?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Announcements of corporate misconduct can trigger negative market reactions. However, our understanding of mechanisms that shape variations of investors’ responses across different disclosed-firms is underdeveloped. From the legitimacy theory perspective, this study focuses on the impact of state ownership on market reaction to misconduct announcements. Using a sample of misconduct announcements of Chinese listed firms from 2010 to 2021 and employing a combination of an event study method and a Heckman two-stage model, this study finds that market reaction to misconduct announcements is weaker if state ownership of the disclosed firm is larger. Furthermore, the affiliation level of SOEs (central SOEs versus local SOEs) weakens the positive association between state ownership and market reaction. The main positive effect is strengthened when the disclosed firms are located in regulated industries.

JEL CODES:

1. Introduction

How to prevent corporate misconduct is a critical academic topic that profoundly influences the interests of shareholders and public investors (Shi et al., Citation2020; Yiu et al., Citation2019). Besides direct punishment decisions made by the regulators, public investors’ response to misconduct announcements is essential to higher costs of illegal behaviors (Wang et al., Citation2019b). Existing literature has explored whether misconduct announcements by regulator could trigger market reactions and evidence show that investors disapprove of all misconduct behaviors significantly. For example, Chen et al. (Citation2005) identify misconduct announcements by regulators in China and present the stock returns are −1.8% for a five-day window. Wang et al. (Citation2019b) examine the punishment actions by the China Securities Regulatory Commission (CSRC) have a negative impact, and the CARs are −0.5% on average for a short-term window.

While these studies have confirmed a negative relationship between misconduct announcements and disclosed-firm value, little academic attention is paid to the variations of market reactions to announced firms and the impact of their equity nature on investors’ responses. Previous studies underscore the assumption that investors respond to misconduct mainly based on their evaluation of specific misconduct cases, such as misconduct category and enforcement actions (Wang et al., Citation2019b). However, this assumption should be challenged, especially in emerging economies. In emerging economies, formal institutions such as rule-making authorities and regulatory enforcement are underdeveloped, generating variations of functions of regulatory processes in different firms (Xie et al., Citation2021). This variation makes investors likely to judge corporate misconduct on informal or social constructions instead of occasional misconduct events or formal enforcement (Zajac & Westphal, Citation2004). State ownership is booming in emerging economies, and the extent to which government owns a firm is a crucial indicator to influence whether the firm can easily obtain critical resources, competitive advantages, and organizational legitimacy (Zhou et al., Citation2017). However, the impact of state ownership on market responses to misconduct announcements is still unexplored in the existing literature.

This article proposes that state ownership profoundly affects market responses to misconduct announcements by regulators. We adopt a legitimacy perspective rooted in the institutional theory (DiMaggio & Powell, Citation1983; Scott, Citation1995; Suchman, Citation1995). Institutional theorists hold that firms strive to build and maintain legitimacy (Zimmerman & Zeitz, Citation2002), and state ownership is the most visible and stable tie with the government, which can counteract the impact of adverse events on organizational legitimacy (Marquis & Qian, Citation2014). In this sense, although there is a general trend of losing legitimacy after misconduct announcements, the negative market reaction is weaker if a firm owns a higher proportion of state ownership. We further propose that the positive effect of state ownership on market reactions hinges on the affiliation level of SOEs (central SOEs versus local SOEs) and whether the firm is located in a state-regulated industry. We find affiliation level weakens the positive relationship, and industry regulation strengthens the main effect.

Using a sample of 12-year misconduct cases announced by the CSRC in the Chinese stock market, we find support for our arguments by employing an event study method and a Heckman two-stage model. The study provides incremental contributions to extant literature. First, this research proposes a new framework to explain the key role of state ownership in shaping investors’ evaluations of misconduct announcements. State ownership affects investors’ assessment and judgment of negative events through the distinctiveness of organizational legitimacy in the context of emerging economies where the formal institution is inadequate (Allen et al., Citation2005), which can advance the conventional view that event attribute is the primary determinant of market reaction (Gong et al., Citation2021; Wang et al., Citation2019b). Second, we contribute to the literature by showing a disproportionate negative market reaction to misconduct with an increment in state ownership in a firm. Extant literature explored that state ownership played a decisive role in deterring fraud (Shi et al., Citation2020; Yiu et al., Citation2019). However, they overlook the impact of state ownership on investors’ reactions to misconduct announcements. Third, research findings of moderators show that a higher affiliation level reduces investors’ tolerance for inappropriate behaviors, and industry regulation strengthens the role of state ownership in the face of legitimacy shock.

2. Literature review and hypotheses development

2.1. Misconduct announcement and market reactions in China

Since the Chinese government established the stock market in the early 1990s, after 30 years of rapid development, securities inspections and regulations have been improved. Founded in 1992, the CSRC is responsible for supervising the operation of the Chinese stock market. The specific functions of the CSRC include issuing regulatory ordinances, managing securities issuance and trading, and checking listed firms’ daily operations. Among these duties, sanctioning and announcing corporate misconduct is an important signal that can cause significant market reactions and profoundly influence regulated firms’ behaviors (Chen et al., Citation2005; W. Xu et al., Citation2017). Listed firms engaged in corporate misconduct will be subject to several punishment measures, such as warnings, fines, and confiscation of illegal benefits, generally divided into administrative and non-administrative punishment. Regarding the severity of these punishment measures, researchers agreed that administrative punishment is more severe than non-administrative punishment in the Chinese stock market (Wang et al., Citation2019b).

Misconduct announcements and punishment increase the cost of corporate misconduct for listed firms. Although firms can obtain economic gains from a part of misconduct behaviors, security sanctions incur regulatory fines and other direct penalties. Moreover, subsequent reputational losses related to the business actions of stakeholders exceed immediate regulatory punishments (Zeidan, Citation2013). Studies have examined shareholder wealth losses, such as CARs after misconduct announcements, primarily based on the event study method. A smaller of them investigated whether market reaction sizes differed for different punishment types. For instance, in China, the wealth losses are around 1-2% in a five-day window surrounding the event disclosure (G. Chen et al., Citation2005). Similarly, in the U.S., negative abnormal returns are 5.3% of financial restatements (Palmrose & Scholz, Citation2004). For market reactions to different punishment types, Wang et al. (Citation2019b) found fines caused more negative market reactions than non-monetary punishments.

Previous studies thus contend that types of incidents and punishments determine the sizes of negative market reactions. There are two underlying premises for this conventional view. First, public investors making financial decisions are dominated by an efficiency logic (Fama, Citation1970). They calculate the costs of being punished and negative economic impacts on the focal firm in the future, usually based on punishment severity, resulting in a significant relationship between the incident type and its market reaction. Second, the misconduct information disclosed by regulators is adequate and transparent to help investors make financial judgments. However, this study argues that the two assumptions should be challenged in emerging economies like China. On the one hand, regulatory enforcement is uncertain due to an underdeveloped legal system, leading to punishment decisions not being the only criteria for the negative impact of misconduct (Mike W Peng, Citation2003; Xie et al., Citation2021). In this sense, investors reacting to misconduct and making judgments are socially constructed and affected by institutional factors (Zajac & Westphal, Citation2004). On the other hand, information disclosed by regulators in emerging economies may be limited and untransparent (Allen et al., Citation2005). Thus, other factors related to firm-specific characteristics are expected to function when investors evaluate the impacts of misconduct on different firms (J. Chen et al., Citation2016).

2.2. State ownership and market reactions to misconduct announcement: a legitimacy perspective

Organizational legitimacy is defined as the ‘generalized perception or assumption’ that ‘the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions’ (Suchman, Citation1995). Institutional theorists contend that organizations must conform to rules, norms, and values prevailing in institutions to gain legitimacy, survive, and obtain crucial resources (DiMaggio & Powell, Citation1983; Meyer & Rowan, Citation1977; Zimmerman & Zeitz, Citation2002). Scott (Citation1995) classified institutions into three pillars: the regulatory, the normative, and the cognitive, and three corresponding types of legitimacy can be illustrated as social acceptance from organizational compliances with regulatory rules, social norms, and cognitive values. The notion of legitimacy emphasizes that it should be evaluated and assessed by ‘the audiences,’ who are usually stakeholders of a firm, such as customers, suppliers, and public investors (Suchman, Citation1995). Although external evaluation complicates the organizational process of building or maintaining legitimacy, situations when the organization loses legitimacy, can be easily judged (Suddaby et al., Citation2017). For example, once a firm is announced to engage in corporate misconduct, its legitimacy will be damaged, and the firm should repair and regain it by conducting social-accepted practices (Galloway et al., Citation2021; L. Zhang et al., Citation2020).

Recent works that apply the institutional theory to explain corporate governance or strategies in emerging economies notice that state ownership is the most obvious way to affect legitimacy assessments by audiences and corporate legitimacy strategies. First, governments directly own and operate SOEs, reducing the requirement for SOEs to gain regulatory legitimacy by complying with formal rules or regulations. Government ownership is prevalent in emerging economies because it is helpful to fill in ‘institutional voids,’ and state ownership can assist the government in attaining social and political goals (Musacchio et al., Citation2015; Tihanyi et al., Citation2019). SOEs are viewed as actors that ‘naturally have legitimacy’ (H. Y. Li & Zhang, Citation2007; Pan et al., Citation2019), and they are naturally easier to get access to financial resources and government protections (M. W. Peng et al., Citation2016). Second, governments in emerging economies over-interfere in economic development, resulting in more significant heterogeneity of legitimate practices between SOEs and non-SOEs. Government and government-related bodies are described as not only rule-maker but also player in the market. They play essential roles in resource allocation, market regulation, and access to business opportunities (Guo et al., Citation2014; D. Xu et al., Citation2013). Over-participation of the government enlarges legitimacy disparities between SOEs and non-SOEs (H. Y. Wu et al., Citation2018).

The decline in firm value after the misconduct announcement reflects the assessment and evaluation of public investors on the impact of corporate misconduct on organizational legitimacy. Due to uncertain regulatory enforcement actions and limited information disclosure in emerging economies, investors are more likely to perceive state ownership can bear substantial legitimacy challenges because SOEs have ‘legitimacy stock’ and they have strong ties with the government, which cannot be easily damaged by occasional adverse events (Pan et al., Citation2019). The more state ownership in a firm, the investors perceive fewer threats of corporate misconduct. Thus, this study posits the following hypothesis:

Hypothesis 1: Market reaction to corporate misconduct is less negative when a firm has larger state ownership.

2.3. Affiliation level as moderator

To reveal the effect of state ownership on market reactions after misconduct announcements, we consider two moderators. Government affiliation of a firm with state ownership represents the affiliation level of government agencies who ultimately control the firm. At the provincial, municipal, and county levels, the central government and local government agencies in China can take equity shares of listed SOEs. The affiliation level plays a vital role in how charging governments operate SOEs and how audiences evaluate organizational legitimacy through judgments of the relationships between SOEs and their charging governments (Hu & Sun, Citation2019). For example, the central government is concerned more about broad national policies that guild and regulate market reform and social welfare. Central SOEs, therefore, behave more likely as a flagship that all other firms attend to and attempt to mimic. The local government emphasizes regional fiscal revenue growth and employment more. Local SOEs thus pay more attention to economic growth and return, which are similar to the goals of private firms (Deng et al., Citation2020; M. H. Li et al., Citation2018).

We argue that affiliation level will weaken the buffering effect of state ownership on market reactions to corporate misconduct. Serving as the role of the flagship in the Chinese stock market, central SOEs have the highest visibility among all listed SOEs. Their behaviors attract more scrutiny, attention, and discussion from the media and the public, which may induce a ripple effect once incidents have been disclosed (Hu & Sun, Citation2019; M. H. Li et al., Citation2018). Unethical behaviors conducted by central SOEs may implicate a broad scope of politicians, such as top executives serving in central SOEs, central government officials even regulators in the SASAC. Public attention to corporate misconduct will reinforce investors’ concerns about the legitimacy of central SOEs because governments may enact administrative punishment to respond to public criticism.

Conversely, for local SOEs which are announced to break the rules, their organizational visibility is at a lower level, and announced misconduct will not draw public attention. Local SOEs are expected to contribute to regional GDP growth and fiscal income of their regional charging government agencies (Deng et al., Citation2020). They are more likely to be sheltered by the local governments, and their legitimacy is less likely to be challenged by adverse incidents. Therefore, we hypothesize:

Hypothesis 2: When a firm has a higher affiliation level, the positive effect of state ownership on market reactions to misconduct announcements is weaker.

2.4. Regulated industry as moderator

In emerging economies, the way governments regulate market economies also contains policy regulations at the industry level. The state imposes specific power in the form of industry regulations to address market imperfections and correct market outcomes (He et al., Citation2020; Rodrik, Citation2008). For example, the Chinese government issues multiple and detailed industry regulations, which involve sectors of finance, energy, transportation, etc. As not all industries are equally regulated, when industry regulation is intense, firms’ behaviors are deeply affected by external constraints, and the regulated ties with governments impact their legitimacy.

When the firm is located in a regulated industry, government intervention through industry regulation amplifies the effect of state ownership. Firms in the regulated sector have less access to resources through market channels as the governments allocate resources in regulatory ways (He et al., Citation2020). State ownership has a more obvious legitimacy advantage in regulated industries than in unregulated ones. He et al. (Citation2020) propose that industry regulations lead SOEs to undertake national development tasks and have stable resource advantages. Moreover, SOEs have a natural monopoly in regulated industries, and the monopoly profits can offset the reduction of resource effect. Thus, the stability of legitimacy advantages in the regulated industry strengthens the buffering effect of state ownership on negative reactions to corporate misconduct. Therefore, we hypothesize:

Hypothesis 3: When a firm is located in the regulated industry, the positive effect of state ownership on market reactions to misconduct announcements is stronger.

3. Methodology

3.1. Data and research design

This study uses the misconduct cases of listed companies disclosed by the China Securities Regulatory Commission from 2010 to 2021 as the research sample. We collected data relating to corporate misconduct and firm-level characteristics from the China Stock Market and Accounting Research (CSMAR) database (X. W. Zhang et al., Citation2021). The relevant information on industry regulation was collected and referred to the 2007 revision of the Catalogue for the Guidance of Foreign Investment Industries issued by the National Development and Reform Commission and the Chinese Ministry of Commerce. According to misconduct announcements by the CSRC, corporate misconduct includes various types, such as financial violations (fictitious profits, etc.), record violations (false records, etc.), disclosure violations (delayed disclosure, etc.), stock manipulation violations (illegal trading of stocks, etc.) (Shi et al., Citation2020). Different types of misconduct are included in the sample for observation. We finally obtained 3093 misconduct cases conducted by 2512 listed firms.

An event study method (McWilliams & Siegel, Citation1997) is used to retrieve the cumulative abnormal return (CAR) of each misconduct case to measure market reactions (Podgorski, Citation2020). Following previous studies, we used an estimation period of 240 days ([-300, −60]) before the focal event date (i.e., the date of the misconduct announcement) and four event windows to measure CAR over the short, medium, and long term, which are [-10, 10], [-15, 15], [-20, 20], [-30, 30] (Capelle-Blancard & Laguna, Citation2010; X. Xu et al., Citation2012). Thus, CAR10, CAR15, CAR20, and CAR30 are four dependent variables.

To avoid sample selection bias, we first employ a Heckman two-stage model developed by Heckman (Heckman, Citation1977). In our sample, the premise of the announcement is that the firm has committed misconduct. However, whether a firm is involved in misconduct is not random, so an endogeneity problem related to the missing third variable will be generated if we directly analyze the impact of state ownership on the CARs (Wang et al., Citation2019a). Thus, our two-step equations are respectively specified as follows.

(1)

(1)

(2)

(2)

EquationEquation (1)(1)

(1) shows the first stage, which estimates the decision equation using a Probit model to yield the Inverse Mills Ratio (IMR), where the dependent variable in the decision equation is a binary number. We thus measure Misconduct to identify whether or not a firm engaged in corporate misconduct for all listed firms. Explanatory variables are factors that may affect the misconduct commission. Lennox et al. (Citation2012) argue that imposing exclusion restrictions in implementing the Heckman two-stage regression is important, even though the IMR can be identified by its nonlinear arguments. In other words, we need at least one variable in the first stage model that affects CARs only through its effects on Misconduct. We use Previous as this variable which suggests whether firms had misconduct before. Firm characteristics which affect Misconduct are put in the first stage, including institutional ownership, equity, ROA, DAR, board size, Size, CEO duality, and region (Khanna et al., Citation2015).

The second step employs the generated IMR as the additional explanatory variable in the equation. The estimated effect of state ownership on the dependent variables would be unbiased (M.-W. Wu & Shen, Citation2013), as shown by EquationEq (2)(2)

(2) . We use OLS regression analysis to investigate the relation between CAR and our main variables. CARs are cumulative abnormal returns for four event windows after employing an event study method. The independent variable is state ownership (SO), measured as the equity share of the largest state shareholder in a listed company (Thomsen & Pedersen, Citation2000). Affiliation level (AL) and industry regulation (IR) are two moderators. The Affiliation Level is measured by the administrative level, which is assigned by the affiliated government of the state controlling shareholder (H. Q. Chen et al., Citation2016). We measure Industry Regulation by referring to the Guidance Catalogue for Foreign Investment Industries issued by the Chinese government, which specifies the extent to which foreign investment is encouraged, restricted, and prohibited in each industry (Guan et al., Citation2021). To rule out confounding explanations, we control a set of variables for market reactions to misconduct announcements. At the firm level, we control for firm performance (ROA), firm leverage level (DAR), and firm size (Size) (Liu et al., Citation2022). At the corporate governance level, we control board size (Board) and CEO duality (Duality) (Tampakoudis et al., Citation2022; Vallelado & Garcia-Olalla, Citation2022). At the event level, we control for the effect of the punishment decisions on market reactions. The types of misconduct affect investor reactions, so we construct the variable CATEGORY, a dummy variable. We construct industrial misconduct (IM) to control the trend of misconduct in different industries. We also control for the regulatory body (RB) that announces the punishment decision (Wang et al., Citation2019b). We lag the explanatory variables measured at the firm level for one year to avoid potential endogeneity problems.

illustrates the names, descriptions, and sources of all variables.

Table 1. Variable measurement.

4. Results

4.1. Descriptive statistics and results of event study method

provides descriptive statistics for the variables in both stages, and CARs for four event windows are negative, suggesting the market views misconduct announcements negatively. For example, the CARs are −2.3% over a 20-day [-10, 10] window, consistent with previous research (Chen et al., Citation2005). reports the correlations. Before the main analysis, we inspected the values of variance inflation factors (VIF) to assess our data for multicollinearity. The mean of VIF values for the variables in our regressions models is 1.13, which is much lower than the commonly accepted threshold value of 10 and demonstrates that multicollinearity is not a problem in our data. The results of the event study analysis are reported in , showing the t-test of CAAR()in four windows and indicating that misconduct announcement has a significantly negative impact on the shareholder wealth of disclosed firms four the four event windows.

Table 2. Descriptive statistics.

Table 3. Correlations.

Table 4. t test of CAAR.

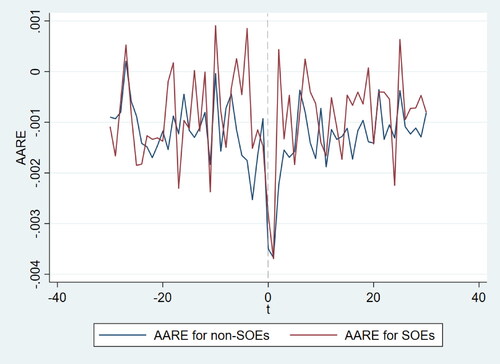

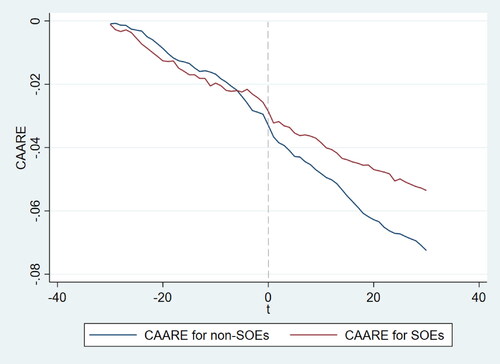

Our study focuses on the impact of state ownership on market reactions to misconduct announcements. Thus, we provide a preliminary demonstration of differences in AAR and CAAR between SOEs and non-SOEs. reports the results of the t-test of difference-in-means of CAAR when we split the sample into non-SOEs and SOEs, indicating that for the four windows, the mean of CAAR for SOEs’ misconduct is significantly higher than that for non-SOEs’ misconduct. and display the variation of AAR each day and CAAR during the event window, respectively, demonstrating that market reactions to SOEs’ misconduct are weaker than non-SOEs’.

Figure 1. AARE for non-SOEs and SOEs during the event window.

Source: Author’s own.

Figure 2. CAARE for non-SOEs and SOEs during the event window.

Source: Author’s own.

Table 5. t test of difference-in-means between non-SOEs and SOEs.

4.2. Results of regression analysis

and present the regression results. Model 1 of reports the result of the first stage using the Probit model, which examines EquationEq (1)(1)

(1) . Model 1 of shows that Previous positively affects Misconduct. The coefficient for Equity is negative and significant (b=-0.193; p < 0.001), indicating that SOEs are less likely to engage in misconduct than non-SOEs, which is consistent with previous research (Shi et al., Citation2020). Models 2-5 of and Models 6-9 of present the regression results when CAR10, CAR15, CAR20, and CAR30 are dependent variables. Hypothesis 1 predicted a positive effect of state ownership on the stock market reaction to a misconduct event. Consistent with this hypothesis, the coefficients for state ownership (

) are positive and significant in all eight models. Hypothesis 2 predicted a negative moderating effect of affiliation level on the relationship between state ownership and market reaction. The coefficients for the interaction between affiliation level and state ownership (

) are negative and significant at the 10% level, supporting hypothesis 2. Hypothesis 3 predicted a positive moderating effect of industry regulation on the main effect. Models 3, 5, and 7 show that the coefficients of interaction terms (

) are positive and significant, and hypothesis 3 is supported.

Table 6. Regression results.

Table 7. Regression results-continued.

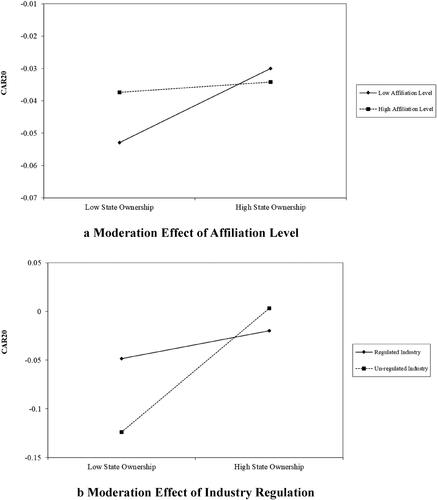

We plotted the moderation effect in . As shows, the line presenting the positive impact of state ownership on CAR becomes flatter when the affiliation level is higher. In , the line becomes steeper when a firm is in a regulated industry. The figures are consistent with our predictions.

Figure 3. (a) Moderation effect of affiliation level. (b) Moderation effect of industry regulation.

Source: Author’s own.

4.3. Robustness check

To ensure the robustness of the above findings, we conduct a robustness check. Following prior studies, we adopt an alternative measure of State Ownership (Xia et al., Citation2014). We measure state ownership as the sum of equity shares of all state owners in the top ten shareholders. We also use the Heckman two-stage model, which is reported in . Model 1, 2, 3, and 4 present regression results for four event windows. The coefficients for state ownership are positive and significant, supporting hypothesis 1. The interaction terms for the two moderators are also significant and are consistent with the predictions for hypotheses 2 and 3.

Table 8. Robustness check.

5. Discussion

Although previous studies confirmed the effectiveness of misconduct announcements issued by regulators in higher misconduct costs by causing investor loss (Chen et al., Citation2005; Wang et al., Citation2019b), this research finds that state ownership of disclosed firms plays an influential role in market reactions. This finding is undertaken by examining the Chinese stock market reaction to misconduct announcements from 2010 to 2021. The study has significant theoretical contributions in the following ways.

First, we provide new sight into understanding investors’ evaluations of organizational illegitimacy by emphasizing the role of state ownership, which is the most critical indicator of organizational legitimacy in emerging economies. Research findings are consistent with previous studies that punishment actions or misconduct nature affect investors’ disapproval of wrongdoing (Gong et al., Citation2021; Wang et al., Citation2019b), but we provide new evidence that investors are confident for SOEs’ legitimate status or even optimistic for SOEs’ remedial actions subsequently, finally responding weaker. This highlights that investors care more about the solidity of ties with governments than the punishment formally enforced by regulators where the legal system is underdeveloped.

Second, we add to the literature by showing that state ownership may reduce the costs of corporate misconduct by buffering negative market reactions. Previous research found that state shareholder plays an orthodox role and is beneficial in deterring financial fraud (Yiu et al., Citation2019). However, extant research overlooks its role in how external audiences perceive, evaluate and judge corporate misconduct and further market reactions. The positive association between state ownership and market reaction may reduce perceived threats of firms with larger state ownership and may, in turn, increase the likelihood of the recurrence of misconduct commission.

Third, this research contributes to understanding the role of identities of controlling shareholders and industry regulation in different aspects of state ownership. Existing literature explains how the identity of controlling shareholders of SOEs (central or local government agencies) affects inappropriate corporate behavior such as fraud and tunneling (Hu & Sun, Citation2019; Yiu et al., Citation2019). From the perspective of market reaction, this study finds that investors are more tolerant of corporate misconduct of local SOEs than central SOEs. Further, industry regulation reinforces the legitimacy advantages of SOEs.

6. Conclusions

This research adopts a legitimacy perspective to investigate the impact of state ownership on market reactions to corporate misconduct announcements. We propose that in emerging economies, investors are more likely to react to corporate misconduct socially-constructed, which means the way they evaluate the negative impact of corporate misconduct on organizational legitimacy is not only dependent on the nature of specific cases as existing literature predicted (Gong et al., Citation2021). We find that if a firm has larger state ownership, the market reaction to misconduct announcements is weaker because investors are confident of organizational legitimacy not being damaged by accidental influences. The affiliation level weakens the relationship between state ownership and market reactions, but industry regulation strengthens the relationship.

6.1. Managerial implication

This study provides important managerial implications. Managers serving in SOEs should act more self-disciplined to avoid misconduct commissions because investors tend to have a favorable opinion of organizational legitimacy and are less likely to make harmful decisions. Shareholders and other external monitoring roles for SOEs should pay attention to deter misconduct as the public reaction will hedge against misconduct costs.

6.2. Practical/social implications

We provide several practical implications for regulators and investors. First, regulators and governments should enhance punishment actions in cases of misconduct by firms owing larger state ownership to improve the cost of corporate wrongdoing. Second, regulators are responsible for enhancing the completeness of information disclosure and providing detailed explanations about punishment decisions to investors according to the severity of corporate misconduct. Third, investors are encouraged to focus on the nature of misconduct cases and make a rational judgment for SOEs’ to avoid the risk of misconduct diffusion due to weaker market reactions.

6.3. Future research

For future research, we call for a more socially-constructed view and an institution-view to understand market reactions to occasional events, which are likely to be influenced by firm-level or institutional-level characteristics (Zajac & Westphal, Citation2004). Ties between firms and formal institutions should be considered when discussing market responses. Moreover, a higher affiliation level of SOEs increases investors’ concerns about the impact of corporate misconduct on organization legitimacy, indicating the distinction between controlling shareholders’ political identities and ownership proportion in SOEs remains theoretically explored and empirically ascertained.

Disclosure statement

No potential conflict of interest was reported by the author.

References

- Allen, F., Qian, J., & Qian, M. (2005). Law, finance, and economic growth in China. Journal of Financial Economics, 77(1), 57–116. https://doi.org/10.1016/j.jfineco.2004.06.010

- Capelle-Blancard, G., & Laguna, M.-A. (2010). How does the stock market respond to chemical disasters? Journal of Environmental Economics and Management, 59(2), 192–205. https://doi.org/10.1016/j.jeem.2009.11.002

- Chen, G., Firth, M., Gao, D. N., & Rui, O. M. (2005). Is China’s securities regulatory agency a toothless tiger? Evidence from enforcement actions. Journal of Accounting and Public Policy, 24(6), 451–488. https://doi.org/10.1016/j.jaccpubpol.2005.10.002

- Chen, H. Q., Li, X. D., Zeng, S. X., Ma, H. Y., & Lin, H. (2016). Does state capitalism matter in firm internationalization? Pace, rhythm, location choice, and product diversity. Management Decision, 54(6), 1320–1342. https://doi.org/10.1108/MD-10-2015-0458

- Chen, J., Cumming, D., Hou, W., & Lee, E. (2016). Does the external monitoring effect of financial analysts deter corporate fraud in China? Journal of Business Ethics, 134(4), 727–742. https://doi.org/10.1007/s10551-014-2393-3

- Deng, Z. L., Yan, J. Y., & Sun, P. (2020). Political status and tax haven investment of emerging market firms: Evidence from China. Journal of Business Ethics, 165(3), 469–488. https://doi.org/10.1007/s10551-018-4090-0

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48, 147–160. https://doi.org/10.2307/2095101

- Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2), 383–417. https://doi.org/10.2307/2325486

- Galloway, T. L., Miller, D. R., & Liu, K. (2021). Guilty by association: Spillover of regulative violations and repair efforts to alliance partners. Journal of Business Ethics, 182, 805–818. https://doi.org/10.1007/s10551-021-05006-9

- Gong, G., Huang, X., Wu, S., Tian, H., & Li, W. (2021). Punishment by securities regulators, corporate social responsibility and the cost of debt. Journal of Business Ethics, 171(2), 337–356. https://doi.org/10.1007/s10551-020-04438-z

- Guan, J., Gao, Z. M., Tan, J., Sun, W. Z., & Shi, F. (2021). Does the mixed ownership reform work? Influence of board chair on performance of state-owned enterprises. Journal of Business Research, 122, 51–59. https://doi.org/10.1016/j.jbusres.2020.08.038

- Guo, H., Tang, J. T., & Su, Z. F. (2014). To be different, or to be the same? The interactive effect of organizational regulatory legitimacy and entrepreneurial orientation on new venture performance. Asia Pacific Journal of Management, 31(3), 665–685. https://doi.org/10.1007/s10490-013-9361-9

- He, X., Cui, L., & Meyer, K. E. (2020). How state and market logics influence firm strategy from within and outside? Evidence from Chinese financial intermediary firms. Asia Pacific Journal of Management, 39, 587–614. https://doi.org/10.1007/s10490-020-09739-5

- Heckman, J. J. (1977). Dummy endogenous variables in a simultaneous equation system. Econometrica, 46(4), 931–959. http://www.jstor.org/stable/1909757 https://doi.org/10.2307/1909757

- Hu, H. W., & Sun, P. (2019). What determines the severity of tunneling in China? Asia Pacific Journal of Management, 36(1), 161–184. https://doi.org/10.1007/s10490-018-9582-z

- Khanna, V., Kim, E. H., & Lu, Y. (2015). CEO connectedness and corporate fraud. The Journal of Finance, 70(3), 1203–1252. https://doi.org/10.1111/jofi.12243

- Lennox, C. S., Francis, J. R., & Wang, Z. (2012). Selection models in accounting research. The Accounting Review, 87(2), 589–616. https://doi.org/10.2308/accr-10195

- Li, H. Y., & Zhang, Y. (2007). The role of managers’ political networking and functional experience in new venture performance: Evidence from China’s transition economy. Strategic Management Journal, 28(8), 791–804. https://doi.org/10.1002/smj.605

- Li, M. H., Cui, L., & Lu, J. (2018). Varieties in state capitalism: Outward FDI strategies of central and local state-owned enterprises from emerging economy countries. In State-owned multinationals (pp. 175–210). Springer. https://doi.org/10.1057/jibs.2014.14

- Liu, C., Wang, S. L., & Li, D. (2022). Hidden in a group? Market reactions to multi‐violator corporate social irresponsibility disclosures. Strategic Management Journal, 43(1), 160–179. https://doi.org/10.1002/smj.3330

- Marquis, C., & Qian, C. (2014). Corporate social responsibility reporting in China: Symbol or substance? Organization Science, 25(1), 127–148. https://doi.org/10.1287/orsc.2013.0837

- McWilliams, A., & Siegel, D. (1997). Event studies in management research: Theoretical and empirical issues. Academy of Management Journal, 40(3), 626–657. https://doi.org/10.5465/257056

- Meyer, J. W., & Rowan, B. (1977). Institutionalized organizations: Formal structure as myth and ceremony. American Journal of Sociology, 83(2), 340–363. https://doi.org/10.1086/226550

- Musacchio, A., Lazzarini, S. G., & Aguilera, R. V. (2015). New varieties of state capitalism: Strategic and governance implications. Academy of Management Perspectives, 29(1), 115–131. https://doi.org/10.5465/amp.2013.0094

- Palmrose, Z. V., & Scholz, S. (2004). The circumstances and legal consequences of non‐GAAP reporting: Evidence from restatements. Contemporary Accounting Research, 21(1), 139–180. https://doi.org/10.1506/WBF9-Y69X-L4DX-JMV1

- Pan, X., Chen, X. J., & Li, X. B. (2019). To fit in or stand out? How optimal distinctiveness in technological diversification affects firm performance. European Management Journal, 37(1), 67–77. https://doi.org/10.1016/j.emj.2018.07.004

- Peng, M. W. (2003). Institutional transitions and strategic choices. Academy of Management Review, 28(2), 275–296. https://doi.org/10.5465/amr.2003.9416341

- Peng, M. W., Bruton, G. D., Stan, C. V., & Huang, Y. Y. (2016). Theories of the (state-owned) firm. Asia Pacific Journal of Management, 33(2), 293–317. https://doi.org/10.1007/s10490-016-9462-3

- Podgorski, B. (2020). Market reactions to unexpected political changes: Evidence from advance emerging markets. Economic Research-Ekonomska Istrazivanja, 33(1), 1562–1580. https://doi.org/10.1080/1331677X.2020.1756370

- Rodrik, D. (2008). Industry Policy For The Twenty First Century. Harvard University, Harvard Kennedy School (HKS).

- Scott, W. R. (1995). Institutions and organizations (Vol. 2). Sage.

- Shi, W., Aguilera, R., & Wang, K. (2020). State ownership and securities fraud: A political governance perspective. Corporate Governance: An International Review, 28(2), 157–176. https://doi.org/10.1111/corg.12313

- Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review, 20(3), 571–610. https://doi.org/10.5465/amr.1995.9508080331

- Suddaby, R., Bitektine, A., & Haack, P. (2017). Legitimacy. Academy of Management Annals, 11(1), 451–478. https://doi.org/10.5465/annals.2015.0101

- Tampakoudis, I., Noulas, A., & Kiosses, N. (2022). The market reaction to syndicated loan announcements before and during the COVID-19 pandemic and the role of corporate governance. Research in International Business and Finance, 60, 101602. https://doi.org/10.1016/j.ribaf.2021.101602

- Thomsen, S., & Pedersen, T. (2000). Ownership structure and economic performance in the largest European companies. Strategic Management Journal, 21(6), 689–705. https://doi.org/10.1002/(SICI)1097-0266(200006)21:6<689::AID-SMJ115>3.0.CO;2-Y

- Tihanyi, L., Aguilera, R. V., Heugens, P., Van Essen, M., Sauerwald, S., Duran, P., & Turturea, R. (2019). State ownership and political connections. Journal of Management, 45(6), 2293–2321. https://doi.org/10.1177/0149206318822113

- Vallelado, E., & Garcia-Olalla, M. (2022). Bank board changes in size and composition: Do they matter for investors? Corporate Governance-an International Review, 30(2), 161–188. https://doi.org/10.1111/corg.12397

- Wang, Y., Ashton, J. K., & Jaafar, A. (2019a). Does mutual fund investment influence accounting fraud? Emerging Markets Review, 38, 142–158. https://doi.org/10.1016/j.ememar.2018.12.005

- Wang, Y., Ashton, J. K., & Jaafar, A. (2019b). Money shouts! How effective are punishments for accounting fraud? British Accounting Review, 51(5), 100824. https://doi.org/10.1016/j.bar.2019.02.006

- Wu, H. Y., Li, S. H., Ying, S. X., & Chen, X. (2018). Politically connected CEOs, firm performance, and CEO pay. Journal of Business Research, 91, 169–180. https://doi.org/10.1016/j.jbusres.2018.06.003

- Wu, M.-W., & Shen, C.-H. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking & Finance, 37(9), 3529–3547. https://doi.org/10.1016/j.jbankfin.2013.04.023

- Xia, J., Ma, X., Lu, J. W., & Yiu, D. W. (2014). Outward foreign direct investment by emerging market firms: A resource dependence logic. Strategic Management Journal, 35(9), 1343–1363. https://doi.org/10.1002/smj.2157

- Xie, X., Shen, W., & Zajac, E. J. (2021). When is a governmental mandate not a mandate? Predicting organizational compliance under semicoercive conditions. Journal of Management, 47(8), 2169–2197. https://doi.org/10.1177/0149206320948579

- Xu, D., & Meyer, K. E. (2013). Linking theory and context: 'Strategy research in emerging economies’ after Wright et al. (2005). Journal of Management Studies, 50(7), 1322–1346. https://doi.org/10.1111/j.1467-6486.2012.01051.x

- Xu, W., Chen, J., & Xu, G. (2017). An empirical analysis of the public enforcement of securities law in China: Finding the missing piece of the puzzle. European Business Organization Law Review, 18(2), 367–389. https://doi.org/10.1007/s40804-017-0070-6

- Xu, X., Zeng, S., & Tam, C. M. (2012). Stock market’s reaction to disclosure of environmental violations: Evidence from China. Journal of Business Ethics, 107(2), 227–237. https://doi.org/10.1007/s10551-011-1035-2

- Yiu, D. W., Wan, W. P., & Xu, Y. (2019). Alternative governance and corporate financial fraud in transition economies: Evidence from China. Journal of Management, 45(7), 2685–2720. https://doi.org/10.1177/0149206318764296

- Zajac, E. J., & Westphal, J. D. (2004). The social construction of market value: Institutionalization and learning perspectives on stock market reactions. American Sociological Review, 69(3), 433–457. https://doi.org/10.1177/000312240406900306

- Zeidan, M. J. (2013). Effects of illegal behavior on the financial performance of US banking institutions. Journal of Business Ethics, 112(2), 313–324. https://doi.org/10.1007/s10551-012-1253-2

- Zhang, L., Xu, Y. H., Chen, H. H., & Jing, R. T. (2020). Corporate philanthropy after fraud punishment: An institutional perspective. Management and Organization Review, 16(1), 33–68. https://doi.org/10.1017/mor.2019.41

- Zhang, X. W., Wang, L. X., & Chen, F. (2021). R&D subsidies, executive background and innovation of Chinese listed companies. Economic Research-Ekonomska Istrazivanja, 34(1), 484–497. https://doi.org/10.1080/1331677X.2020.1792324

- Zhou, K. Z., Gao, G. Y., & Zhao, H. (2017). State ownership and firm innovation in China: An integrated view of institutional and efficiency logics. Administrative Science Quarterly, 62(2), 375–404. https://doi.org/10.1177/0001839216674457

- Zimmerman, M. A., & Zeitz, G. J. (2002). Beyond survival: Achieving new venture growth by building legitimacy. Academy of Management Review, 27(3), 414–431. https://doi.org/10.2307/4134387