?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Rationality is one of the main assumptions in economics, and is represented as the rational expectation in macroeconomics. As such, it is important to note that the effectiveness of economic policy depends on the degree of economic agents’ rationality. According to this point of view, it is only natural to ask how the central bank views economic agents to be either rational or bounded rational. In implementing economic policies, it is possible to assume that the central bank views economic agents to be bounded rational. This is due to the fact that most theoretical arguments state that policy under rationality is not as effective as one under bounded rationality. Based on this argument, this paper employs bounded rational New Keynesian Model proposed by Gabaix to know if rationality matters to the central bank. As a result, as long as the central bank does not follow the full gradualism, it is possible to conclude that the rationality matters to the central bank. However, it is not anymore if the central bank employs full gradualism in monetary policy rule.

1. Introduction

One of the main assumptions in economics is a rationality in decision-making. There are many reasons why it is assumed in an economic analysis; one of them lies on its tractability in generating analytic solutions for theoretical economic problem.

In macroeconomics, according to Robert E. Lucas Jr., the rationality of economic behaviour (or representative agent) in general equilibrium model is expressed in rational expectations. Under such expectations, he casted doubt on the effectiveness of the governments’ economic policy, known as Lucas critique (Lucas, Citation1976), in a sense that the response of the public is not invariant to the change in its economic policy. This is due to the idea of rational expectations that they change their expectation when the government changes its policies.

Subsequently, Barro and Gordon (Citation1983) shows that discretionary policy cannot be effective and a government can generate inflation bias due to time inconsistent policy if the public are rational enough to understand the incentive of the government. Moreover, Ricardian Equivalence, a well-known theorem in public economics, states that rational agents internalise their tax burden when making a decision for consumption.

In contrast, Simon (Citation1955) coined the term ‘bounded rationality’ to replace the global rationality of an economic agent with the rational behaviour compatible with the cognitive ability. Since then, Kahneman and Tversky (Citation1979) shows that Von Neumann-Morgentstern utility theorem, constructed under axioms of rationality, could be violated under risky situation. In turn, Kahneman and Tversky (Citation1979) proposed ‘Prospect Theory’ to complement the rationality assumption in economics.

Based on the arguments mentioned above, it is possible to make a theoretical conclusion that the effectiveness of the policy depends on the rationality of economic agents, and that it is a critical element for a government to consider in devising its policy. In this vein, the Bank of England surveys 6,000 households to know how the public perceive the effect of monetary policy between 2008 and 2014. (Anderson et al., Citation2016) This survey results suggest that the public under-appreciate the indirect way in which they are affected by the changes in monetary policy over this time. This reveals that there is a communication challenge for the central bank when they implement new monetary policy because the public can not know how monetary policy affects them, possibly due to the rationality of the public.

At the same time, Woodford and Xie (Citation2019) theoretically argue that the rational expectation is an idealisation and show that under finite forward expectation, Ricardian Equivalence is violated and aggregated demand can be stimulated by the government transfers. Moreover, based on the simulation result that in absence of fiscal policy changes, inflation targeting causes the price level to fall below the target path when zero lower bound is binding so that temporary price level is more effective to achieve the target path, they show that different finite forward-expectation of economic agents can generate different predicted dynamics of price level and conclude that the finite expectation is shorter, the rule based temporary price level targeting is more efficient. This suggests that the monetary policy should be different and the policy follows the rule if the agent is bounded rational expectation.

In line with these, some papers argue the effectiveness of forward guidance. According to Andrade et al. (Citation2019), the Survey of Professional Forecasters reveals that there is heterogeneous belief on forward guidance between 2011:Q3 and 2012:Q4. From the survey, they find ‘When “Date-based” forward guidance started, professional forecasters’ disagreement on future short-term interest rates one-year and two-year ahead declined sharply and reached a historical low’ (p. 7) Based on this finding, they model two different types of agents in the market, Odyssean and Delphic,Footnote1 and show that the effectiveness of forward guidance depends on the fraction of these agents. This implies that the forward guidance could not be effective as long as Fed follows State-based forward guidance.Footnote2 Therefore, the difference in perception among professional forecasters implies a violation of the rational expectation and supports finite rational expectation or bounded rational expectation.

Recently, Del Negro et al. (Citation2012) show that standard DSGE ((Dynamic Stochastic General Equilibrium) with extreme forward-looking (or rational expectation), predicts unrealistic overreaction of macroeconomic variables to changes in future interest rate even though it is far from present. In other word, the effect of changes in future interest rate has the same effect on current output as the effect of changes in current interest rate. This phenomenon is the so-called ‘forward guidance puzzle’. To handle the puzzle, a recent literature revised the rational expectation assumption. For example, Farhi and Werning (Citation2019) replace the rational expectation with level-k bounded rationality with market frictions and offer the rationalisation of forward guidance puzzle. In addition, Angeletos and Lian (Citation2018) shows that allowing agents to be uncertain about the belief and the response of others can reduces the power of forward guidance by about 90 percent at the five-year horizon. These findings reveal that the effectiveness of monetary policy is relied on the rationality of the public so that the bounded rationality is a considerable component when the central bank implements the policy.

However, even though the rationality of the agents is one of most important factors to determine the effect of economic policy as mentioned in literature, it is unknown if the central bank considers how much the public is rational. This is because most literature are theoretical approach or survey-based approach and these in monetary economics employ simple framework suggested by Taylor (Citation1993) which is successful to explain the monetary policy within Paul Vocker and Alan Greenspan era. Even with this success, however, because one instrument variable, short-term interest rate, describes all decision-making in processes in a central bank, it is not easy to consider how the central bank recognises the public in terms of rationality.Footnote3 In other words, because the actual decision-making process is melted down into Federal funds rate and Federal funds rate is only observable variable, only way to diagnose this issue is explaining the movement of Federal funds rate using the different level of rationality of the public.

To shed light on this topic, the bounded rational New Keynesian Model through cognitive discounting or myopic in Gabaix (Citation2020) is employed to determine the corresponding relationship between the level of bounded rationality and the actual movement of effective Federal funds rate. By changing the parameter for cognitive discounting or myopic, it is possible to reveal what the specific level of the rationality is assumed for the central bank to make a decision, when the model with this level of the rationality is closer to the actual movement of Federal funds rate. To reveal the perception of the central bank to the rationality of the public behind the decision-making, this paper employs Greenbook data, one of Fed internal data. This is because real-time data such as Greenbook data is actually used when the central bank makes a decision. Subsequently, this paper finds out that as long as semi-gradualism is employed or persistent shock is assumed, it is possible to conclude that the rationality matters to the central bank. However, it is not anymore if the central bank follows the full gradualism in monetary policy rule.

In the rest of the paper, section 2 introduces the bounded rational New Keynesian Model proposed by Gabaix (Citation2020) to show how bounded rationality is modelled into small-scale New Keynesian Model. Section 3 discusses issues regarding the estimation and results. Particularly, this section discusses the reason why it is impossible to measure the expectation of the market and shows the result with modified Taylor rule. Section 4 presents different type of the rule matters to how the central bank perceive the public in terms of rationality and section 5 reviews the relation between gradualism and rationality. Finally, section 6 summarises some findings in the paper.

2. Bounded rational New Keynesian Model

In economics, there are several different types of bounded rationality. This is because the bounded rationality is a number of limitation an economic agent faces. Such limitation include; i) lack of information: Sticky Information (Mankiw & Reis, Citation2002), and Without Common Knowledge (Angeletos & Lian, Citation2018), ii) limits of human capability: Rational Inattention (Sims, Citation2003), and iii) different form of the expectations: Myopic (Gabaix, Citation2020), Sunspot (Cass & Shell, Citation1983), level-k thinking (Farhi & Werning, Citation2019), and Sticky expectation (Carroll et al., Citation2020)

A typical definition of the bounded rationality is the concept that individuals make rational decisions under the constraint of available information and mental capabilities. A salient property of such rationality is that the result of decision-making by an agent would be inadequate or sub-optimal. In this regard, a myopic behaviour on the part of the agent would equate to that of the bounded rationality as it is analogues to that of making a decision based on limited information with inadequate mental capabilities. In such case, even if an agent were to be exposed to a rich information environment with unlimited amount of data, he or she would not be able to consider or incorporate all the prevalent information, and the outcome would not be as optimal as that of the fully rational agent.

In this context, Gabaix (Citation2020) has proposed bounded rational New Keynesian Model. Accordingly, if an agent is myopic, he or she would value the future less in making a decision. Psychologically, he or she would pay less attention to the future value whereas cognitively, he or she would discount future value less. Thus, the more myopic an agent, the less he or she would discounts the future. At extreme, he or she would not cognitively discount future value since its value is completely ignored.

Based on this idea, Gabaix (Citation2020) has proposed the following in regards to a small-scale New Keynesian ModelFootnote4:

(1)

(1)

(2)

(2)

in which πt and xt are inflation and output gap, respectively. Moreover, it is a short-term interest rate determined by the central bank, known as Federal Funds rate. As for νt and

are cost-push and preference shocks, respectively, and both of them follow AR(1) process. One important distinction from a traditional small-scale model is that each equation contains myopic parameters such as

and κ. Some parameters in the equations are defined as follows:

in which β and θ are a subjective discounting factor and a fraction of non-price-resetting firms, respectively, and γ is a intertemporal risk parameter. Additionally, r is steady-state real interest rates, thus

Myopic parameters are

and my. The slope of the cognitive discounting is represented as

in which agents perceive less clearly on distant matters, whereas mf represents the level of the cognitive discounting by firms. The level of the cognitive discounting of interest rate and output by individuals are represented as mr and my, respectively. An important property of myopic parameters is the more myopic, the less value of the parameters are:

As mentioned in Gabaix (Citation2020), there is a problem of not being able to calibrate or estimate all the myopic parameters simultaneously in this model. However, this issue is greatly mitigated by the fact that it allows the value of to act as an anchor in which the rest of the parameters (mr, my, and mf) to become dependent on. Thus, ‘These value could be set to 1 (rational value)’ (Gabaix, Citation2020).

Lastly, the model is completed by a modified Taylor rule as follows:

(3)

(3)

in which

represent monetary policy shock and follows AR(1) process, and ρR is the parameter of gradualism or interest rates smoothing. This rule is a type of modified Taylor rule widely used in monetary economics literature, and is known as semi-gradualism due to allowing gradualism as well as AR(1). Since there is no definitive verdict on the gradualism or interest rates smoothing in empirical literature, so most of the literature opts for this rule, combining the rule in Clarida et al. (Citation2000) with the one in Rudebusch (Citation2002). There are many variation of the Taylor rule, but most of them are based on above modification.As known, IS curve (also known as Euler equation) and Phillips Curve represent the result from the optimisation of the household and firms, respectively. Moreover, the central bank, the Federal Reserve, has to follow its ‘Dual Mandate’, which is, by Federal Reserve act mandated by the Congress, Federal Reserve are promoting (1) Maximum Employment (2) Stable Price, and (3) Moderate Long-Term Interest Rate.Footnote5 This implies that the central bank is subject to these economic conditions so that IS curve and Philips curve are constraints to the central bank. This is because IS curve determines equilibrium interest rate while Philips curve decides the price level and unemployment. Thus, a monetary policy, such as Taylor rule, depends not on just economic situation, also the level of optimisation of economic agents through both IS and Philips curves. In short, a monetary policy is subject to IS and Phillips curves in which the rationality of the agents determine the level of optimisation.

3. Estimation

3.1. Calibration and priors

In order to set the value of parameters, the following standard calibrated value is used. (See Panel A in ): The value of the subjective discounting factor implies that annual real interest rate is 2% or 0.5% per quarter. The reciprocal of the real wage elasticity of labour supply, known as Frisch elasticity, is calculated by keeping marginal utility of wealth constant. Despite this value being not as volatile as the volatility in labour market, it is consistent with micro evidence. The most common approach to calculate the inter-temporal risk aversion is consumption-based capital asset pricing model. On the basis of the model, the commonly accepted value lies within 1 and 3, and thus, the moderate value is chosen. According to Rotemberg and Woodford (Citation1997), the firm adjusts its price once a year on average. This implies that the duration of price of firms is 3 quarters. Hence, the fraction of non price resetting firms is 0.75.

Table 1. Values of calibration and priors.

In line with this, the value of shock parameters in the model is based on that of the estimation by Ireland (Citation2004). Since his small-scale model is very similar to the one in this paper, and as such, his estimated parameters are employed for a calibration of the model. (See Panel B in .)

According to An and Schorfheide (Citation2007), ‘the priors for the coefficients in the monetary policy rule are loosely centred around values typically associated with the Taylor rule’ (p. 127). This implies that there is no standard prior for the coefficients in the monetary policy. In this paper, thus, priors of the coefficients of a modified Taylor rule are based on those of Smets and Wouters (Citation2007) (see Panel C in ).

3.2. Data

In regard to the estimation of Taylor rule, Orphanides (Citation2001) argued that Taylor rule ignored the difference between an initial data and subsequent data revision and that the estimated rules cannot provide actual economic situation if the revised data are used. Moreover, as mentioned above, real-time data is more appropriate to reveal the perception of the central bank to the public.

To consider these arguments, the Greenbook data is used to estimate a modified Taylor rule under bounded rationality. The Greenbook data is a one that is produced before each meeting of the Federal Open Market Committee to forecast the future economic situation. (This dataset is available to the public only after a lag of five yearsFootnote6). From the Greenbook data predicted by the Fed, the current quarter forecasting of Core Consumer Price Index and Output Gap from 1987Q3 to 2007Q4 are used. Since, however, a forecasting of Output Gap is done twice within one quarter, an average value is employed. Note that all units in Greenbook data are annualised percentage points. Moreover, Effective Funds rate is aggregated by the average value of a quarter from FRED.Footnote7

3.3. Issue in estimations

One of key issues in the estimation is how the public sector with myopic behaviour expects the future. As mentioned previously, this is due to the fact that all state equations in the estimation are derived from the optimisation of the private sector. As a general rule, all market participants including the public receive commercial forecasts from such source as Blue Chip Survey, Data Resources Inc. or Survey of Professional Forecaster. As these sources are the only available data of forecast to the public, they become the only source in formulating their expectation. Other sources of data such as Federal Reserve internal data including Beigebook, Bluebook, and Greenbook only become available to the public only after a delay of few years. As such, the issue of data availability is key one in determining how the public expects the future.Footnote8 In terms of the model, in other words, because (or

), forecast data which the public uses may already include how they perceive the future.Footnote9 However, it is unknown which forecast data is one the public uses and how the public takes forecast data as an input into the expectation-formation process. This implies that an estimation of the expectation of the public could be impossible. As mentioned in Coibion et al. (Citation2018), in spite of the fact that there are private forecast data, each data has own limitation to estimate the formation of expectations. For example, market measure of expectations can offer high-frequency data, but have the limitation on relatively short history. In contrast, professional forecast can provide long-time series, but it cannot show true belief of the forecasters. Consumer Expectation data such as Michigan Survey of Consumers has the limitation on its sensitivity to survey language. (Consistent with the result of Haldane and McMahon (Citation2018))

According to Romer and Romer (Citation2000), Fed internal data such as inflation forecast and GNP forecast is superior to commercial forecasts. This implies that the rationality of the public in terms of accuracy is inferior to that of the Fed’s since its internal data is only available to the Fed at the time the public makes its decision on the future. Even if the public had access to the Fed’s data, it would be unreasonable to assume that the pubic is fully rational.Footnote10 According to Haldane and McMahon (Citation2018) measured the Flesch-Kincaid reading grade score of Central Bank communication accessibility and concluded that given literacy level of United Kingdom population, more than 90% of the general public could not comprehend the message of the central bank. Moreover, Blinder (Citation2018) predicts that ‘Central Banks will keep trying to communicate with the general public, as they should. But for the most, they will fail’ (p. 569)

Since the Fed uses the internal data which is superior to commercial forecasts and is unavailable to the public and they do not know how much the public are rational when they set up the expectation, it would be possible to assume that the Fed will decide the rationality of the public when they make a decision. Especially, this could be true when the Fed do ‘open-mouth operation’, forward guidance. The main purpose of forward guidance is to communicate the intention of the Fed and to have the public expects the future according to its guidance. In this vein, Gürkaynak et al. (Citation2005) shows that using two factors, target factor and path factor, FOMC statements can affect private expectation through future policy actions. Therefore, the Fed need to know how much the public believes and should make a decision how much they can understand its policy intention to implement forward guidance. This is also true when the Fed implements the interest rate targeting to achieve its policy goals.

Due to the fact that the value of myopic parameter () is still unknown at this time, this paper can only check if the rationality would matters to the central bank, rather than estimating the myopic parameter.

3.4. Results

As shown in panel A in , the rules with the different level of rationality satisfy the wisdom of Taylor rule in a reasonable range of the parameter values. However, all parameters are different except the response to output gap. Even with different level, the response to output gap ranges in between 0.19 and 0.21. Thus, it seems that rationality does not matter in the response to output gap.

Table 2 Results of the rule with both lagged term and AR(1) (Rule 1).

In contrast to this, the response to inflation is higher as the level of rationality is higher, and vice versa. So, the central bank responses strongly to inflation if an agent were to be fully rational, whereas their responses would not be as strong if an agent were to be not fully rational. One possible explanation for this relative strength of response by the central bank is due to inflation bias. As emphasis in Barro and Gordon (Citation1983), the welfare cost of inflation bias is higher under rational expectation. Thus, a strong response to inflation can be expected under fully rational agent to prevent them from having the bias. At the same time, gradualism or interest rate smoothing parameter has an inverse relationship with the level of rationality, whereas the parameter of persistent has a proportional relationship.

Despite a change in Federal Funds rate being gradual, there is no definite verdict on the reason for its gradual movement. Most widely accepted theoretical reason lies in the idea of financial stability. For the central bank to keep financial market stable, the public has to believe in its credibility and understand its policy guideline. Under a low level of rationality, it is safe to assume that the public has trouble understanding the policy guideline of the central bank. Therefore, the most reasonable action in this scenario for the central bank is to change its policy rate gradually as much as possible to have the public follow its future policy. In this light, it is apparent that gradualism or interest rate smoothing parameter could be increased as the level of rationality is decreased, while the persistent parameter could be decreased as the level of rationality decreased. This is because the persistent shock is such a larg amount of forecastable variaination that it requires the higher level of the rationality.

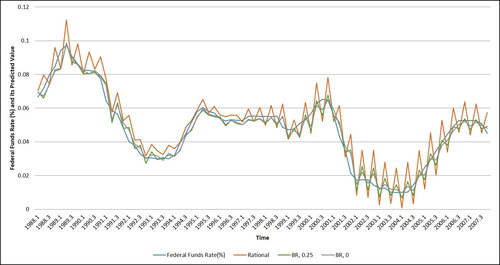

In order to determine the level of rationality the central bank assumes, the fitness of the estimated policy rule under the different level of rationality is shown in . One surprising result in the figure is that the rule under lower level of rationality or bounded rationality is fitted to the data quite well. Especially, dotted line (bounded rationality) or lower level of rationality (BR = 0.25) is outperformed to explain the movement of Federal funds rate. At the same time, Root Mean-Square Error (RMSE) in panel B in shows that lower level of rationality such as or

is better than other levels of rationality including full rationality.

Figure 1. The fitness to actual movement of Federal funds rates with Rule 1. Source: Author’s calculation.

In order to confirm this RMSE difference, the p-values of the hypothesis that the difference of RMSE is different to zero is calculated based on the regression. In the estimation, the dependent variable is the difference of residuals between the rule under full rationality and bounded rationality, Thus, the estimation equation is

Since the hypothesis is to check that the difference is zero, the estimation of constant is just the difference between RMSEs. So, the null hypothesis is c = 0.

In panel C in , the results show that the difference is statistically significant. Despite the difference in two RMSE between (full rationality () vs. bounded rationality (

or

)) is negligible, at least, it is not reasonable to exclude the possibility of bounded rationality or lower level of rationality assumed in monetary policy rule of the central bank. This is because the rule under bounded rationality is statistically significant outperformed.

4. Other issues

In monetary economics literature, different types of modified Taylor rule are employed in empirical estimation or DSGE model, such as (Rule 2), similar to the rule in Clarida et al. (Citation2000), or

(Rule 3) as in Rudebusch (Citation2002).

So, it is natural to wonder if rationality still matter to the central bank with the different types of modified Taylor rule. This is because the movement of Federal funds rate under lower level of rationality could be explained with the different rule if rationality is still matter to the central bank. Technically, moreover, the previous estimations show some osciliations around Federal Funds rate. This implies that the rule allowing both gradualism and AR(1) process would be relatively inferior to explain the movement. Due to these reasons, a rule similar to the rule in Clarida et al. (Citation2000) is estimated.Footnote11

The coefficient in panel A in shows that all parameters are in a reasonable range as in previous estimation. Only difference is that the response to inflation is lower, while the response to output gap is higher. In addition, the magnitude of the response to inflation is higher under a level of fully-rationality, as before. Also, the gradualism or interest smoothing parameter shows same property as there is an inverse relationship with a level of rationality. Therefore, there is no large difference between two estimations, except the magnitudes of parameters.

Table 3. Results of the rule only with lagged term (Rule 2).

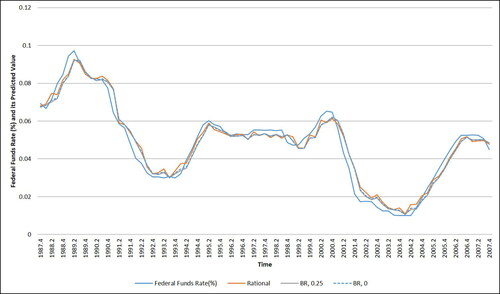

In contrast to these results, the fitness of the rule in is visually more pleasing than the fitness in . All rules with the different level of rationality can explain the movement of Federal Funds rate without oscillations. Especially, it is not easy to find out the visual difference among them. As before, however, RMSE panel B in still shows that lower level of rationality or bounded rationality is still outperformed.

Figure 2. The fitness to actual movement of Federal funds rates with Rule 2. Source: Author’s calculation.

In comparison to previous results, one striking results is that the difference is not statistically significant (see panel C in). Possibly, this is because both models have very lower RMSE so that the difference is negligible. One of possible reasons why the difference is not statistically significant is the different type of the gradualism. (Previous result is based on semi-gradualism, whereas, this result is based on full gradualism.) To the extend that the main motivation of the gradualism is for the central bank to guide the public to a intended future path or avoid a drastic change in policy rate, as mentioned above, it is safe to say that under the gradualism the central bank implicitly assumes that the public is bounded rational. Contradictorily, however, one possible explanation is that if the central bank employs the full gradualism solely, the rationality seems to be unimportant factor. This is because no matter who, either rational or bounded rational agent, under the full gradualism, either does not have any issue to understand the future policy. This is because the full gradualism provides the public relatively more time than any other rules for them to understand or follow the central bank’s guideline. In other words, the gradualism is based on the assumption of the bounded rationality on the one hand, but on the other hand the gradualism is also based on another assumption that no one has an issue to understand or follow the gradualism. Therefore, ironically, although the main motivation behind the gradualism is bounded rationality, under the full gradualism, it does not matter in its implementation. Combined with previous results, this suggests that the rationality can be matter at some level of the gradualism, but it does not at full gradualism. This also implies that as long as the central bank follows the gradualism or interest rate smoothing, but not full gradualism, the rationality could be matter to the central bank so that the central bank assumes the lower level of the rationality. This notion also suggests that there is a possibility that the level of rationality matters to the central bank only when it implements a particular type of interest rate rule.

To check this issue, Rule 3 which has no gradualim but persistent error, AR(1), is also estimated (see panel A in ) and RMSE of the Rule 3 is also checked. As before, the coefficient shows that all parameters are in reasonable range. Moreover, it still shows the property that the response to inflation is higher as the level of rationality is higher and vice versa. However, the rationality is not working in the response to output gap no matter what level of the rationality. Panel B in shows that, as before, the difference in RMSE of the Rule 3 is negligible. However, it shows that the rule with rationality is better to explain the movement of Federal Funds rate, and p-value for the difference in panel C in also shows that null hypothesis that there is no difference is rejected so that the rule under fully rational is outperformed. This implies that rationality, particularly, full rationality, matters to the central bank once the central bank drops the gradualism or interest rate smoothing. Therefore, this results can confirm an argument that rationality matters to the central bank when it implements a particular interest rate rule such as semi-gradualism or a persistent shock.

Table 4. Results of the rule only with persistent shocks (Rule 3).

5. Rationality and gradualism

In general, one of the more controversial issues in monetary economics is on the issue of an inertial movement of Federal funds rates. To explain the inertial movement econometrically, some of monetary economists employ the idea of the gradualism or interest rate smoothing (Clarida et al., Citation2000), while others deny such idea and conclude that the inertial movement is a mere illusion (Rudebusch, Citation2002).

In contrast to empirical approach, some theoretical studies in the literature conclude that the inertial movement of Federal Funds rates is the result of minimising the financial volatility (Cuikerman, Citation1991), maintaining an expected constancy (Goodfriend, Citation1991), or keeping political responsibility (Goodhart, Citation1997). Since a frequent change in Federal Funds rates can cause an unexpected movement in its future rates or increase a volatility in financial markets, Feds need to have a expected constancy to minimise a loss of control. Thus, the theoretical foundation of gradualism relies on how the central bank controls the public response through a policy instrument. If the central bank cannot communicate its policy intention effectively, then public would misunderstand it, which would cause a turbulence in financial market. In this point of view, the gradualism or interest rate smoothing are the rationale for this, and the rationality of the public can be a key factor to explain the gradualism. If the public is fully rational to understand the Fed’s policy intention without any misunderstanding, then there would not be any reason for the central bank to rely on the notion of the gradualism. In such a case, the only notion that the bank need to maintain is its credibility as the public would trust and act accordingly to the policies the Fed implements to achieve its two-mandates.

In above empirical estimations,the rule with both lagged term and AR(1) (Rule 1) represents a semi-gradualism, the rule only with lagged term (Rule 2) a full gradualism, and the rule only with AR(1) (Rule 3) a no gradualism. As empirical results summarised in , Rule 1 prefers bounded rationality to full rationality. Since the notion of the gradualism stands for steady change in funds rates, which results in a longer time to achieve policy goal, the public can have a progressive experience on how the Fed intends to achieve its policy goal. Intuitively speaking, the whole concept of the gradualism mashes well with bounded rational agents due to the fact that a learning curve is positively associated with either experience or time, or both. In case of Rule 2, however, the hypothesis that there is no different in RMSE between rational and bounded rational is not rejected. In other words, even though the lower level of rationality is still outperformed, there is no difference in performance so that the rationality does not matter to the central bank under the full gradualism. Ironically, as mentioned above, as long as the full gradualism, neither rational or bounded rational agent has an issue to understand the policy due to relatively more time to have progressive experience. This is partially contradict to the motivation of gradualism, but it is reasonable in its implementation. Therefore, this implies that under a notion of the gradualism (semi-gradualism), the rationality issue is relevant to the central bank.

Table 5. Summary of the results.

In contrast, Rule 3 prefers a full rationality to bounded rationality and the rule with fully rational model is statistically outperformed. Because Rule 3 implies that inertia evidence reflects persistent shocks, and, thus, it could be a large amount of forecastable variation, the public need to understand its policy intention as soon as possible in order to minimise the distortion due to the policy change. Therefore, the central bank should assume the rationality so that the rationality still matters to the central bank.

In summary, as long as the central bank does not follow the full gradualism, the rationality of the public, either bounded rational or fully rational, matters to the central bank and the types of the monetary policy rules also matters. However, as Ben Bernanke mentioned in 2004 Speech on May 20th, ‘The debate about the source of gradualism is on going and I cannot hope to render a definitive verdict today on the relative merits of these rationales’ (May 20, 2004 Speech), it is unknown that the central bank follows the gradualism and/or how much they follow. This is because all decision-making is melting down into the short-term interest rate, Federal Funds rate, so that it is not observable. At least, it is unacceptable to excluded the possibility that the central bank assumes the lower level of the rationality.

6. Conclusion

In this paper, monetary policy rule with a different level of rationality is estimated and compared. Because the central bank is subject to inflation and output gap, it is also subject to an agent’s rationality. This is because both inflation and output gap are outcome of the agent’s optimal decision-making through IS and Phillips curves. Therefore, the rationality of an agent could factor in the central bank’s decision-making.

Estimation results in this paper show that the hypothesis that rationality matters to central bank could not be excluded because a level of rationality depends on the monetary policy rule. Under a notion of the gradualism, the level of rationality is relevant to the central bank, but as long as the central bank implements the rule with the full gradualism, it stays irrelevant. Therefore, since the rule the central bank implements is key factor to determine how the central bank perceives the public, the rule matters to the central bank in terms of rationality. However, because all decision-making is melting down into the short-term interest rate, it is unknown that the central bank follows the gradualism so that it is uneasy to see how the central bank perceives the public in terms of rationality. This is reason why the gradualism is still controversial and many economists try to explain the movement of Federal Funds rate employing the gradualism or persistent shocks. At least, it is unacceptable to exclude the possibility that the central bank perceives the public as bounded rational. This is because under the lower level of the rationality, the rule with the gradualism explains the movement of the rate very well.

This paper raises the possibility that the central bank perceives the public as bounded rational. Unfortunately, however, because the model employed in this paper is based on small-scale New Keynesian Model, the emprical results are not decisive. For a future, thus, there is a need to extend the model to have it more thoroughly test the rationality assumption in monetary policy.

Disclosure statement

No potential conflict of interest was reported by the author.

Notes

1 Odyssean and Delphic are employed to distinguish the different type of forward guidance. Campbell et al. (2012) defined Odyssean forward guidance as one that the policymakers keep past promise even if an economic situation tempts policymakers to do what seems best at the moment, whereas Delphic forward guidance is defined as a forecast-based statement that Fed can forecast but is not required to commit themselves on the forecast.

2 State-based forward guidance is one that the commitment will be occur if the threshold of economic conditions satisfies criteria preset by the central bank, whereas Date-based forward guidance is simply based on a specific date.

3 Due to this reason, Blinder (1998) states that ‘My experience as a member of the FOMC left me with a strong feeling that the theoretical fiction that monetary policy is made by a single individual maximizing a well-defined preference function misses something important. In my view, monetary theorists should start paying some attention to the nature of decision-making by committee, which is rarely mentioned in the academic literature’ (p. 22). Because, however, the committee decision-making is similar to a game-theoretic situation, it is not easy to model the committee-decision making. In this vein, Cha (2014) suggests team theory to model a committee decision-making.

4 In his original model, there are no cost-push and preference shocks. Due to the scholastically singularity to estimate the model, the shocks are added to the model.

5 See detail at https://www.federalreserve.gov/faqs/money_12848.htm

8 Thank Boragan Aruoba for the helpful comment on the expectation of the private sector.

9 This could be another path of the research how much degree of bounded rationality the public has

10 ‘People think reading the raw transcripts is a way of learning things; I would suggest that if they spend six or eight months reading through some of this stuff, they won’t like it.’ Greenspan, Alan, quoted in the Transcripts, October 22, 1933.

11 Only low levels of rationality such as or

are considered.

References

- An, S., & Schorfheide, F. (2007). Bayesian analysis of DSGE. Econometric Reviews, 26(2–4), 113–172. https://doi.org/https://doi.org/10.1080/07474930701220071

- Anderson, G., Bunn, P., Pugh, A., & Uluc, A. (2016). The Bank of England/NMG survey of household finances. Fiscal Studies, Institute for Fiscal Studies, 37(1), 131–152. https://doi.org/https://doi.org/10.1111/j.1475-5890.2016.12091

- Andrade, P., Gaballo, G., Mengus, E., & Mojon, B. (2019). Forward guidance and heterogeneous beliefs. American Economic Journal: Macroeconomics, 11(3), 1–29. https://doi.org/https://doi.org/10.1257/mac.20180141

- Angeletos, G.-M., & Lian, C. (2018). Forward guidance without common knowledge. American Economic Review, 108(9), 2477–2512. https://doi.org/https://doi.org/10.1257/aer.20161996

- Barro, R. J., & Gordon, D. B. (1983). Rules, discretion, and reputation in a model of monetary policy. Journal of Monetary Economics, 12(1), 101–121. https://doi.org/https://doi.org/10.1016/0304-3932(83)90051-X

- Blinder, A. (1998). Central banking in theory and practice. The MIT Press.

- Blinder, A. S. (2018). Through a crystal ball darkly: The future of monetary policy communication. AEA Papers and Proceedings, 108, 567–571. https://doi.org/https://doi.org/10.1257/pandp.20181080

- Campbell, J. R., Evans, C. L., Fisher, J. D. M., & Jutiniano, A. (2012). Macroeconomic effects of federal reserve forward guidance. Brookings Paper on Economic Activity, 43(1), 1–80.

- Carroll, C. D., Crawley, E., Slacalek, J., Tokuoka, K., & White, M. N. (2020). Sticky expectation and consumption dynamics. American Economic Journal: Macroeconomics, 12(3), 40–76.

- Cass, D., & Shell, K. (1983). Do sunspots matter? Journal of Political Economy, 91(2), 193–227. https://doi.org/https://doi.org/10.1086/261139

- Cha, H. E. (2014). Committee decision-making in monetary policy. Working Paper. CUNY Academic Works. https://academicworks.cuny.edu/gc_etds/410

- Clarida, R., Gali, J., & Gertler, M. (2000). Monetary policy rules and macroeconomic stability: Evidence and some theory. Quarterly Journal of Economics, 115(1), 147–180. https://doi.org/https://doi.org/10.1162/003355300554692

- Coibion, O., Gorodnichenko, Y., & Kamdar, R. (2018). The formation of expectations, inflation, and the Phillips curve. Journal of Economic Literature, 56(4), 1447–1491. https://doi.org/https://doi.org/10.1257/jel.20171300

- Cuikerman, A. (1991). Why does the fed smooth interet rates. In M. T. Belongia (Ed.), Monetary policy on the 75th anniversary of the federal reserve system (pp. 111–147). Springer.

- Del Negro, M., Giannoni, M., & Patterson, C. (2012). The forward guidance puzzle. Staff Report 574. Federal Reserve Bank of New York. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr574.html

- Farhi, E., & Werning, I. (2019). Monetary policy, bounded rationality, and incomplete markets. American Economic Review, 109(11), 3887–3928. https://doi.org/https://doi.org/10.1257/aer.20171400

- Gabaix, X. (2020). A behavioral New Keynesian Model. American Economic Review, 110(8), 2271–2327. https://doi.org/https://doi.org/10.1257/aer.20162005

- Goodfriend, M. (1991). Interest rates and the conduct of monetary policy. Carnegie-Rochester Conference Series on Public Policy, 34(1), 7–30. https://doi.org/https://doi.org/10.1016/0167-2231(91)90002-M

- Goodhart, C. A. E. (1997). Why do the monetary authorities smooth interest rates. In S. Collignon (Ed.), European monetary policy (pp. 111–147). Pinter.

- Gürkaynak, R. S., Sack, B., & Swanson, E. T. (2005). Do actions speak louder than words? The response of asset prices to monetary policy actions and statements. Internation Journal of Central Banking, 1(1), 55–93.

- Haldane, A., & McMahon, M. (2018). Central bank communication and the general public. AEA Papers and Proceedings, 108, 578–583. https://doi.org/https://doi.org/10.1257/pandp.20181082

- Ireland, P. N. (2004). Technology shocks in the New Keynesian Model. Review of Economics and Statistics, 86(4), 923–936. https://doi.org/https://doi.org/10.1162/0034653043125158

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–291. https://doi.org/https://doi.org/10.2307/1914185

- Lucas, R. E. Jr. (1976). Econometric policy evaluation: A critique. Carnegie-Rochester Conference Series on Public Policy, 1, 19–46. https://doi.org/https://doi.org/10.1016/S0167-2231(76)80003-6

- Mankiw, G. N., & Reis, R. (2002). Sticky information versus sticky prices: A proposal to replace the New Keynesian Phillips Curve. The Quarterly Journal of Economics, 117(4), 1295–1328. https://doi.org/https://doi.org/10.1162/003355302320935034

- Orphanides, A. (2001). Monetary policy rules based on real-time data. American Economic Review, 91(4), 964–985. https://doi.org/https://doi.org/10.1257/aer.91.4.964

- Romer, C. D., & Romer, D. H. (2000). Federal reserve information and the behavior of interest rates. American Economic Review, 90(3), 429–457. https://doi.org/https://doi.org/10.1257/aer.90.3.429

- Rotemberg, J., & Woodford, M. (1997). An optimization-based econometric framework for the evaluation of monetary policy. In B. S. Bernanke & J. Rotemberg (Eds.), NBER Macroeconomics Annual 1997 (Vol. 12, pp. 297–361). MIT Press.

- Rudebusch, G. D. (2002). Term structure evidence on interet rate smoothing and monetary policy inertia. Journal of Monetary Economics, 49(6), 1161–1187. https://doi.org/https://doi.org/10.1016/S0304-3932(02)00149-6

- Simon, H. A. (1955). A behavioral model of rational choice. The Quarterly Journal of Economics, 69(1), 99–118. https://doi.org/https://doi.org/10.2307/1884852

- Sims, C. A. (2003). Implications of rational inattention. Journal of Monetary Economics, 50(3), 665–690. https://doi.org/https://doi.org/10.1016/S0304-3932(03)00029-1

- Smets, F., & Wouters, R. (2007). Shocks and frictions in US business cycles: A Bayesian DSGE approach. American Economic Review, 97(3), 586–606. https://doi.org/https://doi.org/10.1257/aer.97.3.586

- Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195–214. https://doi.org/https://doi.org/10.1016/0167-2231(93)90009-L

- Woodford, M., & Xie, Y. (2019). Policy options at the zero lower bound when forsight is limited. AEA Papers and Proceedings, 109, 433–437. https://doi.org/https://doi.org/10.1257/pandp.20191084

Appendix

1. A state-space representation: Kalman filter

In order to estimate the policy responses to an economy under bounded rationality, the system of equations need to be represented by state-space representation, known as Kalman filter. This can be categorised by state-equations, shock processes, and control equation:

(4)

(4)

(5)

(5)

(6)

(6)

Above system of state equations can be represented as:

(7)

(7)

where

Given above, the control equation can be represented as where

is scalar. Also,

and

Thus, the state equations can be rewritten as:

(8)

(8)

Finally, an observation equation is where

and

Based on this representation, Metropolis-Hasting Algorithm of Markov Chain Monte Carlo (MCMC) is implemented to generate a posterior density.