?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study discusses the impact of executives with foreign experience on decisions involving corporate capital structures. Based on a sample of Chinese A-share listed companies, this study finds that firms with (more) executives with foreign experience adjust to the optimal capital structure faster. The effect exists mainly for over-levered firms that need to deleverage. The empirical results remain robust when using alternative methods to estimate target leverage, excluding the effects of mechanical adjustments, controlling the impact of corporate governance, and using the full sample to test asymmetric effects. In addition, firms managed by executives with foreign experience tend to maintain low leverage for a long time. Overall, the results show that executives with foreign experience help companies adopt more efficient and conservative capital structure adjustment decisions. The results enrich the literature on the impact of foreign experience on corporate decision-making.

1. Introduction

Enterprise globalisation has gained widespread public attention in recent decades. Compared to transnational operations, transnational mergers and acquisitions (M&A), and other corporate transnational behaviour (Bhagwat et al., Citation2021; Hormiga & Bolívar-Cruz, Citation2014; Hsu & Chen, Citation2021), the phenomenon and impact of the internationalisation of the senior management team (i.e. executives with foreign experience) is increasingly studied in the field of corporate governance (Cao et al., Citation2019; Yuan & Wen, Citation2018).

Prior research shows that early foreign experience results in significantly different business philosophies among executives (Hambrick & Mason, Citation1984; Green et al., Citation2019), making them more responsible and trustworthy (Guiso et al., Citation2015; Zhang et al., Citation2018). Consistent with this theoretical conjecture, relevant empirical literature shows that companies with foreign executives achieve better performance (Giannetti et al., Citation2015), a higher level of innovation (Yuan & Wen, Citation2018), and a lower risk of stock price crashes (Cao et al., Citation2019).

However, few studies investigate the impact of executives with foreign experience on corporate financing behaviour (i.e. capital structure). Capital structure (the ratio of liabilities to assets) is a core issue in corporate finance and has attracted a number of theoretical and empirical studies. Morellec et al. (Citation2012) expanded on one of the newly developed theories (dynamic trade-off theory) by considering the agency cost of shareholder-agent conflict. This inspired subsequent investigation on the impact of corporate governance on corporate capital structure decisions (Gyimah et al., Citation2021).

This study expands on Morellec et al. (Citation2012)’s research from the perspective of executives with foreign experience. Existing studies reveal that executives with foreign experience reduce the agency cost of shareholder-agent conflicts (Cao et al., Citation2019; Giannetti et al., Citation2015). This study further investigates the impact of foreign executives’ experience on corporate capital structure decisions. Based on a sample of Chinese A-share listed companies, we find that firms with (more) executives with foreign experience adjust to the optimal capital structure faster. The effect exists mainly for over-leveraged firms that need to deleverage. Several robustness tests proved the reliability of the research findings. Firms managed by executives with foreign experience tend to maintain low leverage for a long time.

This study contributes to the literature in two ways. First, the results extend the literature on the economic consequences for executives with foreign experience. Existing studies explore the impact of executives with foreign experience on enterprise behaviour, such as corporate social responsibility, business performance, innovation, and stock price crash risks (Cao et al., Citation2019; Giannetti et al., Citation2015; Yuan & Wen, Citation2018; Zhang et al., Citation2018). This study investigates the impact of executives with foreign experience on corporate capital structure and extends the discussion of the economic consequences of such executives.

Second, this study enriches the literature on the dynamic adjustment of capital structure with the influence of agency costs, as proposed by Morellec et al. (Citation2012). The early empirical results of studies on the dynamic adjustment of capital structure reveal inexplicable aspects when considering only adjustment costs (Byoun, Citation2008; Flannery & Rangan, Citation2006; Graham, Citation2000). Through the relationship between executives with foreign experience and agency costs, this study provides empirical evidence supporting the theoretical framework proposed by Morellec et al. (Citation2012) and adds to the empirical work on the effects of corporate governance on the dynamic adjustment of capital structure (Chang et al., Citation2014; Gyimah et al., Citation2021).

The remainder of this paper is organised as follows. Section 2 reviews the literature and develops the research hypotheses. Section 3 presents our empirical design, section 4 provides the empirical results, and section 5 concludes the paper.

2. Literature review and hypothesis development

Capital structure dynamic adjustment theory argues that the speed of dynamic adjustment toward the target capital structure depends on the relative benefits and costs of adjustment (Fischer et al., Citation1989; Leary & Roberts, Citation2005). However, relevant studies primarily focus on the impacts of adjustment costs, which leads to insufficient explanatory power in some aspects, including generally low or even zero debt (Graham, Citation2000), the lower-than-expected speed of capital structure adjustment (Flannery & Rangan, Citation2006), and asymmetric speeds of capital structure adjustment (Byoun, Citation2008). To solve this, Morellec et al. (Citation2012) propose that considering the agency costs of shareholder-agent conflict can improve the explanatory power of dynamic adjustment to capital structure.

Jensen and Meckling (Citation1976) originally proposed the agency problem of shareholder-agent conflict; they focused on the separation of management and control rights, as commonly seen in modern enterprises. Due to the asymmetry of information, when there is conflict in the interests of managers and shareholders, managers can leverage their information superiority by not maximizing or even harming the interests of shareholders (Hout & Carter, Citation1995; Kumar & Zattoni, Citation2016; Wommack, Citation1979). Therefore, reducing the agency cost of shareholder-agent conflict is an important topic in modern corporate governance. In addition to external supervision or internal governance by analysts, auditors, and institutional investors, managers’ characteristics and experience are of recent research interest (Hu et al., Citation2020; Lin et al., Citation2019; Zhang et al., Citation2015). Foreign experience is an important executive characteristic.

Existing studies show that early education, work, and foreign experience broaden managers’ international horizons, which, in turn, has a significant impact on their behaviours (Green et al., Citation2019). Senior management with an international vision can be more proficient in mastering and utilizing international trading tools to help the company reach their ideal financing structure and risk allocation more quickly (Madura & Wallace, Citation1985); this drives their performance (Giannetti et al., Citation2015) and innovation level (Yuan & Wen, Citation2018). More importantly, executives with foreign experience, a broader international vision, and cross-cultural knowledge structure tend to assume greater social responsibility (Zhang et al., Citation2018) and become more responsible and trustworthy managers (Guiso et al., Citation2015), which improves corporate governance.

Considering the various existing frictions, companies must pursue an optimal capital structure to maximise their value (Modigliani & Miller, Citation1958). However, because of the agency cost of shareholder-agent conflicts, the decisions managers may deviate from maximizing the interests of shareholders, which is also a significant reason for the low speed of capital structure adjustment (Morellec et al., Citation2012). Executives with foreign experience shoulder greater social responsibility. Moreover, gaining experience in countries with more mature markets provides executives with a deeper understanding and respect for the rules (Masulis et al., Citation2012). Therefore, they are more responsible and trustworthy (Guiso et al., Citation2015; Zhang et al., Citation2018), especially in emerging market countries such as China, where executives’ foreign experiences generally come from mature economies such as Europe and the United States (Yuan & Wen, Citation2018). Therefore, hiring such executives will improve corporate governance and lower agency costs in shareholder-agent conflicts (Cao et al., Citation2019). This further implies such companies will actively apply more effort to adjust to their optimal capital structure. Therefore, we propose our first hypothesis.

Hypothesis 1: Companies with more executives with foreign experience adjust to their target capital structure faster than those with fewer executives with foreign experience.

According to the dynamic capital structure theory, over-leveraged enterprises should reduce leverage, while under-leveraged enterprises should increase leverage. However, empirical evidence shows a significant difference between the speed of deleveraging and that of increasing leverage. In particular, the downward adjustment by over-leveraged companies toward the target capital structure is faster than the upward adjustment by under-leveraged companies (Byoun, Citation2008; Faulkender et al., Citation2012), which indicates a more conservative capital structure adjustment behaviour.

Executives with foreign experience usually work or study in developed countries (Yuan & Wen, Citation2018), which brings them professional knowledge and advanced management skills, and provides them with a deeper understanding of and respect for the rules (Masulis et al., Citation2012; Giannetti et al., Citation2015). Therefore, whether learning from mature market experience or avoiding bankruptcy risk, executives with foreign experience will accelerate the enterprise’s adjustment to the target capital structure and promote conservative capital structure decision-making. In other words, executives with foreign experience accelerate the process of reducing leverage for over-leveraged enterprises; however, their impact on under-leverage enterprises to increase leverage is relatively limited. Therefore, we propose the following hypothesis:

Hypothesis 2: The effects of executives with foreign experience on accelerating corporate capital structure adjustment appear mainly in over-leveraged companies and are limited for under-leveraged companies.

3. Research design

3.1. Models and variables

3.1.1. Dynamics of capital structure

Based on a literature review (Byoun, Citation2008; Huang & Ritter, Citation2009; Lemmon et al., Citation2008), part of the standard capital structure adjustment model is set as follows:

(1)

(1)

where Levit and Levi,t-1 refer to the capital structure of company i in years t and t-1, respectively, and TLevit refers to the target capital structure of company i in year t. λ denotes the gap between the actual and target capital structure of the company, closing at a rate of λ, also known as the speed of adjustment toward the target capital structure.

3.1.2. Target capital structure

Regarding the dynamic capital structure model, the key to this study is to evaluate the company's target capital structure. This study used the following model to measure a company’s target capital structure:

(2)

(2)

where Xit-1 denotes a series of variables related to the capital structure. Following Flannery and Rangan (Citation2006) and Faulkender et al. (Citation2012), these variables include (1) size, defined as the natural logarithm of total assets; (2) ROA, defined as net profit to total assets to measure a company’s profitability; (3) growth, defined as sales minus lagged sales divided by lagged sales; (4) Tang, defined as the ratio of property, plant, and equipment to total assets to measure the mortgage capacity of enterprise assets; (5) DEP, measured as the depredation of fixed assets divided by total assets to measure the non-debt tax shield of an enterprise; and (6) Indulev, defined as the industry median capital structure to measure the capital structure performance of the company’s industry.

3.1.3. The impact of Executives with foreign experience on the dynamics of capital structure

Byoun (Citation2008) and Faulkender et al. (Citation2012) studied the impact of financial default/surplus and cash flows on the dynamic adjustment of capital structure. The following empirical regression model was constructed based on these studies to test the hypotheses:

(3)

(3)

where Forit denotes executives with foreign experience. Three indicators were constructed for executives with foreign study or work experience following Yuan and Wen (Citation2018) and Cao et al. (Citation2019). (1) ForDummy: equal to one if there is at least one executive with foreign experience in the company in that year, and zero otherwise. (2) ForRatio denotes the ratio of executives with foreign experience to all executives in that year. (3) ForNumber denotes the natural logarithm of the number of executives with foreign experience in the company in that year plus one. Based on the theoretical analysis and expectations of Hypothesis 1, the coefficient β1 of Model (3) is significantly positive. To address Hypothesis 2, the full sample was divided into two sub-samples: over-leveraged companies (actual leverage above the target) and under-leveraged companies (actual leverage below the target). For overleveraged companies, the coefficient β1 of Model (3) is significantly positive, and for underleveraged companies, β1 is insignificant. summarises the main variables used in this study.

Table 1. Variable definitions.

3.2. Sample and data sources

The initial sample in this study includes all A-share firms listed on the Shanghai and Shenzhen Stock Exchanges from 2008 to 2015. The sample period begins in 2008, as this is the first year during which data on CEO characteristics were available from the China Stock Market & Accounting Research (CSMAR) database. The sample ended in 2015, and the five priority tasks of cutting overcapacity, reducing excess inventory, deleveraging, lowering costs, and strengthening areas of weakness have been promoted in China since 2016. These tasks generally endure great pressure from deleveraging, which consequently affects the enterprise decision-making on capital structure. Moreover, the outbreak of the Sino-US trade war in 2018 and the COVID-19 pandemic in 2020 significantly influenced enterprise decision-making. The following companies are excluded from the sample: (1) those in the financial industry, such as banks, as their balance sheet structure is quite different from that of non-financial enterprises; (2) companies with an asset-liability ratio < 1, as such enterprises are insolvent and can almost be regarded as bankrupt; (3) companies that issue shares in foreign markets, such as B and Hong Kong; and (4) companies with missing data on the primary variables. All variables in this study were obtained from the CSMAR database, and all continuous variables were winsorized at the 1% and 99% levels to eliminate the interference of extreme data in the results.

3.3. Descriptive statistics

presents descriptive statistics for the main variables. The average asset-liability ratio of the sample companies was 46.5%. This result is higher than that reported for mature market enterprises in prior studies such as Byoun (Citation2008) and Faulkender et al. (Citation2012), indicating that emerging market enterprises have higher leverage. Companies with foreign experience executives accounted for 51.5% of the sample. This result is close to the 44.8% reported by Cao et al. (Citation2019). Simultaneously, the average ratio of executives with foreign experience is 5.23% in the sample, with an average of 2.67 (= e0.515 + 1). Additionally, Chinese listed enterprises have acceptable profitability and growth performance, with an approximate annual average ROA of 4.5% and an approximate annual Growth rate of 10.8%.

Table 2. Descriptive statistics.

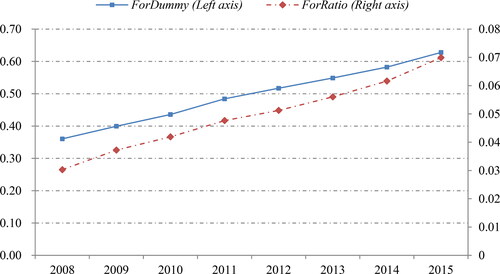

further shows the time trend of the employment of executives with foreign experience in Chinese companies during the sample period. The proportion of Chinese companies hiring such executives increased from 40% in 2008 to 63% in 2015, and the proportion of the executives increased from 3% in 2008 to 7% in 2015, indicating that hiring executives with foreign experience has become a significant feature of Chinese companies.

Figure 1. The trend of executives with foreign experience from 2008 to 2015.

Source: the results of the author’s empirical test.

provides the statistics by industry. The wood, furniture, and electronics sectors in the manufacturing industry; and the information technology, real estate, media, and cultural sectors in the non-manufacturing industry prefer hiring executives with foreign experience, with a ratio of over 60% for executives with foreign experience and a higher average ratio for those in executive teams.

Table 3. Industry distribution of executives with foreign experience.

4. Empirical results

4.1. Dynamics of capital structure

First, the speed of the capital structure adjustment is tested, and the regression results of Model (1) are shown in Panel A of . The first column shows the regression results for the full sample, and the second and third columns show the regression results for the sub-samples that need to adjust leverage downwards (actual leverage above the target) and upwards (actual leverage below the target), respectively. The average capital structure adjustment speed of the full sample, those that need to adjust leverage downwards, and those that need to adjust leverage downwards are 14.1%, 18.1%, and 10.4%, respectively.

Table 4. Dynamics of capital structure.

In general, the capital structure adjustment speed of the sample is slightly lower than that of Byoun (Citation2008) and Faulkender et al. (Citation2012) and other empirical results based on mature market enterprises. To some extent, this reflects the high degree of financial friction in emerging markets, resulting in a slow adjust to their target capital structures.

Moreover, the capital structure adjustment speed of over-leveraged companies is faster than that of under-leveraged companies. To further clarify this asymmetric relationship, Panel B of shows the regression results of Model (2) using the full sample. The results show that the capital structure adjustment speed of over-leveraged companies remained greater than that of under-leveraged companies. The test results for F show that the differences between these two are consistent with the findings of Byoun (Citation2008) and Faulkender et al. (Citation2012).

4.2. Executives with foreign experience and the dynamics of capital structure

We investigate the impact of executives with foreign experience on the dynamic adjustment of capital structure using Model (3). shows the regression results, where Panels A-C present ForDummy, ForRatio, and ForNumber, respectively. Regardless of the indicator, the regression coefficient Dev × For of the full sample remains significantly positive at the 1% level, supporting Hypothesis 1. From an economic perspective, the speed of capital structure adjustments for companies with foreign executives is 31.3% higher than for other companies (0.0442/0.141). The regression coefficient Dev × For is significantly positive only for over-leveraged companies and insignificant for under-leveraged companies, thereby supporting Hypothesis 2.

Table 5. The impacts of executives with foreign experience on the dynamic adjustment of capital structure.

5. Robustness checks

5.1. Re-estimate the target capital structure

According to Byoun (Citation2008), Model (1) assumes that the adjustment process is perfect when forecasting the target capital structure. In other words, the observed capital structure is always equal to the target capital structure, on average. However, considering the existence of adjustment costs, it seems more realistic to assume that a company adjusts its target capital structure. The following model was used to evaluate the robustness of a company’s target capital structure:

(4)

(4)

The coefficient vector β obtained using the estimation in Model (4), was substituted into Model (1) to determine the estimated target capital structure. Considering the dynamic panel estimation problem of Model (4), a system generalised method of moments (GMM) was used to develop the estimate, as in Halling et al. (Citation2016). shows the regression results for Model (3) after re-estimating the target capital structure based on GMM. Regardless of the indicator used for executives with foreign experience, the regression coefficient Dev × For of the full sample and subsample of over-leveraged companies remains significantly positive.

Table 6. Robustness test: Re-estimating the target capital structure based on the GMM method.

5.2. Eliminate the influence of mechanical adjustments

Business activities also affect a company’s capital structure. Net profits are entered directly as equity on the balance sheet. Therefore, profits will reduce the company's leverage ratio, and losses will increase the company's leverage ratio. The resulting leverage adjustment is called a mechanical adjustment (Faulkender et al., Citation2012). Therefore, the capital structures of the last period of Models (1) and (3) were substituted by the total liabilities of the last period/(total assets of the last period + net profit of the period) to retest Model (3). As shows, the regression coefficient Dev × For of the full sample and subsample of over-leveraged companies is still significantly positive, implying that the empirical results are robust.

Table 7. Robustness test: Eliminate the influence of mechanical adjustments.

5.3. Controlling the impact of corporate governance

Corporate governance has direct and indirect impacts on the dynamic adjustment of capital structure (Chang et al., Citation2014; Gyimah et al., Citation2021; Morellec et al., Citation2012), and executives with foreign experience also improve the level of corporate governance (Giannetti et al., Citation2015). Hence, failing to control for the impact of corporate governance may lead to omission of variables. The following model was used to control for the impact of corporate governance.

(5)

(5)

where CG denotes the corporate governance variables, including Com (Executives’ Compensation: the natural logarithm of the sum of the salaries of the top three executives), SOE (a dummy variable equal to one if the ultimate controlling shareholder of a listed firm is the state, and zero otherwise), TOP1 (percentage of total outstanding shares owned by the largest shareholder), and Dual (a dummy variable equal to zero for a company with a separate CEO and board chair, and one otherwise). shows the regression results for Model (5). The regression coefficient Dev × For of the full sample and the subsample of over-leveraged companies is still significantly positive, indicating a robust result.

Table 8. Robustness test: Control the impacts of corporate governance.

5.4. Effect of asymmetry

When adjusting leverage to the target capital upward or downward, the speed of adjustment may differ between companies. Simultaneously, companies endure information asymmetry and transaction cost issues when they choose between equity and debt financing. Instead of testing with subsamples, Byoun (Citation2008) proposed the following dynamic adjustment model of capital structure while considering asymmetric adjustment:

(6)

(6)

where Dev it = TLev it - Levi,t-1 denotes the gap between the company’s previous capital structure and its target capital structure.

is a dummy variable indicating over-leverage; it equals one if the capital structure of year t-1 is greater than the target capital structure of year t, and zero otherwise.

is a dummy variable indicating underleverage; it equals one if the capital structure of year t-1 is less than the target capital structure of year t, and zero otherwise. Furthermore, β1 (β2) denotes the speed of the downward (upward) leverage adjustment of an overleveraged (underleveraged) company toward the target capital structure.

According to Hypothesis 2, the impact of executives with foreign experience on the dynamic adjustment of capital structure differs for companies that need to adjust leverage downward versus upward. Referring to Byoun (Citation2008), we construct the following empirical model to test for asymmetric effects, rather than by subsamples:

(7)

(7)

presents the regression results for Model (7). Evidently, coefficient β1 of the explanatory variable is significantly positive, coefficient β2 of the explanatory variable

is not significant, and the difference between β1 and β2 is significant. Thus, the asymmetry test based on the full sample supports hypothesis 2.

Table 9. Robustness test: Asymmetric effect.

6. Additional tests

6.1. Long-term effect on capital structure

The empirical results above show that enterprises with more foreign executives adjust to the target capital structure faster and that this effect mainly occurs in over-leveraged firms. A possible economic consequence is that such enterprises maintain lower leverage in the long run. This expectation is tested using the following empirical model:

(8)

(8)

where Lowlev indicates whether the enterprise has low leverage. The value equals one if the enterprise's capital structure in the current year is lower than 80% of the target capital structure, and zero otherwise. The long-term effect is tested by considering periods t, t + 1, and t + 2 as phases for Lowlev and testing them simultaneously. Additionally, this study uses an indicator of continuous low leverage that is equal to one if the enterprise's capital structure from t to t + 2 is below the target capital structure of 80%, and zero otherwise (Marchica & Mura, Citation2010). These four groups of indicators constituted the explanatory variables. The explanatory variable refers to executives with foreign experience as previously defined. The control variables include those used in the previous calculation of the target capital structure, including size (natural log of total assets), ROA (net profit to total assets), Growth (sales growth, defined as sales minus lagged sales divided by lagged sales), Tang (capital intensity, defined as the ratio of property, plant, and equipment to total assets), DEP (depreciation of fixed assets divided by total assets), and IndLev (industry median of capital structure). Additionally, this test includes year and industry dummy variables.

Considering that the explained variable was a dummy variable, a logit model was used for the regression. The test results are presented in . The regression coefficient of executives with foreign experience is significantly positive, regardless of the type of low leverage and the definition of executives with foreign experience. This result shows that executives with foreign experience maintain low leverage for a long time, confirming expectations.

Table 10. Additional test: The impacts of executives with foreign experience on the firms’ long-term capital structure.

6.2. Extending the sample period to include the Sino–US trade war

Considering China’s policy of deleveraging after 2015, this study’s sample ended in 2015. Here, we attempt to extend the sample period to ensure that the effect persisted in subsequent years. First, we extend the sample to 2019, as the outbreak of COVID-19 in 2020 changed enterprises’ decisions and behaviour. Second, we eliminate the sample of export enterprises since 2018, considering the complex impact of the Sino–US trade war on executives with foreign experience and capital structure decisions. Thus, we extend the sample period of 2008-2015 to 2008-2017, before the outbreak of Covid-19, but include the Sino–US trade war. This extended sample, with more than a ten-year time period, can better reflect the impact of executives with foreign experience on corporate capital structure decisions, especially considering recent events.

reports the hypothesis test results based on the extended sample from 2008 to 2019. Executives with foreign experience still encourage enterprises to adjust to the target capital structure faster. Such executives significantly accelerate the speed at which leverage is reduced for over-leveraged enterprises, but have no significant impact on increasing leverage among under-leveraged enterprises. Based on the longer sample period from 2008 to 2019, the research conclusions of this study remain unchanged, which further shows that the impact of executives with foreign experience on enterprise capital structure has a certain long-term nature.

Table 11. Additional test: Using the sample including Sino–US trade war (2008–2019).

7. Conclusion

This study investigates the impact of executives with foreign experience on the dynamic adjustment of corporate capital structure using a sample of Chinese A-share listed companies. The results show that firms with more executives and foreign experience adjust to the optimal capital structure faster. The effect exists mainly for over-leveraged firms that need to deleverage. The empirical results remain robust to various tests, including adopting different estimation methods for target leverage, excluding the effects of mechanical adjustments, controlling for other corporate governance factors, and using the full sample to test asymmetric effects. Additionally, executives with foreign experience enable enterprises to maintain low leverage for a long time. In summary, executives with foreign experience help companies adopt more efficient and conservative capital structure adjustments. The results expand the literature on the economic consequences of executives with foreign experience on enterprise decision making (Cao et al., Citation2019), especially regarding capital structure from the perspective of agency cost. These results highlight the impact of corporate governance (Hu et al., Citation2020; Lin et al., Citation2019; Morellec et al., Citation2012; Zhang et al., Citation2015) and provide new empirical evidence to literature.

7.1. Policy and managerial implications

The conclusions of this study also provide important insights into the construction of senior management teams in enterprises in emerging markets. Although enterprises in emerging markets have resource advantages, such as low labour costs, there is a significant gap between enterprises in emerging and developed markets regarding experience and enterprise management ability. Enterprises in emerging markets can promote innovation and reduce stock price crash risk by employing foreign executives (Cao et al., Citation2019). This study further shows that employing more executives with foreign experience can improve the efficiency of capital structure adjustments. Therefore, enterprises in emerging markets can employ such executives to further optimise financing and other decisions, including capital structure.

7.2. Limitation and future research

This study has several limitations. First, the sample was limited to listed companies. Future research can be extended to non-listed companies, especially small and medium-sized enterprises. Second, different kinds of foreign experience have different impact on enterprise decision-making; this should be examined further. However, this study was limited to data available from CSMAR, which does not provide relevant indicators. Thus, future research could be expanded to include them. Additionally, executives that lack foreign experience can optimise decision-making by learning from executives with foreign experience in the same industry. Future studies should consider the possible spill over effects. Despite these limitations, this study provides important insights into how executives with foreign experience affect and optimise enterprise capital structure decisions.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Informed consent

Informed consent was obtained from all individual participants included in the study.

Acknowledgments

This manuscript was edited by Wallace Academic Editing.

Disclosure statement

No potential conflict of interest was reported by the authors.

Availability of data

Data available on request from the authors.

Additional information

Funding

References

- Bates, T. W., Kahle, K. M., & Stulz, R. M. (2009). Why do U.S. firms hold so much more cash than they used to? The Journal of Finance, 64(5), 1985–2022. https://doi.org/10.1111/j.1540-6261.2009.01492.x

- Bhagwat, V., Brogaard, J., & Julio, B. (2021). A BIT goes a long way: Bilateral investment treaties and cross-border mergers. Journal of Financial Economics, 140(2), 514–538. https://doi.org/10.1016/j.jfineco.2020.12.005

- Byoun, S. (2008). How and when do firms adjust their capital structures towards targets. The Journal of Finance, 63(6), 3069–3096. https://doi.org/10.1111/j.1540-6261.2008.01421.x

- Cao, F., Sun, J., & Yuan, R. (2019). Board directors with foreign experience and stock price crash risk: Evidence from China. Journal of Business Finance & Accounting, 46(9–10), 1144–1170. https://doi.org/10.1111/jbfa.12400

- Chang, Y. K., Chou, R. K., & Huang, T. H. (2014). Corporate governance and the dynamics of capital structure: New evidence. Journal of Banking & Finance, 48, 374–385. https://doi.org/10.1016/j.jbankfin.2014.04.026

- Faulkender, M., Flannery, M. J., Hankins, K. W., & Smith, J. M. (2012). Cash flows and leverage adjustments. Journal of Financial Economics, 103(3), 632–646. https://doi.org/10.1016/j.jfineco.2011.10.013

- Fischer, E. O., Heinkel, R., & Zechner, J. (1989). Dynamic capital structure choice: Theory and tests. The Journal of Finance, 44(1), 19–40. https://doi.org/10.1111/j.1540-6261.1989.tb02402.x

- Flannery, M. J., & Rangan, K. (2006). Partial adjustment toward target capital structures. Journal of Financial Economics, 79(3), 469–506. https://doi.org/10.1016/j.jfineco.2005.03.004

- Giannetti, M., Liao, G., & Yu, X. (2015). The brain gain of corporate boards: evidence from China. The Journal of Finance, 70(4), 1629–1682. https://doi.org/10.1111/jofi.12198

- Graham, J. R. (2000). How big are the tax benefits of debt? The Journal of Finance, 55(5), 1901–1941. https://doi.org/10.1111/0022-1082.00277

- Green, T. C., Jame, R., & Lock, B. (2019). Executive extraversion: career and firm outcomes. The Accounting Review, 94(3), 177–204. https://doi.org/10.2308/accr-52208

- Guiso, L., Sapienza, P., & Zingales, L. (2015). The value of corporate culture. Journal of Financial Economics, 117(1), 60–76. https://doi.org/10.1016/j.jfineco.2014.05.010

- Gyimah, D., Kwansa, N. A., Kyiu, A. K., & Sikochi, A. (2021). Multinationality and capital structure dynamics: a corporate governance explanation. International Review of Financial Analysis, 76, 101758. https://doi.org/10.1016/j.irfa.2021.101758

- Halling, M., Yu, J., & Zechner, J. (2016). Leverage dynamics over the business cycle. Journal of Financial Economics, 122(1), 21–41. https://doi.org/10.1016/j.jfineco.2016.07.001

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. The Academy of Management Review, 9(2), 193–206. https://doi.org/10.2307/258434

- Hormiga, E., & Bolívar-Cruz, A. (2014). The relationship between the migration experience and risk perception: a factor in the decision to become an entrepreneur. International Entrepreneurship and Management Journal, 10(2), 297–317. https://doi.org/10.1007/s11365-012-0220-9

- Hout, T. M., & Carter, J. C. (1995). Getting it done: New roles for senior executives. Harvard Business Review, 73(6), 133–145.

- Hsu, B. X., & Chen, Y. M. (2021). Why university matters: The impact of university resources on foreign workers’ human and social capital accumulation. International Entrepreneurship and Management Journal, 17(1), 45–61. https://doi.org/10.1007/s11365-019-00629-x

- Hu, J., Long, W., Tian, G. G., & Yao, D. T. (2020). CEOs' experience of the great Chinese famine and accounting conservatism. Journal of Business Finance & Accounting, 47(9-10), 1089–1112. https://doi.org/10.1111/jbfa.12485

- Huang, R., & Ritter, J. (2009). Testing theories of capital structure and estimating the speed of adjustment. Journal of Financial and Quantitative Analysis, 44(2), 237–271. https://doi.org/10.1017/S0022109009090152

- Jensen, M. C., & Meckling, W. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Kumar, P., & Zattoni, A. (2016). Executive compensation, board functioning, and corporate governance. Corporate Governance: An International Review, 24(1), 2–4. https://doi.org/10.1111/corg.12150

- Leary, M. T., & Roberts, M. (2005). Do firms rebalance their capital structures? The Journal of Finance, 60(6), 2575–2619. https://doi.org/10.1111/j.1540-6261.2005.00811.x

- Lemmon, M. L., Roberts, M. R., & Zender, J. (2008). Back to the beginning: persistence and the cross-section of corporate capital structure. The Journal of Finance, 63(4), 1575–1608. https://doi.org/10.1111/j.1540-6261.2008.01369.x

- Lin, S., Yamakawa, Y., & Li, J. (2019). Emergent learning and change in strategy: Empirical study of Chinese serial entrepreneurs with failure experience. International Entrepreneurship and Management Journal, 15(3), 773–792. https://doi.org/10.1007/s11365-018-0554-z

- Madura, J., & Wallace, R. (1985). A hedge strategy for international portfolios. The Journal of Portfolio Management, 12(1), 70–74. https://doi.org/10.3905/jpm.1985.409025

- Marchica, M. T., & Mura, R. (2010). Financial flexibility, investment ability and firm value: evidence from firms with spare debt capacity. Financial Management, 39(4), 1339–1365. https://doi.org/10.1111/j.1755-053X.2010.01115.x

- Masulis, R. W., Wang, C., & Xie, F. (2012). Globalizing the boardroom—the effects of foreign directors on corporate governance and firm performance. Journal of Accounting and Economics, 53(3), 527–554. https://doi.org/10.1016/j.jacceco.2011.12.003

- Merton, R. C. (1974). On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance, 29(2), 449–470.

- Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporate finance, and the theory of investment. American Economic Review, 48(3), 261–297.

- Morellec, E., Nikolov, B., & Schurhoff, N. (2012). Corporate governance and capital structure dynamics. The Journal of Finance, 67(3), 803–848. https://doi.org/10.1111/j.1540-6261.2012.01735.x

- Wommack, W. W. (1979). Responsibility of the board of directors and management in corporate strategy. Harvard Business Review, 57(5), 48–62.

- Yuan, R., & Wen, W. (2018). Managerial foreign experience and corporate innovation. Journal of Corporate Finance, 48, 752–770. https://doi.org/10.1016/j.jcorpfin.2017.12.015

- Zhang, J., Kong, D., & Wu, J. (2018). Doing good business by hiring directors with foreign experience. Journal of Business Ethics, 153(3), 859–876. https://doi.org/10.1007/s10551-016-3416-z

- Zhang, X., Li, N., Ullrich, J., & Dick, R. (2015). Getting everyone on board: the effect of differentiated transformational leadership by CEOs on top management team effectiveness and leader-rated firm performance. Journal of Management, 41(7), 1898–1933. https://doi.org/10.1177/0149206312471387