?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Whether the intellectual property protection (IPP) system can improve the financing environment for enterprise innovation is a poorly studied research issue. Taking the Chinese ‘three-in-one trial’ reform of intellectual property rights (IPRs) as a quasi-natural experiment; we investigate the impact of strengthening IPP on trade credit financing of high-tech enterprises. The results show that strengthening IPP can promote their trade credit by about 2%, and the technology market effect, innovation effect and information effect are the underlying mechanisms. Further tests indicate that the promotion effects of IPP are more obvious on high-tech enterprises with lower government support, lower proportion of fixed assets and healthier government–business relationship. Different from the previous literature, which focuses on the relationship between IPP and innovation activities or benefits, this article expands the literature by investigating its impact on innovation financing and fills the research gap of the impact of IPP on capital market information searching.

1. Introduction

The IPP is an effective system to ensure enterprise innovation and its income. The research on the effect of the IPP system mainly focuses on evaluating its efficiency to promote innovation activities (Allred & Park, Citation2007; Chen & Puttitanun, Citation2005; Sweet & Maggio, Citation2015) or to protect innovation benefits (Claessens & Laeven, Citation2003; Chen et al., Citation2012). However, there is little literature to answer whether better IPP can improve the financing environment of enterprise innovation. The high-tech enterprise is the key object of the IPP system and the dominant force for enhancing national technological innovation. Due to the positive externality and information asymmetry of innovation activities (Arrow, Citation1962; Howell, Citation2017), they are facing stronger financing constraints. We will evaluate the impact of strengthening IPP on financing of high-tech enterprises from the perspective of trade credit.

Previous studies have shown that innovation achievements can send a positive signal to creditors and help high-tech enterprises reduce information asymmetry, which thus alleviate financing constraints (Hall et al., Citation2005; Francis et al., Citation2012; Hoffmann et al., Citation2019; Hoffmann & Kleimeier, Citation2021). Scholars believe that better IPP makes enterprises be motivated to disclose more innovation information to obtain more financing (Ang et al., Citation2014), while excessive disclosure of R&D information may enable competitors to obtain valuable technical knowledge and thus aggravate the competitive environment (Hall et al., Citation2014). However, this debate only focuses on the motivation of enterprises to actively disclose information, ignoring strengthening IPP may cause the capital market to actively search for innovation information, which maybe the reason why less literature studies the association of IPP and corporate financing.

However, previous studies only focus on the quality of information disclosure of enterprises, ignoring the information searching ability of capital market, which may be the reason why less literature studies the association of IPP and corporate financing. The existing literature usually uses the scores of intellectual property legal texts (like RR index) or intellectual property legislative reform to measure the IPP level (Allred & Park, Citation2007; Lerner, Citation2002; Branstetter et al., Citation2006; Qian, Citation2007; Branstetter et al., Citation2011; Alimov & Officer, Citation2017). However, these two methods only consider the level of legislation but not law enforcement, leading to an overestimation for IPP in countries with the low law enforcement level. On the other hand, the existing literature pays more attention to developed countries, which have established relatively perfect IPP systems so that their protection levels change less with time. Thus, it is difficult to identify the impact of exogenous strengthening of IPP.

China implemented the ‘three-in-one trial’ reform for the intellectual property cases in 2009, which provides a feasible perspective for identifying the exogenous strengthening of IPP. We thus take this reform of IPRs as a quasi-natural experiment and use time-varying DID method to empirically evaluate the impact of strengthening IPP on high-tech enterprises' financing. Due to the lack of collateral for high-tech enterprises in China, they face more restricted bank loans (Guiso, Citation1998) and turn to use more trade credit financing. Therefore, we pay more attention to the impact of the ‘three-in-one trial’ reform on the trade credit financing of high-tech enterprises. We find that strengthening IPP can promote their trade credit financing, especially notes payable. In addition, the promotion effects of IPP are more obvious on high-tech enterprises with lower government support, lower proportion of fixed assets and healthier government–business relationship.

We further use the mediation effect model to test the mechanisms underlying. First, IPP can help to enhance technology market transactions and improve the mortgageability of innovation achievements. Second, the strengthening of IPP can promote the innovation output of enterprises, and thus strengthen the invest willingness of trade creditors, which is consistent with the existing studies. Third, we find that strengthening IPP cannot encourage enterprises to disclose more information but can encourage the capital market to search information, which thereby alleviates information asymmetry.

We contribute to the literature in several ways. First, we expand the IPP literature IPP by introducing an important external financing channel for the high-tech enterprise. Our results prove that better IPP is very important to enterprise' innovation financing. Ang et al. (Citation2014) and Alimov (Citation2019) also prove that IPP is conducive to enterprises to obtain bank loans. However, many high-tech enterprises in developing countries lack collateral for credit financing (Guiso, Citation1998). Therefore, the relationship between IPP and trade credit financing is more meaningful to high-tech enterprises. Unfortunately, there lack the research on the relationship between IPP and trade credit financing of high-tech enterprises. Thus, our research enriches the research on IPP and enterprise financing.

Second, this article distinguishes and compares the enterprises' active information disclosure and capital market information searching, which provides a new perspective for the studies of information asymmetry theory in corporate financing. Existing studies argue that enterprises are reluctant to disclose information because they are worried about the threat from competitors. Strengthening IPP can enhance the willingness of enterprises to actively disclose information (Hall, Citation2002; Brown et al., Citation2009; Ang et al., Citation2014). Our results reveal that the strengthening of IPP does not promote the information disclosure of high-tech enterprises but enhance the investors' willingness to search information, which passively alleviates the information asymmetry.

Third, this article provides a new idea to solve the endogenous problem in the research of IPP. Based on the Chinese ‘three-in-one trial’ reform of IPRs, this article innovatively captures the exogenous changes for IPP, and alleviates the endogenous problem. Although Ang et al. (Citation2014) constructed two provincial indicators reflecting the level of IPP in China, one based on the winning rate of plaintiffs in provincial courts and the other based on the frequency of mentioning intellectual property in provincial official newspapers. However, the former ignores the existence of malicious litigation; while the latter may be biased by the fact that official newspapers may refer to intellectual property very frequently or their varied publicity preferences.

We proceed as follows: Section 2 develops the hypotheses. Section 3 introduces the institutional background and our methodology. Section 4 reports and discusses the baseline results. Section 5 further investigates this research issue and Section 6 concludes this article.

2. Theoretical analysis and hypotheses

The development and rational use of intellectual property in a country is often closely related to economic development (Bryhinets et al., Citation2021). Stronger IPP enables intellectual property holders to maintain stronger market dominance, reduces creditors' concerns about the ability of enterprises to monetise intellectual property through licensing and improves market expectation that intellectual property will bring more stable profits to enterprises (Liu & Wong, Citation2011). Although due to the concerns about the intangibility and reusability, the intellectual property asset is often regarded as non-performing collateral (Hall & Lerner, Citation2010). However, with the advent of the innovation-driven era, the economic value of intellectual property has gradually become prominent, making it more and more widely used in the capital market as collateral (Mann, Citation2018). In case of default, creditors can sell intellectual property collateral in the capital market to partially compensate for the loss (Hart & Moore, Citation1994). Therefore, strengthening IPP can improve the liquidity and reusability of intellectual property, create stronger security interests and thus promote the supply of trade credit financing.

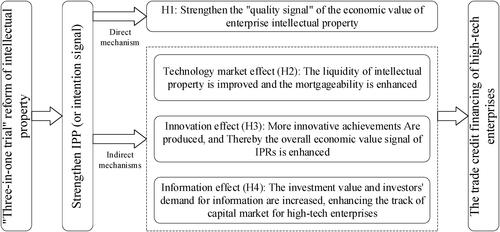

In addition to the above traditional theoretical interpretation framework, we also try to use the signal theory proposed by Spence (Citation1973) to explore the relationship between IPP and trade credit financing. This theory divides signals into quality signals and intention ones according to the transmission content. The quality signal refers to the transformation of capabilities and characteristics that are not easy to observe directly within an organisation into externally observable signals, and the intention signal indicates the direction or intention of the organisation’s behaviour (Stiglitz, Citation2000). On the one hand, because it is difficult for trade creditors to observe the real situation inside one enterprise, there is information asymmetry between them. In a good environment of IPP, the value conversion ability of high-tech enterprises' innovative achievements is improved, making their profits directly be improved due to the stable income stream generated through patent transfer and patent licensing (Liu & Wong, Citation2011). The positive ‘quality signal’ to enhance the value and competitiveness of enterprises makes the impact of innovation achievements on trade credit financing more significant. On the contrary, when the intensity of IPP is weak, the probability of intellectual property infringement increases, leading to the increase in the uncertainty of R&D projects. Especially for high-tech enterprises, due to the lack of high-quality ‘alternative signals’ such as fixed assets, their innovation outputs are the main ‘quality signals’ reflecting their future profitability, while the quality of this signal depends on the IPP level. Even if high-tech enterprises have many high-quality innovation achievements, the potential value will be reduced due to infringement risk. The trade creditors may tend to underestimate the value of high-tech enterprises and overestimate their risk of breach of contract, thus reducing the supply of trade credit financing. On the other hand, the policies and measures of the government or the judiciary are also a kind of signal. For example, the court's publication of the performance data of IPP such as the closing rate and winning rate can be understood as a ‘quality signal’, reflecting the change in the level of IPP, while patent law reform and law enforcement reform are intention signals, showing the government's intention to strengthen IPP. The ‘three-in-one trial’ reform releases the intention signal of strengthening IPP, which in turn strengthens the quality signal of the economic value of intellectual property owned by high-tech enterprises, thus promoting their trade credit financing. Based on this, we put forward the following hypothesis:

H1: IPP can promote the trade credit financing of high-tech enterprises.

Figure 1. Theoretical framework and mechanisms.

First, the developed technology trading market reduces the company's motivation to retain all knowledge internally (Arora et al., Citation2002) and has become an important channel for enterprises to absorb external knowledge. More importantly, the economic value of intellectual property assets largely depends on their tradability. The prosperity of technology trading market can improve the convenience of intellectual property transactions (Arora et al., Citation2008). The circulation and reusability of intellectual property can be improved through licensing and sales, which enhances the ability of intellectual property as collateral for guaranteed debt. Moreover, the technology trading market also alleviates the difficulty in the valuation of intellectual property as intangible assets, making it easier for creditors to accept intellectual property as collateral (Alimov, Citation2019). However, the externality of technology leads to market failure in the technology market (Gambardella, Citation2002). The activity of technology trading is inseparable from good IPP. IPP helps to create and maintain a good technology trading environment, which is more conducive to creditors to realise intellectual property in the technology market. So, better IPP can reduce the risk of creditors and make it easier for high-tech enterprises to obtain trade credit financing through technology market effect.

Second, the supply intention of trade creditors mainly comes from the trade-off between enterprise risk and income. Innovation achievements are the main value source of high-tech enterprises. The stronger the innovation ability of high-tech enterprises, the greater the knowledge spillover and feedback that suppliers and customers benefit from along the supply chain (Zhang et al., Citation2021). Therefore, as trade credit providers, suppliers and customers are more willing to allocate resources to high-tech enterprises with stronger innovation ability to establish a good relationship with them. Strengthening the protection of IPRs can reduce the negative externality of innovation achievements (Arrow, Citation1962), increase the profitability, and therefore encourage high-tech enterprises to improve innovation and obtain more trade credit financing. Thus, IPP can promote the innovations of high-tech enterprises by producing innovation effect and thereby enhance their trade credit financing.

Third, the information related to R&D projects does not belong to compulsory disclosure. Disclosing too much R&D information may enable competitors to obtain valuable technical knowledge (Hall et al., Citation2014). To ensure the safety of innovation information, the managers of high-tech enterprises tend to hide R&D information inside the enterprise. Valuable R&D information is usually excluded from the accounting statements, which aggravates the internal and external information asymmetry of high-tech enterprises. Suppliers and customers cannot know the real innovation status of enterprises, it is difficult to accurately evaluate their progress and future expected benefits. Thus, suppliers and customers will be more cautious in providing trade credit (Anton & Yao, Citation2002; Ueda, Citation2004). When the level of IPP is improved, the infringement of intellectual property is restrained, which encourages high-tech enterprises to disclose more R&D information and thus reduce the internal and external information asymmetry (Hall, Citation2002; Brown et al., Citation2009; Ang et al., Citation2014). Therefore, suppliers and customers can more accurately evaluate the operation status and credit degree of high-tech enterprises. In addition, the strengthening of IPP is good news for high-tech enterprises, because the market's motivation to pay attention to them will also increase. As the external supervisors of enterprises, the increase in market analysts' attention to enterprises is conducive to improving the accuracy of information analysis and alleviating the information asymmetry. Therefore, the strengthening of IPP may also alleviate the information asymmetry by producing information effect, which is helpful for the trade creditors to accurately evaluate the value of high-tech enterprises and thereby increase the trade credit financing. Based on the above analysis, this article puts forward the following research hypotheses:

H2: IPP can promote high-tech enterprises' trade credit financing through technology market effect.

H3: IPP can promote high-tech enterprises' trade credit financing through innovation effect.

H4: IPP can promote high-tech enterprises' trade credit financing through information effect.

3. Institutional background and research design

3.1. Institutional Background

For a long time, the traditional judicial structure arrangement of intellectual property cases in China are ‘separation of three trials’, i.e., the criminal, civil, and administrative cases related to intellectual property are separately tried by corresponding courts. With the development of economy and society, the malpractice of this model, such as the conflict of jurisdiction, the disconnection of trial procedures, and the disunity of trial standards, has gradually emerged. The outline of the Chinese National Intellectual Property Strategy issued on 2008 clearly requires the establishing of a specialised intellectual property institutions that can handle civil, administrative, and criminal cases of IPRs together. Compared with the traditional trial mode of ‘separation of three trials’, and the ‘three-in-one trial’, has its significant advantages. First, the implementation of ‘three-in-one trial’ can effectively integrate trial resources, improve the professional level of judges and ensure the quality of trial. Second, it helps to ensure the uniform judicial standard of intellectual property cases, which is helpful for effectively solving the problem of different judgments in the same court and form a more effective and comprehensive mechanism of IPRs. Third, it can give full play to the role of IPP and protect the economic interests of the obligee. Since 2009, the number of cities implementing the ‘three-in-one trial’ reform has increased year by year. By the end of 2018, 17 Higher People's Courts, 113 intermediate People's Courts and 129 grassroots People's Courts have implemented the ‘three-in-one trial’ reform. This kind of Chinese reform also provides a good perspective for the study of the impact of IPP on social and economic development.

3.2. Data Sources and sample description

This article uses the Chinese ‘three-in-one trial’ reform staggered implemented in time and space by intermediate people's courts as a quasi-natural experiment to measure the change in regional IPP. Our sample is the Chinese high-tech manufacturing companies listed on Shanghai and Shenzhen A-share market from 2009 to 2018. We matched the enterprise data with the ‘three-in-one trial’ reform data by the location cities of enterprise headquarters. According to the Classification of High-tech Industries (Manufacturing Industry) issued by the National Bureau of Statistics in 2017, six high-tech manufacturing industries are selected, including (1) pharmaceutical manufacturing, (2) aviation, spacecraft and equipment manufacturing, (3) electronic and communication equipment manufacturing, (4) computer and office equipment manufacturing, (5) medical equipment and instrumentation manufacturing, and (6) information technology products manufacturing.

The data of related industries and enterprises come from China Stock Market & Accounting Research (CSMAR) database. By searching the official websites of the Intermediate People's Courts, statistical yearbooks and telephone inquiry, we manually collate the data of ‘three-in-one trial’ reform. The patent enforcement data come from the State Intellectual Property Office of China website, while the other city-level data comes from the corresponding city statistical yearbooks. In addition, we process the sample as follows: (1) eliminating the enterprises in cities that have implemented the ‘three-in-one trial’ reform before 2009; (2) excluding the enterprises located in the municipalities directly under the central government; (3) eliminating the non-going concern enterprises during the sample period; (4) eliminating the ST (special treatment) enterprises; (5) excluding the observations with missing values. The final sample contains 2999 firm-year observations, which involves 355 enterprises in 113 cities. In our samples, 38 cities have implemented the ‘three-in-one trial’ reform.

3.3. Model, variables, and descriptive statistics

To identify the influence of the implementation of the ‘three-in-one trial’ reform on the trade credit financing of high-tech enterprises, referring to Autor (Citation2003) and Beck et al. (Citation2010), we construct the following time-varying DID model to do empirical estimations.

(1)

(1)

where i, h, p and t represent the enterprise, industry, province, and year, respectively. According to Mateut (Citation2014), the explained variable

denotes trade credit financing, which is measured by the sum of advance receipts, accounts payable and notes payable divided by the firm assets. The explanatory variable

represents the change in IPP of city

in year

is a dummy variable, which equals 1 if the city

implemented ‘three-in-one trial’ reform in year

otherwise, 0. The coefficient

captures the impact of IPP on trade credit financing of high-tech enterprises. If

is significantly positive, it indicates that there exists a promoting effect.

denotes control variables. Refer to previous studies like Xiang et al. (Citation2021), Chen et al. (Citation2021), and Hoffmann and Kleimeier (Citation2021), control variables include short-term firm bank loans, return on assets, liquidity, growth, size, ability to generate cash, age, state ownership, CEO duality, ten most extensive shareholders ownership, and city-level GDP growth rate. To alleviate the endogeneity bias, all control variables lag for one period. We also control industry (

), year (

), and province × year (

) fixed effect. To avoid the influence of extreme values on our results, all continuous variables are winsorised at 1% in both tails. To control the potential heteroscedasticity and sequence correlation problems, standard errors are clustered at the enterprise level.

3.4. Descriptive Statistics

shows the definitions of variables. reports the descriptive statistical results for the main variables. The minimum, maximum, and average values of variable are 0.015, 0.574, and 0.183, respectively, which indicates that the least, most, and average proportion of trade credit financing in firm assets is 1.5%, 57.4%, and 18.3%, correspondingly. The trade credit financing obtained by enterprises varies a lot. The minimum, maximum, and average values of

variable are 0.096, 0.496, and 0.123, respectively, which indicates that the short-term bank loan of enterprises varies a lot.

Table 1. Descriptive statistics.

4. Baseline results and discussions

4.1. Baseline results

reports baseline results evaluating by the time-varying DID model. We find that the coefficients are always significantly positive no matter whether fixed effect and other control variables are included, which indicates that the implementation of the ‘three-in-one trial’ reform associates a 2% incremental on the trade credit financing of high-tech enterprises. The above results support the view that strengthening IPP can improve the trade credit financing of high-tech enterprises. In a higher IPP city, the high-tech enterprises that lack fixed assets can generate a stable income flow through patent transfer or patent licensing, which can directly improve firm profits, enhance the positive ‘quality signal’ of their value and competitiveness, and bring them more supply of trade credit. Our conclusions are consistent with Alimov (Citation2019), which proved that IPP significantly reduced the bank loan cost of high-tech enterprises in 48 countries. However, this article only focused the impact on bank loans and did not distinguish the differences between developing and developed countries. Ang et al. (Citation2014) focused on the developing country data and found that the effective enforcement of IPRs is helpful to promote the debt financing of high-tech companies, while also fail to investigate the influence on trade credit financing.

Table 2. IPP and trade credit financing.

4.2. Robustness tests

4.2.1. Parallel trend and dynamic effect test

To test whether our samples meet the parallel trend hypothesis, refer to Gopalan et al. (Citation2016), we replace the IPP variable with the year dummy variables, i.e., Before4+, before3, before2, before1, which represent four or more years, three years, two years and one year before the implementation of the reform, respectively, Post, which represents the year of the implementation of the reform, and Post1, Post2, Post3, Post4, Post5+, which represent one year, two years, three years, four years and five or more years after the implementation of the reform, respectively. We report the results in . The coefficients of Before4+, before3, before2, and before1 are not significant, while the coefficients of Post, Post1, Post2, Post3, Post4, and Post5+ are significantly positive. The above results indicate that our sample meets the parallel trend assumption, which supports the DID method results.

(2)

(2)

Table 3. Parallel trend and dynamic effect test.

4.2.2. PSM-DID

To reduce the bias of sample selection, we further use the PSM method to match the experimental group and the control group and construct a new ‘three-in-one trial’ reform dummy variable. According to Heyman et al. (Citation2007), finding the matched control group for the experimental group is by using a year-by-year matching method. Finally, the new control group was the enterprises in non-‘three-in-one trial’ reform cities with the most similar comprehensive characteristics after the matching. We select the Short-term bank loans, Return on assets, Liquidity, Sales growth, Firm size, and Operating Cash flow as covariates and set the calliper to 0.05 to do the 1:1 and 1:4 nearest neighbour matching without replacement, and report the results in column (1) and (2) of , respectively. The results show that the coefficients of IPP are always significantly positive, which further confirms our baseline conclusion.

Table 4. PSM-DID.

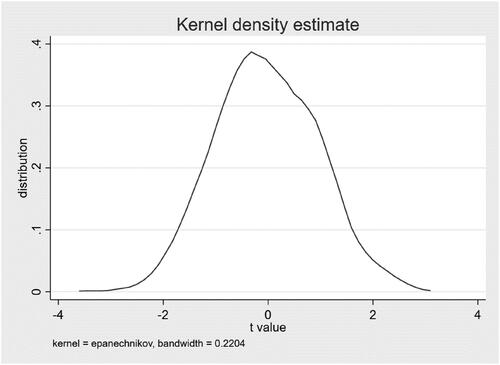

4.2.3. Placebo test

To further eliminate the differences of characteristics between the experimental group and the control group before the ‘three-in-one trial’ reform and the unobservable missing variables bias, we randomly assign the cities implement the ‘three-in-one trial’ reform to the sample enterprises and repeat 1000 times regressions according to the EquationEquation (1)(1)

(1) by using the new experimental and control groups. The placebo test result is reported in the . We find the curve distribution is about 0 and close to the normal distribution, which indicates that the ‘three-in-one trial’ reform does not bring significant differences in the changes in trade credit financing between the experimental group and the control group. Hence, the above result also supports our baseline conclusion.

Figure 2. Placebo test.

4.2.4. Considering the missing variable problem

To further exclude the influence of regional factors, we add some possible regional variables such as the regional financial development level, the opening degree and the education level into the EquationEquation (1)(1)

(1) , where the financial development level is represented by the total amount of deposits and loans of each prefecture level city divided by GDP, the opening degree is measured by the amount of foreign direct investment divided by GDP, and the education level is measured by the proportion of education expenditure to GDP. The column (1) in reports the empirical result, which further proves the baseline conclusion.

Table 5. Other robustness tests.

4.2.5. Counterfactual test

We assume the implementation years of the ‘three-in-one trial’ reform are two or three years ahead of the real time and redo the regressions. The regression results of column (2) and column (3) in show that the assumed ‘three-in-one trial’ reform has no significant effect on the trade credit financing, indicating that the difference between the experimental group and the control group comes from the change in IPP.

4.3. Possible mechanisms

In this section, we examine the underlying mechanisms through which the strength of IPP improves the trade credit financing of high-tech enterprises. Referring to Sobel (Citation1982) and Baron and Kenny (Citation1986), we construct the following mediation effect models.

(3)

(3)

(4)

(4)

where

is the intermediary variable, and other variables are the same as EquationEquation (1)

(1)

(1) . The mediation effect models are divided into three steps. EquationEquation (1) (3)

(3)

(3) and Equation(4)

(4)

(4) are the first, second and third step, respectively. According to Sobel (Citation1982) and Baron and Kenny (Citation1986), if the coefficients

and

are significant, and the size or significance of

is smaller than

there exists a mediation effect.

Test of technology market effect

We use an intermediary variable measured by the logarithm of city-level technology market transactions (techmarket) to check this mechanism. The transaction volume of the municipal technology market is estimated by multiplying the provincial one by the proportion of the number of new patents of each city in its province in the current year. The results in columns (1) and (2) in Panel A of show that the IPP can indeed increase the trade credit financing of high-tech enterprises by promoting technology market transactions, which verifies H2. The stronger IPP level, the more it can promote the development of the technology market and provide channels and carriers for the flow of innovation resources. The ability of intellectual property as collateral is improved, thus, the convenience of creditors to monetise intellectual property in the capital market is also improved, which promotes the trade credit financing of enterprises.

Table 7. Cross sectional results of IPP on trade credit financing.

Test of innovation effect

We use the natural logarithm of the number of patent applications plus 1 (Patent apply) and the natural logarithm of the number of patent grants plus 1 (Patent grant) to measure firm’s innovation ability to identify the innovation effect. Column (1)–(4) in Panel B of reports the results, which show that innovation capability is an essential intermediary factor for IPP enhancing trade credit financing of high-tech enterprises. The supply intention of trade credit providers mainly depends on the trade-off between the firm’s risk and income. Generally, the more vital innovation ability will associate with the more significant knowledge spillover from which suppliers or customers can benefit. Hence, suppliers and customers are more willing to invest in high-tech enterprises with more vital innovation ability and establish a good relationship. The above results confirmed H3.

Table 6. Mechanisms.

Panel B. Innovation effect

Panel C. Information effect

Test of information effect

We next measure the degree of information asymmetry by enterprise information disclosure quality (Kv) and capital market attention (Analyst attention, Research report attention) to check the information effect, where we reference Kim and Verrecchia (Citation2001) to calculate the enterprise information disclosure quality index (Kv) and calculate the level of analyst attention and research report attention by the natural logarithm of the original value added 1, respectively. Columns (1)–(5) in Panel C of report the results, which show that the impact of IPP on enterprise information disclosure quality is not significant, while on capital market, attention is significant. We thus find that strengthening IPP does not encourage enterprises to disclose information but motivate capital market to searching the information of high-tech enterprises, which also reduces information asymmetry. These results indicate that information asymmetry is another important intermediary factor, which thereby verifies H4. The researches most relevant to our findings are Hall (Citation2002) and Brown et al. (Citation2009), which analysed whether the change in institutional environment will change the willingness of enterprise information disclosure. On this basis, we further analyse the impact of the strengthening of IPP on the information searching behaviour of the capital market.

5. Further test

5.1. Cross Sectional differences of IPP on trade credit financing

Enterprises with different levels of government support or fixed assets have different capital demand. Regional government–business relationship will affect enterprises’ decision-making. Thus, the heterogeneities of enterprises or regions may lead to different promotion effects of IPP on enterprises’ trade credit financing. Therefore, this article further compares the cross-sectional differences in these three aspects.

5.1.1. The impact of government support

We divide our sample into higher government support group and lower one by the ratio of government subsidies to total assets. If the ratio of government subsidies to total assets is higher than the average of all observations, it belongs to experience group, otherwise, control group. The empirical results of columns (1) and (2) in show that the strengthening of IPP improves the trade credit financing of high-tech enterprises with lower government support. On the one hand, enterprises with higher government support generally have rich resources, which can help them release positive signals of high credit and low default risk and thereby enhance their own trade credit financing ability; therefore, the marginal value of IPP on enterprise trade credit financing is weakened. On the other hand, due to the paternalism and political protection from local governments, high-tech enterprises with higher government support are relatively easy to obtain bank loans, which contrarily reduce their demand for trade credit financing.

Table 8. The structural heterogeneity of the influence of IPP on trade credit.

5.1.2. The influence of firm fixed assets

We next divide our sample into two groups according to whether the proportion of fixed assets in total assets is higher than the average value of all observations. If one observation is higher than average value, it belongs to experience group, otherwise, control group. From the results of columns (3) and (4) in , we find that IPP can only enhance the trade credit financing of high-tech enterprises with less fixed assets. High tech enterprises with less fixed assets are usually short of collateral with higher debt risk and lower bargaining power, making them difficult to obtain bank loan (Philippe & Patrick, Citation1992; Gregory & Tenev, Citation2001). Therefore, these enterprises are more likely to turn to informal financing channels such as trade credit financing, which is more vulnerable to the change in IPP.

5.1.3. The influence of government–business relationship

By using the city-level government–business relationship health index first constructed by Nie et al. (Citation2019), we divide our sample into two groups. If the index of government–business relationship health in the city, where the enterprise located is greater than the average, it belongs to the experimental group, otherwise, the control group. The results of columns (5) and (6) in show that the promotion of IPP on trade credit financing of high-tech enterprises is more obvious in cities with healthier government–business relationship. When the relationship between government and business is healthier, the government power can be effectively supervised and constrained, so enterprises can fairly and low costly get better property rights protection and more policy resources, which helps to enhance the confidence of trade credit providers.

5.2. The structure of trade credit financing

The trade credit financing can be further divided into the accounts payable for suppliers, bills payable and customers' advance receivables. Due to different contract cost, risk and impact on production and operation, enterprises have different preferences for these three types trade credit financing. Because the enterprise only obtains the right to pay for goods after a period through notes payable and accounts payable, it does not get the real financial support from the supplier, making its flexibility is lower than that from the customer's advance receivables. Compared with accounts payable, on the one hand, bills payable have a series of checking and issuing processes, which increases its transaction cost. On the other hand, bills payable also needs the payer to pay the relevant interest expenses, which further increases firm’s financing cost. Therefore, for trade credit financing of high-tech enterprises, the advance accounts receivable is the best, while the bill payable is relative complicated, and its cost is higher.

This section measures different trade credit financing modes by using advance receipts, accounts payable, and notes payable, respectively, and redo the regressions by introducing the above variables into the EquationEquation (1)(1)

(1) . The results in indicate that IPP only significantly increases the financing of notes payable, which has a higher cost. We guess that it is caused by the various uncontrollable systemic risks in trade credit financing. Even if the strengthening of IPP can boost the confidence of trade credit providers, the promotion is only evident for the notes payable, which has a stronger payment guarantee but higher cost.

6. Conclusion

The research of IPP on enterprise behaviour is still a research frontier. In this study, we investigate the impact of IPP on corporate trade credit financing, which is a less-focused but important external financing channel for the high-tech enterprise. The results show that IPP can effectively promote the trade credit financing of high-tech enterprises, and it has more significant effect on the higher cost but more secure notes payable. In addition, IPP can promote high-tech enterprises to obtain trade credit financing by promoting the prosperity of technology trading market, improving enterprise innovation output and alleviating internal and external information asymmetry. Especially, the mechanism of alleviating information asymmetry is consistent with the most existing literature (Hall, Citation2002; Brown et al., Citation2009; Ang et al., Citation2014), while we further distinguish the enterprises' active information disclosure behaviour and capital market information search behaviour. We also prove that the promotion effects of IPP on high-tech enterprises with lower government support, lower proportion of fixed assets and healthier relationship between government and business are more obvious.

Our study provides theoretical implications. First, we expand the literature of IPP impacting corporate financing by focusing on trade credit financing. Different from the other financing channels like bank loan, equity financing and internal financing, the trade credit financing is important and special for the high-tech enterprises, who are facing more financing constrains, while less studies focus on this research issue. We investigate this important issue and prove that the IPP can promote the corporate trade credit financing. Second, we distinguish and compare two information asymmetry alleviating channels, i.e., the enterprises' active information disclosure and capital market information searching, which provide a new perspective for the researches of information asymmetry theory in corporate financing. We find that behind the promotion of enterprise financing by IPP, the behaviour of analysts and investors actively searching for information of high-tech enterprises in the capital market can also reduce information asymmetry.

Our results also provide practical implications. First, this article provides a basis for the government to help high-tech enterprises obtaining innovation financing by improving the level of IPP. The improvement of the IPP makes trade creditors more willing to invest high-tech enterprises. Therefore, the government should try to improve their IPP level. Second, better IPP is conducive to investors to search for innovation information of high-tech enterprises. However, it is obvious that enhancing IPP cannot encourage enterprises to disclose more information in our article. Thus, our conclusion suggests, on the one hand, that the government needs to constantly improve the construction of capital market to improve its information search ability. On the other hand, we propose to build a safer way for enterprise information disclosure. Third, the government should guide the implementation of the reform policy of intellectual property case trial to improve the IPP level.

Finally, we acknowledge some limitations, which may provide rich opportunities for future researches. First, as the ‘three-in-one trial’ reform is only implemented in China, it is impossible to extend this quasi-natural experiment to more samples from developing countries. Therefore, we expect that our conclusions will be further confirmed by using more reform event data in other developing countries. Second, we only focus on the impact of IPP on trade credit financing. In future researches, we can further compare the influences of IPP on different financing means and thereby find more effective channels to alleviate the financing constrains of high-tech enterprises.

Disclosure statement

The authors declare no potential conflict of interest.

Additional information

Funding

References

- Alimov, A., & Officer, M. S. (2017). Intellectual property rights and cross-border mergers and acquisitions. Journal of Corporate Finance, 45, 360–377. https://doi.org/10.1016/j.jcorpfin.2017.05.015

- Alimov, A. (2019). Intellectual property rights reform and the cost of corporate debt. Journal of International Money and Finance, 91, 195–211. https://doi.org/10.1016/j.jimonfin.2018.12.004

- Allred, B. B., & Park, W. G. (2007). Patent rights and innovative activity: Evidence from national and firm-level data. Journal of International Business Studies, 38(6), 878–900. https://doi.org/10.1057/palgrave.jibs.8400306

- Ang, J. S., Cheng, Y., & Wu, C. (2014). Does enforcement of intellectual property rights matter in China? Evidence from financing and investment choices in the high-tech industry. The Review of Economics and Statistics, 96(2), 332–348. https://doi.org/10.1162/REST_a_00372

- Anton, J. J., & Yao, D. A. (2002). The sale of ideas: Strategic disclosure, property rights, and contracting. Review of Economic Studies, 69(3), 513–531. https://doi.org/10.1111/1467-937X.t01-1-00020

- Arora, A., Fosfuri, A., & Gambardella, A. (2002). Markets for technology in the knowledge economy. International Social Science Journal, 54(171), 115–128. https://doi.org/10.1111/1468-2451.00363

- Arora, A., Fosfuri, A., & Gambardella, A. (2008). Markets for technology: The economics of innovation and corporate strategy. Academy of Management Review, 27, 1275–1276.

- Arrow, K. J. (1962). The economic-implication of learning by doing. The Review of Economic Studies, 29(3), 155–173. https://doi.org/10.2307/2295952

- Autor, D. H. (2003). Outsourcing at will: The contribution of unjust dismissal doctrine to the growth of employment outsourcing. Journal of Labor Economics, 21(1), 1–23. https://doi.org/10.1086/344122

- Baron, R. M., & Kenny, D. A. (1986). The moderator mediator variable distinction in social psychological-research-conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Beck, T., Levine, R., & Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. The Journal of Finance, 65(5), 1637–1667. https://doi.org/10.1111/j.1540-6261.2010.01589.x

- Brown, J. R., Fazzari, S. M., & Petersen, B. C. (2009). Financing innovation and growth: Cash flow, external equity, and the 1990s R&D boom. The Journal of Finance, 64(1), 151–185. https://doi.org/10.1111/j.1540-6261.2008.01431.x

- Branstetter, L. G., Fisman, R., & Foley, C. F. (2006). Do stronger intellectual property rights increase international technology transfer? Empirical evidence from US firm-level panel data. The Quarterly Journal of Economics, 121(1), 321–349. https://doi.org/10.1162/003355306776083482

- Branstetter, L., Fisman, R., Foley, C. F., & Saggi, K. (2011). Does intellectual property rights reform spur industrial development? Journal of International Economics, 83(1), 27–36. https://doi.org/10.1016/j.jinteco.2010.09.001

- Bryhinets, O., Shapoval, R., Bakhaieva, A., Pchelin, V., & Fomenko, A. (2021). Problems of intellectual property in the national security system of the country. Entrepreneurship and Sustainability Issues, 8(3), 471–486. https://doi.org/10.9770/jesi.2021.8.3(30)

- Chen, Y., & Puttitanun, T. (2005). Intellectual property rights and innovation in developing countries. Journal of Development Economics, 78(2), 474–493. https://doi.org/10.1016/j.jdeveco.2004.11.005

- Chen, R., El Ghoul, S., Guedhami, O., Kwok, C. C. Y., & Nash, R. (2021). International evidence on state ownership and trade credit: Opportunities and motivations. Journal of International Business Studies, 52, 1121–1158. https://doi.org/10.1057/s41267-021-00406-5

- Chen, L., Lin, P., & Zou, H. (2012). Does property rights protection affect corporate risk management strategy? Intra- and cross-country evidence. Journal of Corporate Finance, 18(2), 311–330. https://doi.org/10.1016/j.jcorpfin.2011.12.006

- Claessens, S., & Laeven, L. (2003). Financial development, property rights, and growth. The Journal of Finance, 58(6), 2401–2436. https://doi.org/10.1046/j.1540-6261.2003.00610.x

- Francis, B., Hasan, I., Huang, Y., & Sharma, Z. (2012). Do banks value innovation? Evidence from US firms. Financial Management, 41(1), 159–185. https://doi.org/10.1111/j.1755-053X.2012.01181.x

- Gambardella, A. (2002). 'Successes' and 'failures' in the markets for technology. Oxford Review of Economic Policy, 18(1), 52–62. https://doi.org/10.1093/oxrep/18.1.52

- Gopalan, R., Mukherjee, A., & Singh, M. (2016). Do debt contract enforcement costs affect financing and asset structure? Review of Financial Studies, 29(10), 2774–2813. https://doi.org/10.1093/rfs/hhw042

- Gregory, N., & Tenev, S. (2001). The financing of private enterprise in China. Finance & Development, 38, 14–14.

- Guiso, L. (1998). High-tech firms and credit rationing. Journal of Economic Behavior & Organization, 35(1), 39–59. https://doi.org/10.1016/S0167-2681(97)00101-7

- Hall, B. (2002). The financing of research and development. Oxford Review of Economic Policy, 18(1), 35–51. https://doi.org/10.1093/oxrep/18.1.35

- Hall, B. H., Jaffe, A., & Trajtenberg, M. (2005). Market value and patent citations. RAND Journal of Economics, 36, 16–38.

- Hall, B. H., & Lerner, J. (2010). The financing of R&D and innovation. Handbook of the Economics of Innovation, 1, 610–638. https://doi.org/10.1016/S0169-7218(10)01014-2

- Hall, B., Helmers, C., Rogers, M., & Sena, V. (2014). The choice between formal and informal intellectual property: A review. Journal of Economic Literature, 52(2), 375–423. https://doi.org/10.1257/jel.52.2.375

- Hart, O., & Moore, J. (1994). A theory of debt based on the inalienability of human-capital. The Quarterly Journal of Economics, 109(4), 841–879. https://doi.org/10.2307/2118350

- Heyman, F., Sjoholm, F., & Tingvall, P. G. (2007). Is there really a foreign ownership wage premium? Evidence from matched employer-employee data. Journal of International Economics, 73(2), 355–376. https://doi.org/10.1016/j.jinteco.2007.04.003

- Hoffmann, A. O. I., & Kleimeier, S. (2021). How do banks finance R&D intensive firms? The role of patents in overcoming information asymmetry. Finance Research Letters, 38, 101485. https://doi.org/10.1016/j.frl.2020.101485

- Hoffmann, A. O. I., Kleimeier, S., Mimiroglu, N., & Pennings, J. M. E. (2019). The American inventors protection act: A natural experiment on innovation disclosure and the cost of debt. International Review of Finance, 19(3), 641–651. https://doi.org/10.1111/irfi.12174

- Howell, S. T. (2017). Financing innovation: Evidence from R&D grants. American Economic Review, 107(4), 1136–1164. https://doi.org/10.1257/aer.20150808

- Kim, O., & Verrecchia, R. E. (2001). The relation among disclosure, returns, and trading volume information. The Accounting Review, 76(4), 633–654. https://doi.org/10.2308/accr.2001.76.4.633

- Lerner, J. (2002). 150 years of patent protection. American Economic Review, 92(2), 221–225. https://doi.org/10.1257/000282802320189294

- Liu, Q., & Wong, K. P. (2011). Intellectual capital and financing decisions: Evidence from the U.S. patent data. Management Science, 57(10), 1861–1878. https://doi.org/10.1287/mnsc.1110.1380

- Mann, W. (2018). Creditor rights and innovation: Evidence from patent collateral. Journal of Financial Economics, 130(1), 25–47. https://doi.org/10.1016/j.jfineco.2018.07.001

- Mateut, S. (2014). Reverse trade credit or default risk? Explaining the use of prepayments by firms. Journal of Corporate Finance, 29, 303–326. https://doi.org/10.1016/j.jcorpfin.2014.09.009

- Nie, H., Han, D., Ma, L., & Zhang, N. (2019). Ranking list of China's urban political and commercial relations (2018). The National Institute of Development and Strategy. Renmin University of China. (In Chinese)

- Philippe, A., & Patrick, B. (1992). An incomplete contracts approach to financial contracting. The Review of Economic Studies, 59, 473–494.

- Qian, Y. (2007). Do national patent laws stimulate domestic innovation in a global patenting environment? A cross-country analysis of pharmaceutical patent protection, 1978–2002. Review of Economics and Statistics, 89(3), 436–453. https://doi.org/10.1162/rest.89.3.436

- Sobel, M. (1982). Asymptotic confidence intervals for indirect effects in structural equation models. Sociological Methodology, 13, 290–312. https://doi.org/10.2307/270723

- Spence, M. (1973). Job market signaling. The Quarterly Journal of Economics, 87(3), 355–374. https://doi.org/10.2307/1882010

- Stiglitz, J. E. (2000). The contributions of the economics of information to twentieth century economics. The Quarterly Journal of Economics, 115(4), 1441–1478. https://doi.org/10.1162/003355300555015

- Sweet, C. M., & Maggio, D. E. (2015). Do stronger intellectual property rights increase innovation? World Development, 66, 665–677. https://doi.org/10.1016/j.worlddev.2014.08.025

- Ueda, M. (2004). Banks versus venture capital: Project evaluation, screening, and expropriation. The Journal of Finance, 59(2), 601–621. https://doi.org/10.1111/j.1540-6261.2004.00643.x

- Xiang, C., Chen, F., Jones, P., & Xia, S. (2021). The effect of institutional investors’ distraction on firms’ corporate social responsibility engagement: Evidence from China. Review of Managerial Science, 15(6), 1645–1681. https://doi.org/10.1007/s11846-020-00387-z

- Zhang, L., Chen, F.-W., Xia, S.-M., Cao, D.-M., Ye, Z., Shen, C.-R., Maas, G., & Li, Y.-M. (2021). Value co-creation and appropriation of platform-based alliances in cooperative advertising. Industrial Marketing Management, 96, 213–225. https://doi.org/10.1016/j.indmarman.2021.06.001

Table A1.

Variable definitions.