Abstract

This research examines the impact of corporate social responsibility (CSR) dimensions (employee, customer, community, and environment) on the sustainable business performance of the manufacturing industry. Manifestly, the mediating impact of firm reputation is also analyzed between CSR and sustainable business performance. In doing so, we have collected primary data from Italian manufacturing firm’s employees using simple random sampling. Smart-PLS was used to test the reliability of the covariates and relationships among the variables. The results revealed that CSR has a positive association with firm reputation and sustainable business performance. The findings also indicated that firm reputation has a significant and positive association with sustainable business performance. Moreover, firm’s reputation plays a positive and significant mediating role between CSR and sustainable business performance. These results provide valuable recommendations.

1. Introduction

As social and environmental awareness is increasing among the general public, it has become a critical need for business organizations to ensure sustainable business performance to attain a unique position both in the national and international markets and community (Asiaei & Bontis, Citation2019; Pearson et al., Citation2019). Sustainable performance is the act of the organization to carry on its activities without imparting adverse influences on the environmental quality and society (Sharif et al., Citation2019). A sustainable business operates its activities well-being of community and environment both at national and international level (Phillips et al., Citation2019). A firm makes sustainable performance when it is environmentally and socially conscious and focuses more than simply on profits; it has a keen observation of the effects of its activities on society and the environment quality. Such a business can be considered sustainable since it contributes to the social and environmental safety of the community in which it operates, hence contributing to creating an environment in which the business can thrive. Well-known scholars and practitioners have put a lot of effort into the concept of business sustainability. Such as Waheed and Zhang (Citation2020) studied the significance of sustainable business performance in highly competitive enviornment, where environmental and social safety is also demanded from suppliers or sellers along with the required goods or services.

People prefer to do business with organizations concerned about the general public's social and environmental concerns and regulatory bodies. The 'triple bottom line concept, coined by John Elkington, founder of the British consultancy ‘Sustainability’, has been used to determine the business's long-term viability. Society, the environment, and profits are the three components of this concept. A profitable, sustainable business demonstrates social responsibility to the community while safeguarding environmental resources (Pislaru et al., Citation2019). Corporate social responsibility (CSR) is a business paradigm in which firms make voluntary efforts to operate in a manner that enhances rather than degrades society well-being and environmental quality. The standard CSR practices are responsibilities towards employees (human capital enhancement), customers (ethical marketing), environment (environmental sustainability), and community (society improvement and social well-being) (Khan et al., Citation2021; Ye et al., Citation2020). The main objective of CSR is to give back to society, participate in philanthropic and activist causes, and give positive social value. Business organizations are increasingly moving towards CSR, making an exception, developing an excellent brand, and extensive marketing. Common CSR practices include environmental sustainability, human capital enhancement, community welfare, ethical conduct (Ben Abdallah et al., Citation2020; Borges et al., Citation2018). Similarly, the firm reputation implies ‘how the public perceives the firm's performance, triggered by CSR implementation from all four perspectives: environment, society, employees, and customers. Firm reputation is the image of a firm in the eyes of consumers, which affects their interaction with the firms and the level of firm marketing. Thus, the improved reputation of the firm enhances sustainable business performance (Herrera & de las Heras-Rosas, Citation2020).

Our study aims at analyzing the influences of CSR practices like responsibilities towards employees, customers, community, and environment on the firm reputation and sustainable business performance for the manufacturing industry of Italy. Italy is an upper-income economy run by a unitary parliamentary system. As per the gross domestic product (GDP) per capita, Italy is the 27th largest economy globally. According to purchasing parity, it was the 29 largest country in the world in 2019. The estimated nominal GDP for 2019 is $2.106 trillion. There are three main sectors of the economy of Italy: Agriculture, Industry, and Service (Tien et al., Citation2020). Despite accounting for 40.1 percent of GDP in 2004, the industrial sector only employed 12.9 percent of the workforce. Non-state activities accounted for 22.4 percent of industrial production in 2000. The industrial sector grew at an annual pace of 10.3 percent on average from 1994 to 2004. Manufacturing employed 10.2 percent of the workforce and provided 20.3 percent of GDP in 2004. Manufacturing GDP increased at an annual pace of 11.2 percent from 1994 to 2004 (Nguyen et al., Citation2018). The large automobile industry has emerged in the last decade.

Italy, being a developed country, faces many environmental problems. The manufacturing organizations that have a significant portion of the country’s GDP need special attention to accelerate the performance and develop sustainability in the business performance. Our study is an attempt to meet this need with an objective to give the ways to develop sustainability in business performance. The study aims to check the influences of CSR practices like responsibilities towards employees, customers, community, and environment on sustainable business performance. It is also its objective to analyze the role of firm reputation between CSR practices like responsibilities towards employees, customers, community, and environmentally sustainable business performance for the economy of Italy. Thus, the study aims to address the following research questions:

What is the role of SCR practices like responsibilities towards employees, customers, community, and environment in achieving sustainable business performance?

What is the role of CSR practices like responsibilities towards employees, customers, community, and environment in high firm performance?

What is the effect on firm reputation due to sustainable business performance?

What is the role of firm reputation between CSR practices and sustainable business performance?

This paper contributes on three grounds. First, in past studies, the CSR strategy has been mainly discussed without distinguishing its practices as the driver of sustainable financial performance. But current study removes this literary gap by determining CSR practices into the organizations’ responsibilities towards the employee, customers, community, and environment to analyze their impact on sustainable financial development. Second, in the previously conducted theoretical research, mostly one or two practices are used to predict sustainable financial performance. The current study focuses on all four CSR practices for attaining sustainable financial performance. Third, in the existing literature, the direct influences of CSR practices on firm reputation and sustainable business performance, and direct impacts of firm reputation on sustainable business performance. Thus, this study aims to address the firm reputation as a mediator between CSR practices and sustainable business development, which is a reasonable contribution to literature. Third, the study chooses the Italian economy to analyze the understudy constructs, while a lack of research has been done in Italy before this study.

This paper is composed of several parts. After an introduction, 2nd part of the paper deals with the association of CSR and its four dimensions, like responsibilities towards employees, customers, community, and environment, on firm reputation, and the achievement of sustainable business performance in the light of past studies. The 3rd part of the study throws light on the methodology applied to collect the CSR dimensions, like responsibilities towards employees, customers, community, and environment on firm reputation and the achievement of sustainable business performance and analyze its validity. 4th part compares the study results with the findings of other authors about the same subject and thus, approves these results. The paper ends with proper study implications, conclusions, and future recommendations.

2. Literature review

Sustainable business performance refers to the undertaking of the company's activities, functions, and operations so that they do not have harmful effects on the environment or the health of its customers while also fostering better social interactions with its stakeholders. According to Manning et al. (Citation2019), a highly sustainable firm maintains its policies and operations to produce greater profits while protecting the natural environment, thereby benefiting stakeholders (Irfan et al., Citation2021; Sharif et al., Citation2020). Business sustainability and the elements that influence it have received a lot of attention in the literature. This study focuses on the influences of CSR practices like responsibilities towards employees, customers, community, and environment on the firm reputation and sustainable business performance (Weller, Citation2020; Ye et al., Citation2020). The contribution of CSR to getting highly sustainable business performance has a significant position in the literature, which is used to build the following hypotheses.

CSR is a business concept that focuses on self-regulation within integrated enterprises and makes the enterprises socially responsible towards stakeholders like customers, employees, suppliers, investors, and the public (Barauskaite & Streimikiene, Citation2021). Business decisions and their activities have influences on society, the environment, and its economic position. These influences may be contributing or adverse, depending on the nature of decision making and business operations. SCR implementation is helpful to mitigate the negative social and environmental impacts and improve high sustainability in the business performance (Muhmad & Muhamad, Citation2020). The study was conducted by Bacinello et al. (Citation2020), to evaluate the influence of CSR on sustainable innovation and sustainable business performance. The study developed the model of CSRM and SIM for this purpose. The study applied resource-based theory and structural equation modelling along with a sample of 154 enterprises in Brazil to collect the data regarding the CSR responsibilities towards employees and business performance. The study represents that the enterprises which are integrated under CSR give employment opportunities to local workers, develop creative and leading skills in their employees, and take care of their social, emotional, and health needs. These employees become committed to the organization, focus on their duties, and maintain innovation in the business processes in the best interest of the firm. Thus, the effective implementation of CSR enhances sustainable business performance. An article was issued by Islam et al. (Citation2021) to discuss the importance of CSR practices regarding the welfare of customers in getting business sustainability. The study implies that management is concerned with product and customer service quality under the CSR business model. As a result, it uses production techniques and marketing channels to provide economic and emotional satisfaction to customers who interact with the company. In this method, product marketing can be improved by retaining existing customers while attracting new ones, allowing businesses to achieve long-term success. Similarly, empirical research made by Hou (Citation2019) investigates the influences of CSR practices towards the environment on sustainable business performance. The study reveals that under the CSR integration, enterprises operate their activities with great care and always keep a check on the flaws and deficiencies in their resources, techniques, and technologies, which could spoil the natural environment and initiate to remove these deficiencies. Thus, the environmental quality is not disturbed by the business operations. High environmental performance constructs highly sustainable financial performance. These arguments lead us towards the following hypothesis:

H1: The implementation of CSR practices is positively linked with sustainable business performance.

Corporate reputation' is the stakeholders' perception about a company, including its performance, behaviors, and operations (Lombardi et al., Citation2020). The effective implementation of CSR responsibility towards employees, customers, community, and environment, and the description of CSR application in annual reports improve the stakeholders’ perception of the company (Miras‐Rodríguez et al., Citation2020). A study was presented by Park (Citation2019) to explore practices in CSR and their influences on corporate reputation. This study acquired data from a sample of 967 airline service users and analyzed them with the help of structural equation modelling. This study implies that undertaking CSR practices for the improvement of environmental quality (recycling, renewable energy consumption, waste, and water management) and for the welfare of customers’ or general people in the community (charities, employment to local people, and avoidance from falsehood) improves the firm’s reputation among general public and customers. This helps achieve public trust and creates sustainability in the business performance. According to the views of Lu et al. (Citation2018), having implemented a CSR strategy effectively improves a company's conduct toward stakeholders such as employees, customers, suppliers, the general public, and government officials. The firm's representatives' way of treatment toward stakeholders reflects the firm's goals, considerations, and worries. As a result, a positive and polite way of dealing enhances the firm's reputation among stakeholders and propels the company forward. An investigation was made by Yuan et al. (Citation2020) to identify the relationship between CSR practices (ethical conduct) towards employees and customers and the business reputation. First, if the organizational management shows polite behavior towards the customers, provides support showing concern for their needs and motivates them to apply their ideas in business, the employees are committed to the organization and put effort into its reputation. Secondly, if the organization places a higher value on the customers and respects them, through ethical marketing like avoiding false advertisements, it successfully gets a reputation among the customers. Based on the above discussion, we may put the following hypothesis.

H2: The implementation of CSR practices is positively linked with the firm reputation.

Sustainable business performance is to maintain the financial position of the firms by maintaining social and environmental performance. Rehman et al. (Citation2020) define sustainable business performance as the harmonization of social, environmental, and financial objectives. Firms reputation, which represents the way stakeholders and the public perceive the firm, is helpful in leading the firm towards sustainable business performance, as argued by Singh and Misra (Citation2021), who shows a positive association between firm reputation and sustainable business performance. The firms' performance and market position depend on the firm’s reputation aroused by its way of conduct, effectiveness of the business process, quality of goods and customers services, and their impact on the environment and society. Deep research was done by Abbas (Citation2020), who debate on the firm reputation, integration with the stakeholders (suppliers, investors, logistics providers, or employees) who assist in carrying on business processes and sustainable business performance. When a firm has earned a high reputation among the stakeholders because of efficient past performance, they enjoy their trust and can give the firm favours or assistance when needed. Investors can give a large amount of money to invest in business resources or projects that aim to remove negative environmental impacts. The suppliers can allow the delivery of good quality resources in advance. In this situation, it becomes easy to achieve a high rate of sustainable business performance (An et al., Citation2021). The study conducted by Ait Sidhoum and Serra (Citation2018) analyzes the association of firm reputation with sustainable business development. The study analyzes that the marketing of products and services and revenues from sales are determined by the number of clients or consumers who deal with the company. Consumers' interest in items and readiness to buy is influenced by their level of satisfaction with the company's operations, customer service, and product quality. This contentment is engendered in the minds of consumers by the firm's reputation among experienced customers or other stakeholders.

H3: Firm reputation has a positive association with sustainable business performance.

A study was conducted by Cowan and Guzman (Citation2020) to evaluate the relationship among CSR practices towards employees and environment, firm reputation, and sustainable business performance. The authors collect secondary data about 135 different brands across industries and counties. Bivariate analysis and OLS regression were applied to analyze the Data acquired about the 135 domestic and foreign brands. This study implies that CSR focuses that the firms must adopt positive, supportive behaviour towards the employees to create dynamic skills in them and motivate them to work for the firm's best interest, maintaining its reputation. Similarly, when the management takes care of the environmental requirements of the firm, the quality of products and services also improves, which enhances the firm brand reputation. The reputation as a result of CSR ensures sustainability in the business performance. The study conducted by Mousa and Othman (Citation2020), identifies the relationship among the CSR responsibilities towards the stakeholders, firm reputation, and sustainability in business performance. Fourteen semi-structured interviews were conducted with operational managers, human resource managers, and chief executive officers from the healthcare sector in the West Bank. The quantitative data was collected from 69 respondents. Partial least squares structural equation modelling was applied for the analysis of data. The study implies that one of the basic objectives of the CSR is to show positive behavior towards the stakeholders and build strong bonding with them. It is the strong bong with the stakeholders which assists improve the brand image and raising the share of voice for the products and services of firms. The increased firm reputation help retain the customers and achieve sustainable business performance. That is why we can say:

H4: Firm reputation mediates between the implementation of CSR practices and sustainable business performance.

3. Research methodology

This research examines the impact of CSR dimensions such as employee, customer, community, and environment on sustainable business performance. Also, it examines the mediating impact of firm reputation among the nexus of CSR and sustainable business performance of manufacturing companies in Italy. The current research has used quantitative data collection methods and used the survey questionnaires for data collection. The researchers have selected the top twenty-five manufacturing companies of Italy under investigation. The employees of these selected manufacturing companies of Italy are respondents selected using simple random sampling. A total of 1050 survey questionnaires were sent by mail and also by personal visits. After two weeks, only 757 valid questionnaires were returned and used for analysis that represented around 72.10 per cent response rate.

Moreover, the smart-PLS was used to test the reliability and relationships among the variables. The researchers have used this statistical tool because it provides the best estimation in the case of complex models and large data sets (Hair et al., Citation2011). PLS-SEM can quickly evaluate many complex models and smaller sample sizes (Shiau et al., Citation2019). In addition, PLS-SEM has received substantial focus in a variety of disciplines including, management, marketing, health sciences, accounting and environmental studies. Moreover, PLS-SEM has the ability to handle problematic modelling issues that generally occur in the social sciences, like unusual data characteristics and highly complex models. The researchers have adopted one predictor such as CSR with four dimensions named employee, customer, community, and environment. In addition, CSR employee has seven items taken from the past study conducted by Bahta et al. (Citation2021), such as EMP1 ‘Our company takes into account employees’ interests for decision –making’, EMP2 ‘Our company helps employees balance their private and professional lives’, EMP3 ‘Our company’s policies encourage employees to develop their skills and careers’, EMP4 ‘Our company recognizes the importance of stable employment for its employees and society’, EMP5 ‘The managerial decisions related to the employees are usually fair’, EMP6 ‘Our company provides the basic facilities to their employee’, EMP7 ‘Our company provides procedures that help to ensure the health and safety of our employees’.

In addition, CSR customer has five items also taken from the study of Bahta et al. (Citation2021) such as CUS1 ‘Our company incorporates the interests of our customers in our business decisions’, CUS2 ‘Our company provides full and accurate information about its products/services to its customers’, CUS3 ‘Customer satisfaction is highly important for our company’, CUS4 ‘Our company takes measures to prevent customer complaints’, CUS5 ‘Our company responds to customer complaints or inquiries’. Moreover, the CSR community has seven items such as COM1 ‘Our company contributes to the campaigns and projects that promote the well-being of society’, COM2 ‘Our company has transparent relations with the local authorities’, COM3 ‘Our company is considered part of the local community and is concerned with its development and the improvement of its infrastructures’, COM4 ‘Our company encourages its employees to participate in voluntary work’, COM5 ‘Financially support activities (arts, culture, sports) in the communities where we operate’, COM6 ‘Stimulate economic development in the communities where we operate’, COM7 ‘Our company always ready to serve the local society’. Finally, CSR environment has six items taken from the past study conducted by Bahta et al. (Citation2021) such as ENV1 ‘Our company incorporates environmental concerns in business decisions’, ENV2 ‘Our company participates in activities that aim to protect and improve the quality of the natural environment’, ENV3 ‘Our company always ready to serve for environmental improvement’, ENV4 ‘Takes government regulations about the environment beyond what the law requires’, ENV5 ‘Invest/involved in saving energy’, ENV6 ‘Implements programs/involved to reduce water consumption’.

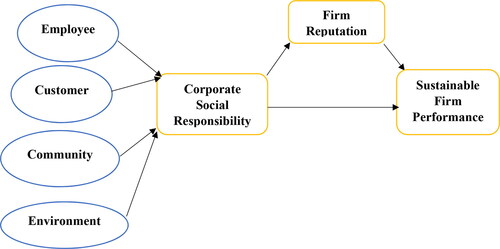

The researchers have taken the firm reputation (FR) as the mediating variable that has five items and also taken from the Bahta et al. (Citation2021) such as FR1 ‘Customers see us as being a very professional organization’, FR2 ‘Customers view our firm as one that is successful’, FR3 ‘Our firm’s reputation is highly regarded’, FR4 ‘Customers view our firm as one that is stable’, FR5 ‘Our firm is viewed as well-established by customers’. In addition, sustainable firm performance (SFP) has been taken as the dependent variable with four items such as SFP1 ‘Return on Assets (ROA)’, SFP2 ‘Return on Sales (ROS)’, SFP3 ‘General firm profitability’, SFP4 ‘Return on investments (ROI)’. These variables are shown in .

Figure 1. Theoretical model.

Source: Authors estimation.

4. Research findings

The current study shows the demographic statistics of the respondents. shows that 59.71 percent of the respondents are male, while 40.29 percent respondents were female. In addition, the results show that 68.96 percent of the respondents have graduation qualifications, while 27.87 percent of the respondents have master qualifications, and only 3.17 percent of the respondents have Ph.D. qualifications. Finally, the results also exposed that 39.50 percent of the respondents have zero to five years of experience while 57.20 percent of the respondents have six to ten years of experience, and only 3.30 percent of the respondents have ten and more years of experience.

Table 1. Demographics of the respondents.

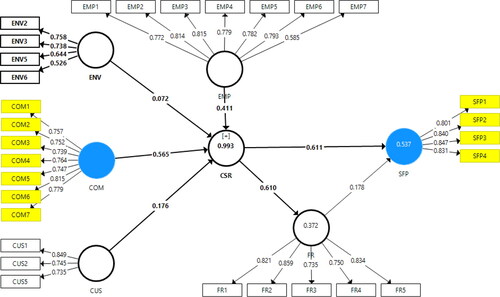

The results below () exhibit the convergent validity that shows the correlation of the items. The thumb rule implies that Alpha and composite reliability (CR) values should be higher than 0.70 while average variance extracted (AVE) and factor loadings values should be higher than 0.50 (Rodríguez et al., Citation2020). The figures below in report that the Alpha and CR values are higher than 0.70. The figures also showed that AVE and factor loadings are larger than 0.50. These figures indicated that high relationships among items and valid convergent validity.

Table 2. Convergent validity.

The results section highlighted the discriminant validity that shows the variable’s correlation. Firstly, the Fornell Larcker correlation was tested (Nasution et al., Citation2020). The figures given below in have been highlighted that the variable itself value that shows the nexus with itself is higher than the rest of the values that guide the relationships with other variables. These figures indicated that low relationships among variables and valid discriminant validity ().

Figure 2. Measurement model assessment.

Source: Authors estimation.

Table 3. Fornell Larcker.

Secondly, cross-loadings were used, and the thumb rule is that the item itself value that shows the association with itself should be larger than the values that show the association with items of other constructs (Nasution et al., Citation2020). The figures given below in show that the variable items themselves values that show the nexus with itself are higher than the rest of the values that show the relationships with other variables. These figures indicated that low relationships among variables and valid discriminant validity.

Table 4. Cross-loadings.

Thirdly, the Heterotrait Monotrait (HTMT) ratio was used, and the threshold value for the HTMT ratios is that it should not be greater than 0.90 (Afthanorhan et al., Citation2021). The figures given below in show that the values are lower than 0.90. These figures indicated that low relationships among variables and valid discriminant validity.

Table 5. Heterotrait monotrait ratio.

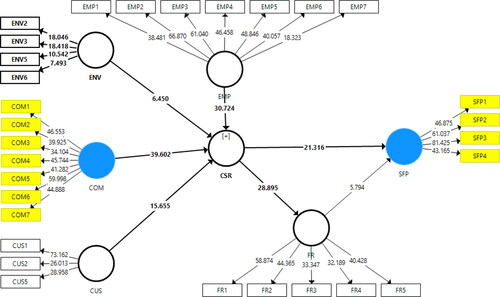

Finally, the results revealed that CSR positively correlates with firm reputation and sustainable business performance and accepts H1 and H2. The findings also indicated that firm reputation has a significant and positive nexus with sustainable business performance and accept H3. In addition, firm reputation also plays a positive and significant mediating role among the nexus of CSR and sustainable business performance and accept H4. shows these relationships.

Table 6. Path analysis.

5. Discussions

The study findings have revealed that the implementation of CRS has a positive association with sustainable business performance. These results align with the previous study of Guo et al. (Citation2020), which states that the effective implementation of CSR practices improves business performance and creates sustainability. Implementing CSR practices like recycling, waste management, and the application of renewable energy resources for business processes helps the firm mitigate the adverse impacts of its activities on the environment. This achieves sustainable business performance in three ways: minimizing the waste reduces cost, improves product quality, and gains public and government support. Consequently, the financial performance of the firm is also high. These results are also supported by the past study of Ghaderi et al. (Citation2019), which analyzes the role of CSR strategy in marketing and sustainable financial performance of the firms. This study analyzes that under the CSR business approach, the management takes care of the quality of products and customer services and, therefore, adopts such production techniques and marketing channels which could provide economic and emotive satisfaction to the consumers who come in contact with the firms. In this way, marketing for the products can be raised by retaining the old customers and attracting new ones, and thus, the firms can have sustainable business performance. These results are also supported by the past study of Uyar et al. (Citation2020), which showed that the manufacturing organizations implement CSR practices efficiently while performing business functions can achieve sustainable business performance ().

Figure 3. Structural model assessment.

Source: Authors estimation.

The study results have indicated that the implementation of CSR has a positive association with firm reputation. These results are supported by Anser et al. (Citation2018), which elaborate on CSR importance in a successful business. This study posits that the effective implementation of CSR strategy improves a firm's behaviors towards stakeholders like employees, suppliers, customers, the general public, and government authorities. The behavior of the firm representatives towards the stakeholders represents its objectives, consideration, and concerns. SO, the improved conduct improves the firm's reputation in the eyes of its stakeholders and turns the business towards success. These results agree with the previous study of Sánchez-Muñoz et al. (Citation2020). The implementation of CSR responsibilities of environmental sustainability, human resource enhancement, community involvement, and ethical marketing improves firm reputations. The work also supports these results out of Siueia et al. (Citation2019). This study suggests that when the company implements the CSR practices like the responsibilities towards the environment through proper waste management, and the effective choice of energy usage, customers through avoiding false descriptions and cooperative interaction, and community through different advertisement or charity programs, it gains high reputation among the general public and customers.

The study results have indicated that the firm reputation has a positive relation to firms' sustainable performance. These results are supported by the previous study of Ngai et al. (Citation2018), which shows that the marketing for the products and services and profits on their sales are dependent on the number of customers or consumers who deal with the concerned organization. Consumers' attention to the products and willingness to buy is shaped by their satisfaction towards the functioning of the concerned firm, their customer services, and product quality. This satisfaction arises in the minds of consumers through the firm's reputation on the part of experienced customers or other stakeholders. These results are in line with the previous study of D’Amato and Falivena (Citation2020), which confirms a positive association between the firm reputation and firm sustainable business performance, as the increase in the firm reputation brings improvement in the sustainability development in firm performance. These results are also supported by the past study of Agudelo et al. (Citation2019), which suggested that a firm's reputation works as an accelerator in getting a sustainable business performance. The firms' goodwill in the eyes of suppliers or logistics providers is helpful in getting the business processes like the internal business operations, production, and marketing of goods and services, as the firms' goodwill could build a healthy relationship of the organization with the suppliers or logistics providers.

The study results have also represented that the firms' reputation plays an appropriate mediating role between the implementation of CRS practices and sustainable business performance. The past study approves these results of Hernández et al. (Citation2020), which throws light on the role of a firm's reputation to build a link between the implementation of CSR practices and the achievement of sustainable business performance. This study elaborates that when a business firm effectively implements CSR practices like analysis of the situation to find flaws in the business processes including production, advertisement, and marketing which could adversely affect the environment, and society removes these flaws, it has the chance to catch sympathy and attention of general public and customers. The increased reputation of the firm among the stakeholders assures the availability of resources (physical and human resources) for the business processes and maintains marketing for the products and services of the goods. It leads to sustainable business performance. Hence, the firm's reputation mediates between CSR implementation and sustainable business performance. These results are also in line with the article written by Kraus et al. (Citation2020). This article suggests that under the CSR approach, which is the private self-regulation of the business organizations, the organization not only looks at the profitability but also takes such initiatives which could remove negative influences of business activities on the environment or minimize the exploitation of the rights of customers or the general public. In such a situation, the quality of products and services also improves. It enhances the firm's reputation among the general public and the circle of business organizations. The increased reputation of the firm enables it to get its policies executed more effectively through cooperation from the stakeholders like suppliers, government, investors, or customers.

5.1. Theoretical and empirical implications

The current study has both theoretical and empirical implications. The study achieves a significant place in the theoretical world because of its considerable contribution to environmental and social welfare literature. The current study analyzes CSR and its four dimensions, like responsibilities towards employees, customers, community, and environment, and analyzes its influences on achieving sustainable business performance. Though the current study has a single variable like CSR to check the change in sustainable business development and its performance, it gives a detailed description of this business strategy describing it from all the four perspectives of employees, customers, community, and environment. Many researchers or scholars have talked about the essential role of CSR in developing sustainability in business performance, but either they have discussed the importance of this strategy as a whole in sustainable businesses, or they have discussed only one or two dimensions out of responsibility towards employees, customers, community, and environment. Thus, our study, which explains CSR practices while analyzing their influences on sustainable business performance, contributes to the literature. Over overtime, the public is getting aware of the social and environmental concerns; this study has a great significance to the business management of manufacturing industries whose activities are considered the major source of environmental pollution and thus, put adverse impact on the social well-being of the public. This stud has importance because it provides a guideline on how to create sustainability in the business performance, which is the combination of social, environmental, and economic performance. This study gives motivation to the businesses that they should apply CSR practices in order to achieve highly sustainable performance. The study suggests that if the business takes care of all the CSR practices like responsibilities towards employees, customers, community, and environment, the firms can have highly sustainable business performance. The study also suggests that with the effective implementation of CSR responsibilities towards employees, customers, community, and environment, firms can achieve a good image among the stakeholders, and improved firm reputation enhances sustainable business performance.

6. Conclusion and limitations

The current study was conducted to provide ways for the manufacturing industry enterprises to create sustainability in the business performance, removing the negative impacts of business practices from the environment, community, or well-being of the people. This study introduces a CSR business strategy for attaining higher business performance. It elaborates the CSR along with its all four dimensions, like responsibilities towards employees, customers, community, and environment, and analyzes its influences on firm reputation and the achievement of sustainable business performance. In order to find the effects of CSR along with its all four dimensions, like responsibilities towards employees, customers, community, and environment on firm reputation and the achievement of sustainable business performance, the study collects relevant data from the Italian manufacturing industries. These results indicated that the effective implementation of different practices of CSR improves the business processes, enhances the production quality, and gains the support of stakeholders like customers, employees, suppliers, and government. Thus, it helps develop sustainability in the business performance. These results proved that, under the CSR integration, the enterprises in any industry themselves regulate their decisions and activities and disclose this fact in their reports. They can gain reputation and trust from people or entities they contact, thus ensuring sustainable business performance. The study concluded that the increase in the reputation of firm help them gain cooperation from their stakeholders in any business matter, and thus, they can have development in the business processes. Moreover, the effective implementation of CSR responsibilities towards employees, customers, community, and environment improves the firm's reputation, which is helpful in the achievement of sustainable business performance.

The current study is exposed to several limitations like many previous ones. These limitations may weaken the effectiveness of this study, but they may provide an opportunity for the authors to prove their efficiency in future studies, having removed these limitations. The most important thing that needs attention is the exploration of only one construct of sustainable business performance, like CSR. The CSR is described in detail with four dimensions such as the responsibilities towards employees, customers, community, and environment, and this study is limited because there are a large number of variables like organizational factors, energy usage, information system, and green finance, etc. (Shahzad et al., Citation2021; Sun et al., Citation2021; Zhuang et al., Citation2021) , which affect the sustainable business performance. So, the scope of the study is limited. Moreover, the author collects the data about the influences of CSR along with its all four dimensions, like responsibilities towards employees, customers, community, and environment, and analyzes its influences on the achievement of sustainable business performance from the manufacturing sector of the Italian economy.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abbas, J. (2020). Impact of total quality management on corporate green performance through the mediating role of corporate social responsibility. Journal of Cleaner Production, 242, 118458. https://doi.org/10.1016/j.jclepro.2019.118458

- Afthanorhan, A., Ghazali, P. L., & Rashid, N. (2021). Discriminant validity: A comparison of CBSEM and consistent PLS using Fornell & Larcker and HTMT approaches. Paper presented at the Journal of Physics: Conference Series.

- Agudelo, M. A. L., Jóhannsdóttir, L., & Davídsdóttir, B. (2019). A literature review of the history and evolution of corporate social responsibility. International Journal of Corporate Social Responsibility, 4(1), 1–23. https://doi.org/10.1186/s40991-018-0039-y

- Ait Sidhoum, A., & Serra, T. (2018). Corporate sustainable development. Revisiting the relationship between corporate social responsibility dimensions. Sustainable Development, 26(4), 365–378. https://doi.org/10.1002/sd.1711

- An, H., Razzaq, A., Nawaz, A., Noman, S. M., & Khan, S. A. R. (2021). Nexus between green logistic operations and triple bottom line: evidence from infrastructure-led Chinese outward foreign direct investment in Belt and Road host countries. Environmental Science and Pollution Research, 28, 51022–51045.

- Anser, M. K., Zhang, Z., & Kanwal, L. (2018). Moderating effect of innovation on corporate social responsibility and firm performance in realm of sustainable development. Corporate Social Responsibility and Environmental Management, 25(5), 799–806. https://doi.org/10.1002/csr.1495

- Asiaei, K., & Bontis, N. (2019). Using a balanced scorecard to manage corporate social responsibility. Knowledge and Process Management, 26(4), 371–379. https://doi.org/10.1002/kpm.1616

- Bacinello, E., Tontini, G., & Alberton, A. (2020). Influence of maturity on corporate social responsibility and sustainable innovation in business performance. Corporate Social Responsibility and Environmental Management, 27(2), 749–759. https://doi.org/10.1002/csr.1841

- Bahta, D., Yun, J., Islam, M. R., & Bikanyi, K. J. (2021). How does CSR enhance the financial performance of SMEs? The mediating role of firm reputation. Economic Research-Ekonomska Istraživanja, 34(1), 1428–1451. https://doi.org/10.1080/1331677X.2020.1828130

- Barauskaite, G., & Streimikiene, D. (2021). Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corporate Social Responsibility and Environmental Management, 28(1), 278–287. https://doi.org/10.1002/csr.2048

- Ben Abdallah, S., Saïdane, D., & Ben Slama, M. (2020). CSR and banking soundness: A causal perspective. Business Ethics: A European Review, 29(4), 706–721. https://doi.org/10.1111/beer.12294

- Borges, M., Anholon, R., Cooper Ordoñez, R., Quelhas, O., Santa-Eulalia, L., & Leal Filho, W. (2018). Corporate Social Responsibility (CSR) practices developed by Brazilian companies: An exploratory study. International Journal of Sustainable Development & World Ecology, 25(6), 509–517. https://doi.org/10.1080/13504509.2017.1416700

- Cowan, K., & Guzman, F. (2020). How CSR reputation, sustainability signals, and country-of-origin sustainability reputation contribute to corporate brand performance: An exploratory study. Journal of Business Research, 117, 683–693. https://doi.org/10.1016/j.jbusres.2018.11.017

- D’Amato, A., & Falivena, C. (2020). Corporate social responsibility and firm value: Do firm size and age matter? Empirical evidence from European listed companies. Corporate Social Responsibility and Environmental Management, 27(2), 909–924. https://doi.org/10.1002/csr.1855

- Ghaderi, Z., Mirzapour, M., Henderson, J. C., & Richardson, S. (2019). Corporate social responsibility and hotel performance: A view from Tehran, Iran. Tourism Management Perspectives, 29, 41–47. https://doi.org/10.1016/j.tmp.2018.10.007

- Guo, R., Lv, S., Liao, T., Xi, F., Zhang, J., Zuo, X., Cao, X., Feng, Z., & Zhang, Y. (2020). Classifying green technologies for sustainable innovation and investment. Resources, Conservation and Recycling, 153, 104580. https://doi.org/10.1016/j.resconrec.2019.104580

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hernández, J. P. S.-I., Yañez-Araque, B., & Moreno-García, J. (2020). Moderating effect of firm size on the influence of corporate social responsibility in the economic performance of micro-, small-and medium-sized enterprises. Technological Forecasting and Social Change, 151, 119–132. https://doi.org/10.1186/s40991-018-0039-y

- Herrera, J., & de las Heras-Rosas, C. (2020). Corporate social responsibility and human resource management: Towards sustainable business organizations. Sustainability, 12(3), 841–853. https://doi.org/10.3390/su12030841

- Hou, T. C. T. (2019). The relationship between corporate social responsibility and sustainable financial performance: Firm‐level evidence from Taiwan. Corporate Social Responsibility and Environmental Management, 26(1), 19–28. https://doi.org/10.1002/csr.1647

- Irfan, M., Razzaq, A., Chupradit, S., Javid, M., Rauf, A., & Farooqi, T. J. A. (2021). Hydrogen production potential from agricultural biomass in Punjab province of Pakistan. International Journal of Hydrogen Energy. https://doi.org/10.1016/j.ijhydene.2021.10.257

- Islam, T., Islam, R., Pitafi, A. H., Xiaobei, L., Rehmani, M., Irfan, M., & Mubarak, M. S. (2021). The impact of corporate social responsibility on customer loyalty: The mediating role of corporate reputation, customer satisfaction, and trust. Sustainable Production and Consumption, 25, 123–135. https://doi.org/10.1016/j.spc.2020.07.019

- Khan, S. A. R., Razzaq, A., Yu, Z., & Miller, S. (2021). Industry 4.0 and circular economy practices: A new era business strategies for environmental sustainability. Business Strategy and the Environment.

- Kraus, S., Rehman, S. U., & García, F. J. S. (2020). Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change, 160, 120262. https://doi.org/10.1016/j.techfore.2020.120262

- Lombardi, R., Manfredi, S., Cuozzo, B., & Palmaccio, M. (2020). The profitable relationship among corporate social responsibility and human resource management: A new sustainable key factor. Corporate Social Responsibility and Environmental Management, 27(6), 2657–2667. https://doi.org/10.1002/csr.1990

- Lu, W., Ye, M., Chau, K., & Flanagan, R. (2018). The paradoxical nexus between corporate social responsibility and sustainable financial performance: Evidence from the international construction business. Corporate Social Responsibility and Environmental Management, 25(5), 844–852. https://doi.org/10.1002/csr.1501

- Manning, B., Braam, G., & Reimsbach, D. (2019). Corporate governance and sustainable business conduct—Effects of board monitoring effectiveness and stakeholder engagement on corporate sustainability performance and disclosure choices. Corporate Social Responsibility and Environmental Management, 26(2), 351–366. https://doi.org/10.1002/csr.1687

- Miras‐Rodríguez, M. d M., Bravo‐Urquiza, F., & Escobar‐Pérez, B. (2020). Does corporate social responsibility reporting actually destroy firm reputation? Corporate Social Responsibility and Environmental Management, 27(4), 1947–1957. https://doi.org/10.1002/csr.1938

- Mousa, S. K., & Othman, M. (2020). The impact of green human resource management practices on sustainable performance in healthcare organisations: A conceptual framework. Journal of Cleaner Production, 243, 118595. https://doi.org/10.1016/j.jclepro.2019.118595

- Muhmad, S. N., & Muhamad, R. (2020). Sustainable business practices and financial performance during pre-and post-SDG adoption periods: A systematic review. Journal of Sustainable Finance & Investment, 5, 1–19. https://doi.org/10.1080/20430795.2020.1727724

- Nasution, M. I., Fahmi, M., & Prayogi, M. A. (2020). The quality of small and medium enterprises performance using the structural equation model-part least square (SEM-PLS). Paper presented at the Journal of Physics: Conference Series. https://doi.org/10.1088/1742-6596/1477/5/052052

- Ngai, E., Law, C. C., Lo, C. W., Poon, J., & Peng, S. (2018). Business sustainability and corporate social responsibility: Case studies of three gas operators in China. International Journal of Production Research, 56(1–2), 660–676. https://doi.org/10.1080/00207543.2017.1387303

- Nguyen, M., Bensemann, J., & Kelly, S. (2018). Corporate social responsibility (CSR) in Vietnam: A conceptual framework. International Journal of Corporate Social Responsibility, 3(1), 1–12. https://doi.org/10.1186/s40991-018-0032-5 https://doi.org/10.1186/s40991-017-0024-x

- Park, E. (2019). Corporate social responsibility as a determinant of corporate reputation in the airline industry. Journal of Retailing and Consumer Services, 47, 215–221. https://doi.org/10.1016/j.jretconser.2018.11.013

- Pearson, Z., Ellingrod, S., Billo, E., & McSweeney, K. (2019). Corporate social responsibility and the reproduction of (neo) colonialism in the Ecuadorian Amazon. The Extractive Industries and Society, 6(3), 881–888. https://doi.org/10.1016/j.exis.2019.05.016

- Phillips, S., Thai, V. V., & Halim, Z. (2019). Airline value chain capabilities and CSR performance: The connection between CSR leadership and CSR culture with CSR performance, customer satisfaction and financial performance. The Asian Journal of Shipping and Logistics, 35(1), 30–40. https://doi.org/10.1016/j.ajsl.2019.03.005

- Pislaru, M., Herghiligiu, I. V., & Robu, I.-B. (2019). Corporate sustainable performance assessment based on fuzzy logic. Journal of Cleaner Production, 223, 998–1013. https://doi.org/10.1016/j.jclepro.2019.03.130

- Rehman, Z. u., Khan, A., & Rahman, A. (2020). Corporate social responsibility's influence on firm risk and firm performance: The mediating role of firm reputation. Corporate Social Responsibility and Environmental Management, 27(6), 2991–3005. https://doi.org/10.1002/csr.2018

- Rodríguez, P. G., Villarreal, R., Valiño, P. C., & Blozis, S. (2020). A PLS-SEM approach to understanding E-SQ, e-satisfaction and e-loyalty for fashion e-retailers in Spain. Journal of Retailing and Consumer Services, 57, 102201. https://doi.org/10.1016/j.jretconser.2020.102201

- Sánchez-Muñoz, C., Muros, J. J., Cañas, J., Courel-Ibáñez, J., Sánchez-Alcaraz, B. J., & Zabala, M. (2020). Anthropometric and physical fitness profiles of world-class male padel players. International Journal of Environmental Research and Public Health, 17(2), 508–514. https://doi.org/10.3390/ijerph17020508

- Shahzad, F., Yannan, D., Kamran, H. W., Suksatan, W., Nik Hashim, N. A. A., & Razzaq, A. (2021). Outbreak of epidemic diseases and stock returns: An event study of emerging economy. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.1941179

- Sharif, A., Baris-Tuzemen, O., Uzuner, G., Ozturk, I., & Sinha, A. (2020). Revisiting the role of renewable and non-renewable energy consumption on Turkey’s ecological footprint: Evidence from Quantile ARDL approach. Sustainable Cities and Society, 57, 102138. https://doi.org/10.1016/j.scs.2020.102138

- Sharif, A., Raza, S. A., Ozturk, I., & Afshan, S. (2019). The dynamic relationship of renewable and nonrenewable energy consumption with carbon emission: A global study with the application of heterogeneous panel estimations. Renewable Energy, 133, 685–691. https://doi.org/10.1016/j.renene.2018.10.052

- Shiau, W.-L., Sarstedt, M., & Hair, J. F. (2019). Internet research using partial least squares structural equation modeling (PLS-SEM). Internet Research, 29(3), 398–406. https://doi.org/10.1108/IntR-10-2018-0447

- Singh, K., & Misra, M. (2021). Linking corporate social responsibility (CSR) and organizational performance: The moderating effect of corporate reputation. European Research on Management and Business Economics, 27(1), 100139–100153. https://doi.org/10.1016/j.iedeen.2020.100139

- Siueia, T. T., Wang, J., & Deladem, T. G. (2019). Corporate social responsibility and financial performance: A comparative study in the Sub-Saharan Africa banking sector. Journal of Cleaner Production, 226, 658–668. https://doi.org/10.1016/j.jclepro.2019.04.027

- Sun, Y., Duru, O. A., Razzaq, A., & Dinca, M. S. (2021). The asymmetric effect eco-innovation and tourism towards carbon neutrality target in Turkey. Journal of Environmental Management, 299, 113653. [PMC][34523535]

- Tien, N. H., Anh, D. B. H., & Ngoc, N. M. (2020). Corporate financial performance due to sustainable development in Vietnam. Corporate Social Responsibility and Environmental Management, 27(2), 694–705. https://doi.org/10.1002/csr.1836

- Uyar, A., Kilic, M., Koseoglu, M. A., Kuzey, C., & Karaman, A. S. (2020). The link among board characteristics, corporate social responsibility performance, and financial performance: Evidence from the hospitality and tourism industry. Tourism Management Perspectives, 35, 100714–100725. https://doi.org/10.1016/j.tmp.2020.100714

- Waheed, A., & Zhang, Q. (2020). Effect of CSR and ethical practices on sustainable competitive performance: A case of emerging markets from stakeholder theory perspective. Journal of Business Ethics, 8, 1–19. https://doi.org/10.1007/s10551-020-04679-y

- Weller, A. (2020). Exploring practitioners’ meaning of “ethics,” “compliance,” and “corporate social responsibility” practices: A communities of practice perspective. Business & Society, 59(3), 518–544. https://doi.org/10.1177/0007650317719263

- Ye, N., Kueh, T.-B., Hou, L., Liu, Y., & Yu, H. (2020). A bibliometric analysis of corporate social responsibility in sustainable development. Journal of Cleaner Production, 272, 122679. https://doi.org/10.1016/j.jclepro.2020.122679

- Yuan, Y., Lu, L. Y., Tian, G., & Yu, Y. (2020). Business strategy and corporate social responsibility. Journal of Business Ethics, 162(2), 359–377. https://doi.org/10.1007/s10551-018-3952-9

- Zhuang, Y., Yang, S., Razzaq, A., & Khan, Z. (2021). Environmental impact of infrastructure-led Chinese outward FDI, tourism development and technology innovation: A regional country analysis. Journal of Environmental Planning and Management. https://doi.org/10.1080/09640568.2021.1989672