?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This article investigates whether the social ties of corporate executives and directors affect short-term return growth during the announcement period of mergers and acquisitions (M&A). We consider both the educational background and employment history of the corporate executives and directors to measure social ties. Specifically, a text analysis algorithm is employed to match employment history. Then, we choose the cumulative abnormal returns to measure the short-term return growth. Using a sample of 157 M&A deals in the Chinese market from 2000 to 2017, we find that acquirer-target social ties have a significantly negative effect on post-merger performance. However, the negative effect of social ties on post-merger firms’ short-term returns will decrease (become less negative) when the firms have good corporate governance mechanisms. Moreover, social ties could also affect the retention of the target firms. The executives and directors are more likely to remain in the post-acquisition firm when the social ties are high. Our results have important implications for policymakers and corporate governance.

1. Introduction

As a resource allocation approach, mergers and acquisitions (M&A) are expected to improve corporate productivity and market share, thus facilitating the implementation of diversification strategy (Andries & Virlan, Citation2017; Yang & Chen, Citation2021). In recent years, the M&A market has been highly active. In 2017, for instance, Chinese M&A transaction volumes were 5,480 (up by 16.45%), with a total transaction value of about $368.07 billion. Although affected by the outbreak of the Novel Coronavirus, 322 M&A cases were recorded in the first quarter of 2020 in China (Staszkiewicz et al., Citation2020). Given the importance of M&A activities, researchers in various disciplines have investigated the factors that have correlations with post-merger performance, including managerial and technological innovation ability (Cui & Leung, Citation2020; Baghdadi et al., Citation2018; Cheng & Yang, Citation2017; Daniliuc et al., Citation2020), CEO tenure and network centrality (El-Khatib et al., Citation2015; Zhou et al., Citation2020), the proportion of the state shares (Changqi & Ningling, Citation2010), corporate social responsibility (Krishnamurti et al., Citation2019), among others.

However, most of the factors in the above studies are extracted from corporate and manager characteristics. Few studies have considered merger and acquisition performance when embedding the enterprise in a social network and focused on the cross-firm connections, especially in a developing economy. Indeed, M&A requires complex decision-making from both firms involved. The interactive nature of the negotiation and decision-making processes makes mergers corporate events where cross-firm social ties are especially relevant. Understanding whether and how such social ties between the acquirer and the target impact decision-making and ultimately affect merger outcomes and shareholder value is, therefore, of particular importance. Also, the concept of Guanxi (as a culture of Chinese interpersonal relationship) plays a crucial role in Chinese society. It is a cultural characteristic that has substantial implications for interpersonal and inter-organisational behaviours in Chinese society. In some cases, it is a primary determinant of successful integration and merger performance. Against this backdrop, it is vital to analyse whether social ties among firms increase M&A return growth in the Chinese market.

This article aims to investigate the effect of cross-firm social ties on post-merger performance, focusing on connections between the two merging firms. Following Ishii and Xuan (Citation2014), we define the relations among directors and executives of acquiring and the target firms as acquirer-target social ties. As the key decision-makers, directors and corporate executives occupy a rich and complex social ties network. These ties can take many forms, including alumni networks from educational institutions, connections through employment activity, or other activities. However, it is difficult to pinpoint the existence or strength of prior social ties between two individuals based on biographies or data sources. Our baseline measure of social ties, therefore, encompasses connections based on both educational background and employment history.

In total, 157 M&A events of A-share listed companies in Shanghai and Shenzhen from 2000 to 2017 are sampled. The cumulative abnormal returns (CAR) are employed to measure short-term M&A return growth. Moreover, we define a matrix consisting of all the directors and executives of the two companies to measure the acquirer-target social ties. Each element of the matrix is a pair of individuals composed of one member from the acquirer and one member from the target. Our finding shows M&A deals with higher social ties are more likely to get lower short-term M&A return growth. However, the negative effect of social ties on post-merger firms’ short-term returns will decrease when the firms have good corporate governance mechanisms. This indicates that corporate governance mechanisms could moderate the relationship between social ties and post-merger performance. Additionally, using two methods to measure the target retention, we find that executives and directors are more likely to remain in the post-acquisition firms when the social ties are high.

The contribution of this study is threefold. First, this article provides a novel influence factor of post-merger performance from the social network perspective and showcases how the connections between acquirer and target affect short-run merger performance. Second, our study is based on the Chinese market, where the Guanxi culture plays an important role in the economic and social activities. Third, our study provides some practical guidance for investment decisions in M&A.

The remainder of the article is structured as follows: Section 2 introduces the theoretical background and research hypotheses. Sections 3 and Section 4 present the methodology and results. Section 5 provides a robust check in which the main variables are measured with other methods. Further discussion is shown in Section 6. Section 7 concludes our study.

2. Theoretical background and hypotheses

Personal connections provide an effective channel for information exchange, allowing the transmission of knowledge, ideas, or private information. These connections can facilitate certain value-creating financial transactions while altering behaviour and even destroying value in other settings (Shanley & Correa, Citation1992; Borlea et al., Citation2017). In the context of M&A, many researchers focus on CEO and board networks’ influence on acquisition performance. For example, El-Khatib et al. (Citation2015) used centrality, structural autonomy, structural equivalence, and density to measure network centrality (Sasaki et al., Citation2020) and studied the effect of CEO network centrality on M&A outcomes. They found that high centrality CEOs use their power and influence to increase entrenchment and reap private benefits. Hence, increasing CEO centrality from the 25th to 75th percentile of the sample decreases acquirer CARs by 3.42 percentage points and total synergies by 3.06 percentage points, on average. In other studies, whereas Cai and Sevilir (Citation2012) found that acquirers earn higher announcement returns when board interlocking connections exist between acquirers and targets in the United States. Renneboog and Zhao (Citation2014) found no such a positive effect in the United Kingdom. Based on Chinese data, Tao et al. (Citation2019) defined firm-level board network centrality and found that greater board network centrality is associated with lower acquirer returns. Besides, Ishii and Xuan (Citation2014) identified connections between board directors and executives in acquiring and target firms. They showed that such connections have negative impacts on post-merger performance. Furthermore, Nguyen et al. (Citation2022) investigated the effect of acquirers’ social capital as reflected through their network position on the level of acquisition premiums and found alliance network social capital provides acquiring firms with information benefits. However, such information benefits are also contingent on target valuation uncertainty and acquirers’ structure exploitation tendency. Given these contrasting findings, this article seeks to provide new evidence on how social ties affect M&A short-term returns, using a sample of Chinese firms.

There are mainly two effect mechanisms about the relation between social connections and post-merger performance. One is that extensive social ties across merging firms foster an enhanced flow of information, leading to better decision-making. According to resource dependence theory, organisations depend on various resources, and the successful procurement of resources is critical. Corporate executives and directors play a crucial role in providing valuable information and strategic advice (Pugliese et al., Citation2014). Well-connected executives and directors of acquiring firms have access to target firms’ valuable information. Therefore, their connections could lower the information asymmetry between two firms and increase the post-merger performance.

An alternative hypothesis is that extensive social connection between an acquirer and a target leads to lower merger performance due to flawed decision-making. First, social ties could lead to a heightened sense of trust. Uzzi (Citation1996) found that social ties can easily bring policymakers closer and promote cooperation. Decision-makers could be more comfortable with one another and shift from a purely exchange-based interaction mode to one based more on trust norms. This trust may cause the acquiring firms to lower due diligence standards or overestimate the merger gains and make acquiring firms ignore better opportunities outside the network, thus lowering the M&A performance. Second, many researchers verify the existence of familiarity bias. That is, individuals prefer status quo choices and familiar goods or people. Dodd et al. (Citation2015) found that investors are more willing to invest in familiar firms. Malmendier et al. (Citation2020) argued that investors have a home bias. In the context of corporate mergers, this familiarity bias can make top managers and directors pay more attention to their familiar targets and neglect better candidates. Third, social ties are only a potential information resource. Whether they can be transformed into information advantages depends on executives and directors. However, many of them are irrational or overconfident, thus leading to the information advantages are not fully used. Finally, the agent problem has always been critical in an enterprise. Conflicts of interest exist between principals (shareholders) and agents (managers and board directors). The acquirer-target connections provide executives and directors with more convenience for seeking individual interests.

Based on the above discussions, we can find that though social ties across merging firms foster an enhanced flow of information, they could affect the decision-maker’s judgements and intensify the agent problem. China has been a ‘relationship-oriented’ society since ancient times. Guanxi is the essential feature of interpersonal relationships (Barbalet, Citation2021; Li et al., Citation2021). The decision-makers are more susceptible to social connections and make inappropriate decisions. Besides, the agent problem can become more prominent in a transitional economy, such as China, due to the weak legal enforcement (Peng & Luo, Citation2000). Therefore, we develop our first hypothesis on the relationship between social ties and merger performance.

Hypothesis 1: The extensive social ties between an acquirer and a target have a negative effect on the abnormal returns to the combined entity upon the merger announcement.

The above analysis has shown that merger performance largely depended on the decision-making of acquiring firms. In essence, corporate governance is a set of mechanisms based on the institution and market to guide a company’s self-interest controller to make decisions that maximise corporate shareholders’ value (Denis & McConnell, Citation2003). Masulis et al. (Citation2007) examined the corporate governance mechanisms on firm acquisitions and found that if the quality of corporate governance is low, the abnormal return is negative. Chae et al. (Citation2009) also found that various corporate governance mechanisms could mitigate agency problems. We argue herein that when the corporate governance of the acquirer is improved, the stockholders will supervise the operator more effectively. Then, the agency conflict will be reduced, and the M&A performance will be improved. Thus, the second hypothesis is as follows.

Hypothesis 2: High-quality corporate governance of the acquiring firms will mitigate social ties’ negative effect on the short-run merger performance.

Krug and Hegarty (Citation1997) found that senior managers’ replacement rate of target firms is higher than acquiring firms after acquisition. Weber and Tarba (Citation2012) pointed out that more than 60% of managers choose to leave the enterprise within five years after acquisition. One possible reason for this is that employees need adapt to the new corporate culture and organisational structure after M&A. However, Agrawal and Walkling (Citation1994) found that most executives of target firms could not find a better new job after leaving office. Under such circumstances, executives and boards will tend to use personal connections to seek retention opportunities. Thus, we put forth the third hypothesis, as follows:

Hypothesis 3: Social ties will increase the retention of the target firm's executives and directors.

3. Research methodology

3.1. Sample selection and data sources

Our data are from the China Stock Market & Accounting Research (CSMAR) database, which belongs to GTA Education Tech Ltd., a leading Chinese financial data provider. We remove unsuccessful trading samples and exclude the samples belonging to the financial industry. If the listed company announces two or more M&A transactions on one day, the target company is the same, accounting and merging it into one deal. We also exclude the samples of two or more M&A transactions announced by the same listed company on the same day, while the targets are different. Besides, we delete these samples in which the distance between two M&As for the same acquiring firm is less than three months. Among the commonly used selection criteria, we filter out samples with a lot of missing data. Our final sample consists of 157 acquisitions in which both the acquirer and the target are Chinese public companies between 2000 and 2017.

3.2. Variable Definition

3.2.1. Short-term M&A return growth (SRG)

Short-term return is a performance measure used to evaluate an investment’s efficiency or compare several different investments’ efficiency. In this article, we focus on the short-term M&A return growth.

We identify the event’s cumulative abnormal returns (CARs) to measure the short-term M&A return growth. For the current study, the event is the acquisition announcement. After identifying the event’s CAR, the results are estimated and statistically analysed to determine the magnitude and direction of the effect of the event on a firm’s performance.

The market model, shown in EquationEquation (1)(1)

(1) , is a well-known one used to estimate CARs.

(1)

(1)

where

is the return of stock i at time t,

is the market return at time t, and

is the random disturbance term. The excess return for each stock can be calculated using formula (2).

(2)

(2)

The cumulative abnormal return in the interval is denoted as:

(3)

(3)

We report CARs for the acquiring firm, the target firm, and the combined entity over the three-day event window (one day before the announcement to one day after the announcement [-1, +1]), the five-day event window ([-2, +2]), and the seven-day event window ([-3, +3]).

3.2.2. Acquirer-target social ties

We construct social ties by focusing on the executives’ and directors’ educational background and employment history. In the CSMAR database, the executives’ and directors’ employment history is shown as a text file. It is very time-consuming to extract the information by hand clearing. Therefore, we first extract employment-related keywords from the text file. Then we use the Levenshtein distance algorithm proposed by Dr. Levenshtein to pairwise match the executives’ and directors’ employment backgrounds. Levenshtein distance is a measure of the similarity between two strings. It calculates least expensive set of insertion, deletion or substitutions that are required to transform one string into another. In this article, we refer to the approach of Putra and Suwardi (Citation2015) to identify two individuals (executives or directors) as sharing a past employment tie if the similarity of their employment background is larger than 0.6. For educational background, we define two individuals as sharing an educational tie if they both obtained degrees from the same school. These could be either undergraduate or graduate degrees. For example, two executives or directors who attended Tsinghua University would be classified as sharing a connection.

The social ties are then defined in the following manner. For each acquisition, there is a relationship matrix constructed by the executives’ and directors’ social ties. Each element of the matrix is a pair of individuals composed of one member from the acquirer and one member from the target. Setting the element equals 1 if the two people have the same educational background or employment history. The social ties are measured by the percentage of 1 in the relation matrix on the matrix’s total elements. For brevity, we label the social ties as ST. Besides, we also construct a dummy variable to describe the connections between two firms. The dummy variable is defined in formula (4) as:

(4)

(4)

3.2.3. Corporate governance quality

A company’s corporate governance is vital to investors since it shows the direction of a company and business integrity. Bargeron et al. (Citation2008) defined the shareholding ratio as the proxy of corporate governance and investigated the relation between corporate governance and M&A performance. Zhang (Citation2014) chose the shareholding ratio of the second to tenth shareholders as the proxy of corporate governance to study the M&A activity. These studies indicate that the shareholding ratio is often treated as the proxy of corporate governance quality.

In hypothesis 1, we argue that the agency problem is one reason for the negative relationship between social ties and merger performance. To gain from M&A, managers might ignore the information advantages brought by social ties and make decisions that go against shareholders. Demsetz and Lehn (Citation1985) found that the high shareholding concentration could help shareholders supervise managers and reduce agency cost. Therefore, this article chooses the shareholding ratio of the top 10 shareholders as the proxy of corporate governance quality which is denoted as CGQ.

3.2.4. Retention rate

We construct two measures for target retention to investigate the relationship between social ties and the target’s retention. The two measures are denoted as follows.

Rete_1= The number of the target's executives and directors retained in the combined firm/Target's pre-acquisition board size;

Rete_2= The number of the target's executives and directors retained in the combined firm/The combined firm's post-acquisition board size.

3.2.5. Control variables

This article controls for the deal characteristics (Ishii & Xuan, Citation2014) and acquiring firms’ characteristics (Ahuja & Katila, Citation2001). The definition and measurement of these variables are shown in .

Table 1. Definition and measurement of control variables.

3.3. Model Specification

Our multivariate analysis model is shown in EquationEquation (5)(5)

(5) . The dependent variable is the three-day cumulative abnormal returns. Our key independent variables are Lock and ST. For robustness, we also control for variables about M&A deal characteristics and acquiring firm characteristics.

(5)

(5)

where CAR is the cumulative abnormal return over the three-day event window, X represents the control variables, and

is the error term which contains other information that might affect CAR. We first test the multicollinearity of the variables. The VIF values of all the variables are smaller than 10, indicating no serious multicollinearity.

To examine how social ties affect target retention, we construct our regression model as follows:

(6)

(6)

where Rete represents the target retention, X represents the control variables, Ability is defined as the average number of firms that the executives and directors work for, and

is the error term. We add the variable Ability in formula (6) to control the effect of executives’ and directors’ ability on their retention.

4. Results

4.1. Descriptive Results

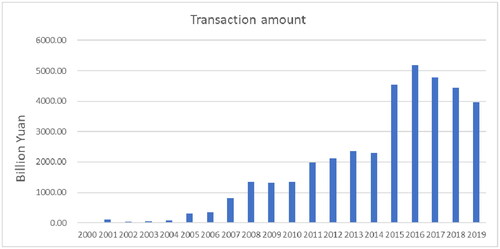

Our final sample consists of 157 acquisitions in which both the acquirer and the target are Chinese public companies. reports the transaction amount from 2000 to 2019 (note: the data are from CVSource: http://www.cvsource.com.cn/). The figure shows an increasing transaction amount with the maximum transaction occurring in 2016.

Figure 1. The transaction amount from 2000 to 2019 in China.

This figure shows the M&A transaction amount from 2000 to 2019 in the Chinese market.

Source: the data is from http://www.cvsource.com.cn/

reports the number of acquisitions categorised by the acquiring firms’ industry. It can be seen that most enterprises belong to the heavy and light industry, accounting for 69.43% of the total sample. Subsamples based on whether the ST is below or above its median indicate that acquisitions in most industries are fairly distributed. The majority of acquisitions in the public utility, business, and comprehensive industries show high social ties. Therefore, in later analysis, we will control the industry fixed effects and year fixed effects.

Table 2. The number of acquisitions.

The summary statistics of CAR are presented in . The acquirer's stock, on average, reacts negatively to the acquisition announcement for the full sample. This adverse reaction is more pronounced when social ties are high. Acquirers with a high social connection experience a negative abnormal return of 2.64% over the seven days around the acquisition announcement. For the combined firms, the CARs are also more negative in the high ST sample. These results suggest that cross-firm social ties are associated with a loss of value to the acquirer's shareholders upon the merger announcement.

Table 3. Summary statistics of CAR.

shows the correlation analysis of major variables. Co_CAR represents the CAR of the combined firms. All the CARs in are calculated over the three-day event window. It can be seen that Co_CAR is negatively related with ST and Lock, namely, the stronger social connections, the lower short-run merger performance. This also preliminarily verified hypothesis 1.

Table 4. Correlation analysis of major variables.

in the Appendix presents the summary statistics and the correlation of control variables used in our article. The mean value of Tran_value is 160.69, indicating the average transaction value of M&A is 160.69 million between 2000 and 2017. Average social ties, our main variable of interest, is 0.12, with a standard deviation of 0.16. Panel B of reports the correlation matrix of the control variables. The main takeaway is that ST does not significantly co-vary with any of the other variables.

4.2. Regression results

This part investigates the impact of social ties on the announcement period abnormal returns. displays the regression results when controlling for the year fixed effects and industry fixed effects. Column 1 and Column 2 focus on acquirer returns. The coefficients on Lock and ST are negative and significant at the 1% level. In Columns 5 and 6, we regress the social ties on combined firm returns. We can see the coefficient of Lock is −1.2285, which is very significant, indicating that compared with M&A events without social ties, M&A events with social relations will lower the performance of the combined firms. Similarly, the negative coefficient of ST in column 4 also suggests that the abnormal return will decrease by about 1.3% when the social ties increase by 1%. This indicates the extensive social connection between an acquirer and a target might lower due diligence standards and make acquiring firms ignore better opportunities outside the network. In Columns 5 and 6, we calculate the effect of ST on targets’ short-term returns. The insignificant coefficients of ST and Lock indicate that social ties will not reduce target firms’ short-term performance.

Table 5. The effect of corporate social ties on M&A performance.

To test hypothesis 2, we add the cross term CGQST in EquationEquation (5)

(5)

(5) . The results are reported in . It can be seen that the cross-term coefficient of ST and CGQ is significantly positive in Column (10). This indicates the good corporate governance of acquiring firms could improve the detracting effect of social ties on post-merger performance. In terms of economic significance, the negative coefficient of ST in column (10) suggests that the abnormal return will decrease by about 1.4978% when the social ties increase by 1% and the acquiring firms have poor corporate governance. In contrast, the abnormal return of the combined firms will lower 1.4927% when the acquiring firms have good corporate governance. Furthermore, the coefficients of CGQ in columns 9 and 10 are also positive, consistent with the conclusions of Masulis et al. (Citation2007) and Thraya et al. (Citation2019). However, they are not significant, indicating that CGQ could not significantly improve the short-run merger performance.

Table 6. Regression results under different corporate governance environments.

reports the relations between social ties and target retention. Across all measures and specifications, the degree of social connection between the acquirer and the target is positively correlated with target board retention after the merger. The effect remains strong after we control for year fixed effects, industry fixed effects, and managers’ ability. For example, based on the regression results in column 14, the ST coefficient is 0.0759, which is significant at 1%.

Table 7. The effect of corporate social ties on the target retention.

5. Robustness analysis

5.1. Changing the event window

We first change the event window and choose CAR[-2, +2] and CAR[-3, +3] as dependent variables to test the hypothesis. The empirical results are reported in . In Columns 3 and 4, the coefficients of ST are significantly negative at 5% level. This suggests that the abnormal returns will decrease by about 1.9% and 2.63%, respectively, when the social ties increase by 1%. The relevant conclusions remain robust when changing the event window.

Table 8. The effect of corporate social ties on the M&A performance.

5.2. Alternative measure of corporate governance quality

Referring to Bizjak et al. (Citation2009), we use the shareholding ratio of executives to measure corporate governance quality. The results in are consistent with our previous evidence.

Table 9. The moderating effect of corporate governance.

6. Discussion

Social ties have been demonstrated to have an impact on various economic activities. This article builds on and contributes to two main strands of literature. First, it is related to a growing literature on the role of social ties and networks on the influence of managers’ corporate decisions. Several studies have investigated the impact of directors' networks (or the connections between CEO and directors) on corporate decisions (Zhou et al., Citation2020; Ishii & Xuan, Citation2014; Hwang & Kim, Citation2009). However, few studies investigate the effect of cross-firm connections on corporate decisions and outcomes, especially in the Chinese market. We focus on whether the connections of acquirer-target executives and directors affect short-run merger performance. Second, this article is related to the M&A literature. Prior research has evaluated the influence of deal characteristics and firm characteristics on merger performance (Travlos, Citation1987; Cui & Leung, Citation2020; Baghdadi et al., Citation2018; Servaes, Citation1991). What has been less explored is the social ties and their effect on post-merger performance.

This article sets out to address three questions. The first question concerns the effect of social ties on short-term merger returns. The second question deals with the moderating effect of the corporate governance environment on the relationship between social ties and merger performance. The third research question is on whether social ties increase target retention?

Our results present a significantly negative relation between social ties and post-merger performance, suggesting that the decision-making associated with social connections could lead to undesirable effects. Tight social ties across firms lead the acquiring firms’ decision-makers to lower due diligence standards for the target firms because of trust or familiarity bias. The existence of principal-agent problem also urges managers to seek benefits for themselves through social ties. Thus, high social connections will negatively affect merger performance. However, when improving the corporate governance mechanisms of the acquiring firms, we find the negative relation is mitigated, indicating that improving corporate governance quality is an effective way to help acquiring firms find appropriate target firms and supervise managers’ and directors’ behaviour. Moreover, we also find that social ties are positively related to the retention of the target firms, suggesting that executives and directors are more likely to remain in the post-acquisition firms when the social ties are high.

The limitations of this study are as follows. First, due to data availability, it is challenging to find appropriate instrumental variables to measure social ties. Thus, caution in the interpretation is warranted, because of the lacking of an endogeneity test. Second, the matching algorithm (Levenshtein distance algorithm) used in our article is a little bit time-consuming. With the development of machine learning, it will be necessary to explore more time-saving methods in the future research. Third, this study only focuses on the short-term return growth. The long-term merger return is also well worth analysing.

7. Conclusions

In this study, we embed the enterprise in a social network and focus on the effect of social ties across firms on post-merger performance in the Chinese market. Using a sample of 157 merger events drawn from the CSMAR database, we test the relation between cross-firm ties and short-term M&A returns. The social ties between two merging firms are measured based on the educational background and employment history of executives and directors. Our results show that more extensive social connections between an acquirer and a target have a negative effect on the merger performance. For every 1% increase in the corporate social ties, the cumulative abnormal returns of post-merger firms will decrease by about 1.3% (Hypothesis 1 is proved). The results are still robust when controlling for Q, leverage, cash flow, relative size, and transaction values. Moreover, the negative effect of social ties on merger performance will be alleviated when the acquirer has a higher governance environment (Hypothesis 2 is confirmed). Besides, our results also indicate that acquirer-target social ties significantly increase the target board retention after the merger, which offers evidence to confirm Hypothesis 3.

Our main findings have important implications for policymakers in China and other economies. Our evidence on the negative relation between social ties and acquisition performance implies that policymakers and managers should pay more attention to the relationships between executives and directors coming from the acquirer and the target. The social relationships could affect the filtering standards for target firms and further affect post-merger performance during M&A. Policymakers should also design more transparent evaluation processes and improve corporate governance mechanisms to weaken the familiarity bias and agent problem when choosing target firms.

We identify several areas for further research. First, in this study, we only use the educational background and employment history to measure social ties. However, there are many other forms of connections between executives and directors. Future studies could focus on whether two executives/directors work in the same office building or love the same sports. Second, this study only focuses on the moderating effect of corporate governance environments. Future studies could discuss other moderator variables, such as media spotlight, corporate social responsibility, and economic policy uncertainty. Third, this study only considers the short-term return growth. The influencing mechanisms of social ties on long-term merger performance may be different.

Acknowledgements

All authors thank the anonymous reviewers and editors for their helpful comments on the revision of this article.

Disclosure statement

The authors report no potential conflict of interest.

References

- Agrawal, A., & Walkling, R. A. (1994). Executive careers and compensation surrounding takeover bids. The Journal of Finance, 49(3), 985–1014. https://doi.org/10.1111/j.1540-6261.1994.tb00085.x

- Ahuja, G., & Katila, R. (2001). Technological acquisitions and the innovation performance of acquiring firms: A longitudinal study. Strategic Management Journal, 22(3), 197–220. https://doi.org/10.1002/smj.157

- Andries, A. M., & Virlan, C. A. (2017). Risk arbitrage in emerging Europe: Are cross-border mergers and acquisition deals more risky. Economic Research-Ekonomska Istraživanja, 30, 1, 1367–1389. https://doi.org/10.1080/1331677x.2017.1355259

- Baghdadi, G. A., Bhatti, I., Nguyen, L. H., & Podolski, E. J. (2018). Skill or effort? Institutional ownership and managerial efficiency. Journal of Banking & Finance, 91(6), 19–33. https://doi.org/10.1016/j.jbankfin.2018.04.002

- Barbalet, J. (2021). Where does Guanxi come from? Bao, Shu, and Renqing in Chinese connections. Asian Journal of Social Science, 49(1), 31–37. https://doi.org/10.1016/j.ajss.2020.11.001

- Bargeron, L. L., Schlingemann, F. P., Stulz, R. M., & Zutter, C. J. (2008). Why do private acquirers pay so little compared to public acquirers. Journal of Financial Economics, 89(3), 375–390. https://doi.org/10.1016/j.jfineco.2007.11.005

- Bizjak, J. M., Lemmon, M. L., & Whitby, R. J. (2009). Option backdating and board interlocks. Review of Financial Studies, 22(11), 4821–4847. https://doi.org/10.1093/rfs/hhn120

- Borlea, S. N., Achim, M. V., & Mare, C. (2017). Board characteristics and firm performances in emerging economies lessons from Romania. Economic Research-Ekonomska Istraživanja, 30(1), 55–75. https://doi.org/10.1080/1331677X.2017.1291359

- Cai, Y., & Sevilir, M. (2012). Board connections and M&A transactions. Journal of Financial Economics, 103(2), 327–349. https://doi.org/10.1016/j.jfineco.2011.05.017

- Chae, J., Kim, S., & Lee, E. J. (2009). How corporate governance affects payout policy under agency problems and external financing constraints. Journal of Banking & Finance, 33(11), 2093–2101. https://doi.org/10.1016/j.jbankfin.2009.05.003

- Changqi, W., & Ningling, X. (2010). Determinants of cross-border merger & acquisition performance of Chinese enterprises. Procedia - Social and Behavioral Sciences, 2(5), 6896–6905. https://doi.org/10.1016/j.sbspro.2010.05.040

- Cheng, C., & Yang, M. (2017). Enhancing performance of cross-border mergers and acquisitions in developed markets: The role of business ties and technological innovation capability. Journal of Business Research, 81, 107–117. https://doi.org/10.1016/j.jbusres.2017.08.019

- Cui, H., & Leung, S. (2020). The long-run performance of acquiring firms in mergers and acquisitions: Does managerial ability matter? Journal of Contemporary Accounting & Economics, 16(1), 100185. https://doi.org/10.1016/j.jcae.2020.100185

- Daniliuc, S. O., Li, L., & Wee, M. (2020). Busy directors and firm performance: Evidence from Australian mergers. Pacific-Basin Finance Journal, 64, 101434. https://doi.org/10.1016/j.pacfin.2020.101434

- Denis, D. K., & McConnell, J. J. (2003). International corporate governance. The Journal of Financial and Quantitative Analysis, 38(1), 1–36. https://doi.org/10.2307/4126762

- Dodd, O., Frijns, B., & Gilbert, A. (2015). On the role of cultural distance in the decision to cross-list. European Financial Management, 21(4), 706–741. https://doi.org/10.1111/j.1468-036X.2013.12038.x

- El-Khatib, R., Fogel, K., & Jandik, T. (2015). CEO network centrality and merger performance. Journal of Financial Economics, 116(2), 349–382. https://doi.org/10.1016/j.jfineco.2015.01.001

- Hwang, B., & Kim, S. (2009). It pays to have friends. Journal of Financial Economics, 93(1), 138–158. https://doi.org/10.1016/j.jfineco.2008.07.005

- Ishii, J., & Xuan, Y. (2014). Acquirer-target social ties and merger outcomes. Journal of Financial Economics, 112(3), 344–363. https://doi.org/10.1016/j.jfineco.2014.02.007

- Krishnamurti, C., Shams, S., Pensiero, D., & Velayutham, E. (2019). Socially responsible firms and mergers and acquisitions performance: Australian evidence. Pacific-Basin Finance Journal, 57, 101193. https://doi.org/10.1016/j.pacfin.2019.101193

- Krug, J. A., & Hegarty, W. H. (1997). Post-acquisition turnover among U.S. top management teams: An analysis of the effects of foreign vs. domestic acquisitions of U.S. targets. Strategic Management Journal, 18(8), 667–675. https://doi.org/10.1002/(sici)1097-0266(199709)18:8<667::aid-smj918>3.0.co;2-e

- Demsetz, H., & Lehn, K. (1985). The structure of corporate ownership: Causes and consequences Kenneth Lehn. Journal of Political Economy, 93(6), 1155–1177. https://doi.org/10.1086/261354

- Li, Y., Tian, G. G., & Wang, X. (2021). The effect of Guanxi culture on the voting of independent directors: Evidence from China. Pacific-Basin Finance Journal, 67(5), 101524. https://doi.org/10.1016/j.pacfin.2021.101524

- Malmendier, U., Pouzo, D., & Vanasco, V. (2020). Investor experiences and international capital flows. Journal of International Economics, 124, 103302. https://doi.org/10.1016/j.jinteco.2020.103302

- Masulis, R. W., Wang, C., & Xie, F. (2007). Corporate governance and acquirer returns. The Journal of Finance, 62(4), 1851–1889. https://doi.org/10.1111/j.1540-6261.2007.01259.x

- Nguyen, H. W., Zhu, Z., Jung, Y. H., & Kim, D. S. (2022). Determinants of M&A acquisition premium: A social capital perspective. Competitiveness Review: An International Business Journal, 32(2), 214–229. https://doi.org/10.1108/CR-05-2020-0074

- Peng, M. W., & Luo, Y. (2000). Managerial ties and firm performance in a transition economy: The nature of a micro-macro link. Academy of Management Journal, 43(3), 486–501. https://doi.org/10.5465/1556406

- Pugliese, A., Minichilli, A., & Zattoni, A. (2014). Integrating agency and resource dependence theory: Firm profitability, industry regulation, and board task performance. Journal of Business Research, 67(6), 1189–1200. https://doi.org/10.1016/j.jbusres.2013.05.003

- Putra, M. E., & Suwardi, I. S. (2015). Structural off-line handwriting character recognition using approximate subgraph matching and Levenshtein distance. Procedia Computer Science, 59, 340–349. https://doi.org/10.1016/j.procs.2015.07.529

- Renneboog, L., & Zhao, Y. (2014). Director networks and takeovers. Journal of Corporate Finance, 28, 218–234. https://doi.org/10.1016/j.jcorpfin.2013.11.012

- Sasaki, H., Fugetsu, B., & Sakata, I. (2020). Emerging scientific field detection using citation networks and topic models—A case study of the nanocarbon field. Applied System Innovation, 3(3), 40. https://doi.org/10.3390/asi3030040

- Servaes, H. (1991). Tobin's Q and the gains from takeovers. Journal of Finance, 46(1), 409–419. https://doi.org/10.1111/j.1540-6261.1991.tb03758.x

- Shanley, M. T., & Correa, M. E. (1992). Agreement between top Management teams and expectations for post acquisition performance. Strategic Management Journal, 13(4), 245–266. https://doi.org/10.1002/smj.4250130402

- Staszkiewicz, P., Chomiak-Orsa, I., & Staszkiewicz, I. (2020). Dynamics of the COVID-19 contagion and mortality: Country factors, social media, and market response evidence from a global panel analysis. IEEE Access, 8, 106009–106022. https://doi.org/10.1109/ACCESS.2020.2999614

- Tao, Q., Li, H., Wu, Q., Zhang, T., & Zhu, Y. (2019). The dark side of board network centrality: Evidence from merger performance. Journal of Business Research, 104(104), 215–232. https://doi.org/10.1016/j.jbusres.2019.07.019

- Travlos, N. G. (1987). Corporate takeover bids, methods of payment, and bidding firms' stock returns. The Journal of Finance, 42(4), 943–963. https://doi.org/10.1111/j.1540-6261.1987.tb03921.x

- Thraya, M. F., Lichy, J., Louizi, A., & Rzem, M. (2019). High-tech acquirers and the moderating role of corporate governance. The Journal of High Technology Management Research, 30(2), 100354. https://doi.org/10.1016/j.hitech.2019.100354

- Uzzi, B. (1996). The sources and consequences of embeddedness for the economic performance of organizations: The network effect. American Sociological Review, 61(4), 674–698. https://doi.org/10.2307/2096399

- Weber, Y., & Tarba, S. Y. (2012). Mergers and acquisitions process: The use of corporate culture analysis. Cross Cultural Management: An International Journal, 19(3), 288–303. https://doi.org/10.1108/13527601211247053

- Yang, S., & Chen, S. (2021). Market reactions for targets of M&A rumours-evidence from China. Economic Research-Ekonomska Istraživanja, 34(1), 2956–2974. https://doi.org/10.1080/1331677X.2020.1865826

- Zhang, Z. (2014). Internal financing capability, corporate governance quality and M&A performance. Research on Financial and Economic Issues, (6), 51–56.

- Zhou, B., Dutta, S., & Zhu, P. (2020). CEO tenure and mergers and acquisitions. Finance Research Letters, 34, 101277. https://doi.org/10.1016/j.frl.2019.08.025

Appendix A

Table A1. Summary statistics of the control variables.