?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Relying on panel firm-level data from an emerging economy, the paper postulates and empirically verifies the pattern of a U-shaped relationship between cash flows and cash holdings. The positive cash-cash flow sensitivity is postulated to be driven by precautionary motive, which is engendered by excessive volatility of cash flows. Therefore, cash accumulation appears to serve the primary purpose of mitigating the problem of unpredictability of cash flows. While revealing no significant cash-cash flow relationship for the majority of firms, the analysis of firm-level cash-cash flow sensitivity coefficients shows that the companies with the lowest and the highest cash flows maintain disproportionately higher cash reserves than their counterparts with intermediate cash flows. The firms exhibiting negative cash-cash flow relationship are found to be of younger age, smaller size, lower liquidity, and asset tangibility than the remainder of the research sample. These firms are evidenced to accumulate cash reserves from equity issuances, while their overall capacity to procure external financing remains impaired. Their financing patterns are reminiscent of the agency problem of ‘gambling for resurrection’. In turn, the firms exhibiting positive cash-cash flow sensitivity are documented to maintain cash reserves in order to be able to alleviate cash flow volatility.

1. Introduction

The advancements in the theory of information asymmetry and capital market frictions allowed for a better understanding of the underlying mechanisms shaping corporate financial management strategies (Bernanke & Gertler, Citation1989; Myers & Majluf, Citation1984; Stiglitz & Weiss, Citation1981). Empirical studies evidenced that capital market imperfections may exercise a profound impact on every aspect of corporate decision making including corporate investment (Bhagat et al., Citation2005, Cleary, Citation1999; Fazzari et al., Citation1988; etc.), financing decisions (Faulkender & Petersen, Citation2006; Hugonnier et al., Citation2015, etc.), and cash management practices (Almeida et al., Citation2004; Han & Qiu, Citation2007; Polak et al., Citation2018, etc.).

Conventionally, it is assumed that a firm’s marginal propensity to accumulate cash holdings should be monotonically increasing in its exposure to financing constraints (Almeida et al., Citation2004). The company’s limited capacity to substitute external financing for the plummeting cash flows may force the management to recur to precautionary cash savings. Due to their larger exposure to information asymmetry and adverse selection on capital markets, young growth companies with valuable growth opportunities are expected to exhibit the highest propensity to accumulate cash holdings in anticipation of cash flow fluctuations and emergence of attractive investment projects (Hadlock & Pierce, Citation2010).

Empirical evidence, however, demonstrates that the overall increase in the level of corporate cash holdings may not be fully explained with the increased volatility of cash flows and the degree of financing constraints (Bates et al., Citation2009; Chen et al., Citation2017). The fact that in many cases the levels of corporate cash holdings are more than sufficient to repay the companies’ entire outstanding debt or to replace their fixed assets, makes the study of determinants of corporate cash holdings a worthy research problem. It is true that liquidity reserves have served firms well in insulating them from external shocks related to both credit market crunch, like the one of 2008, which limited firms’ access to external financing and forced them to deleverage, and demand-side contraction like the one of 2020 caused by the COVID19 pandemic. Increasing global uncertainty provides a justification for corporate austerity (Phan et al., Citation2019). However, the persistence of precautionary cash reserves in times of robust aggregate demand may become a source of hindrance and put a downside pressure on corporate performance.

The conventional theory postulates that for the financially constrained companies, cash holdings are an increasing function of the internally generated cash flows, while the financially unconstrained firms should exhibit no significant cash-cash flow relationship (Almeida et al., Citation2004; Hadlock & Pierce, Citation2010). While this argument is indeed compelling and enjoys an overall consent in the empirical literature (Acharya et al., Citation2007; Campello et al., Citation2010; Michalski et al., Citation2017), it may provide an incomplete picture of the cash management tradeoffs under capital market frictions. We argue that the cash-cash flow relationship manifests nonmonotonicity: while for the majority of firms, there is a positive relationship between cash flows and cash holdings, a certain subsample of firms may exhibit negative cash-cash flow sensitivity. Along with studying the distinguishing features of these firms, we demonstrate that the presence of the empirically observed nonlinearity may complicate the measurement of cash-cash flow sensitivity coefficients. The latter are frequently used as indicator/measure of the degree of financing constraints.

To start with, empirical studies do not report any cases of the empirically observed negative cash-cash flow sensitivity. While not being explicitly accommodated in the theoretical model of liquidity demand, which allows only for a positive and indeterminate cash-cash flow relationship (Almeida et al., Citation2004), the negative cash-cash flow sensitivity may represent a non-trivial case of cash management strategy, which deviates from the traditionally postulated patterns. One may inquire into the reasons forcing a firm to accumulate cash reserves as cash flows decrease and vice versa. In our opinion, the explanation for this pattern of decision making may be derived from the existing analytical models of intermediated lending (for example, the model by Holmström and Tirole (Citation1997) or by Martin and Santomero (Citation1997)), which stipulate that obtaining access to external finance requires that firms either generate stable cash flows or maintain substantial internal liquidity reserves. The liquidity reserves may signal the quality of envisaged investment projects to the uninformed investors, while simultaneously providing the necessary cushion for accommodating emerging investment projects, which may not have been financed from the limited cash flows. If that is the case, we may expect the three following conjectures to hold: 1) the firms generating the lowest cash flows should primarily accumulate their cash reserves from the proceeds of equity issuances; 2) the firms with the lowest cash flows should exhibit negative cash flow sensitivity of cash holdings; 3) the firms with the lowest cash flows should have an impaired capacity to incur external financing. Excessive volatility of cash flow accompanied with lack of possibilities to hedge against the underlying risk factors may force firms to hold precautionary cash reserves (Duchin et al., Citation2010; Chen et al., Citation2020): the precautionary cash reserves play the role of a hedging device with the cost being the return on investments that the company has to forego in order to fuel its liquidity reserves. That being said, one should expect the companies experiencing substantial cash flow volatility to put aside a major portion of their cash flows in order to cater for the future liquidity needs. Therefore, the choice of a cash management strategy becomes contingent upon the predicted cash flow fluctuations: cash reserves stockpiled by the firms should be sufficient to finance their future investment demand, financial liabilities, and potential operating losses, which have probabilistic nature and cannot be predicted with certainty. The situation may be complicated by the fact, that due to the opaqueness of its operation or lack of sufficient collateral, the firm may experience difficulties accessing external capital markets (Keefe & Yaghoubi, Citation2016). The binding financing constraints may increase the company’s propensity to accumulate cash reserves with the only source of funds being the internally generated operational cash flow.

Our theoretical predictions have been tested on empirical data from the largest emerging economy of the CEE region – Poland. Empirical literature appears to offer only a limited coverage of the manifestations of financing constraints and their consequences on emerging markets, particularly in the domain of corporate treasury management. Transitioning financial markets are characterised with a relatively more difficult access to external financing, which complicates the implementation of long-term investment projects. A lack of a well-functioning and liquid public capital markets force companies – many of which are still at relatively early stages of their life cycle – to rely on internal cash flows to fund investment opportunities, which may hinder growth and delay the implementation of expansion options. Poland represents an interesting case in this respect as its financial markets exhibit several inherent features worthy of empirical investigation with regards to their impact on corporate financial management strategies. To start with, Polish firms tend to largely rely on intermediated rather than direct financing. Banks play a preponderant role in providing firm with external capital. The bulk of credit action is initiated by 38 large and mostly foreign-owned commercial banks (Jackowicz et al., Citation2020), which prioritise collaterised lending thereby effectively curtailing the access of younger and more intangible businesses to the currently plentiful external capital. Cooperative banks, which tend to build longer-term customer relationships and specialise in dealing with borrower-lender information asymmetry, may partially alleviate the problem (Hasan et al., Citation2017). However, the scale of these banks’ operations remain limited due to their relatively smaller size. Public capital markets are characterised by relatively low liquidity and insufficient depth. Bond market is dominated by government debt while the stock market appears to experience a lack of inflow of funding from large long-term institutional investors. As a result, empirical data demonstrate that Polish firms continue experiencing the repercussions of binding financing constraints despite deregulation and rapid development of financial intermediation (Jackowicz et al., Citation2016), which may bear substantial consequences for financial management strategies in the Polish corporate sector. In particular, uncertain and frequently limited access to external financing coupled with elevated volatility of internally generated cash flows – which is inherent in emerging markets - may cause Polish firms to amass higher precautionary cash reserves (Phan et al., Citation2019). That, in turn, may impede their investment demand and constrain organic growth.

Recognising the possible distortionary impact that capital market frictions may have on companies’ financials, we inquire into intertemporal patterns of cash management within Polish firms. The principal research question the study attempts to answer is as follows:

RQ. What is the impact of financing constraints on the cash management practices of Polish companies?

We start by studying the determinants of firm-level cash-cash flow sensitivity coefficients. We document that the highest cash-cash flow sensitivity is exhibited by firms, which are larger and older than the remainder of the sample. These companies generate the highest cash flows, have the highest asset tangibility, and the greatest growth opportunities measured by market-to-book value ratio. The fundamentals of these firms along with their relatively higher capacity to procure external financing and higher propensity to pay dividends, are not indicative of their financially constrained status. However, one of the decisive features forcing them to accumulate cash is the high volatility of cash flows. Therefore, we postulate that for these companies, cash reserves play the role of a hedging device against anticipated cash flow fluctuations. In contrast, firms exhibiting negative cash flow sensitivity of cash holdings are found to be younger, smaller, and less tangible than the remainder of the sample. In line with our predictions, along with maintaining the highest cash reserves in the sample, these firms are evidenced to exhibit the highest sensitivity of cash holdings to equity issuances. Their overall capacity to use external financing is documented to be the lowest in the sample.

The paper contributes to the discussion of the financial management practices under incomplete capital markets. We revisit the role of financial intermediation in shaping corporate decisions with regards to liquidity management. We document the nonlinearity of cash-cash flow relationship, which accords with the existing theoretical models of financial intermediation, but which, to our best knowledge, has not been reported in the literature.

The remainder of the paper is structured as follows. First, we introduce the research sample and outline the research methodology utilised in the empirical part of the paper. A further section explains the key empirical findings while relating them to prior econometric studies on the topic of financing constraints. The final section is dedicated to the discussion of managerial and policy implications of the key findings.

2. The Sample Structure

The research sample, which is used for testing our conjectures, comprises all non-financial public Polish companies observed over the period 1999–2017. The sample englobes all firms, which were listed on the Warsaw Stock Exchange, including those which have been delisted or ceased to exist. In order to study the population patterns, we do not impose any restrictions on the company fundamentals, i.e., we do not eliminate negative cash flow observations as well as those which represent cases of non-organic growth, e.g., mergers and acquisitions. The data were compiled from Thomson Reuters Eikon and Notoria databasesFootnote1 as well as from the Polish National Company Registrar. We eliminated all financial companies (based on general industry classification codes) due to the specificity of their operational activities.

The key research variables were trimmed at 1% and 99% levels in order to eliminate outliers. The resulting unbalanced panel dataset comprises 8244 observations covering 960 companies. The minimum length of the observation window for each company is one year, the maximum length is 18 years. The definitions of all variables used in econometric models are presented in Panel A of . The descriptive statistics for the research sample are summarised in Panel B of .

Table 1. Definitions of variables and descriptive statistics for the research sample.

The descriptive statistics demonstrate that the sample is heterogenous in terms of company fundamentals. The research covers 25 industries (under national classification) and may be regarded as broadly representative of the population of Polish companies. Some of them are young and small, and have only recently started their track record as public companies by offering stocks through the NewConnect platform for small-cap firms. Others (large industrial conglomerates) have a long history of state stewardship, and have recently gone through a process of privatisation and restructuring.

3. The Specification of Variables

For the purposes of econometric analysis, cash flows ( are defined as operating cash flows adjusted for extraordinary items. Cash holdings (

are defined as the value of the company’s cash and cash equivalents reported in the balance sheet in a given year. We use contemporaneous value of firms’ fixed assets (

) to scale the nominal variables. All nominal variables were adjusted for inflation.

In order to explain the cash management patterns exhibited by sampled firms, we use various proxies for the factors, which have been commonly identified as the key determinants of liquidity demand in the empirical literature.

The price-to-book value ratio ( is used as a proxy for medium- and long-term growth opportunities. The possible measurement errors, which render the market-to-book value ratios a noisy measure of growth opportunities (Cummins et al., Citation2006), make us recur to alternative proxies for immediate growth opportunities, e.g., 1) sales growth, which is calculated as the year-on-year relative change in the value of firms’ revenue; 2) capital expenditures scaled by contemporaneous value of firms’ fixed assets (

).

Asset tangibility, defined as a ratio of the company’s fixed assets to the value of total assets, is used as a proxy for the company’s borrowing capacity and the availability of pledgeable assets, which may both alleviate the degree of financing constraints and reduce the need to maintain significant cash reserves (Moshirian et al., Citation2017). Similarly, debt-to-equity ratio may reasonably well approximate the company’s access to external finance as well as the company’s propensity to utilise its debt capacity (Kaplan & Zingales, Citation1997).

The hedging needs of the company are described using two variables, which reflect the riskiness of the company’s operations: 1) the volatility of cash flows defined as the standard deviation of the variable 2) cash flow fluctuations calculated as the year-on-year relative change of

The overall financial situation of the company is reflected in the value of the Altman’s Z-score (Altman, Citation2000).

The company’s age (measured as the number of years from the start of the company’s operations), size (approximated by the natural logarithm of the value of total assets adjusted for inflation) and the dividend payout ratio are approximating the degree of information asymmetry (Devereux & Schiantarelli, Citation1990), the exposure to binding financing constraints (Fazzari et al., Citation1988; Hadlock & Pierce, Citation2010) and the stage of the company’s life cycle (Mueller, Citation1972).

In addition to the above variables, we use data retrieved directly from the cash flow statements of the sampled companies and featuring the following variables: 1) net equity issuances defined as the difference between the value of shares issued and repurchased in the given year by the given company; 2) the net debt issuances defined as the difference between the value of the debt issued (through direct or intermediated lending) and debt repaid (securities repurchased/redeemed by the company); 3) net cash accumulation (), which is defined as the change in the balance sheet value of the company’s cash holdings in the given year.

4. The Determinants of the Firm-Level Cash Flow Sensitivity of Cash

Almeida et al. (Citation2004) document that the cash-cash flow sensitivity is primarily driven by the degree of financing constraints that the company faces. Due to their reliance on internal financial resources, the constrained firms are expected to exhibit positive cash flow sensitivity of cash, while the unconstrained firms should exhibit an indeterminate relationship between the dynamics of cash flows and cash holdings. The validity of this argument hinges upon the assumption of the existence of a positive monotonic relationship between the degree of financing constraints and the exhibited patterns of cash flow sensitivity of cash. It might be the case, that the relationship is actually nonmonotonic, which may distort the measurement and interpretation of the empirical findings.

An attempt to distinguish between the firms exhibiting different cash-cash flow sensitivity patterns relying on any specific criteria (e.g., different proxies for the degree of financing constraints) may result in ignoring firm-specific patterns. We show that both the positive and negative cash flow sensitive companies may face binding financing constraints. However, they manifest diverging cash management patterns.

In order to avoid any bias while allocating firms to a particular cash-cash flow sensitivity subsample, it seems reasonable to start by measuring firm-level cash flow sensitivity of cash holdings. The heterogenous firm-level cash-cash flow sensitivity coefficients should better reflect the specific circumstances of each particular company and therefore, are less prone to bias (Hovakimian, Citation2009).

In order to determine the individual cash-cash flow sensitivity coefficients, we run separate univariate regressions for each firm:

(1)

(1)

where

– the firm’s cash holdings in year t scaled by the contemporaneous value of fixed assets;

– the firm’s standardised operating cash flows scaled by the value of fixed assets. The equation features no additional control variables, since including them would mean hardwiring the impact of those variables into the subsequent sample partition. The latter may deprive one of the possibility to disentangle the impact of the particular variables on cash management patterns.

The obtained individual cash-cash flow sensitivity estimates are subsequently used to classify the firm-year observations into three subsamples: 1) the firms exhibiting positive cash-cash flow sensitivity (The Positive CF-Sensitive Subsample); 2) the firms exhibiting negative cash-cash flow sensitivity (The Negative CF-Sensitive Subsample); 3) the firms exhibiting an indeterminate relationship between cash holdings and cash flows (CF-Insensitive Subsample). In contrast to prior studies, we find that a non-negligible subsample of firms (124 companies) exhibit a persistently significant negative relationship between cash holdings and cash flows.

The static panel regression analysis using Equationequation (1)(1)

(1) at the level of the cash flow sensitivity subsamples demonstrates that the patterns revealed at the firm level persist (). The positive CF-sensitive subsample exhibits the highest positive sensitivity of cash holdings to the dynamics of cash flows. The negative CF-sensitive firms manifest a negative cash-cash flow association. At the same time, the cash holdings of these firms appear to be strongly driven by the availability of attractive growth opportunities approximated by the price-to-book value ratio. Surprisingly, the CF-insensitive firms demonstrate positive cash-cash flow sensitivity at the subsample level.

Table 2. The estimates of cash flow sensitivity of cash holdings based on the repartition of the research sample relying on heterogenous cash-cash flow sensitivity coefficients.

At this stage, no straightforward conclusions may be reached with regards to the firm-specific features driving cash management decisions in each of the subsamples. In order to analyse the specific features of each of the subsamples, we run binary logit regressions, which estimate the likelihood of the firm being allocated to a particular cash flow sensitivity subsample. The results are presented in .

Table 3. The results of the binary logit regressions estimating the likelihood of the firm being classified into a particular cash-cash flow sensitivity subsample.

The quantitative multivariate analysis suggests that the three cash-cash flow sensitivity subsamples exhibit distinguishing fundamental characteristics, which may significantly impact their financial decisions. The firms, which have been identified as positive CF-sensitive, are found to generate higher cash flows, than the remainder of the research sample. The opposite is true in case of the negative CF-sensitive firms, which are found to generate the lowest cash flow while simultaneously maintaining the highest cash reserves in the research sample.

The positive CF-sensitive firms are evidenced to be larger than the remaining firms and older than the negative CF-sensitive firms. In view of their relative maturity, the positive CF-sensitive firms are found to possess more tangible assets and pay a higher dividend than other companies.

Overall, the preliminary analysis suggests that the positive CF-sensitive firms are the least financially constrained, if one uses age, size and dividend payout as the criteria for operationalising financing constraints as suggested by the empirical literature. Therefore, it seems surprising that these firms exhibit the highest cash flow sensitivity of cash holdings. On the contrary, the negative CF-sensitive firms appear to be the most financially constrained since in addition to being smaller and younger than their counterparts, they possess less tangible assets and generate meager cash flows. In line with prior studies, one would suggest that these firms should exhibit the highest cash-cash flow sensitivity. However, their case is special: as explained by Opler et al. (Citation1999), the largest reductions of the cash reserves are caused by operational losses. Due to the fact that most of the negative CF-sensitive firms consistently exhibit unsatisfactory operating results (negative cash flows), they are the most likely to deplete their liquidity slack. One may logically inquire into the source of cash accumulation by the firms, which while generating the lowest cash flows, manage to maintain the highest (relative) cash reserves. The next section explores this problem in detail.

Continuing the analysis of the cash management patterns within the cash flow sensitivity subsamples, we turn to the measures of the riskiness of cash flows. As argued in the theoretical discussion, cash accumulation may be used as a hedging device against the anticipated cash flow fluctuations. Therefore, one should expect the firms, which historically experienced the highest volatility of cash flows to maintain the highest cash reserves for precautionary reasons.

presents the results of binary logit regressions, which study the impact of the firm’s overall financial health and the riskiness of cash flows on its likelihood of being allocated to a particular cash-cash flow sensitivity subsample.

Table 4. The results of the binary logit regressions estimating the likelihood of the firm being classified into a particular cash-cash flow sensitivity subsample.

The results reported in confirm our prior conjectures. The positive CF-sensitive firms are found to exhibit a relatively higher volatility and more intense cash flow fluctuations than the remaining firms in the sample. At the same time, these companies have a better Z-score and therefore, enjoy a better overall financial standing. In contrast, the negative CF-sensitive firms are found to exhibit the lowest cash flow volatility, while their overall financial health appears to be impaired.

The results of the quantitative analysis strongly suggest that the positive CF-sensitive firms accumulate substantial cash reserves for two reasons: 1) they attempt to alleviate the consequences of the relatively higher cash flow volatility; 2) they enjoy relatively higher cash flows and, therefore, may afford higher rate of cash accumulation without endangering their investment plans or interfering with the financial cash flows. In turn, the primary motive of the negative CF-sensitive firms is the improvement of their relatively weaker financial standing caused by a modest cash flow generating capacity. The negative CF-sensitive firms need to signal the investors, that the company is able to cover the potential losses and expects to continue its operations despite a dismal performance record.

5. The U-Shaped Cash-Cash Flow Relationship: Empirical Evidence

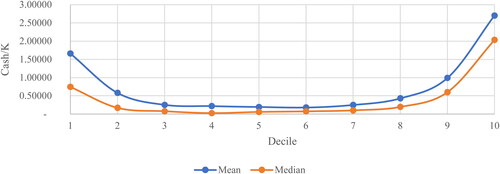

In this section, we test the postulated U-shaped cash-cash flow relationship on the empirical data. First, we calculate the mean and median values of for the sample deciles split on the basis of value of contemporaneous cash flows

in ascending order. evidences the presence of the conjectured pattern of nonlinearity of the cash-cash flow relationship.

Figure 1. The empirically observed U-shaped cash-cash flow relationship.

Source: own elaboration. The chart presents the mean and median values of cash holdings (scaled by the contemporaneous value of the firm’s fixed assets) by sample decile ranked by the value of contemporaneous standardised operating cash flows (scaled by the value of fixed assets) in ascending order

A non-negligible share of research sample exhibits negative cash flow sensitivity of cash holdings. It implies, that for these companies, a decrease of cash flows is accompanied with a higher propensity to accumulate cash reserves. Confirming the prior findings of the static panel regression analysis, the majority of firms are demonstrated to exhibit no evident cash-cash flow sensitivity pattern. In turn, the firms with the highest cash flows (relative to the size of their fixed assets) are found to accumulate the highest amount of cash holdings. The graphical analysis suggests that the cash-cash flow relationship may be reasonably well approximated with a quadratic polynomial function.

In order to confirm the findings derived from graphical analysis, we recur to static panel regression analysis in order to ascertain the robustness of the nonlinear relationship and to check for the presence of convexity, which may be inferred from the initial data screening. The model specification suggested for the empirical tests may be formulated as follows:

(2)

(2)

where

– the vector of control variables. Control variables feature proxies for the firm’s size (natural logarithm of the firm’s total assets), growth opportunities (price-to-book value ratio) and working capital management (

– net working capital investment normalised by the value of the firm’s fixed assets). Size is evidenced to play a major role in shaping corporate liquidity demand due to the presence of the economies of scale in cash management (Opler et al., Citation1999). The price-to-book value ratio is included into the regression since the model of liquidity demand developed by Almeida et al. (Citation2004) explains the company’s liquidity preferences by the value of future investment opportunities available to the company with the relationship reported to be monotonically increasing. Finally, net working capital investment should be included for two reasons: 1) working capital investments constitute one of the uses of the cash flows generated by the company and may, therefore, compete with the cash accumulation for the limited amount of available internal financing; 2) working capital is liquid, therefore, working capital investments may be rescaled in accordance with the company’s ongoing needs without incurring excessive adjustment costs (Fazzari & Petersen, Citation1993). In addition to a vector of control variables, all regression models incorporate year and industry dummies (not reported for reasons of brevity).

The results of the analysis are presented in . The tests suggest that despite an overall positive slope, the cash-cash flow relationship manifests nonlinearity, which may be well approximated with a quadratic function. The dynamics of cash flows is evidenced to play the central role in shaping the firm’s propensity to maintain cash reserves. The analysis of negative cash flow observations confirmed that the negative cash-cash flow relationship is primarily driven by unsatisfactory operating performance with cash holdings playing the role of a buffer assuring the continuity of business.

Table 5. The quadratic polynomial approximation of the cash-cash flow relationship on the complete research sample.

6. The Influence of Cash Management on the Modes of External Financing and Cash Flow Allocation of the Polish Companies

The revealed patterns of cash management pose a question regarding their possible impact on the financing and investment policies of the studied companies. If a representative company manages to sustain significant cash reserves despite consequently bearing operating losses, one should inquire into the sources of financing, which help sustain adequate liquidity despite significant drawdowns. Therefore, in this section, we study the interplay of the cash-cash flow sensitivity patterns with the sources of cash procurement.

A typical company procures cash from two sources: 1) cash flows generated by operating activities; 2) external finance represented by equity injections and debt (both direct and intermediated). If the company experiences feeble cash flows, its only option is to tap on the external sources. However, as evidenced by the implications of the Holmström-Tirole (Citation1997) model, debt financing becomes available only if the company sustains sufficient internal financial resources. Therefore, one should expect cash-strapped firms to primarily rely on equity injections (Park, 2019). Shareholders may be the only party interested in the sustainment and continuation of the company’s operations. The agency problem consisting in financing of the loss-generating business ventures in hope for a reversal of unfavourable trends is called ‘gamble for resurrection’ (Décamps & Faure-Grimaud, Citation2000).

In order to analyse the repartition of the sources of cash relied on by the sampled firms, we formulated the following empirical model:

(3)

(3)

all variables have been defined in the preceding sections. While the patterns of cash flow allocation contingent upon firms’ exposure to financing constraints have been studied on mature markets (Gatchev et al., Citation2010), any such inquiries covering emerging markets are missing.

reports the results of the empirical tests of the model (3). Several important conclusions may be derived therefrom. First of all, the negative CF-sensitive firms manifest the highest propensity to draw on their cash reserves in case of cash flow contraction. This finding confirms our prior conjecture stating that the negative CF-sensitive firms accumulate cash in order to be able to cushion the anticipated fluctuations of cash flows. The propensity to deplete cash reserves decreases along the three cash flow sensitivity subsamples with the positive CF-sensitive firms manifesting the lowest magnitude. In line with expectations, the negative CF-sensitive firms are evidenced to be the most reliant on net equity issuances in filling up their cash reserves. Overall, one may cautiously conclude that the behaviour of negative CF-sensitive firms alludes to the problem of ‘gamble for resurrection’. The reliance on equity finance on the part of the remaining firms is significantly lower.

Table 6. The cash accumulation from the contemporaneous equity and debt issuances.

The coefficients at net debt issuances are similar across the three subsamples. Despite their dismal performance record, the negative CF-sensitive firms are not cut off from capital markets, which may be at least partially due to their substantial liquidity reserves. The latter may serve as an assurance of the shareholders’ commitment to the continuation of firms’ operations and their readiness to step up as primary donors of funds.

Next, we verify, how the cash-cash flow sensitivity patterns may impact the cash flow allocation of the sampled companies. In particular, we would like to investigate, whether the cash flow sensitivity subsamples exhibit any specific patterns with regards to their capacity to procure external financing or fund their investment expansion.

Recognising that the uses of cash flows are intertemporally connected through a chain of business decisions, we recur to the simultaneous equations methodology (Dasgupta & Sengupta, Citation2007; Gatchev et al., Citation2010) to inquire into the patterns of cash flow allocation exhibited by Polish firms.

The system of simultaneous equations deriving from the basic cash flow identity describes the uses of contemporaneous operating cash flows generated by the company. It allows to account for the interplay between alternative uses of funds and therefore, presents an unbiased view on the patterns of short-term business decisions. The general equation specification used in this study may be formulated as follows:

(4)

(4)

where

– the value of fixed investments reported by the i-th firm in the cash flow statement for year t;

– the dividend payment in year t;

– the value of external financing in the form of net equity and net debt issuances procured in year t;

– the change in the end-of-year cash balance of the firm. All variables are scaled by the contemporaneous value of the firm’s total assets in order for the following equalities to hold:

(5)

(5)

(6)

(6)

The equality (5) implies that the system of equations (4) shows the way in which a representative company allocates an incremental unit of contemporaneous cash flows, thereby allowing to infer the sample-specific patterns of decision making. The results of testing of the system (4) on the cash-cash flow sensitivity subsamples are presented in .

Table 7. The patterns of cash flow allocation exhibited by cash-cash flow sensitivity subsamples.

The first distinguishable pattern contributing to the cash-cash flow sensitivity is the firm-level capacity to incur external financing. In particular, one notices that the negative CF-sensitive companies exhibit the lowest ability to procure external financing. If the contemporaneous cash flows drop by one monetary unit, the negative CF-sensitive company is able to procure 0.43 m.u. of external capital in the form of equity and debt; a representative CF-insensitive firm is able to procure 0.51 m.u. of external capital; while the positive CF-sensitive firms incur 0.55 m.u. of external funds. Therefore, an impaired capacity to tap the capital markets appears to be one of the major issues that the negative CF-sensitive companies struggle with by means of accumulating cash reserves. Similarly, the negative and positive CF-sensitive companies exhibit a significantly higher propensity to allocate the contemporaneous cash flows towards investment. Due to high investment demand, the negative CF-sensitive firms are forced to withhold any dividend distribution, while the positive CF-sensitive firms have to cut their cash accruals. The latter inference suggests that in addition to the precautionary motive, the cash accumulation patterns exhibited by Polish firm may be considerably impacted by their anticipated investment demand as was previously suggested by Almeida et al. (Citation2004), Sher (Citation2014), and Luo et al. (Citation2020).

7. The Discussion of Research Implications

Empirical results reported in the paper constitute a multi-faceted answer to the principal research question formulated in the introductory part. We demonstrate that binding financing constraints exercise a pronounced impact on firm-level cash management strategies by altering the patterns of intertemporal cash flow allocation and forcing companies to hold precautionary cash reserves to mitigate cash flow volatility. Importantly, we show that two decades of rapid evolution and modernisation of the Polish capital market and softening monetary policy have not eliminated the distortionary impact of capital market frictions on firms’ financial management strategies.

The present study confirms the existence of a nonmonotonicity of cash holdings with respect to cash flows. We document that cash holdings are not monotonically increasing in the degree of financing constraints as suggested by the empirical literature. In contrast, we distinguish between three subsamples exhibiting differing cash-cash flow sensitivity patterns: 1) positive CF sensitivity; 2) indeterminate CF sensitivity; 3) negative CF sensitivity.

The positive CF-sensitive firms, which are documented to hold the largest cash reserves, are found to be larger and older than their counterparts. Therefore, within the framework of most of the financing constraints measures, these firms would not be classified as financially constrained. What makes them different is the relatively higher volatility of cash flows, which preconditions the need to use liquidity cushion as a hedge against cash flow fluctuations. Cash flows accumulated by these firms assure the fund sufficiency for the future investment needs, as well as for servicing the financial liabilities. Despite manifesting the highest volatility of cash flows, the positive CF-sensitive companies are found to exhibit the highest capacity to procure external financing in an event of negative cash flow shocks. We argue that the access to external funds is largely the merit of their liquidity position, which assures the investors of the firms’ ability to meet their financial obligations. This pattern is consistent with the implications of the Holmström-Tirole (1997) model of intermediated lending.

The negative CF-sensitive companies are found to be in the most precarious position due to unsatisfactory operational performance, lack of collateral, young age and small size. These firms appear to accumulate cash holdings in order to cover their operating losses as well as to assure the investors of the shareholders’ commitment to the continuation of the firms’ operations. Therefore, these firms accumulate cash reserves from the contemporaneous equity issuances. The firms’ owners appear to bet on the future reversal of the current operational performance, a pattern known as ‘gamble for resurrection’.

Overall, we do not find any evidence, which would suggest that the sampled companies maintain excessive cash reserves. The more liquid firms exhibit a higher propensity to allocate the operating cash flows towards investment uses, which in view of their unpredictable cash flows, may justify the higher cash holdings. Overall, we agree that at least to a certain extent, the cash management strategy is investment-driven (Almeida et a., 2004; Luo et al., Citation2020).

This study is the first to draw attention to the nonmonotonicity of cash-cash flow relationship thereby recognising that firm-level cash management strategies are contingent upon exposure to binding financing constraints. By employing simultaneous-equation framework, we demonstrate that inadequate access to external financing may substantially alter the patterns of intertemporal cash flow allocation between investment and precautionary uses.

Importantly, we demonstrate that Polish companies continue exhibiting symptoms of financing constraints suggesting that improvements to the regulatory framework may be warranted to facilitate the allocation of external financing within the corporate sector. For lack of collateral and proven performance record, some firms are constrained to maintaining cash reserves to signal the quality of envisaged investment opportunities and shareholders’ commitment to support firms’ operations in the event of adverse cash flow shocks.

While we do not find any evidence suggesting that cash accumulation causes firms to underinvest, we recognise that precautionary cash savings inflict a deadweight loss on the corporate sector by forcing it to resign from alternative productive uses of funds. The availability of flexible credit lines could probably remedy the issue (Ivashina & Scharfstein, Citation2010). However, as suggested by the model of intermediated lending, the financial institutions are willing to lend only is the company either maintains adequate liquidity reserves or generates stable cash flows. Therefore, alternative financing vehicles or modes of financing for the companies confronted with financing constraints should be envisaged. Establishment of dedicated development funds earmarked for support of growth of financially constrained but dynamically growing ventures have been envisaged by regulatory bodies across CEE region to respond to the growing investment demand on the part of fundamentally sound firms having difficulties tapping bank financing.

Despite contributing to the relatively modest body of empirical literature inquiring into the impact of financing constraints on the intertemporal cash management patterns of firms on emerging markets, the study has a number of limitations. In particular, it is based on the data for public companies, which generally enjoy a better access to external financing than their closely-held counterparts thanks to a lower degree of information asymmetry and a longer verifiable performance record. Secondly, the study does not address the reasons behind cash management decisions of the subsample of firms exhibiting negative cash-cash flow relationship. While the patterns exhibited by these firms are reminiscent of ‘gamble for resurrection’, it remains unclear why the owners of these firms are willing to inject fresh equity despite a dissatisfactory historical performance record. Further studies may elucidate the drivers of such decisions. Thirdly, due to methodological challenges, our study does not disentangle and quantify transactional and precautionary motives behind cash accumulation. Modelling of firm-level function operationalising factor-specific demand for cash reserves within a separate study could remedy the issue. Finally, while the paper purports to investigate a generalisable pattern of cash-cash flow sensitivity and its interplay with firm-level degree of financing constraints, the sample is constrained to a single geography, therefore, wider cross-geographical corroboratory studies appear warranted.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 The creation of the dataset started with the list of all companies, which have been listed on the Warsaw Stock Exchange since 1994 (including those which ceased to exist at the time of the study due to bankruptcy, M&A transactions or which were delisted). The dataset initially compiled from Thomson Reuters Eikon database contained gaps in time series of financial data for some of the firms comprising the research sample. Those gaps had to be completed relying on firms’ financial reports provided by Notoria database. Eikon also lacks the full coverage of financial data for small-cap companies quoted on the NewConnect platform, which are also included in the research sample. The financial data for NewConnect-listed firms were assembled from Notoria. The data were taken as reported by the sample firms in order to insure data compatibility between databases. Data regarding the official dates of incorporation of sample firms were collected from the Polish National Company Registrar.

References

- Acharya, V., Almeida, H., & Campello, M. (2007). Cash Negative Debt? Journal of Financial Intermediation, 16(4), 515–554. https://doi.org/https://doi.org/10.1016/j.jfi.2007.04.001

- Almeida, H., Campello, M., & Weisbach, M. (2004). The Cash Flow Sensitivity of Cash. The Journal of Finance, 59(4), 1777–1804. https://doi.org/https://doi.org/10.1111/j.1540-6261.2004.00679.x

- Altman, E. (2000). Predicting Financial Distress of Companies: Revisiting the Z-Score and ZETA Models. New York University, 5(8), 1–54.

- Bates, T., Kahle, K., & Stulz, R. (2009). Why do U.S. firms hold so much more cash than they used to? The Journal of Finance, 64(5), 1985–2021. https://doi.org/https://doi.org/10.1111/j.1540-6261.2009.01492.x

- Bernanke, B., & Gertler, M. (1989). Agency Costs, Net Worth, and Business Fluctuations. American Economic Review, 79(1), 14–31.

- Bhagat, S., Moyen, N., & Suh, I. (2005). Investment and internal funds of distressed firms. Journal of Corporate Finance, 11(3), 449–472. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2004.09.002

- Campello, M., Graham, J., & Harvey, C. (2010). The real effects of financial constraints: evidence from a financial crisis. Journal of Financial Economics, 97(3), 470–487. https://doi.org/https://doi.org/10.1016/j.jfineco.2010.02.009

- Chen, P., Karabarbounis, L., & Neiman, B. (2017). The global rise of corporate saving. Journal of Monetary Economics, 89, 1–19. https://doi.org/https://doi.org/10.1016/j.jmoneco.2017.03.004

- Chen, H., Yang, D., Zhang, J., & Zhou, H. (2020). Internal controls, risk management, and cash holdings. Journal of Corporate Finance, 64, 101695. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2020.101695

- Cleary, S. (1999). The Relationship between firm investment and financial status. The Journal of Finance, 54(2), 673–692. https://doi.org/https://doi.org/10.1111/0022-1082.00121

- Cummins, J., Hassett, K., & Oliner, S. (2006). Investment behavior, observable expectations, and internal funds. American Economic Review, 96(3), 796–810. https://doi.org/https://doi.org/10.1257/aer.96.3.796

- Dasgupta, S., & Sengupta, K. (2007). Corporate liquidity, investment and financial constraints: implications from a multi-period model. Journal of Financial Intermediation, 16(2), 151–174. https://doi.org/https://doi.org/10.1016/j.jfi.2006.09.002

- Décamps, J., & Faure-Grimaud, A. (2000). Bankruptcy costs, ex post renegotiation and gambling for resurrection. Finance, 21, 71–84.

- Devereux, M., & Schiantarelli, F. (1990). Investment, financial factors, and cash flow: Evidence from UK panel data. In R. Hubbard (Ed.), Asymmetric Information, Corporate Finance and Investment (pp. 279–306). University of Chicago Press.

- Duchin, R., Ozbas, O., & Sensoy, B. (2010). Costly external finance, corporate investment, and the subprime mortgage credit crisis. Journal of Financial Economics, 97(3), 418–435. https://doi.org/https://doi.org/10.1016/j.jfineco.2009.12.008

- Faulkender, M., & Petersen, M. (2006). Does the Source of Capital Affect Capital Structure? Review of Financial Studies, 19(1), 45–79. https://doi.org/https://doi.org/10.1093/rfs/hhj003

- Fazzari, S., Hubbard, G., Petersen, B., Blinder, A., & Poterba, J. (1988). Financing constraints and corporate investment. Brookings Papers on Economic Activity, 1988(1), 141–206. ), https://doi.org/https://doi.org/10.2307/2534426

- Fazzari, S., & Petersen, B. (1993). Working capital and fixed investment: New evidence on financing constraints. The RAND Journal of Economics, 24(3), 328–342. https://doi.org/https://doi.org/10.2307/2555961

- Gatchev, V., Pulvino, T., & Tarhan, V. (2010). The interdependent and intertemporal nature of financial decisions: An application to cash flow sensitivities. The Journal of Finance, 65(2), 725–763. https://doi.org/https://doi.org/10.1111/j.1540-6261.2009.01549.x

- Hadlock, C., & Pierce, J. (2010). New evidence on measuring financial constraints: moving beyond the kz index. Review of Financial Studies, 23(5), 1909–1940. https://doi.org/https://doi.org/10.1093/rfs/hhq009

- Han, S., & Qiu, J. (2007). Corporate precautionary cash holdings. Journal of Corporate Finance, 13(1), 43–57. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2006.05.002

- Hasan, I., Jackowicz, K., Kowalewski, O., & Kozlowski, L. (2017). Do local banking market structures matter for SME financing and performance? New evidence from an emerging economy. Journal of Banking & Finance, 79, 142–158.

- Holmström, B., & Tirole, J. (1997). Financial intermediation, loanable funds, and the real sector. Quarterly Journal of Economics, 112(3), 663–691.

- Hovakimian, G. (2009). Determinants of investment cash flow sensitivity. Financial Management, 38(1), 161–183. https://doi.org/https://doi.org/10.1111/j.1755-053X.2009.01032.x

- Hugonnier, J., Malamud, S., & Morellec, E. (2015). Capital supply uncertainty, cash holdings, and investmen. Review of Financial Studies, 28(2), 391–445. https://doi.org/https://doi.org/10.1093/rfs/hhu081

- Ivashina, V., & Scharfstein, D. (2010). Bank lending during the financial crisis of 2008. Journal of Financial Economics, 97(3), 319–338. https://doi.org/https://doi.org/10.1016/j.jfineco.2009.12.001

- Jackowicz, K., Kozłowski, Ł., & Mielcarz, P. (2016). Financial constraints in Poland: the role of size and political connections. Argumenta Oeconomica, 1(36), 225–240. https://doi.org/https://doi.org/10.15611/aoe.2016.1.09

- Jackowicz, K., Kozłowski, Ł., Wnuczak, P. (2020). Location, location, … and its significance for small banks. Eastern European Economics, 58(1), 1–33. https://doi.org/https://doi.org/10.1080/00128775.2019.1651654

- Kaplan, S., & Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics, 112(1), 169–215. https://doi.org/https://doi.org/10.1162/003355397555163

- Keefe, M., & Yaghoubi, M. (2016). The influence of cash flow volatility on capital structure and the use of debt of different maturities. Journal of Corporate Finance, 38, 18–36. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2016.03.001

- Luo, P., Chen, B., & Liu, F. (2020). Growth option, debt maturity and cash reserves with bank-tax-interaction. The North American Journal of Economics and Finance, 52, 101144. (C). https://doi.org/https://doi.org/10.1016/j.najef.2020.101144

- Martin, S., & Santomero, A. (1997). Investment opportunities and corporate demand for lines of credit. Journal of Banking & Finance, 21(10), 1331–1350. https://doi.org/https://doi.org/10.1016/S0378-4266(97)00030-7

- Michalski, G., Rutkowska-Podołowska, M., & Sulich, A. (2017). Remodeling of FLIEM: the cash management in Polish small and medium firms with full operating cycle in various business environments. Efficiency in Business and Economics, 119–132. https://doi.org/https://doi.org/10.1007/978-3-319-68285-3_10

- Moshirian, F., Nanda, V., Vadilyev, A., & Bohui, Z. (2017). What drives investment–cash flow sensitivity around the World? An asset tangibility Perspective. Journal of Banking & Finance, 77, 1–17.

- Mueller, D. (1972). A life cycle theory of the firm. The Journal of Industrial Economics, 20(3), 199–219. https://doi.org/https://doi.org/10.2307/2098055

- Myers, S., & Majluf, S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221. https://doi.org/https://doi.org/10.1016/0304-405X(84)90023-0

- Opler, L., Pinkowitz, T., Stulz, R., & Williamson, R. (1999). The determinants and implications of corporate cash holdings. Journal of Financial Economics, 52(1), 3–46. https://doi.org/https://doi.org/10.1016/S0304-405X(99)00003-3

- Phan, H. V., Nguyen, N. H., Nguyen, H. T., & Hegde, S. (2019). Policy uncertainty and firm cash holdings. Journal of Business Research, 95, 71–82. https://doi.org/https://doi.org/10.1016/j.jbusres.2018.10.001

- Polak, P., Masquelier, F., & Michalski, G. (2018). Towards treasury 4.0/The evolving role of corporate treasury management for 2020. Management: Journal of Contemporary Management Issues, 23(2), 189–197.

- Sher, G. (2014). Cashing in for growth: corporate cash holdings as an opportunity for investment in Japan. IMF Working Papers, 14(221), 1. 9781498322. https://doi.org/https://doi.org/10.5089/9781498322171.001

- Stiglitz, J., & Weiss, A. (1981). Credit rationing in markets with imperfect information. American Economic Review, 71, 393–410.