?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Against the institutional background of building an innovative country, this article constructs the influence mechanism of the accounting standards for intangible assets for enterprise technology innovation. We select panel data from the Shanghai Stock Exchange and Shenzhen Stock Exchange from 2002 to 2015. We focus on the two dimensions of innovation input and innovation output and use Poisson regression, negative binomial regression, zero expansion regression, and other methods to examine the effects of the revision of the intangible assets accounting standards on enterprise technology innovation. Our research reveals the following: (1) In general, the revision of the intangible assets accounting standards can promote enterprises’ technological innovation activities; (2) This effect is heterogeneous by ownership: before the revision of accounting standards for intangible assets, state-owned enterprises had more innovation input than non-state-owned enterprises, but the innovation output of non-state-owned enterprises has become greater than that of state-owned enterprises even though the policy only significantly improved the innovation output of the latter; and (3) The system lacks a continuous effect. The revision of the intangible assets accounting standards has only a one-year lag effect on the incentive effect of enterprise innovation input activities, mainly because enterprise innovation input has only a one- to two-year lag effect on output. The implementation of this system has not changed the status quo that Chinese patent rights are based on applied short-term technology research and development. Based on the findings, this article proposes some pertinent policy suggestions.

1. Introduction

The report of the 19th National Congress of the Communist Party of China stated that innovation is the primary driving force for development and for the strategic support necessary to build a modern economic system. To accelerate the pace of building an innovative country, we must implement the new development concepts of innovation, coordination, greenness, openness, and sharing. Chinese President Xi Jinping clearly stated that a focus on innovation will provide a solution to the problem of force for development. Enterprises are the main force for innovation. Under this innovation-driven development strategy, enterprises’ level of technological innovation has become a key measure of their development potential and competitive edge (Porter, Citation1992). Data from The Ministry of Science and Technology show that Chinese R&D input has increased year by year, and its intensity has also increased steadily. In 2013, R&D input broke 2% for the first time, reaching 2.08%. However, the Thomson Reuters list of the “Top 100 Global Innovative Enterprises” (as shown in ) included few Chinese companies during 2011–2015. This shows that the quality of innovation and development by Chinese enterprises is not high and must be improved. Therefore, determining how to increase innovation potential, improve the quality of innovation, and enhance the international competitiveness of Chinese enterprises has become a top priority.

Table 1. List of global innovation firms on Thomson Reuters.

Enterprises are the mainstay of innovation, and their innovative decision-making behaviour affects the overall level of technological innovation in China. Innovation activities are a key strategy for enterprises to cultivate core competitiveness (Stuart, Citation2000), but it is a long-term and multi-stage process that is risky, unpredictable, labour-intensive, and idiosyncratic (Holmstrom, Citation1989). Thus, innovation output is highly uncertain, and innovation also has many externalities. Entrepreneurs’ intention and motivation for innovation input are insufficient. The policy is therefore an important strategy for the state to promote social economic innovation and development, as well as enterprises’ technological innovation and development. The Ministry of Science and Technology, the Ministry of Finance, and other government departments have successively promulgated a series of systems aimed at stimulating enterprises’ technological innovation activities. In terms of accounting standards, the results of technological innovation activities are mainly reflected in intangible assets. In 2006, the “Accounting Standards for Business Enterprises – No. 6 Intangible Assets” issued by the Ministry of Finance of China fundamentally changed the accounting method for R&D spending. The accounting system for intangible assets is an intermediary of national macroeconomic policies and enterprises’ micro-innovation activities. The state thus seeks to increase attention to and support for enterprises’ technological innovation activities. Then, does the institution of intangible assets accounting standards have an incentive effect on enterprises’ technological innovation? What is the incentive effect on enterprise heterogeneity, and what is the duration of this effect? What is the incentive effect of the intangible assets accounting standards revision on enterprise technology innovation? The answers to these questions are theoretically and practically significant for optimising intangible assets accounting standards and adjusting the direction and strength of the state’s policy support for enterprise technology innovation.

The innovations of this article are as follows. First, the driving effects of the revision of intangible asset accounting standards on enterprise technology innovation are examined. Second, this article finds that the panel data volume is large and the time is long, so the results are more persuasive. Third, this article analyses the heterogeneity of enterprises and the persistence of the driving effect of intangible assets accounting standards.

The remainder of this article proceeds as follows. The second section reviews the literature and proposes our hypotheses. The third section introduces the research design and sample selection. The fourth section presents the results of the research and analysis. The final section gives our conclusions and recommendations.

2. Literature review and research hypotheses

2.1. Literature review

With the advent of the knowledge economy era, technological innovation activities have become a key factor for enterprises to maintain their competitive edge (Kalafut & Low, Citation2001). Since Schumpeter (Citation1911) proposed the concept of innovation, scholars’ research on the factors driving enterprises’ technological innovation has focused on both internal and external factors. Among internal factors, the current research focuses on enterprise attributes, including corporate heterogeneity (Choi et al., Citation2011), corporate governance (Balsmeier et al., Citation2017; Galasso & Schankerman, Citation2015; Holmstrom, Citation1989), positioning of corporate shareholders (Flammer & Kacperczyk, Citation2016), intra-firm trade (Levine et al., Citation2016), and the human capital of corporate executives (Chemmanur et al., Citation2016), and discusses their impact on enterprise technology innovation. Among external factors, the current research focuses on financial development (Dong et al., Citation2017), the capital market (Fang et al., Citation2014), policies and regulations (Brown et al., Citation2017; Fang et al., Citation2017; Howell, Citation2017; Laux & Stocken, Citation2018; Lerner, Citation2009), financing constraints (Brown et al., Citation2012), the product market (Chemmanur et al., Citation2016), and bank competition (Cornaggia et al., Citation2015) and discusses their impact on enterprise technology innovation.

R&D activities are the enterprises’ source of technological innovation. The content and form of R&D are becoming increasingly complicated, and the accounting treatment of enterprises’ R&D expenditures cannot truly reflect the essence of their R&D activities. Therefore, in 1999, the International Accounting Standards Board adopted a phased approach to deal with R&D expenditure. The research shows that the policy environment is the key factor for determining enterprises’ innovation efficiency. Good innovation policy can effectively improve enterprises’ enthusiasm for innovation input and the conversion rate of innovation output (Brown et al., Citation2013). The 2006 version of the intangible assets accounting standards thus aroused heated scholarly discussion. The research mainly focuses on the impact of the revision of the standards on enterprise value, enterprise performance, and enterprise stock price. From an institutional perspective, the literature on the impact of national macro-policies on enterprises’ technological innovation mainly focuses on preferential tax policies (Brown et al., Citation2017), government subsidy policy (Howell, Citation2017), and intellectual property protection systems (Fang et al., Citation2017; Lerner, Citation2009). The value relevance of capitalised R&D appears to decrease from pre- to post-I.F.R.S. period(Shah et al., Citation2013; Tsoligkas & Tsalavoutas, Citation2011). The capitalised development costs (an asset) is highly significant about stock prices and enhances the relevance of the voluntary disclosures (Chen et al., Citation2017). High‐quality accounting information system can improve research and development activities, firms with high‐quality financial reporting transform investment inputs into greater innovation outcomes (Park, Citation2018).

The revised standards have had a positive impact on the innovation investment activities of enterprises. (Lev & Zarowin, Citation1999); however, they have severely weakened investment in R&D (Nix & Peters, Citation1988). As the literature shows, it is of great theoretical and practical significance to explore the effects on micro-enterprise technological innovation from the perspective of the macro-accounting system. However, as the largest economy in the world, China has its unique institutional background. First of all, the formulation and modification of the accounting standards for intangible assets are implemented by the Ministry of Finance, and mandatory information disclosure by listed companies is required. Secondly, compared with non-state-owned enterprises, state-owned enterprises are managed by the State-owned Assets Supervision and Administration Commission of the State Council (S.A.S.A.C.), and it is easier to obtain support from policies and funds. Now there are relevant research literature, mostly from the perspective of law or fiscal and taxation policies to discuss the impact on enterprise technological innovation, even if it is discussed from the perspective of the accounting system, it is more from the perspectives of financing structure (Khan et al., Citation2018) and the quality of financial reports (Park, Citation2018). The literature that explores the driving force of technological innovation from the perspective of accounting standards, especially the revision of intangible asset standards, which is most relevant to innovation.

2.2. Research hypotheses

China has used two versions of intangible assets accounting standards. The revised intangible assets accounting standards introduced in 2006 focus on the accounting treatment of R&D expenditures to reflect enterprises’ R&D activities and the transformation of innovation outcomes more realistically. The process provides a reference for the next investment decisions of management and external investors.

From the perspective of technological innovation input, before the revision, the cost-based approach led to increases in the current costs of enterprises and a sharp decline in profits. Management was reluctant to invest in R&D projects, instead of pursuing short-term profit targets. After the revision, the phased accounting method eliminated these drawbacks and reduced the risk of R&D investment. Therefore, enterprises’ enthusiasm for R&D investment has increased, and innovation investments have increased year by year.

From the perspective of technological innovation output, the standards do not directly stipulate the relevant behaviour of innovation output, but studies have shown that the revision has led to increased investment in technological innovation, mainly in the enhancement of human capital or the increase of technological reserves. The research team and core technology are the key factors affecting enterprises’ output of technological innovation. Therefore, improving them will increase the success rate of enterprises’ innovation output. Based on the above, this article proposes the following hypothesis:

Hypothesis 1 (H1): The revision of the intangible asset accounting standards motivates corporate technology innovation activities (input and output).

Institutional theory emphasises the impact of differences institutions on corporate behaviour, and external institutions often act through micro-factors within the enterprise. China has its unique institutional background, and companies differ like property rights. Therefore, the impact of the macrosystem on different types of enterprises may be different. The type of ownership is one of the most important attributes of an enterprise, and it determines the enterprise’s ultimate makers. State-owned enterprises are China’s national economic lifeline and have shouldered the burden of maintaining stable economic operations, so they can obtain more government financial support. This convenient financing environment will increase enterprises’ willingness to invest in R&D. Therefore, compared with non-state-owned enterprises, state-owned enterprises are under the management of S.A.S.A.C., it is easier to obtain support from policies and funds. In terms of R&D investment, they are more willing to be consistent with the policy of innovative enterprises (encouraging investment). However, the governance structure and incentive mechanism of state-owned enterprises have great defects, and the operating system of state-owned enterprises leads to a lack of motivation to achieve innovation success, which leads to low innovation output efficiency (Clarke et al., Citation2003). In contrast, non-state-owned enterprises aim to maximise the benefits of their R & D investment more actively, it has a strong motivation to improve the efficiency of transforming R & D investment inputs into greater innovation outcomes. Therefore, the innovation output of non-state-owned enterprises is greater than that of state-owned enterprises (Choi et al., Citation2011). Accounting policy has important influences on business decision-making. Because the intangible asset accounting standards are an inclusive policy system, their revision will not affect the difference in innovation input caused by the difference in ownership. However, the effects of the standards on innovation output vary. As the backbone of the Chinese industry, state-owned enterprises are an important part of innovation activities, but they are more subject to government intervention. Therefore, the revision has stimulated the innovation output efficiency of state-owned enterprises to a certain extent. This article proposes the following hypothesis:

Hypothesis 2 (H2): Before the revision of the guidelines, state-owned enterprises invested more in innovation than non-state-owned enterprises, but non-state-owned enterprises had more innovation output than state-owned enterprises. The revision stimulated the innovation output of state-owned enterprises but did not affect the difference in innovation investment.

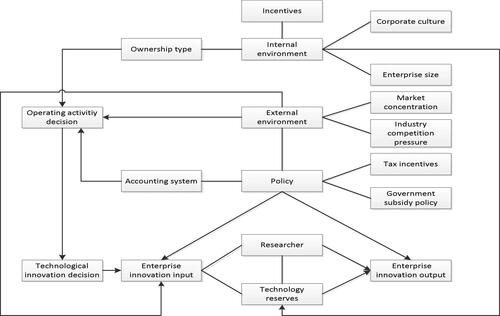

We use institutional theory and technological innovation theory to analyse the impact of the revision of the intangible assets accounting standards on enterprise technology innovation, as shown in .

Figure 1. The influence mechanism of the accounting standards of intangible assets for enterprises’ technological innovation.

Source: The authors.

3. Research design and sample selection

3.1. Sample selection

This article selects A-share main board listed companies from Shanghai Stock Exchange and Shenzhen Stock Exchange from 2002 to 2015 as its sample. The data are taken mainly from the CSMAR database, which is missing R&D expenditure data before 2007. Therefore, the R&D expenditure data for 2002 to 2006 were obtained by inspecting the financial statement annotations of listed companies and manually sorting them. Since the implementation of the new standards in 2007, “development expenditure” has been included to account for enterprises’ R&D expenditures. Therefore, the R&D expenditure data for 2007 to 2015 were obtained through the development of expenditure reports.

To ensure the integrity of the data, the sample was processed as follows: (1) Companies with ST and *ST in their names were excluded; (2) Central state-owned enterprises and local state-owned enterprises were combined into a state-owned enterprise group; private enterprises, foreign-funded enterprises, and other types of enterprises were merged into a non-state-owned enterprise group; and enterprises that could not be classified were deleted; and (3) According to Chinese high-tech enterprise qualification certification standards, companies with high-tech certification and companies that possess the high-tech project, technology centers and high-tech products were classified as high-tech enterprises, whereas companies without the qualification certification were classified as non-high-tech enterprises. As a result, 6,788 samples were obtained. Because the R&D expenditure and the number of patent applications in the sample have many zero values, to ensure the accuracy and robustness of the research results, the samples were divided into three categories: TYPE = −1 (with R&D expenditure, without patent output), TYPE = 0 (without R&D expenditure, with patent output), and TYPE = 1 (with R&D expenditure, with patent output).

3.2. Variable definition

Based on the literature, this article measures the level of technological innovation in terms of the two dimensions of innovation input and innovation output to ensure the comprehensiveness and robustness of the results. Innovation investment is measured using the natural logarithm of R&D expenditure (Matolcsy & Wyatt, Citation2008), expressed as LNRD. Innovation output is measured using the number of patent applications (Atanassov, Citation2013), expressed as PATENT.

A dummy variable is used to indicate the revision of the intangible assets accounting standards. The sample period is divided into two sub-samples: the first is from 2002 to 2006, during which enterprises followed the old accounting standards for intangible assets, and the second is 2007–2015, during which enterprises followed the new version of the intangible assets accounting standards. YEAR06 indicates the year of revision of the intangible assets accounting standards, YEAR06 = 0 indicates the period before the revision, and YEAR06 = 1 indicates after the revision. The definition and description of variables in this paper are shown in .

Ownership (S.O.E.). The nature of corporate ownership greatly affects enterprises’ technological innovation activities (Choi et al., Citation2011), including the number of patents, and this effect is more significant for private enterprises. This article uses the dummy variable S.O.E. to indicate the nature of corporate ownership: S.O.E.=0 indicates non-state-owned enterprises, and S.O.E.=1 indicates state-owned enterprises.

Enterprise characteristics (Q.U.A.). There are huge differences in the technological innovation activities of labour-intensive, capital-intensive, and technology-intensive enterprises. This article sets the dummy variable Q.U.A. to indicate high-tech enterprises: Q.U.A.=0 indicates non-high-tech enterprises, and Q.U.A.=1 indicates high-tech enterprises.

Enterprise size (SIZE). We use the natural logarithm of total assets at the end of the period to measure enterprise size, following the literature.

Profitability (R.O.E.). This article uses the return on net assets as a measure of corporate profitability, expressed as R.O.E.

Cash holdings (CASH). This article uses the ratio of net cash flow from operating cash to net profit to measure the level of cash flow of enterprises, expressed as CASH.

Capital structure (L.E.V.). This article uses the asset-liability ratio as a measure, expressed in L.E.V.

Growth ability (GROWTH). We use the growth rate of operating income to measure the growth ability of an enterprise, expressed as GROWTH.

Table 2. Variable definitions and descriptions.

3.3. Model setting

To test H1 and H2, based on theoretical analysis, the following regression models are constructed from two dimensions, innovation input and innovation output:

(model1)

(model1)

(model2)

(model2)

3.4. Descriptive statistics

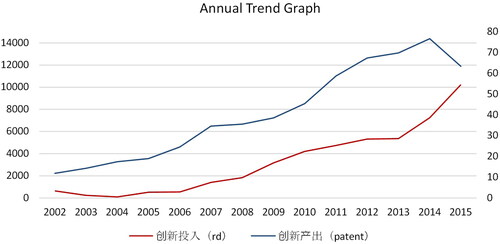

As shows, between 2002 and 2015, the technological innovation of Chinese listed companies shows growth trends both in annual average input quantity and annual average output quantity (although the average annual number of patents in 2015 was slightly less than in 2014), and the revision of the intangible assets accounting standards has a significant driving effect on the technological innovation input and output of enterprises.

Figure 2. Annual trends of innovation input and innovation output.

Source: The authors’ own estimations.

The following conclusions can be drawn from .

Table 3. Descriptive statistics of the sample enterprise variables before and after the revision of the standards.

(1) Enterprise innovation output. Before the revision of the standards, the maximum number of patent applications filed by listed companies is 2,724, the average value is only 18.16, and the standard deviation is 92.70, indicating that the number of patent applications by Chinese listed companies varies greatly. The minimum value is 0 and the median is only 3, indicating that the number of patent applications for most listed companies is very low. After the revision, the maximum number of patent applications for sample listed companies increases to 6,327, and the average also rises to 56.22, indicating that the innovation output of listed companies improved after the revision. The standard deviation rises to 294.69, which indicates that the patent output gap between listed companies has further widened. The minimum value is still 0, and the median increases slightly to 8. These descriptive statistics are consistent with the reality of Chinese innovation output.

(2) Enterprise innovation input. From the perspective of innovation input, the maximum value of R&D input is 10.65 before the implementation of the new standards, and the average value is only 2.14. There is still a large variation in R&D inputs across the sample listed companies: the minimum and median are 0. It can be seen that most listed companies in China still do not attach enough importance to R&D. After the implementation of the new standards, the maximum value of R&D input rose to 13.81, and the average increased from 2.14 to 3.07, indicating that the problem of insufficient R&D input by listed companies improved since the implementation of the new standards. However, the minimum and median are still 0, which indicates that China must still force listed companies to actively carry out technological innovation activities.

To further analyse the impact of the revision of accounting standards on enterprise technology innovation, we conduct univariate analyses of the enterprises’ technological innovation activities, as well as t-tests. The average values of and significant differences between the variables are shown in .

Table 4. Univariate analysis before and after the 2006 revision of the standards.

From the results in , before the 2006 revision, the average number of patent applications and average R&D input are 18.16 and 2.14, respectively, whereas, after the revision, they are 56.22 and 3.07, respectively. The mean increases are 38.06 and 0.93, indicating that the revision has driven enterprises’ technological innovation activities.

In terms of ownership, before the revision, the average values of innovation output and innovation input of the treatment group are 15.47 and 2.22, respectively, and the average values of innovation output and innovation input of the control group are 36.92 and 1.64, respectively. The mean differences are −21.45 and 0.58, respectively, indicating that the innovation output of non-state-owned enterprises was more than that of state-owned enterprises, while the innovation input was the opposite. After the revision, the average values of innovation output and innovation input of the treatment group are 57.94 and 3.25, respectively, and the average values of innovation output and innovation input of the control group are 52.53 and 2.70, respectively. The mean differences are 5.41 and 0.55, respectively, indicating that state-owned enterprises have greater innovation output and innovation input than non-state-owned enterprises.

According to the characteristics of the enterprises, before the revision, the average values of the innovation output and innovation input of the treatment group are 36.92 and 1.64, respectively, and the average values of the innovation output and innovation input of the control group are 17.70 and 2.15, respectively. The mean differences are 19.22 and −0.51, indicating that the innovation output of high-tech enterprises was greater than that of non-high-tech enterprises, while the input of innovation was the opposite. After the revision of the standards, the average values of innovation output and innovation input of the treatment group are 59.50 and 3.30, respectively, and the average values of innovation output and innovation input are 54.69 and 2.97, respectively. The mean differences are 4.81 and 0.33, respectively, indicating that the innovation output and input of high-tech enterprises were greater than that of non-high-tech enterprises.

4. Research results and analysis

4.1. Revision of Intangible Assets Standards and Enterprise Technology Innovation

For the dimension of innovation input, we use model 1 to verify hypothesis 1 (H1), and the regression results are shown in . In the general regression model, the full-sample regression model (1) shows that the regression coefficients of the intangible assets revision (YEAR06) and the enterprise innovation input (LNRD) are positive and significant at the 1% level, indicating that after the revision of intangible assets accounting standards in 2006, enterprise technology innovation input activities were significantly stimulated. Sub-sample regression models (2)–(4) show that the impact of the revision on innovation input is significant at the 1% level, and the coefficient is positive; thus, from the innovation input dimensions, H1 is supported. In the panel data regression models (5)–(8), the coefficients of the intangible asset accounting standards revision and the enterprise innovation input are both positive and significant at the 5% level or above, which is a good confirmation of the robustness of H1 from the input dimension.

Table 5. Effect of revision of intangible assets standards on enterprise innovation input.

From the dimension of innovation output, we use model 2 to verify H1, and the regression results are shown in .

Table 6. Effect of revision of intangible assets standards on enterprise innovation output.

Because there are many zero values in the sample, to ensure the accuracy and stability of the empirical results, the full sample and the subsample (TYPE = 1) models are used for the regression, respectively. In the subsample (TYPE = 1) regression model, the Poisson regression (1) shows that the coefficients of enterprise innovation input (LNRD) and innovation output (PATENT) are positive and significant at the 1% level, indicating that enterprise innovation input has a positive effect on innovation output. The impact of the revision of the intangible assets standards (YEAR06) on the enterprise innovation output (PATENT) is significant at the 1% level, and the regression coefficient is positive, indicating that the revision had a positive effect on enterprise innovation output. The negative binomial regression (2) shows that the coefficient of the innovation input, revision of the intangible asset’s standards, and innovation output is positive, and all are significant at the 1% level, indicating that the revision significantly stimulated the technological innovation output of enterprises and that the greater the R&D input of enterprises, the greater the patent output. Thus, from the dimension of innovation output, H1 is supported. In the full-sample regression model, because there are more zero-value expansion phenomena in the whole sample, this article also uses the Z.I.P. model and the Z.I.N.B. model to make the test results more reliable and persuasive. In regression models (3) and (4), the innovation input, the revision of the intangible asset’s standards, and the enterprise innovation output are positively correlated, significant at the 10% level and above, which confirms the robustness of H1 from the output dimension.

In summary, even from different dimensions (innovation input and innovation output) and with different types of samples (subsamples and full samples) and regression methods (general regression, panel data regression, Poisson regression, etc.) for the empirical analysis, the driving effect of the revision of intangible asset accounting standards on enterprises technology innovation activities remains significant and robust.

4.2. Revision of Intangible Assets Standards, Enterprise Heterogeneity, and Enterprise Technology Innovation

In China, there are significant differences between state-owned enterprises and non-state-owned enterprises in terms of innovation resource acquisition, transformation, and human resources. Besides, there are significant differences between high-tech and non-high-tech enterprises in terms of fulfillment of their R&D input obligations and their tax benefits. Also considering China’s unique institutional background and enterprise characteristics, this article further explores the impact of the revision of the intangible asset’s standards and enterprise heterogeneity (whether enterprises are state-owned or high-tech) on enterprise technology innovation.

and below show the regressions of the revision of the intangible asset’s standards and ownership type on the technological innovation activities of enterprises. In , when the model (1) does not include the ownership (S.O.E.) variables, the impact of the dummy variable of standards revision on innovation input is significantly positive at the 1% level. After adding ownership type in the model (2), the regression coefficient of the intangible asset’s standards revision is still significantly positive, while the coefficient of ownership type is positive but not significant. After the implementation of the new standards, the R&D input of both state-owned enterprises and non-state-owned enterprises improved, but the difference is not statistically significant. However, the cross-term of the revision of the standards and ownership type (YEAR06*S.O.E.) is positively correlated and is significant at the 10% level, which indicates that the revision of the intangible asset’s standards had an incremental effect on the technological innovation input of state-owned enterprises. Therefore, the revision of the standards has produced a difference in the technological innovation input of enterprises in terms of ownership type.

Table 7. Regression results of the revision of intangible assets standards, ownership type, and technological innovation input of enterprises.

Table 8. Regression results of the revision of the intangible assets standards, ownership type, and technological innovation output of enterprises.

The regression results for the intangible assets standards, ownership type, and enterprise technology innovation output are shown in . In the full-sample regression model (1), the regression coefficient of innovation input is negative, which is different from the previous findings, perhaps because there are too many zero values in the sample. Ownership type and innovation output are significantly negatively correlated at the 1% level, indicating that non-state-owned enterprises have more innovation output than state-owned enterprises both before and after the implementation of the standards. However, after the intangible asset’s standards revision, the regression coefficient of the interaction between the standards dummy variable and ownership type is significantly positive at the 5% level, which indicates that after the revision, the situation reversed: the innovation output of state-owned enterprises became less than that of non-state-owned enterprises. Therefore, overall, the revision of the standards has an incremental effect on the innovation output of state-owned enterprises, and hypothesis 2 (H2) is supported in terms of the output dimension. In the TYPE = 1 regression model (2), the coefficient of ownership is negative, while the cross-term regression coefficient of ownership and the standards revision is positive; both are significant at the 5% level, which is the same as the conclusion of the model (1). This further indicates the robustness of H2 from the output dimension. Besides, the regression coefficient of the control variable is roughly the same as that in model (1).

The regression results for the intangible assets standards, enterprise qualifications, and enterprise technology innovation activities are shown in and .

Table 9. Regression results of the revision of intangible assets standards, enterprise qualifications, and enterprise technology innovation inputs.

Table 10. Regression results of the revision of the intangible assets standards, enterprise qualifications, and enterprise technology innovation output.

In above, when the model (1) does not include the enterprise qualification (Q.U.A.) variable, the impact of the standards revision dummy variable on the innovation input is significantly positive at the 1% level. In models (2) and (3), after adding the enterprise qualification variable, the regression coefficient of the intangible asset’s standards revision is still significantly positive, while the coefficient of enterprise qualification is negative but not significant. The interaction term between the standards revision variable and the enterprise qualification variable (YEAR06*Q.U.A.) has a positive correlation that is significant at the 10% level, indicating that the revision of the intangible assets standards has an incremental effect on the innovation input of high-tech enterprises. Thus, the revision of the standards has produced differences in enterprise traits in terms of the input of enterprise technology innovation.

The revision of the intangible assets standards and the regression results of the high-tech enterprise qualifications on technological innovation output are shown in below. When a model (1) does not include the enterprise qualification (Q.U.A.) variable, the impact of the standards revision dummy variable on innovation output is significantly positive at the 1% level, indicating that the revision of the standards can increase enterprises’ R&D input and thus increase innovation output. In models (2) and (3), after adding the variables of enterprise qualification, the regression coefficient of the intangible asset’s standards revision is still significantly positive, while the regression coefficient of enterprise qualification is significantly negative. However, the t-test indicates that the regression coefficients are significantly different, the sum of their regression coefficients is greater than zero, and the interaction term between the revised criterion variable and the enterprise qualification variable (YEAR06*Q.U.A.) shows a significant positive correlation, indicating that although the innovation output of high-tech enterprises is not as great as that of non-high-tech enterprises, the revision of the intangible assets standards has had additional incremental output effects on high-tech enterprises.

From the analysis of the results in and , the revision of the intangible assets accounting standards has produced significant differences in enterprise traits.

4.3. Further Analysis

The intangible asset accounting standards promulgated in 2006 substantially reformed the accounting treatment of R&D expenditures. The treatment of these expenses in different stages has directly affected motivations for R&D input activities. The sample is from 2002 to 2015, during which China successively introduced policies such as the Enterprise Income Tax Law and the R&D Cost Additional Deduction Policy, which may affect the reliability of the above regression results. To further test the sustainable driving effect of the revision on enterprises’ innovation input, the full sample is symmetrically divided into five small samples according to the introduction of various policies. The regression results are shown in below.

Table 11. Effect of the accounting standards revision and enterprise technology innovation input (corresponding interval test).

To make the regression coefficients of each group in comparable, the core variables of the panel data are de-centered, and the individual effects are removed. We then conduct a seemingly unrelated regression (S.U.R.) estimation and t-test between groups. The results show significant differences in the regression coefficients of the revision dummy variables of each group. The coefficients are 0.172, 0.218, 0.380, 0.476, and 0.482, and the increments are 0.046, 0.162, 0.096, and 0.006. The results show that the annual average driving effect of enterprises’ technological innovation input is strongest after three years after the implementation of the standards for the 2002 to 2011 period. These results also show that the driving effect of the revision of the standards on enterprises’ technological innovation varies annually in persistence and in driving strength.

4.4. Robustness analysis

This article also pairs the samples before and after the implementation of the new intangible assets accounting standards to conduct a robustness test. Both one-to-many and one-to-one matching models are used to make the conclusions more robust. First, the balance test and univariate test are performed to measure the appropriateness of the matching tool variables, and inappropriate tool variables are eliminated in different sets of regressions. The propensity score matching analysis results are shown in .

Table 12. PSM analysis results.

In above, the differences between groups after propensity score matching are significantly positive for both one-to-many matching and one-to-one matching. The results show that the revision of the intangible assets standards has a significant driving effect on enterprise technology innovation activities.

To eliminate the endogeneity between the revision of intangible assets accounting standards and enterprise technology innovation, the lagged variables of enterprise technology innovation input and output are selected and models 1 and 2 are used to conduct the regressions. The results are shown in and .

Table 13. Endogeneity Analysis of the Revision of Standards and Enterprise Innovation Input.

Table 14. Results of the Endogeneity Analysis of the Revision of the Standards and the Innovation Output of Enterprises.

Chinese patent law stipulates that patent rights include invention patents, utility model patents, and design patents. Because of the short construction time of intellectual property rights in China, most of the technological innovation contained in patent rights – usually utility models and designs – is not valuable, and the development time of such patents is short, generally one to two years. This article selects the innovation output – the first- and second-order lag models of the number of patent applications – for the regression. Because the sample data contain a large number of zero values, we also use the zero-expansion Poisson model and the zero-expansion negative binomial model to further analyse the relationship between innovation input and innovation output with model 2. The regression results are shown in .

The regression results in and confirm that the improvement of technological innovation in enterprises is to some extent caused by the revision of the intangible assets accounting standards.

5. Research conclusions and recommendations

5.1. Research conclusions

After exploring the incentive effects of the 2006 revision of the intangible assets accounting standards, this article finds the following: (1) In general, the revision of the standards has had a significant positive incentive effect on enterprise technology innovation activities; (2) Further analysis shows that before the revision of the standards, state-owned enterprises had more innovation input than non-state-owned enterprises, whereas non-state-owned enterprises had more innovation output than state-owned enterprises. The revision of the standards stimulated the innovation output of state-owned enterprises but did not affect innovation input. The formulation of accounting standards is political and has produced significant differences in the R&D behaviour of state-owned enterprises and non-state-owned enterprises; and (3) The 2006 version of the intangible assets accounting standards had a one-year lag effect on the innovation input activities of enterprises, and there is no continuity. Innovation input activities had a positive impact on the innovation output of enterprises, but the impact had only a one- or two-year lag period. After the revision of accounting standards, the driving effect changes from weak to strong and then gradually weaker. The revision did not change the status of Chinese patent rights based on applied technology research and development.

5.2. Policy recommendations

This article proposes the following targeted policy recommendations based on the theoretical analysis and empirical regression results.

First, overall, the revision of the accounting standards for intangible assets has a driving effect on the technological innovation activities of enterprises, but the effect is strongest within three years after the implementation of the standards for the 2002 to 2011 period, and the sustained effect driven by the system is insufficient. An important reason is that the internal R&D patent right of the enterprise adopts the cost measurement model, and the intangible assets purchased externally are relatively small part compared with the whole value of intangible assets of enterprises, which is easily underestimated or ignored by investors. Another reason is that, in the 2018 Letter No. 21 of the Ministry of Finance, although the classified financial information of the intellectual property (generalised intangible assets) of enterprises was disclosed, the intellectual property input of the enterprises did not correspond to their intellectual property output. This disclosure does not reflect the efficiency of enterprises’ intellectual property creation, enterprises’ risk control level, and internal control quality, or enterprises’ enthusiasm for innovation. Therefore, relevant government departments should select more appropriate measurement methods to reflect the intrinsic value of the independent research and development of intangible assets to support, protect, and respect the core intellectual property rights of enterprises.

Second, after the revision of the intangible asset's standard, although the overall innovation output of state-owned enterprises has been significantly improved, the current innovation output is mainly based on applied patents, the R&D investment, and output of enterprises facing future technology reserves are not enough. Therefore, the direction of scientific and technological research and development should be changed, and enterprises should be encouraged to continue research and development of key core intellectual property rights.

There are some research limitations of this article: (1) Considering China's special institutional background, the article is a supplement and expansion of the existing literature, and its research conclusions may not have general applicability; (2) As China’s accounting standards stipulated that R&D expenses should be included in administrative expenses before 2007, and China’s R&D expenses and patent databases are not yet complete, the data on R&D expenses and patent rights from 2002 to 2006 were collected manually, which lacked authority; and (3) Unlike the U.S. and the U.K., the formulation and modification of China's accounting standards are implemented by the Ministry of Finance, which has the characteristics of mandatory information disclosure for listed companies. Therefore, it is not suitable to adopt D.I.D. research methods.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Atanassov, J. (2013). Do hostile takeovers stifle innovation? Evidence from antitakeover legislation and corporate patenting. Journal of Finance, 6, 1097–1131.

- Balsmeier, B., Fleming, L., & Manso, G. (2017). Independent boards and innovation. Journal of Financial Economics, 123(3), 536–557. https://doi.org/https://doi.org/10.1016/j.jfineco.2016.12.005

- Brown, J. R., Martinsson, G., & Petersen, B. C. (2013). Law, stock markets, and innovation. The Journal of Finance, 68(4), 1517–1549. https://doi.org/https://doi.org/10.1111/jofi.12040

- Brown, J., Martinsson, G., & Petersen, B. (2012). Do financing constraints matter for R&D? European Economic Review, 56(8), 1512–1529. https://doi.org/https://doi.org/10.1016/j.euroecorev.2012.07.007

- Brown, J., Martinsson, G., & Petersen, B. (2017). What promotes R&D? Comparative evidence from around the world. Research Policy, 46(2), 447–462. https://doi.org/https://doi.org/10.1016/j.respol.2016.11.010

- Chemmanur, T., He, J., He, S., & Nandy, D. (2016). Product market characteristics and the choice between IPOs and acquisitions. Journal of Financial and Quantitative Analysis, 53(2), 681–721.

- Chen, E., Gavious, I., & Lev, B. (2017). The positive externalities of IFRS R&D capitalization: enhanced voluntary disclosure. Review of Accounting Studies, 22(2), 677–714. https://doi.org/https://doi.org/10.1007/s11142-017-9399-x

- Choi, S. B., Lee, S. H., & Williams, C. (2011). Ownership and firm innovation in a transition economy: Evidence from China. Research Policy, 40(3), 441–452. https://doi.org/https://doi.org/10.1016/j.respol.2011.01.004

- Clarke, G. R. G., Xu, L. C., & Zou, H. F. (2003). Finance and income inequality: Test of alternative theories. Policy Research Working Paper, 2003(72), 578–596.

- Cornaggia, J., Mao, Y., Tian, X., & Wolfe, B. (2015). Does banking competition affect innovation? Journal of Financial Economics, 115(1), 189–209. https://doi.org/https://doi.org/10.1016/j.jfineco.2014.09.001

- Dong, M., Hirshleifer, D., Teoh, S. H. (2017). Stock market overvaluation, moon shots, and corporate innovation. Working paper, University of California, Irvine.

- Fang, L. H., Lerner, J., & Wu, C. (2017). Intellectual property rights protection, ownership, and innovation: Evidence from China. The Review of Financial Studies, 30(7), 2446–2477. https://doi.org/https://doi.org/10.1093/rfs/hhx023

- Fang, V. W., Tian, X., & Tice, S. (2014). Does stock liquidity enhance or impede firm innovation? The Journal of Finance, 69(5), 2085–2125. https://doi.org/https://doi.org/10.1111/jofi.12187

- Flammer, C., & Kacperczyk, A. (2016). The impact of stakeholder orientation on innovation: Evidence from a natural experiment. Management Science, 62(7), 1982–2001. https://doi.org/https://doi.org/10.1287/mnsc.2015.2229

- Galasso, A., & Schankerman, M. (2015). Patents and cumulative innovation: Causal evidence from the courts. The Quarterly Journal of Economics, 130(1), 317–369. https://doi.org/https://doi.org/10.1093/qje/qju029

- Holmstrom, B. (1989). Agency costs and innovation. Journal of Economic Behavior & Organization, 12(3), 305–327. https://doi.org/https://doi.org/10.1016/0167-2681(89)90025-5

- Howell, S. T. (2017). Financing innovation: evidence from R&D grants. American Economic Review, 107(4), 1136–1164. https://doi.org/https://doi.org/10.1257/aer.20150808

- Kalafut, P. C., & Low, J. (2001). The value creation Index: Quantifying intangble performance value. Strategy & Leadership, 29(5), 9–15. https://doi.org/https://doi.org/10.1108/10878570110696632

- Khan, M. K., He, Y., Akram, U., Zulfiqar, S., & Usman, M. (2018). Firms’ technology innovation activity: Does financial structure matter? Asia‐Pacific Journal of Financial Studies, 47(2), 329–353.

- Laux, V., & Stocken, P. C. (2018). Accounting standards, regulatory enforcement, and innovation. Journal of Accounting and Economics, 65(2–3), 221–236. https://doi.org/https://doi.org/10.1016/j.jacceco.2017.11.001

- Lerner, J. (2009). The empirical impact of intellectual property rights on innovation: Puzzles and clues. American Economic Review, 99(2), 343–348. https://doi.org/https://doi.org/10.1257/aer.99.2.343

- Lev, B., & Zarowin, P. (1999). The boundaries of financial reporting and how to extend them. Journal of Accounting Research, 37(2), 353–385. https://doi.org/https://doi.org/10.2307/2491413

- Levine, R., Lin, C., Wei, L. (2016). Insider trading and innovation. NBER Working paper No. 21634.

- Matolcsy, Z. P., & Wyatt, A. (2008). The association between technological conditions and the market value of equity. The Accounting Review, 83(2), 479–518. https://www.jstor.org/stable/30245365

- Nix, P. E., & Peters, R. M. (1988). Accounting for R&D expenditures. Research-Technology Management, 31(1), 39–41. https://doi.org/https://doi.org/10.1080/08956308.1988.11670500

- Park, K. E. (2018). Financial reporting quality and corporate innovation. Social Ence Electronic Publishing, 45(7–8), 871–894.

- Porter, M. (1992). Capital disadvantage: America’s failing capital investment system. Harvard Business Review, 70(5), 65–82.

- Schumpeter, J. A. (1911). The theory of economic development. Harvard Economic Studies.

- Shah, S. Z. A., Liang, S., & Akbar, S. (2013). International financial reporting standards and the value relevance of R&D expenditures: Pre and post IFRS analysis. International Review of Financial Analysis, 30, 158–169. https://doi.org/https://doi.org/10.1016/j.irfa.2013.08.001

- Stuart, T. E. (2000). Interorganizational alliances and the performance of firms: A study of growth and innovation rates in a high‐technology industry. Strategic Management Journal, 21(8), 791–811. https://doi.org/https://doi.org/10.1002/1097-0266(200008)21:8<791::AID-SMJ121>3.0.CO;2-K

- Tsoligkas, F., & Tsalavoutas, I. (2011). Value relevance of R&D in the UK after IFRS mandatory implementation. Applied Financial Economics, 21(13), 957–967. https://doi.org/https://doi.org/10.1080/09603107.2011.556588