Abstract

The COVID-19 crisis has had deep adverse effects on a global level, affecting many economies and worsening their conditions which may have led to severe recession or even depression. The numbers of positive cases have risen sharply over the last few months, and the fatalities have also reached their peak. This study aims to examine the impact of the global financial crisis, and the COVID-19 pandemic on the macroeconomic variables of the US economy. It also provides an understanding in a descriptive format, to analyze and compare the global financial crisis and COVID-19 pandemic, in a tabulated and graphical format. For analysis purposes, the tables and average method have been used. For the graphical formats, charts have been used for the later year of 2008, and the beginning of the 2009 global financial crisis. The first six months of the spread of the COVID-19 pandemic have also been taken into consideration. The results have confirmed that the current COVID-19 pandemic shows more severity in terms of economic activity, than the global financial crisis had experienced. Moreover, the impact of the crisis on the recession probabilities in the current pandemic is lower than that at the time of the global financial crisis.

1. Introduction

The novel coronavirus or COVID-19 has a huge impact on the economies globally which is devastating in nature (Gao et al., Citation2021; Su et al., Citation2021a). The contagious disease has limited people to its homes which in turn affected the daily working life of the citizens. Unlike the other pandemics, it has an unprecedented impact on the labor market and consumer market. COVID-19, when declared pandemic on 12th march 2020, after China and South Korea, US market experienced shocks in response to the spread of the pandemic across the country and the Oil market crash, which affect the economy going downward and into recession (Su et al., Citation2021b). The COVID-19, combined with the oil market crisis, is affecting the US economy, which is experiencing stock market volatility, unemployment, lower consumer confidence and consumption, and lower industrial output. The economic and monetary policies are experiencing effects and swings that are similar or exceeding in nature than the major crises in the US before, i.e., global crisis 2008, Crash of 1978, and depression of 1929. Furthermore, the health issue, which is more important to limit people by introducing lockdown, has resulted in millions of American’s job losses and livelihoods.

Similarly, the imposing of lockdown across America impacts the general market completely, equal to recession. Economists revealed that financial markets jumped 18 times low and high in 25 days of March 2020 which is compared to bad news in the market, other than that, the contraction in US GDP, increase in prices of daily consumer goods, a huge decline in the industrial production along with services output, and low turnout of the stock exchange is expected (Su et al., Citation2020b; Umar et al., Citation2021b). Furthermore, due to the economic losses, unemployment is increased faster than the great financial crisis. The labor market and Morgan Stanley forecasts that the unemployment in the global crisis of 2008 went to 10 percent while the unemployment rate in the pandemic can reach up to 12.8 percent, which is alarming and can affect the job market badly. It is also stated that 3.3 million workers filed initial claims for insurance to the government in the second last week of March, which increased from 0.2 million workers in the previous week. Adding insult to the injury, Unemployment and consumer consumption is at the lowest level while most of the citizens and the job losses may lose their health insurance.

Additionally, In comparison to the global financial crisis of 2008, The COVID-19 pandemic is worse than GFC. While the global crisis of 2008 was evident that the US Economy had some structural problems before the crisis but in the case of the Pandemic 2020, it is proved that it is with one distinctive feature shock the US economy and the rest of the world just by spreading into the countries which compelled the US government to limit and restrict every movement and program to stop the contagion. The crisis caused by the pandemic in the US is now known as Black Swan or the great compression. Similarly, in the aftermath of the contagion, it is widely observed that de-globalization is in the making. Countries are closing their borders, movements of people, Airlines, and traveling by other means. Many Journalists, Economists, and authors have compared this crisis to the global war because of the contraction in the economies worldwide, including big G seven countries which supplies and fulfill demands almost of the rest of the world by supplying goods, exporting, and importing goods, producing 70% of goods globally have limited these services, which in turn had a massive effect on the stock markets and labor markets.

The pandemic has already started showing its consequences which we see in the world generally while specifically in the US, COVID-19 have affected the micro level and macro level firms eventually, i.e., the production and supplies are already disturbed physically, the routes and transport via Air Cargo and via sea from and to the US. This leads to the restriction of people working, which means job loss. Also, the low production and high demand will increase product prices, leading to high inflation and recession. The closing down of the economy in the US amid high positive daily cases also impacts the Oil index, Dow Jones, and Major stock exchanges. Compared to the other crisis, which was Financial crunches and more like in nature of Financial flaws, while the Current crisis of 2020 outcomes is in nature completely uncertain, it cannot be told when will it end and when will the economies bounce back. Major countries like the US, Germany, Canada, China, and Europe are surviving their economies with the help of reserves, while smaller countries may not and will fall into recession or even depression.

The study aims to examine the impact of the novel coronavirus on the macroeconomic variables of the US economy. It also provides an understanding in a descriptive format to analyze and compare both the crisis Global financial crisis and COVID-19 pandemic in a tabulated and graphical format. Moreover, this study highlights the present circumstances and the future economic outcomes in a reasonable manner. The paper also attempts to compare the GFC (Global Financial Crisis) and the current pandemic outbreak in the US. The study is not measuring any specific variable or outcome quantitatively because of the evolving model of the pandemic in the US. The research on the effects of the novel coronavirus pandemic on the macroeconomic variables is important in several meaningful ways: First, the findings of the study suggest some helpful insights which will help out the researchers to understand better the current economic conditions in relation to the available data, it will also present a view of macro-economic impacts and a wider view to understand the short-run and long-run impacts of the macroeconomic factors of the US economy in a tabulated and graphical manner. Second, the descriptive research will also make it easy that policymakers shall consider it while mitigating the risks of the outbreaks of economic threats.

2. Literature review

The literature on the impact of the COVID-19 pandemic on key macroeconomic variables is not rich. Few studies have worked on the COVID-19 in different directions (Mirza et al., Citation2020a; Rizvi et al., Citation2020b). (Mirza et al., Citation2020b) examine the performance and volatility in European investment funds during the outbreak of COVID-19. Using the monthly data for six months, the authors found that the investment funds show weekly performance. Similarly, (Yarovaya et al., Citation2021) examined the performance of equity funds and their relationship with human capital efficiency during the COVID-19. The authors found that the equity funds ranked higher in HCE outperformed their counterparts during the pandemic period. (Mirza et al., Citation2020b) examined the solvency profile of the firms in the EU states during COVID-19. The authors found that the solvency profile of all firms deteriorates during the pandemic. (Rizvi et al., Citation2020a) examine the performance of European funds during the outbreak. The findings of the study show that social entrepreneurship funds show a positive return during the outbreak.

(Sharif et al., Citation2020) Examined the linkage among variables related to the economy, i.e., the recent spread of the contagious disease COVID-19, Stock Prices, Oil prices and market volatility, Geopolitical scenario, and the uncertainty in the economic policy in the US by using the time series analysis for a specific time period. The author uses the Wavelet method and wavelet granger tests applied to the daily released data of COVID-19, Geopolitical risk, Stock market volatility, and oil Prices shocks and prices (Umar et al., Citation2021a). The results found in the study that the impact of the COVID-19 on the geopolitical risk is higher in the US than the economic uncertainty in the country. The pandemic Crisis can be seen differently over different time periods, which means that it can be seen as an economic crisis in the short run and while in the long run, it seems to be the geopolitical risk of the country.

Similarly, In the case of Unemployment in the US, Gangopadhyaya and Garrett (Citation2020) observed unemployment compared to both crises: the global financial crisis and the COVID-19 recent crisis. They took the Data of different health and industrial related employees and researched their job loss cum insurance loss. The study suggests that during GFC (Global Financial Crisis) 2008, unemployment reached 10 percent, while in the pandemic, the unemployment spike to 12 percent is still in the crisis. They also found that 3.5 million job workers have already filed an insurance claim to the US government during March.

Based on the Consumption of Consumer expenditures (Chen et al., Citation2020), the author studied different cities in China in consumer consumption expenditure and examined the impact of COVID-19 on the real consumer expenditure of consumption in China. The Consumption data of consumers were collected from 214 cities in china daily. This study used difference-in-differences for the offline consumption of consumers and those consumers who use union pay and QR scanner transactions (Su et al., Citation2021d). The author found out that during February and March, the offline consumption of consumers fell by 1% of the GDP, which is roughly estimated to 1 trillion RMB (Su et al., Citation2021d). They also implied that the situation continues the same as in the next two weeks. It could lead to 6 percent of GDP soon.

Additionally, the research about the psychological problems of the people during the pandemic is also documented. (Holingue et al., Citation2020) examined the consumers cum people facing stress and psychological distress due to the COVID-19 pandemic. The study aimed to protect people from mental health conditions and psychological distress during the pandemic. The data was collected from the American pew research center, which consisted of 9678 people and transformed into a survey-based questionnaire. A multi-linear regression model was used to find the actual results of anxiety, stress, mental condition, and psychological distress. The author finds out that 3 percent of the people were distress and tried using social media and other platforms on the internet to know about the coronavirus.

The Recreational and Tourism industry is also affected badly in the US. (Roy et al., Citation2020) examined the fact that the philanthropic and recreational industry is among the worst-hit industry in the US economy. They analyzed the data of 26 states where jobless applications were filed in these states and used the model of statistical approach, which is known as the top modeling approach. The study found out that there is a strong dissimilarity between the job losses before the pandemic and after the pandemic. The author also suggests the huge losses faced by any US industry and recreational and philanthropic sector. They also compare the low job losses in the industry and the higher ones in the industry based on the press reports of the companies and media outlets.

(Barua, Citation2020) explained the coronavirus and its impact on the entire world generally and on the G7 economies specifically. In the descriptive research, he also analyzed that most countries are going into recession, and some may face depression. He further presented the variables of the macro economy which are affected by the pandemic during 2020. It is believed that the pandemic is still an ongoing process. Therefore, it is accepted that the variables that really impact the US economy are analyzed and concluded. The author further analyzed that pandemic has hit the demand and supply channels, investment and trade, Financial markets, international cooperation, economic and financial stability, and policy and economic growth (Su et al., Citation2020a). The author aims to take an overall overview from the macro variables about the situation of the US economy. The study described each variable in a tabulated and graphical form and done the mapping to suggest to the policymakers how much a country’s economy has been affected by the pandemic during 2020.

(Wenzhi et al., Citation2020) checked the corporate immunity to COVID 19 Pandemic and firms’ response to the crisis in the meantime. Corporations are the backbone of the country’s economy and provide the largest chunk of monies to the economy. The author investigated 6000 companies of 56 economies worldwide. The study evaluated the reaction of corporate firms’ characteristics and stock price reactions to COVID-19 pandemic cases. The study concluded that for those firms with the largest pre-flexes from the pandemic, their supply chains were strong and customer channels were stable, and the executives are not embedded with lesser or milder effects on it by the pandemic crisis. Furthermore, the author finds out that companies with a greater corporate hedge fund in derivatives were affected than those major firms that were not involved in the corporate hedge funding or hedging their risk through derivatives in large amounts.

Additionally, to see whether the COVID-19 cases daily affect the stock prices in the US market (Alfaro et al., Citation2020) examined the impact of the pandemic trajectory on the daily infectious diseases in people on the stock return. The author estimated that doubling diseases in the trajectories would affect the stock prices from 4 percent to 11 percent in the decrease or an increasing timeline. The study finds out that the equity market will bounce back even the cases are increasing in nature if in the trajectories the infections are not worse than before. The study also finds out that firms with an environment mostly related and conducive to infections will have a high impact on the firm’s value and suffer job losses and vice versa. Furthermore, companies with high leverage will affect by the trajectories of the infection.

(Baker et al., Citation2020) measured the economic uncertainty and bloom picture of the Market policy. The study evaluated more than 12000 newspaper articles related to the mega-events, i.e., World war 1 and World War 2, the bankruptcy of the Lehman brothers, the Global financial crisis, and US presidential elections. The study finds out that the economic policy uncertainty is mostly based on the stock price fluctuations, reduction in the foreign and local direct investment, and unemployment in the sectors like defense, health, finance, and infrastructure construction which is most sensitive when it comes to economic policy creation. The economic policy uncertainty at the macro level can be affected in policy innovations that affect investments, output, and employment in the United States.

In the case of developing economies, Pakistan is also one of the major affected countries. (Ahmad et al., Citation2020) examined the impact of COVID-19 on the Pakistan stock exchange and its stock volatility. The author uses data of COVID-19 daily positive cases, fatalities and recoveries, and the 25 days of March beginning index of the Pakistan stock exchange. The author finds out that the recoveries are positively related to the stock exchange index while the fatalities and deaths are negatively related to stock prices (Su et al., Citation2021c).

To sum up, a bulk of research is carried out to examine the impact of COVID-19 on different dimensions of the economy. However, no study has been carried out to compare the consequences of the COVID-19 with the previous global financial crises. Hence, this study contributes to the existing literature by examining the impact of the novel coronavirus on the US economy’s macroeconomic variables and comparing both crises, such as the global financial crisis and the COVID-19 pandemic. Further, this is the first one to assess the impact of COVID-19 on present circumstances and future economic outcomes. The findings of the study have great managerial and policy implications. Since, one of the inspirations of this study is to assess the impact of COVID-19 on key macroeconomic variables such as industrial production, real personal consumption expenditure, recession probabilities, total business inventories, and unemployment rate (Su et al., Citation2020b). The most noteworthy of these include the smoothed US Recession probabilities during the two major crises, such as global financial crises and COVID-19. It is imperative to find out the probability of a recession in the US market. Based on the average possibility of a recession and to control the situation, the government would be able to take necessary steps. Moreover, the government would be able to ensure public safety and bail out the economy where the businesses jumped up to its normal level in a specific time. Hence, it is interesting to assess the response of the key macroeconomic variables during the outbreak and their comparative performance vis-à-vis in global financial crises. In the next section, the possible impact of COVID-19 and global financial crises on key macroeconomic variables has been presented in more detail. Further research is organized in descriptive analysis and mapping of the variables related to the US economy. The section is based on the results and discussion, and section four is on the conclusion, while the last part of section five is based on the policy recommendation.

3. Discussions on different macroeconomic variables

The major objective of this research is to show the implications of the COVID 19 pandemic crisis on macroeconomic variables. It also compares the COVID-19 pandemic and Global financial crisis to show how which crisis affects how much the US economy in general. It is understood that the current crisis is evolving in nature, and no such quantitative results can be produced, but descriptive research should be organized and documented in a tabulated and graphical format to understand the comparison between the two worse crises in the recent decade.

It is also to be noted that the current data is evolving daily and changing asymmetrically. The data for comparing the two crises are collected from different sources, i.e., Federal Reserve Bank of St Louis, Economic research division, IMF, World Bank, and World economic forum. presents the descriptive statistics of the key macroeconomic variables used in the study. The data covers the time period from October 01, 2007, to October 01, 2020. The high standard deviation of variables demonstrates that there is a high variation in all the macroeconomic variables. Moreover, the variables are skewed. The significant value of the Jarque-Bera statistics shows that the data is not normally distributed. Hence, we can argue that the global financial crises and COVID-19 pandemic have strongly affected the trend in key macroeconomic variables.

Table 1. Descriptive Statistics of the Key Macroeconomic Variables.

3.1. Overview of the US economy

The COVID-19 Pandemic has a huge impact on the United States of America. COVID-19 has suspended a large toll of operations and economic sectors in the US, which has created an ambiguous situation in the growth prospects and the country facing a deep recession. It is observed that the contagion has caused the biggest upset to the country’s economy since the great depression. GDP fell 32.9% at an annual rate which is the highest since the great depression. Unemployment is also received a huge shock, i.e., 30.2 million workers were receiving unemployment checks at the end of July. Moreover, Industrial production has also faced a huge setback, and the country’s growth is wiped out that is the last five years of growth is completely finished. Furthermore, the huge amount of income generated is hoarded because, in the first quarter, the consumer savings jumped from 1.59 trillion dollars to 4.59 trillion dollars. Consumer spending in this regard, which is more than two-thirds of the US economy, plunged at 34.6% this year. Investment in oil production and non-residential purposes dropped to 34.9 percent, while the overall business investments fell by 27 percent this year. Investments in infrastructures fell at a rate of 38.7 percent.

The descriptive research critically documented the tabulations and mapping through graphs to find out the impact of COVID-19 on the US economy macro variables i.e., Industrial production, real personal consumption expenditure, Recession probabilities, Total business inventories, and unemployment rate. However, the study also tries to examine the comparison of the current contagion crisis with the global financial crisis. The data for the following variables have already been adjusted monthly and seasonally.

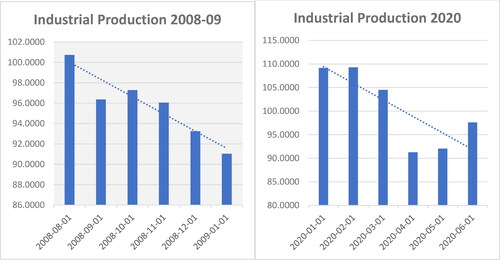

provides a detailed overview of US industrial production. A recent shock to the economy by the Pandemic is critical and full of impact on the US economy. The closures of borders, Transport routes ban, limitation of human’s movements and reduction in the flow of international trade. In Industrial production index fell from 109.2 in the first month of January 2020 to 98.9 in July 2020, which is higher in magnitude, and the average drop is even higher than the global financial crisis. In , industrial production was 100.8 in the month of August 2008, and it fell to 91.1, where the average drop rate is 95.8, which is lower in magnitude than the recent COVID-19 pandemic crisis. It is to be noted that in the 2008 Global financial crisis, the leaks in the economy were structural and human-made and controlled well at that time. Furthermore, it is to be noted that this contagious disease has given shocks to each and every area of resources whether these are labors, imports or exports, and raw materials production. Another comparison that can be made is that Banks in GFC were dried up, liquidity was shrinking, and because of its endogenous nature of the crisis, the economy bounced back after two years while in the recent pandemic, everything was normal, Banks were full of reserves, and by exogenous nature of the crisis, the industrial production is hit worse than that in the global financial crisis.

Figure 1. Comparison of Industrial Production During GFC and COVID-19.

Source: Authors own calculations.

Table 2. Industrial Production.

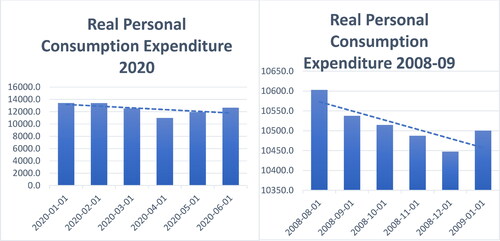

provides details about real personal consumption expenditures, also known as consumer spending, sharply dropped in the first and second quarter because of the repercussions of lockdowns and stoppage of daily activities of US citizens. In 2008 It did drop because of the financial crunch and no money issue. However, still, the Pandemic has a severe shock in the dropping of consumer spending as can been seen from the consumer spending dropped from 10603 million dollars to 10500.6 million dollars where the average point of the global financial crisis last 6 months were 10515.3. In contrast, the COVID-19 has a sharp decline on the average figure it is 12489.3, which can easily be understood that pandemic has a worse effect on the consumer spending than the Global financial crisis. The reason for such a sharp decline is that government and Counties had closed down businesses in the first two-quarters of the Pandemic in 2020 because of the extreme contagion of the virus and the first wave of it. While in the Global financial crisis, the problems during the crisis were the financial crunch and the mortgage issues where bank panic was created, later on the government introduced new laws and put trillions of dollars to rescue the economy () .

Figure 2. Real Personal Consumption Expenditures During GFC and COVID-19.

Source: Authors own calculations.

Table 3. Real Personal Consumption Expenditure.

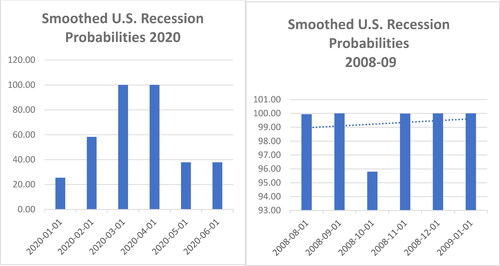

provides smooth recession probabilities in the US during the financial crisis in 2008-09 can be observed from where the probability at the start of 2009 was 100% because of the bankruptcy of large reserve firms, the bank panic in the country, and high inflation, While in the scenario of 2020 first half-year, . The country based on the average possibility and to control the situation by the government, first, three months were high in crisis, later on, The US government opened businesses time by time to let the situation out of the crisis. It is also to be noted that the US government introduced smart lockdowns with complete SOPs to ensure public safety and bail out the economy, where the businesses jumped up to its normal level after the first four months.

Figure 3. Smoothed US Recession Probabilities During Financial Crises and COVID.

Source: Authors own calculations.

Table 4. Smoothed US Recession Probabilities.

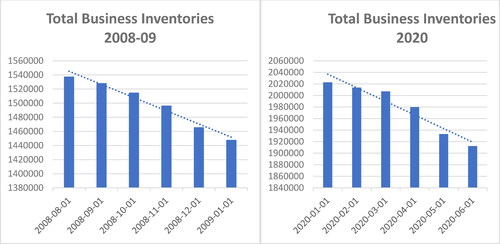

provides key figures about total business inventories in the US. As shown in , the key feature of the Global financial crisis was that the rapid decline of international trade is considered a country’s backbone. In the US, the total business inventory declined from 1537602 to 1448031, which is 5.8 percent, while in the Pandemic, the decline is near the GFC, 5 percent. In the latter end of 2008 and the beginning quarter of 2009, the business inventory dropped 10.8 percent, which is the highest during the Global financial crisis. Many suggest, such as (Economist April 2008), that the deep decline in the business inventory is because of the financial drying up in the economy, while the others suggest that the decline is because of the decline of the economic activity. The reason for the total business inventory is that in COVID 19 later months after the first quarter, the government ease the lockdowns in different states as well as the online e-commerce businesses like Amazon, eBay was in full support furthermore, the Inventory fell sharply in the month of April and may but bounce back in the July and the third quarter of the year.

Figure 4. Total Business Inventories During Financial Crises and COVID–19.

Source: Authors own calculations.

Table 5. Total Business Inventories, Millions of Dollars.

provides a detailed overview of US unemployment during financial crises and pandemics. presents the unemployment rate during the two major crises. It is evident from and figures that the unemployment rate was lesser in 2008 than in the 2020 Pandemic crisis. The reason for the higher unemployment rate during the current pandemic is mostly on a health basis. The sharp decline in the economic activity and lockdowns on an immediate basis across the country has suffered jobs to millions of Americans. In the case of the Global crisis, no such limits were in the application as compared to the current pandemic. (Banerdt et al., Citation2020) forecasts that the current unemployment rate can go up to 15 percent if the lockdown and the stoppage of the economic activity are still the same.

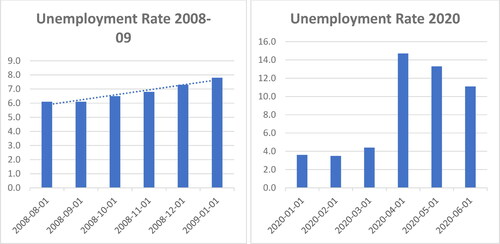

Figure 5. Unemployment Rate During Financial Crises and Pandemic.

Source: Authors own calculations.

Table 6. Unemployment Rate.

4. Conclusion and policy implications

This paper examines the role of COVID-19 and its impact on the macroeconomic variables of the US economy in comparison with the Global Financial Crisis. The variables we show in tabulated format and the graphical format for the six months of both the crisis where the crisis of nature was at a peak. We also explained each variable in descriptive format and depicted the economy’s picture in a descriptive format. It is understood that the current crisis may not be empirically and quantitatively not happening because of its evolving nature. Moreover, to the best of our knowledge, no single detailed study is available to compare GFC (global financial crisis and COVID-19) pandemic. Therefore, this study attempts to thoroughly explain the global financial crisis and COVID 19 impact on the US economy’s macroeconomic variables.

For the analysis, the study first collected the data from different trusted sources Economic research division of America and Federal Reserve Bank of America. The study analyzed each variable where each variable’s average change and average were calculated and then depicted in the graphical format to check the crisis’s impact. Industrial production, Consumer spending, total business inventories, and unemployment are severely impacted in the current pandemic crisis than the global financial crisis. Furthermore, the Smooth recessions probabilities were high in the Global financial crisis because of the financial crunch and drying up of banks and investment companies. In the end, we find that it is not exceptional that economies are not going into recession during the crisis. Such a crisis badly impacts the inventory level and affects international trade, leading to a decline in industrial production and employment level. The unemployment then further creates the space for low consumer spending.

For policy implications, such as exogenous crisis, the countries, especially the United States, should mostly focus on E-commerce, Advanced technology. For the pandemics like these, the US government should aggressively focus on making an innovative policy that should prevent the looming. The country should end the lockdown and introduce smart lockdowns in the area where the daily positive cases are high. The industries and financial markets should fully implement the standard operating procedures to start the economic engine. Furthermore, the US government should introduce online training and other such innovations where it is at ease not to stop the economic activity. However, waiting for the pandemic to end may lead the country into depression.

This research is limited to the role of COVID-19 and its impact on the macroeconomic variables of the US economy compared to the Global Financial Crisis. Future research may be carried out to examine the performance and volatility of equity funds of the USA during the evolution of COVID-19. Moreover, a future study is required to highlight the effects of this contagion COVID-19 on businesses across the country.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Ahmad, E., Stern, N., & Xie, C. (2020). From rescue to recovery: towards a post-pandemic sustainable transition for China [Working paper]. China Development Research Foundation. https://cdrf.org.cn/jjh/pdf/towards%20a%20postpandemic%20sustainable%20transition%20for%20China.pdf.

- Alfaro, L., Chari, A., Greenland, A. N., & Schott, P. K. (2020). Aggregate and firm-level stock returns during pandemics, in real time. National Bureau of Economic Research.

- Baker, S. R., Bloom, N., Davis, S. J., & Terry, S. J. (2020). Covid-induced economic uncertainty. National Bureau of Economic Research.

- Banerdt, W. B., Smrekar, S. E., Banfield, D., Giardini, D., Golombek, M., Johnson, C. L., Lognonné, P., Spiga, A., Spohn, T., Perrin, C., Stähler, S. C., Antonangeli, D., Asmar, S., Beghein, C., Bowles, N., Bozdag, E., Chi, P., Christensen, U., Clinton, J., … Wieczorek, M. (2020). Initial results from the InSight mission on Mars. Nature Geoscience, 13(3), 183–189. https://doi.org/10.1038/s41561-020-0544-y

- Barua, S. (2020). Understanding coronanomics: The economic implications of the coronavirus (COVID-19) pandemic. https://dx.doi.org/10.2139/ssrn.3566477, https://ssrn.com/abstract=3566477

- Chen, H., Qian, W., & Wen, Q. (2020). The impact of the COVID-19 pandemic on consumption: Learning from high frequency transaction data. Available at SSRN 3568574.

- Gangopadhyaya, A., & Garrett, A. B. (2020). Unemployment, health insurance, and the COVID-19 recession. Health Insurance, and the COVID-19 Recession. Retrieved April 1, 2020 from https://dx.doi.org/10.2139/ssrn.3568489, https://ssrn.com/abstract=3568489

- Gao, X., Ren, Y., & Umar, M. (2021). To what extent does COVID-19 drive stock market volatility? A comparison between the U.S. and China. Economic Research-Ekonomska Istraživanja, 1–21. https://doi.org/10.1080/1331677X.2021.1906730

- Holingue, C., Badillo-Goicoechea, E., Riehm, K. E., Veldhuis, C. B., Thrul, J., Johnson, R. M., Fallin, M. D., Kreuter, F., Stuart, E. A., & Kalb, L. G. (2020). Mental distress during the COVID-19 pandemic among US adults without a pre-existing mental health condition: Findings from American trend panel survey. Preventive Medicine, 139, 106231. https://doi.org/10.1016/j.ypmed.2020.106231

- Mirza, N., Hasnaoui, J. A., Naqvi, B., & Rizvi, S. K. A. (2020a). The impact of human capital efficiency on Latin American mutual funds during Covid-19 outbreak. Swiss Journal of Economics and Statistics, 156(1), 1–7. https://doi.org/10.1186/s41937-020-00066-6

- Mirza, N., Naqvi, B., Rahat, B., & Rizvi, S. K. A. (2020b). Price reaction, volatility timing and funds' performance during Covid-19. Finance Research Letters, 36, 101657. https://doi.org/10.1016/j.frl.2020.101657

- Rizvi, S. K. A., Mirza, N., Naqvi, B., & Rahat, B. (2020a). Covid-19 and asset management in EU: A preliminary assessment of performance and investment styles. Journal of Asset Management, 21(4), 281–291. https://doi.org/10.1057/s41260-020-00172-3

- Rizvi, S. K. A., Yarovaya, L., Mirza, N., & Naqvi, B. (2020b). The impact of COVID-19 on valuations of non-financial European firms. Available at SSRN 3705462.

- Roy, D., Tripathy, S., Kar, S. K., Sharma, N., Verma, S. K., & Kaushal, V. (2020). Study of knowledge, attitude, anxiety & perceived mental healthcare need in Indian population during COVID-19 pandemic. Asian Journal of Psychiatry, 51, 102083. https://doi.org/10.1016/j.ajp.2020.102083

- Sharif, A., Aloui, C., & Yarovaya, L. (2020). COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis, 70, 101496. https://doi.org/10.1016/j.irfa.2020.101496

- Su, C.-W., Dai, K., Ullah, S., & Andlib, Z. (2021a). COVID-19 pandemic and unemployment dynamics in European economies. Economic Research-Ekonomska Istraživanja, 1–13. https://doi.org/10.1080/1331677X.2021.1912627

- Su, C.-W., Huang, S.-W., Qin, M., & Umar, M. (2021b). Does crude oil price stimulate economic policy uncertainty in BRICS? Pacific-Basin Finance Journal, 66, 101519. https://doi.org/10.1016/j.pacfin.2021.101519

- Su, C.-W., Khan, K., Tao, R., & Umar, M. (2020a). A review of resource curse burden on inflation in Venezuela. Energy, 204, 117925. https://doi.org/10.1016/j.energy.2020.117925

- Su, C.-W., Qin, M., Tao, R., & Umar, M. (2020b). Financial implications of fourth industrial revolution: Can bitcoin improve prospects of energy investment? Technological Forecasting and Social Change, 158, 120178. https://doi.org/10.1016/j.techfore.2020.120178

- Su, C.-W., Song, Y., & Umar, M. (2021c). Financial aspects of marine economic growth: From the perspective of coastal provinces and regions in China. Ocean & Coastal Management, 204, 105550. https://doi.org/10.1016/j.ocecoaman.2021.105550

- Su, C.-W., Umar, M., & Khan, Z. (2021d). Does fiscal decentralization and eco-innovation promote renewable energy consumption? Analyzing the role of political risk. Science of the Total Environment, 751, 142220. https://doi.org/10.1016/j.scitotenv.2020.142220

- Umar, M., Su, C.-W., Rizvi, S. K. A., & Lobonţ, O.-R. (2021a). Driven by fundamentals or exploded by emotions: Detecting bubbles in oil prices. Energy, 231, 120873. https://doi.org/10.1016/j.energy.2021.120873

- Umar, M., Su, C.-W., Rizvi, S. K. A., & Shao, X.-F. (2021b). Bitcoin: A safe haven asset and a winner amid political and economic uncertainties in the US? Technological Forecasting and Social Change, 167, 120680. https://doi.org/10.1016/j.techfore.2021.120680

- Wenzhi, Z., Suyun, H. U., Lianhua, H. O. U., Tao, Y., Xin, L., Bincheng, G. U. O., & Zhi, Y. (2020). Types and resource potential of continental shale oil in China and its boundary with tight oil. Petroleum Exploration and Development, 47(1), 1–11.

- Yarovaya, L., Mirza, N., Abaidi, J., & Hasnaoui, A. (2021). Human capital efficiency and equity funds’ performance during the COVID-19 pandemic. International Review of Economics & Finance, 71, 584–591. https://doi.org/10.1016/j.iref.2020.09.017