moreover, (Kersten, Harms, Liket, & Maas, Citation2017) reviews studies related to SMEs. One main of their study’s main findings indicates that programs that provide financing to SMEs could enhance their performance, increase investment in SMEs and decrease unemployment. (Arraiz, Melendez, & Stucchi, Citation2014) examine the influence of guarantee funds on SMEs’ performance among Colombian firms. Their study covers the period 1997 to 2007, for a large panel dataset. The results indicate that firms that joined the fund-guarantee program enhanced their output and employment, while there was no influence on wages and productivity.

2.2. Hypothesis development

Non-performance loans, as a percentage of default loans to total loans, was widely used in the literature on banks and risk, and efficiency indicators (Bernini & Brighi, Citation2017; Delis, Staikouras, & Tsoumas, Citation2016; Delis & Staikouras, Citation2011; Morgan & Pontines, Citation2018; Nguyen, Ta, & Nguyen, Citation2018; Sahyouni & Wang, Citation2018; Shihadeh & Liu, Citation2019). Therefore, this investigation follows the previous studies in using non-performing loans as a risk indicator. Banks expand their networks so as to reach more clients and offer more services and, thus, earn higher profits. During this process, banks carry out activities that incur such risks as capital and investment losses and defaults on loans. Some of the banking literature uses the branch as bank size and links the number of branches to bank performance and risk, (Bernini & Brighi, Citation2017; Shihadeh & Liu, Citation2019). On the topic of branch networks, (Salas & Saurina, Citation2002) find that, in Spain, networks with more branches incur increases in loan problems within three years among commercial banks, and four years among savings banks. Furthermore, some studies use bank assets as a proxy to bank size and the internal determinant of non-performing loans. However, (Bhattarai, Citation2017) find that there is no relationship between bank size and non-performing loans among Nepalese commercial banks. Further, (Fernandez de Lis, Pagés, & Jesus, Citation2000; Hu, Li, & Chiu, Citation2004) find a negatively significant relationship between assets and non-performing loans in Spain, which means that the size of a bank’s assets could decrease the incidence of NPLs. Also, several studies address and use banks’ assets as a microeconomic proxy for banks, (Distinguin, Roulet, & Tarazi, Citation2013; Imbierowicz & Rauch, Citation2014, Chatterjee, Citation2015; Ono & Uesugi, Citation2009; Swamy, Citation2018).

The study uses the value of banks’ capital as the internal control variable. Studies on banking exhibit different ways of using the value of banks’ capital as determinants of bank performance and risk. Other studies use the capital ratio (capital-to-assets) or its amount of capital as internal determinants of bank risk, (Fungacova & Weill, Citation2012; Horvath, Seidler, & Weill, Citation2014; Tan, Citation2016). The relationship between a bank’s capital and its NPLs go in opposite directions; that is, an increase a bank’s NPLs would negatively influence the value of its assets and, thus, the earnings that reflect on its capital, (Kumarasinghe, Citation2017).

For the external control variable, we use GDP, the percentage of annual growth, in Palestine. This indicator is usually used to measure the macroeconomic environment that could influence and be affected by the production units in the economy. The previous studies that examined the banks performance and risk also used GDP as the external control variable (Fadzlan & Kahazanah, Citation2009; Horvath et al., Citation2014; Rashid & Jabeen, Citation2016; Sahyouni & Wang, Citation2018). (Dash & Kabra, Citation2010) point out a reverse relationship between GDP and non-performing loans in the case of India. (Kjosevski & Petkovski, Citation2016) address the reciprocal relationship between NPLs and GDP. Further, (Umar & Sun, Citation2016) include GDP as a proxy to control the business cycle; here, in the case of Chinese banks, they point out that the influence of GDP on NPLs is unclear. Moreover, (Tanasković & Jandrić, Citation2015) analyzes the factors that could influence NPLs among CEEC and SEE countries (Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Hungary, Lithuania, Montenegro, FYR Macedonia, Romania, Serbia and Slovenia) for the period 2006 to 2013. This study notes that the GDP in these countries could decrease the incidence of NPLs.

The above studies address the issues of banks’ targets of achieving profits and decreasing risk and global institutions’ objectives of achieving SME growth and sustainability as significant keys to sustainable development and economic stability. Following this research, we link the factor of SMEs’ access to credit and SMEs sustainability with non-performing loans as a risk indicator for banks. Therefore, we examine the relationship between financing SMEs and banks’ risk. Thus, we propose the following hypotheses:

H0: Extending credit to SMEs has no significant influence on banks’ risk in Palestine

H1: Extending credit to SMEs has a significant influence on banks’ risk in Palestine

2.3. Sustainability in SMEs, bank’s credits, and risk

Previous research points to the importance of SMEs in creating jobs and contributing to economic growth and stability. It also points to the need to ensure that SMEs fulfil their role in innovation so they can continue to be a major contributing factor in the economy. To help SMEs accomplish this, government institutions and formal financial sources should work to overcome the obstacles SMEs face in this regard, the main obstacle being access to and use of sources of finance, (Al-Hyari et al., Citation2012; Badaj & Radi, Citation2017; Beck & Demirgüç-Kunt, Citation2006; Bruns & Fletcher, Citation2008; Beck et al., Citation2008; Petersen & Rajan, Citation1994). Therefore, the global plan should be primarily to promote the sustainability of SMEs through reforming the infrastructure, regulations, and rules pertaining to financing so as to provide a suitable environment for SME growth, (World Bank, Citation2014). The financial services providers (i.e., banks) can develop services in line with SMEs’ needs, from the cost of these services to the types of services provided, (Abraham & Schmukler, Citation2017). Meanwhile, SMEs should be able to use banks loans more efficiently so as to manage these sources, develop financial systems and enhance their performance and growth.

SMEs should have access the formal financial sector which provides diverse services and continuity in funding sources. Also, some banks and microfinance institutions (MFIs) offer analysis and technical consultancy services. These services and funding sources could help SMEs innovate, develop their products and distribution channels, reach new markets, increase their investments in technology and enhance their business performance and growth, (Al-Hyari et al., Citation2012). If these developments were to occur in this vital sector, then this could positively reflect on job creation, poverty alleviation and inequality issues, and it could enhance innovation and increase living standards, thereby contributing to sustainability in economic growth and development. The main factor standing in the way of all of this is banks’ risk in extending credit services to SMEs and how to address this risk.

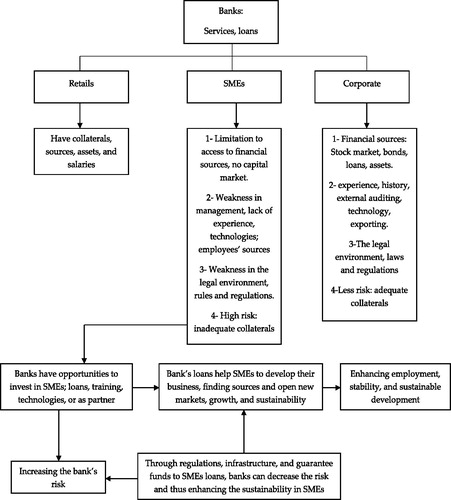

Banks looking to decrease their risk through; investment diversification, reaching more clients, finding more sources, discovering new opportunities of investment, and knowing more about environments to manage the risks. Therefore, balancing these issues require from bank's managers and policymakers to find whether investing in SMEs through credits can enhance bank’s performance, as well as, adding benefits to the economic and development sustainability. Meanwhile, previous studies pointed out that investing in SMEs through credits carried out more risks for the banks for several reasons as addressed in the earlier sections. Other studies find out that credits to SMEs and retail are less risky than corporate, (Jacobson et al., Citation2005). Further, banks can invest in SMEs in different ways such as technologies, training, and developing their services, (De la Torre et al., Citation2010). , presents the factors which could influence the SMEs accessing to the financial services. Further, how that banks can enhance the sustainability in SMEs, and decrease the risk through credits and guarantee fund. Therefore, enhancing the economic development and sustainability in the economy.

Figure 1. Sustainability in SMEs and bank’s risk.

3. Data and research method

3.1. The data

This study uses banks’ annual reports for the period 2006 to 2016, for 15 banks operating in Palestine. The data is collected for 13 commercial banks and 2 Islamic banks; the panel data contains 165 observations on non-performing loans as percentage from net direct credit, bank size (number of branches), total assets, and total capital. Some of the banks included in their annual reports data on their credit to SMEs, other banks did not; thus, to calculate this figure and include it in the analysis for those banks that did not offer this information, we follow the percentages published by (European Commission, Citation2016), which constitutes 6% of total direct credit. Data on annual GDP growth and inflation index, are collected from the World Bank indicators. Further, we could not access to more bank’s data before established the EPCGF, thus, to analyze its influence on bank’s risk before and after, therefore, this issue considering as study’s limitation.

3.2. The variables

We chose the variables for the current study based on the hypotheses developed in section two and on previous studies. The dependent variable for our analysis include the value of non-performing loans as a percentage of the value of net direct credit, which represents the default loans for 180 days and more. For the independent variables, we use access to sources of finance, which is considered a barrier to sustainability and growth in SMEs. Therefore, the study uses the amount of credit extended to SME as a key variable of SME sustainability. A second independent variable is bank size as measured by the number of branches as this could influence the value of non-performing loans. The analysis also uses as independent and internal control variables the banks’ net assets and their paid amount of capital, by amount. We also include as an external control variable the annual growth in GDP and inflation, consumer price index.

3.3. The empirical model

To examine the study’s hypotheses, we employ and develop the following model and empirical analysis:

(1)

(1)

We can re-write the statistical equation to an econometrics equation; thus, Equationeq.1(1)

(1) will be as follows:

(2)

(2)

where NPL represents the non-performing loans; CSME is the amount of credit extended to SMEs; SIZE represents the number of bank branches; GDP is the annual percentage rate of growth; ASS is the banks’ total net assets; CAP is the amount of bank’s capital. To get robust results, the study’s analysis follows fourth stages of empirical regressions: first, we use a descriptive analysis and correlation matrix to explain the study’s data and present the initial indicators on the relationship between the outcome and the predictors; second, we analyse the causal relationship between the dependent and independent variables, by using the panel vector autoregression technique (PVAR), the fisher unit root test, and the granger causality test; third, we use dynamic panel techniques, fixed and random effects, and the Hausman test to choose the most suitable technique for the data; fourth, we include inflation (the consumer price index) as the external control variable that could influence the outcome. These stages of the analysis will give us robust results and, thus, enhance our conclusions so we can present recommendations to the policymakers in developing countries.

4. The empirical analysis

4.1. Descriptive analysis

presents the descriptive statistics for this study, including the basic characteristics of the data, such as the mean, and the minimum and maximum values for the standard deviations. From the table, we note that there are 162 observations among all of the variables. One bank merged with another bank in 2016 and, for another bank, for two years of data are missing.

Table 1. Descriptive statistics.

presents the correlation coefficient for the study variables; the matrix of the correlation presents indicators of the directions for the outcome variable and the predictor variables. The table also presents a high correlation coefficient, around 0.81, between banks’ capital and size as presented in the number of branches. In fact, the banks in the study usually use their capital to establish new branches and offices, to invest in technology and other banking-related matter; thus, one would expect to see a high correlation between a bank’s capital and its number of branches. Further, the table indicates a high correlation coefficient between credit to SMEs and banks’ assets, this is normal as the amount of credit extended to SMEs is a part a bank’s total credit, and the last component of a bank’s balance sheet is its assets.

Table 2. Correlation matrix.

Meanwhile, there is no specific percentage correlation coefficient to indicate multicollinearity between the independent variables; however, some researchers point out that if the correlation coefficient is 0.80 or less, then there is no multicollinearity problem. Furthermore, this study employs the variance inflation factor (VIF) test. The result of the VIF test is 4.23, which indicates no multicollinearity; that is, if the VIF is less than 10, then there is no multicollinearity among the independent variables, (see, for instance, Appendix A in ), (Field, Citation2000; Hassan, Citation2009; Shihadeh et al., Citation2018). Based on the above, the multicollinearity problem does not exist in this case, and the high correlations between some of independent variables have practical and rational explanations, (Gujarati, Citation2004; Kennedy, Citation2008; Kjosevski & Petkovski, Citation2016).

4.2. Causality relationship

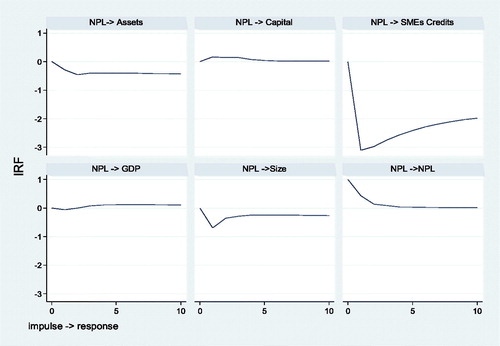

This section presents the results of the causality analysis, based on the PVAR technique. To find the causal relationship between the NPLs, as a bank-risk indicator, and credit to SMEs, as our key variable, and other control variables, this analysis follows Abrigo and Love, (Abrigo & Love, Citation2015). These researchers present a set of Stata program and developed the panel VAR model selection, estimation and inference in a generalised method of moments (GMM) framework. The analysis in our study presents how these variables influence each other and in which direction. After running the PVAR model, we use impulse response functions (IRFs) to present the responses of the NPLs, (De Bock & Demyanets, Citation2012; Fainstein & Novikov, Citation2011; Jakšić, Erjavec, & Cota, Citation2012).

Further, as the study panel is missing some data and is, therefore, unbalanced, we use the Fisher unit root test as it is suitable in this case, (Kjosevski & Petkovski, Citation2016; Tanasković & Jandrić, Citation2015). First, we lag the variables at their first lag; after this, we run the unit root test. The results indicate that all of the variables are stable and stationery except for banks’ capital. Thus, we transform this variable to the first difference, run the test again, and obtain stationary and stable data. As we are going to examine the relationship between the NPLs, over a period of 180 days and more, and other micro- and macroeconomic factors, we use the first lag because it is reasonable in this case. presents the direction of the NPLs according to the variable obtained by using the IRF.

Figure 2. IRFs of NPL. Source: Authors’ calculations.

After running the PVAR and testing the stationarity, we run the Granger causality test. presents the results. These indicate that the micro- and macroeconomics factors have a direct effect on banks’ non-performing loans in Palestine. For instance, credit to SMEs has a direct effect on NPLs, and the direction of this influence is negative, which means that increasing credit to SMEs could decrease NPLs, a result that is consistent with (Jacobson et al., Citation2005). Credit helps SMEs enhance their business and growth and, thus, their sustainability and their ability to better contribute to overall development sustainability. Further, banks could join the EPCGF program in term to decrease their credit risk and enhance their performance. These results could encourage SMEs to rearrange their legal situation by registering their firm and enhance their connection to the financial system, and business plans. Also, banks could specialise in providing more sources of financing to SMEs and increasing their portfolio of clients from this significant sector. Further, this result supports our theoretical discussion in Section 2.

Table 3. Granger causality test results.

Bank size, as measured by the number of branches, has a direct effect on NPLs. That is, banks with more branches could increase their rate of non-performance by increasing their credit portfolio. This result is consistent with (Salas & Saurina, Citation2002). All other variables have a negative effect on NPLs. Thus, banks in Palestine could enhance the value of their net capital and assets by decreasing their non-performing loans. Further, improvements in GDP could decrease the incidence of banks’ non-performing loans. That is, if the number of non-performing loans decreases, then this could increase the amount of credit banks make available to SMEs and also increase their number of branches; this could also increase growth in GDP and in banks’ assets. As the value of non-performing loans increases, the banks lose money, and this negatively influences all bank activities, particularly in relation to SMEs.

4.3. Robust analysis

In this section, we follow the third and fourth stages of the methodology discussed in Section 3. First, we run the fixed- and random-effects techniques for the basic model. Then we run the Hausman test, which indicates that the fixed-effects technique is suitable for the study’s data. Next, we include inflation as proxy of the macroeconomics, and run the fixed-, random-effects and Hausman tests again. Appendix B in presents the results of the Hausman test, which indicates the suitability of the fixed-effects technique for the study’s data.

presents the results of the fixed-effects technique. The results indicate that extending credit to SMEs has a significant influence on NPLs in both models. This indicates that when more credit is directed towards SMEs, this could decrease the value of banks’ non-performing loans in Palestine. Furthermore, enhancing credit to SMEs would reflect in their sustainability and growth, as accessing sources of finance is a main barrier to growth for SMEs.

Table 4. Fixed effect results.

The results also indicate that bank size and capital, as bank’s proxies, have no effect on non-performing loans, in both models 1 and 2. However, banks’ assets have a significant effect on non-performing loans in both models. Therefore, enhancing the assets components of banks would decrease their risk. Further, the results in indicate that inflation, as proxy of the macroeconomics, has no effect on banks’ risk, as is shown in model 2.

The results in are generally consistent with those in and the other analyses in this study, particularly those related to our key variable—the provision of credit to SMEs. Therefore, this study presents a significant and robust analysis of credit to SMEs and banks’ risk.

5. Conclusion and policy implications

This study empirically examines the influence of credit to SMEs as a factor of their sustainability and also on banks’ risk. The study uses data from 15 banks operating in Palestine and covers the 11-year period from 2006 to 2016. In addition to the key variable, the study uses several micro- and macroeconomic variables to capture the factors that could influence the non-performance of loans as a risk indicator. To this end, the study applies both descriptive and empirical analyses through the PVAR model, the Granger causality test, and fixed and random effects to obtain robust results. In addition to the empirical examinations, this study draws a theoretical framework of the relationship between a guarantee fund, banks’ risk, and the supply of credit to and the sustainability of SMEs. The framework helps us test the study’s hypotheses and, thus, presents robust and significant results for the literature on banks and SMEs.

For credit to SMEs as a significant factor of SME growth and sustainability, the results indicate that enhancing credits to SMEs would decrease the value of non-performing loans in banks operating in Palestine. Joining the EPCGF program encourages banks to extend more credit to SMEs, at a minimum level of risk. These loans mean SMEs can invest in their growth and sustainability. When SME’s are able to access sources of financing and enhance their negotiating ability, they are able to improve their business-development activities and production technologies. As SMEs make significant contributions in the economy, supporting their growth and sustainability should be an important component of economic policy.

Formal institutions, such as the Palestine Monetary Authority, can encourage banks that have not already done so to join the EPCGF program. This program enhances banking by reducing the credit risk associated with lending to SMEs. In turn, this positively influences SMEs’ activities by providing access to sources of financing. Banks can also become involved in other SME activity, such as providing training and financial management, and investing in technologies (De la Torre et al., Citation2010). Therefore, convincing banks of the usefulness of investing in SMEs through providing credit could in turn reflect on their own financial performance, that of the SMEs they support, and on the economy and society, in general.

The results of this study present new evidence from one developing country on the role of providing credit to SMEs, through a fund that provides guarantees on banks’ risk. The application of a guarantee fund could be used in other developing countries to encourage banks to extend more credit to SMEs. Furthermore, formal institutions in developing countries could work to contribute more to the necessary credit environment and infrastructure, and devise regulations that would provide SMEs with access to the financial sources with workable conditions, such as reasonable collateral requirements.

Based on the above results and conclusions, we recommend that future studies on developing countries focus on the relationship between loans to SMEs and banks’ risk. Also, future researchers could empirically examine the influence of a guarantee fund on both SMEs’ and banks’ performance and risk. A study on the influence of bank credit on the sustainability and growth of SMEs from different sides, such as employment, performance, growth, the environment, and poverty alleviation, would also be useful. More studies could be conducted on the effect of banks’ credits in SMEs, such as investment in technologies, financial management training, and consulting. Banks could also develop more services to cover the needs of SMEs that extend beyond direct access to credit.

Acknowledgements

The authors are thankful to Bo Liu, Ousseini Amadou Maiga, and Yipeng Wang for their suggestions. We also extend our thankful to the anonymous reviewers for their valuable comments and suggestions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Abraham, F., & Schmukler, S. L. (2017). Addressing the SME Finance Problem. Research and Policy brief. World Bank Malaysia hub. No. 9. World Bank.

- Arraiz, I., Melendez, M., & Stucchi, R. (2014). Partial credit guarantees and firm performance: Evidence from the Colombian National Guarantee Fund. Small Business Economics, 43(3), 711–724. doi: 10.1007/s11187-014-9558-4

- Al-Hyari, K., Al-Weshah, G., & Alnsour, M. (2012). Barriers to internationalisation in SMEs: Evidence from Jordan. Marketing Intelligence & Planning, 30(2), 188–211. doi: 10.1108/02634501211211975

- Abrigo, M. R., & Love, I. (2015, February). Estimation of panel vector autoregression in Stata: A package of programs. manuscript, 2015. http://paneldataconference2015.ceu.hu/Program/Michael-Abrigo.pdf.

- Bauchet, J., & Morduch, J. (2013). Is micro too small? Microcredit vs. SME finance. World Development, 43, 288–297. doi: 10.1016/j.worlddev.2012.10.008

- Batrancea, I., Morar, I. D., Masca, E., Catalin, S., & Bechis, L. (2018). Econometric modeling of SME performance. Case of Romania. Sustainability, 10(1), 192. doi: 10.3390/su10010192

- Berger, A., & Udell, G. (2006). A more complete conceptual framework for SME finance. Journal of Banking & Finance, 30(11), 2945–2966. doi: 10.1016/j.jbankfin.2006.05.008

- Beck, T., Senbet, L., & Simbanegavi, W. (2015). Financial inclusion and innovation in Africa: An overview. Journal of African Economies, 24(suppl 1), i3–i11. doi: 10.1093/jae/eju031

- Beck, T., & Demirgüç-Kunt, A. (2006). Small and medium-size enterprises: Access to finance as a growth constraint. Journal of Banking & Finance, 30(11), 2931–2943. doi: 10.1016/j.jbankfin.2006.05.009

- Beck, T., & Demirguc-Kunt, A., Maksimovic, V. (2008). Financing patterns around the world: The role of institutions. Journal of Financial Economics, 90, 467–487.

- Badaj, F., & Radi, B. (2017). Empirical investigation of SMEs’ perceptions towards PLS financing in Morocco. International Journal of Islamic and Middle Eastern Finance and Management, 11, 250–273. doi: 10.1108/IMEFM-05-2017-0133

- Bruns, V., & Fletcher, M. (2008). Banks’ risk assessment of Swedish SMEs. Venture Capital, 10(2), 171–194. doi: 10.1080/13691060801946089

- Berger, A., & Udell, G. F. (1998). The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. Journal of Banking and Finance, 22(6–8), 613–673.

- Bernini, C., & Brighi, P. (2017). Bank branches expansion, efficiency and local economic growth. Regional Studies, 52, 114. doi: 10.1080/00343404.2017.1380304

- Bhattarai, S. (2017). Determinants of non-performing loan in Nepalese commercial banks. Economic Journal of Development Issues, 19(1–2), 22–38. doi: 10.3126/ejdi.v19i1-2.17700

- Chatterjee, U. K. (2015). Bank liquidity creation and asset market liquidity. Journal of Financial Stability, 18, 139–153. doi: 10.1016/j.jfs.2015.03.006

- Duygan-Bump, B., Levkov, A., & Montoriol-Garriga, J. (2015). Financing constraints and unemployment: Evidence from the great recession. Journal of Monetary Economics, 75, 89–105. doi: 10.1016/j.jmoneco.2014.12.011

- Delis, M. D., & Staikouras, P. K. (2011). Supervisory effectiveness and bank risk. Review of Finance, 15(3), 511–543. doi: 10.1093/rof/rfq035

- Delis, M. D., Staikouras, P. K., & Tsoumas, C. (2016). Formal enforcement actions and bank behavior. Management Science, 63(4), 95987. doi: 10.1287/mnsc.2015.2343

- De Bock, R., & Demyanets, A. (2012). Bank asset quality in emerging markets; determinants and spillovers (IMF Working Papers 12/71), International Monetary Fund. doi: 10.5089/9781475502237.001

- De la Torre, A., Pería, M. S., & Schmukler, S. L. (2010). Bank involvement with SMEs: Beyond relationship lending. Journal of Banking & Finance, 34(9), 2280–2293. doi: 10.1016/j.jbankfin.2010.02.014

- Dash, M. K., & Kabra, G. (2010). The determinants of non-performing assets in Indian commercial bank: An econometric study. Middle Eastern Finance and Economics, 7, 94–106.

- Distinguin, I., Roulet, C., & Tarazi, A. (2013). Bank regulatory capital and liquidity: Evidence from US and European publicly traded banks. Journal of Banking & Finance, 37(9), 3295–3317. doi: 10.1016/j.jbankfin.2013.04.027

- Erdogan, A. I. (2018). Factors affecting SME access to bank financing: An interview study with Turkish bankers. Small Enterprise Research, 25(1), 23–35. doi: 10.1080/13215906.2018.1428911

- European Palestinian Credit Guarantee Fund. http://www.cgf-palestine.com/partners.

- European Commission. (2016). EU initiatives for financial inclusion. DG for Neighbourhood and Enlargement Negotiations. Retrieved from https://ec.europa.eu/neighbourhoodenlargement/sites/near/files/neighbourhood/pdf/key-documents/nif/20160601-eu-initiative-for-financial-inclusion.pdf

- Fainstein, G., & Novikov, I. (2011). The comparative analysis of credit risk determinants in the banking sector of the Baltic states. Review of Economics & Finance, 1, 20–45.

- Fernandez de Lis, S., Pagés, J. M., & Jesus, S. (2000). Credit growth, problem loans and credit risk provisioning in Spain. Banco de Espana Working Paper 18.

- Fungacova, Z., & Weill, L. (2012). Bank liquidity creation in Russia. Eurasian Geography and Economics, 53(2), 285–299. doi: 10.2747/1539-7216.53.2.285

- Fadzlan, S., & Kahazanah, N. B. (2009). Determinants of bank profitability in a developing economy: empirical evidence from the China banking sector. Journal of Asia-Pacific Business, 10(4), 201–307.

- Field, A. (2000). Discovering statistics: Using SPSS for windows (1st ed.). London: Sage.

- Gill, A., & Biger, N. (2012). Barriers to small business growth in Canada. Journal of Small Business and Enterprise Development, 19(4), 656–668. doi: 10.1108/14626001211277451

- Gozzi, J. C., & Schmukler, S. L. (2015). Public credit guarantees and access to finance. European economy: Banks, regulation, and the real sector, 2, 101–117.

- Gujarati, D. N. (2004). Basic econometrics (4rd ed.). New York: McGraw-Hill Press

- Horvath, R., Seidler, J., & Weill, L. (2014). Bank capital and liquidity creation: Granger-causality evidence. Journal of Financial Services Research, 45(3), 341–361. doi: 10.1007/s10693-013-0164-4

- Hu, J. L., Li, Y., & Chiu, Y. H. (2004). Ownership and nonperforming loans: Evidence from Taiwan’s banks. The Developing Economies, 42(3), 405–420. doi: 10.1111/j.1746-1049.2004.tb00945.x

- Hassan, MK. (2009). UAE corporations-specific characteristics and level of risk disclosure. Managerial Auditing Journal, 24(7), 668–687.

- Imbierowicz, B., & Rauch, C. (2014). The relationship between liquidity risk and credit risk in banks. Journal of Banking & Finance, 40, 242–256. doi: 10.1016/j.jbankfin.2013.11.030

- International Monetary Fund. (2014). The Middle East and Central Asia Regional Economic Outlook. Access to finance for small and medium-sized enterprises in the MENAP and CCA regions. www.imf.org

- Jacobson, T., Lindé, J., & Roszbach, K. (2005). Credit risk versus capital requirements under Basel II: Are SME loans and retail credit really different? Journal of Financial Services Research, 28(1–3), 43. doi: 10.1007/s10693-005-4356-4

- Jakšić, N., Erjavec, B., & Cota, S. (2012). Impact of macroeconomic shocks on real output fluctuations in Croatia. Zagreb International Review of Economics and Business, 15(issue Special Conference Issue), 69–78. http://EconPapers.repec.org/ RePEc: Zag: Zirebs: V:13: Y:2010: I: Sci: P:69-78

- Kumar, S., & Rao, P. (2015). A conceptual framework for identifying financing preferences of SMEs. Small Enterprise Research, 22(1), 99–112. doi: 10.1080/13215906.2015.1036504

- Kersten, R., Harms, J., Liket, K., & Maas, K. (2017). Small firms, large impact? A systematic review of the SME finance literature. World Development, 97, 330–348. doi: 10.1016/j.worlddev.2017.04.012

- Kumarasinghe, P. J. (2017). Determinants of non-performing loans: Evidence from Sri Lanka. International Journal of Management Excellence, 9(2), 1113–1121. doi: 10.17722/ijme.v9i2.367

- Kjosevski, J., & Petkovski, M. (2016). Non-performing loans in Baltic states: Determinants and macroeconomic effects. Baltic Journal of Economics, 17, 25–44. doi: 10.1080/1406099X.2016.1246234

- Kennedy, P. (2008). A guide to econometric (6th ed.). Malden, MA: Blackwell.

- Lee, N., Sameen, H., & Cowling, M. (2015). Access to finance for innovative SMEs since the financial crisis. Research Policy, 44(2), 370–380. doi: 10.1016/j.respol.2014.09.008

- Morgan, P., & Pontines, V. (2018). Financial stability and financial inclusion: the case of SME lending. Singapore Economic Review, 63(1), 111–124. doi: 10.1142/S0217590818410035

- Nguyen, D. T., Ta, H. T., & Nguyen, H. T. (2018). What determines the profitability of Vietnam commercial banks? International Business Research, 11(2), 231. doi: 10.5539/ibr.v11n2p231

- Nasr, S., & Pearce, D. (2012). Middle East and North Africa Region - SMEs for job creation in the Arab world: SME access to financial services. Washington, DC: World Bank. http://documents.worldbank.org/curated/en/687631468110059492/Middle-East-and-North-Africa-Region-SMEs-for-job-creation-in-the-Arab-world-SME-access-to-financial-services

- Ono, A., & Uesugi, I. (2009). Role of collateral and personal guarantees in relationship lending: Evidence from Japan's SME loan market. Journal of Money, Credit and Banking, 41(5), 935–960. doi: 10.1111/j.1538-4616.2009.00239.x

- Petersen, M. A., & Rajan, R. G. (1994). The benefits of lending relationships: Evidence from small business data. The Journal of Finance, 49(1), 3–37. doi: 10.2307/2329133

- Pilloff, S. J. (1996). Performance changes and shareholder wealth creation associated with mergers of publicly traded banking institutions. Journal of Money, Credit and Banking, 28(3), 294–310. doi: 10.2307/2077976

- Quartey, P., Turkson, E., Abor, J. Y., & Iddrisu, A. M. (2017). Financing the growth of SMEs in Africa: What are the constraints to SME financing within ECOWAS? Review of Development Finance, 7(1), 18–28. doi: 10.1016/j.rdf.2017.03.001

- Rashid, A., & Jabeen, S. (2016). Analyzing performance determinants: Conventional versus Islamic banks in Pakistan. Borsa Istanbul Review, 16(2), 92–107. doi: 10.1016/j.bir.2016.03.002

- Sahyouni, A., & Wang, M. (2018). The determinants of bank profitability: Does liquidity creation matter? Journal of Economics and Financial Analysis, 2(2), 61–85. http://dx.doi.org/10.1991/jefa.v2i2.a18

- Salas, V., & Saurina, J. (2002). Credit risk in two institutional regimes: Spanish commercial and savings banks. Journal of Financial Services Research, 22(3), 203–224. doi: 10.1023/A:1019781109676

- Swamy, V. (2018). Basel III capital regulations and bank profitability. Review of Financial Economics, 00, 1–14. doi: 10.1002/rfe.1023

- Shinozaki, S. (2012). A new regime of SME finance in emerging Asia: Empowering growth-oriented SMEs to build resilient national economies. ADB Working Paper Series on Regional Economic Integration: No. 104.

- Shihadeh, F. H., Hannon, A. (M. T.), Guan, J., Ul Haq, I., & Wang, X. (2018). Does financial inclusion improve the banks’ performance? Evidence from Jordan. In J. W. Kensinger (Ed.), Global tensions in financial markets. Research in finance (Vol. 34, pp.117–138). Bradford: Emerald Publishing Limited. doi: 10.1108/S0196-382120170000034005

- Shihadeh, F., & Liu, B. (2019). Does financial inclusion influence the banks risk and performance? Evidence from global prospects. Academy of Accounting and Financial Studies Journal, 23(3), 1–12. https://www.abacademies.org/articles/Does-Financial-Inclusion-Influence-the-Banks-Risk-and-Performance-1528-2635-23-3-403.pdf

- Shihadeh, F. H. (2018). How individual’s characteristics influence financial inclusion: Evidence from MENAP. International Journal of Islamic and Middle Eastern Finance and Management, 11(4), 553. doi: 10.1108/IMEFM-06-2017-0153

- Tan, Y. (2016). The impacts of risk and competition on bank profitability in China. Journal of International Financial Markets, Institutions and Money, 40, 85–110. doi: 10.1016/j.intfin.2015.09.003

- Tanasković, S., & Jandrić, M. (2015). Macroeconomic and institutional determinants of non-performing loans. Journal of Central Banking Theory and Practice, 4(1), 47–62. doi: 10.1515/jcbtp-2015-0004

- Umar, M., & Sun, G. (2016). Non-performing loans (NPLs), liquidity creation, and moral hazard: Case of Chinese banks. China Finance and Economic Review, 4(1) , 10. doi: 10.1186/s40589-016-0034-y

- Walsh, G. S., Przychodzen, J., & Przychodzen, W. (2017). Supporting the SME commercialization process: The case of 3D printing platforms. Small Enterprise Research, 24(3), 257. doi: 10.1080/13215906.2017.1396490

- Wang, X. H., & Shihadeh, F. H. (2015). Financial inclusion: Policies, status, and challenges in Palestine. International Journal of Economics and Finance, 7(8), 196–207. doi: 10.5539/ijef.v7n8p196

- Wellalage, N., & Locke, S. (2017). Access to credit by SMEs in South Asia: Do women entrepreneurs face discrimination. Research in International Business and Finance, 41, 336–346. doi: 10.1016/j.ribaf.2017.04.053

- Werner, R. A. (2016). A lost century in economics: Three theories of banking and the conclusive evidence. International Review of Financial Analysis, 46, 361–379. doi: 10.1016/j.irfa.2015.08.014

- Wonglimpiyarat, J. (2015). Challenges of SMEs innovation and entrepreneurial financing. World Journal of Entrepreneurship, Management and Sustainable Development, 11(4), 295–311. doi: 10.1108/WJEMSD-04-2015-0019

- World Bank. http://www.enterprisesurveys.org/data/exploretopics/finance#middle-east-north-africa.

- World Bank. (2014). SMEs, growth, and poverty, Do Pro - SME policies work? Note no.268. http://rru.worldbank.org/Viewpoint/index.asp.

Appendix A

Table A1. Multicollinearity test.

Appendix B

Table B1. Hausman test.