?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The purpose of this paper is to investigate the links between a company’s ultimate owner and the risk involved with financial performance. The study tests hypotheses on the relation between ultimate ownership origin and risk of return on assets. The research adopts cross-sectional data from a unique sample of 32,614 companies across 43 European countries with ultimate owners from 105 countries. The results indicate that the domestic ultimate owner is, in general, less likely to be a risk-taker than overseas investors. The research develops the nature of ownership-performance relations in the specific economic context of Europe. The results add robust evidence on attitudes towards performance risk of Europe wide ultimate owners.

Subject classification codes:

1. Introduction

This study asks whether the level of risk involved with the performance of European companies is associated with the origin of the ultimate owner. An ultimate owner is a shareholder who has determining voting rights in the firm and who is not controlled by anyone else (Haw, Hu, Hwang, & Wu, Citation2004, p. 437).

Effective decision-making within the company is a widely discussed area both in practice and within the research community. The separation of ownership and control has encouraged agency conflict between managers and owners (Fama & Jensen, Citation1983; Grossman & Hart, Citation1988; Jensen & Meckling, Citation1976; Mirrlees, Citation1976; Ross, Citation1973; Stiglitz, Citation1974, Citation1975). Thus, a central focus for corporate governance is the reduction of agency costs produced due to manager and shareholder information asymmetry. The reduction of those costs should increase a firm’s value (Sánchez-Ballesta & García-Meca, Citation2007). One aspect of corporate governance is the relationship between ownership structure and company performance.

This paper applies the agency theory framework to characterize the principal. It addresses the limitation in the current literature on the relationship between ultimate owners and company risk. As immediate ownership is insufficient for defining the ownership and control structures, this study enhances prior research (Aluchna & Kaminski, Citation2017; Laeven & Levine, Citation2008) by testing the existence of a relationship between the ultimate owner and company performance risk.

Using the regression model, we test hypotheses and analyze the relation between ownership structure and company performance risk by measuring absolute return on assets (ROA). We sampled 32,614 firms from 43 European countries with ultimate owners from 105 home countries. Our study provides a host country perspective and is, to our knowledge, the first attempt to track the relationship between the ultimate owners and performance of European companies on a large scale.

This paper contributes to the literature on ownership and performance research in several ways. Firstly, it provides robust evidence of the risk attitude asymmetry between domestic and overseas ultimate owners. Domestic ultimate owners are significantly more risk-averse. Secondly, this study also provides evidence that risk perception changes when the ultimate owner accepts a direct holding in contrast to being indirectly engaged. Thirdly, we advance Aluchna and Kaminski’s (Citation2017) findings in both the Europe and risk dimensions. Fourthly, we provide a more comprehensive picture of the real effects of concentration as many existing studies analyze immediate ownership and firms from a single country or focus on listed companies only.

2. Literature review and hypotheses development

It has already been noted by Berle and Means (Citation1932) that managers’ interests tend to be contradictory to the interests of shareholders. The impact of owners can be broadly associated with two views: global advantage hypothesis and home advantage hypothesis (Duqi & Al-Tamimi, Citation2018). External owners might outperform domestic in numerous aspects e.g. better access to capital, excessive liquidity, efficient risk diversification, or know-how and technology development. Consequently, the foreign investor is at an information disadvantage in comparison to local shareholders (Berger, Dai, Ongena, & Smith, Citation2003; Choe, Kho, & Stulz, Citation2005).

Research that has looked at the relationship between ownership structure and company performance has focused on the attitudes of owners in relation to the company’s performance risk (e.g. Gürsoy & Aydogan, Citation2002). Existing studies reveal mixed results when looking at ownership concentration and company performance risks (Kapopoulos & Lazaretou, Citation2007; Saona & San Martín, Citation2016). The prior studies concentrate mainly on concentration-performance aspects of immediate ownership without looking specifically at ultimate ownership. As a consequence of the above the literature has not provided conclusive results about ultimate owner concentration-risk performance issues.

2.1. Concentration

The agency theory implies that a reduction in agency costs results in an increase of corporate value, but the existing evidence on the link between shareholder structure and performance, where there is any, is inconclusive (Kapopoulos & Lazaretou, Citation2007) and marginal (Thomson & Pedersen, Citation2000). In the diversified structure of shareholding, the majority and minority shareholders might earn different benefits. While the minority enjoy the dividend payouts and capital gains, the majority might benefit as well from the related party transactions (Bona-Sánchez, Fernández-Senra, & Pérez-Alemán, Citation2017). A tradeoff exists between the reduction of the agency costs and disposal of the shares in companies with both groups of shareholders. Majority shareholders have more incentive to reduce the information asymmetry instead of selling stocks or even to challenge the minority holders. This observation hinders the ability to generalize all shareholder behavior. In fact, Bedo and Ács (Citation2007) report that the dominant shareholders may gain private benefits at the expense of minority investors. The inefficiency of the financial market information mechanism combined with a weak institutional environment supports those incentives (La Porta, Lopez-De-Silanes, & Shleifer, Citation1999; Thomson & Pedersen, Citation2000; Wang & Shailer, Citation2015). On the other hand, the dominant shareholders might both decorate and support the value of the entity (Uddin, Citation2016). The dominant shareholder might impact the company both directly and indirectly.

2.2. Ultimate owner

Agency problems and shareholder structures are multifold. The existence of the information asymmetry and differences in motivation between the management and shareholders implies only that management should receive performance-based compensation (Grossman & Hart, Citation1988). The relationship is clear in the case of one shareholder as the principal versus one manager as an agent. In reality, we deal with structures of shareholders, thus a minority shareholder might not necessary effectively monitor management because of free rider problems (Easterbrook & Fischel, Citation1983). Thus, the large and dominant shareholders are motivated to do this monitoring, but they face the agency costs as well. In liquid markets instead of providing guidance to managers, the shareholders can reduce their engagement in the equity by disposing of stocks. In addition, the composition of the immediate ownership can differ from the structure of the ultimate owners. The first might fluctuate as the results of the business framework changes (e.g. tax topicalization) while the second can be persistent (e.g. due to the control premium). Thus, the motivations of direct and ultimate owners might not necessarily be the same. Following Haw et al. (Citation2004) we apply the ultimate owner perspective as immediate ownership is insufficient for defining the ownership and control structures. The ultimate owner’s voting rights level is set at 50.01% and is not traced any further, assuming an absolute majority of voting rights beyond 50.01%. If a company has more than one ultimate owner, consistent with prior studies (Fan & Wong, Citation2005; Haw et al., Citation2004), we consider the largest ultimate owner.

2.3. Risk attitude

Risks can be viewed both as a negative (threat) and a positive (opportunity). Risk perceptions impact decision making under risk and help us understand results that cannot be explained by the standard model of expected utility delivered by von Neumann and Morgenstern (Citation1944). Thus, a combination of the choice and risk aspects attracts ample research (Sarin & Weber, Citation1993). Heaton and Lucas (Citation2000) showed that poorly diversified entrepreneurs should require a large return premium over public equity. Kerins et al. (Citation2004) applied simulation and suggest that exposure to idiosyncratic risk is expensive while Mueller (Citation2011) confirmed this relation with empirical evidence. Gürsoy and Aydogan (Citation2002) examined the impact of concentration of ownership on the performance and risk-taking behavior of Turkish non-financial companies. They reported that higher concentration leads to better market performance. Tykvová and Borell (Citation2012) examined financial distress risks of European companies around the buyout event. They asked whether buyout companies go bankrupt more often than comparable non-buyout companies. The authors concluded that private equity investors select companies which are less financially distressed than comparable non-buyout companies and when companies are backed by experienced private equity funds, their bankruptcy rates are lower.

Based on 156 responses to an opinion questionnaire survey, Zhang and Qian (Citation2017) indicate that not only risk itself but the risk perception impacts the cooperation between agent and principal. The relational risk perception and the performance risk perception of contractors build up obstacles to collaboration. Within the agency theory, risk attracts attention in cases of the principal-principal aspects (Boubakri, Cosset, & Saffar, Citation2013; Mahto & Khanin, Citation2015; W. Su & Lee, Citation2013; Uddin, Citation2016), but the literature is less abundant on the risk aspects of the ultimate owner and risk performance. Uddin (Citation2016) traced principal-principal conflict between government and private owners and firm risk attitude. He observed that the link between government ownership and risk taking is non-linear. Duqi and Al-Tamimi (Citation2018) examined the impact of the owner’s identity on banks’ capital adequacy and liquidity risk for banks domiciled in the Middle East and North Africa. They concluded that private and foreign investors have a stronger preference for higher levels of capital. The mentioned study concentrates on the impact of the ultimate owner on a firm’s performance or risk. With this study we applied the absolute value of ROA as the risk instrument to capture the risk perception of the ultimate owner. We would like to shift the attention from the entity to the owner perspective, which led us to the following working hypothesis:

H1.1 Ultimate owner control is negatively related to firm performance risk.

Wang and Shailer (Citation2015) applied meta-analysis of 42 papers on public companies from 18 emerging economies and concluded that ownership concentration has a negative link to firm performance. However, that study does not distinguish differences in the way the owners, direct or not, control the entity. With this research we would like to address this aspect, which led us to the next working hypothesis:

H1.2. Direct ultimate owner control is negatively related to firm performance risk.

This eclectic theory states that the extent, form, and pattern of international production are determined by ownership concentration, location, and internalized advantage (Dunning, 1988). We challenge this framework with the hypothesis that the location of the owner affects the type of risk profile the firms have. External owners might outperform domestic in numerous aspects e.g. better access to capital, excessive liquidity, efficient risk diversification, or know-how and technology development. On the other hand, the foreign investor is at an information disadvantage compared to local investors (Berger et al., Citation2003; Choe et al., Citation2005). Weak investor protections and less developed institutions enhance investor risk, agency costs, and create an incentive to engage in private benefits and related party transactions (La Porta et al., Citation1999; Wang and Shailer, Citation2015). This in turn, might lead to differences in the risk environments and behaviors for domestic and foreign investors due to information asymmetry. Looking at three theories of capital structure, namely: the trade-off, market timing models, and pecking order. The last postulates that the cost of financing increases with asymmetric information (Donaldson, Citation1961; Myers & Majluf, Citation1984). The entrenchment theory implies when managers hold some equity and shareholders are too dispersed to take action against non-value maximization behavior, insiders may deploy corporate actions to obtain personal benefits (Farinha, Citation2002). Since the impact of the ultimate shareholder information asymmetry resulting from the geographic location has not been widely studied, we challenge that domestic owners outperform foreigners with local knowledge and risk assessments. Thus, the next hypothesis is:

H2. Domestic ultimate owners are negatively related to firm performance risk.

The geographical evidence of the links between ownership structures and performance have been studied before. There are a number of studies focusing on a particular economy: Brazil (da Cunha & Bortolon, Citation2016), Czech Republic (Konecny & Castek, Citation2016), China (Liang & Wang, Citation2017; Ruiqi, Wang, Xu, & Yuan, Citation2017), Greece (Kapopoulos & Lazaretou, Citation2007) to name a few. Some studies refer to regions, including: Asia (Heugens, van Essen, & (Hans) van Oosterhout, 2009), Europe (Renders, Gaeremynck, & Sercu, Citation2010; Thomson & Pedersen, Citation2000), Western Europe (Luis Gallizo, Moreno, & Salvador, Citation2014), East Asia and Western Europe (Haw et al., Citation2004), Central and Eastern Europe (Bedo & Ács, Citation2007; Szarzec & Nowara, Citation2017). Those studies focus mainly on the performance response to the concentration in specific countries or regions, we aim to reverse the perspective towards performance risk and the origin of the ultimate owner not the company itself.

Boubakri et al. (Citation2013) examined the impact of shareholder identity on corporate risk-taking behavior. They concluded that foreign ownership is positively related to corporate risk-taking. The impact of home country effects on firm performance (home bias) (Hawawini, Subramanian, & Verdin, Citation2004) was widely discussed in international business, international economics, and finance. McGahan and Victer (Citation2010) studied the relative importance of home country, industry, and firm influences on corporate profitability they concluded that home country and industry effects are more important to domestic firms than to multinationals. Xia and Walker (Citation2015) sampled manufacturing firms and examined how much ownership contributes to firm performance. They concluded that ownership interacts with region and time. We follow the perspectives of Renders et al. (Citation2010), and Thomson and Pedersen (Citation2000) as our study focuses on Europe as the host region for global investors, thus we formulated the following hypothesis:

H3. Origin of the ultimate owner is negatively related to firm performance risk.

There have been a number of empirical studies showing how differences between owner types influence firm performance e.g.: state (Chen, Firth, & Xu, Citation2009; Goldeng, Grünfeld, & Benito, Citation2008; Y. Su, Xu, & Phan, Citation2008; Thomsen, Pedersen, & Kvist, Citation2006), industry investors (George & Kabir, Citation2012; Renneboog, Citation2007), managers (Cheng, Su, & Zhu, Citation2012; Davies, Hillier, & McColgan, Citation2005; de Miguel, Pindado, & de la Torre, Citation2004), and financial institutions (David, Bloom, & Hillman, Citation2007; Erenburg, Smith, & Smith, Citation2016; Ferreira & Matos, Citation2008; Nagel, Qayyum, & Roskelley, Citation2015; Thomsen et al., Citation2006). However, little is known about whether the ultimate owners are natural to the sector of the economy they are involved in, thus this paper proposes:

H4. Ultimate owner performance risk attitudes are indifferent across industry, commerce, and services.

We identified four areas of contradictory results and potential research deficiencies. The current research fails to provide evidence on the relation between the ultimate owner and firm performance risk (H1). We are unsure if the above relation difference in case of the domestic ultimate owner (H2) it’s home country (H3) or the type of the industry (H4).

3. Data and methodology

3.1. Data and sample

We drew the source data from the Amadeus database (Bureau, Citation2017). This study uses a data set on the ownership and control structures of ultimate owners, not immediate shareholders. We center the research on medium and large European companies, both public and private, to avoid small business governance bias. We sampled companies from 43 European countries. We limited the sample to existing companies, operating in 2016, having available data for assets, current assets, debtors, shareholder funds, and those with at least 250 employees. Our usable sample consisted of 32,614 companies across Europe. The source data relates to all companies domiciled in European countries. . provides the details on the data selection strategy.

Table 1. Data search strategy.

The data derived from the database includes the performance measure of return on assets (ROA) and the standard set of the controlling variables including size of the domestic group, which follows prior studies (Aluchna & Kaminski, Citation2017; Sánchez-Ballesta & García-Meca, Citation2007). The analysis was performed using the R language (R Core Team, Citation2018).

Prior studies offer different specifications for ownership and structure measurements, we follow broadly Aluchna and Kaminski (Citation2017). For the risk performance measure, we applied the absolute value of ROA, the base variable ROA follows the prior research specifications (Aluchna & Kaminski, Citation2017; Thomson & Pedersen, Citation2000). Our sample was restricted to non-financial institutions, thus, contrary to Duqi & Al-Tamimi (Citation2018) we did not use the capital requirement as a risk proxy.

The ultimate ownership concentration we measured in both ways, as a percentage of shares held irrespective of the underlying structure (GUOt) and as a percentage of shares held directly (GUOd). We measured the stake in percentage instead of the binary variable to account for the differences between the ultimate owners’ engagements. Prior research (Perrini, Rossi, & Rovetta, Citation2008; van Essen et al., Citation2015) applies the size of the ownership stake as a percentage variable. To reflect the bargaining power of the owner at a company level we control the number of shareholders. To analyze the home bias, we grouped the 105 identified ultimate owners home countries into broader groups namely: Europe, the USA, China, Japan, Asia (without China, Japan), and America (both Americas without the USA). To verify the hypothesis that the location of the owner affects the type of risk profile of the firms, we split the entire population between ultimate owners domiciled in the same country as the company and those not. We isolated those ultimate owners coming from the country listed as a non-cooperative tax jurisdiction. Finally, we examined the investment across the economy sectors: industry, commerce, and services based on the Standard Industrial Classification codes.

We used the standard control variables like assets and debts (Sánchez-Ballesta & García-Meca, Citation2007; Wright, Ferris, Sarin, & Awasthi, Citation1996), as well as the numbers of non-ultimate owners (shareholders) and sub-groups (subsidiaries) to control the diversification of the organizational structures. The definition of used variables is given in .

Table 2. Variables definitions.

3.2. Methodology

We applied the absolute value of ROA as the explained variable in the analysis of company performance risk. The ROA is widely used as a performance indicator (Earle et al., Citation2005; E. R. Gedajlovic & Shapiro, Citation1998; Thomsen et al., Citation2006), contrary to the market based indicators such as Tobin’s Q, which is a weak instrument if stock markets are less efficient (Worthington & Higgs, Citation2004). Among the different risk measurements (compare e.g.: Altman & Saunders, Citation1997; Duqi & Al-Tamimi, Citation2018; Staszkiewicz, Citation2018) we applied absolute values of ROA to capture the entire spectrum of performance volatility.

We based our specifications on Aluchna and Kaminski (Citation2017), however, we used the absolute value of dependent variables to mimic the riskiness of return. We enhanced the initial model with a set of binary variables to control the different origin of the ultimate owner. The set of variables we tested in respect of the potential collinearity. In line with Aluchna and Kaminski (Citation2017), we expect potentially closely linked variables, namely assets and debts. In fact, the correlation between both variables amounts to 0.79, thus we applied the log transformation. The omission of debts from the system did not significantly affect results. Our initial specifications suffered from heteroscedasticity, thus we trimmed the observation on the 99th quantile and applied a robust standard error estimator. We tested a reference model for specifications with the application of the RESET - Ramsey Regression Equation Specification Error Test (Zeileis & Hothorn, Citation2002), finally, we controlled the model with quadratic, cubic, and joint effects of the continuous variables to address the nonlinearity aspects in the final models. Our final specifications passed the joint test of potential collinearity with a variance inflation factor below two.

The abbreviated analytical form of our model shows the following specifications:

We estimated the pooled model on the subsets of industry, commerce, and services companies.

4. Empirical results

In we report the descriptive statistic of continuous variables pooled and by type of major branches.

Table 3. Descriptive statistics continuous variables.

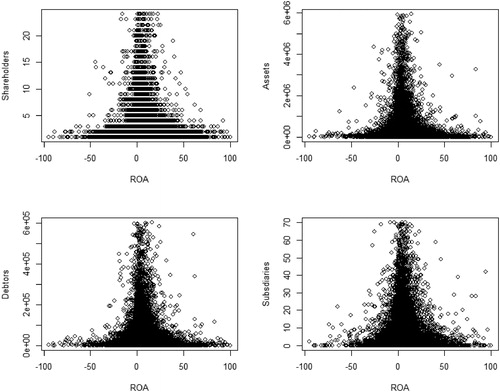

We analyzed the descriptive statistics and identified four instances of negative debtors and treated these observations as errors thus we impute the negative values as nulls. For the model’s computation and scatterplots, we trimmed data at the 99th quantile to eliminate outliers. Probably the most intuitive result of our examination is the scatterplot of the continuous variables against the ROA. shows the mentioned relations on the trimmed data for ROA against the number of shareholders, total assets, debtor values, and the number of subsidiaries.

Figure 1. Scatterplots of the number of shareholders, total assets, debtor values and the number of subsidiaries against return on assets.

We observed a general relation that increasing the values of debtors, assets, numbers of shareholders or subsidiaries resulted in a diminishing return of asset absolute values. In addition, the scatterplots indicate a nonlinear relation among variables, which reconciles to prior research (e.g. Uddin, Citation2016). This observation supports the application of the absolute value of the ROA as the risk dimension for this study.

shows the numbers of ultimate owners by geographic regions and type of industry they operate in within Europe. The data shows that most ultimate owners are in Europe and the majority of them are domestic investors.

Table 4. Interrelation of the binary (dummy) variables.Table Footnote*

The structure of the domicile of the ultimate owner is stable across different sectors. The impact of the ultimate owners in non-cooperative tax jurisdictions is marginal. We subsequently tested specifications with and without the inclusion of the offshore companies, we did not observe any significant effects thus we resigned to isolating the offshore effect in the final model. The results of the estimation are displayed in .

Table 5. Estimation results.

Because the ROA and ROE capture different aspects of performance (Aluchna & Kaminski, Citation2017; Bedo & Ács, Citation2007; Wang & Shailer, Citation2015) and consequently provide different dimensions of risk assessment we tested the specifications for robustness. We replaced the absolute ROA with ROE in the regression equation keeping all remaining variables and verified the signs of the parameters. Both dimensions of the ultimate owner involvement were confirmed to have the same sign and significance (GUOt = 0.034, GUOd = - 0.110). We modified the regression equation to include a control for whether the company was public or private. The estimation of the parameters changed, however, the significance of the variables remained unaffected.

5. Discussion

Our results advance Wang and Shailer’s (Citation2015) conclusion that ownership has a negative correlation with firm performance by disclosing a substantial variation of this link in the case of ownership dilution. In fact, we observed a negative correlation between the risk of performance and shareholder concentration for direct holding. This supports our hypothesis H1.2. On the other hand, we noticed a positive correlation between total holdings and performance risk, despite Wang and Shailer’s (Citation2015) prior observation, meaning H1.2 is supported. The evidence we gathered supports Thomsen and Pedersen (Citation2000) on the marginal effect of the link between ownership and performance. The former contradictory evidence on the direction and strength of the concentration, and performance of Hanousek et al. (Citation2007), Earle et al (Citation2005), Bedo and Ács (Citation2007), or Moscu et al. (Citation2015), reconcile to our scatterplots findings. Our findings are, thus, in line with Uddin’s (Citation2016) observation that risk relations are non-linear.

The dichotomy in the relation between the attitudes toward risk of direct and indirect ultimate owners implies the existence of Easterbrook and Fischel’s (Citation1983) concerns on the shareholder division between minority and majority. Direct involvement of the ultimate owner reduces the performance risk in contrast to indirect involvement. This evidence casts another perspective on Wang and Shailer’s (Citation2015) meta-analysis, which suggested that the relation is affected by the way the ultimate owner controls the entity. Our findings reconcile to Boubakri et al. (Citation2013) that foreign ownership is positively related to corporate risk-taking for the US and America based ultimate owners, however, the link is not necessarily universal across the globe.

Our models provided support for H2. We observed significant and sustainable risk aversion among domestic ultimate owners across different industries. These results indicate that the tradeoff between the global advantage and home advantage hypotheses (Duqi & Al-Tamimi, Citation2018) is unbalanced for Europe. The attitude toward risk of the domestic owners might come from a local information advantage (Berger et al., Citation2003; Choe et al., Citation2005), however, our setting does not allow us to derive conclusions on this. Another plausible explanation is that the overseas investors can divest the continental risk against a wider portfolio of investments across different continents.

Referring to the origin of ultimate owners (H3) our findings stay contrary to Duqi and Al-Tamimi (Citation2018), due to non-domestic investors being more likely to accept higher risk. Investors from America, including the US, and Oceania are more likely to be risk-takers. Our results show the same direction both for pooled and service data, which reconciles to Boubakri et al.’s (Citation2013) observation that foreign ownership is positively related to corporate risk-taking. Those discrepancies might come from different sample representation, for example, in services we sampled both banks and other financial institutions, while Duqi and Al-Tamimi focus on only the banking sector. On the other hand, Faccio and Lang (Citation2002) report that widely held and family-controlled firms dominate in Europe, thus our result suggests that overall both instructional and private willingness to take risks dominates in English driven economies compared to the rest of the world. Our results for Europe and America (including the US), support the home bias hypothesis. The significance of the domestic ultimate owner supports McGahan and Victer’s (Citation2010) conclusions. It stays contrary to Xia and Walker’s (Citation2015) findings on China, however is consistent with Stiglitz’s (Citation1999) observation that market oriented state shareholders may be more appropriate in countries with weak institutional environments. In general, the European companies operate in the environment with the strong institutional framework.

Finally, we did not find persuasive evidence for the link between ownership risk consistency across branches (no support for H4). The results we report suggest that ultimate owner performance risk attitudes are different across industry, commerce, and services. The dichotomy in risk attitudes for the ultimate owners holds true across all branches. We understand these results reinforce the lack of homogeneity between the types of the ultimate owners. Even the ultimate owners differ in term of their specializations, thus a general approach does not reveal any consistent picture of their risk attitudes.

This study applies the percentage of votes controlled by the ultimate owner as the proxy for the real power of the shareholder. Due to the limitation in our dataset we were unable to observe the control leverage (for example: dual class shares, shareholder coalitions and agreements, pyramidal ownership, golden shares), thus the results should be interpreted only in respect to the ultimate owner voting control power.

The study relied on cross‐sectional methods that embody the implicit assumption that model parameters are stable across firms and over time. Such a method, however, allows for substantial sample size, which is not necessary achievable with other methods, thus it anchors the economy picture and serves as the reference point for further studies. The results suggest that the risk attitudes of the ultimate owner depend on its origin. This observation has implications for policy setters. In the case of an economy which attracts foreign investments, the policy should differentiate between risk-averse and risk-taker investors. Thus, to be efficient the policy setters might focus on matching investors from less risk-oriented countries with lower risk potential investment opportunities in the policy setter’s economy. This observation might be important to the transition’s economies.

6. Conclusions

With this study, we ask whether the riskiness of the performance of European entities is associated with the origin of the ultimate owner. We identified the dichotomy in risk attitude. The domestic ultimate owners are, in general, less likely to be risk-takers than overseas investors. We also observe significant risk aversion of domestic ultimate owners across different industry branches.

Our study advances the efficiency of ownership structures discussed in the corporate governance in several ways. Firstly, we discovered a substantial difference among the overseas and domestic owners with respect to risk acceptance. Secondly, we enhance prior studies on concentration and performance with a risk perspective, showing the dichotomy in terms of the direct ultimate owner influence. Thirdly, we confirmed the nonlinear relation between concentration and risk performance. Fourthly, we provide robust evidence from the European perspective for further research.

Our findings have policy implications as the investigation into domestic-overseas ultimate owners’ preferences might support cross-European economic policy.

The study results indicate potential areas for further research. We are unaware of the causes of the risk-averse nature of domestic owners versus that of the overseas owners. It is possible that inside-knowledge of the local environment plays a role. We hope to be able to address this issue in the future.

Acknowledgements

While retaining responsibility for any error, the authors thank anonymous referees for comments and suggestions. A special acknowledgement goes to Dariusz Owczarek and Piotr Śniadowski at SGH Information Technology Department for virtual machines support. Joanna Rudaś, Maciej Bednarczyk and Marek Sieradz supported us with the relevant literature search. We own the gratitude to participants of Edward Altman Lecture Series 2019, section leader Marek Gruszczyński and co-speakers: Natalia Nehrebecka, Mateusz Czerwiński for valuable comments to the early version of this paper. We thank Roman Sobiecki, Gabriel Główka, Andrzej Fierla, Marek Bryx for the organizational and financial support of the project. Paper was partly financed from the project 216149/E-334/S/2018 KNOP/S18/04/18.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Altman, E. I., & Saunders, A. (1997). Credit risk measurement: Developments over the last 20 years. Journal of Banking & Finance, 21, 1721–1742. doi:10.1016/S0378-4266(97)00036-8

- Aluchna, M., & Kaminski, B. (2017). Ownership structure and company performance: A panel study from Poland. Baltic Journal of Management, 12(4), 485–502. doi:10.1108/BJM-01-2017-0025

- Bedo, Z., & Ács, B. (2007). The impact of ownership concentration, and identity on company performance in the US and in Central and Eastern Europe. Baltic Journal of Management, 2(2), 125–139. doi:10.1108/17465260710750955

- Berger, A. N., Dai, Q., Ongena, S., & Smith, D. C. (2003). To what extent will the banking industry be globalized? A study of bank nationality and reach in 20 European nations. Journal of Banking & Finance, 27(3), 383–415. doi:10.1016/S0378-4266(02)00386-2

- Berle, A. A., & Means, G. G. C. (1932). The modern corporation and private property. New York, NY: The Macmillan Company.

- Bona-Sánchez, C., Fernández-Senra, C. L., & Pérez-Alemán, J. (2017). Related-party transactions, dominant owners and firm value. BRQ Business Research Quarterly, 20(1), 4–17. doi:10.1016/j.brq.2016.07.002

- Boubakri, N., Cosset, J.-C., & Saffar, W. (2013). The role of state and foreign owners in corporate risk-taking: Evidence from privatization. Journal of Financial Economics, 108(3), 641–658. doi:10.1016/j.jfineco.2012.12.007

- Bureau, V. D. (2017). Amadeus. Retrieved from https://amadeus.bvdinfo.com

- Chen, G., Firth, M., & Xu, L. (2009). Does the type of ownership control matter? Evidence from China’s listed companies. Journal of Banking & Finance, 33(1), 171–181. doi:10.1016/j.jbankfin.2007.12.023

- Cheng, P., Su, L. N., & Zhu, X. K. (2012). Managerial ownership, board monitoring and firm performance in a family-concentrated corporate environment. Accounting & Finance, 52(4), 1061–1081. doi:10.1111/j.1467-629X.2011.00448.x

- Choe, H., Kho, B.-C., & Stulz, R. M. (2005). Do domestic investors have an edge? The trading experience of foreign investors in Korea. Review of Financial Studies, 18(3), 795–829. doi:10.1093/rfs/hhi028

- da Cunha, C. M. P., & Bortolon, P. M. (2016). The role of ownership concentration and debt in downturns: Evidence from Brazilian firms during the 2008–9 financial crisis. Emerging Markets Finance and Trade, 52(11), 2610–2623. doi:10.1080/1540496X.2015.1087793

- David, P., Bloom, M., & Hillman, A. J. (2007). Investor activism, managerial responsiveness, and corporate social performance. Strategic Management Journal, 28(1), 91–100. doi:10.1002/smj.571

- Davies, J. R., Hillier, D., & McColgan, P. (2005). Ownership structure, managerial behavior and corporate value. Journal of Corporate Finance, 11(4), 645–660. doi:10.1016/j.jcorpfin.2004.07.001

- de Miguel, A., Pindado, J., & de la Torre, C. (2004). Ownership structure and firm value: new evidence from Spain. Strategic Management Journal, 25(12), 1199–1207. doi:10.1002/smj.430

- Donaldson, G. (1961). Corporate debt capacity: A study of corporate debt policy and the determination of corporate debt capacity. Washington, DC: Beard Books.

- Duqi, A., & Al-Tamimi, H. (2018). The impact of owner’s identity on banks’ capital adequacy and liquidity risk. Emerging Markets Finance and Trade, 54(2), 468–488. doi:10.1080/1540496X.2016.1262255

- Earle, J. S., Kucsera, C., & Telegdy, A. (2005). Ownership concentration and corporate performance on the Budapest stock exchange: Do too many cooks spoil the Goulash? Corporate Governance, 13(2), 254–264. doi:10.1111/j.1467-8683.2005.00420.x

- Easterbrook, F. H., & Fischel, D. R. (1983). Voting in corporate law. The Journal of Law and Economics, 26(2), 395–427. doi:10.1086/467043

- Erenburg, G., Smith, J. K., & Smith, R. (2016). Which institutional investors matter for firm survival and performance? The North American Journal of Economics and Finance, 37, 348–373. doi:10.1016/j.najef.2016.05.012

- Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325. doi:10.1086/467037

- Faccio, M., & Lang, L. H. P. (2002). The ultimate ownership of Western European corporations. Journal of Financial Economics, 65(3), 365–395. doi:10.1016/S0304-405X(02)00146-0

- Fan, J. P. H., & Wong, T. J. (2005). Do external auditors perform a corporate governance role in emerging markets? Evidence from East Asia. Journal of Accounting Research, 43(1), 35–72. doi:10.1111/j.1475-679x.2004.00162.x

- Farinha, J. (2002). Dividend policy, corporate governance and the managerial entherchment hyphothesis: An empirical analysis. Corporate Governance, 30(351), 1–42.

- Ferreira, M. A., & Matos, P. (2008). The colors of investors’ money: The role of institutional investors around the world. Journal of Financial Economics, 88(3), 499–533. doi:10.1016/j.jfineco.2007.07.003

- Gedajlovic, E. R., & Shapiro, D. M. (1998). Management and ownership effects: Evidence from five countries. Strategic Management Journal, 19(6), 533–553. https://doi.org/10.1002/(SICI)1097-0266(199806)19:6

- George, R., & Kabir, R. (2012). Heterogeneity in business groups and the corporate diversification–firm performance relationship. Journal of Business Research, 65(3), 412–420. doi:10.1016/j.jbusres.2011.07.005

- Goldeng, E., Grünfeld, L. A., & Benito, G. R. G. (2008). The performance differential between private and state owned enterprises: The roles of ownership, management and market structure. Journal of Management Studies, 45(7), 1244–1273. doi:10.1111/j.1467-6486.2008.00790.x

- Grossman, S. J., & Hart, O. D. (1988). One share-one vote and the market for corporate control. Journal of Financial Economics, 20, 175–202. doi:10.1016/0304-405X(88)90044-X

- Gürsoy, G., & Aydogan, K. (2002). Equity ownership structure, risk taking, and performance: an empirical investigation in Turkish listed companies. Emerging Markets Finance & Trade, 38(6), 6–25.

- Hanousek, J., Kočenda, E., & Svejnar, J. (2007). Origin and concentration. Economics of Transition, 15(1), 1–31. doi:10.1111/j.1468-0351.2007.00278.x

- Haw, I.-M., Hu, B., Hwang, L.-S., & Wu, W. (2004). Ultimate ownership, income management, and legal and extra-legal institutions. Journal of Accounting Research, 42(2), 423–462. doi:10.1111/j.1475-679X.2004.00144.x

- Hawawini, G., Subramanian, V., & Verdin, P. (2004). The home country in the age of globalization: How much does it matter for firm performance? Journal of World Business, 39(2), 121–135. doi:10.1016/j.jwb.2003.08.012

- Heaton, J., & Lucas, D. (2000). Portfolio choice and asset prices: The importance of entrepreneurial risk. The Journal of Finance, 55(3), 1163–1198. doi:10.1111/0022-1082.00244

- Heugens, P. P. M. A. R., van Essen, M., & (Hans) van Oosterhout, J. (2009). Meta-analyzing ownership concentration and firm performance in Asia: Towards a more fine-grained understanding. Asia Pacific Journal of Management, 26(3), 481–512. doi:10.1007/s10490-008-9109-0

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. doi:10.1016/0304-405X(76)90026-X

- Kapopoulos, P., & Lazaretou, S. (2007). Corporate ownership structure and firm performance: Evidence from Greek firms. Corporate Governance: An International Review, 15(2), 144–158. doi:10.1111/j.1467-8683.2007.00551.x

- Kerins, F., Smith, J. K., & Smith, R. (2004). Opportunity cost of capital for venture capital investors and entrepreneurs. Journal of Financial and Quantitative Analysis, 39(2), 385. doi:10.1017/S0022109000003124

- Konecny, L., & Castek, O. (2016). The effect of ownership structure on corporate financial performance in the Czech Republic. Ekonomicy Casopis, 64(5), 477–498.

- La Porta, R., Lopez-De-Silanes, F., & Shleifer, A. (1999). Corporate ownership around the world. The Journal of Finance, 54(2), 471–517. doi:10.1111/0022-1082.00115

- Laeven, L., & Levine, R. (2008). Complex ownership structures and corporate valuations. Review of Financial Studies, 21(2), 579–604. doi:10.1093/rfs/hhm068

- Liang, H., & Wang, R. (2017). Decisions made by the controlling shareholder under financial crisis. Emerging Markets Finance and Trade, 53(6), 1405–1424. doi:10.1080/1540496X.2017.1321538

- Luis Gallizo, J., Moreno, J., & Salvador, M. (2014). European banking integration: is foreign ownership affecting banking efficiency? Journal of Business Economics and Management, 16(2), 340–368. doi:10.3846/16111699.2013.769023

- Mahto, R. V., & Khanin, D. (2015). Satisfaction with past financial performance, risk taking, and future performance expectations in the family business. Journal of Small Business Management, 53(3), 801–818. doi:10.1111/jsbm.12088

- McGahan, A. M., & Victer, R. (2010). How much does home country matter to corporate profitability? Journal of International Business Studies, 41(1), 142–165. doi:10.1057/jibs.2009.69

- Mirrlees, J. A. (1976). The optimal structure of incentives and authority within an organization. The Bell Journal of Economics, 7(1), 105–131. doi:10.2307/3003192

- Moscu, R. G., Grigorescu, C. J., & Prodan, L. (2015). Does ownership structure affect firm performance. Knowledge Horizons Economics, 7(3), 194–917. https://doi.org/10.1016/B978-0-7506-7247-4.50007-0

- Mueller, E. (2011). Returns to private equity - Idiosyncratic risk does matter! Review of Finance, 15(3), 545–574. doi:10.1093/rof/rfq003

- Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. doi:10.1016/0304-405X(84)90023-0

- Nagel, G. L., Qayyum, M. A., & Roskelley, K. D. (2015). Do motivated institutional investors monitor firm payout and performance? Journal of Financial Research, 38(3), 349–377. doi:10.1111/jfir.12063

- Perrini, F., Rossi, G., & Rovetta, B. (2008). Does ownership structure affect performance? Evidence from the Italian market. Corporate Governance: An International Review, 16(4), 312–325. doi:10.1111/j.1467-8683.2008.00695.x

- R Core Team. (2018). R: A language and environment for statistical computing. Vienna: Foundation for Statistical Computing.

- Renders, A., Gaeremynck, A., & Sercu, P. (2010). Corporate-governance ratings and company performance: A Cross-European Study. Corporate Governance: An International Review, 18(2), 87–106. doi:10.1111/j.1467-8683.2010.00791.x

- Renneboog, L. (2007). Corporate governance and corporate finance: A European Perspective (Vol. 24). New York, NY: Routledge. https://doi.org/10.4324/9780203940136

- Ross, S. A. (1973). The economic theory of agency: The principal’s problem. The American Economic Review, 63(2), 134–139.

- Ruiqi, W., Wang, F., Xu, L., & Yuan, C. (2017). R&D expenditures, ultimate ownership and future performance: Evidence from China. Journal of Business Research, 71, 47–54. doi:10.1016/j.jbusres.2016.10.018

- Sánchez-Ballesta, J. P., & García-Meca, E. (2007). A meta-analytic vision of the effect of ownership structure on firm performance. Corporate Governance: An International Review, 15(5), 879–892. doi:10.1111/j.1467-8683.2007.00604.x

- Saona, P., & San Martín, P. (2016). Country level governance variables and ownership concentration as determinants of firm value in Latin America. International Review of Law and Economics, 47, 84–95. doi:10.1016/j.irle.2016.06.004

- Sarin, R. K., & Weber, M. (1993). Risk-value models. European Journal of Operational Research, 70(2), 135–149. doi:10.1016/0377-2217(93)90033-J

- Staszkiewicz, P. (2018). Model zysków nadzwyczajnych dla przemysłu chemicznego. Przemysł Chemiczny, 1(2), 82–83. doi:10.15199/62.2018.2.8

- Stiglitz, J. E. (1974). Incentives and risk sharing in sharecropping. The Review of Economic Studies, 41(2), 219. doi:10.2307/2296714

- Stiglitz, J. E. (1975). Incentives, risk, and information: notes towards a theory of hierarchy. The Bell Journal of Economics, 6(2), 552–579. doi:10.2307/3003243

- Stiglitz, J. E. (1999). Wither reform? Ten years of transition, Keynote Address. Annual Bank Conference on Development Economics. Washington, DC: the World Bank.

- Su, W., & Lee, C.-Y. (2013). Effects of corporate governance on risk taking in Taiwanese family firms during institutional reform. Asia Pacific Journal of Management, 30(3), 809–828. doi:10.1007/s10490-012-9292-x

- Su, Y., Xu, D., & Phan, P. H. (2008). Principal—Principal conflict in the governance of the Chinese Public Corporation. Management and Organization Review, 4(1), 17–38. doi:10.1111/j.1740-8784.2007.00090.x

- Szarzec, K., & Nowara, W. (2017). The economic performance of state-owned enterprises in Central and Eastern Europe. Post-Communist Economies, 29(3), 375–391. doi:10.1080/14631377.2017.1316546

- Thomsen, S., & Pedersen, T. (2000). Ownership structure and economic performance in the largest european companies. Strateg. Manag. J., 21, 689–705. doi:10.1002/(SICI)1097-0266(200006)21:6<689::AID-SMJ115>3.0.CO;2-Y.

- Thomsen, S., Pedersen, T., & Kvist, H. K. (2006). Blockholder ownership: Effects on firm value in market and control based governance systems. Journal of Corporate Finance, 12(2), 246–269. doi:10.1016/j.jcorpfin.2005.03.001

- Thomson, S., & Pedersen, T. (2000). Ownership structure and economic performance in the largest European Companies. The Journal of Finance, 21(10), 981–996. https://doi.org/10.2307/3094306

- Tykvová, T., & Borell, M. (2012). Do private equity owners increase risk of financial distress and bankruptcy? Journal of Corporate Finance, 18(1), 138–150. doi:10.1016/j.jcorpfin.2011.11.004

- Uddin, M. H. (2016). Effect of government share ownership on corporate risk taking: Case of the United Arab Emirates. Research in International Business and Finance, 36, 322–339. doi:10.1016/j.ribaf.2015.09.033

- van Essen, M., Carney, M., Gedajlovic, E. R., & Heugens, P. P. M. A. R. (2015). How does family control influence firm strategy and performance? A meta-analysis of US publicly listed firms. Corporate Governance: An International Review, 23(1), 3–24. doi:10.1111/corg.12080

- Von Neumann, J., & Morgenstern, O. (1944). Theory of games and economic behavior. Princeton, NJ: Princeton University Press.

- Wang, K., & Shailer, G. (2015). Ownership concentration and firm performance in emerging markets: A meta-analysis. Journal of Economic Surveys, 29(2), 199–229. doi:10.1111/joes.12048

- Worthington, A. C., & Higgs, H. (2004). Random walks and market efficiency in European equity markets. Global Journal of Finance and Economics, 1(1), 59–78.

- Wright, P., Ferris, S. P., Sarin, A., & Awasthi, V. (1996). Imapct of corportate insider, blockholder, and institutional equity ownership on firm risk taking. Academy of Management Journal, 39(2), 441–458. doi:10.2307/256787

- Xia, F., & Walker, G. (2015). How much does owner type matter for firm performance? Manufacturing firms in China 1998–2007. Strategic Management Journal, 36(4), 576–585. doi:10.1002/smj.2233

- Zeileis, A., & Hothorn, T. (2002). Diagnostic checking in regression relationships. R News, 2, 7–10.

- Zhang, L., & Qian, Q. (2017). How mediated power affects opportunism in owner–contractor relationships: The role of risk perceptions. International Journal of Project Management, 35(3), 516–529. doi:10.1016/j.ijproman.2016.12.003