?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Despite the harmonisation process within the EU area, there are many economic and political differences among European countries in promoting energy policies. Moreover, the status of implementation of environmental tax reforms in the new EU countries is very different from that in the old EU countries, and the economic and environmental impacts of such taxation are diverse. The objective of this paper was therefore to investigate whether the role of environmental taxes in reducing final energy consumption is the same in old and new EU countries. The analysis was conducted for 16 old and 11 new EU member states over the period 1995–2020 using Pooled Mean Group (PMG) and Mean Group (MG) estimators. The results indicate that environmental taxes have a negative long-term impact on final energy consumption in both groups of countries. However, this impact is much smaller in the new EU countries. Moreover, economic growth and greenhouse gas emissions increase final energy consumption. These results also suggest that in order to achieve climate neutrality by 2050, the new EU countries need to apply some stringent regulations and introduce further institutional and environmental reforms that support increasing the share of clean energy sources in the energy mix.

1. Introduction

The recent challenges of climate change and the global COVID −19 pandemic have led many scientists to examine how to make the best economic use of resources while minimizing their harmful effects on the environment. As a result, numerous agreements and declarations have been signed. For example, the goal of the Paris Agreement (United Nations (UN), Citation2015) is to limit global warming to below 2.0, preferably 1.5 degrees Celsius. This requires deep emission reductions where immediate action is needed. In Europe, effective action requires the cooperation of all member states to achieve the European Union’s (EU) climate targets: reduce greenhouse gas (GHG) emissions by 55% by 2030 compared to 1990, increase the share of renewable energy to 40%, and improve energy efficiency by 32.5% (European Commission [EC], 2014, 2022). To tackle the problem of global warming, the EU has adopted the European Green Deal Initiative (EC, Citation2019), which consists of a set of policy instruments to reduce GHG emissions to zero and make Europe climate neutral by 2050. The main sources of GHG emissions are energy production and consumption. Final energy consumption in the EU increased slowly since 1994 until it reached its highest level in 2006. However, by 2020, final energy consumption in the EU decreased by 10.5% from its peak. In addition, GHG emissions also decreased by 31% compared to 1990, due to the impact of the pandemic on energy consumption, but also to ongoing decarbonisation trends such as the switch from fossil fuels to renewables (Eurostat, Citation2021). The share of renewable energy sources in the total EU energy mix reached 22.1% in 2020, although some Member States are at risk of missing their national binding target (Eurostat, Citation2022b). Under the REPowerEU plan (EC, Citation2022), the Commission proposed to further increase the share of renewable energy to 45% by 2030. The expected resurgence of energy demand in 2021 and 2022 will make reaching the proposed 2030 target more difficult than the 2020 target. Member States and the EU as a whole will therefore need to take additional measures in all energy sectors and rapidly advance the introduction of renewable energy and energy efficiency measures, with environmental taxes being one of the most important instruments.

Environmental taxes allow the internalisation of the external costs of air pollution in the energy sector. They are also the main economic instrument to mitigate the environmental impacts of various economic activities. Given the importance of the energy sector in terms of its contribution to total atmospheric emissions in the EU, environmental taxes are important drivers of sustainable energy development. They are levied to provide incentives for reducing fossil fuel consumption and switching to renewable energy sources or fuels that have lower carbon content and thus cause less pollution. Environmental taxes as a fiscal policy tool should ensure fiscal sustainability by raising revenue and may have distributional implications. According to Eurostat, environmental taxes are divided into four main categories: energy taxes, transport taxes, pollution taxes, and resource taxes. Energy taxes include taxes on energy products (e.g., coal, oil products, natural gas, and electricity) used for stationary and transport purposes. This tax category also includes taxes on CO2, as they are usually levied on energy products. Transport taxes mainly include taxes on the ownership and use of motor vehicles. Taxes on pollution and resource use include taxes on various air and water emissions, solid waste disposal, noise, and taxes on the extraction and use of natural resources (e.g., oil, gas, water).

At the level of the 27 EU member states, environmental tax revenues have doubled from EUR 166 billion in 1995 to EUR 325 billion in 2021 (Eurostat, Citation2023). However, this growth is mainly due to the increase in revenues in the new EU countries. In Bulgaria, Estonia, Latvia, Poland, and Slovakia, revenues from environmental taxes more than doubled between 2002 and 2019. In the old EU countries, on the other hand, revenues from environmental taxes are steadily declining and in 2021 were 26% lower than in 1995. The contributions of environmental taxes to the financing of country budgets also show large differences, ranging from 4.5% in Germany and Luxembourg to around 10% in Greece and Bulgaria (Eurostat, Citation2023).

Regardless of increasing green awareness in the EU, the share of revenues from environmental taxes in total taxes have declined (from 6.7% in 1995 to 5.4% in 2021), for several reasons. First, countries are increasingly using other instruments as part of their environmental policies. Second, due to rising oil prices, there is growing political pressure to reduce excise duties on motor fuels to at least partially mitigate this increase. Third, countries are implementing measures to increase energy efficiency and consequently decrease energy consumption. However, this effect is somewhat weaker in the new EU member states due to the older technological structure in place and higher energy intensity.

The EU must implement an energy policy in solidarity with all member states. This also relates to the new EU countries that joined the EU after 2004 and whose economic development and potential is at a lower level than that of the old EU countries. Since the economies of the new EU countries are based on conventional energy sources that consume a lot of energy, and due to investment problems, these countries will be much slower to achieve the above goals. In addition, there have been many positive changes in the development of sustainable energy in these countries as well. They have reduced the pollutant-intensive industries in the economy and invested in modern technologies to deal with the existing environmental burdens. Many new EU countries have adapted existing economic instruments and increased environmental taxes to support and encourage environmental improvements.

According to the above statement, the main objective of this paper is to investigate the relationship between environmental taxes and final energy consumption in the old and new EU countries in the period 1995–2020, taking into account GHG emissions and economic growth. The main motivation for this paper is to investigate whether environmental taxes reduce final energy consumption equally in old and new EU countries. Another contribution is to examine whether EU environmental policies have been successful so far. The analysis conducted in this paper aims to correct the shortcomings of most studies published so far, which focus mainly on the EU as a whole or only on the new EU countries. The distinction between old and new EU countries is made because both groups of countries share similar political and economic characteristics that indicate similar trends in environmental taxes, energy consumption, and economic growth. They all need to reduce fossil fuel consumption and GHG emissions to meet the European Green Deal targets (EC, Citation2019) and support the Sustainable Development Goals (UN, Citation2015). Therefore, our main hypothesis is that environmental taxes have a negative impact on final energy consumption in both groups of countries. However, this influence is expected to be smaller in the new EU countries. The novelty of our study is that this is the first paper to empirically investigate and compare the impact of environmental taxes on final energy consumption in the old and new EU countries. The obtained research results could provide some interesting policy guidelines for the post COVID − 19 period.

The rest of the paper is organised as follows. The introduction is followed by a brief literature review of the main studies and results. The data and research methods are described in the following section. Section four discusses the results and implications for energy policy, while section five provides concluding remarks, limitations of the research, and recommendations for further research.

2. Literature review

Climate change has forced EU countries to accelerate the transition to sustainable development. However, this is not possible without environmental policy reforms and appropriate economic instruments such as environmental taxes. Most empirical studies have confirmed that higher environmental taxation has positive environmental effects. However, the existing literature there are no alliances on the impact of environmental taxes on energy consumption. The main role of environmental taxes is to prevent pollution, but also to improve environmental quality without jeopardising economic growth.

Bashir, Ma, et al. (Citation2021) examined the role of environmental taxes in minimising energy consumption and energy intensity using a sample of 29 OECD countries over the period 1994–2018, and their results show that environmental taxes help control total energy consumption and promote energy efficiency. They recommend that innovative policies should focus on adopting environmentally friendly technologies for sustainable development and reducing energy consumption from fossil fuels. Similarly, Doğan et al. (Citation2022) examined the marginal effects of an environmental tax on traditional energy consumption, natural resource rent, and renewable energy consumption using a sample of G7 countries over the period 1994–2014. Their results suggest that environmental taxes reduce emissions and have a marginal effect on energy consumption. The results also suggest that environmental tax laws help firms shift their production to environmentally friendly sources. Ahmed et al. (Citation2022) examined the relationship between ecotaxes, energy intensity, and energy consumption in the Nordic countries over the period 1994–2020. Using econometric methods such as fully modified ordinary least squares, dynamic ordinary least squares, and panel quantile regression, they found that ecotaxes contribute to reducing total energy consumption in the Nordic countries.

Environmental taxes encourage industry to reduce energy consumption and invest in green technologies; however, countries need to build a green financing system to promote clean energy (Bashir, Benjiang, et al., Citation2021). Shahzad et al. (Citation2021) analysed the impact of environmental taxes, environmental policy stringency index and technologies on renewable electricity generation based on a sample of 29 developed countries during 1994–2018, concluding that factors such as technologies, urbanisation, and the environmental stringency index have a favourable impact on renewable energy. Analysing 18 Latin American and Caribbean countries, Wolde-Rufael and Mulat-Weldemeskel (Citation2022) found that environmental taxes and renewable energy improve environmental quality. The authors argue that environmental taxes enable the reduction of CO2 emissions and promote the use of renewable energy. He et al. (Citation2019) argue that the introduction of taxes can be a path to sustainable transformation. Dogan et al. (Citation2022) studied the impact of green growth and environmental taxes on CO2 emissions in 25 environmentally friendly countries during 1994–2018 and found that environmental taxes, renewable energy, and energy efficiency are important components for reducing CO2 emissions. Sharif et al. (Citation2023) found similar results for Nordic countries, while Depren et al. (Citation2023) found mixed results for the same group of countries. In addition, Maxim and Zander (Citation2019) concluded that environmental taxes are the most important instrument to promote green tax reforms. Ghazouani et al. (Citation2021) analysed nine European economies (Belgium, the Czech Republic, France, Germany, Italy, the Netherlands, Poland, Spain, and the UK) over the period 1994-2018 and concluded that taxes and energy policies are effective tools to promote a clean and green EU. A study by Fang et al. (Citation2023) examined the relationship between green tax policies and energy transformation in China. They found that green tax policies have a positive effect on energy consumption transformation, but this positive effect decreases as the intensity of the green tax increases.

On the other hand, Liobikienė et al. (Citation2019) showed that energy tax policies are ineffective by analysing EU-28 countries during 1995–2012. The authors argue that tax policies should be reformed and combined with an emissions trading scheme to mitigate climate change. Morley (Citation2012) analysed 23 European countries and Norway over the period 1995–2006 and found that environmental taxes have a negative effect on carbon emissions but no effect on energy consumption. Aydin and Esen (Citation2018) studied the impact of environmental taxes on CO2 emissions in the 15 EU member states during 1995–2013 and found that environmental taxes reduce CO2 emissions, but only above a threshold of 3.02%. However, Silajdzic and Mehic (Citation2018) examined the same effects in ten Central and Eastern European economies over the period 1995–2015 and found that environmental taxes do not appear to be effective in protecting the environment.

Miller and Vela (Citation2013) examined the effectiveness of environmental taxes in 50 countries, most of which are part of the OECD. Using a cross-sectional regression and a dynamic panel regression, they found that countries with higher revenues from environmental taxes experienced greater reductions in CO2 emissions and energy consumption. According to Gore et al. (Citation2022), EU member states with greener tax systems, where polluters bear a larger share of the cost of their environmental damage, tend to have more progressive tax systems and lower inequality. In many EU countries, there is considerable scope for progressive environmental tax reforms. In the new EU countries in particular, there is scope for shifting taxes from the low-income earners to the environment and the high-income earners. The new EU countries have specificities in terms of economic structure, nature of transition, and intensity of CO2 emissions that present several structural, institutional, and policy barriers that have led to delays in environmental reforms in these economies. For example, Gurkov (Citation2015) found that countries that were first in transition experienced high price volatility, declining growth, and high unemployment. For example, Zugravu et al. (Citation2008) found that environmental policy reforms in the new EU countries led to a 58% decline in emissions from 1990 levels. They emphasise the importance of strong institutions in the pursuit of a cleaner environment. Similarly, studying a panel of 14 new EU countries, Bercu et al. (Citation2019) found that good governance and strong institutions could impact energy consumption and lead to higher energy efficiency in the new EU countries. Hodžić and Bratić (Citation2015) concluded that environmental taxes in the EU lead to increased revenues and economic growth. Huang et al. (Citation2008) found that economic growth leads to higher energy consumption in middle-income countries. In high-income countries, on the other hand, economic growth has a negative impact on energy consumption, as the environment improves greatly due to more efficient energy use and lower CO2 release. Based on the above arguments, there is not yet sufficient evidence in the literature on the relationship between environmental taxes and energy consumption in the old and new EU countries. Therefore, the main hypothesis of this paper is that environmental taxes have a negative impact on final energy consumption in both group of countries.

3. Data and model

This paper examines the relationship between final energy consumption, environmental taxes, GHG emissions, and economic growth in 16 old (Austria, Belgium, Cyprus, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, Netherlands, Portugal, Spain, Sweden) and 11 new EU countries (Bulgaria, Czech Republic, Croatia, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia, and Slovenia) over the period 1995–2020. All annual data were collected from the Eurostat. The Pooled Mean Group estimator (PMG) and the Mean Group (MG) estimator were used to analyse the long-term and short-term relationship between the variables.

In view of the above, the model is specified as follows:

(1)

(1)

the indices i and t denote the country and the period, respectively. In the above model, the dependent variable is final energy consumption (FEC) in thousand tonnes of oil equivalent (TOE), while the independent variables are total environmental taxes in millions of euros (ENVTAX), gross domestic product at market prices in millions of euros (GDP), and greenhouse gas emissions (excluding LULUCF and memo items, including international transport) in millions of tonnes (GHG). In the rest of the analysis, the logarithmized values of the variables are used. summarises the descriptive statistics of the analysed variables for 16 old and 11 new EU countries. For each variable, the mean, standard deviation, minimum and maximum values were calculated. The STATA 14 programme was used to estimate the relationship between the variables.

Table 1. Descriptive statistics.

The descriptive statistics show that the observed variables vary widely across the old and new EU countries. In the old EU countries, average GDP and environmental tax revenues are seven times higher than in the new EU countries, while average final energy consumption is three times higher. In both groups of countries, the standard deviation is highest for GDP, but lowest for GHG emissions. and show the development of the variables used in the analysis, separately for the old and new EU countries.

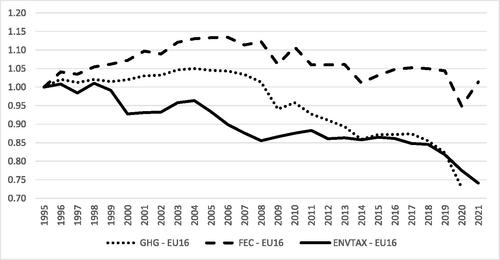

Figure 1. The change in final energy consumption, revenues from environmnetal tax and greenhouse gas emissions in old EU countries (index 1995 = 100). Source. Authors calculation based on data from Eurostat (Citation2023).

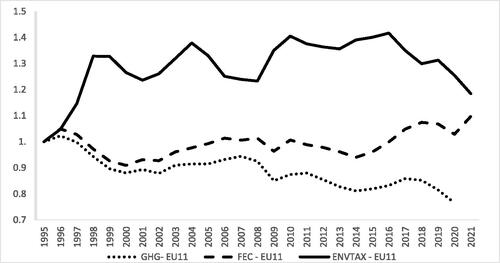

Figure 2. The change in final energy consumption, revenues from environmental tax and greenhouse gas emissions in new EU countries (index 1995 = 100). Source. Authors calculation based on data from Eurostat (Citation2023).

It can be clearly seen that revenues from environmental taxes and GHG emissions in the old EU countries show a declining trend, especially after 2005, when the Kyoto Protocol came into force. Final energy consumption increased until 2006, but declined steadily thereafter, demonstrating the success of EU energy policy. The next figure shows the development of variables in the new EU countries.

Compared to the old EU countries, the new member states experienced a higher increase in environmental taxes until 2016 (41% compared to 1995), after which a decreasing trend is observed. This is mainly due to the fact that they had to adapt to EU energy policies and existing economic instruments, while increasing environmental taxes to support and encourage environmental improvements. Nevertheless, final energy consumption shows an increasing trend, especially after 2014. It is surprising that despite the increasing energy consumption, GHG emissions have continuously decreased and in 2020 they were 25% lower than in 1995. One of the reasons is that the pollution-intensive industries in the economy have been reduced and environmental taxes have been increased to deal with the existing environmental burdens.

Empirical analysis begins by examining cross-sectional dependence because it can lead to inconsistent and biased empirical results (Phillips & Sul, Citation2003). From an economic perspective, cross-sectional dependence is justified by the EU membership of the countries in the panel and the historical developments that brought new EU countries into the same communist sphere of influence before 1990. From a statistical point of view, cross-sectional dependence (CD) is tested using the empirical test proposed by Pesaran (Citation2004). After confirming CD, we performed the second generation unit root tests because they can overcome the problem of low significance for CD. For this purpose, we chose the Breitung unit root test (Breitung, Citation2000; Breitung & Das, Citation2005) and the Cross-sectionally Augmented Dickey-Fuller (CADF) panel unit root test (Pesaran, Citation2007) because these statistical tests account for heterogeneity and cross-sectional dependence throughout the data set.

To determine whether or not the variables under consideration move together in the long run, we use the Pedroni panel cointegration test (Pedroni, Citation1999) and the Westerlund panel cointegration test (Westerlund, Citation2005). Since the cointegration relationship has been established, this paper uses an autoregressive distributive lag (ARDL) panel model using the PMG (Pesaran et al., Citation1999) and the MG estimator (Pesaran & Smith, Citation1995).

The PMG estimator is used to determine the short and long run relationship between selected variables and final energy consumption. PMG estimator accounts for heterogeneous short-run dynamics and identical long-run coefficients across countries. Two types of relationships can be evaluated: a short-run relationship related to the lagged differences of the selected variables, and a long-run relationship related to error correction term (ECT). To confirm a long-run relationship between the selected variables, the ECT must be negative. The main advantage of the PMG estimator is that the intercept, slope coefficient, and error variance can vary across countries, allowing for heterogeneity across countries. A disadvantage of the PMG estimator is if time series are not long enough there is a problem with degrees of freedom (Gemmell et al., Citation2016). An alternative model specification is the MG, which does not take to the account that across countries there might be the same economic conditions in the long run (Sulaiman & Abdul-Rahim, Citation2020).

EU member states are subject to the same environmental policies to achieve the pollution reduction targets set by European Green Deal (EC, Citation2019). Legislation associated to mitigating climate challenges sets pollution reduction targets through a number of common measures such as improving energy efficiency, increasing the use of renewable energy, and energy conservation. We therefore anticipate that there will be differences in baseline levels of energy consumption between the old and new EU countries, due to different levels of economic development. However, EU energy policy has common goals for all EU countries in terms of energy savings.

4. Empirical results and discussion

The empirical results of the CD and second-generation unit root tests are presented in and confirm the existence of a cross-section in the data set. After confirming CD in the data, we examined the integrated level of the variables using the Breitung (Breitung, Citation2000; Breitung & Das, Citation2005) and the cross-sectionally extended Dickey-Fuller (CADF) panel unit root test (Pesaran, Citation2007). The unit root tests showed that almost all variables have unit root problems at the level, except for environmental tax and GDP in the new EU countries, but the data series become stationary at first difference with both tests.

Table 2. Results of cross-sectional and unit-root tests.

The results of the CD and the second-generation unit root test contribute to the implementation of the Pedroni panel cointegration test (Pedroni, Citation1999) and the Westerlund panel cointegration test (Westerlund, Citation2005). These tests can be used to determine if there is a long-term stochastic trend between variables. The results of the cointegration tests are presented in .

Table 3. Panel cointegration test results.

The empirical estimates, based on robust pvalue, provide strong evidence of cointegration between the data sets. Thus, we can conclude that the analysed variables exhibit a long-run relationship. contains the results that help to choose the best estimation method by comparing the PMG estimates with those obtained with the MG method.

Table 4. Estimation results of the dynamic panel model.

The test for differences between the PMG and MG models is performed using the well-known Hausman test. According to the Hausman test, the PMG model should be chosen for both groups of EU countries.

Using a PMG estimator, the results showed that in 16 old EU countries, changes in environmental tax revenues have a negative impact on final energy consumption in the short and long run. The negative coefficient confirms that environmental taxes are an effective policy tool to prevent environmental degradation, which can be attributed to sustainable energy policies. These results also suggest that overall energy consumption can be controlled through strict regulations and tax reforms, which in turn helps to achieve the goals of sustainable development and cleaner production in EU countries. Although revenues from environmental taxes in the old EU countries have declined steadily over the past twenty years, they appear to have a significant impact on final energy consumption. These results are consistent with those of Bashir, Ma, et al. (Citation2021) for OECD countries, Doğan et al. (Citation2022) for G7 countries and Ahmed et al. (Citation2022) for Nordic countries. Results are inconsistent with those of Liobikienė et al. (Citation2019) for EU-28 countries and Morley (Citation2012) for EU-23 countries and Norway.

The PMG estimation results show that in the new EU countries changes in environmental taxes also have a negative impact on final energy consumption, but only in the long run and much smaller than in the old EU countries. The long-run coefficient for environmental taxes is statistically significant, indicating that a 1% increase in revenue from environmental taxes decreases final energy consumption by only 0.03%, compared to 0.10% in the old EU countries. The results are consistent with the findings of Miller and Vela (Citation2013), who analysed the effectiveness of environmental taxes in 50 mostly OECD countries. They found that countries with higher revenues from environmental taxes experience greater reductions in CO2 emissions and energy consumption.

Economic growth has a significant and positive long-term impact on final energy consumption in both groups of countries. In the short term, it has a positive effect only in the old EU countries, while it is insignificant in the new EU countries. The coefficient of economic growth is 0.207 in the old EU countries and 0.187 in the new EU countries, which means that a 1% increase in GDP increases final energy consumption by 0.207% in the old EU countries and 0.187% in the new EU countries. Therefore, effective and efficient policies should prioritise clean energy sources in both groups of EU countries. The results are inconsistent with those of a study on this topic by Huang et al. (Citation2008), who found that economic growth leads to higher energy consumption only in middle-income countries because high-income countries invest in improving the environment and use energy more efficiently. The relationship between economic growth and final energy consumption suggests that both group of EU countries still need to promote the decoupling of economic growth from energy consumption. The new EU countries do not yet have the same level of economic development as the old EU countries, and therefore energy consumption will not decrease if they improve their economic growth.

GHG emissions have a positive and significant impact on final energy consumption in both groups of countries in the short and long term. A 1% increase in GHG emissions is expected to increase final energy consumption by 0.421% in the old EU countries and by 0.546% in the new EU countries. Our results are consistent with the findings of Saidi and Hammami (Citation2015), who concluded that economic growth and CO2 emissions have a positive impact on per capita energy consumption in EU countries. Also, according to Zaharia et al. (Citation2019), energy consumption is boosted by an increase in GHG emissions and GDP in EU countries.

The PMG estimator results indicate that the ECT coefficients are significantly negative in both groups of countries, representing a steady and converging long-run relationship between environmental taxes, final energy consumption, GDP, and GHG emissions. It can be concluded that the deviation from their long-term equilibrium is gradually decreasing. The value for the adjustment rate of the estimation discrepancy shows a correction of 29.5% in the old EU countries and 31.6% in the new EU countries. In other words, 29.5% and 31.6%, respectively, of the imbalance observed in the previous year are corrected in the current year.

The results of the econometric analysis confirm the main hypothesis that environmental taxes reduce final energy consumption in both groups of countries, which means that a higher tax rate is directly associated with lower final energy consumption. However, this effect is much smaller in the new EU countries than in the old ones. Although the new EU countries have increased environmental taxes, the total revenue from them is still seven times lower than in the old EU countries. These results also suggest that to achieve climate neutrality by 2050, the new EU countries will need to adopt some stringent environmental practises and introduce additional institutional and environmental reforms that support the growth of renewable energy. However, due to the significantly lower GDP in the new EU countries, implementing further environmental reforms will be much more difficult for these countries.

Although the EU aims for an internal energy market and common energy targets for all member states, different energy policies need to be implemented for each group of countries. The research results obtained represent a major challenge for economic and energy policy makers in the countries studied. The above results have significant implications for the development of economic and energy policies, especially in relation to environmental reforms and energy conservation measures.

5. Conclusion

Environmental awareness is pushing policymakers to pursue sustainable economic practises with the dual goal of combining economic efficiency with reduced environmental impacts. EU countries use environmental taxes primarily to address environmental problems and reduce other taxes. The main objective is to analyse the role of environmental taxes in reducing final energy consumption in old and new EU countries in order to find new solutions to climate change problems caused by increasing energy demand. This paper traces the success of environmental taxes in EU countries to assess how they can be used to achieve EU targets and the Sustainable Development Goals. Panel data were collected for 16 old and 11 new EU countries from 1995 to 2020. To identify the potential impacts between final energy consumption and its determinants, PMG and MG estimators were used to examine the long and short term outcomes and impacts.

EU countries differ in terms of economic development, energy consumption, and environmental reforms implemented. The old EU member states have already transformed their economies to service-oriented and low energy-intensive industries. In addition, the old EU countries have been successful in using clean energy and increasing energy efficiency, which is crucial for reducing GHG emissions. It will be much more difficult for the new EU countries to achieve the targets set under the European Green Deal due to their higher energy intensity and much lower GDP.

Consistent with the theoretical literature and the empirical results, the empirical findings show that environmental taxes have a negative impact on final energy consumption in both groups of EU countries. The empirical evidence suggests that environmental taxes are effective in reducing final energy consumption, which in turn helps to achieve sustainable development and clean production goals in EU countries. However, this effect is much smaller in the new EU countries, even though they have doubled the revenue from environmental taxes. Economic growth and GHG emissions have a positive impact on final energy consumption, which means that effective and efficient policies should prioritise clean energy sources in EU countries.

The recommendation to policymakers is that to address climate challenges, the EU needs fundamental and rapid change in all sectors of the economy and urgent reform of environmental taxes. The new EU countries need to figure out how to link their economic growth with energy savings and emissions reductions. To respond to global climate change, innovative technologies for energy use must be transformed, and the clean development mechanism must be implemented. Policymakers are recommended to focus on reducing energy consumption through various instruments such as incentives or tax reductions, and to promote the importance of energy savings and energy efficiency in all sectors of the economy. In addition, environmental taxes can reduce manufacturing costs and the environmental footprint of businesses. This can be achieved through the implementation of effective administrative policies and regulations.

The limitations of this study are the variables chosen and the sample of EU countries. The conclusions may not be generalizable to other countries or regions due to differences in economic, political, and cultural factors. There are many opportunities for future research by including different variables such as renewable energy sources, energy efficiency, and CO2 emissions to evaluate public policies that can contribute to carbon neutrality and green growth. The use of the new data for 2021 and 2022 will bring a new dynamic due to the drastic changes in the economic environment caused by the COVID −19 pandemic, but also by the war between Russia and Ukraine.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Ahmed, N., Sheikh, A. A., Hamid, Z., Senkus, P., Borda, R. C., Wysokińska-Senkus, A., & Glabiszewski, W. (2022). Exploring the causal relationship among green taxes, energy intensity, and energy consumption in nordic countries: Dumitrescu and Hurlin causality approach. Energies, 15(14), 5199. https://doi.org/10.3390/en15145199

- Aydin, C., & Esen, Ö. (2018). Reducing CO2 emissions in the EU member states: Do environmental taxes work? Journal of Environmental Planning and Management, 61(13), 2396–2420. https://doi.org/10.1080/09640568.2017.1395731

- Bashir, F. M., Ma, B., Bashir, M. A., Radulescu, M., & Shahzad, U. (2021). Investigating the role of environmental taxes and regulations for renewable energy consumption: Evidence from developed economies. Economic Research-Ekonomska Istraživanja, 35(1), 1262–1284. https://doi.org/10.1080/1331677X.2021.1962383

- Bashir, F. M., Benjiang, M. A., Shahbaz, M., Shahzad, U., & Vo, X. V. (2021). Unveiling the heterogeneous impacts of environmental taxes on energy consumption and energy intensity: Empirical evidence from OECD countries. Energy, 226, 120366. https://doi.org/10.1016/j.energy.2021.120366

- Bercu, A.-M., Paraschiv, G., & Lupu, D. (2019). Investigating the energy–economic growth–governance nexus: Evidence from Central and Eastern European countries. Sustainability, 11(12), 3355. https://doi.org/10.3390/su11123355

- Breitung, J. (2000). The local power of some unit root tests for panel data. In B. H. Baltagi (Ed.), Advances in econometrics: Nonstationary panels, panel cointegration, and dynamic panels (Vol. 15, pp. 161–178). JAI Press.

- Breitung, J., & Das, S. (2005). Panel unit root tests under cross-sectional dependence. Statistica Neerlandica, 59(4), 414–433. https://doi.org/10.1111/j.1467-9574.2005.00299.x

- Depren, Ö., Kartal, M. T., Ayhan, F., & Depren, S. K. (2023). Heterogeneous impact of environmental taxes on environmental quality: Tax domain based evidence from the nordic countries by nonparametric quantile approaches. Journal of Environmental Management, 329, 117031. https://doi.org/10.1016/j.jenvman.2022.117031

- Doğan, B., Chu, L. K., Ghosh, S., Truong, H. H. D., & Balsalobre-Lorente, D. (2022). How are environmental tax and carbon emissions related in the G7 economies? Renewable Energy. 187, 645–656. https://doi.org/10.1016/j.renene.2022.01.077

- Dogan, E., Hodžić, S., & Fatur Šikić, T. (2022). A way forward in reducing carbon emissions in environmentally friendly countries: The role of green growth and environmental taxes. Economic Research-Ekonomska Istraživanja, 35(1), 5879–5894. https://doi.org/10.1080/1331677X.2022.2039261

- European Commission (EC). (2014). A policy framework for climate and energy in the period from 2020 to 2030 COM/2014/015 Final, Brussels, Belgium: EU Publication Office.

- European Commission (EC). (2019). The European Green Deal COM/2019/640 Final, Brussels, Belgium: EU Publication Office.

- European Commission (EC). (2022). REPowerEU Plan COM/2022/230 Final, Brussels, Belgium: EU Publication Office.

- Eurostat. (2021). Eurostat releases for the first time estimates of quarterly EU greenhouse gas emissions. Retrieved April 14, 2021, from https://ec.europa.eu/eurostat/web/products-eurostat-news/-/DDN-20211129-1

- Eurostat. (2022b). Renewable energy statistics. Retrieved April 14, 2022, from https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Renewable_energy_statistics

- Eurostat. (2023). Environmental tax revenues statistics. Retreived February 17, 2022, from https://ec.europa.eu/eurostat/databrowser/view/ENV_AC_TAX__custom_4951251/default/table?lang=en

- Fang, G., Chen, G., Yang, K., Yin, W., & Tian, L. (2023). Can green tax policy promote China’s energy transformation?—A nonlinear analysis from production and consumption perspectives. Energy, 269, 126818. https://doi.org/10.1016/j.energy.2023.126818

- Gemmell, N., Kneller, R., & Sanz, I. (2016). Does the Composition of Government Expenditure Matter for Long-Run GDP Levels?. Oxford Bulletin of Economics and Statistics, 78(4), 522–547. https://doi.org/10.1111/obes.12121

- Ghazouani, A., Jebli, M. B. & Shahzad, U. (2021). Impacts of environmental taxes and technologies on greenhouse gas emissions: contextual evidence from leading emitter European countries. Environmental Science and Pollution Research, 28, 22758–22767. https://doi.org/10.1007/s11356-020-11911-9

- Gore, T., Urios, J., & Karamperi, M. (2022). Green and fair taxation in the EU, Institute for European Environmental Policy. Retrieved April 14, 2022, from https://ieep.eu/uploads/articles/attachments/ec138345-9b33-42e5-9bd8-74f550597af1/Green%20and%20fair%20taxation%20in%20the%20EU_IEEP%20(2022).pdf?v=63812080710

- Gurkov, I. (2015). Transition economy. In C. L. Cooper, M. Vodosek, D. N. Hartog, & J. M. McNett (Eds.), Wiley encyclopedia of management. John Wiley & Sons. https://doi.org/10.1002/9781118785317.weom060204

- He, P., Chen, L., Zou, X., Li, S., Shen, H., & Jian, J. (2019). Energy taxes, carbon dioxide emissions, energy consumption and economic consequences: A comparative study of nordic and G7 countries. Sustainability, 11(21), 6100. https://doi.org/10.3390/su11216100

- Hodžić, S., & Bratić, V. (2015). Comparative analysis of environmental taxes in EU and Croatia. Economic Thought and Practice, 2, 555–578.

- Huang, B. N., Hwang, M. J., & Yang, C. W. (2008). Causal relationship between energy consumption and GDP growth revisited: A dynamic panel data approach. Ecological Economics, 67(1), 41–54. https://doi.org/10.1016/j.ecolecon.2007.11.006

- Liobikienė, G., Butkus, M., & Matuzevičiūtė, K. (2019). The contribution of energy taxes to climate change policy in the European Union (EU). Resources, 8(2), 63. https://doi.org/10.3390/resources8020063

- Maxim, M., & Zander, K. (2019). Can a green tax reform entail employment double dividend in European and non-European Countries? A survey of the empirical evidence. International Journal of Energy Economics and Policy, 9(3), 218–228. https://doi.org/10.32479/ijeep.7578

- Miller, S. J., & Vela, M. A. (2013). Are environmentally related taxes effective? Inter-American Development Bank Working Series No. IDB-WP-467. Inter-American Development Bank.

- Morley, B. (2012). Empirical evidence on the effectiveness of environmental taxes. Applied Economics Letters, 19(18), 1817–1820. https://doi.org/10.1080/13504851.2011.650324

- Pedroni, P. (1999). Critical values for cointegration tests in heterogeneous panels with multiple regressors. Oxford Bulletin of Economics and Statistics, 61(S1), 653–670. https://doi.org/10.1111/1468-0084.61.s1.14

- Pesaran, M. H., & Smith, R. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79–113. https://doi.org/10.1016/0304-4076(94)01644-F

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. https://doi.org/10.2307/2670182

- Pesaran, M. H. (2004). General Diagnostic Tests for Cross Section Dependence in Panels. https://doi.org/10.17863/CAM.5113

- Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross‐section dependence. Journal of Applied Econometrics, 22(2), 265–312. https://doi.org/10.1002/jae.951

- Phillips, P. C., & Sul, D. (2003). Dynamic panel estimation and homogeneity testing under cross section dependence. The Econometrics Journal, 6(1), 217–259. https://doi.org/10.1111/1368-423X.00108

- Saidi, K., & Hammami, S. (2015). The impact of CO2 emissions and economic growth on energy consumption in 58 countries. Energy Reports, 1, 62–70. https://doi.org/10.1016/j.egyr.2015.01.003

- Silajdzic, S., & Mehic, E. (2018). Do environmental taxes pay off? The impact of energy and transport taxes on CO2 emissions in transition economies. South East European Journal of Economics and Business, 13(2), 126–143. https://doi.org/10.2478/jeb-2018-0016

- Shahzad, U., Radulescu, M., Rahim, S., Isik, C., Yousaf, Z., & Ionescu, S. A. (2021). Do environment-related policy instruments and technologies facilitate renewable energy generation? Exploring the contextual evidence from developed economies. Energies, 14(3), 690. https://doi.org/10.3390/en14030690

- Sharif, A., Kartal, M. T., Bekun, F. V., Pata, U. K., Chan, L. F., & Depren, S. K. (2023). Role of green technology, environmental taxes, and green energy towards sustainable environment: Insights from sovereign nordic countries by CS-ARDL approach. Gondwana Research, 117, 194–206. https://doi.org/10.1016/j.gr.2023.01.009

- Sulaiman, C., & Abdul-Rahim, A. S. (2020). The impact of wood fuel energy on economic growth in sub-Saharan Africa: Dynamic macro-panel approach. Sustainability, 12(8), 3280. https://doi.org/10.3390/su12083280

- United Nations (UN). (2015). Adoption of the Paris Agreement (Decision 1/CP.21. Article 2.1(a)). United Nations.

- United Nations (UN). (2016). Transforming our world: The 2030 agenda for sustainable development. Retrieved April 14, 2016, from https://stg-wedocs.unep.org/bitstream/handle/20.500.11822/11125/unepswiosm1inf7sdg.pdf?sequence=1

- Westerlund, J. (2005). A panel CUSUM test of the null of cointegration. Oxford Bulletin of Economics and Statistics, 67(2), 231–262. https://doi.org/10.1111/j.1468-0084.2004.00118.x

- Wolde-Rufael, Y., & Mulat-Weldemeskel, E. (2022). The moderating role of environmental tax and renewable energy in CO2 emissions in Latin America and Caribbean countries: Evidence from method of moments quantile regression. Environmental Challenges, 6, 100412. https://doi.org/10.1016/j.envc.2021.100412

- Zaharia, A., Diaconeasa, M. C., Brad, L., Lădaru, G. R., & Ioanăș, C. (2019). Factors influencing energy consumption in the context of sustainable development. Sustainability, 11(15), 4147. https://doi.org/10.3390/su11154147

- Zugravu, N., Millock, K., & Duchene, G. (2008). The factors behind CO2 emission reduction in transition economies. Retrieved March 30, 2008, from https://www.gate.cnrs.fr/IMG/pdf/Millock.pdf