Abstract

We explore the trade-offs between social legitimacy and economic efficiency in the context of corporate philanthropic giving (C.P.G.). C.P.G. is viewed as a cost to seek legitimacy, which also serves as a resource to seek efficiency. Using a longitudinal panel data set of Chinese publicly listed firms, we examine how state ownership and institutional development shape firms’ response to C.P.G., and the contingent role of firm visibility and political ties. State ownership enables firms to prioritise legitimacy over efficiency, whereas institutional development enables firms to emphasise efficiency over legitimacy. We also suggest that the positive effect of state ownership on C.P.G. increases for visible firms, and the negative effect of institutional development on C.P.G. increases for visible firms but decreases for politically connected firms. We discuss the theoretical and practical implications of these findings.

1. Introduction

Institutional theory provides several unique insights into how firms react to institutional pressures (Jeong & Kim, Citation2019; Oliver, Citation1997). Firms’ legitimacy-seeking activities depend on their response to institutional pressures and significantly impact their economic efficiency through legitimacy-management costs, legitimacy benefits, and illegitimacy penalties (Jeong & Kim, Citation2019). On one hand, legitimacy literature suggests that in facing institutional pressures (Marquis & Qian, Citation2014), firms continually ensure that their behaviours are perceived as meeting or exceeding social norms and expectations. On the other hand, economic efficiency literature indicates that firms’ behaviours are substantially influenced not only by transactional cost, but also by the most efficient use of resources and capabilities (Jia, Citation2018). Current research provides evidence that social legitimacy and economic efficiency are the primary concerns of firms’ behaviour decisions (Jia, Citation2018), and present contradictions between firms’ legitimacy-seeking strategies and economic efficiency goals (Jeong & Kim, Citation2019; Oliver, Citation1997). Legitimacy-seeking behaviours have significant implications for gaining legitimacy benefits and avoiding illegitimacy penalties. However, they may threaten economic efficiency through legitimacy-management costs (Jeong & Kim, Citation2019; Lev et al., Citation2009). Firms are also subject to both legitimacy and efficiency threats if their behaviour does not conform to institutional norms and values (Nason et al., Citation2018). Consequently, firms may encounter difficulties in detecting the trade-offs between social legitimacy and economic efficiency.

To address this question, we explore how institutional elements and firm characteristics shape the firms’ response to social legitimacy and economic efficiency (Peng, Citation2003; Zhang et al., Citation2016). We argue that the extent of conformity pressure varies across firms even if they operate in the same institutional environment. Institutional literature suggests that government intervention and market liberation have a diverse impact on firm behaviour decisions. Market liberation causes firms to pay attention to market regulations to improve economic efficiency. Accordingly, we examine whether a firms’ behaviour varies with the institutional pressure, typically from two environments, namely, state ownership and market-oriented institutional development (Liang et al., Citation2015; Zhou et al., Citation2017). Moreover, when facing the same institution, different firms exhibit dissimilar responses to the same pressure (Schilke, Citation2018).

Recognising this trend, institutional theorists suggest that institutional pressure cannot sufficiently account for firm behaviour. Rather, firm heterogeneity may influence such behaviours by changing vulnerabilities to, or defusing, institutional pressures (Ge & Micelotta, Citation2019; Oliver, Citation1997). Firm heterogeneity refers to relatively durable differences in firms’ behaviour decisions that tend to produce a sustainable competitive advantage and economic efficiency (Oliver, Citation1997). For example, if heterogeneity changes its vulnerability to institutional pressures, then firms must meet external demands to obtain legitimacy. In contrast, if heterogeneity can help firms defuse institutional pressures, then firms may respond less to external demands. Wang and Qian (Citation2011) and Ge and Micelotta (Citation2019) theorise firm visibility and political ties as channels of institutional pressures. Building on their efforts, we examine the moderating effect of these two factors on firms’ response.

This study investigates the trade-offs between social legitimacy and economic efficiency by exploring how institutional elements (state ownership and institutional development) and heterogeneity (firm visibility and political ties) impact firm behaviour within the context of corporate philanthropic giving (C.P.G.). C.P.G. is a critical means of firms’ response to institutional pressures and helps in obtaining social legitimacy. Furthermore, C.P.G. has different impacts on a firms’ economic efficiency. On one hand, C.P.G. positively impacts a firm’s economic efficiency because such decision can be made strategically to defend the firm’s legitimacy, and gain critical and valuable resources from stakeholders (Lev et al., Citation2009; Wang & Qian, Citation2011). On the other hand, C.P.G. negatively influences a firm's economic efficiency when it merely represents an expenditure that transforms valuable resources to areas not associated with the firm’s functions. In addition, a firm may be penalised for not engaging in C.P.G., thereby threatening its economic efficiency. Consequently, C.P.G. is viewed as a legitimacy-seeking cost, which firms strategically manage by considering both social legitimacy and economic efficiency (Jeong & Kim, Citation2019).

We test our model in the context of China. The Chinese government is a key stakeholder driving several business strategies as it controls critical resources, particularly regarding firms’ social responsibilities. Therefore, political ties to the government are of vital importance for business success (Zhang et al., Citation2016). Charitable donation has become an institutional expectation and a legitimacy-seeking behaviour (Wang & Qian, Citation2011). Also, with market-oriented reforms, China exhibits unbalanced institutional development in different regions. Hence, it provides an ideal context for investigating the effect of state ownership and institutional development on C.P.G.

2. Theory and hypotheses

2.1. State ownership and C.P.G

State ownership is the percentage of ownership that the government holds in a firm. S.O.E.s are firms owned and controlled by the government (Zhou et al., Citation2017). Under state ownership, the government utilises S.O.E.s to pursue political and economic goals. In turn, as extensions of the public bureaucracy, S.O.E.s also play profound roles in accelerating the country’s economic development, and in implementing and improving social welfare projects (Cuervo-Cazurra et al., Citation2014). Specifically, S.O.E.s must respond to national economic demands and consequently help the government control state economic development because they constitute an intrinsic part of the state economic system as governmental assets (Cui & Jiang, Citation2012). Compared with private-owned enterprises (P.O.E.s), S.O.E.s have greater obligations to serve political mandates and align their interests with national institutions rather than pursue socially desirable objectives such as education, health care, or maximising employment rate (Cuervo-Cazurra et al., Citation2014; Zhang et al., Citation2011). Institution-related literature suggests that state ownership shapes the political attachment of a firm with the national government. Thus, S.O.E.s can attach considerable dependence on the government for critical resources and political support, while enduring the impact to its legitimacy as perceived by national governments (Cuervo-Cazurra et al., Citation2014; Cui & Jiang, Citation2012; Meyer et al., Citation2014). Such political dependence and perception not only prompt S.O.E.s to suffer greater government intervention and institutional pressures than P.O.Es, but also induces them to prioritise political goals.

C.P.G. is commonly viewed as a means of achieving a political goal because it mitigates the governmental financial burden, especially when sufficient resources allow firms to engage in local communities and social welfare projects (Wang & Qian, Citation2011). Despite its cost, C.P.G. is still conducted by S.O.E.s due to concerns for long-term benefits and short-term losses. First, S.O.E.s are obliged to serve political mandates because of their attachment to the government. Those that neglect such obligation avoid the decline of firm efficiency in the short term but lose their long-term legitimacy and receive an illegitimacy-penalty. Moreover, the degree and extent of punishment may increase because S.O.E.s have a strong state imprint and are more dependent on governmental resources (Wang & Luo, Citation2019). Second, C.P.G. behaviour not only signals that firms are sincere in responding to governmental demands but also enables them to secure political legitimacy. In turn, the government may offer such S.O.E.s additional valuable resources and policies that could help reduce economic losses and strengthen competitive advantages. Therefore, we state our first hypothesis as follows:

Hypothesis 1 (H1). State-owned firms are more likely to conduct C.P.G. than private-owned firms.

2.2. Institutional development and C.P.G

Institutional development refers to the implementation of rules and regulations that facilitate market exchanges and limit government intervention in economic activities. The institutional economic view posits that institutional development reduces government intervention in economic activities, contributes to market liberalisation, and consequently increases firms’ tendency to conform to market rules rather than political systems during management decision. In addition, regulatory relaxation and constraint significantly impact the degree of managerial discretion or latitude of action. Thus, institutional development is conducive to enhancing a firm’s managerial discretion because the reduction of governmental intervention and the improvement of the market environment decrease external constraints and increase the firms’ latitude of action (Peteraf & Reed, Citation2007).

Institutional development provides a liberated market environment in which firms are less constrained in making behaviour decisions. Such an environment means that the need for institutional legitimacy decreases because the government is a critical channel of resources and legitimacy only when it is involved in economic activities. Conversely, profit maximisation theorists also emphasise that economic efficiency must offset the costs associated with legitimacy-seeking activities, which otherwise may not be undertaken. Consequently, institutional development may decrease the political benefits from the government, thereby reducing the firms’ inner motivation to continuously engage in legitimacy-seeking activities.

In considering the trade-offs between legitimacy and efficiency, we further hypothesise that firms in the institutional development environment may have a less favourable view of philanthropic activities for at least three reasons. First, the characteristics of institutional development imply that C.P.G. may only serve to increase costs and hamper economic efficiency. This is because such activity can help firms gain socio-political legitimacy, but not critical political resources and support. Second, given the reduction of government intervention in resource allocation and the driving forces of economic efficiency maximisation, the level of institutional development enhances the negative relationship between C.P.G. and financial performance, thereby resulting in lowered expectations of C.P.G. outcome. Third, under the context of lesser external constraints and greater managerial discretion, the decision of C.P.G. is determined by the philanthropic activities themselves. Engagement in C.P.G. in the context of institutional development not only hinders abundant legitimacy benefits, but also threatens economic efficiency. By comparison, firms that do not engage in philanthropy do not suffer an illegitimacy-penalty. Thus, firms are less likely to engage in C.P.G., as stated below in our second hypothesis:

Hypothesis 2 (H2). Firms in a more institutionally developed region are less likely to do C.P.G.

2.3. The moderating role of visibility and political tie

High-visibility firms tend to receive more attention from stakeholders than their low visibility counterparts. Numerous studies focus on the effects of such public attention. They indicate that high-visibility firms are more likely to reduce their information asymmetry with stakeholders (Jia & Zhang, Citation2015) due to greater stakeholder scrutiny and monitoring, and greater government intervention than in low visibility firms. Notably, high-visibility firms suffer stronger institutional pressures and expectations from external stakeholders due to their public prominence (Ge & Micelotta, Citation2019; Wang & Qian, Citation2011). Moreover, they are more likely to respond to stakeholder expectations and are increasingly socially responsible (Kim & Oh, Citation2019).

We propose that S.O.E.s and firms located in an institutionally developed region are more likely to engage in C.P.G. when they are visible to external stakeholders. First, new media may disseminate information of high-visibility firms to external stakeholders, thereby increasing their familiarity with corporate philanthropic activities. Meanwhile, attention is a scarce resource that stakeholders may pay more to high-visibility firms, and expect them to engage in more philanthropic activities than low visibility firms. Second, for high-visibility firms, close public scrutiny and monitoring have a profound influence on firms’ decisions (Chiu & Sharfman, Citation2011) by generating greater external pressures on them.

Visible S.O.E.s are more motivated to engage in C.P.G. First, they capture more attention from political stakeholders, and thus are under governmental scrutiny and monitoring. This forces S.O.E.s to positively satisfy governmental expectation. Second, Chinese S.O.E.s often receive favourable treatment from the government. If they fail to meet expectations of political stakeholders, visible S.O.E.s may suffer more than their counterparts because visible S.O.E.s have more advantages in securing available political capital (Gao, Citation2011). In other words, S.O.E.s are more likely to be forced by the government to engage in philanthropic activities to show their leadership and model role in society. By contrast, if high-visibility firms do not engage in C.P.G., then such irresponsible behaviour may signal the aggravation of illegitimacy and cause a significant decline of stock prices (Jia & Zhang, Citation2015; Wang & Qian, Citation2011).Therefore, engaging in C.P.G. for visible S.O.E.s can maintain political legitimacy and ensure that they secure political resources to improve economic efficiency. If not, they would suffer more than invisible counterparts.

In a similar vein, although firms operating in institutionally developed regions have more managerial discretion, they draw more attention, scrutiny, and monitoring from the government and the media or the public, especially when they are visible. As a result, higher visibility of a firm reduces its managerial discretion, and subjects’ managers to perceive higher external pressure to be socially responsible. In a market-oriented institution, economic stakeholders (e.g., supplier, competitor, customer) may be more important than political stakeholders. Firms may benefit more from engaging in C.P.G. under high-visibility than under low visibility. This is because higher visibility to economic stakeholders can magnify the benefit of C.P.G. (Li, Ferguson, Gao & Hafsi, Citation2015). That is, firms have greater motivation to build a good image and reputation by donating more in a market-orientated institution. As a way of responding to external pressures, C.P.G. not only enhances firms’ legitimacy, but also maintains its image and reputation associated with external expectations. The effectiveness of C.P.G. will become higher when firms are more visible to external stakeholders. According to the above discussion, we propose the following hypotheses:

Hypothesis 3a (H3a). The positive relationship between state ownership and C.P.G. is stronger for high-visibility firms.

Hypothesis 3b (H3b). The relationship between institutional development and C.P.G. is less negative for high-visibility firms.

Political ties refer to personal links of the firm with members of state and political parties. These ties are a key component of corporate strategy in different institutional environments. The benefits associated with political ties for the firm have been studied via access to influence, resource, information, and legitimacy (Zhang et al., Citation2016; Zheng et al., Citation2015). First, political ties influence the enactment, interpretation, and implementation of laws, rules, and regulations (Zheng et al., Citation2017). These ties also assist firms to avoid, defy, and manipulate the laws, rules, and regulations or even escapes their enforcement. Second, human and social capitals related to politically connected directors bring firms to actual and potential resources that including individual expertise, experience, skills, and social networks. Third, politically connected directors can provide advice, counsel, and referral to aid strategic plans, information sharing, and resource acquisition by taking advantage of their insight and networks in the state sector. Lastly, firms’ political ties also signal a high level of legitimacy to other stakeholders because these political ties shape spill-over legitimacy and secure the firms’ legitimacy image (Zheng et al., Citation2015). The benefits of political ties may offer different values for the firm depending on the institutional context in which they are embedded. Zhang et al. (Citation2016) believe that the effectiveness of political connections depends on the degree of state monopoly in the firm’s industry or the level of market-oriented institutional development in its location. Given the heterogeneity of external pressures and stakeholder expectations, we further explore how the effectiveness of political ties is impacted by institutional environments such as state ownership and institutional development.

As bridges between businesses and the government, political ties are a key component of corporate political strategy in different institutional environments. In the case of state ownership, most politically connected directors are usually appointed by the central government and agencies to gain control over these firms (Fan & Wang, Citation2018). As government representatives, politically connected directors have a fiduciary duty to fulfil the government's demands and goals. These features help firms build or maintain political legitimacy. Drawing on institution-related literature, we propose that C.P.G. is a legitimacy-seeking activity and that political ties constitute a channel through which institutional pressure is exerted (Ge & Micelotta, Citation2019; Wang & Qian, Citation2011). Meanwhile, considering that S.O.E.s depend on political resources and need legitimacy, we propose that politically connected directors induce S.O.E.s to engage in C.P.G. In turn, such activities not only maintain political legitimacy but also endow firms with costly and rare information, preferential treatment, and critical and valuable resources. This helps improve firm efficiency. For example, Zheng et al. (Citation2015) find evidence that political ties improve firm survival and financial performance using data from the television manufacturing industry. Li et al. (Citation2018) also find that firms depend on political stakeholders to obtain resources and support that enhance their innovation performance. Conversely, politically connected directors can be promoted to high ranks of government institutions if they help the government achieve social and political goals. Therefore, we suggest the following hypothesis:

Hypothesis 4a (H4a). Board political ties strengthen the relationship between state ownership and C.P.G.

The effectiveness of political ties depends on the levels of institutional development (Zheng et al., Citation2015). Such dependency further changes the legitimacy–efficiency trade-offs in different institutional contexts. In underdeveloped institutional contexts, firms are likely to turn to rule-based, impersonal, and market-oriented transactions because the costs of maintaining political ties exceed the benefits. This makes political capital a liability to firms (Sun et al., Citation2012). According to the market efficiency logic, the efficiency of political ties weakens when the market forces play an increasing role in business decisions and outcomes. For example, Sheng et al. (Citation2011) provide evidence that political ties play a less significant role in promoting firm performance compared with business ties because of the improvement of legal institutions and the reduction of market uncertainty. By contrast, the potential social capital embedded in political ties may be more important in imperfect institutional environments as such connections can compensate for institutional voids, gain more valuable resources and governmental support, and then improve firm performance. Chen et al. (Citation2011) find that governmental rent-seeking motivates firms to look for safeguards and legitimacy through political ties in less market-oriented regions. Consequently, in underdeveloped institutional contexts, firms are more likely to view political ties as a competitive strategy to gain critical resources and maintain socio-political legitimacy. Conversely, firms in developed institutional contexts are more likely to rely on business organisations rather than political relationships to improve economic efficiency. Moreover, both the effectiveness of political ties and the motivation of maintaining institutional legitimacy decrease in institutional development contexts because the cost involved not only reduces firm efficiency but also fails to gain valuable resources and supports. Therefore, we suggest the following hypothesis:

Hypothesis 4b (H4b). Board political ties strengthen the relationship between institutional development and C.P.G.

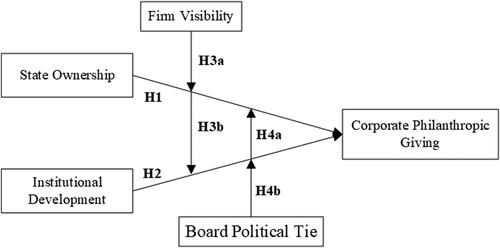

presents the conceptual model regarding state ownership, institutional development, firm visibility, board political tie, and the hypotheses derived from them to predict C.P.G.

Figure 1. The conceptual model.

Source: Derived From H1-H4.

3. Methodology

3.1. Sample and data

This study examines C.P.G. as a legitimacy–efficiency trade-offs in the context of all Chinese publicly firms listed in either the Shanghai or Shenzhen Stock Exchange from 2009 to 2016. We set 2009 as the beginning year to avoid the intervention of natural disasters (such as the Sichuan earthquake) and social events (such as the Beijing Olympics in 2008). After removing observations with missing key values, our final unbalanced samples (several firms were newly listed or delisted during the observation period) consist of 16,674 firm-year observations for 2,840 firms. According to the one-digit Standard Industrial Classification (S.I.C.) code issued by the China Securities Regulatory Commission in 2012, 18 different industries are identified. The distribution of the 2,840 sample firms is as follows: 41 (agriculture), 64 (mining), 1742 (manufacturing), 81 (power), 87 (construction), 165 (wholesale and retail), 102 (transportation), 9 (hotels and catering services), 209 (information service), 52 (finance), 122 (real estate), 47 (leasing and business service), 25 (scientific research and technical services), 40 (public utility), 9 (repair service), 4 (education), 4 (health and social network), and 37 (culture and entertainment). This covers all relevant sectors of firms on Chinese stock exchanges.

C.P.G. data, firm governance characteristics, and financial information are obtained from the China Stock Market & Accounting Research Database (C.S.M.A.R.) database. In our empirical context, two remarkable features are superior to those found in prior C.P.G. studies. First, prior studies are limited to a specific array of firms, such as large-sized and P.O.E.s firms, which likely leads to sample selection bias and limits the generality of their conclusions. By investigating the C.P.G. practices of all publicly listed firms in China over the years, we endeavour to ameliorate the likelihood of sample selection bias. Second, legitimacy–efficiency trade-offs are seen as an enduring and routine practice for firms across industries rather than an ad hoc response to a one-off event. Our observation year starts from 2009 within a specific timeframe to avoid remarkable events, natural disasters, or social events.

3.2. Measurement

3.2.1. Dependent variable

We measure our dependent variable, C.P.G., as the total amount of corporate monetary donation each year. Due to highly skewed values, the log-transformed (+1) dependent variable is used as rectification (Gao & Hafsi, Citation2015; Wang & Qian, Citation2011).

3.2.2. Independent variables

State ownership is a binary variable coded as 1 if the firm is owned by the Chinese government and its agencies, and 0 otherwise. Institutional development in 31 Chinese provinces is evaluated from marketisation indexes compiled by N.E.R.I. (Fan & Wang, Citation2018). This captures the progress of institutional development from various perspectives. A high marketisation index indicates high development of provincial institutions. This index captures province-level institutional development using five factors: (1) government-market relations; (2) share of non-state-owned firms; (3) level of development of product markets; (4) level of development of factor markets; and

(5) level of development of market intermediaries and legal system. These factors have been widely used to measure province-level institutional development (Gao & Hafsi, Citation2015; Wang & Qian, Citation2011; Zhang et al., Citation2016). Therefore, the N.E.R.I. score of every province where a firm headquarters is located is operationalised as the level of institutional development for a focal firm.

3.2.3. Moderators

Following prior research, firm size is utilised as a proxy for firm visibility (Gao, Citation2011). This variable is computed as the natural logarithm of total sales in a financial year. Total sales are used to capture firm visibility because it avoids over-inflating the standard error in the regression, resulting in results being insignificant (Sheng et al., Citation2011). Following previous research on board political ties, we first identify directors who previously acted as or are serving as a member of the central and local government, and the People’s Congress of the People’s Political Consultative Conference. Then, the number of politically connected directors is divided by the total number of board members to gauge the proportion of board political ties. To facilitate the interpretation of regression results, the interaction terms, the marketisation indexes, firm visibility values, and board political ties are standardised.

3.2.4. Control variables

According to extant literature, we control for variables that may influence the C.P.G. decision and our results. Firm-level characteristics suggested by prior studies as determinates of corporate philanthropy are controlled for. We include employee numbers (the natural logarithm of employee numbers) and firm age (the number of years since a firm’s foundation) as larger and established firms may have more resources and be expected to give more donations (Wang & Qian, Citation2011). Firms with high leverage have fewer financial resources to support charities. Leverage is measured as the ratio of total debt to total asset (Gao & Hafsi, Citation2015). By contrast, C.P.G. is more likely in firms with slack resources, which we measure by cash flow over total asset (Zhang et al., Citation2016). A well-performing firm should have more resources to commit to social causes (Wang & Qian, Citation2011). We control for firm profitability as measured by the net operating income (in RMB billion) for each financial year. Previous studies suggest that owners can effectively monitor the donation making-decision under high ownership concentration. This is controlled by the ratio of equity held by the three largest shareholders and state ownership (the proportion of state-owned shares).

3.2.5. Partnering and competing peers

According to the three-digit S.I.C., we first identify 84 different industries and then calculate the total amount of firms for every industry (each firm belongs to only one S.I.C.). We define competing peers as those in the three-digit S.I.C. with the focal firm. The total number of competing firms is used to capture industrial competition. We define the partnering peer network as those listed firms connected through interlocking directorial networks, which among listed firms, are identified as a critical tool to diffuse organisational practices.

Following these definitions, we calculate the average C.P.G. of competing and partnering peers for each year. Competing peers’ average C.P.G. is calculated by the average amount of donations by all firms within the same three-digit S.I.C., excluding the focal firm (the total amount of C.P.G. from donating competing peers/the number of all the focal firm’s competitors) (Gao & Hafsi, Citation2015). Similarly, we measure partnering peers’ average C.P.G. by the average amount of donations by all of the focal firm's partners, excluding the focal firm (the total amount of C.P.G. from donating partnering peers/the number of all the focal firm’s partners). We also control for donating partnering peers, as measured by the number of donating partnering peers over the total number of the focal firms’ partners through director interlocks. Similarly, donating competing peers is measured by the number of donating competing peers over the total number of the focal firms’ competitors at the three-digit S.I.C. level.

Firms occupying a central position in director interlocks enhance their visibility to external audiences. High firm visibility indicates greater pressure due to greater external scrutiny. Therefore, a central firm is likely to exert considerable philanthropic effort. We utilise an eigenvector-based indicator to capture an actor’s centrality (Bonacich, Citation1972) as calculated by using R software (see Bao et al., Citation2019 for details). We control for the focal firm’ centrality, the partnering peers’ average centrality (the sum of all partnering peers’ centrality over the total number of all partnering peers), and the competing peers’ average centrality (the sum of all competing peers’ centrality over the total number of all competing peers).

Board characteristics may likewise influence the effects of governance mechanisms (Lu et al., Citation2016; Saona et al., Citation2020). Thus, we control for board size, percentage of female directors, duality of the chairman and C.E.O., director ownership, and the C.E.O.’s and chairman’s shareholdings. Prior studies (e.g., Williams, Citation2003) suggest that firms with a higher proportion of female directors on their boards are likely to give more. The percentage of female directors is calculated by dividing their number by the total number of directors. We measure board size by the total number of all directors on the firm’s board. By bringing together more knowledge and skills, a larger board size may correlate with effective shareholder management. To use C.E.O. duality as proxy for executive power, we set duality as equal to 1 if the Chairman and C.E.O. is the same person, and 0 otherwise. In considering the abovementioned ownership effect on C.P.G., director ownership, calculated as the percentage of shares held by all directors (Chang et al., Citation2017), is controlled. The C.E.O.’s or chairman’s shareholdings may move their interests to align with those of shareholders and make them more careful in making decisions. Therefore, we separately control for such shareholdings that are measured as the ratio of shares held by these actors to total shares outstanding.

Furthermore, to capture potential industrial heterogeneous effects on corporate philanthropy, 17 industry dummies are included in each model to represent 18 different industry categories as identified by the one-digit S.I.C. In line with the causal sequence implied by our hypotheses, all independent and control variables, except for industry dummy variables, are lagged by one year. The common practice of a lagged dependent variable is utilised in addressing the pooled time-series and cross-sectional panel data, and thus ameliorates concerns on reverse causality.

3.2.6. Analysis

Tobit regression model is an appropriate method for C.P.G. amount. When dependent variables are limited, O.L.S. will not yield consistent estimates. To alleviate this problem, the Tobit model is employed in this study (Tobin, Citation1958). By specifying the left-censoring of C.P.G. at zero and firm-fixed effects, Tobit regression is preferred in our context to address the concern that firms that never donated during the observation period are substantially distinctive from those that donated during the same period (Lu et al., Citation2016).

4. Results

presents the descriptive statistics and correlations for all variables. In our sample, the average C.P.G. is RMB 4,819,591 (USD 713,823 according to the 2017 average exchange rate at RMB 6.7518 to USD 1). This amount represents a significant increase compared with RMB 860,000 reported in Li et al. (Citation2015). The results in preliminarily indicate that C.P.G. is significantly associated with state ownership, total sales, and board political ties at the 1% level, except for the marketisation index. This suggests a need to examine the interactions among these variables with C.P.G. Most control variables are also significantly correlated with C.P.G.. Among them, ‘female director’ has a mean value of 0.13, suggesting that approximately 13% of all observed firms have female directors on the board. The mean value of share percentage of three largest shareholders and the proportion of state ownership are 0.48 and 0.05, respectively. This indicates that Chinese listed firms have concentrated ownership structures, and approximately 5% of them are government controlled. The mean value of donating partner ratio, donating competitor ratio, partner average C.P.G., and competitor average C.P.G. are low, suggesting that only a few partners or competitors make some donation. The variance inflation factor (V.I.F.) procedure is used to test for potential multicollinearity problems. All V.I.F. values among models are below the rule-of-thumb threshold of 5 with a maximum value of 3.3. Thus, multicollinearity is not an issue. presents the results of the Tobit regression predicting C.P.G. Model 1 includes only the control variables to represent the baseline model. Models 2–6 include independent variables, moderators, and interaction items, respectively. Model 7 represents the full model.

Table 1. Descriptive statistics and correlations.

Table 2. Result of regression predicting C.P.G.

Regarding control variables, firms with large sizes, good performance, high ratios of donating partnering peers, and healthy cash flow tend to engage in considerable C.P.G. This demonstrates that firm performance is a significant predictor of C.P.G, and supports the findings of prior studies. Thus, when facing high-efficiency pressures, poor-performing firms are reluctant to allocate their limited attention and resources to philanthropic initiatives. By contrast, established firms are less likely to donate more possibly because established firms have taken years to obtain legitimate advantages. Thus, they experience less dual pressure from legitimacy and efficiency relative to young firms. Industrial competition density negatively correlates with C.P.G., thereby suggesting that firms with numerous competitors face highly competitive pressure and have fewer resources to support charities.

The proportion of donating partnering peers among the firm’s partners is significantly and positively related to C.P.G.. Thus, a high proportion of donating partnering peers indicates the considerable experience of focal firm’s social legitimacy and large donations. However, the effect of partnering peers’ average C.P.G. on the focal firm’ C.P.G. is marginally significant and negative (Marquis & Tilcsik, Citation2016). Taken together, the results suggest that by facing social legitimacy pressure from donating partners, focal firms would decide to donate but at an acceptable level rather than too much without significant loss of efficiency. Tension inevitably exists between efficiency and legitimacy (Jeong & Kim, Citation2019). By contrast, both proportion of donating competing peers and competing peers’ average C.P.G. correlate insignificantly with a focal firm’s C.P.G. Only one firm governance control (namely, chairman shareholdings) is significantly negative in any of the models, and other governance controls are either not always significant or are insignificant.

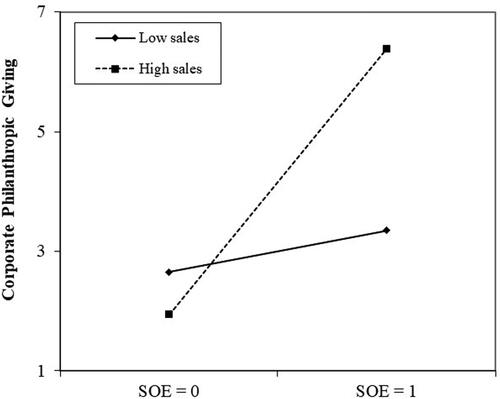

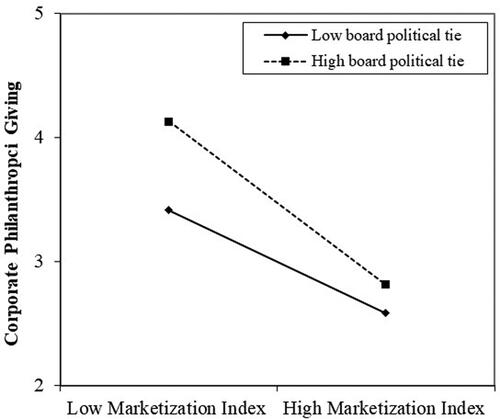

Model 2 provides significant evidence to support H1 and H2. A statistically significantly positive relationship is found between S.O.E. and C.P.G. A negative relationship exists between institutional development and C.P.G. This result lends support to H1 and H2. Models 3 and 4 are similar to Model 2 but show firm visibility and its interactions with S.O.E. and the marketisation index, respectively. According to H3, with high firm visibility, C.P.G. exhibits a stronger relationship with S.O.E. but a weaker relationship with the marketisation index. The results from Model 3 are consistent with H3a, and the interaction effect is plotted in (Aiken & West, Citation1991). Thus, consistent with H3a, the high-visibility of S.O.E.s results in more donations. However, Model 4 results do not support H3b. Models 5 and 6 test the moderating effect of board political ties on the relationship between S.O.E., marketisation index, and C.P.G. Contradictory to our prediction, Model 5 reveals that the interaction between state ownership and board political tie is statistically negative, and thus is not supportive of H4b. the possible reason is that both state ownership and board political tie play similar role for the firm, and thus are substitutes for each other. Consistent with our prediction, Model 6 shows that the coefficient on the interaction between marketisation index and board political tie is negative and statistically significant. This indicates that a politically connected firm operating in a more developed institution setting is less likely to give more donations. illustrates this relationship.

Figure 2. Interactive effect between state ownership and firm visibility on C.P.G.

Source: Authors' calculation based on Model 3 in .

Figure 3. Interactive effect between marketization index and board political tie on C.P.G.

Source: Authors' calculation based on Model 6 in

4.1. Robustness check

We conduct several supplementary tests to probe the robustness of our results and evaluate potentially meaningful relationships that are not formally hypothesised but may inform future research. First, following recent suggestions (Bernerth & Aguinis, Citation2016), we analyse our models by excluding control variables. The results are robust, thereby suggesting that our conclusion is unduly driven by control variables. Second, in place of the S.O.E. dummy to indicate whether a firm was an S.O.E., we treat state ownership as a continuous variable and measure the percentage of stakes owned by the government. We also measure our dependent variable by a firm’s giving as the ratio of its corporate giving to its sales. The two measures generate consistent results. Third, we also regress the models with different levels clustered, including the firm, province, and year levels, to similar results as those in .

5. Discussion and conclusion

This study examines the question of how much a firm spends to manage external legitimacy in the context of C.P.G. where high pressures for normative legitimacy exist. However, this giving comes at a cost to seek external legitimacy. We argue that firms strategically manage corporate giving while considering the trade-offs between social legitimacy and economic efficiency. This study is a modest step towards developing a theoretically sound interpretation for managing this tension. Its implications will be beneficial to both scholars and practitioners.

Previous studies indicate that P.O.E.s are more likely to donate than S.O.E.s (Su & He, Citation2010), highlighting the opportunity to display their social conscience. In emerging economies, compared to economic stakeholders, political stakeholders pose more powerful effect on firms’ action (Li et al., Citation2018). S.O.E.s have privileged access to state resources compared with their non-S.O.E. counterparts, and can be pressured to meet government expectation. In other words, S.O.E.s may risk losing political privileges if they fail to meet government expectation. Conversely, P.O.E.s have little privileges per se, and thus may not be under pressure to meet government expectations. In short, considering the significant costs of losing political capital in an emerging country, S.O.E.s may be more likely than P.O.E.s to perceive the costs and risk of failing to comply with expectations of political stakeholders (Gao, Citation2011). Therefore, S.O.E.s are more likely to conduct corporate philanthropy.

5.1. Theoretical implications

Our findings provide novel insights into the role of institutional elements and firm characteristics on the legitimacy–efficiency trade-offs and contribute to extant literature in three ways. First, this study expands the current research on legitimacy and efficiency in the context of C.P.G. Both arguments have been well-documented but concerns on how legitimacy-seeking affects economic efficiency and how to balance them have been underexplored (Jeong & Kim, Citation2019). Seeking legitimacy at a reasonable cost threatens corporate efficiency. Yet, established legitimacy can translate into institutional capital that adds to firm efficiency (Yang & Su, Citation2013). In this regard, the present study contributes to our knowledge through an integrative scheme or framework that unifies fragmented observations and reveals the related aspects of C.P.G.

Second, we offer a new framework of institutional elements and firm characteristics to explain the implications of C.P.G. on legitimacy–efficiency trade-offs. As our findings show, state ownership enables firms to prioritise institutional legitimacy rather than economic efficiency. Institutional development enables firms to prioritise economic efficiency rather than institutional legitimacy. However, on its own, institutional elements cannot tell the entire story of legitimacy–efficiency trade-offs, which firm characteristics likewise affect. By considering this joint effect, our framework offers a more complete understanding of their roles on C.P.G. and helps reconcile existing contradictory legitimacy and efficiency perspectives.

Third, this study contributes to the literature on the role of visibility and political ties in understanding legitimacy–efficiency trade-offs. An organisation is often assumed to submit itself to institutional pressures to become a legitimised member. However, the extent to which an organisation responds to institutional pressures can change as a function of firm characteristics. These characteristics can change a firm’s vulnerability to institutional pressures or its ability to defuse such pressures. To improve our understanding of the variation in the response of firms to institutional pressures, we investigate how firm-level factors influence the relationship between institutional pressure and organisational practices. Our findings suggest that visibility and political ties explain why certain firms respond more than others for legitimacy, and exhibit both different dynamic adjustments between legitimacy and economic efficiency.

5.2. Managerial implications

Our findings offer important practical guidance for managers who must understand both external pressure and their own firm’s characteristics. First, few firms have sufficient resources to simultaneously tackle legitimacy and economic efficiency pressures, thereby suggesting that considerable tension exists between legitimacy and efficiency. In such scenarios, managers must design sets of priority rules to determine which challenges should be prioritised. Second, we suggest that when facing severe institutional pressures, firms should address immediate legitimacy challenge (Peng, Citation2003). Obtaining external legitimacy is critical for an organisation’s survival and performance (Oliver, Citation1997). Failure to do so may lead to serious social and economic consequences due to illegitimacy penalties (Zuckerman, Citation1999). Legitimacy often has a higher priority. Economic efficiency typically follows from social acceptance. Third, firms need not always submit themselves to institutional pressure. The extent to which firms meet social expectations vary with their capabilities, which may change its vulnerability to or even defuse institutional pressures. Therefore, we suggest that a firm’s own characteristics can be a vital contingency factor in determining their response to legitimacy and efficiency. Managers are advised to fully consider both institutional aspects and their firm's characteristics to effectively orchestrate their efforts in legitimacy versus efficiency of C.P.G.

5.3. Limitation and further research

The present results need to be explained considering the following limitations. First, institutional literature suggests that conforming to institutional pressures does not always entail a cost (Jeong & Kim, Citation2019; Oliver, Citation1997). In several situations, organisations also obtain expected legitimacy by symbolically adopting but not implementing institutionalised practices. Without a significant loss of economic efficiency, both legitimacy and efficiency can be simultaneously achieved. Therefore, the tension between them may become less salient for organisations. Future research can delineate when and how legitimacy–efficiency trade-offs play a role in determining the symbolical adoption and/or implementation of institutionalised practices. Second, we focus only on the role of state ownership. However, ownership structures in China are quite complex (Zhou et al., Citation2017). Further research could identify the differences and similarities among different ownership structures. Third, the sample may limit the generalisability of our findings. In China, the government plays a strong role in guiding firm behaviour. Institutional environments in emerging economies are constantly changing. Additional tests are necessary in other emerging and developed economies to examine the robustness of our findings.

Disclosure statement

The authors have no competing interests do declare.

Additional information

Funding

References

- Aiken, L. S., & West, S. G. (1991). Multiple regression: Testing and interpreting interactions. SAGE.

- Bao, F., Zhao, Y., Tian, L., & Li, Y. (2019). From financial misdemeanants to recidivists: The perspective of social networks. Management and Organization Review, 15(4), 809–827. https://doi.org/https://doi.org/10.1017/mor.2019.13

- Bernerth, J. B., & Aguinis, H. (2016). A critical review and best-practice recommendations for control variable usage. Personnel Psychology, 69(1), 229–283. https://doi.org/https://doi.org/10.1111/peps.12103

- Bonacich, P. (1972). Factoring and weighting approaches to status scores and clique identification. The Journal of Mathematical Sociology, 2(1), 113–120. https://doi.org/https://doi.org/10.1080/0022250X.1972.9989806

- Chang, Y. K., Oh, W. Y., Park, J. H., & Jang, M. G. (2017). Exploring the relationship between board characteristics and CSR: Empirical evidence from Korea. Journal of Business Ethics, 140(2), 225–242. https://doi.org/https://doi.org/10.1007/s10551-015-2651-z

- Chen, C. J., Li, Z., Su, X., & Sun, Z. (2011). Rent-seeking incentives, corporate political connections, and the control structure of private firms: Chinese evidence. Journal of Corporate Finance, 17(2), 229–243. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2010.09.009

- Chiu, S. C., & Sharfman, M. (2011). Legitimacy, visibility, and the antecedents of corporate social performance: An investigation of the instrumental perspective. Journal of Management, 37(6), 1558–1585. https://doi.org/https://doi.org/10.1177/0149206309347958

- Cuervo-Cazurra, A., Inkpen, A., Musacchio, A., & Ramaswamy, K. (2014). Governments as owners: State-owned multinational companies. Journal of International Business Studies, 45(8), 919–942. https://doi.org/https://doi.org/10.1057/jibs.2014.43

- Cui, L., & Jiang, F. (2012). State ownership effect on firms' FDI ownership decisions under institutional pressure: A study of Chinese outward-investing firms. Journal of International Business Studies, 43(3), 264–284. https://doi.org/https://doi.org/10.1057/jibs.2012.1

- Fan, G., & Wang, X. L. (2018). Marketization index of China’s provinces. Economic Science Press.

- Gao, Y. (2011). Philanthropic disaster relief giving as a response to institutional pressure: Evidence from China. Journal of Business Research, 64(12), 1377–1382. https://doi.org/https://doi.org/10.1016/j.jbusres.2010.12.003

- Gao, Y., & Hafsi, T. (2015). Government intervention, peers’ giving and corporate philanthropy: Evidence from Chinese private SMEs. Journal of Business Ethics, 132(2), 433–447. https://doi.org/https://doi.org/10.1007/s10551-014-2329-y

- Ge, J., & Micelotta, E. (2019). When does the family matter? Institutional pressures and corporate philanthropy in China. Organization Studies, 40(6), 833–857. https://doi.org/https://doi.org/10.1177/0170840619836709

- Jeong, Y. C., & Kim, T. Y. (2019). Between legitimacy and efficiency: An institutional theory of corporate giving. Academy of Management Journal, 62(5), 1583–1608. https://doi.org/https://doi.org/10.5465/amj.2016.0575

- Jia, N. (2018). The “make and/or buy” decisions of corporate political lobbying: Integrating the economic efficiency and legitimacy perspectives. Academy of Management Review, 43(2), 307–326. https://doi.org/https://doi.org/10.5465/amr.2016.0148

- Jia, M., & Zhang, Z. (2015). News visibility and corporate philanthropic response: Evidence from privately owned Chinese firms following the Wenchuan earthquake. Journal of Business Ethics, 129(1), 93–114. https://doi.org/https://doi.org/10.1007/s10551-014-2150-7

- Kim, W. S., & Oh, S. (2019). Corporate social responsibility, business groups and financial performance: A study of listed Indian firms. Economic research-Ekonomska Istraživanja, 32(1), 1777–1793. https://doi.org/https://doi.org/10.1080/1331677X.2019.1637764

- Lev, B., Petrovits, C., & Radhakrishnan, S. (2009). Is doing good for you? How corporate charitable contributions enhance revenue growth. Strategic Management Journal, 31(2), n/a–200. https://doi.org/https://doi.org/10.1002/smj.810

- Liang, H., Ren, B., & Sun, S. L. (2015). An anatomy of state control in the globalization of state-owned enterprises. Journal of International Business Studies, 46(2), 223–240. https://doi.org/https://doi.org/10.1057/jibs.2014.35

- Li, Y., Ferguson, J., Gao, Y., & Hafsi, T. (2015). Competition in corporate philanthropic disaster giving. Chinese Management Studies, 9(3), 311–332. https://doi.org/https://doi.org/10.1108/CMS-06-2014-0112

- Li, S., Song, X., & Wu, H. (2015). Political connection, ownership structure, and corporate philanthropy in China: A strategic-political perspective. Journal of Business Ethics, 129(2), 399–411. https://doi.org/https://doi.org/10.1007/s10551-014-2167-y

- Li, J., Xia, J., & Zajac, E. J. (2018). On the duality of political and economic stakeholder influence on firm innovation performance: Theory and evidence from Chinese firms. Strategic Management Journal, 39(1), 193–216. https://doi.org/https://doi.org/10.1002/smj.2697

- Lu, Y., Shailer, G., & Wilson, M. (2016). Corporate political donations: Influences from directors’ networks. Journal of Business Ethics, 135(3), 461–481. https://doi.org/https://doi.org/10.1007/s10551-014-2458-3

- Marquis, C., & Qian, C. (2014). Corporate social responsibility reporting in China: Symbol or substance? Organization Science, 25(1), 127–148. https://doi.org/https://doi.org/10.1287/orsc.2013.0837

- Marquis, C., & Tilcsik, A. (2016). Institutional equivalence: How industry and community peers influence corporate philanthropy. Organization Science, 27(5), 1325–1341. https://doi.org/https://doi.org/10.1287/orsc.2016.1083

- Meyer, K. E., Ding, Y., Li, J., & Zhang, H. (2014). Overcoming distrust: How state-owned enterprises adapt their foreign entries to institutional pressures abroad. Journal of International Business Studies, 45(8), 1005–1028. https://doi.org/https://doi.org/10.1057/jibs.2014.15

- Nason, R. S., Bacq, S., & Gras, D. (2018). A behavioral theory of social performance: Social identity and stakeholder expectations. Academy of Management Review, 43(2), 259–283. https://doi.org/https://doi.org/10.5465/amr.2015.0081

- Oliver, C. (1997). Sustainable competitive advantage: Combining institutional and resource-based views. Strategic Management Journal, 18(9), 697–713. https://doi.org/https://doi.org/10.1002/(SICI)1097-0266(199710)18:9<697::AID-SMJ909>3.0.CO;2-C

- Peng, M. W. (2003). Institutional transitions and strategic choices. Academy of Management Review, 28(2), 275–296. https://doi.org/https://doi.org/10.5465/amr.2003.9416341

- Peteraf, M., & Reed, R. (2007). Managerial discretion and internal alignment under regulatory constraints and change. Strategic Management Journal, 28(11), 1089–1112. https://doi.org/https://doi.org/10.1002/smj.628

- Saona, P., Muro, L., San Martín, P., & Cid, C. (2020). Ibero-American corporate ownership and boards of directors: Implementation and impact on firm value in Chile and Spain. Economic Research-Ekonomska Istraživanja, 33(1), 2133–2138. https://doi.org/https://doi.org/10.1080/1331677X.2019.1694558

- Schilke, O. (2018). A micro-institutional inquiry into resistance to environmental pressures. Academy of Management Journal, 61(4), 1431–1466. https://doi.org/https://doi.org/10.5465/amj.2016.0762

- Sheng, S., Zhou, K. Z., & Li, J. J. (2011). The effects of business and political ties on firm performance: Evidence from China. Journal of Marketing, 75(1), 1–15. https://doi.org/https://doi.org/10.1509/jm.75.1.1

- Su, J., & He, J. (2010). Does giving lead to getting? Evidence from Chinese private enterprises. Journal of Business Ethics, 93(1), 73–90. https://doi.org/https://doi.org/10.1007/s10551-009-0183-0

- Sun, P., Mellahi, K., & Wright, M. (2012). The contingent value of corporate political ties. Academy of Management Perspectives, 26(3), 68–82. https://doi.org/https://doi.org/10.5465/amp.2011.0164

- Tobin, J. (1958). Estimation of relationships for limited dependent variables. Econometrica, 26(1), 24–36. https://doi.org/https://doi.org/10.2307/1907382

- Wang, D., & Luo, X. R. (2019). Retire in peace: Officials’ political incentives and corporate diversification in China. Administrative Science Quarterly, 64(4), 737–777. https://doi.org/https://doi.org/10.1177/0001839218786263

- Wang, H., & Qian, C. (2011). Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Academy of Management Journal, 54(6), 1159–1181. https://doi.org/https://doi.org/10.5465/amj.2009.0548

- Williams, R. J. (2003). Women on corporate boards of directors and their influence on corporate philanthropy. Journal of Business Ethics, 42(1), 1–10. https://doi.org/https://doi.org/10.1023/A:1021626024014

- Yang, Z., & Su, C. (2013). Understanding Asian business strategy: Modelling institution-based legitimacy-embedded efficiency. Journal of Business Research, 66(12), 2369–2374. https://doi.org/https://doi.org/10.1016/j.jbusres.2013.05.022

- Zhang, J., Marquis, C., & Qiao, K. (2016). Do political connections buffer firms from or bind firms to the government? A study of corporate charitable donations of Chinese firms. Organization Science, 27(5), 1307–1324. https://doi.org/https://doi.org/10.1287/orsc.2016.1084

- Zhang, J., Zhou, C., & Ebbers, H. (2011). Completion of Chinese overseas acquisitions: Institutional perspectives and evidence. International Business Review, 20(2), 226–238. https://doi.org/https://doi.org/10.1016/j.ibusrev.2010.07.003

- Zheng, W., Singh, K., & Chung, C. N. (2017). Ties to unbind: Political ties and firm sell-offs during institutional transition. Journal of Management, 43(7), 2005–2036. https://doi.org/https://doi.org/10.1177/0149206315575553

- Zheng, W., Singh, K., & Mitchell, W. (2015). Buffering and enabling: The impact of interlocking political ties on firm survival and sales growth. Strategic Management Journal, 36(11), 1615–1636. https://doi.org/https://doi.org/10.1002/smj.2301

- Zhou, K. Z., Gao, G. Y., & Zhao, H. (2017). State ownership and firm innovation in China: An integrated view of institutional and efficiency logics. Administrative Science Quarterly, 62(2), 375–404. https://doi.org/https://doi.org/10.1177/0001839216674457

- Zuckerman, E. W. (1999). The categorical imperative: Securities analysts and the illegitimacy discount. American Journal of Sociology, 104(5), 1398–1438. https://doi.org/https://doi.org/10.1086/210178