?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to analyse the connection between energy efficiency and renewable energy consumption in the emerging seven (E7) economies during the period 1990–2020. This study also examines the impact of economic growth, carbon emissions and technological innovation on renewable energy. This study employs various panel data approaches that validate the irregular distribution of data and the heterogeneous slopes coefficients. The cross-section dependence test confirms that cross-section dependence is present in the study variables. While these variables are cointegrated. Using non-parametric panel data approaches, the moments' quantile regression results unveil that economic growth is positively associated with renewable energy in all quantiles. Whereas energy efficiency and carbon emissions showed mixed results, negatively affect renewable energy consumption in the lower quantiles, insignificant in the medium quantiles and positive in the higher quantiles. On the other hand, technological innovation is found negatively related to renewable energy consumption. Bidirectional causal association is found between explanatory variables and renewable energy consumption. Based on the empirical findings, this study suggests policies to divert economic growth from fossil fuel energy consumption, enhancing investment in the renewable energy sector, promoting energy efficiency and investment in environmental-related technologies to promote renewable energy.

1. Introduction

Energy is a critical source for industrial and residential sectors development, and it must be utilised efficiently, with minimal damage to the environment, even at the minimum expense (Abeykoon et al., Citation2021). Economic progress has always been linked to rising energy utilisation and pollution emissions, resulting in substantial environmental consequences and a strong reliance on fossil fuels (Qudrat-Ullah et al., Citation2021). There has been a growing risk to the environment in recent times, particularly in light of the already noticeable rise in global temperatures. As a result of such increased environmental issues, technical advancements in natural resources utilisation for energy have arisen and their accessibility to all productive economic and manufacturing sectors (Renna & Materi, Citation2021). In other words, economies across the globe are targeting renewable energy investment, production and consumption to tackle the issue of climate change and environmental degradation (Jiang et al., Citation2022; Luan et al., Citation2022). The attention of governments and policy-makers towards renewable energy generation and consumption attract the scholarly attention towards the exploration of the critical factors affecting renewable energy consumption. Following the trend, this study also tends to discover the influential factors affecting renewable energy in the emerging economies since these economies are struggling to achieve sustainable development via expanding production and industrial sector.

At all stages, energy conservation, appropriate energy usage and effective utilisation of power sources are critical. The necessity of energy conservation and efficiency methods is demonstrated because of the need to cut energy bills, reduce energy dependency on other economies of the globe, reduce pollution emissions and the procurement of emissions right to the Kyoto Protocol commitments. Energy efficiency, which includes household, industrial and governmental energy savings, is vital for countries worldwide to fulfil their respective climate change and energy objectives (la Cruz-Lovera et al., Citation2017). Energy efficiency is still the most cost-effective way to accomplish national climate change targets. Energy efficiency is a critical strategy for achieving carbon-free economic growth and mitigating environmental change. This can be described as using less energy to produce a similar quantity of output (Akram et al., Citation2020). Since energy efficiency initiatives have a great potentiality in reducing carbon (CO2) emissions, economies are curious about the link between energy efficiency and economic growth. Energy efficiency is a priority for underdeveloped countries, particularly to meet the development needs of energy usage to develop their economies (Cantore et al., Citation2016).

Energy consumption (particularly for fossil fuels) has grown rapidly in recent years (Al-Mulali et al., Citation2015), and is expected to continue to expand at a rate of 48% from 2017 till 2040. (World Energy Outlook (WEO), Citation2017). Since developing economies rely heavily on fossil fuels to attain fast economic growth, these nations are considered responsible for most of the increase in energy consumption. For instance, the emerging seven economies are responsible for a major portion of the global economy and environmental degradation. Some of these emerging economies, such as China and India are among the top pollution emission economies globally. As these economies have paid more attention to economic growth, it is expected that these economies will account for 152,617 billion dollars in 2050. Beside the fact that these economies have paid less attention to environmental sustainability, yet initiatives have been taken to reduce emissions via adopting energy efficiency, renewable energy consumption, and technological innovations as tools. Whereas the literature covers such aspects of renewable energy, energy efficiency and technological innovation regarding its economic and environmental impacts. What captures the idea of this paper is whether any association exists between energy efficiency and renewable energy? Which is noted as relatively ignored in the existing literature. Besides, the existing literature covers the association of technological innovation and carbon emissions with that of economic growth. Still, they ignored the possible factors that influence renewable energy consumption, which is an important indicator of sustainable environment and substitute for traditional energy resources. Therefore, it is crucial to discover the significant factors affecting renewable energy consumption. Empirical results of this study will open the doors for a new debate among the scholars regarding the discoveries of factors helping renewable energy growth.

The primary objective of this study is to analyse the association between energy efficiency and renewable energy consumption in emerging economies. Since the academic literature is extensive regarding the influence of renewable energy and energy efficiency on environmental quality. Still it lacks empirical evidence regarding the association between these two (energy efficiency and renewable energy consumption) variables. Therefore it is crucial to analyse the specific influence as well as the causal nexus between the two. In addition, this study also aims to reinvestigate the association between economic growth and renewable energy consumption. Although, the literature provides empirical results along with the policy suggestions. Yet, this study noted contradictory findings regarding the said association, which requires further empirical evidence for valid policy implications. Furthermore, the empirical estimates regarding the influence of Renewable Energy on CO2 emissions are already discovered by many studies as mentioned in the literature. However, no study is found that could consider the impact of CO2 emissions on renewable energy consumption in any region, which is an important factor in achieving carbon neutrality. The last objective of this study is to examine the nexus of technological innovation and renewable energy consumption. Although the scholars and policy-makers are well-known of the substantial effects of technological innovation in various economic and environmental indicators. Yet, this study tends to explore the influence of tech-innovation on the indicator of energy as well.

Following the persistent research gap and objectives of the study stated above, this study plays a vital and pioneering role regarding the exploration of nexus between energy efficiency and renewable energy consumption, which is a novel contribution to the existing literature. Since the governments and policy-makers have established policies that are targeting environmental sustainability, and promoting energy efficiency as well as renewable energy consumption. Thus, the empirical results could help authorities to take serious and appropriate steps towards environmental sustainability and renewable energy promotion. Concerning economic growth and renewable energy nexus, the existing empirical results provide contradictory results, which could adversely affect the economy and could be harmful for the policy construction regarding renewable energy production, consumption and implementation. Therefore, the empirical results of this study could provide a clear path for the policy-makers in emerging countries that could lead them towards sustainable development. Furthermore, this study is also significant in terms of discovering the mostly overlooked question of whether carbon emissions plays any role in renewable energy consumption. Which is one of the novel contribution of this study and could open the doors for a new debate in the academic. Moreover, the studies have empirically investigated the impact of technological innovation on environmental quality and economic growth. Still, the literature lacks empirical evidence regarding the impact of technological innovation on renewable energy. Hence, this study as a while, is a novel contribution to the existing literature that provides innovative and appropriate policy implications for scholars and decision-makers.

The rest of the paper is organised in the following four sections: Section 2 presents relevant literature review; Section 3 depicts data and the methodology adopted for empirical analysis; Section 4 shows empirical estimates and discussion on the results; Section 5 portrays conclusion and policy Implications.

2. Literature review

Since the last few decades, the issue of climate change, global warming and environmental degradation is on the rise, which attracts the scholarly and policy level attention to construct and implement policies to achieve low carbon economy. Specifically, natural resources are the one that are used for running industrial sector and economic activities, which have a substantial influence on economic growth of the country (Rahim et al., Citation2021). However, the economic growth further expand the industrial production, which demands more energy and pollute environment (Qin, Raheem, et al., Citation2021). Apart from economic, there are various financial and energy related factors that causes increase in the environmental degradation, which are also harmful to human health (Cai et al., Citation2022; Wei et al., Citation2022). As a result, scholars have suggested that renewable energy generation, environmental related taxes, investment in energy industry and environmental related research and development to tackle the issue of increased pollution and enhance renewable energy use for environmental sustainability (Jiang et al., Citation2022; Luan et al., Citation2022; Qin, Hou, et al., Citation2021; Shahzad et al., Citation2021).

2.1. Relationship between renewable energy and energy efficiency

Prevailing literature on energy efficiency and renewable energy association is very scarce. However, to evaluate the association between efficient energy and renewable energy, it is obligatory to know energy efficiency? According to the Environmental and Energy study institute (EESI),Footnote1 Energy efficiency is termed as utilising less energy to do the same task that helps reduce carbon emissions and costs on the domestic and worldwide level. Renewable energy sources can acquire an efficient form of energy. The energy demand is on the increase to meet the development needs and welfare of the people. As climate change is a hazard to global development, the world can be environmentally friendly if the energy sources are converted to a renewable form of energy (Riti & Shu, Citation2016). Increasing the efficient forms of energy use such as conversion to renewable energy reduces dependence on fossil fuel and its hostile consequences on the environment. Several policy analysts preferred that energy efficiency is necessary for eliminating externalities. It will also reduce pollution emissions that cause climate change (Vine, Citation2008). Bayar and Gavriletea (Citation2019) investigated that energy efficiency and renewable energy have an inverse association with carbon dioxide emissions and affect economic growth in the short-run (Ponce & Khan, Citation2021). The practices for energy efficiency are the portion of sustainable energy policy, whereas renewable energy and energy efficiency are binary pillars of sustainable policy. Gielen et al. (Citation2019) recommended that both are necessary and their synergies are essential. Energy efficiency is required to sluggish the energy demand growth that breaks fossil fuel usage, which is the mainstay of development in several underprivileged economies. Specific energy efficiency standards can be adopted to stimulate growth, climate mitigation, and renewable energy consumption (Geller et al., Citation2004). Riti and Shu (Citation2016) suggested that energy-efficient products are necessary for an eco-friendly environment. The energy efficiency and renewable energy initiatives have both direct and indirect benefits to the economy. It will stimulate investment opportunities, create employment opportunities, enhance people's health, and increase productivity in the economy (EPA, Citation2018).

2.2. How do carbon emissions and economic growth influence renewable energy?

The connection between carbon emissions, economic growth and renewable energy has gained much attention from world researchers and analysts over the years due to global warming and its harmful impacts on this planet. Interest has been increased theoretically and empirically. Predominant literature on this field can be classified into three groups for a better and clear understanding of the topic. First, there will be some casual association between economic growth and renewable energy consumption, while the second would be related to the relationship between carbon emissions and renewable energy consumption. Third, the last but not least would be on combined abovementioned associations to detect the links among carbon emissions, economic growth and renewable energy.

For the association between economic growth and renewable energy consumption, the studies like Mardani et al. (Citation2019), and Acaravci and Ozturk (Citation2010) found that there is bi-directional causality between the growth of the economy and renewable energy consumption. Further, the positive and significant association is due to increasing capital formation (Chien & Hu, Citation2008). Bhattacharya et al. (Citation2016) applied renewable energy attractive index for 38 energy consumption countries to determine the relation. Their panel findings indicated a positive influence of renewable energy on economic growth. For the subsequent group, studies like Gielen et al. (Citation2019), Ponce and Khan (Citation2021), Omri and Nguyen (Citation2014) and Chen et al. (Citation2019) investigated that carbon and renewable energy have a negative association between them. CO2 emissions are the chief cause of renewable energy consumption. Technologies made with renewable technologies (i.e., solar PVs) will be fruitful in reducing emissions as they can become a key element in reducing GHG and carbon emissions. Lastly, the combined associations among carbon emissions, economic growth and renewable energy are mentioned. For instance, Padhan et al. (Citation2020) examined the impact of GDP, oil price and CO2 emissions on renewable energy consumption for 30 ‘Organization of Economic Cooperation and Development (OECD)’ economies. Their empirical findings suggest that GDP and carbon emissions affect renewable energy consumption while oil prices affect energy consumption over the influence of fossil fuels. They have a long-run association among the variables. Precisely, the real GDP income, carbon emissions and renewable consumption have a significantly positive relationship. Due to economic globalisation increase in the use of advanced technology ultimately leads to an increase in renewable energy consumption. Likewise, Antonakakis et al. (Citation2017) examined intense response function in 106 countries from 1971 to 2011. They applied panel autoregression and the outcomes revealed causality between renewable energy consumption and economic growth i.e., bidirectional, which is due to the presence of feedback theory behind it. The feedback theory relates to the bi-directional causality of renewable energy consumption and the growth of the economy (GDP). They discovered that augmented economic growth leads to increasing GHG emissions. Furthermore, renewable energy consumption can also promote economic growth more sustainably. The outcomes of the aforementioned research can be dissimilar due to differences in sample periods of different countries, including different econometric techniques for estimating. Governments, energy institutions and agencies require efficiency for low carbon-growth economies internationally for sustainable economic and environmental development. Apart from the discussion regarding the factors affecting renewable energy consumption, some pf the recent studies explored the factors affecting energy demand. Specifically, Fang et al. (Citation2021) utilised the augmented mean group estimator and asserted that economic growth is a substantial factor that enhance energy demand in the OECD economies during 1978–2016. However, it is economic complexity and real energy prices that exhibit negative impact on the energy demand of the said region. In the same line, Lu et al. (Citation2021) reveals that young age dependency, overall age dependency and urbanisation reduces energy demand in BRICS economies. Whereas, economic growth and old age dependency substantially enhances energy demand for both renewables and non-renewables. In case of Saudi Arabia, Mahalik et al. (Citation2017) discovered the inverted U-shaped association between financial development and energy demand. On the contrary to earlier studies, this studies reveal that economic growth adversely, whereas capital and urbanisation are the significant factor of increased energy demand. In case of renewable energy, the study of Gozgor et al. (Citation2020) illustrates that per capita emissions, per capita income, urbanisation and oil prices significantly enhances its demand. Hence, the study suggested policies for improved economic growth and urbanisation to increase renewable energy demand.

2.3. Empirical shreds of evidence related to emerging economies

Salim and Rafiq (Citation2012) analysed the factors of renewable energy consumption in six world emerging economies. Their empirical findings suggested that there is a long-run association between renewable energy and income that is determined by emissions and income. Applying FMOLS, DOLS & Granger causality techniques, they recommended that increasing energy efficiency and renewable share can substantially reduce carbon emissions in emerging economies (Turkey, Brazil, Indonesia, China, Philippines and India). Khan et al. (Citation2019) examined green ideology in Asian emerging economies. Their outcomes revealed that very scarce literature is present on renewable energy and green ideology to resolve environmental concerns. Nibedita and Irfan (Citation2021) inspected the energy efficiency strategy in the case of the world's largest emerging economies. Their findings exposed that there is a negative long-run influence of diversity in energy, on energy efficiency. Moreover, they emphasised that increasing 1% of energy efficiency could condense emissions by at least 1.2%. Therefore, low carbon strategies are needed to be promoted in Russia, India, Brazil, China, Mexico, Indonesia and Turkey (emerging economies). In a predictive analysis of carbon emissions in another study of emerging economies like China, Brazil, South Africa and India, the authors claimed that these countries were the highest carbon emitter and severely susceptible countries to receive negative impacts of climate change. The empirical outcomes discovered that the intensity of emissions would be continued in these countries. Environmental green technology (renewable energy) might help reduce carbon emissions and attain economic growth goals alongside (Ahmed et al., Citation2020). An additional case of emerging economies, Rahman et al. (Citation2022), examined that carbon dioxide emissions are increasing due to higher consumption of energy, industrial activity and hasty globalisation. However, only one increase in renewable energy decreases 0.003 units of carbon intensity, concluding that green energies and technologies are a practicable solution for carbon reduction in emerging economies.

3. Data and methodology

3.1. Data and model specification

Based on the objectives and literature above, this study uses five variables: renewable energy consumption (REC) is the focus variable. While the main independent variable in this study is regarded as energy efficiency (ENEF). In addition, economic growth captured by gross domestic product (GDP), environmental quality represented via carbon (CO2) emissions and technological innovation are the secondary independent variables. These variables are collected from one source, covering the period from 1990 to 2020 for seven emerging (E7) economies, including Mexico, Brazil, China, Indonesia, Russia, Turkey and India. The primary reason behind the selection of emerging economies is that the progress of the E7 nations has been measured relative to the size of the G7 economies, which included many of the world's greatest countries in the 20th century. In 2011, it was expected that the E7 will have greater economies than the industrialised (G7) economies by 2020 (Dunkley, Citation2011). By 2014, the E7 economies had surpassed the G7 nations in terms of purchasing power parity (PPP) (Nadda et al., Citation2017). According to further estimates, the E7 represented 80% of the G7 by PPP in 2016 (Park, Citation2016). In 2016, it was anticipated that by 2030, the economies of the E7 will be greater than those of the G7 (Hodges, Citation2016). As per Xing (Citation2016), it is anticipated that by 2050, the E7 may be 75% bigger than the G7 in terms of PPP. Since the higher economic growth and income level tends the governments and general public to utilise environmentally friendly energy resources for environmental recovery and pollution prevention. Therefore, these economies have the potential to enhance renewable energy consumption. Besides, the existing literature is silent in the terms of empirical evidence relevant to the E7 economies, which is the need of the time. Specifications of variables along with the data source is provided in .

Table 1. Variables specifications and sources.

The theoretical notion through which energy efficiency, economic growth, carbon emissions and technological innovation affect renewable energy is provided in this section. Federal and local investments in renewable energy and energy efficiency may provide major advantages, such as reduced fuel and power prices, higher grid dependability, improved air quality and public health and more employment possibilities.Footnote2 In addition to saving money, increasing energy efficiency reduces your need for renewable energy, which may make your trip to net-zero emissions less costly.Footnote3 Further, it decreases the environmental effect of producing, distributing and deploying renewable energy. Apart from reducing the cost, energy efficiency could promote the use of renewable energy in the competition of lowering environmental degradation. Therefore, it is assumed that energy efficiency could play a vital role in the enhancement of renewable energy consumption. Nonetheless, the economic growth, technological innovation and carbon emissions are interlinked through various channels. For instance, the higher economic growth relied on increased industrial production and expansion. Due to which, the emerging economies are utilising traditional fossil fuel and non-renewable energy resources. As a result, the carbon emissions level increases, that causes climate change and global warming (Shahzad et al., Citation2021). Economies across the globe realises the harmful impacts of increased carbon emissions level. Due to which, economies increases their investments in environmentally friendly resources and technologies. Consequently, the increased investment for environmental recovery tends to increase the utilisation of renewable energy resources that causes no harm to the environment in terms of carbon emissions. Therefore, the economic growth, carbon emissions and technological innovations are expected to play a vital role in renewable energy consumption.

In order to empirically analyse the said nexus, this study constructed the following model:

Model

However, the above general model could be transformed into econometric or regression form for empirical examination, given as:

(1)

(1)

where the above equation reveals that

and

is the function of

Whereas

are the coefficients of estimates. Besides,

is the random error component, while t and i in the subscript represents time and cross-sections, respectively.

3.2. Estimation strategy

This research provides descriptive statistics, including the mean, median and range (maximum and minimum) values to summarise the data. In addition, we calculate the standard deviation, which reflects the difference of observational value and the mean value of a variable. Besides, the skewness and Kurtosis evaluated to measure the data normality. In contrast, the extended measurement of data normality is also used for the data distribution. Specifically, we used the normality test developed by Jarque and Bera (Citation1987) (J.B hereafter), which is provided in its conventional form as follows:

(2)

(2)

The preceding equation shows that the number of observations is captured by N, S represents skewness and K is excess Kurtosis. In a J.B test, the null hypothesis asserts that both estimates are zero and illustrates the data is normally distributed.

Once the descriptive and normality estimates are obtained, this research examines panel data properties, including slope coefficient heterogeneity (SCH) and cross-section dependency. Ignoring the panel data diagnostic tests could lead to the unproductive results (Breitung, Citation2005; Le & Bao, Citation2020). This research employs Pesaran and Yamagata (Citation2008) SCH test to address the SCH problem. Because this test offers both the SCH and adjusted SCH (ASCH), it is efficient, given as:

(3)

(3)

(4)

(4)

where

is the slope coefficient homogeneity from EquationEquation (3)

(3)

(3) , and

is the adjusted slope coefficient homogeneity. Where the null hypothesis assumes homogenous slopes coefficients till the estimates are insignificant. Besides, neglecting the cross-section dependence (CD) also lead to conflicting predictions in empirical research (Campello et al., Citation2019). Hence, we apply the Pesaran (Citation2021) CD test to see cross-sectional interdependence in the E-7 economies. The conventional equation for cross-sectional dependency is as follows:

(5)

(5)

The test's null proposition shows that cross-sections are not dependent across the panel.

With cross-sectional dependence and heterogeneous slope coefficients, this research may employ an estimator that can handle both panel data challenges. Accordingly, we employed Pesaran's (Citation2007) cross-sectionally augmented IPS (CIPS). Prior to Pesaran (Citation2007), Pesaran (Citation2006) proposed factor modelling to deal with cross-section dependence. This tool estimates cross-sectional averages as a representation of common unobserved components. Pesaran (Citation2007) uses the mean and first difference of lagged cross-sections to expand the Augmented Dickey-Fuller (ADF) regression. This strategy is effective in addressing cross-section dependency even though the panel is imbalanced (T > N or N > T). The cross-section ADF regression equation in its standard form is given as:

(6)

(6)

where

captures the mean of N observation. To deal with the serial correlation issue, the prior EquationEquation (6)

(6)

(6) may be augmented via adding the first difference lags of

and

given as:

(7)

(7)

Hence, the Pesaran (Citation2007) CIPS may be analysed in the selected panel economies by using the t-statistics’ average for every unit of cross-section (CADFi). The CIPS in an equation form is given as:

(8)

(8)

This (CIPS) test assumes the existence of a unit root in the time series as a null proposition.

This research used the Westerlund (Citation2007) error correction model (ECM) to analyse long-run cointegration here between variables in the panel of E-7 economies. By combining panel and group mean statistics, this test delivers efficient estimates for handling cross-sectional dependency along with slope heterogeneity. The following is the typical form of assessing both statistics:

The mean group statistics are and

while the panel statistics may be obtained as,

and

Apart from the Westerlund (Citation2007) ECM, this study also employed the Westerlund and Edgerton panel cointegration test with structural breaks, that not only provides statistics estimates for no shift, mean shift and regime shift, but also identifies the periods of structural breaks in a time-series of the panel data. Both the under-discussion tests assume the no cointegration association between the selected variables in the model. Whereas the significant estimates could reject the null hypothesis, which concludes the presence of cointegration.

Koenker and Bassett (Citation1978) first presented panel quantile regression, which estimates conditional variance and dependent mean, based on explanatory parameter values. If the dataset has atypical distribution qualities, quantile regression yields efficient estimates. Due to the data's irregular distributional patterns, we used Machado and Silva (Citation2019) novel method of moment’s quantile regression (MMQR from now). This new technique examines quantile numbers' redistributive and heterogeneous features (Sarkodie & Strezov, Citation2019). A basic equation may be used to get the conditional quantile location-scale variant estimation:

(9)

(9)

where EquationEquation (9)

(9)

(9) refers to

While

and

are the estimated coefficients. Here, i in the subscript refers to fixed effect as shown in

and

Besides, the k-vector of standard elements of X is depicted by Z, a distinguishing modification with

component, given as follows:

(10)

(10)

In the above equation, is distributed independently and identically for every specific i and t (time). Similarly,

is orthogonal to

and is dispersed across time and fixed cross-section (Machado & Silva, Citation2019). This helps stabilise elements and prevents intense exogenous behaviour. Hence, the priorly discussed EquationEquation (1)

(1)

(1) may be transformed as follows:

(11)

(11)

where EquationEquation (11)

(11)

(11) indicates that

is the vector of regressors that captures

All these variables are taken on natural log form for empirical examination. The left side of prior equation indicates vector of dependent variable, i.e.,

– captures

and may be defined as conditional on explanatory variable’s location and

Additionally,

is scalar coefficient demonstrating fixed effect of

quantiles for individual cross-section (i). In contrast, individual effects do not cause a change in the intercept like existing least-square fixed effects. Because the variables are time-invariant, heterogeneous impacts are likely to change. Finally,

designates the quantiles’

-th sample, where this study takes into account four, i.e., 25th, 50th, 75th and 90th quantiles to investigates the case. The quantile equation utilised in this investigation may be expressed as follows:

(12)

(12)

where exposes the check function.

This work employs bootstrap quantile regression (BSQR) in addition to MMQR as a robustness instrument and to validate the empirical findings of the former method. BSQR is a substitutional way to analyse confidence intervals and significance tests. The advantage of this specification is that it resamples the data to acquire the statistical findings while removing the parametric assumption of asymptotically normal sample distribution (Efron & Tibshirani, Citation1994).

Although the MMQR and BSQR technique gives estimated output for each regressor at a certain location and scale but not the causal relationship between variables. This investigation used the Granger panel causality heterogeneity test of Dumitrescu and Hurlin (Citation2012) to identify causality. This test is more efficient and stronger in addressing imbalanced panels (). It also addresses panel data heterogeneity and cross-sectional dependency issues (Banday & Aneja, Citation2020).

4. Results and discussion

This section begins with evaluating descriptive and normality statistics as reported in . The mean, median and the range values are found positive for all the study variables, including

and

Whereas a slight difference has been observed in the mean and median values. Yet, a substantial difference has been found in the minimum and maximum values, demonstrating the existence of volatility in each variable under study. In this sense, the standard deviation of each specific variable has been calculated, which is 0.390 for

0.346 for

0.479 for

0.263 for

and 0.644 for

These values demonstrate that every observation deviates from the given value from the mean value. On the other hand, the statistical estimates for the normality test are also provided in the same table. That is, skewness and Kurtosis are found different than their formulated values, i.e., 1 and 3, respectively. This reveals that all the variables are not normally distributed. However, the J.B test estimates asserted that statistical values are significant at the 1% level, rejecting the null hypothesis of normally distributed data. The said test concludes that both the skewness and excess Kurtosis are not equal to zero, leading to the rejection of proposition and the results that disclosed that the data is non-normally distributed.

Table 2. Descriptive and normality statistics.

After the descriptive and normality statistics, this study estimated the slope coefficient heterogeneity and cross-section dependence, provided in and , respectively. As discussed earlier, an economy depends on other economies for various reasons: it may be financial, economic, environmental, social, technological, among others. Due to these reasons, a state or economy may resemble other economies. However, neglecting such an issue in panel data estimations could lead to biased estimates (Campello et al., Citation2019; Le & Bao, Citation2020). Therefore, it is important to investigate the slope heterogeneity and cross-section dependence of the emerging economies that will lead to adopting an appropriate unit root testing approach. The estimated results for SCH and ASCH captured by and

respectively, are found highly statistically significant. This rejects the null hypothesis of slopes being homogenous; instead, the alternative hypothesis demonstrates that the slope coefficients are heterogeneous. On the other hand, the values for all the variables are found highly statistically significant at 1% level, which is enough evidence for rejecting the null proposition of Pesaran (Citation2021) CD test. Concluding that all the variables are cross-sectionally dependent. Since the slopes are heterogenous and cross-section dependence is present in the panel, an appropriate unit root estimator is required to deal with the mentioned panel data issues.

Table 3. Slope heterogeneity.

Table 4. Cross-section dependence.

Since the Pesaran and Yamagata (Citation2008) SCH test validates the slope coefficients are heterogeneous, the Pesaran (Citation2021) CD test confirms the cross-sectional dependency among the variables under consideration. Therefore, this study adopts the Pesaran (Citation2007) unit root testing approach that deals with the existing panel data issues, including slope heterogeneity and cross-section dependence. The estimated results of the CD test are shown in , indicating that all the variables are non-stationary at I(0). This reveals that the unit root is present in the study variables at levelled data. However, all the variables revealed statistically significant estimates at I(1), significant at 1% level – demonstrating no unit root for the variables in both the intercept and trend. The stationary data allows the current study to investigate the cointegration between the variables empirically.

Table 5. Unit root testing (Pesaran, Citation2007).

provides empirical results for the cointegration association between the variables obtained via employing the Westerlund (Citation2007) specifications. Concerning the null proposition of the said test, it is assumed that the ECT is zero. Whereas, the statistical value of

and

are highly statistically significant at the 1% level. On the other hand, the empirical results of the Westerlund and Edgerton (2008) panel cointegration with structural breaks are reported in , along with the detected structural breaks. The empirical results of the said test asserted that the statistical values for no break, mean shift and regime shift are highly statistically significant at 1% level. Besides, the structural breaks identified in this test is also reported, which are 1998, 2002, 2008, 2010 and 2014. These significant estimates reject the said test's proposition and conclude that the error correction is present, demonstrating that the long-run cointegration association exists between the variables. Therefore, we are allowed to estimate the long-run association of explanatory variables with the dependent variable (

).

Table 6. Cointegration results (Westerlund, Citation2007).

Table 7. Westerlund and Edgerton panel cointegration analysis with structural breaks.

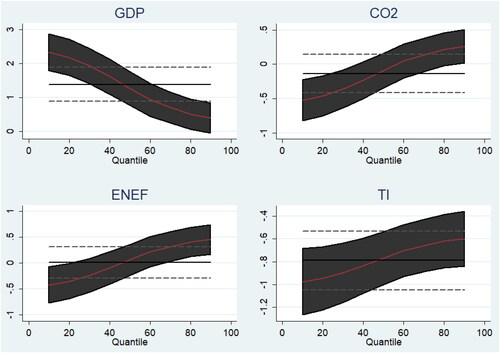

Since the cointegration association is found between the study variables, therefore, we are allowed to analyse the specific influence of each explanatory variable on (). Prior to that, this study noted that all the variables followed the irregular distribution paths. In this regard, the current study utilises an appropriate approach that deals with the issue of data’s non-normality. Specifically, we employed the moment's quantile regression (MMQR) approach and the results are displayed in . The primary advantage of this estimator is that it analyzes the influence of an explanatory variable at a specific location, scale and quantile. The examined results reveal that economic growth captured by

and energy efficiency (

) positively and statistically significant impact on

Whereas, the

emissions and

negatively and significantly affects

at various quantiles. To be more specific, a 1% increase in the

enhance

by 0.396–2.076%, which is statistically significant at 1% level. The magnitude of impact and the significance level is noted declining from lower (Q0.25) quantile(s) to upper (Q0.90) quantile(s). The positive influence demonstrates that enhancement in the income level leads to increased demand and renewable energy consumption. Such findings are consistent with the earlier findings of Bhattacharya et al. (Citation2016) in 38 energy-consuming economies and Padhan et al. (Citation2020) in OECD economies. Specifically, the economic growth in a country enhances the general public's purchasing power and increases the saving and investment levels. In this sense, the individual level income and aggregate investments are more devoted to the adoption of renewables and structural transformation of the industrial sector. This improves the economic growth level and enhances the environmental quality of the region (Mardani et al., Citation2019). On the other hand, the

emissions exhibit mixed influence on

That is, a 1% increase in the

emission reduces

by 0.420% in Q0.25 at 1% level of significance level, while enhancing

by 0.262% in the upper quantile (Q0.90) at 5% level of significance. This demonstrates that in the lower quantiles, the

are negatively associated with

due to lower levels of emissions. As the level of emissions increases, consumption of renewable energy also enhances due to controlling environmental degradation. The negative association between

emissions and

are consistent with the earlier studies of Omri and Nguyen (Citation2014), Gielen et al. (Citation2019) and Ponce and Khan (Citation2021). Besides, the impact of

emissions on

are negative in Q0.50 and positive in Q0.75, but insignificant in both the quantiles.

Table 8. Estimates of quantile regression – MMQR.

On the other hand, is found in mixed association with

and

is having a negative association with the

Specifically, a 1% increase in the

significantly enhances

by 0.361 and 0.459% in Q0.75 and Q0.90. However,

adversely affects

by 0.304 in the first quantile. These results are statistically significant at 5%, 1% and 10% levels, respectively. The mixed influence asserted that demand for renewables is not very attractive at the lower level of energy efficiency. However, at a higher level of energy efficiency, the demand and consumption of renewable energy are also enhanced. Since both of these measures are used to tackle environmental issues and climate change, including CO2 and GHG emissions (Riti & Shu, Citation2016). As depicted by the latter quantiles, increasing the energy efficiency leads to enhancement in renewable energy use and adoption, which simultaneously leads to lower demand for fossil fuel consumption and enhances environmental quality by tackling the emission level (Bayar & Gavriletea, Citation2019; Vine, Citation2008). In addition, the

exhibits a negative impact on the

particularly in the emerging seven economies. Specifically, a 1% increase in the

lowers

by 0.598–0.924%, where it is noted that the magnitude level of the impact is decreasing from lower to upper quantile. Since the study economies are emerging economies, more attention is paid to the growth and sustainability of economic growth. Therefore, the technological innovation in these economies is diverted to the production and industrial sector, where the primary focus is on enhancing production levels and expanding the industrial sector. However, the industrial sector in these economies is more dependent on fossil fuel economies, which promote fossil fuel energy and reduce renewable energy consumption. The specific influence of each explanatory variable on

is reported in .

Figure 1. Graphical representation of quantiles.

Source: drawn by the authors.

Once the empirical results of the MMQR are obtained, this study also test the robustness of the model via employing the bootstrap quantile regression (BSQR). Since the BSQR also deals the issue of data’s non-normality. Therefore, it is efficient to utilise the said approach, for which the empirical results are reported in . The BSQR results asserted that economic growth (GDP), carbon emissions and energy efficiency significantly enhances renewable energy consumption in the concerned group of economies. Thus, these variables are the significant factors of renewable energy. However, the technological innovation is found to have adverse impact in renewable energy consumption. The estimated results of BSQR are highly statistically significant at 1% level, which also validates the empirical findings of MMQR, and are consistent the studies mentioned earlier.

Table 9. Robust test results – BSQR.

Nonetheless, the MMQR provides the specific influence of regressors on the However, this specification does not show the causal association between the variables. In this regard, current study employed the Dumitrescu and Hurlin (Citation2012) panel Granger causality test and the estimates are provided in . The results indicate that there are significant causalities from

and

to

However, the feedback effect is also found from

all other variables at 5% and 1% significance levels. In other words, any policy changes in any of the explanatory variables could significantly cause changes in

At the same time, policy changes in the latter could also influence policies regarding the explanatory variables. Not only in this study, but the earlier studies also found that there is a bidirectional causal nexus between economic growth and renewable energy. Consistent with the studies of Acaravci and Ozturk (Citation2010) and Mardani et al. (Citation2019), the bidirectional association between these variables is due to the feedback theory, as mentioned by Antonakakis et al. (Citation2017).

Table 10. Dumitrescu-Hurlin panel causality.

5. Conclusion and policy implications

This study analyzes the nexus of energy efficiency and renewable energy consumption in the case of emerging economies. Also, this study considers the impact of economic growth, carbon emissions and technological innovation on renewable energy consumption during the last three decades. Using non-parametric panel data approaches, this study employed a slope heterogenous test, that reveals that the slopes are heterogeneous across the panel. Besides, the panel cross-section dependence validates that the cross-section dependence is present in the panel of emerging economies. Based on these results, a second-generation unit root test is utilised, which asserted that all the variables are stationary at first difference. On the other hand, the J.B test affirms that all the variables follow the property of non-normal distribution, which could provide misleading results. Therefore, this study employed the MMQR approach to tackle the non-normality issue. The findings unveil that economic growth positively influences renewable energy consumption at all quantiles. Enhancement in the income level substantially promotes the use of renewables due to affordability and a high level of investment in the renewable energy sector. On the other hand, the impact of CO2 emissions and energy efficiency is mixed across quantiles. In other words, CO2 emissions and energy efficiency significantly reduce renewable energy consumption in the lower quantile, while significantly enhancing renewable energy consumption in upper quantiles. However, the medium quantiles showed an insignificant impact of these variables on renewable energy. The mixed impact reveals that a lower level of CO2 emissions and energy efficiency reduces demand for renewable energy, making flexible policies regarding environmental quality possible. However, as the emissions level enhances, renewable energy requirements enhance, and the energy efficiency promotes the culture of renewable energy adoption at the household level and at the industrial level. Hence, the higher level of CO2 emissions and energy efficiency is positively associated with increased renewable energy consumption. Based on the fact that the emerging economies are more concerned about economic growth and sustainability. Due to this, these countries' primary focus is diverted towards economic growth maintenance – leads to enhanced production levels and expanding the industrial sector. Therefore, technologies regarding growth are adopted that are more energy-intensive and could be obtained from traditional fossil fuel energy sources. In this sense, demand for fossil fuel energy increases and renewable energy consumption reduces, which is alarming for the environmental sustainability of emerging economies.

Based on the empirical results, this study suggests policies that could provide a path for developing the renewable energy sector and renewables’ consumption. Particular, economic growth could be used to reduce fossil fuel energy or fossil energy-based industry. The higher level of income shall be directed towards the structural transformation of the industrial sector. Subsidization of the industries for renewable energy consumption and imposing high taxes on those utilising fossil fuel energy could be a priority policy measure for the emerging economies. In addition, the existing literature unveils that both energy efficiency and renewable energy could be used as prominent factors for reducing environmental degradation and emissions levels. While this study formulates that enhancement in energy efficiency could also enhance renewable energy consumption. Therefore, policies could adopt energy efficiency tools and techniques to reduce energy demand and the use of non-renewable energy, particularly in developing economies. Besides, implementing policies for improving energy efficiency leads to a substantial increase in renewable energy consumption, which is not only beneficial for environmental recovery, but also contributes to economic and sustainable development. Lastly, this study noted that technological innovation adversely affects renewable energy consumption. Therefore, policies must adopt technological improvement by considering the environmental quality forcing adoption and consumption of renewable energy. Since the E7 are emerging economies and mainly focuses on the development of industrial sector. Therefore, these economies should enhance investment in the environmental related technological innovation, which could help increase the use of renewable energy and prevent pollution level without effecting the economic progress.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

2 For more details, visit: https://www.epa.gov/sites/default/files/2018-07/documents/mbg_1_multiplebenefits.pdf.

3 For more information, visit: https://100percentrenewables.com.au/importance-of-energy-efficiency-in-reaching-net-zero-emissions/.

References

- Abeykoon, C., McMillan, A., & Nguyen, B. K. (2021). Energy efficiency in extrusion-related polymer processing: A review of state of the art and potential efficiency improvements. Renewable and Sustainable Energy Reviews, 147, 111219. https://doi.org/10.1016/j.rser.2021.111219

- Acaravci, A., & Ozturk, I. (2010). On the relationship between energy consumption, CO2 emissions, and economic growth in. Energy, 35(12), 5412–5420. https://doi.org/10.1016/j.energy.2010.07.009

- Ahmed, S., Ahmed, K., & Ismail, M. (2020). Predictive analysis of CO2 emissions and the role of environmental technology, energy use and economic output: Evidence from emerging economies. Air Quality, Atmosphere & Health, 13(9), 1035–1044. https://doi.org/10.1007/s11869-020-00855-1

- Akram, R., Chen, F., Khalid, F., Ye, Z., & Majeed, M. T. (2020). Heterogeneous effects of energy efficiency and renewable energy on carbon emissions: Evidence from developing countries. Journal of Cleaner Production, 247, 119122. https://doi.org/10.1016/j.jclepro.2019.119122

- Al-Mulali, U., Weng-Wai, C., Sheau-Ting, L., & Mohammed, A. H. (2015). Investigating the environmental Kuznets curve (EKC) hypothesis by utilizing the ecological footprint as an indicator of environmental degradation. Ecological Indicators, 48, 315–323. https://doi.org/10.1016/j.ecolind.2014.08.029

- Antonakakis, N., Chatziantoniou, I., & Filis, G. (2017). Energy consumption, CO2 emissions, and economic growth: An ethical dilemma. Renewable and Sustainable Energy Reviews, 68, 808–824. https://doi.org/10.1016/j.rser.2016.09.105

- Banday, U. J., & Aneja, R. (2020). Renewable and non-renewable energy consumption, economic growth and carbon emission in BRICS: Evidence from bootstrap panel causality. International Journal of Energy Sector Management, 14(1), 248–260. https://doi.org/10.1108/IJESM-02-2019-0007

- Bayar, Y., & Gavriletea, M. D. (2019). Energy efficiency, renewable energy, economic growth: Evidence from emerging market economies. Quality & Quantity, 53(4), 2221–2234. https://doi.org/10.1007/s11135-019-00867-9

- Bhattacharya, M., Paramati, S. R., Ozturk, I., & Bhattacharya, S. (2016). The effect of renewable energy consumption on economic growth: Evidence from top 38 countries. Applied Energy, 162, 733–741. https://doi.org/10.1016/j.apenergy.2015.10.104

- Breitung, J. (2005). A parametric approach to the estimation of cointegration vectors in panel data. Econometric Reviews, 24(2), 151–173. https://doi.org/10.1081/ETC-200067895

- Cai, X., Wang, W., Rao, A., Rahim, S., & Zhao, X. (2022). Regional sustainable development and spatial effects from the perspective of renewable energy. Frontiers in Environmental Science, 10, 166. https://doi.org/10.3389/fenvs.2022.859523

- Campello, M., Galvao, A. F., & Juhl, T. (2019). Testing for slope heterogeneity bias in panel data models. Journal of Business & Economic Statistics, 37(4), 749–760. https://doi.org/10.1080/07350015.2017.1421545

- Cantore, N., Calì, M., & te Velde, D. W. (2016). Does energy efficiency improve technological change and economic growth in developing countries? Energy Policy, 92, 279–285. https://doi.org/10.1016/j.enpol.2016.01.040

- Chen, Y., Wang, Z., & Zhong, Z. (2019). CO2 emissions, economic growth, renewable and non-renewable energy production and foreign trade in China. Renewable Energy, 131, 208–216. https://doi.org/10.1016/j.renene.2018.07.047

- Chien, T., & Hu, J. L. (2008). Renewable energy: An efficient mechanism to improve GDP. Energy Policy, 36(8), 3045–3052. https://doi.org/10.1016/j.enpol.2008.04.012

- Dumitrescu, E. I., & Hurlin, C. (2012). Testing for Granger non-causality in heterogeneous panels. Economic Modelling, 29(4), 1450–1460. https://doi.org/10.1016/j.econmod.2012.02.014

- Dunkley, E. (2011). China to overtake US by 2018–PwC. Investment Week, 13.

- Efron, B., & Tibshirani, R. J. (1994). An introduction to the bootstrap. CRC press.

- EPA. (2018). Quantifying the multiple benefits of energy efficiency and renewable energy: A guide for state and local governments.

- Fang, J., Gozgor, G., Mahalik, M. K., Padhan, H., & Xu, R. (2021). The impact of economic complexity on energy demand in OECD countries. Environmental Science and Pollution Research International, 28(26), 33771–33780. https://doi.org/10.1007/s11356-020-12089-w

- Geller, H., Schaeffer, R., Szklo, A., & Tolmasquim, M. (2004). Policies for advancing energy efficiency and renewable energy use in Brazil. Energy Policy, 32(12), 1437–1450. https://doi.org/10.1016/S0301-4215(03)00122-8

- Gielen, D., Boshell, F., Saygin, D., Bazilian, M. D., Wagner, N., & Gorini, R. (2019). The role of renewable energy in the global energy transformation. Energy Strategy Reviews, 24, 38–50. https://doi.org/10.1016/j.esr.2019.01.006

- Gozgor, G., Mahalik, M. K., Demir, E., & Padhan, H. (2020). The impact of economic globalization on renewable energy in the OECD countries. Energy Policy, 139, 111365. https://doi.org/10.1016/j.enpol.2020.111365

- Hodges, J. (2016). Managing and leading people through organizational change: The theory and practice of sustaining change through people. Kogan Page Publishers.

- Jarque, C. M., & Bera, A. K. (1987). A test for normality of observations and regression residuals. International Statistical Review/Revue Internationale de Statistique, 55(2), 163–172. https://doi.org/10.2307/1403192

- Jiang, S., Chishti, M. Z., Rjoub, H., & Rahim, S. (2022). Environmental R&D and trade-adjusted carbon emissions: Evaluating the role of international trade. Environmental Science and Pollution Research, 1–16. https://doi.org/10.1007/s11356-022-20003-9

- Khan, S. A. R., Sharif, A., Golpîra, H., & Kumar, A. (2019). A green ideology in Asian emerging economies: From environmental policy and sustainable development. Sustainable Development, 27(6), 1063–1075. https://doi.org/10.1002/sd.1958

- Koenker, R., & Bassett, G. (1978). Regression quantiles. Econometrica, 46(1), 33–50. https://doi.org/10.2307/1913643

- la Cruz-Lovera, D., Perea-Moreno, A. J., la Cruz-Fernández, D., Alvarez-Bermejo, J. A., & Manzano-Agugliaro, F. (2017). Worldwide research on energy efficiency and sustainability in public buildings. Sustainability, 9(8), 1294. https://doi.org/10.3390/su9081294

- Le, H. P., & Bao, H. H. G. (2020). Renewable and nonrenewable energy consumption, government expenditure, institution quality, financial development, trade openness, and sustainable development in Latin America and Caribbean emerging Market and developing economies. International Journal of Energy Economics and Policy, 10(1), 242–248. https://doi.org/10.32479/ijeep.8506

- Lu, Z., Mahalik, M. K., Padhan, H., Gupta, M., & Gozgor, G. (2021). Effects of age dependency and urbanization on energy demand in BRICS: Evidence from the machine learning estimator. Frontiers in Energy Research, 9, 749065. https://doi.org/10.3389/fenrg.2021.749065

- Luan, S., Hussain, M., Ali, S., & Rahim, S. (2022). China’s investment in energy industry to neutralize carbon emissions: Evidence from provincial data. Environmental Science and Pollution Research International, 29(26), 39375–39383. https://doi.org/10.1007/s11356-021-18141-7

- Machado, J. A., & Silva, J. S. (2019). Quantiles via moments. Journal of Econometrics, 213(1), 145–173. https://doi.org/10.1016/j.jeconom.2019.04.009

- Mahalik, M. K., Babu, M. S., Loganathan, N., & Shahbaz, M. (2017). Does financial development intensify energy consumption in Saudi Arabia? Renewable and Sustainable Energy Reviews, 75, 1022–1034. https://doi.org/10.1016/j.rser.2016.11.081

- Mardani, A., Streimikiene, D., Cavallaro, F., Loganathan, N., & Khoshnoudi, M. (2019). Carbon dioxide (CO2) emissions and economic growth: A systematic review of two decades of research from 1995 to 2017. The Science of the Total Environment, 649, 31–49. https://doi.org/10.1016/j.scitotenv.2018.08.229

- Nadda, V., Dadwal, S., & Rahimi, R. (Eds.) (2017). Promotional strategies and new service opportunities in emerging economies. IGI Global.

- Nibedita, B., & Irfan, M. (2021). The role of energy efficiency and energy diversity in reducing carbon emissions: Empirical evidence on the long-run trade-off or synergy in emerging economies. Environmental Science and Pollution Research, 28(40), 56938–56917. https://doi.org/10.1007/s11356-021-14642-7

- Omri, A., & Nguyen, D. K. (2014). On the determinants of renewable energy consumption: International evidence. Energy, 72, 554–560. https://doi.org/10.1016/j.energy.2014.05.081

- Padhan, H., Padhang, P. C., Tiwari, A. K., Ahmed, R., & Hammoudeh, S. (2020). Renewable energy consumption and robust globalization(s) in OECD countries: Do oil, carbon emissions and economic activity matter? Energy Strategy Reviews, 32, 100535. https://doi.org/10.1016/j.esr.2020.100535

- Park, G. (2016). Integral operational leadership: A relationally intelligent approach to sustained performance in the twenty-first century. Routledge.

- Pesaran, M. H. (2006). Estimation and inference in large heterogeneous panels with a multifactor error structure. Econometrica, 74(4), 967–1012. https://doi.org/10.1111/j.1468-0262.2006.00692.x

- Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross‐section dependence. Journal of Applied Econometrics, 22(2), 265–312. https://doi.org/10.1002/jae.951

- Pesaran, M. H. (2021). General diagnostic tests for cross-sectional dependence in panels. Empirical Economics, 60(1), 13–50. https://doi.org/10.1007/s00181-020-01875-7

- Pesaran, M. H., & Yamagata, T. (2008). Testing slope homogeneity in large panels. Journal of Econometrics, 142(1), 50–93. https://doi.org/10.1016/j.jeconom.2007.05.010

- Ponce, P., & Khan, S. A. R. (2021). A causal link between renewable energy, energy efficiency, property rights, and CO2 emissions in developed countries: A road map for environmental sustainability. Environmental Science and Pollution Research, 28(28), 37804–37814. https://doi.org/10.1007/s11356-021-12465-0

- Qin, L., Hou, Y., Miao, X., Zhang, X., Rahim, S., & Kirikkaleli, D. (2021). Revisiting financial development and renewable energy electricity role in attaining China's carbon neutrality target. Journal of Environmental Management, 297, 113335. https://doi.org/10.1016/j.jenvman.2021.113335

- Qin, L., Raheem, S., Murshed, M., Miao, X., Khan, Z., & Kirikkaleli, D. (2021). Does financial inclusion limit carbon dioxide emissions? Analyzing the role of globalization and renewable electricity output. Sustainable Development, 29(6), 1138–1154. https://doi.org/10.1002/sd.2208

- Qudrat-Ullah, H., Kayal, A., & Mugumya, A. (2021). Cost-effective energy billing mechanisms for small and medium-scale industrial customers in Uganda. Energy, 227, 120488. https://doi.org/10.1016/j.energy.2021.120488

- Rahim, S., Murshed, M., Umarbeyli, S., Kirikkaleli, D., Ahmad, M., Tufail, M., & Wahab, S. (2021). Do natural resources abundance and human capital development promote economic growth? A study on the resource curse hypothesis in Next Eleven countries. Resources, Environment and Sustainability, 4, 100018. https://doi.org/10.1016/j.resenv.2021.100018

- Rahman, M. M., Sultana, N., & Velayutham, E. (2022). Renewable energy, energy intensity and carbon reduction: Experience of large emerging economies. Renewable Energy, 184, 252–265. https://doi.org/10.1016/j.renene.2021.11.068

- Renna, P., & Materi, S. (2021). A literature review of energy efficiency and sustainability in manufacturing systems. Applied Sciences, 11(16), 7366. https://doi.org/10.3390/app11167366

- Riti, J. S., & Shu, Y. (2016). Renewable energy, energy efficiency, and eco-friendly environment (RE5) in Nigeria. Energy, Sustainability and Society, 6(1), 1–16. https://doi.org/10.1186/s13705-016-0072-1

- Salim, R. A., & Rafiq, S. (2012). Why do some emerging economies proactively accelerate the adoption of renewable energy? Energy Economics, 34(4), 1051–1057. https://doi.org/10.1016/j.eneco.2011.08.015

- Sarkodie, S. A., & Strezov, V. (2019). A review on environmental Kuznets curve hypothesis using bibliometric and meta-analysis. The Science of the Total Environment, 649, 128–145. https://doi.org/10.1016/j.scitotenv.2018.08.276

- Shahzad, U., Radulescu, M., Rahim, S., Isik, C., Yousaf, Z., & Ionescu, S. A. (2021). Do environment-related policy instruments and technologies facilitate renewable energy generation? Exploring the contextual evidence from developed economies. Energies, 14(3), 690. https://doi.org/10.3390/en14030690

- Vine, E. (2008). Breaking down the silos: The integration of energy efficiency, renewable energy, demand response, and climate change. Energy Efficiency, 1(1), 49–63. https://doi.org/10.1007/s12053-008-9004-z

- Wei, J., Rahim, S., & Wang, S. (2022). Role of environmental degradation, institutional quality, and government health expenditures for human health: Evidence from emerging seven countries. Frontiers in Public Health, 10, 870767. https://doi.org/10.3389/fpubh.2022.870767

- Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69(6), 709–748. https://doi.org/10.1111/j.1468-0084.2007.00477.x

- World Energy Outlook (WEO). (2017). Energy access outlook 2017: From poverty to prosperity [Special report].

- Xing, L. (2016). The BRICS and beyond: The international political economy of the emergence of a new world order. Routledge.