Abstract

Using a text analysis of Chinese newspaper articles covering 1321 proposed mergers during 2008–2018, this study proposes attribution theory to examine how the media is susceptible to stereotype bias. Evidence reveals that the media pays considerable attention to and exhibits favourable sentiments toward overseas-experienced acquirers, which is found only in non-state-owned enterprises. Further analyses on the amplifying effect of stereotype bias show that the media slant more positively on large-scale overseas experiences. Results indicate that the media is biased, referring to impression migration from merger and acquisition experience.

1. Introduction

The media plays an essential role by providing information or monitoring firm behaviour for stakeholders (Bednar, Citation2012; Deephouse, Citation2000; Dyck et al., Citation2010; Miller, Citation2006; Pollock & Rindova, Citation2003; Westphal et al., Citation2012). Specifically, the media is proved to affect the outcome of merger and acquisition (M&A) transactions (Borochin & Cu, Citation2018). Social psychology perspective emphasizes how media bias influences public opinion and views (Baron, Citation2006; Cohen et al., Citation2017; Pollock & Rindova, Citation2003) and provides a useful framework for understanding media tendency in democratic societies (Baron, Citation2006; Chiang & Knight, Citation2011; Gentzkow & Shapiro, Citation2006, Citation2010; Hopmann et al., Citation2010; Reuter & Zitzewitz, Citation2006). However, the inherent media bias in socialist countries has not yet to be clearly examined. This study aims to investigate the forces that shape media bias in M&As in China, which is the largest socialist country and newspaper market in the world.

Attribution theory provides a theoretical framework for answering the question on how the media deviates from objectivity. Limitations in information processing capacity allow evaluators to simplify the complex problem by applying an event to a given experience (Jones & Davis, Citation1965). For example, one of the causes of stereotypes is that evaluators attribute an event to a character regardless of situational factors (Myers & Spencer, Citation2006). Addressed concretely to media bias in M&As, political goals and profitable incentives have revealed the manifestation of visible biases (Gurun & Butler, Citation2012; Lott & Hassett, Citation2014). However, invisible media bias, such as stereotype bias, is ubiquitous but rarely discussed. The development of text analysis tool makes it possible to analyse the sentiment of newspaper articles and provides methods to visualize invisible bias (Bednar, Citation2012; Borochin & Cu, Citation2018; Tetlock et al., Citation2008; You, Zhang, et al., Citation2018). We investigate stereotype bias by examining how the impression of overseas experience migrates in media coverage on M&As in China. By outlining invisible bias of media response, this article brings a behavioural perspective to the understanding of the media in M&As and ultimately raises questions about how effectively the media can function as an infomediary or social arbitrator.

2. Literature review

2.1. The role of media coverage

The media is believed to be an integral part of corporate governance, especially in asset pricing (Bhattacharya et al., Citation2009) and capital allocation (Bednar et al., Citation2013). The social arbiter view takes media coverage as a proxy for corporate reputation, which affects performance and market returns (Bednar, Citation2012; Deephouse, Citation2000; Dyck et al., Citation2008; Joe, Citation2003; Miller, Citation2006; Pfarrer et al., Citation2010; Wartick, Citation1992). The information intermediary view emphasizes how media coverage legitimate firms by influencing stakeholders’ perceptions (Barber & Odean, Citation2008; Bushee et al., Citation2010; Frankel & Li, Citation2004; Joe et al., Citation2009; Pollock et al., Citation2008; Pollock & Rindova, Citation2003).

Along with large-scale financial budgeting and long event periods, M&A announcements constantly catch the attention of investors and the media (Zaremba & Płotnicki, Citation2016). Both short-term and long-term performance at the announcement date are widely discussed in the value creation of M&As (Farinós et al., Citation2020; Latorre et al., Citation2014). Efficient contracting theory suggests that CEO reputation is positively associated with stock market responses to announcements of capital investments (Jian & Lee, Citation2011). Liu and McConnell (Citation2013) illustrated that media sentiments can affect managers’ sensitivity to stock price reactions in deciding whether to abandon an acquisition attempt. Chen et al. (Citation2017) demonstrated that negative coverage affects the termination of M&A. Twitter can likewise play a key role in reducing information asymmetry in market reactions to acquisition announcements (Mazboudi & Khalil, Citation2017). Yang et al. (Citation2019) showed that positive media coverage before M&A predicts stock returns in both short and long run. Gamache and Mcnamara (Citation2019) verified that negative media reaction to M&As will influence the subsequent acquisition activity.

2.2. The form of media bias

Bias deviates from objectivity, accuracy and realism (McQuail, Citation1992). While Takens et al. (Citation2010) divided bias into issue-based and actor-based biases, Eberl et al. (Citation2017) identified three bias subtypes (visible bias, tonality bias, and agenda bias). Fiske and Taylor (Citation2013) and Swim et al. (Citation2003) addressed blatant bias and subtle bias. Aronson et al. (Citation2015) expounded on the cognitive side of bias, namely, stereotypes, conformity, in-group preference and out-group prejudice.

Political bias and economic benefits are most widely discussed in social media (Gentzkow & Shapiro, Citation2010; Reuter & Zitzewitz, Citation2006). Groseclose and Milyo (Citation2005) firstly examined the liberal bias and found that media outlets would slant the coverage to the left. Chiang and Knight (Citation2011) demonstrated that media endorsement influences voters’ behavior. Lott and Hassett (Citation2014) suggested that American newspapers show an obviously positive tendency on Democrats compared with Republicans. Baloria and Heese (Citation2018) noted that firms located in districts with slanted media coverage exposure can suppress negative coverage before the election.

For economic benefits, Reuter and Zitzewitz (Citation2006) verified the positive correlation between mutual fund recommendations and advertising in personal newspapers compared with national newspapers. Gurun and Butler (Citation2012) indicated that the local media uses fewer negative words when reporting on local firms compared with nonlocal firms. Gentzkow and Shapiro (Citation2006, Citation2010) indicated that publications slant reports toward the beliefs of their audience, and that bias can be alleviated when audiences receive independent evidence.

2.3. Causal attribution of media bias

Despite evidence that independence and accuracy are important determinants of media coverage (Bednar, Citation2012; Frankel & Li, Citation2004; Joe et al., Citation2009), causal attribution of the media is generally underemphasized. Bednar et al. (Citation2015) demonstrated that managers are likely to suffer a severe reputational penalty when evaluators make internal attributions regarding the adoption of poison pill. Jones and Harris (Citation1967) identified antecedent factors that affect evaluators’ attribution of a specific behaviour to one factor over another. Heider (Citation1958) argued the covariation of antecedent factors in causal attribution and explained the formation of bias. For example, stereotypes generate fundamental attribution errors by over-reliance on existing information, which form biases (Kelley & Michela, Citation1980).

Cultural evidence showed that East Asians make less fundamental attribution errors than Westerners (Choi et al., Citation2003; Ishii et al., Citation2003; Miyamoto & Kitayama, Citation2002; Morris & Peng, Citation1994). In the Chinese media, the politico-economic trade-off generates market segmentation under the context of fierce competition and strict supervision (Qin et al., Citation2018). Borochin and Cu (Citation2018) verified that the Chinese media employs few negative words for local and overseas M&A deals. You, Chen, et al. (Citation2018) proved that the Chinese media report more positively on companies in region of prosperous economies, developed systems, and high levels of social trust. You, Zhang, et al. (Citation2018) find that articles from market-oriented media are more critical and accurate than those from state-controlled media.

3. Theory and hypotheses

3.1. Media bias in M&As

Despite the abundant research on media coverage and M&As in efficient markets, the predictive effect of media coverage on capital allocation for inefficient markets as China is relatively vague. Zhang and Su (Citation2015) empirically identified that a strong media governance environment restricts Chinese firms’ overinvestment behaviour. Borochin and Cu (Citation2018) indicated that the predictive power of media coverage on M&A outcomes is found only in non-SOEs.

In developing economies such as China, media coverage is produced under the context of government censorship and vibrant competition (Qin et al., Citation2018; You, Zhang, et al., Citation2018). Borochin and Cu (Citation2018) have shown that media coverage of overseas deals is more favourable, which are encouraged by the Chinese government. We extend the concept of stereotype bias and expect that perception of a previous transaction should lead to increased favourable evaluations of the media, especially those encouraged by the government. Thus, one would expect the favourability of an M&A deal’s coverage to increase if the bidder has overseas experiences. Our hypothesis can be summarized as follows:

H1: If the newspaper coverage of Chinese M&As shows stereotype bias, then the media coverage of overseas-experienced deals should be more favourable.

3.2. Media bias under political sensitivity

Previous literature has shown that political connections exert an important influence on firm decisions and performance in China (Claessens et al., Citation2000; Fan et al., Citation2007; Gul et al., Citation2010; Li & Zhou, Citation2005). The difference between SOEs and non-SOEs lies not only in ownership but also in external governance mechanisms, such as monitoring and takeovers (Li et al., Citation2011; Liao et al., Citation2014). Evidence from China also suggests that negative coverage can influence non-SOEs to abandon acquisition attempts by reducing the asymmetry information, which is not found in SOEs (Borochin & Cu, Citation2018). As SOEs are naturally politically controlled (Aharony et al., Citation2000; Allen et al., Citation2005; Sun & Tong, Citation2003), the political information provided by overseas experience is more effective for the media response regarding to M&As of non-SOEs. Therefore, we expect to observe stereotype bias in non-SOEs compared with SOEs. Our hypothesis can be summarized as follows:

H2: The media coverage of overseas-experienced deals should be more favourable for non-SOEs than for SOEs.

4. Sample and methods

4.1. Sample description

We obtain all M&As announced by Chinese listed companies between January 1, 2008 and December 31, 2018 from the Zephyr Database. The final sample is selected as follows: (1) the acquirer should initially own less than 50% of the target firm’s shares before the acquisition and seek to own more than 50% of the target firm’s shares from the acquisition; (2) the deal value of a transaction should be at least 100 million CNY; and (3) acquirers in financial industry are excluded (two-digit standard industrial classification codes between 60 and 69). Financial records data are obtained from the China Stock Market and Accounting Research (CSMAR) Database. The ultimate controller data are identified from the Sinofin Economic and Financial Database. Our final sample contains a set of 1321 transactions. presents the variable definitions.

Table 1. Variable definitions.

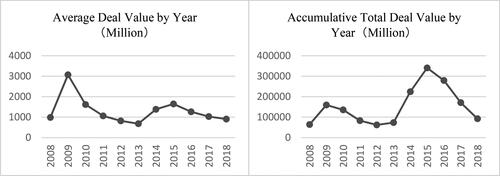

describes the deal value of the M&A transactions in our sample. In 2008, only 65 transactions occurred with an accumulative total deal value of 64.085 billion. The transaction deal value peaked in 2015, with an accumulative total deal value of 340.513 billion for 207 transactions. The average deal value peaked in 2009, indicating that the occurrence of increased block transactions before 2010 and the subsequent rise in the number of transactions.

Figure 1. Sample of evolution of M&A transactions during 2008–2018.

Source: Authors formation.

4.2. Variable construction

Media Coverage. Following Borochin and Cu (Citation2018), Lott and Hassett (Citation2014), and Tetlock (Citation2007), we count the proportion of positive words in a news text to measure the tendency of the media tone. Newspaper articles are collected by searching for target and bidder names in the China Core Newspaper Full-text Database. The sample window is from the date of an acquisition announcement to 60 days after or to the end of the negotiations, whichever comes first (Borochin & Cu, Citation2018). The number of newspapers constructs the media attention variable Media Attention. We then use the text analysis tool employed by Borochin and Cu (Citation2018) to obtain the proportion of positive words and get the Positive Tone variable,Footnote1 which is bounded between 0 and 1. Then we generate the Positive Stock variable as the product of Media Attention and Positive Tone.

Additionally, we identify eight large financial newspapers and categorize them into state-controlled newspapers (the China Securities Journal, Securities Daily, Securities Times, and the Shanghai Securities Journal) and market-oriented newspapers (the China Business Journal, First Financial Daily, The Economic Observer, and the 21st Century Business Herald) as You, Zhang, et al. (Citation2018) did. The number of articles in the state-controlled newspapers is defined as the State Media Attention, and the proportion of positive words in the state-controlled newspapers is defined as the State Positive Tone. We create the State Positive Stock as the product of State Media Attention and State Positive Tone. Cosh x, we create the Market Positive Stock from market-oriented newspapers.

Overseas Experience Dummy. We identify whether a bidder’s previous M&A transaction is an overseas deal as the proxy index for stereotype bias since 2000.

4.3. Descriptive statistics

presents the descriptive statistics of the variables. In the 1321 observations, 678 M&A transactions receive at least one news article. While 81.42% of the transactions attract the attention of state-controlled media, only 28.61% of the transactions capture the attention of market-controlled media. The average positive tone is 44%, with a standard deviation of 15.6%. State-controlled media shows higher positive tone than market-controlled media. As for M&A experience, 46.33% of the M&A deals have an M&A experience while only 7% have overseas M&A experience.

Table 2. Summary statistics.

The deal characteristics show that the average Deal Size is 6.162 million, with a standard deviation of 1.179. Only 4.5% of our sample are cross-border transactions, whereas 10.8% are cross-industry transactions. Only 8.2% of our M&A transactions are withdrawn, and 43.8% of the acquirers’ ultimate controller are SOEs. Prior to an announcement, the average Management Ownership of the acquirer is 12.6%, with a maximum is 82.2%. Moreover, the mean of the leverage debt ratio is 44.3%. The average total asset turnover and selling expense growth are 0.671 and 3.53, respectively.

5. Empirical results

5.1. Univariate analysis of key variables

The univariate test in presents that the possibility of prior experience and Gap Days are both higher for the SOE acquirers than for the non-SOE acquirers on average. The deal size of the SOE acquirers are significantly higher than those of the non-SOE acquirers. However, the non-SOE acquirers have a significantly higher return on assets, board independence, and management shareholding ratio. As for operating abilities, the non-SOE acquirers perform better than the SOE acquirers in terms of liquidity. However, the SOE acquirers have a higher total asset turnover ratio compared with the non-SOE acquirers.

Table 3. Univariate test of differences between SOE and non-SOE acquirers.

5.2. Regressions of positive media coverage

We evaluate our hypotheses in multivariate linear regression analyses with other factors controlled.

Column 1 of reports that the media prefers larger-scale M&A transactions and overseas deals. The bidder characteristics indicate that financial performance (ROA) and sales expense growth are positively associated with positive coverage, whereas the management shareholding ratio is negatively related to positive coverage.

Table 4. Regression of overseas M&A experience on positive coverage.

The results of this estimation of H1 are given in column 2 of . The coefficient of the Overseas Experience Dummy is positive and statistically significant (p-value < 0.05). H1 is supported that the media demonstrates stereotype bias by slanting politically supported deal experiences, which is consistent with the conclusion in Borochin and Cu (Citation2018). The significantly positive coefficient of the Overseas Deal Dummy (p-value < 0.01) suggests that the relationship between overseas experience and positive coverage is not based on the transfer of learning.

To assess H2, we estimate the regression by dividing the sample into SOE acquirers and non-SOE acquirers. According to , the Overseas Experience Dummy is positively associated with Positive Stock (p-value < 0.05) for the non-SOE acquirers other than the SOE acquirers. H2 is verified that the politically supported deal experience adds more information in non-SOEs. The association between deal size and positive coverage are significant in both SOEs and non-SOEs. In the non-SOEs, overseas transactions and high sales expense growth acquirers are positively associated with positive coverage, whereas asset turnover is negatively related to positive coverage. In the SOEs, positive coverage is negatively associated with the possibility whether a transaction is completed, whereas financial performance (ROA) and board independence are positively related to positive coverage.

5.3. Regressions of media attention

We extend our tests by examining the association between overseas M&A experience and media attention.

reports that the coefficient of the Overseas Experience Dummy is statistically significant, which exits only for the non-SOE acquirers. The results of media attention also support H1 and H2 and provide further evidence that the media shows stereotype bias in the attribution process.

Table 5. Regression of overseas M&A experience on media attention.

Interestingly, the large-scale deals and those that are highly likely to be withdrawn receive more media attention in both subsamples. As for the acquirer characteristics, the overseas deals of the non-SOE acquirers attract more media attention. The leverage debt ratio and selling expense growth are positively associated with media attention for the non-SOE acquirers, whereas the board independence of the SOE acquirers is positively related to media attention.

5.4. Interaction effect of deal size

We further explore the interaction of overseas experience and deal size of the previous transaction on both positive coverage and media attention.

indicates that the interaction term of overseas experience and previous deal size is positive and statistically significant (p-value < 0.01). Paradoxically, the deal size of a previous transaction is negatively associated with positive coverage. The result of the interaction term also indicates that large-scale overseas M&A experience receives more favourable coverage, which is consistent with our assumption. Subsample results show that the coefficient of the interaction term between overseas experience and prior deal size is significantly positive in the non-SOE acquirers compared with the SOE acquirers. This finding suggests that the amplify effect of Prior Deal Size exits only for the non-SOE acquirers.

Table 6. Interaction effect of deal size and overseas experience on positive coverage.

According to , the interaction effect of prior deal size and overseas experience is positively correlated with media attention (p-value < 0.01) and the amplify effect is valid only for non-SOEs. For non-SOE acquirers, media would show stereotype bias toward overseas-experienced bidders and the effect would be considerably impressive for large-scale transactions.

Table 7. Interaction effect of deal size and overseas experience on media attention.

5.5. Comparison between state-controlled media and market-oriented media

illustrates that the market-oriented media pays more attention to the overseas-experienced deals than the state-controlled media. Evidence also reveals that the coefficient of overseas experience is positive and statistically significant for the non-SOE acquirers compared with the SOE acquirers in both subsamples, as stated in H2. The results show that the market-oriented media exhibits more stereotype bias than the state-controlled media. Considering You et al. (2018b) who find that market-oriented media have significant corporate governance impact, the empirical finding of invisible bias in market-oriented media provides new insights in understanding the information efficiency in the Chinese market.

Table 8. Comparison between state-controlled media and market-oriented Media.

5.6. Robustness test

To address the problem of strategic selection, we use propensity score matching models (PSM) to match treated and control samples on their observable. We compare overseas-experienced deals with a propensity score-matched control sample of M&A deals without overseas experience for the standard nearest-neighbour matching estimator (1:1). Results indicate an average treatment effect of future potential of 2.93 (p < 0.5) when the dependent variable is media attention. demonstrates that most characteristics are insignificantly different after matching. Media attention is significantly higher for overseas-experienced deals than deals without overseas experience even after controlling for the characteristics in the PSM model. These findings suggest that our main results are robust to self-selection concerns.

Table 9. PSM estimation.

6. Conclusions

One assumption of media’s monitoring role in M&A transactions is that the media is impartial. However, bias is undoubtedly widespread in media coverage. Based on attribution framework, we test the idea that the media demonstrates stereotype bias and memorizes the impression formed by bidders’ previous transactions.

Using a measure of positive coverage for Chinese M&A announcements, we find that overseas experience is significantly correlated with positive coverage. We interpret this finding to mean that stereotype bias is shaped when information is excessive in the attribution process of the media. Moreover, the correlation between overseas experience and positive coverage exists only in non-SOE acquirers. This finding verifies that political impression only provides excess information to non-SOE acquirers compared with SOE acquirers. Results also verify that market-oriented media significantly pays more attention to overseas-experienced deals than state-controlled media, which reinforces the evidence provided by You, Zhang, et al. (Citation2018). Our results strongly suggest that stereotype bias slant media coverage in M&A transactions. Future studies will consider other types of biases, such as conformity or out-group prejudice.

Disclosure statement

No potential competing interest was reported by the authors.

Additional information

Funding

Notes

1 The Chinese text-mining software ROST EA, which was developed by Professor Yang Shen and his team at Tsinghua University, is widely used for text analysis, webpage crawling, news analysis, online public opinion, micro blogs, and so on.

References

- Aharony, J., Lee, C. W. J., & Wong, T. J. (2000). Financial packaging of IPO firms in China. Journal of Accounting Research, 38(1), 103–126. https://doi.org/10.2307/2672924

- Allen, F., Qian, J., & Qian, M. (2005). Law, finance, and economic growth in China. Journal of Financial Economics, 77(1), 57–116. https://doi.org/10.1016/j.jfineco.2004.06.010

- Aronson, E., Wilson, T., Akert, R., & Sommers, S. (2015). Social psychology (9th ed.). Pearson Education.

- Baloria, V. P., & Heese, J. (2018). The effects of media slant on firm behavior. Journal of Financial Economics, 129(1), 184–202. https://doi.org/10.1016/j.jfineco.2018.04.004

- Barber, B. M., & Odean, T. (2008). All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. Review of Financial Studies, 21(2), 785–818. https://doi.org/10.1093/rfs/hhm079

- Baron, D. P. (2006). Persistent media bias. Journal of Public Economics, 90(1-2), 1–36. https://doi.org/10.1016/j.jpubeco.2004.10.006

- Bednar, M. K., Boivie, S., & Prince, N. R. (2013). Burr under the saddle: How media coverage influences strategic change. Organization Science, 24(3), 910–925. https://doi.org/10.1287/orsc.1120.0770

- Bednar, M. K., Love, E. G., & Kraatz, M. (2015). Paying the price? The impact of controversial governance practices on managerial reputation. Academy of Management Journal, 58(6), 1740–1760. https://doi.org/10.5465/amj.2012.1091

- Bednar, M. K. (2012). Watchdog or lapdog? A behavioral view of the media as a corporate governance mechanism. Academy of Management Journal, 55(1), 131–150. https://doi.org/10.5465/amj.2009.0862

- Bhattacharya, U., Galpin, N., Ray, R., & Yu, X. (2009). The role of the media in the internet IPO bubble. Journal of Financial and Quantitative Analysis, 44(3), 657–682. https://doi.org/10.1017/S0022109009990056

- Borochin, P., & Cu, W. H. (2018). Alternative corporate governance: Domestic media coverage of mergers and acquisitions in China. Journal of Banking & Finance, 87, 1–25. https://doi.org/10.1016/j.jbankfin.2017.08.020

- Bushee, B. J., Core, J. E., Guay, W., & Hamm, S. J. W. (2010). The role of the business press as an information intermediary. Journal of Accounting Research, 48(1), 1–19. https://doi.org/10.1111/j.1475-679X.2009.00357.x

- Chen, Z. Y., Li, C. Q., & Wei, Z. H. (2017). 媒体负面报道影响并购成败吗——来自上市公司重大资产重组的经验证据 [Does negative coverage affect the success or termination of M&A: Evidence from material assets reorganization]. 南开管理评论, [Nankai Business Review], 20(1), 96–107. (in Chinese)

- Chiang, C. F., & Knight, B. (2011). Media bias and influence: Evidence from newspaper endorsements. The Review of Economic Studies, 78(3), 795–820. https://doi.org/10.1093/restud/rdq037

- Choi, I., Dalal, R., Kim-Prieto, C., & Park, H. (2003). Culture and judgement of causal relevance. Journal of Personality and Social Psychology, 84(1), 46–59.

- Claessens, S., Djankov, S., & Lang, L. H. P. (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58(1-2), 81–112. https://doi.org/10.1016/S0304-405X(00)00067-2

- Cohen, J., Ding, Y., Lesage, C., & Stolowy, H. (2017). Media bias and the persistence of the expectation gap: An analysis of press articles on corporate fraud. Journal of Business Ethics, 144(3), 637–659. https://doi.org/10.1007/s10551-015-2851-6

- Deephouse, D. L. (2000). Media reputation as a strategic resource: An integration of mass communication and resource-based theories. Journal of Management, 26(6), 1091–1112. https://doi.org/10.1177/014920630002600602

- Dyck, A., Morse, A., & Zingales, L. (2010). Who blows the whistle on corporate fraud? The Journal of Finance, 65(6), 2213–2253. https://doi.org/10.1111/j.1540-6261.2010.01614.x

- Dyck, A., Volchkova, N., & Zingales, L. (2008). The corporate governance role of the media: Evidence from Russia. The Journal of Finance, 63(3), 1093–1135. https://doi.org/10.1111/j.1540-6261.2008.01353.x

- Eberl, J. M., Boomgaarden, H. G., & Wagner, M. (2017). One bias fits all? Three types of media bias and their effects on party preferences. Communication Research, 44(8), 1125–1148. https://doi.org/10.1177/0093650215614364

- Fan, J. P. H., Wong, T. J., & Zhang, T. (2007). Politically connected CEOs, corporate governance, and Post-IPO performance of China's newly partially privatized firms. Journal of Financial Economics, 84(2), 330–357. https://doi.org/10.1016/j.jfineco.2006.03.008

- Farinós, J. E., Herrero, B., & Latorre, y M. A. (2020). Market valuation and acquiring firm performance in the short and long term: Out-of-sample evidence from Spain. Business Research Quarterly, 23, 1–14.

- Fiske, S. T., & Taylor, S. E. (2013). Social cognition: From brains to culture. Sage.

- Frankel, R., & Li, X. (2004). Characteristics of a firm's information environment and the information asymmetry between insiders and outsiders. Journal of Accounting and Economics, 37(2), 229–259. https://doi.org/10.1016/j.jacceco.2003.09.004

- Gamache, D., & Mcnamara, G. (2019). Responding to bad press: How CEO temporal focus influences the sensitivity to negative media coverage of acquisitions. Academy of Management Journal, 62(3), 918–943. https://doi.org/10.5465/amj.2017.0526

- Gentzkow, M., & Shapiro, J. M. (2006). Media bias and reputation. Journal of Political Economy, 114(2), 280–316. https://doi.org/10.1086/499414

- Gentzkow, M., & Shapiro, J. M. (2010). What drives media slant? Evidence from US daily newspapers. Econometrica, 78(1), 35–71.

- Groseclose, T., & Milyo, J. (2005). A measure of media bias. The Quarterly Journal of Economics, 120(4), 1191–1237. https://doi.org/10.1162/003355305775097542

- Gul, F. A., Kim, J. B., & Qiu, A. A. (2010). Ownership concentration, foreign shareholding, audit quality, and stock price synchronicity: Evidence from China. Journal of Financial Economics, 95(3), 425–442. https://doi.org/10.1016/j.jfineco.2009.11.005

- Gurun, U. G., & Butler, A. W. (2012). Don't believe the hype: Local media slant, local advertising, and firm value. The Journal of Finance, 67(2), 561–598. https://doi.org/10.1111/j.1540-6261.2012.01725.x

- Heider, F. (1958). The psychology of interpersonal relations. Psychology Press.

- Hopmann, D. N., Vliegenthart, R., De Vreese, C., & Albaek, E. (2010). Effects of election news coverage: How visibility and tone influence party choice. Political Communication, 27(4), 389–405. https://doi.org/10.1080/10584609.2010.516798

- Ishii, K., Reyes, J. A., & Kitayama, S. (2003). Spontaneous attention to word content versus emotional tone: Differences among three cultures. Psychological Science, 14(1), 39–46. https://doi.org/10.1111/1467-9280.01416

- Jian, M., & Lee, K. W. (2011). Does CEO reputation matter for capital investments? Journal of Corporate Finance, 17(4), 929–946. https://doi.org/10.1016/j.jcorpfin.2011.04.004

- Joe, J. R., Louis, H., & Robinson, D. (2009). Managers’ and investors’ responses to media exposure of board ineffectiveness. Journal of Financial and Quantitative Analysis, 44(3), 579–605. https://doi.org/10.1017/S0022109009990044

- Joe, J. R. (2003). Why press coverage of a client influences the audit opinion. Journal of Accounting Research, 41(1), 109–133. https://doi.org/10.1111/1475-679X.00098

- Jones, E. E., & Davis, K. E. (1965). From acts to dispositions the attribution process in person perception. Advances in Experimental Social Psychology, 2, 219–266.

- Jones, E. E., & Harris, V. A. (1967). The attribution of attitudes. Journal of Experimental Social Psychology, 3(1), 1–24. https://doi.org/10.1016/0022-1031(67)90034-0

- Kelley, H. H., & Michela, J. L. (1980). Attribution theory and research. Annual Review of Psychology, 31(1), 457–501. https://doi.org/10.1146/annurev.ps.31.020180.002325

- Latorre, M. A., Herrero, B., & Farinós, y J. E. (2014). Do acquirers’ stock prices fully react to the acquisition announcement of listed versus unlisted target firms? Out-of-sample evidence from Spain. Applied Economics Letters, 21 (15), 1075–1078. https://doi.org/10.1080/13504851.2014.909566

- Li, H., & Zhou, L. A. (2005). Political turnover and economic performance: The incentive role of personnel control in China. Journal of Public Economics, 89(9-10), 1743–1762. https://doi.org/10.1016/j.jpubeco.2004.06.009

- Li, K., Wang, T., Cheung, Y. L., & Jiang, P. (2011). Privatization and risk sharing: Evidence from the split share structure reform in China. Review of Financial Studies, 24(7), 2499–2525. https://doi.org/10.1093/rfs/hhr025

- Liao, L., Liu, B., & Wang, H. (2014). China’s secondary privatization: Perspectives from the split-share structure reform. Journal of Financial Economics, 113(3), 500–518. https://doi.org/10.1016/j.jfineco.2014.05.007

- Liu, B., & McConnell, J. J. (2013). The role of the media in corporate governance: Do the media influence managers' capital allocation decisions? Journal of Financial Economics, 110(1), 1–17. https://doi.org/10.1016/j.jfineco.2013.06.003

- Lott, J. R., & Hassett, K. A. (2014). Is newspaper coverage of economic events politically biased? Public Choice, 160(1-2), 65–108. https://doi.org/10.1007/s11127-014-0171-5

- Mazboudi, M., & Khalil, S. (2017). The attenuation effect of social media: Evidence from acquisitions by large firms. Journal of Financial Stability, 28, 115–124. https://doi.org/10.1016/j.jfs.2016.11.010

- McQuail, D. (1992). Media performance: Mass communication and the public interest. Sage.

- Miller, G. S. (2006). The press as a watchdog for accounting fraud. Journal of Accounting Research, 44(5), 1001–1033. https://doi.org/10.1111/j.1475-679X.2006.00224.x

- Miyamoto, Y., & Kitayama, S. (2002). Cultural variation in correspondence bias: The critical role of attitude diagnosticity of socially constrained behavior. Journal of Personality and Social Psychology, 83(5), 1239–1248.

- Morris, M. W., & Peng, K. (1994). Culture and cause: American and Chinese attributions for social and physical events. Journal of Personality and Social Psychology, 67(6), 949–971. https://doi.org/10.1037/0022-3514.67.6.949

- Myers, D. G., & Spencer, S. J. (2006). Social psychology (3rd ed.). McGraw.

- Pfarrer, M. D., Pollock, T. G., & Rindova, V. P. (2010). A tale of two assets: The effects of firm reputation and celebrity on earnings surprises and investors' reactions. Academy of Management Journal, 53(5), 1131–1152. https://doi.org/10.5465/amj.2010.54533222

- Pollock, T. G., Rindova, V. P., & Maggitti, P. G. (2008). Market watch: Information and availability cascades among the media and investors in the US IPO market. Academy of Management Journal, 51(2), 335–358. https://doi.org/10.5465/amj.2008.31767275

- Pollock, T. G., & Rindova, V. P. (2003). Media legitimation effects in the market for initial public offerings. Academy of Management Journal, 46(5), 631–642.

- Qin, B., Strömberg, D., & Wu, Y. (2018). Media bias in China. American Economic Review, 108(9), 2442–2476. https://doi.org/10.1257/aer.20170947

- Reuter, J., & Zitzewitz, E. (2006). Do ads influence editors? Advertising and bias in the financial media. The Quarterly Journal of Economics, 121(1), 197–227.

- Sun, Q., & Tong, W. H. S. (2003). China share issue privatization: The extent of its success. Journal of Financial Economics, 70(2), 183–222. https://doi.org/10.1016/S0304-405X(03)00145-4

- Swim, J. K., Scott, E. D., Sechrist, G. B., Campbell, B., & Stangor, C. (2003). The role of intent and harm in judgments of prejudice and discrimination. Journal of Personality and Social Psychology, 84(5), 944–959. https://doi.org/10.1037/0022-3514.84.5.944

- Takens, J., Ruigrok, N., van Hoof, A. M. J., & Scholten, O. (2010). Old ties from a new (s) perspective: Diversity in the Dutch press coverage of the 2006 general election campaign. Communications, 35(4), 417–438. https://doi.org/10.1515/comm.2010.022

- Tetlock, P. C. (2007). Giving content to investor sentiment: The role of media in the stock market. The Journal of Finance, 62(3), 1139–1168. https://doi.org/10.1111/j.1540-6261.2007.01232.x

- Tetlock, P. C., Saar‐Tsechansky, M., & Macskassy, S. (2008). More than words: Quantifying language to measure firms' fundamentals. The Journal of Finance, 63(3), 1437–1467. https://doi.org/10.1111/j.1540-6261.2008.01362.x

- Wartick, S. L. (1992). The relationship between intense media exposure and change in corporate reputation. Business & Society, 31(1), 33–49. https://doi.org/10.1177/000765039203100104

- Westphal, J. D., Park, S. H., McDonald, M. L., & Hayward, M. L. (2012). Helping other CEOs avoid bad press social exchange and impression management support among CEOs in communications with journalists. Administrative Science Quarterly, 57(2), 217–268. https://doi.org/10.1177/0001839212453267

- Yang, B., Sun, J., Guo, J. M., & Fu, J. (2019). Can financial media sentiment predict merger and acquisition performance? Economic Modelling, 80, 121–129. https://doi.org/10.1016/j.econmod.2018.10.009

- You, J., Chen, Z., Xiao, Z., & Xue, X. (2018). 财经媒体地域偏见实证研究 [An empirical study of religion bias in the financial media]. 经济研究 [Economic Research Journal], 53(04), 167–182. (in Chinese)

- You, J., Zhang, B., & Zhang, L. (2018). Who captures the power of the pen? The Review of Financial Studies, 31(1), 43–96. https://doi.org/10.1093/rfs/hhx055

- Zaremba, A., & Płotnicki, M. (2016). Mergers and acquisitions: Evidence on post-announcement performance from CEE stock markets. Journal of Business Economics and Management, 17(2), 251–266. https://doi.org/10.3846/16111699.2015.1104384

- Zhang, H., & Su, Z. (2015). Does media governance restrict corporate overinvestment behavior? Evidence from Chinese listed firms. China Journal of Accounting Research, 8(1), 41–57. https://doi.org/10.1016/j.cjar.2014.10.001