?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The capability of individuals to manage their finances is essential to the outcomes of their entrepreneurial activities. Using panel data from the China Household Finance Survey (C.H.F.S.) in 2013, 2015 and 2017, this article examines how financial capability affects entrepreneurial performance in rural China. The results demonstrate that financial capability is positively correlated with the scale, profitability and sustainability of entrepreneurship, which is robust in consideration of endogeneity. The effects of financial capability are heterogeneous for different entrepreneurs. Furthermore, technology, labour and land act as the mediating variables through which financial capability improves entrepreneurial performance. Therefore, to facilitate entrepreneurial success, it is important to provide entrepreneurs with financial education. Meanwhile, improvements to the financial environment should also be considered. Additionally, financial institutions should combine financial services with factors, such as technology, land and labour, to improve entrepreneurial performance.

JEL CLASSIFICATIONS:

1. Introduction

Accessibility to financial services is viewed as an indispensable driver of entrepreneurial performance (Schumpeter, Citation1912). Several studies have highlighted that the acquisition of financial resources promotes entrepreneurshipFootnote1 (Paulson & Townsend, Citation2004; Turvey & Kong, Citation2010; Klychova et al., Citation2015; Zhang & Shu, Citation2020). However, the availability of financial services and products is not synonymous with the appropriate allocation of financial resources, but the effective utilisation of financial factors is also an important factor for entrepreneurial success (Schultz, Citation1964). Considering that entrepreneurship is a systematic process that includes decision-making regarding investment, financing and risk management, entrepreneurs’ knowledge and ability in managing their financial resources, i.e., financial capability, is essential to ensure the success of their entrepreneurial activities (Su & Kong, Citation2019).

Regarding the relationship between financial capability and entrepreneurial performance, previous studies mainly focused on the positive effects of financial literacy on entrepreneurship activities. These studies argued that, with the proper financial knowledge and skills, entrepreneurs could obtain more financial resources, especially formal credit, thus mitigating liquidity issues and improving the revenues and profits of their businesses. As a concept extended from financial literacy, financial capability further includes financial behaviours and the financial environment, which can not only ensure that entrepreneurs have more accesses to financial resources but also benefit the decision-making process in entrepreneurial activities. Therefore, financial capability may theoretically play a greater role in improving entrepreneurial performance than financial literacy. Consequently, it is imperative to explore the interaction between financial capability and entrepreneurial performance.

As the largest developing country in the world, in China farmers’ entrepreneurship is booming and forms the cornerstone of its agricultural economy. Investigating the relationship between financial capability and entrepreneurial performance in rural China can provide insights into financial and agricultural policymaking for developing countries throughout the world. Additionally, the financial market in rural areas is relatively backward compared with that in urban areas due to China’s dual financial structure. Given the substitutional relationship between financial capability and financial resources, examining the effects of financial capability on entrepreneurial outcomes in the context of liquidity constraints can not only help to promote the financial capability of farmers but also facilitate entrepreneurship in rural areas.

Using the China Household Finance Survey (C.H.F.S.) panel data, this study seeks to examine the relationship between financial capability and entrepreneurial performance to complement the research on financial capability and economic well-being. Moreover, by examining the mediating effects of labour, land and technology, this study further investigates the mechanism of financial capability on business performance. Additionally, this research explores the heterogeneous effects of financial capability on the different types of entrepreneurs. These results will not only help to formulate policies that enhance the financial capabilities of entrepreneurs but also facilitate their success.

This study contributes to existing literature on financial capability and entrepreneurial performance in three ways. First, this study incorporates financial behaviours and financial environment into the measurement of financial capability and evaluate the financial capability of entrepreneurs based on micro-level data. Second, this article further investigates the mediating effects of the various factors by which financial capability affects entrepreneurial outcomes. Third, the current study reveals that effects of financial capability on entrepreneurial performance are heterogeneous based on the different entrepreneur types from an industrial perspective.

The remainder of this article is organised as follows: Section 2 describes the research hypotheses; Section 3 presents the research data; Section 4 reports the main empirical findings; and Section 5 discusses the conclusions and policy implications.

2. Literature review

The topic of financial capability has been receiving increasing interest among academics (Atkinson et al., Citation2006; O’Donnell & Keeney, Citation2009; Sherraden, Citation2013; Xiao et al., Citation2015; Friedline & West, Citation2016; Millimet et al., Citation2018; Nam & Loibl, Citation2021; Khan et al., Citation2022). Several studies have shed light on the definition and measurement of financial capability. Using survey data from the Financial Services Authority (F.S.A.) in Britain, Atkinson et al. (Citation2006) initially proposed the concept of financial capability, which emphasised the importance of financial literacy. Building on Atkinson et al.’s definition (2006), scholars began emphasising the role of financial behaviours when discussing the concept of financial capability. A strand of literature has defined financial capability as ‘a combination of awareness, knowledge, skills, attitudes and behaviours necessary to make sound financial decisions and ultimately achieve individual financial well-being’ (Robb & Woodyard, Citation2011; Taylor, Citation2011; Xiao et al., Citation2015; Caplinska & Ohotina, Citation2019). Without adaptive behaviours, people may find it difficult to achieve financial literacy. Additionally, significant attention has been paid to the external financial environment in last decade. Several studies have argued that the financial conditions and settings are critical components of financial capability. In other words, if people have the necessary information and knowledge about financial products and services but cannot access them, then those services and products will be underutilised (Huang et al.,Citation2015; Tan & Peng, Citation2019).

Considering the significance of financial capability to the outcomes of entrepreneurial activities, the relationship between financial capability and entrepreneurial performance has been a public policy concern. However, previous literature has mainly concentrated on the interaction between financial literacy and entrepreneurship decisions, or the association between financial literacy and entrepreneurial performance (Yin et al., Citation2015; Li & Yu, Citation2018; Oggero et al., Citation2020; Burchi et al., Citation2021). Ćumurović and Hyll (Citation2019) and Li and Qian (Citation2020) explored the role of financial literacy on entrepreneurial decisions and outcomes; they found that financially literate individuals are more efficient in acquiring and processing fundamental information regarding financial issues, have better opportunities to finance their ventures and are more willing to take risks. Additionally, many scholars have argued that financial literacy is an intangible human resource, which helps to manage business finances and acquire tangible financial resources, and has significantly positive effects on entrepreneurial performance (Yin et al., Citation2015). Thus, as a concept extended from financial literacy, financial capability could not only optimise entrepreneurs’ choice of borrowing channels, increase effective credit demand and ease liquidity constraints, but also promote entrepreneurial decision-making and management level, which plays a substantial role in business operation outcomes. Accordingly, financial capability could play a greater role in entrepreneurial performance than financial literacy, theoretically.

Hypothesis 1: As a kind of human capital, including financial literacy, financial behaviours and the financial environment, financial capacity can promote entrepreneurial performance.

Similarly, discussion on the mechanism between financial capacity and entrepreneurial performance also focused on the mediating roles through which financial literacy improves entrepreneurial performance in the previous literature (Su & Kong, Citation2019; Song et al., Citation2020). Clearly, investment is necessary to launch a new venture, accordingly, liquidity constraint is one of the difficulties entrepreneurs faced. Entrepreneurs with financial literacy would make better use of borrowing opportunities and obtain credit form informal and formal financial institutions, which eases their liquidity to a large extent. Consequently, entrepreneurs are able to introduce equipment, employ labour and transfer land without limit, thereby promoting entrepreneurial performance including revenue, profit and so on (Zhang et al., Citation2021). As stated above, financial literacy could not function well without proper behaviours and good environment, hence, the effects of financial capability on entrepreneurial performance need to explore in depth. However, little attention has been paid to the mechanism between financial capacity and entrepreneurial performance.

Entrepreneurship is the process of launching a new venture or recombining the existing production model. Therefore, outcomes of entrepreneurial activities mainly depend on the quantity and efficiency of productive factors like technology, labour, and land. However, without adaptive financial capability, entrepreneurs may find it hard to obtain and make full use of these necessary factors (Luo et al., Citation2021). On the one hand, entrepreneurs with proper financial capability could get more accesses to formal and informal credit and mitigate liquidity constraints, which ensures that they would invest enough money to labour, land and equipment, thereby realising optimal production scale. On the other hand, financial capability could also promote the efficiency of the above factors (Zhang et al., Citation2021). A financially capable entrepreneur can create an appropriate budget to meet the expenditure of aforementioned productive factors and allocate them effectively based on the market situation, improving the performance of business indirectly (Struckell et al., Citation2022). In summary, production expansion behaviours such as technology adoption, labour employment and land transfers may serve as intermediaries between financial capability and entrepreneurial performance.

Hypothesis 2: Financial capability improves entrepreneurial performance through production expansion behaviours such as technology adoption, labour employment and land transfers.

3. Methodology

3.1. Data

The data used in this study was obtained from the C.H.F.S. conducted by the Survey and Research Center for China Household Finance of Southwestern University of Finance and Economics in 2013, 2015 and 2017. The survey collected samples from more than 25 provinces (municipalities, autonomous regions), 80 counties and 320 communities. The survey collects household information on financial literacy, financial behaviours, financial environment, entrepreneurial performance and demographic characteristics. Building on earlier works (Cheng & Luo, Citation2009; Zhang et al., Citation2013), we define entrepreneurial farmer (E.F.) as a household who is registered in rural areas while starting business in the industrial and commercial sectors, or operating farms more than 50 mu in size. Additionally, we define the former as non-agricultural entrepreneurial farmer (N.E.F.) and the latter as agriculture-related entrepreneurial farmer (A.E.F.). According to our definitions, this article selected 1,046 E.F.s who participated in three surveys continuously among all households. Specifically, there are 722 N.E.F.s and 324 A.E.F.s. The data on entrepreneurial environment comes from China Statistical Yearbook issues 2014, 2016 and 2018. The summary statistics of these variables are presented in .

Table 1. Definitions and statistic features of variables.

3.2. Model

We utilised the following model to examine the effects of financial capability on entrepreneurial performance:

(1)

(1)

where,

represents entrepreneurial performance. Revenue, profit and success were selected as dependent variables to proxy for entrepreneurial performance from the scale, profitability and sustainability perspectives.

represents financial capability and was measured using a composite index that included financial literacy, financial behaviours and financial environment based on the entropy method.

is a vector of the control variables. We utilised demographic, household and environmental characteristics as control variables. Specifically, the demographic characteristics included the householders’ gender, age, marital status and risk appetite. The household characteristics comprised family participants and political status, while the environmental characteristics were measured by the number of enterprises.

is error term that obeys the normal distribution.

Since the empirical data was the balanced panel data in the third period, the Hausman test was conducted to determine which model should be employed in this study. The p value was 0.00, significantly rejecting the null hypothesis that the independent variables are not correlated with the residuals. Hence, the fixed effect model was adopted in this study to examine the effects of financial capability on entrepreneurial performance.

3.3. Descriptive statistics

3.3.1. Measurement of financial capability

Earlier works measured financial capability mainly from the perspectives of financial literacy (Atkinson et al., Citation2006; Lusardi, Citation2011; Taylor, Citation2011; Xiao et al., Citation2014). However, as stated above, more and more studies highlighted the importance of financial behaviours and financial environment. Therefore, we define financial capability as a combination of financial literacy, financial behaviours and financial environment and then measure it by means of entropy method. The financial capability index is constructed based on questionnaires about financial knowledge, education, insurance, payment, asset allocation and availability of formal and informal credit. shows the measurement of the financial capability index.

Table 2. Measurement of Financial Capability Index.

3.3.2. Financial capability of entrepreneurial farmers

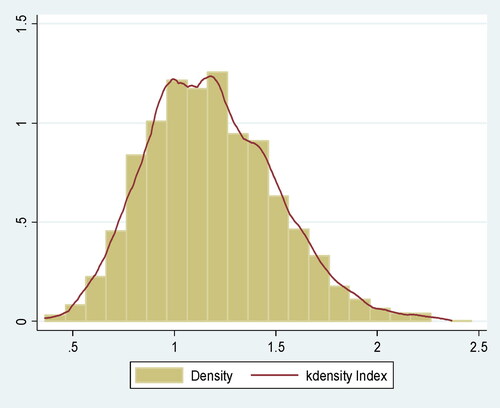

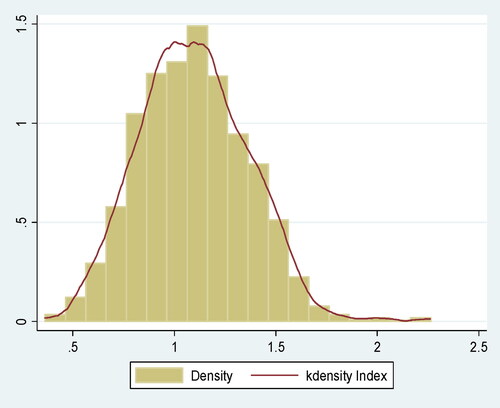

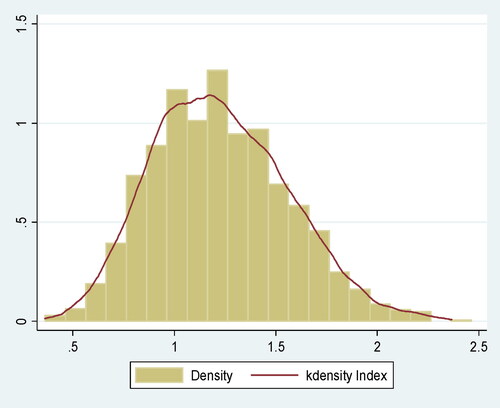

The distribution of financial capability index is summarised in . It has a mean of 1.22 and varies between 0.22 and 9.82. Higher index indicates higher financial capability. Although the distribution has a long right tail, the majority of observations actually lie between 0.5 and 2. Additionally, and plot the financial capability index distribution of A.E.F.s and N.E.F.s, average financial capability index of the former and the latter are 1.08 and 1.26 respectively. By extension, although the distribution of the two types of farmers is similar, average financial capability index of the latter is 16.98% bigger than the former.

Figure 1. Financial capability distribution of E.F.

Source: Author's Calculated.

Figure 2. Financial capability distribution of A.E.F.

Source: Author's Calculated.

Figure 3. Financial capability distribution of N.E.F.

Source: Author's Calculated.

3.3.3. Financial capability and entrepreneurial performance

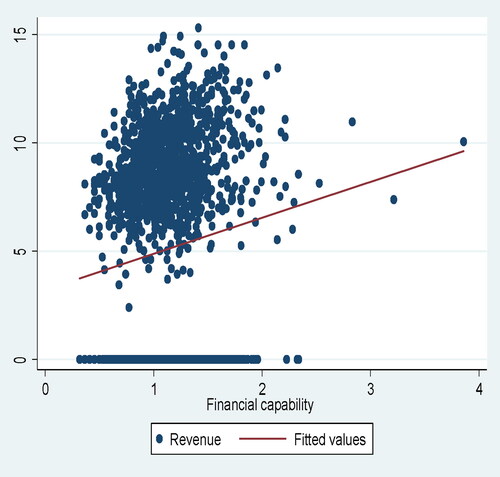

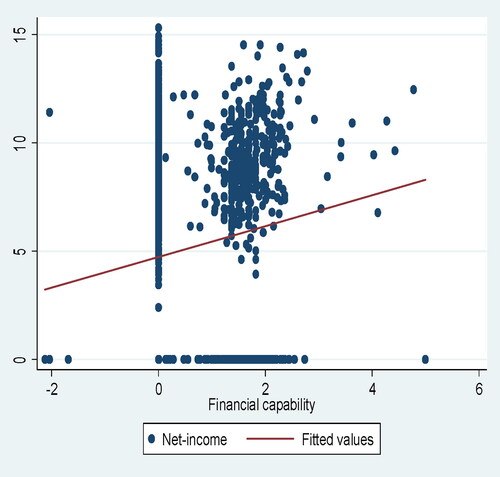

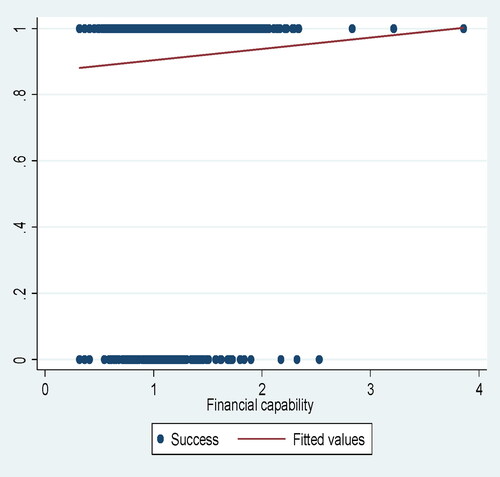

Simple scatterplots are shown in , which illustrates that financial capability has a clearly positive relationship with revenue, profit and success, indicating that financial capability could promote the performance of entrepreneurial activities. In other words, financial capability fosters the entrepreneurial performance from the perspectives of scale, profitability and sustainability.

Figure 4. Financial capability and revenue.

Source: Author's Calculated.

Figure 5. Financial capability and profit.

Source: Author's Calculated.

Figure 6. Financial capability and success.

Source: Author's Calculated.

4. Empirical Results

4.1. Baseline regression

reports the baseline regression results. As shown in columns 1–3, the regression coefficients of capability on revenue, profit and success are significantly positive at a magnitude of 1.16, 1.45 and 0.25, which indicates that financial capability significantly promotes entrepreneurial performance. With stronger financial capability, E.F.s can introduce more advanced technology, hire more labour and transfer in more land, thereby increasing operating income and net income. Hence, hypothesis 1 is supported.

Table 3. The effects of financial capability on entrepreneurial performance.

Regarding the control variables, risk appetite has significantly positive effects on entrepreneurial performance. There is a positive relationship between risk appetite and entrepreneurship. Stronger risk appetite is associated with stronger entrepreneurship and better entrepreneurial outcomes. Number of family participants has significantly positive effects on revenue, profit and success, the more family participants involve in entrepreneurial activities, the higher the output and less labour cost will be, which ensures more profit. Additionally, more family participants may lead the decisions more rationally and raise the success rate of entrepreneurial activities. Entrepreneurial environment has significantly positive effects on entrepreneurial performance. A good entrepreneurial environment will facilitate the spillover effects of technology and capital, so as to expand scale, increase profitability and enhance sustainability of entrepreneurship.

4.2. Heterogeneity results

Given the differences in returns and risks between the agricultural sector and the non-agricultural sector, the effects of financial capability on entrepreneurial performance are probably heterogeneous for A.E.F.s and N.E.F.s. This sub-section examines the heterogeneous impacts of financial capability on entrepreneurial outcomes based on entrepreneur types. For this purpose, the sample was divided into two categories, i.e., A.E.F.s and N.E.F.s. The regression results are presented in .

According to the regression results for N.E.F.s, reported in Columns 4–6, the coefficients of revenue, profit and success were 1.31, 1.97 and 0.38, respectively, which were all significantly positive. In contrast, the corresponding coefficients of A.E.F.s were 0.80, 0.93 and 0.19, respectively. These results suggest that financial capability can improve the entrepreneurial performance of both types of farmers, while the marginal effect of financial capability is greater for the former rather than the latter. The possible explanations for this finding are as follows. First, from a financial literacy perspective, N.E.F.s tend to possess more financial knowledge as they operate in non-agricultural sectors and have more frequent dealings with financial institutions. Second, from a financial environment perspective, due to the binary structure of finance, the financial development in urban areas is relatively higher than in rural areas, indicating the presence of more financial institutions and financial assets in urban areas. Since N.E.F.s typically operate their businesses in urban areas, they can obtain financial resources much easier than A.E.F.s. Third, from a financial behaviour perspective, N.E.F.s can obtain credit more easily as they have more assets to mortgage.

4.3. Endogeneity

The empirical results may indicate the presence of endogeneity arising from missing variables or reverse causality. In other words, the results may indicate that entrepreneurial performance has a reverse effect on financial capability. To address this concern, we take the highest educational level of parents (discrete variable from 1 = No schooling at all to 9 = Doctoral degree) as the instrumental variable. According to Yin et al. (Citation2014), respondents can learn from their parents to improve their basic computing skills and understandings of economics and financial knowledge. Therefore, educational level of parents will influence the respondent’s financial capability directly. However, there was no direct connection between the educational level of parents and the entrepreneurial outcomes of the respondents. The two-stage-least-squares (2.S.L.S.) method was utilised to regress the models with revenue and profit as their dependent variables since these variables are discrete. Furthermore, the instrumental variable probit (Ivprobit) was utilised to regress models with successful dependent variables as it is a dummy variable.

As shown in , the values of the Wu-Hausman endogeneity tests rejected the null hypothesis, indicating that there is an endogeneity problem for financial capability. Moreover, in the first-stage regression, the t values of the instrumental variable were 4.55, 4.21, 4.27, 4.56, 4.39, 4.63, 4.57, 3.49 and 4.22, respectively, which were all significantly positive at the 1% level, suggesting that the instrumental variable was exogenous. The F values during the first-stage regression were 20.82, 19.15, 25.78, 27.85, 25.77, 26.98, 38.16, 31.17 and 34.88, respectively, indicating that there was no weak instrumental variable problem. After introducing the IV, the coefficients of financial capability were still significantly positive, indicating that the effects of financial capability on entrepreneurial performance were robust in terms of endogeneity.

Table 4. The effects of financial capability on entrepreneurial performance: IV regressions.

4.4. Mechanism results

As mentioned in Section 2, financial capability improves entrepreneurial performance through production expansion behaviours such as technology adoption, labour employment and land transition. However, the operation models of N.E.F.s and A.E.F.s are different, land is an essential but unnecessary factor for the former. In view of this, we discuss mediating effects of N.E.F.s and A.E.F.s respectively in this article. To test the mediating effect, we applied the following models:

(2)

(2)

(3)

(3)

(4)

(4)

where,

represents entrepreneurial performance,

represents financial capability,

is a vector of the mediating variables,

is a vector of the control variables and

is error term which follows a normal distribution.

4.4.1. Mediating effect of N.E.F.s

presents the regression results of the mediating effect test for N.E.F.s. The results obtained when technology was selected as mediating variable are shown in Columns 1–4. The results in Column 1 show that the coefficient of capability was 0.32, indicating that financial capability leads to the increasing adoption of technology by N.E.F.s. After adding technology, the coefficients for revenue, profit and success were significantly positive at the magnitudes of 0.97, 1.01 and 0.08, respectively. Additionally, these coefficients were lower than their corresponding values in , suggesting that technology has a certain mediating effect on the relationship between financial capability and entrepreneurial performance. This mediating effect was estimated according to Mackinnon et al. (Citation1995) study. The results indicate that the effects of technology as a mediating variable on revenue, profit and success were 25.72%, 26.36% and 21.87%, respectively.

Table 5. Mediating effect of N.E.F.s.

Columns 5–8 report the regression results when labour was selected as a mediating variable for the relationship between capability and entrepreneurial performance. The results in Column 5 show that the coefficient of capability was 0.45, indicating that financial capability increases the employment of labour by N.E.F.s. After adding labour, the coefficients of revenue, profit and success were significantly positive at 1.05, 1.12 and 0.21, respectively. These coefficients were lower than their corresponding values in , suggesting that labour has a certain mediating effect on the relationship between financial capability and entrepreneurial performance. Additionally, the mediating effects of labour on revenue, profit and success were found to be 33.01%, 29.27% and 25.53%, respectively.

4.4.2. Mediating effect of A.E.F.s

reports the regression results of mediating effect test of A.E.F.s, the effects of capability when technology is selected as mediating variable for entrepreneurial performance are shown in columns 1–4. The result in column 1 shows that the coefficient of capability is 0.46, indicating that financial capability increases technology adoption of A.E.F.s. After adding technology, the coefficients of capability on revenue, profit and success are significantly positive at a magnitude of 0.65, 0.76 and 0.07, respectively. Additionally, the coefficients are lower than the corresponding values in , suggesting that technology has a certain mediating effect. Furthermore, the mediating effects of revenue, profit and success are significantly positive at a magnitude of 21.19%, 27.28% and 34.45%, respectively.

Table 6. Mediating effect of A.E.F.s.

Columns 5–8 report the regression results of capability when labour is selected as mediating variable for entrepreneurial performance. The results in column 5 show that the coefficient of capability is 0.28, indicating that financial capability increases labour employment of A.E.F.s. After adding labour, the coefficients of capability on revenue, profit and success are significantly positive at a magnitude of 0.61, 0.88 and 0.08, respectively. Moreover, the coefficients are lower than the corresponding values in , suggesting that labour has a certain mediating effect. Additionally, we further compute the mediating effect of labour, the results are 16.16%, 17.57% and 23.95%, respectively.

Columns 9–12 present the regression results of capability when land is selected as a mediating variable for entrepreneurial performance. The results in Column 9 show that the coefficient of capability was 0.26, indicating that financial capability increases the transfer of land by A.E.F.s. After adding the variable land, the coefficients of revenue, profit and success were significantly positive at magnitudes of 0.59, 0.83 and 0.05, respectively. Moreover, these coefficients were lower than their corresponding values in , suggesting that land has a certain mediating effect on the relationship between financial capability and entrepreneurial performance. Additionally, the results for the mediating effect of land on revenue, profit and success were 13.62%, 14.01% and 26.68%, respectively. The results in sections 4.4.1 and 4.4.2 show that financial capability improves the entrepreneurial performance of A.E.F.s and N.E.F.s via technology, labour and land. First, entrepreneurs with a stronger financial capability face less liquidity constraints, which allows them to introduce technologies that can boost production efficiency. These findings are consistent with those of Hastings et al. (Citation2013). Second, entrepreneurs with a stronger financial capability can hire more labour and transfer more land by obtaining credit, thus expanding the scale of their operations. Third, entrepreneurs with a stronger financial capability can employ these three factors (i.e., technology, labour and land) more effectively. Therefore, the entrepreneurial outcomes for entrepreneurs with strong financial capabilities are better than those for entrepreneurs with weaker financial capability; this finding is consistent with Yin et al. (Citation2015) results. Hence, hypothesis 2 is supported.

5. Conclusions

Entrepreneurship is a systematic process that includes decision-making regarding investment, financing and risk management. Therefore, entrepreneurs’ financial literacy, financial behaviours and financial environment are essential for the successful operation of entrepreneurial businesses. Based on C.H.F.S. data for the years 2013, 2015 and 2017, this article researched the relationship between financial capability and entrepreneurial performance. First, the effect of financial capability on entrepreneurial outcomes was examined. Second, the heterogeneous effects of financial capability on both A.E.F.s and N.E.F.s were analysed. Finally, the mediating effects of production expansion were investigated.

The results revealed that financial capability can facilitate entrepreneurial performance. This conclusion was robust in consideration of the endogeneity. Moreover, the marginal effect of financial capability on entrepreneurial performance was greater for N.E.F.s than for A.E.F.s. A possible reason for this finding is the presence of industrial heterogeneity. Additionally, financial capability was found to improve the performance of N.E.F.s through technology adoption and labour employment, while facilitating the performance of A.E.F.s through technology adoption, labour employment and land transfers.

These findings have valuable implications for policymakers. For countries in transition like China, the first priority should be enhancing he financial literacy of entrepreneurs. The government should enhance entrepreneurs’ financial knowledge and their skills in managing financial resources via financial education. These initiatives should be more focused in rural areas since the entrepreneurs in these areas usually lack these capabilities. Additionally, the financial environment should also be optimised by introducing more financial institutions and assets in rural areas.

Furthermore, considering that financial capability has a significantly lower marginal effect on entrepreneurial performance for A.E.F.s than for N.E.F.s, policymakers should pay more attention to promoting the financial capabilities of A.E.F.s, especially considering the background that developing countries like China seek to achieve urban-rural integration in the foreseeable future. Additionally, initiatives to subsidise A.E.F.s’ loans and the price of their products should also be implemented.

Finally, the results of mediating effect test imply that financial capability improves entrepreneurial performance via technology, labour and land. Therefore, financial institutions should consider combining the provision of credit with these factors. For example, financial institutions can design financial products to facilitate entrepreneurs’ introduction of equipment, labour employment and land transfers.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1 According to Schumpeter (Citation1912), entrepreneurship is defined as the process of launching a new venture or recombining the existing production model.

References

- Atkinson, A., McKay, S. D., Kempson, H. E., & Collard, S. B. (2006). Levels of financial capability in the UK: Results of a baseline survey (Consumer Research 47). Financial Services Authority. http://www.fsa.gov.uk/pubs/consumer-research/crpr47.pdf

- Burchi, A., Włodarczyk, B., Szturo, M., & Martelli, D. (2021). The effects of financial literacy on sustainable entrepreneurship. Sustainability, 13(9), 5070. https://doi.org/10.3390/su13095070

- Caplinska, A., & Ohotina, A. (2019). Analysis of financial literacy tendencies with young people. Entrepreneurship and Sustainability Issues, 6(4), 1736–1749. https://doi.org/10.9770/jesi.2019.6.4(13)

- Cheng, Y., & Luo, D. (2009). Farmers’ entrepreneurial choice under credit constraint: An empirical analysis based on Chinese farmers’ survey. Chinese Rural Economy, 299(11), 25–38. (in Chinese).

- Ćumurović, A., & Hyll, W. (2019). Financial literacy and self-employment. Journal of Consumer Affairs, 53(2), 455–487. https://doi.org/10.1111/joca.12198

- Friedline, T., & West, S. (2016). Financial education is not enough: Millennials may need financial capability to demonstrate healthier financial behaviors. Journal of Family and Economic Issues, 37(4), 649–671. https://doi.org/10.1007/s10834-015-9475-y

- Hastings, J. S., Madrian, B. C., & Skimmyhorn, W. L. (2013). Financial literacy, financial education, and economic outcomes. Annual Review of Economics, 5(1), 347–373. https://doi.org/10.1146/annurev-economics-082312-125807

- Huang, J., Nam, Y., & Lee, E. J. (2015). Financial capability and economic hardship among low-income older Asian immigrants in a supported employment program. Journal of Family and Economic Issues, 36(2), 239–250. https://doi.org/10.1007/s10834-014-9398-z

- Khan, K. A., Çera, G., & Pinto Alves, S. R. (2022). Financial capability as a function of financial literacy, financial advice, and financial satisfaction. E + M Ekonomie a Management, 25(1), 143–160. https://doi.org/10.15240/tul/001/2022-1-009

- Klychova, G. S., Fakhretdinova, E. N., Klychova, A. S., & Antonova, N. V. (2015). Development of accounting and financial reporting for small and medium-sized businesses in accordance with international financial reporting standards. Asian Social Science, 11(11), 318–322. https://doi.org/10.5539/ass.v11n11p318

- Li, R., & Qian, Y. (2020). Entrepreneurial participation and performance: The role of financial literacy. Management Decision, 58(3), 583–599. https://doi.org/10.1108/MD-11-2018-1283

- Li, S., & Yu, W. C. (2018). Research on the mechanism of the impact of rural financial diversity on farmers’ entrepreneurship. Journal of Finance and Economics, 44(1), 4–19. (in Chinese).

- Luo, Y., Peng, Y., & Zeng, L. (2021). Digital financial capability and entrepreneurial performance. International Review of Economics & Finance, 76, 55–74. https://doi.org/10.1016/j.iref.2021.05.010

- Lusardi, A. (2011). Americans’ financial capability [No. w17103]. National Bureau of Economic Research. https://doi.org/10.3386/w17103

- Mackinnon, D. P., Warsi, G., & Dwyer, J. H. (1995). A simulation study of mediated effect measures. Multivariate Behavioral Research, 30(1), 41–62. https://doi.org/10.1207/s15327906mbr3001_3

- Millimet, D. L., McDonough, I. K., & Fomby, T. B. (2018). Financial capability and food security in extremely vulnerable households. American Journal of Agricultural Economics, 100(4), 1224–1291. https://doi.org/10.1093/ajae/aay029

- Nam, Y., & Loibl, C. (2021). Financial capability and financial planning at the verge of retirement age. Journal of Family and Economic Issues, 42(1), 133–150. https://doi.org/10.1007/s10834-020-09699-4

- O'Donnell, N., & Keeney, M. J. (2009). Financial capability: New evidence for Ireland (No. 1/RT/09). Dublin: Central Bank of Ireland.

- Oggero, N., Rossi, M. C., & Ughetto, E. (2020). Entrepreneurial spirits in women and men. The role of financial literacy and digital skills. Small Business Economics, 55(2), 313–327. https://doi.org/10.1007/s11187-019-00299-7

- Paulson, A. L., & Townsend, R. (2004). Entrepreneurship and financial constraints in Thailand. Journal of Corporate Finance, 10(2), 229–262. https://doi.org/10.1016/S0929-1199(03)00056-7

- Robb, C. A., & Woodyard, A. S. (2011). Financial knowledge and best practice behavior. Journal of Financial Counseling and Planning, 22(1), 60–70. https://files.eric.ed.gov/fulltext/EJ941903.pdf

- Schultz, T. W. (1964). Transforming traditional agriculture. The University of Chicago Press, Chicago.

- Schumpeter, J. (1912). The theory of economic development Cambridge. Harvard University Press.

- Sherraden, M. (2013). Building blocks of financial capability. Oxford University Press.

- Song, Q. Y., Wu, Y., & Y, Z. C. (2020). Impact of financial literacy on the survival of entrepreneurship. Science Research Management, 41(11), 133–142. (in Chinese). https://doi.org/10.19571/j.cnki.1000-2995.2020.11.013

- Struckell, E. M., Patel, P. C., Ojha, D., & Oghazi, P. (2022). Financial literacy and self employment – The moderating effect of gender and race. Journal of Business Research, 139, 639–653. https://doi.org/10.1016/j.jbusres.2021.10.003

- Su, L. L., & Kong, R. (2019). Financial literacy, entrepreneurial training and farmers’ entrepreneurial decision-making. Journal of South China Agricultural University (Social Science Edition), 18(03), 53–66. (in Chinese).

- Tan, Y. Z., & Peng, Q. R. (2019). Financial capability, financial decision and poverty. Economic Theory and Business Management, 2, 62–77. (in Chinese).

- Taylor, M. (2011). Measuring financial capability and its determinants using survey data. Social Indicators Research, 102(2), 297–314. https://doi.org/10.1007/s11205-010-9681-9

- Turvey, C. G., & Kong, R. (2010). Informal lending amongst friends and relatives: Can microcredit compete in rural China? China Economic Review, 21(4), 544–556. https://doi.org/10.1016/j.chieco.2010.05.001

- Xiao, J. J., Chen, C., & Chen, F. (2014). Consumer financial capability and financial satisfaction. Social Indicators Research, 118(1), 415–432. https://doi.org/10.1007/s11205-013-0414-8

- Xiao, J. J., Chen, C., & Sun, L. (2015). Age differences in consumer financial capability. International Journal of Consumer Studies, 39(4), 387–395. https://doi.org/10.1111/ijcs.12205

- Yin, Z. C., Song, Q. Y., & Wu, Y. (2014). Financial knowledge, investment experience and household asset selection. Economic Research Journal, 9(4), 62–75. (in Chinese).

- Yin, Z. C., Song, Q. Y., & Wu, Y. (2015). Financial knowledge, entrepreneurial decision and entrepreneurial motivation. Management World, 30(1), 87–98. (in Chinese).

- Zhang, L. Y., Yang, J., & Zhang, H. N. (2013). Financial development, family entrepreneurship and urban and rural residents’ income: An empirical analysis based on micro perspective. Chinese Rural Economy, 7, 47–57. (in Chinese).

- Zhang, Z. Y., & Shu, H. T. (2020). Can farmers’ entrepreneurship and financial service innovation achieve coordinated development. Journal of Southwest University (Social Sciences Edition, 46(2), 59–70+192. (in Chinese).

- Zhang, Z. Y., Shu, H. T., & Liu, R. M. (2021). Research on the mechanism of farmers’ financial literacy on entrepreneurship performance. Journal of Southwest University (Social Sciences Edition), 47(04), 117–128+229 (in Chinese). https://doi.org/10.13718/j.cnki.xdsk.2021.04.011.