Abstract

The aim of this paper is to review the impact of entrepreneurs' attitudes toward the defined business risks on the perception of the future of small and medium-sized enterprises (SMEs). 454 SMEs from the Czech Republic (CR) participated in the research and completed an online questionnaire. Structural equation modelling and factor analysis were used to identify the causal relationships between the examined variables. Entrepreneurs' attitudes toward business failure also have a positive effect on the future of the SME. The perception of financial risk in positive indicators of financial performance and the perception of financial risk as part of the company's everyday life have the most significant impact on future business. Operational risk is reflected in the utilisation of corporate resources, reducing customer complaints about the quality of the company's products and the company's independence of a limited number of suppliers. The company's sales volume adequacy provides a source of market risk. It has the third strongest positive impact on the future business in the SME segment. The research results provide a valuable platform for the authors of national and regional development strategic plans looking for SME support and development as well as the authors of the relevant policies.

1. Introduction

The responsibility of an SME owner/top SME manager to make strategic decisions plays the key role in ensuring financial prosperity and the sustainability of SMEs in the business environment (Cepel et al., Citation2018) or a smooth digitalization process (Dincă et al., Citation2019). Business decisions are made under uncertainty and risk. SMEs are becoming more aware of the need for risk management and control (Wegner et al., Citation2017).

The benefits of SME risk management are highlighted by several authors. The primary effects are seen in the gradual increase of SME financial performance; improving the SME position in the business segment; improving services/products for customers and the employee productivity (Psarska et al., Citation2019). The secondary effects become evident not only in the improved economic indicators (purchasing power of the population, etc.) in the SME location (city, region) but also in the country’s macroeconomic indicators (Audretsch & Keilbach, Citation2005).

It is important to help companies with risk management, i.e. identify, analyse, evaluate and manage risks (Belas et al., Citation2018). The diagnostics of risk sources in SMEs is the most important phase of risk management because preventive actions can only be devised to eliminate the identified risk (Gorzeń-Mitka, Citation2019).

The adverse consequences of the absence of business risk management threaten the very existence of a company (Balcaen & Ooghe, Citation2006). This includes the inability to pay debts to suppliers, employees, the state, and the lack of job orders from customers, unfavourable values of financial indicators of the company, or stressful situations between employees and the management. These side effects translate into the company’s insolvency and often lead to its liquidation (Chłodnicka & Zimon, Citation2020).

Given the important position of SMEs in the overall economic system of national policies and the European Union as a whole, there are efforts to analyse the business risks and their relationship to the direction of a business in the future in more detail (Lima et al., Citation2020).

The study was motivated by these consistent facts, focusing on the perception of business risks and business failure in relation to future business in the SME segment.

The structure of the paper is as follows: The literature review is focused on business risk management. In the next part of the study, the database, methodology and procedures are described. The analytical part contains a proposed and verified SEM model with fit-test characteristics and the most important results of factor analysis. They provide a platform for the discussion part and conclusions. The conclusion of the study is a comprehensive evaluation of the results and their applicability for different types of policies. It also implies many topics for subsequent research in this field.

2. Literature review

Fear of the future is amongst the most important reasons why entrepreneurs do not engage in business (Cacciotti et al., Citation2016). Business literature identified the difference between entrepreneurs and managers lies in their level of openness to experience (e.g. Zhao & Seibert, Citation2006). Shane et al. (Citation2010) says that openness to experience explains much of the variation in the genetic predisposition of an individual and underlines its importance in the business process. Business stability and performance is based on the implementation of an enterprise risk management system (Gordon et al., Citation2009).

Several studies (e.g. Dvorsky et al., Citation2020; Grimsdottir & Edvardsson, Citation2018) confirm the application of strategic management elements in the SME sector is somewhat different compared to large enterprises and it is considerably limited and questionable. Svarova and Vrchota (Citation2013) examined a sample of 176 respondents for the relationship between the implementation of strategic management in the SME segment and its market stability and financial success of the company. The authors concluded based on empirical research that a formulated strategy has a positive effect on the SME financial performance while at the same time it does not influence the financial success of the SME. Klammer et al. (Citation2017) provide that SMEs that are business-oriented and willing to learn can have successful strategic management.

H1: The entrepreneur's attitude toward strategic risk management has a positive effect on the perception of a company's future (FB).

Market risk is determined by a number of causes focused on the overall level of market competitiveness (Malega et al., Citation2019). Market risk can be defined as the strategic risk of SMEs which consists in the long-term retention of the existing customers and in the acquisition and retention of new customers and in the production of new products or delivery of new services (Rowland et al., Citation2019). Nothing but a sufficient number of customers allows SMEs to implement a reasonable sales volume which allows them to maintain their market position (Herath & Mahmood, Citation2014). The level of a company's competitiveness is largely based on two main factors of the competitive environment: customers and competitors (De Clercq et al., Citation2013). SMEs must develop their competitive advantages to survive; the companies managing scarce resources that are difficult to replace typically gain a competitive advantage (Vochozka & Psarska, Citation2016). One such resource is human resources (Caseiro & Coelho, Citation2018). Businesses must be able to innovate new products, achieve success and growth, and satisfy consumer demand (O'Cass & Sok, Citation2014). Business performance is the primary goal of any type of firm, being a top priority for managers (Trif et al., Citation2019).

H2: The entrepreneur's attitude toward market risk management has a positive effect on the perception of a company's future.

The level of financial risk must be assessed in terms of the risk performance in a company towards successful financial risk management decisions because risk is considered an integral part of a company's business (Olah et al., Citation2019). Financial risk is one of the main threats to SME business (Yang, Citation2017). Difficulties in business financing and lack of funds are the most common symptoms of SME financial risk (Bosma et al., Citation2018) because most of the operation of the company is financed by the capital of owners or managers themselves. This may result in the increase of operating costs and corporate debt, and debt repayment problems and consequently high financial risk. Access to finance is likely to improve the quality of a business environment by leading firms toward a more productive scope of business.

The purpose of the Yao Wang study (Citation2016) was to analyse the biggest obstacles to the growth of SMEs from the perspective of business managers based on the World Bank enterprise survey including data from 119 developing countries. SMEs consider the access to funds as the critical obstacle to their growth while managers consider the access to finance, tax rates and competition as the biggest obstacles to the external financing of SMEs.

H3: The entrepreneur's attitude toward financial risk management has a positive effect on the perception of a company's future.

The quality of human capital in a company provides the basis for increasing the company’s performance (Gede Riana et al., Citation2020). Empirical studies show that voluntary efforts by employees will increase productivity and ultimately performance (Neary et al., Citation2018). They also create a competitive advantage for the company (Habanik et al., Citation2020). It is important to develop a positive interpersonal relationship between individuals working at different levels of the organisation (Alnoor, Citation2020). Employees working together with others to build a social interpersonal relationship uphold the need for affiliation and fellowship. The social exchange and reciprocity theories explain how managers and the behaviour of co-workers determine the quality of this relationship and influence the judgments of employees (Redmond & Sharafizad, Citation2020).

H4: The entrepreneur's attitude toward personnel risk management has a positive effect on the perception of a company's future.

The political stability and orientation of a country the company chooses to operate in are highly important for SMEs. Political factors set up the legal framework and control the business environment (Dickson & Weaver, Citation2008).

Cepel et al. (Citation2018) says the political and legal environment provides a legal and supporting framework for business activities and it regulates the international business relations, tax and levy policies, antitrust policy, the stability of the legal environment, judicial efficiency, and law enforcement, or the administrative burden on businesses, etc.

The government regulation is perceived as the major obstacle to market entry (Lutz et al., Citation2010). Stenholm et al. (Citation2013) studied a sample of 65 countries to identify how differences in the institutional organisation may affect business activities in a country. The authors consider the institutional methods and regulatory provisions are connected to the level of business activities, and therefore they suggest to facilitate the entry of new companies into the market which may have a positive effect on business activities.

H5: The entrepreneur's attitude toward legal risk management has a positive effect on the perception of a company's future.

The impact of SME internal capabilities on a competitive advantage was studied by Games and Roliza (Citation2019) while they also considered the age of the company. In the case of Indonesia, the SME internal capability had a strong and positive correlation with a competitive advantage. For SMEs with less than five years of operation, this connection is weak in comparison to older companies. Innovation has a profound and significant influence on the company's competitiveness through increasing productivity as documented in the transitional market study (Ngoc Mai et al., Citation2019). A higher level of customer satisfaction and loyalty leads to a higher support for the purchasing processes. The important indicators that may affect the narrower business environment include the support of business customers and suppliers (Balan et al., Citation2019). The support of corporate customers has a greater effect on the narrower business environment. Mafini and Muposhi (Citation2017) studied the relationship between SMEs and their suppliers. The authors suggest the existence of long-term relationships between SMEs and their suppliers does not automatically lead to better risk management.

H6: The entrepreneur's attitude toward operational risk management has a positive effect on the perception of a company's future.

Empirical studies emphasize the determinants and consequences of business failure (Karabag, Citation2019). In general, SME bankruptcy research can be divided into three main parts: (i) predictive models, (ii) finance and law, and (iii) organizational failure. Another current research topic addresses the issue of perception, consequences and costs of business failure (Ucbasaran et al., Citation2013).

The significant causes of business failure include: lack of planning activities of the company's management; lack of working capital; offering too much credit to customers (Hanzaee et al., Citation2011); failure to implement rapid outsourcing; market competition; insufficient monitoring of corporate finances (Santisteban & Mauricio, Citation2017).

Other factors may also contribute to business failure. Süsi and Lukason (Citation2019) stated the risk of failure decreases as the manager’s age increases and managerial ownership is present. On the other hand, the presence of larger management boards and managers in other companies will increase the risk of failure.

H7: The entrepreneur's attitude toward business failure (BF) has a positive effect on the perception of a company's future.

3. Purpose, data and methodology

The aim of this paper is to review the impact of entrepreneurs' attitudes toward the defined business risks on the perception of the future of SMEs. Following the goal definition, empirical research was conducted using online questionnaires. Data was collected in the CR from 9/2019 to 3/2020. 8250 SMEs were randomly selected from the Cribis database. This SME database is considered to be the most reliable sources of information concerning businesses in the Czech business environment. The questioning technique was used to receive feedback from respondents to specific statements by completing an online questionnaire. In the first phase, respondents were contacted by email with a structured request for completion of a questionnaire. In the second phase, SMEs were contacted by telephone.

The questionnaire consisted of several parts. The questions were assigned to the questionnaire by random (except for the demographic characteristics of respondent). The statements concerning business risks, the perception of BF and future business were formulated in a positive way to maintain the continuity of logical thinking. Provided that business risks are managed correctly by SMEs, then the future of SMEs is perceived more positively. The average return of questionnaires was 3.6%. Respondents’ opinions were based on the Likert's five-point scale: 1 "I strongly agree" to 5 "I strongly disagree" with a statement. The questionnaire was completed by 465 respondents. The number of correctly/incorrectly completed questionnaires (hereinafter referred to as the sample) was represented by 454/11 respondents. The general evaluation of questions looking at the characteristics of a company and respondent is shown in .

Table 1. Structure of respondents according to demographic characteristics.

To achieve the aim of the study, the authors selected methods of mathematical statistics (factor analysis (FA) and structural equation modelling - SEM) for verification.

The FA was applied in the first step. The process of the FA exploration technique can be logically organized into three steps: i. data validation; ii. factor extraction; iii. factor rotation (Brown, Citation2015).

The SEM method is an appropriate tool for constructing, identifying and quantifying the relationships between latent variables (Smith et al., Citation1998) as well as their graphical representation using a structural model. The final structural model can identify and quantify complex, not only direct but also indirect relationships of latent variables to each other and between latent and manifest variables (Levy, Citation2011).

Latent variables are considered to be the most significant business risks that are impossible to measure directly. Latent variables can be defined using manifest variables (Babin et al., Citation2008).

The suitability of a test model can be verified by selected measures: Goodness of Fit (GFI); CMIN/DF - The minimum discrepancy; Comparative Fit index (CFI); Roat Mean Square Error of Approximation (RMSEA); Normed fit index (NFI). The SEM model is statistically significant if: the GFI p-value is greater than 0.05 (Hooper et al., Citation2008); CMIN/Df value is within the interval of −2 to 2 (Byrne & Reinhart, Citation1989); the RMSA value ranges from 0 to 0.05 (Smith et al., Citation1998); the NFI index value is greater than 0.9 (Bentler, Citation1990); the CFI value is greater than 0.95 (Wheaton et al., Citation1977). All the above tests were performed through IBM SPSS Statistics and IBM SPSS Amos.

4. Results

The general description of business risk indicators, BF indicators and the perceived future of business (mean (M), standard deviation (SD), sample skewness (S) and kurtosis (K)) are summarized in . shows the results of factor reliability and the relationship between the corrected item (CI) and the total correlation (TC) of a selected factor.

Table 2. Descriptive statistics (DS) of indicators and Cronbach´s Alpha (CA) test results.

The results in show that although the Cochran´s alpha values exceed 0.7, the corrected item-total correlation (CI-TC) of indicators such as MR4, FR1, FR4, LEG4, BF5 is lower than 0.5. The indicator reliability is not acceptable according to Hair et al. (Citation2010). These results were also confirmed in the individual (factor) KMO tests. The factor loading (FL) understood as a correlation of each item and a factor should be better than 0.5 (Hair et al., Citation2010) to ensure the indicator is correlated with the type of business risk or BF. The results indicate that MR4 (FL = 0.214); FR3 (FL = 0.284); FR4 (FL = 0.322); LEG2 (FL = 0.417); PER3 (FL = 0.474); PER4 (FL = 0.451); BF3 (FL = 0.397) do not meet the above threshold requirements. The results of a KMO test and Bartlet test of sphericity without the above indicators are illustrated in .

Table 3. Kaiser-Meyer-Olkin test (KMO) and Bartlett´s test results.

The KMO test results in confirmed a proportion of variance of the individual variables that can be explained by background factors. The reason is that the KMO test value is close to the value of 1, or a large proportion of the variance is explained by factors. Also, the results of the Bartlet test (P - value = 0.000) showing the null hypotheses that the correlation coefficient of the variables in the sample is zero are accepted at a significance level of 0.05.

The Varimax rotation technique (6 iterations) was used to interpret the factor matrix. If the results of the indicator iterative process showed a less communality of indicators with high transverse overload (> | 0.4 |), then they were removed. summarizes the results of the rotated solution of the indicator matrix.

Table 4. Rotated component matrix – indicator to business risk relationship.

The results obtained with the Principal Component Analysis extraction method: 8 factors; the maximum number in the range of 5-10 factors. The result of the BIC method is 8 factors. The obtained results are very satisfactory in view of the defined number of latent variables (6 - business risk types, 1 - perception of BF by the respondent) and 1 endogenous variable (perception of future business by the respondent). shows the results of the total variance explained by the above factors.

Table 5. Total variance explained.

Based on the values in , it was concluded that the selected factors explain nearly 64.7% of the variability in the total variance. Based on the results in and , it was concluded that all selected factors are identified. These results are identical to the scree plot which also confirmed the number of 8 factors since the very 8 components, consequently denoted by factors, were obtained using Kaiser rule (more than 1% of the total variance; Bentler, Citation1990). Other non-significant indicators which do not strongly correlate with the selected factors are shown below the running mark in the scree plot (MR4, FR3, FR4, LEG2, PER3, PER4 and BF3 - see also ). The scree plot is not included in the results due to duplicated results obtained in and .

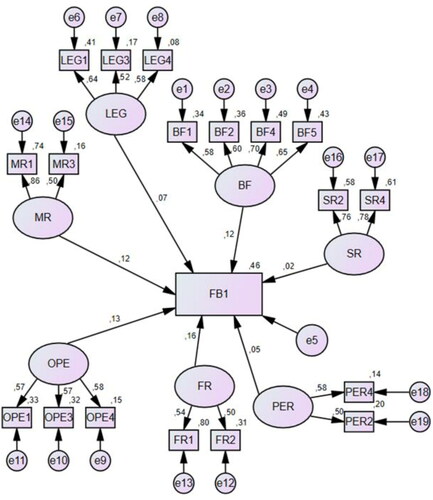

The characteristics of a structural model () that was subsequently verified by the summary fit characteristics are as follows: one dependent variable and seven independent variables; latent variables measured by manifest variables (indicators), each manifest variable contains an unexplained part (residual errors not explained by the model); the relationship between latent exogenous variables (SR, …, OPE, BF) and endogenous variables (FB) is determined by an arrow. The above process resulted in a structural (SEM) model () of the relationship between business risks, perception of BF and perception of future business.

Figure 1. SEM model with standardized estimates. Source: created by the authors in the IBM SPSS AMOS software.

The resulting model () is the best solution to the proposed model and empirical data based on the Summary Fit Model (see ). The resulting model assumes that selected types of business risks are independent. To achieve satisfactory results, it was necessary to remove variables from the SEM model (based on the path coefficient: OPE2, MR2, SR1, SR3, BF3. Before interpreting the structural model of relationships (see ), the most important FIT tests of the created SEM model were calculated and interpreted (see and ).

Table 6. Hypothesis testing and path coefficients (positive effects).

Table 7. SEM model - summary fit model.

The results of the GFI characteristic (see ) demonstrated the statistical significance of the structural model (p-value = 0.061). The SEM model has the value of CMIN/Df. = 1.914. This value is at the upper limit of acceptability because the CMIN/Df value higher than 2 indicates a poor fit of the proposed SEM model with data in the sample of SME attitudes. The RMSA value is higher than the recommended SEM model acceptance interval <0; 0.5>. However, Smith et al. (Citation1998) provides that if the RMSA value is in the range <0.5; 0.8>, the SEM model is accepted. The values of the NFI and CFI fit tests are below the limit of perfect agreement.

Based on the above results of the SEM model verification, hypotheses H1,…, H7 are supported.

5. Discussion

The results of the SEM model of the specific research areas of business risks and BFs allowed us to set up an interesting discussion platform. It was identified that the perception of positive future business is influenced by all identified types of business risks. The level of their impact is not the same as that which is also connected with the many macroeconomic effects as well as the attitudes of the examined SMEs. The effective risk management in SMEs is deciding to a large extent whether they are fit to survive in the market and contributes to the development not only of a company but also its market and social environment. At the same time, note the appropriate risk management requires a certain degree of risk perception in a given business environment, risk identification, planning and alignment of preventive measures, or risk management systems (Ślusarczyk & Grondys, Citation2019). The results show that financial risk has the most significant positive impact on a perception of the future (path coefficient - PC = 0.16). Financial risk is determined by a positive perception of financial risk as part of everyday life as well as a positive perception of financial performance. Financial risk largely explains the perception of the financial performance of a business which is linked to the perception of financial risk as part of everyday life. Ausloos et al. (Citation2018) argues that a reasonable company's performance assessment is required to review the need for investment in the light of a credible expected long-term increase in sales, assets and other profitability indicators. The indicators such as the respondent's ability to understand the most important aspect of financial risk and the respondent's ability to properly manage financial risk do not form financial risk. It appears that the level of financial risk is most dependent on the macroeconomic situation of the country, thus macroeconomic indicators, and to a lesser extent on managerial characteristics. It raises many questions for discussion related to the survey of managerial competencies and the personality traits of managers, or their financial literacy, etc.

Operational risk has the second most important positive effect on the perception of a positive future (PC = 0.13). Operational risk is determined by a reasonable utilisation of corporate resources, reducing customer complaints concerning the quality of products/services as well as the company not being so dependent on a limited number of suppliers. Operational risk as a factor is best explained by the reasonable utilisation of corporate resources. An interesting finding is that service/product innovation and their positive reflection on the stability (performance) of a company is not an indicator that would determine operational risk. It is because operational risk is attached to the quality of the business process management while innovation processes are attached to the company at the stage preceding the process management, e.g. at the stage of product development, investment decision-making, modernization of production and services, etc. The results of the research are also supported by Mafini and Muposhi (Citation2017) and Sinha et al. (Citation2011) studies.

Market risk is another significant factor with a positive effect on the perception of a favourable future of the company (PC = 0.12). A positive perception of capital adequacy, i.e. expected lack of sales, as well as a reasonable challenge for selling products/services determines market risk. These results are supported by the conclusions of O'Cass and Sok (Citation2014). The influence of business competitors as a driving factor for entrepreneurs and the company's ability to acquire new markets in innovative ways have not been confirmed as important determinants of market risk. The results of the research are opposite to the results of studies by Vargas-Hernández et al. (Citation2016) and De Clercq et al. (Citation2013) who argue that SMEs have low working capital in comparison with their bigger competitors and they must adopt sophisticated and effective investment, innovation and competitive strategies. Therefore, it becomes the focus to examine the extent to which and in what types of companies, with a view to their sector differentiation and size, innovative development is important as a factor of prosperity and long-term progress of a company. Innovative development is associated with the allocation of capital which may not be available to every company. In particular, SMEs have many limitations in terms of their access to or funding of innovation.

The values similar to market risk were also identified in the perception of BF (PC = 0.12). Positive attitudes of entrepreneurs toward statements: BF is a natural part of business; BF does not mean the entrepreneur’s failure; BF does not reduce self-confidence, and the correct understanding of a commitment to prevent BF has a positive effect on the entrepreneurs' perception of a positive future. BF as a factor best explains the entrepreneurs’attitudes toward the self-confidence statement. The perception of BF (bankruptcy) as a factor is not derived from the indicator: the specific BF experience of an entrepreneur. Cacciotti et al. (Citation2016) says that fear of failure may also affect business motivation but not always in a negative way. In many cases, it may involve the decision to take an even more conservative approach. In addition, there are business performance, prosperity and profit margin implications. Thus it becomes the focus to more deeply study the factors determining the managers’ risk acceptance level depending on the risk quantification and the impact on the further development of a company. Being highly conservative in the decision-making processes can lead to business stagnation, a low level of creativity in the process of the identification of the ways for business growth and ultimately, apathetic managers and hampering their motivation levels in other business activities.

Legal risk is an equally positive factor that influences the perception of future business (PC = 0.07). The positive attitude of entrepreneurs was as follows: i. the legal environment in the CR is not overregulated; ii. legal risk is considered as reasonable (without any adverse impact on business); iii. the basic legal aspect of business as a factor (legal risk) has a positive effect on the positive perception of future business. These findings are directly proportional to the study of Cepel et al. (Citation2018). It would be interesting to review these attitudes in different phases of the business cycle, e.g. in the aftermath of the economic crisis, or after a pandemic and any other globalisation threats when managers are more sensitive to the legal aspects of business and tend to exert pressure and seek legislative changes through many relevant institutions.

Personnel risk is another significant factor with a positive impact on the perception of a positive future (PC = 0.05). The positive attitudes of entrepreneurs toward the interest of employees to increase their performance and low employee turnover in the company are the indicators that measure personnel risk. Redmond and Sharafizad (Citation2020) also emphasize the interest of employees to improve their performance. Respondents' attitudes toward the employee error rate or the adequacy of personnel risk are not measured by this indicator. These factors can also be identified as traditional where changes are seldom observed. The company's performance and a low turnover rate have always been the essential parameter of business success in different types of companies and are also the cardinal indicators of measurement systems.

The positive perception of future business is also influenced by the positive attitudes of entrepreneurs toward the selected statements on strategic risk (PC = 0.02). This factor has the least impact on the perception of future business. Regular monitoring, evaluation and management of strategic risk by the company as well as the fact that the company has implemented a strategic management system are all of the indicators that measure strategic risk. Regular monitoring, evaluation and management of strategic risks by the company is better explained by strategic risk. This factor is not determined by the opinion of entrepreneurs that quality strategic management increases the company’s competitiveness. These conclusions are in direct agreement with Klammer et al. (Citation2017). Nor this factor is determined by the position that strategic management is an important part of corporate governance. This attitude of the companies under review shows a lack of perception of the importance of strategic management in the SME segment, the absence of the development of formalized strategies and their related strategic planning processes. This in turn explains why SMEs do not implement performance measurement and management systems that have been used abroad for more than two decades and are also applied by SMEs. No measurement system can be set up without vision and strategy definition, and strategic and operational goals, and without a monitoring and evaluation system in place, and this is another reason why many small companies will not survive during challenging times.

6. Conclusion

The aim of the study was to review the impact of entrepreneurs' attitudes toward the defined business risks on the perception of the future of companies in the SME sector.

The results show the identified market, financial, personnel and operational risk have a positive effect on future business of SMEs. Operational risk has the most significant positive effect on future business in the form of the utilisation of corporate resources. Other significant risks with a positive effect include financial and strategic risk. The results showed a positive effect of corporate risk management and entrepreneurs' attitudes toward the threat of business failure on the perception of future business of a company. Different types of risks and their impact on future business were also confronted with research studies to provide a discussion platform. In the crisis and post-crisis times, these comparative trajectories may lose their significance due to changes in the risk prioritization currently perceived by entrepreneurs. A financial and economic crises will significantly change the views of risk management not only within SMEs but also in large companies. Companies of all sizes are now taking a proactive approach to risk management, seeking to centralize risk management and develop integrated management systems. It is not only a national but a pan-European trend. The most common goal of risk management would be to eliminate the impact of risk on the economic result. Businesses try to eliminate the negative impact of the different types of risks on the economic result in accordance with legal requirements which was evident when the area of legal risks was reviewed. Businesses are aware of the need for better risk management in connection with the ever more challenging external business conditions in the post-crisis times, so they must pay more attention to internal controls and process changes to eliminate risk. Importantly, businesses must also identify new types of risks not previously monitored and evaluated by them. Legal risk, as well as risks involved in international trade become ever more challenging which generates pressures to set up special risk management teams, or even departments and divisions in large companies. The biggest barriers that will prevent companies from managing risks effectively in the future include the availability of information, both internal and external, required to manage and evaluate risks and integrate them into decision-making processes. The study and its results call for the creation of specific databases to support research in this field and help develop relevant policies and set up stabilisation and regulatory mechanisms for SME support and eliminate the impact of economic and epidemiological crises and disasters directly projected into the economy of countries and their further development.

The study is limited by a lower number of respondents in the research sample (454) although the total number of business entities invited to participate was quite high − 8000 SMEs in the CR. It is not the issue of data collection in a given country, or a problem stemming from the nature of research, but a clear consequence of general apathy and the burden perceived by entrepreneurs to monitor and submit any kind of data about their businesses. As a result, agencies focused on the support of the business environment and did not gather extensive and comprehensive business data which does not provide a platform for creating the necessary conceptual framework of policies for the government and other relevant institutions. The results of the study were supposed to eliminate this research gap and provide the current relevant outputs from the research of various types of risks for the future business and development of SMEs. At the same time, they highly appeal for creating dedicated SME databases to support the formation of national and international benchmarking indicators. During the covid-19 pandemic, the importance of dealing with this issue has significantly grown and provides a strategic platform in the economic policy of governments.

Future research will focus on verifying the results achieved on a new sample of SMEs in the CR, but also on the identification of disparities within the perception of the business risks on the future of enterprises between entrepreneurs the Vysehrad Group countries.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Alnoor, A. (2020). Human capital dimensions and firm performance, mediating role of knowledge management. International Journal of Business Excellence, 20(2), 149–168. doi:https://doi.org/10.1504/IJBEX.2020.105357

- Audretsch, D. B., & Keilbach, M. (2005). Entrepreneurship capital and regional growth. The Annals of Regional Science, 39(3), 457–469. doi:https://doi.org/10.1007/s00168-005-0246-9

- Ausloos, M., Cerqueti, R., Bartolacci, F., & Castellano, N. G. (2018). SME investment best strategies. Outliers for assessing how to optimize performance. Physica A: Statistical Mechanics and Its Applications, 509, 754–765. https://doi.org/https://doi.org/10.1016/j.physa.2018.06.039Ff

- Babin, B. J., Hair, J. F., & Boles, J. S. (2008). Publishing research in marketing journals using structural equations modeling. Journal of Marketing Theory and Practice, 16(4), 279–285. doi:https://doi.org/10.2753/MTP1069-6679160401

- Balan, M., Marin, S., Mitan, A., Pînzaru, F., Vătămănescu, E.-M., & Zbuchea, A. (2019). Leaders in focus: Generational differences from a personality-centric perspective. Management & Marketing. Challenges for the Knowledge Society, 14(4), 372–385. doi:https://doi.org/10.2478/mmcks-2019-0026

- Balcaen, S., & Ooghe, H. (2006). 35 years of studies on business failure: An overview of the classic statistical methodologies and their related problems. British Accounting Review, 38(1), 63–93. https://doi.org/https://doi.org/10.1016/j.bar.2005.09.001

- Belas, J., Smrcka, L., Gavurova, B., & Dvorsky, J. (2018). The impact of social and economic factors in the credit risk management of sme. Technological and Economic Development of Economy, 24(3), 1215–1230. doi:https://doi.org/10.3846/tede.2018.1968

- Bentler, P. M. (1990). Comparative fit indexes in structural models. Psychological Bulletin, 107(2), 238–246. https://doi.org/https://doi.org/10.1037/0033-2909.107.2.238

- Bosma, N., Content, J., Sanders, M., & Stam, E. (2018). Institutions, entrepreneurship, and economic growth in Europe. Small Business Economics, 51(2), 483–499. https://doi.org/https://doi.org/10.1007/s11187-018-0012-x

- Brown, T. A. (2015). Confirmatory factor analysis for applied research. The Guilford Press. 2015. ISBN 978-1462-1536-3.

- Byrne, D. G., & Reinhart, M. I. (1989). Work characteristics, occupational achievement and the type A behaviour pattern. Journal of Occupational Psychology, 62(2), 123–134. doi:https://doi.org/10.1111/j.2044-8325.1989.tb00483.x

- Cacciotti, G., Hayton, J. C., Mitchell, J. R., & Giazitzoglu, A. (2016). A reconceptualization of fear of failure in entrepreneurship. Journal of Business Venturing, 31(3), 302–325. doi:https://doi.org/10.1016/j.jbusvent.2016.02.002

- Caseiro, N., & Coelho, A. (2018). Business intelligence and competitiveness: The mediating role of entrepreneurial orientation. Competitiveness Review: An International Business Journal, 28(2), 213–226. doi:https://doi.org/10.1108/cr-09-2016-0054

- Cepel, M., Stasiukynas, A., Kotaskova, A., & Dvorsky, J. (2018). Business environment quality index in the SME segment. Journal of Competitiveness, 10(2), 21–40. doi:https://doi.org/10.7441/joc.2018.02.02

- Chłodnicka, H., & Zimon, G. (2020). Bankruptcu risk assessment measures of polish SMEs. WSEAS Transactions on Business and Economics, 17, 14–20. https://doi.org/https://doi.org/10.37394/23207.2020.17.3

- De Clercq, D., Dimov, D., & Thongpapanl, N. T. (2013). Organizational social capital, formalization, and internal knowledge sharing in entrepreneurial orientation formation. Entrepreneurship: Theory and Practice, 37(3), 505–537. doi:https://doi.org/10.1111/etap.12021

- Dickson, P. H., & Weaver, K. M. (2008). The role of the institutional environment in determining firm orientations towards entrepreneurial behavior. International Entrepreneurship and Management Journal, 4(4), 467–483. doi:https://doi.org/10.1007/s11365-008-0088-x

- Dincă, V. M., Dima, A. M., & Rozsa, Z. (2019). Determinants of cloud computing adoption by Romanian SMEs in the digital economy. Journal of Business Economics and Management, 20(4), 798–798. https://doi.org/https://doi.org/10.3846/jbem.2019.985620.

- Dvorsky, J., Petrakova, Z., Ajaz Khan, K., Formanek, I., & Mikolas, Z. (2020). Selected aspects of strategic management in the service sector. Journal of Tourism and Services, 11(20), 109–123. doi:https://doi.org/10.29036/jots.v11i20.146.

- Games, D., & Roliza, R. (2019). SME internal capability and competitive advantage in an emerging market: Moderating effects of firm age. AMAR (Andalas Management Review)), 3(1), 103–114. doi:https://doi.org/10.25077/amar.3.1.103-114.2019

- Gede Riana, I., Suparna, G., Gusti Made, I., Kot, S., & Rajiani, I. (2020). Human resource management in promoting innovation and organizational performance. Problems and Perspectives in Management, 18(1), 107–118. doi:https://doi.org/10.21511/ppm.18(1).2020.10

- Gordon, L. A., Loeb, M. P., & Tseng, C. (2009). Enterprise risk management and firm performance: A contingency perspective. Journal of Accounting and Public Policy, 28(4), 301–327. doi:https://doi.org/10.1016/j.jaccpubpol.2009.06.006

- Gorzeń-Mitka, I. (2019). Interpretive structural modeling approach to analyze the interaction among key factors of risk management process in SMEs: Polish experience. European Journal of Sustainable Development, 8(1), 339–349. doi:https://doi.org/10.14207/ejsd.2019.v8n1p339

- Grimsdottir, E., & Edvardsson, I. R. (2018). Knowledge management, knowledge creation, and open innovation in icelandic SMEs. Entrepreneurship/Small Business, 8(4), 1–13. https://doi.org/https://doi.org/10.1177/2158244018807320

- Herath, H. M. A., & Mahmood, R. (2014). Strategic orientations and SME performance: Moderating effect of absorptive capacity of the firm. Asian Social Science, 10(13), 95–107. doi:https://doi.org/10.5539/ass.v10n13p95

- Habanik, J., Martosova, A., & Letkova, N. (2020). The impact of managerial decision-making on employee motivation in manufacturing companies. Journal of Competitiveness, 12(2), 38–50. doi:https://doi.org/10.7441/joc.2020.02.03

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate data analysis. Prentice Hall.

- Hanzaee, K. H., Ghalandari, K., & Norouzi, A. (2011). The effect of brand social power dimensions on purchasing decision based on Iranian customers' subjective readiness. World Applied Sciences Journal, 13(5), 1197–1208.

- Hooper, D., Coughlan, J., & Mullen, M. R. (2008). Structural equation modelling: Guidelines for determining model fit. Electronic Journal of Business Research Methods, 6(1), 53–60.

- Karabag, S. F. (2019). Factors impacting firm failure and technological development: A study of three emerging-economy firms. Journal of Business Research, 98, 462–474. doi:https://doi.org/10.1016/j.jbusres.2018.03.008

- Klammer, A., Gueldenberg, S., Kraus, S., & ÓDwyer, M. (2017). To change or not to change – antecedents and outcomes of strategic renewal in SMEs. International Entrepreneurship and Management Journal, 13(3), 739–756. doi:https://doi.org/10.1007/s11365-016-0420-9

- Levy, R. (2011). Bayesian data-model fit assessment for structural equation modeling. Structural Equation Modeling, 18(4), 663–685. doi:https://doi.org/10.1080/10705511.2011.607723

- Lima, P. F. D., Crema, M., & Verbano, C. (2020). Risk management in SMEs: A systematic literature review and future directions. European Management Journal, 38(1), 78–94. doi:https://doi.org/10.1016/j.emj.2019.06.005

- Lutz, C. H. M., Kemp, R. G. M., & Dijkstra, S. G. (2010). Perceptions regarding strategic and structural entry barriers. Small Business Economics, 35(1), 19–33. doi:https://doi.org/10.1007/s11187-008-9159-1

- Mafini, C., & Muposhi, A. (2017). Predictive analytics for supply chain collaboration, risk management and financial performance in small to medium enterprises. Southern African Business Review, 21, 311–338.

- Malega, P., Rudy, V., Kovac, J., & Kovac, J. (2019). The competitive market map as the basis for an evaluation of the competitiveness of the Slovak Republic on an International Scale. Journal of Competitiveness, 11(4), 113–119. doi:https://doi.org/10.7441/joc.2019.04.07

- Neary, B., Horak, J., Kovacova, M., & Valaskova, K. (2018). The future of work: Disruptive business practices, technology-driven economic growth, and computer-induced job displacement. Journal of Self-Governance and Management Economics, 6(4), 19–24. https://doi.org/https://doi.org/10.22381/JSME6420183

- Ngoc Mai, A., Van Vu, H., Xuan Bui, B., & Quang Tran, T. (2019). The lasting effects of innovation on firm profitability: Panel evidencefrom a transitional economy. Economic Research-Ekonomska Istraživanja, 32(1), 3417–3430. doi:https://doi.org/10.1080/1331677X.2019.1660199

- O’Cass, A., & Sok, P. (2014). The role of intellectual resources, product innovation capability, reputational resources and marketing capability combinations in firm growth. International Small Business Journal: Researching Entrepreneurship, 32(8), 996–1018. doi:https://doi.org/10.1177/0266242613480225

- Olah, J., Kovacs, S., Virglerova, Z., Lakner, Z., Kovacova, M., & Popp, J. (2019). Analysis and comparison of economic and financial risk sources in SMEs of the visegrad group and Serbia. Sustainability, 11(7), 1853.

- Psarska, M., Vochozka, M., & Machova, V. (2019). Performance management in small and medium-sized manufacturing enterprises operating in automotive in the context of future changes and challenges in SR. AD ALTA: Journal of Interdisciplinary Research, 9(2), 281–287.

- Redmond, J., & Sharafizad, J. (2020). Discretionary effort of regional hospitality small business employees: Impact of non-monetary work factors. International Journal of Hospitality Management, 86, 102452. doi:https://doi.org/10.1016/j.ijhm.2020.102452

- Rowland, Z., Machova, V., Horak, J., & Hejda, J. (2019). Determining the market value of the enterprise using the modified method of capitalized net incomes and Metfessel allocation of input data. AD ALTA: Journal of Interdisciplinary Research, 9(2), 305–310.

- Santisteban, J., & Mauricio, D. (2017). Systematic literature review of critical success factors of information technology startups. Academy of Entrepreneurship Journal, 23(2), 1–23.

- Shane, S., Nicolaou, N., Cherkas, L., & Spector, T. D. (2010). Do openness to experience and recognizing opportunities have the same genetic source? Human Resource Management, 49(2), 291–303. doi:https://doi.org/10.1002/hrm.20343

- Sinha, P., Akoorie, M. E., Ding, Q., & Wu, Q. (2011). What motivates manufacturing SMEs to outsource offshore in China? Comparing the perspectives of SME manufacturers and their suppliers. Strategic Outsourcing: An International Journal, 4(1), 67–88. doi:https://doi.org/10.1108/17538291111108435

- Ślusarczyk, B., & Grondys, K. (2019). Parametric conditions of high financial risk in the SME Sector. Risks, 7(84), 1–17. doi:https://doi.org/10.3390/risks7030084

- Smith, R. M., Schumacker, R. E., & Bush, M. J. (1998). Using item mean squares to evaluate fit to the Rasch model. Journal of Outcome Measurement, 2(1), 66–78.

- Stenholm, P., Acs, Z. J., & Wuebker, R. (2013). Exploring country-level institutional arrangements on the rate and type of entrepreneurial activity. Journal of Business Venturing, 28(1), 176–193. doi:https://doi.org/10.1016/j.jbusvent.2011.11.002

- Süsi, V., &Lukason, O. (2019). Corporate governance and failure risk: evidence from Estonian SME population. Management Research Review, 42(6), 703–720. doi:https://doi.org/10.1108/MRR-03-2018-0105

- Svarova, M., & Vrchota, J. (2013). Strategic management in micro, small and medium-sized businesses in relation to financial success of the enterprise. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 61(7), 2859–2866. doi:https://doi.org/10.11118/actaun201361072859

- Trif, S.-M., Duțu, C., & Tuleu, D.-L. (2019). Linking CRM capabilities to business performance: A comparison within markets and between products. Management & Marketing. Challenges for the Knowledge Society, 14(3), 292–303. doi:https://doi.org/10.2478/mmcks-2019-0021.

- Ucbasaran, D., Shepherd, D. A., Lockett, A., & Lyon, S. J. (2013). Life after business failure: The process and consequences of business failure for entrepreneurs. Journal of Management, 39(1), 163–202. doi:https://doi.org/10.1177/0149206312457823

- Vargas-Hernández, J. G., Casas Cardenaz, R., & Calderón Campos, P. (2016). Internal control and organizational culture in small businesses: A conjunction to competitiveness. Journal of Organisational Studies and Innovation, 3(2), 16–30.

- Vochozka, M., Psarska, M. (2016). Factors supporting growth of added value, performance and competitiveness of SMEs and selected EU countries. In Proceedings of the Innovation Management Entrepreneurship and Corporate Sustainability (pp. 756–767).

- Wang, Y. (2016). What are the biggest obstacles to growth of SMEs in developing countries? – An empirical evidence from an enterprise survey. Borsa Istanbul Review, 16(3), 167–176. doi:https://doi.org/10.1016/j.bir.2016.06.001

- Wegner, D., Zarpelon, F. M., Verschoore, J. R., & Balestrin, A. (2017). Management practices of small-firm networks and the performance of member firms. Business: Theory and Practice, 18 (0), 197–207. doi:https://doi.org/10.3846/btp.2017.021

- Wheaton, B., Muthén, B., Alwin, D. F., & Summers, G. F. (1977). Assessing reliability and stability in panel models. In D. R. Heise (Ed.), Soxciological methodology 1977 (pp. 84–136). Jossey-Bass. https://doi.org/https://doi.org/10.2307/270754[]

- Yang, J. S. (2017). The governance environment and innovative SMEs. Small Business Economics, 48(3), 525–541. https://doi.org/https://doi.org/10.1007/s11187-016-9802-1

- Zhao, H., & Seibert, S. E. (2006). The big five personality dimensions and entrepreneurial status: A meta-analytical review. The Journal of Applied Psychology, 91(2), 259–271. https://doi.org/https://doi.org/10.1037/0021-9010.91.2.259