Abstract

This paper investigates the collective impact of financial literacy and inclusion on individuals’ financial capability focusing on the mediating role of financial behaviour. The research is conducted on an individual-level survey. The relationships were examined by using PLS-SEM. Financial capability can be improved by increasing individuals’ financial knowledge, financial behaviour and promoting their inclusion in financial services. Furthermore, the indirect effect of financial knowledge and attitude on financial capability is found to be significant, highlighting the importance of financial behaviour. The results assist policymakers and industry leaders in understanding the most influential factors on financial capability in the context of a post-communist transition country. This enables them to design policies and services aimed at equipping citizens with knowledge and skills to make best use of their financial resources.

1. Introduction

The government, continuously strive for providing a congenial environment for people to understand the complexities of their finance, take the right financial decisions, and plan their retirement and other financial goals wisely. To do so, people must develop a desirable financial attitude, knowledge, and behaviour. In recent studies, it is also brought into the notice that the intention of promoting financial literacy and all the related efforts through regulations, policies, plans, and business practices must cause helping individuals to enhance their financial capabilities (Hira, Citation2012). It is readily noted that financial literacy is a widely used terminology (Bongini et al., Citation2018; Hensley, Citation2015), but recently, a new notion has been getting buzz, i.e. financial capability (Hira, Citation2012). This is supported by the OECD (Citation2015) report which shows that Europeans often lack financial awareness and skills. Recently, emerging studies highlighting the increasing comparison between financial literacy and financial capability, and financial capability is becoming a wider notion than financial literacy (Johnson & Sherraden, Citation2007). A recent focus is turning attention towards financial capability measurement. There is scope to expand related studies to compare and establish the rationale behind financial capability advent (Kempson et al., Citation2013; Luukkanen & Uusitalo, Citation2019; Santini et al., Citation2019).

The present paper has adopted only such definition out of many where financial literacy is inclusive of financial attitude, financial knowledge, and financial behaviour as this concept is widely used in the collected works (Huston, Citation2010). Financial literacy is people’s capability to process economic facts and figures so they can make cognizant decisions about financial planning, wealth build-up, annuities, and debt management (Lusardi & Mitchell, Citation2014). A report from OECD (Citation2013) defines financial literacy as a mixture of skill, behaviour, awareness, attitude, and knowledge, which are essential for sound financial decisions making for an individual to achieve the state of financial well-being. Many scholars and experts stated that financial literacy is inclusive of the three components: financial attitude, financial knowledge, and financial behaviour (Atkinson & Messy, Citation2012; Garg & Singh, Citation2018; Huston, Citation2010; Potrich et al., Citation2015; Santini et al., Citation2019). Thus, the above expositions expressed that financial literacy covered three broad concepts: financial attitude, financial knowledge, and financial behaviour.

The question is how financial literacy is related to financial capability. The financial capability concept was introduced in 2006 (Atkinson et al., Citation2006). Few experts advocated that financial literacy is a helpful but not a sufficient idea. Financial literacy is about the ability to act but cannot include the opportunity to act (Despard & Chowa, Citation2014; Johnson & Sherraden, Citation2007). In recent years, the significance of promoting financial capability has been on the rise (Loke et al., Citation2015; Luukkanen & Uusitalo, Citation2019). Financial literacy includes the ability to act, and financial inclusion means the opportunity to act, and both together develop financial capability (Sherraden, Citation2013). Financial capability has been introduced to broaden the concept compared to the thin idea of financial literacy (Kempson et al., Citation2013), comprising both ability and opportunity. If an individual gains skills and knowledge but does not use or apply it in practical decision making, it is termed as incapable (Piotrowska, Citation2019; Vlaev & Elliott, Citation2017). Financially capable people must have both the ability and the opportunity to improve their financial well-being by making prudent financial decisions and actions. Here financial literacy fails as it does not cover the external factor i.e. financial inclusion and, it is the major component for financial capability (Johnson & Sherraden, Citation2007; Sherraden, Citation2013). Financial capability covers both the components, financial literacy plus external opportunity through financial inclusion. Thus, financial capability comprises knowledge development and access to financial services (Loke et al., Citation2015). In recent times, policymakers have been making stronger calls to increase financial capacity (Batty et al., Citation2015).

Scholars have found that financial knowledge affects financial management performances and behaviours, and higher financial knowledge able consumers have better financial behaviour (Hilgert et al., Citation2003; Mitchell & Lusardi, Citation2011; Nguyen & Rozsa, Citation2019). On the other side, it was also found that money attitudes and its usage differs as per the consumers’ financial goals (Shih & Ke, Citation2014) and attitudes towards money management effect financial behaviour (Henchoz et al., Citation2019). Another study stated that the most people who have comparatively higher knowledge and attitude reflect better in behaviour (Fessler et al., Citation2019). The financial literacy and financial inclusion aim is to improve financial capability of youth (Despard & Chowa, Citation2014), and not only the ability to act but the opportunity to act together affects financial capability (Johnson & Sherraden, Citation2007). Several studies found that financial attitude and knowledge are the antecedents of financial behaviour (Hayhoe et al., Citation2005; Potrich et al., Citation2016; Yong et al., Citation2018) and financial capability is the descendent of financial behaviour as improved behaviours boost financial capability (Batty et al., Citation2015). Considering all the above-discussed literature reveals that financial behaviour plays a significant mediating role with the two mentioned variables, the same is the reason for considering financial behaviour as a core element of the conceptual framework. This is the driving motivation to conduct the current study. Hence, the objective of the paper is to answer three research questions: (1) Do financial attitude and knowledge directly influence financial behaviour in the context of a post-communist transition country? (2) Do financial literacy dimensions and financial inclusion directly influence financial capability? (3) Does financial behaviour mediates the influences of financial attitude and financial knowledge on financial capability?

Economic, social and political reforms started flooding since, the early 1990s in Albanian and changing the whole picture of the financial market, consumers, products, and services constantly. Considering the dual aim of the Albanian government, first is to improve people financial education to boost financial market development and growth and second, aligning the country’s financial system and the level of financial literacy to become the member of European Union, as these are pre-requisite to joining the European Union (European Commission, Citation2016). To the best of the authors’ knowledge, no study has covered, specifically, relationships between financial attitude, financial knowledge, and financial capability with financial behaviour as a mediator. Outcomes of the study are likely to help policymakers to develop financial education programs to improve the behaviour of individuals to enhance financial capability for their well-being. Thus, the originality of the current research focuses on: (1) Direct and indirect effect of financial attitude and financial knowledge on financial capability; (2) analysing the mediating role of financial behaviour in the framework of financial capability, and (3) the direct impact of financial inclusion on financial capability. This research seeks to address the above-mentioned research gaps. The present paper examines how identified factors influence the individuals’ financial capability and the mediating role of financial behaviour at individual levels.

2. Theoretical background and hypotheses

The current study retrieved the support from three perspectives: Sen’s (Citation1993) capability theory, Bandura’s (Citation1977) self-efficacy theory, and Berzonsky’s (Citation1989) identity processing style. The capability approach contains functioning and capabilities at the individual level. Functioning is about what individuals do (e.g. making prudent financial decisions) and what they are (e.g. are they financially literate?). Individuals’ financial literacy is grounded in these functioning. The capability is a derivative concept and reflects the various functioning an individual might achieve and it involves the individuals’ choice. So, capabilities are about the set of choices an individual makes to achieve a set goal to be a financially capable individual (Clark, Citation2005). The focus of the current study advocates financial capability, as it is a state of being financially capable to protect individuals from current and future financial instability to acquire financial freedom. Bandura’s (Citation1977) self-efficacy theory refers to individuals’ assessment of their capacity to attain the desired financial behaviour and to achieve financial capability through financial knowledge, financial attitude, and financial inclusion (Danes & Haberman, Citation2007). This study will also relate to the identity development process (Berzonsky, Citation1989). In context of current study, the financial identification development process includes financial attitude, knowledge, and behaviour within the framework of financial capability (Shim et al., Citation2013).

Financial behaviour is a key element of financial literacy (Atkinson & Messy, Citation2012; Lusardi & Mitchell, Citation2014; Potrich et al., Citation2015; Shkvarchuk & Slav’yuk, Citation2019), and financial attitude precedes financial behaviour (Potrich et al., Citation2016; Yong et al., Citation2018). It was found that an attitude is a crucial term to comprehend behaviour (Ajzen, Citation1991). Various studies have explored that FAs play a significant role in shaping a person’s financial behaviour (Serido et al., Citation2013; Shih & Ke, Citation2014). Moreover, attitudes have a substantial influence on financial decision making also, as financial attitudes are significantly related to financial management behaviour (Yap et al., Citation2018). It was also found that attitudes and behaviours are related to each other (Joo & Grable, Citation2004), and attitude envisages behaviour (Sample & Warland, Citation1973). Financial attitudes are established through economic and non-economic beliefs held by an individual on the results of certain behaviour and it is a vital factor in the individual decision-making process (Ajzen, Citation1991; Potrich et al., Citation2015). Thus,

H1: Financial attitude positively affects financial behaviour.

Financial knowledge denotes the basic understanding of financial concepts (Huston, Citation2010) as financial knowledge helps individuals to manage their financial challenges in better ways to ensure their financial stability and growth (Hilgert et al., Citation2003). Financial knowledge is associated with financial behaviour (Civelek et al., Citation2019; Kalmi, Citation2018; Moreland, Citation2018) both for the long term and short term (K. T. Kim et al., Citation2019) because people with the high level of education and study related to business have a positive relationship with the probability of regular personal saving (Belás et al., Citation2016; Nguyen et al., Citation2017). Another study showed that financial knowledge impacts borrowing, saving, and investment, all those similar kinds of financial decisions and behaviour (Lusardi & Mitchell, Citation2014). This reveals that higher financial knowledge leads to improved retirement planning and investments in financial products successfully as well (Mitchell & Lusardi, Citation2011; Robb & Woodyard, Citation2011). Also, evidence showed a strong link between an individual’s financial knowledge and financial practices, it enables them to schedule their payment obligations, keeping funds for emergencies, making prudent investment and setting financial goals (Chu et al., Citation2017). The above arguments lead to:

H2: Individuals’ financial behaviour is positively influenced by financial knowledge.

Financial behaviour is a very important factor that shapes financial capability (Potocki & Cierpiał-Wolan, Citation2019; Xiao, Chen, et al., Citation2014). Higher financial capability is associated with favourable and less risky financial behaviours. financial capability has both individual and structural elements that combine the individual’s ability to act and the opportunity to act, i.e. financial inclusion (Johnson & Sherraden, Citation2007). Financial capability can be measured through financial behaviours (Mitchell & Lusardi, Citation2011), and it is also stated that financial behaviour is one of the important factors of financial capability (Xiao, Chen, et al., Citation2014). Financial capability refers to the application of financial knowledge underpinned by desirable financial behaviours to attain financial well-being (Potocki & Cierpiał-Wolan, Citation2019; Xiao, Chen, et al., Citation2014). Hence, a new hypothesis is proposed as:

H3: Financial behaviour positively affects financial capability.

Attitude expresses implicit beliefs that can affect behavioural intents (Ajzen, Citation1991). In the financial context, attitude can be elucidated as an opinion and a mind-set about how an individual manages financial affairs and make financial decisions (Arifin, Citation2018). Attitude is about confidence to take suitable financial decisions, and it influences an individual’s financial capability (Shim et al., Citation2013). Improved attitudes boost financial capability (Batty et al., Citation2015). If a person can make sound financial decisions, it can be termed as financially capable. Considering the above discussion, the following hypothesis can be formulated:

H4: Individuals’ financial capability is positively influenced by financial attitude.

Attitude precedes individuals’ behaviour (Ajzen, Citation1991; Yong et al., Citation2018). Numerous studies indicated that attitude reflects prognostic relations with behaviour (Hira, Citation2012), show a direct and positive relationship. On the other side, financial behaviour impacts financial capability. financial behaviour is one of the most significant factors that shape the level of financial capability (Potocki & Cierpiał-Wolan, Citation2019; Xiao, Chen, et al., Citation2014). As financial behaviour succeeds financial attitude and precedes financial capability, therefore financial behaviour falls between financial attitude and financial capability. It highlights that attitude results in behaviour and behaviour results capability; therefore, financial behaviour has a mediator role between attitude and capability. Thus, to address this gap in the research literature, the following hypothesis has been framed:

H4a: The effect of financial attitude on financial capability is mediated by financial behaviour.

Financial knowledge is explained as an individual’s understanding of micro, macroeconomics, and personal finance (Atlas et al., Citation2019; Rothwell et al., Citation2016). A person’s knowledge of financial markets and systems is an essential component of financial capability (Lusardi & Mitchell, Citation2014). As mentioned earlier, financial knowledge is one of the major components of financial literacy, which has to be studied individually to bring out specific effects of financial knowledge on financial capability (Rothwell et al., Citation2016), because the focus has shifted towards financial capability among consumers (Atkinson et al., Citation2006). Learning financial concepts are associated with improved attitudes and behaviours, and if they persist, it may result in enhanced financial capability (Batty et al., Citation2015). Individuals who possess less education, are more likely to showcase behaviours correlated with low financial capability, therefore increasing financial knowledge is the base for improving financial capability. Financial knowledge positively impacts future financial capability, but currently does not have enough support in the literature (Batty et al., Citation2015) and this is the new insight to look into. Thus, another relationship to test is:

H5: Financial knowledge positively affects financial capability.

It is assumed that financial knowledge’s effect on financial capability is not only direct but also indirect via financial behaviour. Scholars have asserted that higher financial knowledge is a way to promote better financial behaviours (Hilgert et al., Citation2003; Hira, Citation2012; Huston, Citation2010; Potrich et al., Citation2016). Lesser financial knowledge has higher chances of experiencing problems in debt management (Lusardi & Tufano, Citation2015), and higher financial knowledge is more likely to hold emergency savings compared to those with lower levels of financial knowledge (Babiarz & Robb, Citation2014). Higher knowledge results in better financial behaviour which in return can enhance higher financial capability and control, with higher capability an individual can plan financial commitments, better financial planning and cash flows in much better ways. As mentioned earlier, financial behaviour is a core element that shapes the level of financial capability (Potocki & Cierpiał-Wolan, Citation2019), and financial knowledge precedes financial behaviour (Hayhoe et al., Citation2005; Potrich et al., Citation2016; Yong et al., Citation2018). Learning financial topics can improve attitudes and behaviours, and in the long run, it can enhance financial capability (Batty et al., Citation2015). Consequently, financial behaviour succeeds financial knowledge and precedes financial capability, so financial behaviour falls between financial knowledge and financial capability. Hence, a gap has been identified regarding the mediate role of financial behaviour on the relationship between financial knowledge and financial capability. Thus, a new hypothesis can be formulated:

H5a: The effect of financial knowledge on financial capability is mediated by financial behaviour.

Financial capability is also about the opportunity to act, referred to as financial inclusion (external capabilities) (Johnson & Sherraden, Citation2007; Sherraden, Citation2013). According to OECD (Citation2013), financial inclusion is about awareness, availability, and the accessibility of financial products and services, therefore ensuring that an individual can reach to financial services and products easily. Low levels of financial inclusion are about failing to access and avail financial services that restrict people’s saving their money properly, efficient planning for cost-effective borrowing, and to safeguard themselves and their families from basic calamities of hunger, crime, and natural disaster (GPFI., Citation2010). Therefore, financial inclusion enhancement is required, and it can cause financial capability building (ACCION, Citation2019). Timely, accessible, cost-effective, financially attractive, easy to use, safe & secure, and reliable financial products & services lead to financial inclusion (Aprea et al., Citation2016; Nizam et al., Citation2020; Sherraden, Citation2013). Another study stressed external factors (i.e., access to and use of services and products) concerning financial capability improvement and stated financial inclusion is an important point to be taken care of, for financial capability development (Chowa et al., Citation2014). Increased financial inclusion expands individuals’ ability to invest and protect from risk, and financial inclusion, is strongly and positively associated with an individual’s savings as access to bank accounts is related to financial inclusion (Kempson et al., Citation2013), ultimately enhanced saving increases individuals financial safety. The capability approach is also about the external environment, within that, an individual has to operate, related to the other environments. Thus,

H6: Financial inclusion positively affects financial capability.

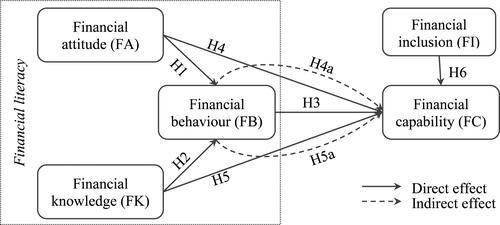

Proposed hypotheses are clearly illustrated in the theoretical model (see ).

Figure 1. Theoretical model.

3. Methods

3.1. Sample

To test the hypotheses in the proposed theoretical model, a questionnaire was initially developed based on the literature review and then its contents were revised by three academics. This technique of data collection is widely used by scholars (Friedline & West, Citation2016; Potrich et al., Citation2016; Xiao & O’Neill, 2016). The questionnaire was composed of two main sections: general information about the respondent, and indicators for the five constructs of the proposed model. It was designed based on the questionnaire of National Financial Capability Study (NFCS) (FINRA., Citation2012). To ensure consistency, a pilot test was administrated with 40 adult individuals. The data collection phase took place in June 2019 in Albania. The stratified sampling method was applied in approaching the respondents. Hence, the sample was designed based on the population distribution considering age categories, gender and regions. To approach the respondents the university Alumni database was used. It was asked each alumni to give the contact of one of their relatives who recently had his/her birthday. Then, this list of people were contacted following the above quotas. Finally, 280 individuals filled in the questionnaire (face-to-face). After cleaning the data, the final sample reached 200 valid records, satisfying the minimum sample size’s requirement (Bagozzi & Yi, Citation2012).

The research was conducted in Albania for several reasons. Firstly, as in other post-communist countries, in Albania was noted a lack of knowledge about how to behave in a market-oriented economy, which was a consequence of the practice of a central economy (Ramadani & Dana, Citation2013). Financial markets did not exist and individuals possessed low level of financial knowledge. Therefore, the level of financial literacy is low in Balkan countries as in Albania (Klapper et al., Citation2015). Secondly, not least because Albania is a transition economy that is aiming to join the European Union, it is putting efforts in establishing strong institutional environment and economic development. Individuals should be equipped with adequate level of financial literacy to enable them to deal with new challenges, as people in advanced economies do. In addition, in recent years, there has been an increased awareness in financial literacy, this was the result of concerted efforts and campaigns by the Central Bank of Albania to raise the level of financial literacy in the country (Ceca et al., Citation2014). shows the final sample profile of the respondents.

Table 1. Sample profile.

3.2. Analyses

To test the relationships proposed in the theoretical model, partial least squares structural equation modelling (PLS-SEM) was employed (Hair et al., Citation2017). PLS-SEM was used because constructs were not normally distributed and this study requires latent variable scores for follow-up analyses (Hair et al., Citation2019). All latent variables in the current study were the results of reflective indicators. PLS-SEM was executed through SmartPLS 3.0 (Ringle et al., Citation2015), using the bootstrap procedure with 5000 iterations of resampling.

Harman’s single factor test and questionnaire design were chosen as the two suitable methods for the current study because the dependent and independent variables cannot be kept from different sources (Podsakoff et al., Citation2003). Hence, the title for each section of items was not provided in the questionnaire. Furthermore, according to Harman’s single-factor test, a significant level of common method variance exists when a single factor emerges or the first capture the most of the variance (50%) (Podsakoff et al., Citation2003). Based on principal axis factoring, 33.31% of the total variance was explained by this single factor. Consequently, these results indicated that common method variance is not an issue in this research.

3.3. Variables

All constructs were measured as self-reported and they are summarised in . Each of the proposed constructs’ items was answered on a five-point Likert-type scale.

Table 2. Measurement model.

Based on the analysis (see ), financial attitude, financial knowledge, and financial behaviour demonstrated a reasonable reliability as the values of Cronbach’s alpha and composite reliability were between 0.70 and 0.95. These statistics for financial capability and financial inclusion satisfied the criteria applied in exploratory research (Hair et al., Citation2019), thus the factor model is correct. Moreover, constructs showed sufficient convergent validity since they explained more than half of their indicators’ variance investigated by AVE values. Additionally, the VIF values were below the conservative threshold of signalling collinearity. Finally, all the Heterotrait-Monotrait coefficients (Henseler et al., Citation2015) were below 0.85, indicating that all constructs were distinct one from another. Therefore, it was concluded that the discriminant validity is established for this research.

4. Results

Ensuring that no violation of PLS-SEM assumptions has occurred, lead to next step of the analysis which is the investigation of structural model. The model explains 34.9% of the variation in financial behaviour and 30.4% in financial capability. The retrieved results from the model are shown in . No problems with multicollinearity was detected, since the VIF values of the latent variables were reported nicely below the conservative threshold of 3 (Hair et al., Citation2019). Based on the theoretical framework, financial behaviour is determined by financial attitude and financial knowledge. Indeed, it was found that financial behaviour is positively impacted by financial attitude (β = 0.426, p < 0.001) and financial knowledge (β = 0.248, p < 0.01). Considering Cohen’s (Cohen, Citation1988) benchmarks, the size of the effects on financial behaviour were moderate from financial attitude(f2 = 0.209) and small from financial knowledge (f2 = 0.071). Thus, sufficient evidence has been identified to support H1 and H2. Regarding the determinants of financial capability, results revealed that financial capability is positively affected by financial behaviour with a moderate effect (β = 0.289, p < 0.001, f2 = 0.077), financial knowledge with a small effect (β = 0.192, p < 0.01, f2 = 0.037) and financial inclusion with small effect (β = 0.201, p < 0.01, f2 = 0.05). Therefore, substantial evidence were found to support H3, H5 and H6.

Table 3. Hypotheses testing.

The direct influence of financial attitude on financial capability was reported insignificant (β = 0.056, p > 0.10) (see ). However, its indirect effect on financial capability through financial behaviour was statistically significant (β = 0.123, p < 0.01). Moreover, the total effect of financial attitude on financial capability was significant (β = 0.179, t = 2.065, p < 0.05). So, in case of financial attitude, mediation effect existed, but no direct effect, which is called as indirect-only mediation (Zhao et al., Citation2010), representing the best-case situation as it shows that our mediator fully complies with the hypothesized theoretical framework. Therefore, evidence supported H4a, as it asserted that the relationship between financial attitude and financial capability is statistically mediated by financial behaviour. Referring to the indirect effect of financial knowledge on financial capability, data analysis revealed a positive and significant mediation (β = 0.072, p < 0.05). Even the total effect was statistically significant (β = 0.264, t = 3.625, p < 0.001). According to Zhao et al. (Zhao et al., Citation2010), this situation is called complementary mediation, as mediated and direct effects both exist and point at the same direction. Taking all together, evidence provided support for the hypothesized mediating relationship. So, the impact of financial knowledge on financial capability was statistically mediated by financial behaviour supporting H5b.

5. Discussion

The findings of the current study are discussed in the following paragraphs. Firstly, the study confirms that financial attitude and financial knowledge are important drivers for enhancing individuals’ financial behaviour. Therefore, there is a coherent message here for the government, education institutions and the financial industry leaders to set relevant policies and curriculum development which aim to increase the level of individuals’ financial knowledge and awareness. The financial knowledge may lead to an improvement in their financial behaviour and therefore, financial capability. The current research findings show that appropriate financial attitude and financial knowledge are critical for achieving better levels in individuals’ financial behaviour even in the context of a post-communist transition country like Albania. These findings are consistent with prior research (Fessler et al., Citation2019; Garg & Singh, Citation2018; Potrich et al., Citation2016). The present finding is a further addition to the existing literature. It reveals a positive linkage between financial knowledge and financial behaviour and is parallel with previous studies, for example financial knowledge is positively associated with better returns from a mutual fund holding (Chu et al., Citation2017) indicating better financial decision-making behaviour. Other studies also support the same finding that financial knowledge has a positive connection with both short-term and long-term financial behaviour (K. T. Kim et al., Citation2019). Similarly, the positive association between financial attitude and financial behaviour also matches with the results of other studies emphasising that financial attitude is a significant influencing factor on financial behaviour (Yap et al., Citation2018).

Secondly, it was found that financial capability can be improved by enhancing individuals’ financial knowledge, financial behaviour, and financial inclusion. However, the effect of financial attitude on financial capability was insignificant. This could be due to the following reasons. First, conceptually, there is a difference between financial attitude and financial capability. Having a certain level of attitude towards money does not necessarily mean that it should be reflected in the ability and opportunity to act (financial capability), as a prior study demonstrated (Çera et al., Citation2019; von Stumm et al., Citation2013). Second, the findings should be discussed concerning the context where the research took place. The Albanians are introduced relatively late to the free market principles since Albania was a communist country (Çera & Tuzi, Citation2019). Furthermore, more could be achieved in equipping citizens with adequate financial knowledge, as the percentage of the population, aged 15+ holding a specific product (e.g. account at a financial institution) is among the lowest in Europe (OECD, Citation2016). In addition, another study, which investigates the influence of financial components and technology usage on online purchasing in a data set of 600 respondents from Albania, reported an insignificant effect of financial attitude on the decision to purchase online (Çera et al., Citation2020). This seems logical as online shopping is part of digital financial inclusion (Hasan et al., Citation2020). It eventually falls within financial inclusion which is an integral part of financial capability. Participating in online purchasing activity is a component of financial capability. This connection gives credibility to the present findings. Thus, the Albanians’ ability and opportunity to act regarding financial matters are not at adequate levels. Along with financial knowledge, improving financial inclusion is likely to be a positive factor for building Albanian financial capability. Since the present study shows a positive impact of financial inclusion on financial capability, it is consistent with prior studies. It highlights the role of financial inclusion as a crucial factor in the context of an external opportunity for financial capability building (Huang et al., Citation2013; Johnson & Sherraden, Citation2007; Sherraden et al., Citation2015).

Thirdly, findings confirm the critical mediating role of financial behaviour in the influences of financial attitude and financial knowledge on financial capability. To the best of the authors’ knowledge, this is the first study in which such effects have been investigated. Specifically, although the influence of financial attitude on financial capability was insignificant, substantial evidence from this study was found to support the mediating effect of financial behaviour on this relationship. As Vlaev and Elliott (Citation2017) asserted, a person that does not use or apply financial attitude and financial knowledge in practical decision making is incapable. To avoid this situation, this paper found that financial behaviour can help in this regard. As a result, financial behaviour is not just crucial in improving financial capability, but also in governing the effects of financial attitude and financial knowledge toward financial capability. The overall results of the present study addressed the identified gap in recent studies and support the direct and indirect empirical findings such as, for example, financial concepts learning improves financial attitudes and behaviors. It may result in enhanced financial capability in the long run (Batty et al., Citation2015). This highlights the role of financial knowledge via financial behaviour on individuals’ financial capability, which is in line with the present study outcomes. Furthermore, another study shows that the persons’ financial capability can be assessed through financial behaviour (Mitchell & Lusardi, Citation2011). Similarly, the current study found a positive association between the two. The core findings of this study established that financial behaviour has a significant impact on the financial capability of individuals. This agrees with other studies which indicated that financial behaviour is an essential factor to determine a person’s financial capability (Potocki & Cierpiał-Wolan, Citation2019; Xiao, Chen, et al., Citation2014).

These findings are important especially in the context of a post-communist country like Albania because data showed that upgrading individuals’ financial attitude and financial knowledge lead to higher levels in financial behaviour (e.g. money management, establishing financial targets for the long-term, adopting a weekly or monthly plan for expenses etc.), which in turn positively influences financial capability. In short, the study brings out the importance of financial behaviour as a mediator and it achieves its intended objectives. It is important that these findings are brought to the attention of policymakers and social workers in order to develop policies and training programmes aimed at developing and enhancing individuals’ financial knowledge which should lead to improved financial attitude. It also recommends further investigation concerning financial attitude with a larger sample and comparison under different economic scenarios.

6. Conclusions

This research has several useful contributions. Firstly, by highlighting the application of three perspectives (capability theory, self-efficacy theory, and identity processing style), this work explores the mediation role of financial behaviour on the influence of financial literacy components collectively, such as financial attitude and financial knowledge, on financial capability. To the best of the authors’ knowledge, prior studies have been focused only on direct relationships between financial literacy components and financial capability. Our findings complement the accumulated knowledge in this field and shed further light on the relationships between financial literacy components and financial capability by demonstrating that these linkages are primarily mediated by financial behaviour. Consequently, by employing the mediation model, this research recommends a more comprehensive framework for examining the linkages between financial literacy components and financial capability by identifying the importance of the mediating role of financial behaviour.

Secondly, substantial evidence was provided that financial attitude and financial knowledge positively influence financial behaviour even in case of a post-communist transition country like Albania, which is consistent to prior studies administrated in developed countries (i.e. Fessler et al., Citation2019). Thus, the importance of financial knowledge and attitude in improving individuals’ financial behaviour is crucial not only for advanced economies, but for developing countries, as well. Hence, what matters is the level of financial literacy in the two categories of countries, and not the impact of financial knowledge and financial attitude on financial behaviour. This is supported by an international report (Klapper et al., Citation2015) and the same issue is noted regarding financial inclusion. In post-communist transition countries like the Balkans or Caucasians, the proportion of the population aged 15+ holding a specific financial product is very low when compared to developed countries (OECD, Citation2016).

This study provides useful insights for policymakers. By having a clear idea how to increase financial capability, policymakers can design policies to achieve better results in equipping citizens with adequate financial literacy and capability that are needed in contemporary society (Çera et al., Citation2020). In this regard, the triple helix model (Y. Kim et al., Citation2012) can be a useful way of increasing individuals’ financial literacy and financial capability levels. According to this model the way how government, educational institutions, and industry align their policies and strategies can encourage individuals to engage in start-ups. This principle can be applied even in the case of financial capability. For instance, banks in some European countries have developed partnerships with local educational institutions by introducing initiatives based on the online management and virtual portfolio of securities. By doing so, young individuals can learn and develop understanding of financial products and markets and experience investing in securities (OECD, Citation2016). Indeed, similar to Bank of Italy, Bank of Albania has introduced a special program dealing with financial literacy. We recommended that this program is extended to cover other institutions and industries as well, and to cover all age-groups of the population. In this regard, Albania could follow the best practices in other European countries.

There are some limitations in the research. Firstly, the data was collected by asking individuals to self-report their opinion on selected indicators. Thus, their responses were subject to recall (Xiao, Ahn, et al., Citation2014). The use of financial diaries as a tool to collect data and information is believed to overcome this limitation (Potocki & Cierpiał-Wolan, Citation2019). Secondly, this paper covers only one country and this limits its findings’ generalisation to other countries. Nevertheless, the replication of the conceptual framework used by this paper, can contribute to overcoming these limitations. Additionally, in the current research, financial inclusion was measured by two indicators which limit retrieved findings. Therefore, the development of a financial inclusion scale in a way to capture a wider range of indicators is needed. This can be considered by scholars in further research. From a marketing’s point of view, there is a need to investigate the role of financial capability in the individuals’ decision to purchase, including online channels. It is believed that the higher the level of the individuals’ financial capability, the more likely their involvement in online shopping will be.

Disclosure statement

No potential conflict of interest was reported by the authors.

Correction Statement

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

References

- ACCION. (2019). Seizing the moment on the road to financial inclusion. Center for Financial Inclusion.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/https://doi.org/10.1016/0749-5978(91)90020-T

- Aprea, C., Wuttke, E., Breuer, K., Koh, N. K., Davies, P., Greimel-Fuhrmann, B., & Lopus, J. S. (2016). International handbook of financial literacy. Springer. https://doi.org/https://doi.org/10.1007/978-981-10-0360-8

- Arifin, A. Z. (2018). Influence factors toward financial satisfaction with financial behavior as intervening variable on Jakarta area workforce. European Research Studies Journal, XXI(1), 90–103. https://doi.org/https://doi.org/10.11214/thalassinos.21.01.008

- Atkinson, A., McKay, S., Kempson, E., & Collard, S. (2006). Levels of financial capability in the UK: Results of a baseline survey. Financial Services Authority.

- Atkinson, A., & Messy, F.-A. (2012). Measuring financial literacy: Results of the OECD/International Network on Financial Education (INFE) pilot study. OECD Publishing. https://doi.org/https://doi.org/10.1787/5k9csfs90fr4-en

- Atlas, S. A., Lu, J., Micu, P. D., & Porto, N. (2019). Financial knowledge, confidence, credit use, and financial satisfaction. Journal of Financial Counseling and Planning, 30(2), 175–190. Retrieved from https://connect.springerpub.com/content/sgrjfcp/30/2/175

- Babiarz, P., & Robb, C. A. (2014). Financial literacy and emergency saving. Journal of Family and Economic Issues, 35(1), 40–50. https://doi.org/https://doi.org/10.1007/s10834-013-9369-9

- Bagozzi, R. P., & Yi, Y. (2012). Specification, evaluation, and interpretation of structural equation models. Journal of the Academy of Marketing Science, 40(1), 8–34. https://doi.org/https://doi.org/10.1007/s11747-011-0278-x

- Bandura, A. (1977). Self-efficacy: Toward a unifying theory of behavioral change. Psychological Review, 84(2), 191–215. https://doi.org/https://doi.org/10.1037/0033-295X.84.2.191

- Batty, M., Collins, J. M., & Odders-White, E. (2015). Experimental evidence on the effects of financial education on elementary school students’ knowledge, behavior, and attitudes. Journal of Consumer Affairs, 49(1), 69–96. https://doi.org/https://doi.org/10.1111/joca.12058

- Belás, J., Nguyen, A., Smrčka, L., Kolembus, J., & Cipovová, E. (2016). Financial literacy of secondary school students. Case study from the Czech Republic and Slovakia. Economics & Sociology, 9(4), 191–206. https://doi.org/https://doi.org/10.14254/2071-789X.2016/9-4/12

- Berzonsky, M. D. (1989). Identity style: Conceptualization and measurement. Journal of Adolescent Research, 4(3), 268–282. https://doi.org/https://doi.org/10.1177/074355488943002

- Bongini, P., Iannello, P., Rinaldi, E. E., Zenga, M., & Antonietti, A. (2018). The challenge of assessing financial literacy: Alternative data analysis methods within the Italian context. Empirical Research in Vocational Education and Training, 10(1), 12. https://doi.org/https://doi.org/10.1186/s40461-018-0073-8

- Ceca, K., Koleniço, A., Isaku, E., Haxhimusaj, B. (2014). Financial literacy in Albania: Survey results for measuring financial literacy of the population, 2011 (50 No. 11). https://www.bankofalbania.org/web/Financial_literacy_in_Albania_Survey_results_for_measuring_financial_literacy_of_the_population_2011_6910_2.php

- Çera, G., Poleshi, B., Khan, K. A., Shumeli, A., & Kojku, O. (2019). Determinants of financial capability: Evidence from a developing country [Paper presentation]. The 15th International Bata Conference for Ph.D. Students and Young Researchers, UTB: Zlin. https://doi.org/https://doi.org/10.7441/dokbat.2019.018

- Çera, G., Phan, Q. P. T., Androniceanu, A., & Çera, E. (2020). Financial capability and technology implications for online shopping. E + M Ekonomie a Management, 23(2), 156–172. https://doi.org/https://doi.org/10.15240/tul/001/2020-2-011

- Çera, G., & Tuzi, B. (2019). Does gender matter in financial literacy? A case study of young people in Tirana. Scientific Papers of the University of Pardubice, Series D, 45(1), 5–16. https://dk.upce.cz/handle/10195/72241

- Chowa, G., Ansong, D., & Despard, M. R. (2014). Financial capabilities: Multilevel modeling of the impact of internal and external capabilities of rural households. Social Work Research, 38(1), 19–35. https://doi.org/https://doi.org/10.1093/swr/svu002

- Chu, Z., Wang, Z., Xiao, J. J., & Zhang, W. (2017). Financial literacy, portfolio choice and financial well-being. Social Indicators Research, 132(2), 799–820. https://doi.org/https://doi.org/10.1007/s11205-016-1309-2

- Civelek, M., Ključnikov, A., Krajčík, V., & Žufan, J. (2019). The importance of discount rate and trustfulness of a local currency for the development of local tourism. Journal of Tourism and Services, 10(19), 77–92. https://doi.org/https://doi.org/10.29036/jots.v10i19.117

- Clark, D. A. (2005). Sen’s capability approach and the many spaces of human well-being. Journal of Development Studies, 41(8), 1339–1368. https://doi.org/https://doi.org/10.1080/00220380500186853

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). L. Erlbaum Associates.

- Danes, S. M., & Haberman, H. R. (2007). Teen financial knowledge, self-efficacy, and behavior: A gendered view. Financial Counseling and Planning, 18(2), 48–99.

- Despard, M. R., & Chowa, G. A. (2014). Testing a measurement model of financial capability among youth in Ghana. Journal of Consumer Affairs, 48(2), 301–322. https://doi.org/https://doi.org/10.1111/joca.12031

- European Commission. (2016). Commission staff working document Albania 2016 Report. European Commission, Brussel. Retrieved from https://ec.europa.eu/neighbourhood-enlargement/sites/near/files/pdf/key_documents/2016/20161109_report_albania.pdf

- Fessler, P., Silgoner, M., & Weber, R. (2019). Financial knowledge, attitude and behavior: Evidence from the Austrian Survey of Financial Literacy. Empirica, 1–11. https://doi.org/https://doi.org/10.1007/s10663-019-09465-2

- FINRA. (2012). National financial capability study military survey. Financial Industry Regulatory Authority Investor Education Foundation. https://www.usfinancialcapability.org/

- Friedline, T., & West, S. (2016). Financial education is not enough: Millennials may need financial capability to demonstrate healthier financial behaviors. Journal of Family and Economic Issues, 37(4), 649–671. https://doi.org/https://doi.org/10.1007/s10834-015-9475-y

- Garg, N., & Singh, S. (2018). Financial literacy among youth. International Journal of Social Economics, 45(1), 173–186. https://doi.org/https://doi.org/10.1108/IJSE-11-2016-0303

- GPFI. (2010). G20 principles for innovative financial inclusion. Global Partnership for Financial Inclusion.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (2nd ed.). Sage.

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/https://doi.org/10.1108/EBR-11-2018-0203

- Hasan, M. M., Yajuan, L., & Mahmud, A. (2020). Regional development of China’s inclusive finance through financial technology. SAGE Open, 10(1), 215824401990125. https://doi.org/https://doi.org/10.1177/2158244019901252

- Hayhoe, C. R., Leach, L., Allen, M. W., & Edwards, R. (2005). Credit cards held by college students. Journal of Financial Counseling and Planning, 16(1), 1–10.

- Henchoz, C., Coste, T., & Wernli, B. (2019). Culture, money attitudes and economic outcomes. Swiss Journal of Economics and Statistics, 155(1), 1–13. https://doi.org/https://doi.org/10.1186/s41937-019-0028-4

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/https://doi.org/10.1007/s11747-014-0403-8

- Hensley, B. J. (2015). Enhancing links between research and practice to improve consumer financial education and well-being. Journal of Financial Counseling and Planning, 26(1), 94–101. https://doi.org/https://doi.org/10.1891/1052-3073.26.1.94

- Hilgert, M. A., Hogarth, J. M., & Beverly, S. G. (2003). Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin, 106, 309–322.

- Hira, T. K. (2012). Promoting sustainable financial behaviour: Implications for education and research. International Journal of Consumer Studies, 36(5), 502–507. https://doi.org/https://doi.org/10.1111/j.1470-6431.2012.01115.x

- Huang, J., Nam, Y., & Sherraden, M. S. (2013). Financial knowledge and child development account policy: A test of financial capability. Journal of Consumer Affairs, 47(1), 1–26. https://doi.org/https://doi.org/10.1111/joca.12000

- Huston, S. J. (2010). Measuring financial literacy. Journal of Consumer Affairs, 44(2), 296–316. https://doi.org/https://doi.org/10.1111/j.1745-6606.2010.01170.x

- Johnson, E., & Sherraden, M. S. (2007). From financial literacy to financial capability among youth. The Journal of Sociology & Social Welfare, 34(3), 119–147.

- Joo, S., & Grable, J. (2000). Improving employee productivity: The role of financial counseling and education. Journal of Employment Counseling, 37(1), 2–15.

- Joo, S., & Grable, J. (2004). An exploratory framework of the determinants of financial satisfaction. Journal of Family and Economic Issues, 25(1), 25–50. https://doi.org/https://doi.org/10.1023/B:JEEI.0000016722.37994.9f

- Kalmi, P. (2018). The effects of financial education: Evidence from Finnish lower secondary schools. Economic Notes, 47(2–3), 353–386. https://doi.org/https://doi.org/10.1111/ecno.12114

- Kempson, E., Perotti, V., & Scott, K. (2013). Measuring financial capability: A new instrument and results from low- and middle-income countries.

- Kim, K. T., Anderson, S. G., & Seay, M. C. (2019). Financial knowledge and short-term and long-term financial behaviors of millennials in the United States. Journal of Family and Economic Issues, 40(2), 194–208. https://doi.org/https://doi.org/10.1007/s10834-018-9595-2

- Kim, Y., Kim, W., & Yang, T. (2012). The effect of the triple helix system and habitat on regional entrepreneurship: Empirical evidence from the U.S. Research Policy, 41(1), 154–166. https://doi.org/https://doi.org/10.1016/j.respol.2011.08.003

- Klapper, L., Lusardi, A., van Oudheusden, P. (2015). Financial literacy around the world: Insights from the Standard & Poor’S ratings Services Global Financial Literacy Survey. World Bank. http://www.openfininc.org/wp-content/uploads/2016/04/2015-Finlit_paper_17_F3_SINGLES.pdf

- Loke, V., Choi, L., & Libby, M. (2015). Increasing youth financial capability: An evaluation of the MyPath savings initiative. Journal of Consumer Affairs, 49(1), 97–126. https://doi.org/https://doi.org/10.1111/joca.12066

- Lusardi, A., & Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. https://doi.org/https://doi.org/10.1257/jel.52.1.5

- Lusardi, A., & Tufano, P. (2015). Debt literacy, financial experiences, and overindebtedness. Journal of Pension Economics and Finance, 14(4), 332–368. https://doi.org/https://doi.org/10.1017/S1474747215000232

- Luukkanen, L., & Uusitalo, O. (2019). Toward financial capability—Empowering the young. Journal of Consumer Affairs, 53(2), 263–295. https://doi.org/https://doi.org/10.1111/joca.12186

- Mitchell, O. S., & Lusardi, A. (2011). Financial literacy and planning: Implications for retirement well-being. Implications for Retirement Security and the Financial Marketplace. https://doi.org/https://doi.org/10.1093/acprof:oso/9780199696819.003.0002

- Moreland, K. A. (2018). Seeking financial advice and other desirable financial behaviors. Journal of Financial Counseling and Planning, 29(2), 198–206. https://doi.org/https://doi.org/10.1891/1052-3073.29.2.198

- Nguyen, T. A. N., & Rozsa, Z. (2019). Financial literacy and financial advice seeking for retirement investment choice. Journal of Competitiveness, 11(1), 70–83. https://doi.org/https://doi.org/10.7441/joc.2019.01.05

- Nguyen, T. A. N., Rózsa, Z., Belás, J., & Belásová, Ľ. Ľ. (2017). The effects of perceived and actual financial knowledge on regular personal savings: Case of Vietnam. Journal of International Studies, 10(2), 278–291. https://doi.org/https://doi.org/10.14254/2071-8330.2017/10-2/19

- Nizam, R., Karim, Z. A., Rahman, A. A., & Sarmidi, T. (2020). Financial inclusiveness and economic growth: New evidence using a threshold regression analysis. Economic Research-Ekonomska Istraživanja, 33(1), 1465–1484. https://doi.org/https://doi.org/10.1080/1331677X.2020.1748508

- OECD. (2013). Financial literacy and inclusion. Financial literacy & education. Organisation for Economic Co-operation and Development. https://doi.org/https://doi.org/10.1787/9789264254855-en

- OECD. (2015). National strategies for financial education: OECD/INFE policy handbook. https://www.oecd.org/daf/fin/financial-education/national-strategies-for-financial-education-policy-handbook.htm

- OECD. (2016). Financial education in Europe: Trends and recent developments. Organisation for Economic Co-operation and Development. https://doi.org/https://doi.org/10.1787/9789264254855-en

- Perry, V. G., & Morris, M. D. (2005). Who is in control? the role of self-perception, knowledge, and income inexplaining consumer financial behavior. Journal of Consumer Affairs. https://doi.org/https://doi.org/10.1111/j.1745-6606.2005.00016.x

- Piotrowska, M. (2019). Facets of competitiveness in improving the professional skills. Journal of Competitiveness, 11(2), 95–112. https://doi.org/https://doi.org/10.7441/joc.2019.02.07

- Podsakoff, P. M., MacKenzie, S. B., Lee, J.-Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. The Journal of Applied Psychology, 88(5), 879–903. https://doi.org/https://doi.org/10.1037/0021-9010.88.5.879

- Potocki, T., & Cierpiał-Wolan, M. (2019). Factors shaping the financial capability of low-income consumers from rural regions of Poland. International Journal of Consumer Studies, 43(2), 187–198. https://doi.org/https://doi.org/10.1111/ijcs.12498

- Potrich, A. C. G., Vieira, K. M., & Kirch, G. (2015). Determinants of financial literacy: Analysis of the influence of socioeconomic and demographic variables. Revista Contabilidade & Finanças, 26(69), 362–377. https://doi.org/https://doi.org/10.1590/1808-057x201501040

- Potrich, A. C. G., Vieira, K. M., & Mendes-Da-Silva, W. (2016). Development of a financial literacy model for university students. Management Research Review, 39(3), 356–376. https://doi.org/https://doi.org/10.1108/MRR-06-2014-0143

- Ramadani, V., & Dana, L.-P. (2013). The state of entrepreneurship in the Balkans: Evidence from selected countries. In V. Ramadani & R. Schneider (eds.), Entrepreneurship in the Balkans (pp. 217–250). Springer Berlin Heidelberg. https://doi.org/https://doi.org/10.1007/978-3-642-36577-5_12

- Ringle, C. M., Wende, S., & Becker, J.-M. (2015). SmartPLS. SmartPLS GmbH. http://www.smartpls.com

- Robb, C. A., & Woodyard, A. S. (2011). Financial knowledge and best practice behavior. Journal of Financial Counseling and Planning, 22(1), 60–70.

- Rothwell, D. W., Khan, M. N., & Cherney, K. (2016). Building financial knowledge is not enough: Financial self-efficacy as a mediator in the financial capability of low-income families. Journal of Community Practice, 24(4), 368–388. https://doi.org/https://doi.org/10.1080/10705422.2016.1233162

- Sample, J., & Warland, R. (1973). Attitude and prediction of behavior author. Social Forces, 51(3), 292–304. https://doi.org/https://doi.org/10.2307/2577135

- Santini, F. D. O., Ladeira, W. J., Mette, F. M. B., & Ponchio, M. C. (2019). The antecedents and consequences of financial literacy: A meta-analysis. International Journal of Bank Marketing, 37(6), 1462–1479. https://doi.org/https://doi.org/10.1108/IJBM-10-2018-0281

- Sen, A. (1993). Does business ethics make economic sense? Business Ethics Quarterly, 3(1), 45–66. https://doi.org/https://doi.org/10.1007/978-94-015-8165-3_6

- Serido, J., Shim, S., & Tang, C. (2013). A developmental model of financial capability: A framework for promoting a successful transition to adulthood. International Journal of Behavioral Development, 37(4), 287–297. https://doi.org/https://doi.org/10.1177/0165025413479476

- Sherraden, M. S. (2013). Building blocks of financial capability. In J. Birkenmaier, M. Sherraden, & J. Curley (Eds.), Financial capability and asset development (pp. 3–43). Oxford University Press. https://doi.org/https://doi.org/10.1093/acprof:oso/9780199755950.003.0012

- Sherraden, M. S., Huang, J., Jacobson Frey, J., Birkenmaier, J., Callahan, C., Clancy, M. M., & Sherraden, M. (2015). Financial capability and asset building for all. American Academy of Social Work and Social Welfare.

- Shih, T. Y., & Ke, S. C. (2014). Determinates of financial behavior: Insights into consumer money attitudes and financial literacy. Service Business, 8(2), 217–238. https://doi.org/https://doi.org/10.1007/s11628-013-0194-x

- Shim, S., Serido, J., Bosch, L., & Tang, C. (2013). Financial identity-processing styles among young adults: A longitudinal study of socialization factors and consequences for financial capabilities. Journal of Consumer Affairs, 47(1), 128–152. https://doi.org/https://doi.org/10.1111/joca.12002

- Shkvarchuk, L., & Slav’yuk, R. (2019). The financial behavior of households in Ukraine. Journal of Competitiveness, 11(3), 144–159. https://doi.org/https://doi.org/10.7441/joc.2019.03.09

- Vlaev, I., & Elliott, A. (2017). Defining and influencing financial capability. In R. Ranyard (Ed.), Economic psychology (pp. 187–205). John Wiley & Sons. https://doi.org/https://doi.org/10.1002/9781118926352.ch12

- von Stumm, S., Fenton O’Creevy, M., & Furnham, A. (2013). Financial capability, money attitudes and socioeconomic status: Risks for experiencing adverse financial events. Personality and Individual Differences, 54(3), 344–349. https://doi.org/https://doi.org/10.1016/j.paid.2012.09.019

- Xiao, J. J., & O'Neill, B. (2016). Consumer financial education and financial capability. International Journal of Consumer Studies, 40(6), 712–721. https://doi.org/https://doi.org/10.1111/ijcs.12285

- Xiao, J. J., Ahn, S. Y., Serido, J., & Shim, S. (2014). Earlier financial literacy and later financial behaviour of college students. International Journal of Consumer Studies, 38(6), 593–601. https://doi.org/https://doi.org/10.1111/ijcs.12122

- Xiao, J. J., Chen, C., & Chen, F. (2014). Consumer financial capability and financial satisfaction. Social Indicators Research, 118(1), 415–432. https://doi.org/https://doi.org/10.1007/s11205-013-0414-8

- Yap, R. J. C., Komalasari, F., & Hadiansah, I. (2018). The effect of financial literacy and attitude on financial management behavior and satisfaction. Bisnis & Birokrasi Journal, 23(3), 140–146. https://doi.org/https://doi.org/10.20476/jbb.v23i3.9175

- Yong, C. C., Yew, S. Y., & Wee, C. K. (2018). Financial knowledge, attitude and behaviour of young working adults in Malaysia. Institutions and Economies, 10(4), 21–48.

- Zhao, X., Lynch, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and Truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206. https://doi.org/https://doi.org/10.1086/651257

- Zins, A., & Weill, L. (2016). The determinants of financial inclusion in Africa. Review of Development Finance, 6(1), 46–57. https://doi.org/https://doi.org/10.1016/j.rdf.2016.05.001