?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Sustainable business performance is the major concern of every organisation globally and influenced by many factors that gained the attention of regulators and recent studies. Thus, the goal of this study was to examine the impact of corporate social responsibilities (CSR) on sustainable business performance in BRICS countries. These data were extracted from the financial statements and CSR reports of the top listed firms in BRICS countries. This study had adopted random effect model (REM) and generalised method of moments (GMM) to examine the nexus among the understudy variables. The results indicated that CSR have a positive association with the sustainable business performance in BRICS countries. These results are helpful for the policymakers while developing the policies related to the CSR and sustainable business performance.

Introduction

In the early 2000s, after Goldman Sachs economist Jim O'neil coined the word BRIC, the economies of Brazil, Russia, India, and China have been the primary subject of global politics and economics. South Africa joined the group in 2010, extending the tentacles of the main economies of the developing markets on four continents formally. By 2013, the BRICS served approximately 3 billion people, with a collective nominal gross domestic product (GDP) of 16,039 trillion dollars. The BRICS maintain about 4 trillion dollars in international assets, including more than a fifth in China alone. The success of the BRICS financial markets has been sterling in recent years. Reuters (2012) data disclose that Morgan Stanley Capital International (MSCI) has returned a striking 40% measure, seen within the 10-year horizon, compared with 320% and 98% of other developing and established markets. Between 2001 and 2007, the BRIC index of MSCI returned 500% to the other emerging markets. Recent evidence, however, shows that hay days may soon be over. In the last period, slumps with declines of 8.6% in dollars over the last five years have occurred. China's remarkable double-digit growth spurt is also diminishing. Brazil and South Africa have seen anaemic development, and Russia faces oil and gas problems as India's reforms are weak. The instability of growth rates and stock market results poses major concerns related to finance, fund diversification, and BRICS’s ultimate position in global economic growth (Hsu et al., Citation2021; Radulescu et al., Citation2014).

Consumers, financial firms, and policymakers ought to know foreign capital exchange organisations in a globalised environment. The awareness of knowledge ties and business connections is critical for policymakers and fund managers in their investment and risk management financial decisions (Aldakhil et al., Citation2018; Huang et al., Citation2021c; Mensi et al., Citation2017). If various countries have a similar role, participating in different equity markets will not result in the necessary diversification of portfolios. For this reason, a detailed evaluation of the degree and existence of the connection between the returns on the world stock market is essential. Convergence will also allow policymaking to evolve appropriate economic policies to cope with the crisis from other markets to domestic markets. Detailed research on stock market convergence would also be quite relevant today. Integration of the capital markets is a method of unifying the markets, and unlimited access by the investors to different business segments promotes integration. The globalisation of capital markets and the elimination of foreign cross-list controls have contributed to greater transfers of capital across economies, encouraged ownership and securities trade across the world Equity markets across the world have undergone growing integrations inside and across boundaries, powered by deregulation, globalisation, and developments in information technology (Arrive & Feng, Citation2018; Boubaker & Raza, Citation2017; Huang et al., Citation2021b). Increased market convergence has contributed to a stronger connection and interdependence over time among the world's current financial markets. In this analysis, the interdependence between BRIC economies is a modest attempt. In economics, BRIC is a collective acronym that applies to Brazil, Russia, India, and China that are perceived to have formed around a similar period. Global markets have experienced a lot of bumps and uncertainty over the years. This is the primary explanation why BRIC countries have become extremely relevant in the eyes of global investors. Literature indicates that reducing domestic economic growth rates, declining demand on the domestic sector, posing substantial challenges to Global investors' sustainability, finding different ways to spend their funds in order to ensure decent returns on capital and even protection for their capital (Contini et al., Citation2020; Huang et al., Citation2021a). ‘BRIC countries are promising a high degree of economic development with an expected sustained pace of economic operation over a few decades’. Because of the volatile global market situation, BRIC countries are drawn by the high rate of return on equity plus a projected capital appreciation. As a Global Investor, the development promise of these countries cannot be overlooked, and any expenditure in these countries will include portfolio performance enhancement. This has turned most foreign investors from western countries' focus to BRIC countries (Ali et al., Citation2018; Li et al., Citation2021; Tashman et al., Citation2019). Again, this global emphasis will help these countries leverage their capital, rendering those economies more efficient and ensuring better consumer openness.

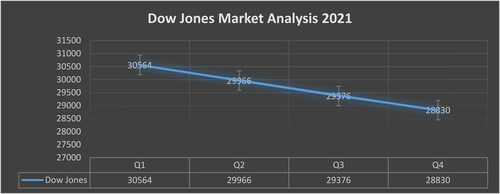

The Dow Jones Industrial Average is one of the U.S. benchmarks most closely tracked. It is a price-weighted index that measures the success of 30 giant, well-known American copies listed most of them on the New York Stock Exchange. The Industrial Average of Dow Jones is 40.94 as of 26 May 1896. Wall Street closed in the green on the first week of February 2021. Despite a weak January unemployment update, S&P 500 booked a new peak, and high indexes achieved their strongest week since November, with additional stimulus expectations growing. The Department of Labor said that the U.S. only generated 49,000 workers in the first month of 2021 when the losses in December were revised to 227,000 from 140,000, which triggered uncertainty about the economy’s condition. In the policy area, the Senate introduced a budget resolution at the beginning of Friday and Democrats moved a $1.9 trillion stimulus bill without Republican support. The Dow Jones added 92 or 0.3% to 31,148 marks. The S&P 500 earned a fresh high of 15 points or 0.4% to 3887. The Nasdaq climbed 79 points to 13,856, or 0.6%. The three big clues registered large gains throughout the week, with Dow Jones rising by 3.9%, S&P 500 4.7%, and Nasdaq 6%. The current market price of the stock stands at 31,175 with a rise of 0.41% compared to the second week of February 2021. Some highlights of the Dow Jones Market are given in .

Figure 1. Dow Jones market analysis 2021.

Literature review

Stock return is an important element for companies and countries. International eyes extend their look on the stock exchange of developing countries to initiate their projects with large investments. Stock return is also linked with corporate social responsibility disclosure because it enlarges the influences in different ways. In some BRICS organisations, the disclosure of CSR has been countered as a critical element impacting in various ways. While emphasising the banking sector, the composition of the board and the size of board trends with a wide impact on the CSR disclosure, which ultimately relates to stock return (Liu, Tang et al., Citation2021; Rouf & Hossan, Citation2021). Companies have their strong stock return while having the communication of CSR disclosure. Various implications of CSR disclosure have been depicted in the organisations that extend the financial performance. This is only due to the strong policies introduced for CSR disclosure which takes to the reputable markets where the share of stock return could be retrieved (Basheer et al., Citation2020; Liu, Lan et al., Citation2021). The dominance of financial performance is analysed with the effectiveness of corporate profitability and corporate governance in BRICS firms. These elements are wide disclosure of CSR disclosure and its implications on the value of companies, enabling the dominance of the given factors (Kamaliah, Citation2020; Othman et al., Citation2020). With effective corporate social responsibility disclosure, the stock return could gain positive results that enhance organisational operations.

Although, many other Mediterranean countries are also emphasising CSR disclosure due to its immense impacts on the stock exchange. This is only due to the effectiveness of some financial factors which dominate stock markets. The significance of return factors is also considered as important in BRICS organisations. They have inserted a broader look at the CSR disclosure by analysing the influence on the stock returns. A strong relationship exists between firms’ performance and CSR disclosure while checking from the perspectives of stakeholders (Buallay et al., Citation2020; Sadiq, Alajlani et al., Citation2021). The performance of corporate, financial, and operational markets has a significant influence on CSR disclosure, which provides various means to counter the issues of external effects. It is upon the good corporate governance in many countries that faces the depletion in stock returns. Various external factors of the economy significantly impact on the stock return. Therefore, from the initial aspects of organisations, corporate social responsibility disclosure is countered as a critical element in BRICS countries to eliminate the various effects. Some moderating factors have also been prominent among the effective corporate governance over the corporate values (Sadiq, Nonthapot et al., Citation2021; Suhadak et al., Citation2019). This is by introducing the relationship between financial performance and stock returns which extends their moderating effects on effectiveness.

The CSR disclosure is described as a crucial factor inducing the impact on stock markets. It is an ultimate effect of the organisational behaviour, which enables the influencing elements on the performance. Therefore, the elements of internal control induce its importance among the organisation to counter the issues that reduce the financial performance. The effects of internal controls are analysed among different qualities of returns while specifying the financial reporting in some firms (Lari Dashtbayaz et al., Citation2019; Sadiq, Hsu et al., Citation2021). Most of the BRICS firms have introduced the eminence of internal control through its robustness over the quality of financial reporting. So, serious considerations are always required among the stock markets. This will benefit the organisations by stating the effectiveness of internal controls to enhance the stock market returns. Most organisations emphasise internal control as an effective factor that states the strategies to tackle the indifferent situation that prevails in BRICS emerging markets. This part is strongly associated with the internal controls and information technology among the state agencies of many countries (Abbaszadeh Mohammad et al., Citation2019; Tan et al., Citation2021). Some administrative controls are viewed as primary factors striving over the internal controls. Therefore, the overall base of the internal control is to check the communication, risks, and activities in the organisation, which is better for interpreting stock returns.

The evaluations of internal controls specify the deficiencies that prevail in the organisations and have strong influencing parties. These parties are widely elaborated by the internal controls, and it is dependent on the administrative controls to insert the measures. These measures are required to control the effects that could be harmful to the BRICS stock market returns. Some reporting effects of the relationships between quality reports and internal controls are also depicted in the opinions of internal auditors (Gramling & Schneider, Citation2018; Xiang et al., Citation2021). Although, internal controls are not for eliminating weaknesses that prevail in the organisations and harming stock returns. Therefore, the dependence on internal controls could be helpful for the development of effective policies that are overweighing their influence on the stock return. Mostly, the attention of investors is diverted due to the reports of internal auditors. The reports are based on the facts that are performed in the organisations and causing mismanagement. This problematic situation could be covered in certain ways specified in the internal controls of BRICS organisations. These contain the dominance of internal controls for the uplifting of stock returns, which are highly linked with various precise elements. These elements are related to the attention of investors dominating with index volume and stating its impact on the stock return (Ehsanullah et al., Citation2021; Swamy & Dharani, Citation2019; Xueying et al., Citation2021). Some directions are always required in the stock return, whether forming a relationship with the profits or operational strategies.

Certain descriptions about the return on assets are highlighted, which is enumerated among the certainty of liquidity and leverage. The given enumeration about return on assets is stated by the disclosures of risky governance, which impact the stock return. Various financial elements describing the eminence of return on assets clearly illustrate the categories in organisations and their performance in BRICS markets. Although, a significant relationship exists between banking profitability and risk governance, with different comparisons prevailing in the emerging stock markets (Karyani et al., Citation2019; Zhao et al., Citation2021). It is upon the evaluators who are decided on earlier adoptions that are trending among the variety of investing structures. For certain feedbacks about return structures, the return on assets is denoted as a governing element for the stock return. Among the management levels, the variety of returns on assets and governing risks provide a significant portion of return. It is based on the organisation of return on assets that have been taken based on corporate performance. The board’s diversity and financial performance are positively related to each other in the BRICS countries (Chien, Sadiq et al., Citation2021; Sahar et al., Citation2018). While specifying the association of these factors, the diversity in genders also plays an important role in forming the legitimacy of return on asset theories.

Usually, the policymakers form various measures to have a positive stock return, but the ultimate effects of green stock markets also prevail. These are linked with the levels of investments that placed among the firm’s assets. This investment placement provides clear views of future stock return predictions with the relevance of marketing ratios and market capitalisation, especially in BRICS firms. It is among the stock return cross-sections and asset growths that are correlated with each other forming a significant position in emerging markets (Chien, Zhang et al., Citation2021; Constantinou et al., Citation2017). Stock returns are related to the return on assets which are based on the growth of investment in numerous firms. The influences of good governance are eminently stated in the organisation's structures. This is only due to the exact predictability of financial factors that provides an effective stock return. Many factors also influence the stock return, but the significance of return on asset is positively introduced in organisations. A variety of mediating elements form significant influences on financial performance and stock returns with the applicability of corporate value and corporate governance (Chien, Ananzeh et al., Citation2021; Kurniati, Citation2019). These are based on the acts of directions which are placed by the change in return on assets with the importance of investment in assets. It is important for the companies' return and the values among emerging stock markets.

Many economies face the effects of financial factors that affect stock returns. It is prevalent on the stock market factors, though, which endorses a variety of implications towards the stock returns. The factors comprise a variety of ratios and return on equity which implicates the impact towards a stock return. Stock return is positively associated with the effects of return on equity and book-to-market ratios (Araújo & Machado, Citation2018; Chien, Sadiq et al., Citation2021). It is the significance of risk factors that prevail among the variables of liquidity and BRICS capital markets. Besides this, some feasible investment strategies are also crucial that announce the significant benefits towards companies. Among the different industries of certain countries, the role of return on equity is considerably highlighted. The elements of financial liquidators are more considerable variables that form the combined effect on the stock return. The leverage measures have a strong revelation towards the profitability of BRICS companies. In the industries of some countries, the influences of financial leverage and liquidity dominate the profitability of firms (Samo Asif & Murad, Citation2019). Return on equity is enumerated by the formation of some leverage factors, which clears the views upon stock returns. Although stock markets are unpredictable, the ease of financial indicators has a strong eminence towards a stock return.

While using the elements of financial leverage for enhancing the financial performance of businesses, return on equity induces an important role. The inducement of financial factors has stated the importance of return on equity which forms various measures to strengthen stock return. This is only by return on assets, sales, capital, and many other factors, especially in BRICS organisations. Thus, indicates the major impact on the profitability in real estate companies by the financial leverage factor (Nguyen et al., Citation2019). This includes the role of return on equity and many elements related to return on assets and sales, which jointly form influences. Corporate governance is related to organisational performance because it endorses a portion towards a stock return. Return on equity is significantly linked with the era of corporate governance and many corporate architectures that provide positive stock returns. This is only by policy implications and proper evaluation of stock market factors, especially in BRICS organisations. There is an eminent link between corporate value, financial performance, good corporate governance, and financial architecture, which pleads its impact on stock market return (Suhadak et al., Citation2019). Corporate values also extend their support by the feasibility of return on equity which establishes robust stock returns.

Many organisations are conscious of the stock market returns. These have a positive association of market-related factors and the factors related to the firm size. Although financial factors also endorse one side impact, the organisational structure also places some effective role. This is due to the growth of firms and the growth of size in firms which states the proportionate influence among a variety of firms (Yadav et al., Citation2020). Many BRICS firms confirm the effects of the firm size, which extends the stock return, especially those that are disrupted due to the negative implications of economic grounds. Economies of many countries have faced negative and positive impacts of firm size. This is taken by the organisations of BRICS countries, which emphasised the role of firm size. This is important among the factors related to the growth of GDP, variables of the stock market, and liquidity ratio. The implication is upon the likelihood of targeted firms that place their role in the emerging markets. The takeover likelihood, marketing conditions, and firm size are positively associated with each other with slight cost relevance (Tunyi, Citation2019). It also includes GDP growth rate with the association of good economic conditions.

Among the financial factors, the role of macroeconomic factors could not be eluded. These factors are eminent among a variety of countries disrupting the economic conditions. The elaboration of these factors is prevailing under the monetary aspects clears the indication among BRICS stock exchange. Mostly, the influence of macroeconomic conditions over the sensitivity of investing cash flows states the matter of firm size and business affiliations (Gupta & Mahakud, Citation2019). The decisions of investments are internally and externally associated with each other, which constrains the financial impacts. It could add the elements that negatively impact the stock return, but the positive aspects could not be omitted. While stabilising the firms in some countries, the factors of organisational size could not be hidden. This can be taken by the positive implications of organisational structure, including firm size. This is based on the ownership structure and monopoly, which forces to enlarges the firm size, specifically in BRICS firms. The linkage of the firm size usually stabilises the stock returns from the perspectives of investors, which are found in emerging markets (Dumrongwong, Citation2020). Wide institutional underpricing and ownership is the wide indication of a firm size which helps in volatile stock return. Numerous highlights are also eminent towards deeper understandings that represent the effectiveness of policymakers in financial markets.

Research methods

The goal of the research was to investigate the impact of CSR and internal control along with the return on assets, return on equity, and firm size on the stock return of the firms in BRICS countries. These data were obtained from quantitative methods and gathered published secondary data. Then, the data were extracted from the financial statements and CSR reports of the top listed firm of BRICS countries. The random effect model (REM) and generalised method of moments (GMM) were employed to examine the nexus among the understudy variables. The following equation was developed based on past reviewed literature:

where;

SR = Stock Return

i = Firm

t = Time Period

CSRD = Corporate Social Responsibilities Disclosure

IC = Internal Control

ROA = Return on Assets

ROE = Return on Equity

FS = Firm Size

The stock return was used as a dependent variable measured as the market value of the share to the face value of the share. In addition, CSR disclosure was used as the predictor and measured as the value 0 for CSR not reporting firm and 1 for CSR reporting firm. Internal control was taken as the independent variable and measured as the time spent by directors to the total time required. Return on assets were measured as the ratio of net income to total assets, return on equity as the ratio of net income to total equity, and firm size as the log of total assets was used as the control variables of the study. These constructs with their measurement are shown in .

Table 1. Measurements of variables.

This study examined the multicollinearity assumption of the regression using the variance inflation factor (VIF). If the values of the VIF exceed the value of five than multicollinearity exist and vice versa. The equations for the estimation of VIF are given as follows:

(2)

(2)

(3)

(3)

The Hausman test was performed to check a suitable model for the study. The results indicated that REM is suitable for the study, and the study examined the nexus among the understudy variables using REM. Under REM, the total residual variance can be partitioned into two components: the between-school variance and the within-school variance. The estimations equations for the REM are given as follows:

(4)

(4)

(5)

(5)

In the above equation wit = εi + μit and εi shows the individual-specific error component and μit shows the time-series error component. Thus, this study established the estimation equation using the understudy variables as follows:

(6)

(6)

The nexus among the variables was examined using GMM model because it controls the effects of violation of the assumption of regression such as heteroscedasticity. The estimation equation of the GMM model is given as follows:

(7)

(7)

In the above equation, represented the lag term of the predictive variables and by adding understudy variables, this study established the GMM estimation equation as given below:

(8)

(8)

Results

The findings showed the minimum and maximum values along with the mean and standard deviation of the variables under descriptive statistics. The data highlighted that the average value of SR is 1.629, while the mean value of IC is 0.284. In addition, results showed that the average value of CSRD is 0.821, while the mean value of ROA is 1.291. Moreover, the outcomes highlighted that the average value of FS is 5.401, while the mean value of ROE is 5.439. These values are mentioned in .

Table 2. Descriptive statistics.

The findings also showed the relationships among the variables and showed that all the predictors such as IC, CSRD, ROA, FS, and ROE positively associate with SR. The results also showed that if 1% increase in IC and ROE, the SR increase by 4.5% and 36.6%, respectively (). On the contrary, if 1% change in CSRD, the SR also change by 12.8%. Moreover, the outcomes revealed that if 1% increase in ROA, the SR also increase by 34.1% while if 1% change in FS, the SR also change by 15.1%.

Table 3. Matrix of correlations.

The results of the multicollinearity assumption highlighted that the values of VIF are lower than five, which means no issue of multicollinearity in the data. In contrast, Hausman test results exhibited a probability value less than 0.05 indicates that the REM model is suitable.

In this study, the REM was used to test the relationships among the variables. The results revealed that CSR, internal control, return on assets, return on equity, and firm size have a positive association with the firm's stock return in BRICS countries. R square value highlighted that 43.6% variations in the stock return are due to the understudy variables, as shown in .

Table 4. Random Effect Model (REM).

Similarly, the GMM model results also showed that CSR, internal control, return on assets, return on equity, and firm size were positively associated with the firm's stock return in BRICS countries ().

Table 5. Generalized Method of Moments (GMM).

Discussion

This study examined the CSR disclosure impact on the financial performance of emerging countries like Brazil, Russia, India, and China. In these BRIC countries, China is considered the fastest and biggest emerging economy. Based on statistical results, CSR activities were positively associated with the financial position of developing countries like BRICs. It exhibited the prominent position of the company’s strength. The positive correlation between CSR and economic position encourages the policy initiative with CSR activities. The results corresponded with the study conducted by Lau et al. (Citation2016). It is noted that better CSR disclosure enhances the shareholders' value. Additionally, the CSR disclosure index is considered a potential tool that promotes a firm reputation in society. As a result, the firm enjoys a higher stock return in the stock exchange. Another study predicted the same positive relationship between stock return and CSR disclosure having higher scores and elaborated that CSR plays a vital role in making the interconnection between the firm and its shareholders while giving the awareness regarding their beneficial social activities (Jizi et al., Citation2016).

We found that firms with strong internal control may get more stock return. A significant positive relationship exists between these variables. The positive relationship is also reported by Mensi et al. (Citation2014). They stated that the firms that have command on internal control, environment, accounting system, policies, and monitor their all-operations avail financial benefits. The sound internal control system may ensure the business’s success. Ultimately, the firm gets a maximum stock return. Al-Thuneibat et al. (Citation2015) stated that a firm's strong internal control system might provide shelter from failure and provide a driver to boost business financial performance. In this sense, strong internal control of a firm has strong stock return similar to our study.

Other than that, the statistical results showed the relationship between ROA and stock return. The results indicated a positive relationship between these variables. Return on assets has directly influenced the stock return of the firm. Return on asset ratio calculated to examine that how a company utilises the assets to maximise the net profit. Likewise, Rostami et al. (Citation2016) suggested that ROA has a significant and positive impact on the stock return of a company. The research explained that the management had utilised the incredible positive return on assets signal. The positive association minimises the conflict between managers and shareholders, reducing the agency issues. In addition, Mubeen et al. (Citation2014) empirically assessed the impact of return on equity on stock return. High the return on equity indicates that the firm is using additional working capital for the company’s operation that ultimately maximises the stock return.

Furthermore, Purnamasari (Citation2015) explored the significant positive relationship between ROE and stock return. The researcher noted that the (ROE) positively affects stock return. The reason is that the company's pattern and investment procedure are very effective and fruitful, generating more profit and positively affecting the stock exchange. The more significant the return on equity ratio, the higher the stock return and better position. The prediction of this study is the same as our prediction and conclusion. Moreover, Bauer et al. (Citation2004) found that the firm's size positively impacts the stock return ratio. Their study established that the stock of small-sized firms enjoys more returns than the large-sized firm's stock as we are discussing firm size situated in BRIC countries. Therefore, it confirms that the firm size and stock returns have a significant and positive relationship even in developing the stock market, which is considered less efficient. In addition, Wong (Citation1989) confirmed that portfolios carrying the firm’s size and earnings/price (E/P) ratios experience higher stock returns than those who followed the CAPM model. By setting the standard American Stock Exchange, it is found that the most prominent is the firm size in the existence of a firm’s size effect and earing price effect. It is examined that earnings’ yields (E/P ratios), firm size, and returns on the firms' stock have a significant association in BRIC countries' Stock Exchange. This study has the same observation from 2016 to 2020; in the stock of firms related to BRIC countries, the risk-adjusted return is directly affected by the size of the firm.

Conclusion, implications and limitations

This paper examined the impact of CSR on sustainable business performance in BRICS countries. Specifically, this study analysed the association of CSR, internal control, and financial performance on stock returns by taking firm size as a control variable for the most top firms listed in the stock exchange from 2016 to 2020. Through in-depth study and data analysis, the firms can get the maximum stock return and more financial efficiency through better CSR disclosures, internal control, and appropriate capital structure. The standard-setting bodies and regulators recognise that sound internal control systems is an important tool to achieve management's fundamental objectives. The government should formulate rules and business laws that mandate all business and financial entities to submit their compliance. The local government should be imposed to submit the report regarding CSR by the managers. Also, the government should perform their duties to revise the requirement regarding CSR disclosure. The company’s stakeholders are interested in improving the report of their CSR practices and the formulated framework. The disclosure practice is vital for the effectiveness of business performance. By disclosing CSR reports and compliance, the companies can revise their strategies and broaden their vision and mission to improve their business profitability. This study suggests that emerging economies must be initiated by improving their corporate profitability to compete with developed countries.

The results of this study are crucial information for the government, policymakers, financial concerns, business credentials, and academia. By observing the positive linkage, the government of emerging economies motivates to give financial benefits to firms that have better results in CSR activities. The positive relationship between CSR and financial position encourages the policymakers to formulate CSR driving policies and revise the business law system. This study's analysis evaluated the business characteristics of values, management systems, and business regulations impact CSR practices. Consequently, this study is helpful for the policymakers while developing the policies related to CSR and stock return. Hence, this study is beneficial for business operations. As a result of the disclosure, companies will give special attention to their social responsibilities and operating issues.

In this study, data have been extracted from top listed companies of BRIC economies. Those companies that have government influence presented a better performance in CSR. More investigation about CSR activities of private firms related to developing countries, especially BRICS, is needed for more accurate data that represent the actual situation. It is recommended to further study with short and medium-sized firms of emerging countries to investigate their financial performance. Only internal control governance has been applied to measure the stock return in this study. More research can be conducted by applying an external governance mechanism to investigate the firms' financial position. Published data have been used to investigate the relationship between variables on the CSR of firms, but it is not clear of the actual performance of firms in CSR activities. The time horizon of this study is cross-sectional covered five years (2016--2020) and suggested that future studies should add more time span in their analysis.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Abbaszadeh Mohammad, R., Salehi, M., & Faiz Seyed, M. (2019). Association of information technology and internal controls of Iranian state agencies. International Journal of Law and Management, 61(1), 133–150. https://doi.org/10.1108/IJLMA-12-2017-0304

- Aldakhil, A. M., Nassani, A. A., Awan, U., Abro, M. M. Q., & Zaman, K. (2018). Determinants of green logistics in BRICS countries: An integrated supply chain model for green business. Journal of Cleaner Production, 195, 861–868. https://doi.org/10.1016/j.jclepro.2018.05.248

- Ali, S., Hussain, T., Zhang, G., Nurunnabi, M., & Li, B. (2018). The implementation of sustainable development goals in “BRICS” countries. Sustainability, 10(7), 2513–23. https://doi.org/10.3390/su10072513

- Al-Thuneibat, A. A., Al-Rehaily, A. S., & Basodan, Y. A. (2015). The impact of internal control requirements on profitability of Saudi shareholding companies. International Journal of Commerce and Management, 25(2), 196–217. https://doi.org/10.1108/IJCOMA-04-2013-0033

- Araújo, R. C. d C., & Machado, M. A. V. (2018). Book-to-market ratio, return on equity and Brazilian stock returns. RAUSP Management Journal, 53(3), 324–344. https://doi.org/10.1108/rausp-04-2018-001

- Arrive, J. T., & Feng, M. (2018). Corporate social responsibility disclosure: Evidence from BRICS nations. Corporate Social Responsibility and Environmental Management, 25(5), 920–927. https://doi.org/10.1002/csr.1508

- Basheer, M. F., Muneer, S., Nawaz, M. A., & Ahmad, Z. (2020). The antecedents of corporate social and environmental responsibility discourse in Pakistan: Multiple theoretical perspectives. Abasyn University Journal of Social Sciences, 13(1), 1–11. https://doi.org/10.34091/AJSS.13.1.01

- Bauer, R., Guenster, N., & Otten, R. (2004). Empirical evidence on corporate governance in Europe: The effect on stock returns, firm value and performance. Journal of Asset Management, 5(2), 91–104. https://doi.org/10.1057/palgrave.jam.2240131

- Boubaker, H., & Raza, S. A. (2017). A wavelet analysis of mean and volatility spillovers between oil and BRICS stock markets. Energy Economics, 64, 105–117. https://doi.org/10.1016/j.eneco.2017.01.026

- Buallay, A., Kukreja, G., Aldhaen, E., Al Mubarak, M., & Hamdan Allam, M. (2020). Corporate social responsibility disclosure and firms' performance in Mediterranean countries: A stakeholders' perspective. EuroMed Journal of Business, 15(3), 361–375. https://doi.org/10.1108/EMJB-05-2019-0066

- Chien, F., Sadiq, M., Nawaz, M. A., Hussain, M. S., Tran, T. D., & Le Thanh, T. (2021). A step toward reducing air pollution in top Asian economies: The role of green energy, eco-innovation, and environmental taxes. Journal of Environmental Management, 297, 113420. https://doi.org/10.1016/j.jenvman.2021.113420

- Chien, F., Zhang, Y., Sadiq, M., & Hsu, C. C. (2021). Financing for energy efficiency solutions to mitigate opportunity cost of coal consumption: An empirical analysis of Chinese industries. Environmental Science and Pollution Research, 29(2), 2448–2465. https://doi.org/10.1007/s11356-021-15701-9

- Chien, F., Ananzeh, M., Mirza, F., Bakar, A., Vu, H. M., & Ngo, T. Q. (2021). The effects of green growth, environmental-related tax, and eco-innovation towards carbon neutrality target in the US economy. Journal of Environmental Management, 299, 113633. https://doi.org/10.1016/j.jenvman.2021.113633

- Chien, F., Sadiq, M., Kamran, H. W., Nawaz, M. A., Hussain, M. S., & Raza, M. (2021). Co-movement of energy prices and stock market return: environmental wavelet nexus of COVID-19 pandemic from the USA, Europe, and China. Environmental Science and Pollution Research, 28(25), 32359–32373. https://doi.org/10.1007/s11356-021-12938-2

- Constantinou, G., Karali, A., & Papanastasopoulos, G. (2017). Asset growth and the cross-section of stock returns: Evidence from Greek listed firms. Management Decision, 55(5), 826–841. https://doi.org/10.1108/MD-05-2016-0344

- Contini, M., Annunziata, E., Rizzi, F., & Frey, M. (2020). Exploring the influence of Corporate Social Responsibility (CSR) domains on consumers’ loyalty: An experiment in BRICS countries. Journal of Cleaner Production, 247, 119158. https://doi.org/10.1016/j.jclepro.2019.119158

- Dumrongwong, K. (2020). Do institutional investors stabilize stock returns? Evidence from emerging IPO markets. Pacific Accounting Review, 32(4), 585–600. https://doi.org/10.1108/PAR-11-2019-0145

- Ehsanullah, S., Tran, Q. H., Sadiq, M., Bashir, S., Mohsin, M., & Iram, R. (2021). How energy insecurity leads to energy poverty? Do environmental consideration and climate change concerns matters. Environmental Science and Pollution Research International, 28(39), 55041–55052. https://doi.org/10.1007/s11356-021-14415-2

- Gramling, A., & Schneider, A. (2018). Effects of reporting relationship and type of internal control deficiency on internal auditors’ internal control evaluations. Managerial Auditing Journal, 33(3), 318–335. https://doi.org/10.1108/MAJ-07-2017-1606

- Gupta, G., & Mahakud, J. (2019). The impact of macroeconomic condition on investment-cash flow sensitivity of Indian firms: Do business group affiliation and firm size matter? South Asian Journal of Business Studies, 9(1), 19–42. https://doi.org/10.1108/SAJBS-06-2018-0073

- Hsu, C. C., Quang-Thanh, N., Chien, F., Li, L., & Mohsin, M. (2021). Evaluating green innovation and performance of financial development: mediating concerns of environmental regulation. Environmental Science and Pollution Research International, 28(40), 57386–57397. https://doi.org/10.1007/s11356-021-14499-w

- Huang, S. Z., Sadiq, M., & Chien, F. (2021a). The impact of natural resource rent, financial development, and urbanization on carbon emission. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-021-16818-7

- Huang, S. Z., Sadiq, M., & Chien, F. (2021b). Dynamic nexus between transportation, urbanization, economic growth and environmental pollution in ASEAN countries: Does environmental regulations matter? Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-021-17533-z

- Huang, S. Z., Chien, F., & Sadiq, M. (2021c). A gateway towards a sustainable environment in emerging countries: the nexus between green energy and human Capital. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.2012218

- Jizi, M., Nehme, R., & Salama, A. (2016). Do social responsibility disclosures show improvements on stock price? The Journal of Developing Areas, 50(2), 77–95. https://doi.org/10.1353/jda.2016.0075

- Kamaliah, K. (2020). Disclosure of corporate social responsibility (CSR) and its implications on company value as a result of the impact of corporate governance and profitability. International Journal of Law and Management, 62(4), 339–354. https://doi.org/10.1108/IJLMA-08-2017-0197

- Karyani, E., Dewo Setio, A., Santoso, W., & Frensidy, B. (2019). Risk governance and bank profitability in ASEAN-5: A comparative and empirical study. International Journal of Emerging Markets, 15(5), 949–969. https://doi.org/10.1108/IJOEM-03-2018-0132

- Kurniati, S. (2019). Stock returns and financial performance as mediation variables in the influence of good corporate governance on corporate value. Corporate Governance: The International Journal of Business in Society, 19(6), 1289–1309. https://doi.org/10.1108/CG-10-2018-0308

- Lari Dashtbayaz, M., Salehi, M., & Safdel, T. (2019). The effect of internal controls on financial reporting quality in Iranian family firms. Journal of Family Business Management, 9(3), 254–270. https://doi.org/10.1108/JFBM-09-2018-0047

- Lau, C., Lu, Y., & Liang, Q. (2016). Corporate social responsibility in China: A corporate governance approach. Journal of Business Ethics, 136(1), 73–87. https://doi.org/10.1007/s10551-014-2513-0

- Li, W., Chien, F., Kamran, H. W., Aldeehani, T. M., Sadiq, M., Nguyen, V. C., & Taghizadeh-Hesary, F. (2021). The nexus between COVID-19 fear and stock market volatility. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2021.1914125

- Liu, Z., Lan, J., Chien, F., Sadiq, M., & Nawaz, M. A. (2021). Role of tourism development in environmental degradation: A step towards emission reduction. Journal of Environmental Management, 303, 114078. https://doi.org/10.1016/j.jenvman.2021.114078

- Liu, Z., Tang, Y. M., Chau, K. Y., Chien, F., Iqbal, W., & Sadiq, M. (2021). Incorporating strategic petroleum reserve and welfare losses: A way forward for the policy development of crude oil resources in South Asia. Resources Policy, 74, 102309. https://doi.org/10.1016/j.resourpol.2021.102309

- Mensi, W., Hammoudeh, S., & Kang, S. H. (2017). Dynamic linkages between developed and BRICS stock markets: Portfolio risk analysis. Finance Research Letters, 21, 26–33. https://doi.org/10.1016/j.frl.2016.11.016

- Mensi, W., Hammoudeh, S., Reboredo, J. C., & Nguyen, D. K. (2014). Do global factors impact BRICS stock markets? A quantile regression approach. Emerging Markets Review, 19, 1–17. https://doi.org/10.1016/j.ememar.2014.04.002

- Mubeen, M., Iqbal, A., & Hussain, A. (2014). Determinant of return on assets and return on equity and its industry wise effects: Evidence from KSE (Karachi Stock Exchange). Research Journal of Finance and Accounting, 5(15), 148–157.

- Nguyen, V., Nguyen, T., Tran, T., & Nghiem, T. (2019). The impact of financial leverage on the profitability of real estate companies: A study from Vietnam stock exchange. Management Science Letters, 9(13), 2315–2326. https://doi.org/10.5267/j.msl.2019.7.023.

- Othman, Z., Nordin, M. F. F., & Sadiq, M. (2020). GST fraud prevention to ensure business sustainability: A Malaysian case study. Journal of Asian Business and Economic Studies, 27(3), 245–265. https://doi.org/10.1108/JABES-11-2019-0113

- Purnamasari, D. (2015). The effect of changes in return on assets, return on equity, and economic value added to the stock price changes and its impact on earnings per share. Research Journal of Finance and Accounting, 6(6), 80–90.

- Radulescu, I. G., Panait, M., & Voica, C. (2014). BRICS countries challenge to the world economy new trends. Procedia Economics and Finance, 8, 605–613. https://doi.org/10.1016/S2212-5671(14)00135-X

- Rostami, S., Rostami, Z., & Kohansal, S. (2016). The effect of corporate governance components on return on assets and stock return of companies listed in Tehran stock exchange. Procedia Economics and Finance, 36, 137–146. https://doi.org/10.1016/S2212-5671(16)30025-9

- Rouf, M. A., & Hossan, M. A. (2021). The effects of board size and board composition on CSR disclosure: A study of banking sectors in Bangladesh. International Journal of Ethics and Systems, 37(1), 105–121. https://doi.org/10.1108/IJOES-06-2020-0079

- Sadiq, M., Hsu, C. C., Zhang, Y., & Chien, F. S. (2021). COVID-19 fear and volatility index movements: Empirical insights from ASEAN stock markets. Environmental Science and Pollution Research International, 28(47), 67167–67184. https://doi.org/10.1007/s11356-021-15064-1

- Sadiq, M., Nonthapot, S., Mohamad, S., Chee Keong, O., Ehsanullah, S., & Iqbal, N. (2021). Does green finance matters for sustainable entrepreneurship and environmental corporate social responsibility during Covid-19?. China Finance Review International. https://doi.org/10.1108/CFRI-02-2021-0038

- Sadiq, M., Alajlani, S., Hussain, M. S., Ahmad, R., Bashir, F., & Chupradit, S. (2021). Impact of credit, liquidity, and systematic risk on financial structure: Comparative investigation from sustainable production. Environmental Science and Pollution Research. https://doi.org/10.1007/s11356-021-17276-x

- Sahar, E., Zulkifli, N., & Zakaria, Z. (2018). A moderated mediation model for board diversity and corporate performance in ASEAN countries. Sustainability, 10(2), 1–20. https://doi.org/10.3390/su10020556

- Samo Asif, H., & Murad, H. (2019). Impact of liquidity and financial leverage on firm’s profitability – An empirical analysis of the textile industry of Pakistan. Research Journal of Textile and Apparel, 23(4), 291–305. https://doi.org/10.1108/RJTA-09-2018-0055

- Suhadak, S., Kurniaty, K., Handayani Siti, R., & Rahayu Sri, M. (2019). Stock return and financial performance as moderation variable in influence of good corporate governance towards corporate value. Asian Journal of Accounting Research, 4(1), 18–34. https://doi.org/10.1108/AJAR-07-2018-0021

- Suhadak, S., Mangesti Rahayu, S., & Handayani Siti, R. (2019). GCG, financial architecture on stock return, financial performance and corporate value. International Journal of Productivity and Performance Management, 69(9), 1813–1831. https://doi.org/10.1108/IJPPM-09-2017-0224

- Swamy, V., & Dharani, M. (2019). Investor attention using the Google search volume index – Impact on stock returns. Review of Behavioral Finance, 11(1), 55–69. https://doi.org/10.1108/RBF-04-2018-0033

- Tashman, P., Marano, V., & Kostova, T. (2019). Walking the walk or talking the talk? Corporate social responsibility decoupling in emerging market multinationals. Journal of International Business Studies, 50(2), 153–171. https://doi.org/10.1057/s41267-018-0171-7

- Tan, L. P., Sadiq, M., Aldeehani, T. M., Ehsanullah, S., Mutira, P., & Vu, H. M. (2021). How COVID-19 induced panic on stock price and green finance markets: Global economic recovery nexus from volatility dynamics. Environmental Science and Pollution Research, https://doi.org/10.1007/s11356-021-17774-y

- Tunyi, A. (2019). Firm size, market conditions and takeover likelihood. Review of Accounting and Finance, 18(3), 483–507. https://doi.org/10.1108/RAF-07-2018-0145

- Wong, K. A. (1989). The firm size effect on stock returns in a developing stock market. Economics Letters, 30(1), 61–65. https://doi.org/10.1016/0165-1765(89)90157-2

- Xiang, H., Ch, P., Nawaz, M. A., Chupradit, S., Fatima, A., & Sadiq, M. (2021). Integration and economic viability of fueling the future with green hydrogen: An integration of its determinants from renewable economics. International Journal of Hydrogen Energy, 46(77), 38145–38162. https://doi.org/10.1016/j.ijhydene.2021.09.067

- Xueying, W., Sadiq, M., Chien, F., Ngo, T. Q., & Nguyen, A. T. (2021). Testing role of green financing on climate change mitigation: Evidences from G7 and E7 countries, https://doi.org/10.1007/s11356-021-15023-w

- Yadav, I. S., Pahi, D., & Goyari, P. (2020). The size and growth of firms: new evidence on law of proportionate effect from Asia. Journal of Asia Business Studies, 14(1), 91–108. https://doi.org/10.1108/JABS-12-2018-0348

- Zhao, L., Zhang, Y., Sadiq, M., Hieu, V. M., & Ngo, T. Q. (2021). Testing green fiscal policies for green investment, innovation and green productivity amid the COVID-19 era. Economic Change and Restructuring. https://doi.org/10.1007/s10644-021-09367-z