ABSTRACT

Behavioral economics has long defined itself in opposition to neoclassical economics, but recent developments suggest a synthesis may be on the horizon. In particular, several economists have argued that behavioral factors can be incorporated into standard theory, and that the days of behavioral economics are therefore numbered. This paper explores the proposed synthesis and argues that it is distinctly behavioral in nature – not neoclassical. Far from indicating that behavioral economics as a stand-alone research program is over, the proposed synthesis represents the consummate conversion of neoclassical economists into behavioral ones.

GRAPHICAL ABSTRACT

1. Introduction

Behavioral economics has long defined itself, at least in part, in opposition to standard (neoclassical) economics. This was true for the ‘old’ behavioral economics of Herbert A. Simon, whose work on procedural rationality (e.g. Citation1976) was premised on the contrast with standard economists' substantive rationality. And it is true for the ‘new’ behavioral economics of Amos Tversky and Daniel Kahneman, whose work on heuristics and biases (Citation1974) and prospect theory (Citation1979) was developed against the background of standard rationality. The contrast with standard economics lives on in definitions of behavioral economics, which emphasize the way in which it is more psychologically ‘realistic’ or ‘plausible’ than standard economics (Angner & Loewenstein, Citation2012; Camerer & Loewenstein, Citation2004) and/or the way in which it relaxes standard assumptions (Mullainathan & Thaler, Citation2001). Finally, arguments for and against behavioral economics have long taken the form of arguments for and against its superiority over standard economics.

Recently, however, something appears to have shifted: neoclassical and behavioral economists nowadays often go out of their way to downplay the differences. I first noticed the shift when my publisher requested referee reports ahead of commissioning a second edition of my textbook (Angner, Citation2016a). One of the recurring comments in these reports was that I made too much of the differences between behavioral and neoclassical economics, and that these differences were ultimately unimportant. Instead of talking about differences, several referees argued, I should emphasize that each approach provides the economist with tools that may come in handy at times, and between which practicing economists can pick and choose as required. But the most interesting thing about these reports, to me, was that I couldn't tell whether they came from the behavioral or the neoclassical camp. It appeared to me as though both kinds of economist were suddenly equally eager to emphasize the continuities.

The shift struck me as momentous. When I was a graduate student in the early aughts, behavioral and neoclassical economists did not see eye to eye. Behavioral economists at the time weren't even taken seriously as economists: the behavioral courses I took as a graduate student were offered in a department of social and decision sciences, not in a traditional department of economics. And I recall a prominent behavioralist saying he wouldn't even talk to neoclassical economists until they developed ‘the emotional maturity to take data seriously’. It is easy to forget that until fairly recently even experimental economics was still regarded with skepticism by elements of the profession. As late as 1999, The Economic Journal published a symposium in its ‘Controversy’ series where contributors asked why we should experiment at all (Binmore, Citation1999) and whether experimental economics was ‘hard science or wasteful tinkering’ (Starmer, Citation1999).

The new conciliatory tone is increasingly explicit in academic literature. Here, I will focus on Raj Chetty's prestigious 2015 Richard T. Ely Lecture, ‘Behavioral Economics and Public Policy: A Pragmatic Perspective’, which I take to be representative of the new mainstream attitude to behavioral themes. Chetty begins his lecture by pointing out that debates about behavioral versus neoclassical approaches often concern more or less philosophical foundations, including the assumption that people are rational in market settings. But he evidently has little interest in or patience for that sort of discussion. Chetty just notes, meekly, that ‘this debate has proved to be contentious, with compelling arguments in favor of each viewpoint in different settings’ (Chetty, Citation2015, p. 1). He continues:

In this paper, I approach the debate on behavioral economics from a more pragmatic, policy-oriented perspective. Instead of posing the central research question as "Are the assumptions of the neoclassical economic model valid?,” the pragmatic approach starts from a policy question … and incorporates behavioral factors to the extent that they improve empirical predictions and policy decisions. (Chetty, Citation2015, p. 1)Footnote1

Chetty's case feeds into an increasingly common narrative according to which behavioral economics is ‘doomed’ (cf. Levine, Citation2012). Here's the story in broad outline. Neoclassical models succeed in explaining and predicting a wide range of phenomena observed in the field and in the lab. One class of phenomena explored by behavioral economists are in fact consistent with the standard framework, and can be immediately accounted for. Social preferences fall into this category, since they can be accommodated simply by adding another argument in a standard utility function (Angner, Citation2016a, sec. 11.2). A second class of phenomena cannot be replicated, and should be treated as experimental artifacts of no practical or theoretical interest. Behavioral priming may fall into this category (Doyen, Klein, Pichon, & Cleeremans, Citation2012). Finally, there's a third class of phenomena that are inconsistent with the standard framework and which cannot be dismissed as experimental artifacts. But such behavioral phenomena can be – and in many cases already have been – successfully incorporated into standard economics by adding behavioral factors as necessary. Therefore, the argument concludes, neoclassical economics has assimilated or will assimilate all the important insights and behavioral economics as a stand-alone research program is over.

My goal in this paper is to examine the attempted reconciliation of behavioral and neoclassical economics. For now, I will call it the new synthesis, by analogy to the ‘neoclassical synthesis’ that took place in macroeconomics in the 1950s (Samuelson, Citation1955, p. 212) and the ‘neo-Darwinian synthesis’ that took place in biology during the first half of the century (Huxley, Citation1942). My purpose is not to criticize Chetty's decision to skirt foundational issues in order to address policy questions. In actual scientific practice, explicit attention to philosophical foundations can be a distraction. And pressing policy questions of the kind that interest him cannot be ignored until such a time that all controversy regarding assumptions have been dispelled. My purpose, rather, is to explore the nature of the new synthesis and what it means for contemporary economics.

My thesis is that the new synthesis is distinctly behavioral in nature – not neoclassical. Chetty's pragmatic approach does not bypass questions of the philosophical foundations of behavioral economics so much as it simply assumes an answer to them. And the answers are the same as those of the behavioral economists. The new synthesis could therefore easily be dubbed the behavioral synthesis. It does not represent the elimination of behavioral economics as a stand-alone research program, but rather the consummated conversion of neoclassical economists into behavioral ones. To the extent that we endorse the synthesis, we're all behavioral economists now.

2. A mystery

One thing to notice is that if Chetty and his fellow travelers are right, it is a mystery how neoclassical and behavioral economists could come to disagree so vigorously for so long. As indicated in Section 1, behavioral and neoclassical economists were locked into occasionally acrimonious disputes for decades, if not generations. Disputes concerned not just theory, but scientific method, evidence, data, and policy implications (Angner & Loewenstein, Citation2012). Assuming it was true all along that there is no contradiction or even tension between neoclassical and behavioral economics, it is hard to avoid the conclusion that the entire debate was just a mistake rooted in an inadequate understanding of the nature of neoclassical and/or behavioral economics. But it would be entirely mysterious how one or more generations of economists – including the first generation(s) of behavioral economists – could be so wrong about their own discipline.

By my lights, the probability of such self-misunderstanding is low, and consequently, so is the likelihood that Chetty is right. But to draw more confident conclusions, we need to take a closer look at the details of his proposal.

3. The ‘pragmatic’ approach

What is Chetty's pragmatic approach – and what is supposed to be new about it? Chetty demonstrates his approach in the context of research on three major life decisions: how much you save, how much you work, and where you choose to live. Chetty notes that all three raise pressing policy questions, and adds that his aim is ‘to illustrate how insights from behavioral economics can yield better answers to these long-standing policy questions’ (Chetty, Citation2015, p. 2).

Behavioral economics produces better answers in several ways, Chetty (Citation2015, pp. 1–2) says. First, behavioral economics generates a better understanding of the range of policy tools, or ‘levers’, available to the policy-maker. Whenever behavioral economics introduces ‘behavioral’ factors – which will often be intervening variables located ‘in the head’ of the decision maker, such as framing and mental accounting – it gives the policy-maker one more variable potentially to intervene on. Second, Chetty argues, behavioral economics yields better predictions of the effects of various policy decisions on people's behavior. Taking explicit account of things like framing, defaults, and inertia improves our predictions about how people respond to various policy changes. Third, behavioral economics generates better predictions of the welfare effect of policy changes. Better predictions improve our ability to identify the optimal policy, which in turn should help us promote the general welfare.

What in Chetty's view makes this pragmatic approach different, and what makes it novel, is the fact that it does not prejudge whether a neoclassical or behavioral model will be more suitable in any given case. In some applications, he points out, behavioral factors need not play a major role, and a simpler neoclassical model may be sufficiently accurate to explain and predict economic phenomena and to inform policy. In others, behavioral factors play a major role, and a behavioral model is required to predict, explain, and inform policy. The decision to use a behavioral model – or not – should be treated like any other modeling decision, such as whether to assume a time-separable utility function: in some contexts, the simpler utility function does just fine, but in others, it introduces unacceptable distortions. Behavioral economics, in this view, just becomes one more arrow in the economist's quiver:

In this sense, behavioral economics is better viewed as part of all economists' toolkit (like other tools in applied theory) rather than as a separate subfield. Dividing our field into ‘behavioral’ and ‘neoclassical’ economics is akin to distinguishing ‘time separable’ economists from others. (Chetty, Citation2015, p. 29)

The virtue of the pragmatic approach, to Chetty, is that it bypasses abstract ‘philosophical’ arguments about the superiority of neoclassical vs. behavioral economics. As he puts it: ‘This pragmatic, application-specific approach to behavioral economics may ultimately be more productive than attempting to resolve whether the assumptions of neoclassical or behavioral models are correct at a general level’ (Chetty, Citation2015, p. 3). Chetty clearly does not think arguments about the philosophical foundations of behavioral vs. neoclassical economics, on the margin, are a good use of economists' time. One benefit of the pragmatic approach, then, would be to justify reallocating that scarce resource to more productive uses.

Chetty is right that major life decisions about how much to save, how much to work, and where to live are good candidates for a behavioral treatment. First, major life decisions are relatively rare and their consequences delayed, which means that you have few opportunities to learn from personal experience over the course of a lifetime. And even standard economists have agreed that neoclassical models are unlikely to apply except when decision problems are relatively simple, incentives are adequate, and trial-and-error learning is sufficient (Binmore, Citation1999, pp. F16–F17). Second, in major life decisions stakes are high, which means that successful policy interventions that help people make better decisions can potentially be hugely beneficial. Even a small increase in monthly savings early in one's career can make a big difference in retirement.

There is, however, nothing radically new about Chetty's pragmatic approach. The approach that he describes is what behavioral economists have advocated all along.Footnote2

The first thing to note is that behavioral economists have never opposed the use of standard theory when conditions call for it. In fact, a number of behavioralists have gone out of their way to praise its explanatory and predictive powers, not to mention its usefulness in policy applications. Here is Matthew Rabin:

[Behavioral economics] is not only built on the premise that economic methods are great, but also that most mainstream economic assumptions are great. It does not abandon the correct insights of neoclassical economics, but supplements these insights with the insights to be had from realistic new assumptions. (Rabin, Citation2002, pp. 658–659)

At the core of behavioral economics is the conviction that increasing the realism of the psychological underpinnings of economic analysis will improve the field of economics on its own terms – generating theoretical insights, making better predictions of field phenomena, and suggesting better policy. This conviction does not imply a wholesale rejection of the neoclassical approach to economics based on utility maximization, equilibrium, and efficiency. The neoclassical approach is useful because it provides economists with a theoretical framework that can be applied to almost any form of economic (and even noneconomic) behavior, and it makes refutable predictions. (Camerer & Loewenstein, Citation2004, p. 3)

When it comes to policy too, behavioral economists agree that traditional economics sometimes offers the best prescriptions. Loewenstein and Nick Chater (Citation2017) argue that conventional economic policy solutions may be the best choice even when the underlying problems are behavioral in origin. Thus, a sin tax may be the best way to manage the consumption of addictive substances, even if people use them because the future is discounted hyperbolically. The unprompted praise for neoclassical theory and its policy applications may strike the casual observer as puzzling. But as we will see in the next section, practicing behavioral economists have long made good use of neoclassical models when they fit the application at hand.

What, then, makes the behavioral approach different from the traditional neoclassical one? By definition, behavioral economics tries to increase the explanatory and predictive power of economic theory on the margin by providing it with more psychologically plausible foundations, where ‘psychologically plausible’ means consistent with the best available psychological theory (Angner & Loewenstein, Citation2012, p. 642). Getting rid of neoclassical theories, methods, and assumptions when they work would amount to throwing the baby out with the bathwater, and there is nothing in behavioral economics that would recommend doing so. What behavioral economists recommend instead is incorporating ideas drawn above all from contemporary psychology when necessary and appropriate in order to explain, predict, and inform policy. But this is, of course, the exact procedure that Chetty advocates. Chetty's pragmatic approach to behavioral economics just is behavioral economics.

As we saw above, Chetty sees abstract, ‘philosophical’, debates about the superiority of behavioral vs. neoclassical approaches as a distraction from economists' real work. He advises behavioral economists to stop searching for anomalies that challenge conventional economic theory: ‘At this point, it may be more productive to instead ask how behavioral models can contribute to answering core economic questions’ (Chetty, Citation2015, p. 29). But the advice is misplaced, since this is what behavioral economists have done – or tried to do – all along. Consider this passage of Rabin's, suggesting he gets little pleasure from the ‘philosophical’ debates:

As a rule, it is bad to spend time on ‘methodological’ and broad-stroke issues rather than the nitty gritty of the phenomena being studied. The goal of this research program is that it become ‘normal science’, and, as such, the nitty gritty is the point. Papers and talks should … address the substance of this new research, not its methodological legitimacy … What most of us doing psychological economics spend most of our time on – and wish we could spend all of our time on – is not debates over methodology, but doing normal science. Because this approach is clearly gaining acceptance, essays like this should soon become anachronistic. (Rabin, Citation2002, p. 659)

It is true that behavioral economists have long argued against the thesis that neoclassical theory is always and everywhere the most suitable model for purposes of explaining, predicting, and informing policy. In the process, they have spent considerable time and effort gathering data to support their claim. The thesis is the kind of ‘philosophical’ claim Chetty would rather not discuss. But notice that behavioral economists don't have the luxury of not taking a stand on the thesis. If it were true, there would be no need to incorporate behavioral factors, and a behavioral approach – pragmatic or not – would never be called for. Now, Chetty's situation is identical: he does not have the luxury of not taking a stand on this thesis. If it were true, his pragmatic approach would be dead in the water. Thus, Chetty's approach does not bypass questions of the philosophical foundations of behavioral economics; it simply assumes answers to these questions. And the answers are the same as those of the behavioral economists, who have long argued that it is legitimate and sometimes necessary to incorporate behavioral factors in economic models.

One could object that Chetty is not representative of mainstream economists' attitude to behavioral economics. I admit that I do not have the hard data that would establish the hypothesis beyond reasonable doubt. But we should expect Chetty's lecture to be at the same time a leading and a trailing indicator of the profession writ large: a leading indicator because the Ely lecture (which is held annually at the American Economic Association meetings) is highly influential, and a trailing indicator because his selection reflects the values and interests of a broader community of scholars. Moreover, behavioral and neoclassical economists alike have incentives to downplay their differences. Behavioral economists may want access to resources, positions, and awards controlled wholly or in part by neoclassical economists; neoclassical economists may wish to be able to help themselves to ideas drawn from behavioral economics when it is convenient to do so. Both camps may have grown tired of the conflict, which started before many practicing economists today were born.

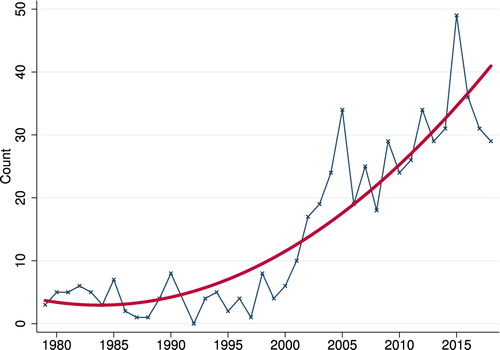

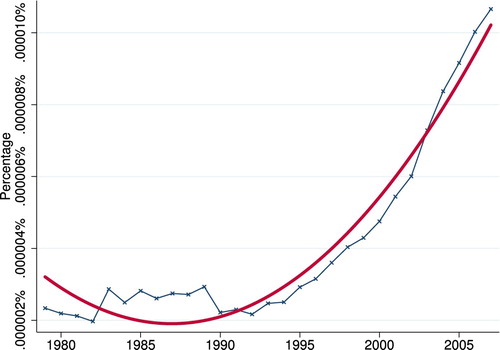

Bibliometric data support the hypothesis that interest in behavioral economics has risen dramatically over the last quarter of a century, even at mainstream journals and conferences. Geiger (Citation2017) shows that the number of occurrences of key terms such as ‘behavioral economics’ and ‘bounded rationality’ in academic literature has increased sharply, especially after the year 2000 and in top journals. Other data tell a similar story. shows the number of occurrences of ‘behavioral’ in programs of the Allied Social Sciences Association (ASSA) meetings from 1979, the year of publication of Kahneman and Tversky's prospect theory paper and coincidentally Chetty's birth year, to 2018, the year of writing.Footnote3 The absolute numbers on the y-axis should not be ascribed much importance: since programs list only titles of sessions and individual papers, many references to behavioral economics in abstracts and bodies of papers were not counted. The sharp increase over time seems important, however, especially following the late 1990s. (It is true that programs have gotten longer over the same time period, but not at the same clip.) The increase suggests mainstream economists – operationalized as economists invited to present at ASSA meetings – increasingly incorporate behavioral ideas into their work. shows the percentage of books published in the United States in English that mention the term ‘behavioral economics’ between 1979 and 2007, the latest date available.Footnote4 The graph reveals that mentions have been increasing at an accelerating rate since the early 1990s. Again, not too much should be read into the numbers on the y-axis, but the increase appears important. (Since the percentage of books that mentioned ‘economics’ over the same period was slightly declining, the increase cannot be explained by a general rise in interest in all kinds of economics.)

Figure 1. Number of occurrences of ‘behavioral’ in the programs of the Allied Social Sciences Association (ASSA) meetings, 1979–2018, along with a fitted quadratic curve. Data from the American Economic Association.

Figure 2. Percentage of books published in the United States in English that contain the term ‘behavioral economics’, 1979–2007, along with a fitted quadratic curve. Data from Google Books.

4. The asymmetry of behavioral and neoclassical economics

Chetty repeatedly emphasizes the continuities between neoclassical and behavioral economics. Among other things, he writes that ‘from a pragmatic perspective, behavioral economics represents a natural progression of (rather than a challenge to) neoclassical economic methods’ (Chetty, Citation2015, p. 1). This ‘natural progression’ is underscored by the metaphor of behavioral economics as just another tool in the economist's toolkit – as opposed to a whole new toolkit replacing the old one. The same rhetoric appears in the work of some behavioral economists. In the paper cited above, Rabin writes that behavioral economics ‘is not an alternative to the economic research program into which we were all socialized in graduate school, but the natural continuation of this research program’ (Rabin, Citation2002, p. 659). Such rhetoric might seem to support the contention that there is nothing distinctly behavioral about the new synthesis, and that it is better described as a simple extension of neoclassical theory. This is, however, a mistake: it overlooks an important asymmetry inherent in the relationship between neoclassical and behavioral economics.

Throughout, I use ‘neoclassical economics’ and ‘behavioral economics’ to refer to the respective research programs. I take a research program to consist not just of theories and models, but also of a nebulous collection of correspondence rules, which tell us how theories and models relate to observations made in the field or laboratory; methodological strictures, which tell us how to go about our inquiries and how not to; cognitive and non-cognitive values, which tell us what's important and what's not; and so on. By contrast, I use ‘neoclassical (economic) theory’ and ‘behavioral (economic) theory’ to refer more specifically to the formal (and perhaps informal) theories and models traditionally employed by economists of the two kinds.

First, neoclassical economics understood as a research program strictly speaking does not permit the inclusion of behavioral factors of any kind. What we now call neoclassical economics is the so-called ‘postwar neoclassical synthesis’, which emerged during the first half of the twentieth century and became dominant around the middle of the century.Footnote5 Postwar neoclassical economics was a reaction against a set of approaches based on the principles of hedonic psychology: the theory that all human behavior is driven by pleasure and pain. Postwar economists were disappointed with the degree of scientific progress that had been attained using a foundation of hedonic psychology. Inspired by a series of parallel developments in other disciplines – such as behaviorism in psychology, logical positivism in philosophy, and operationalism in physics – they had also come to believe that references to unobservable entities ‘in the head’ of the economic agent were scientifically illegitimate. Various developments in positive and normative economics had reassured them that references to unobservable entities were not only illegitimate but also dispensable. Thus, the concept of preference came to be the primitive notion of economic theory, and references to psychological theory came to be avoided.

The point is that neoclassical economics – as it has been practiced for more than half a century – is based on the explicit and vigorous repudiation of any references to unobservable entities, including what Chetty calls ‘behavioral factors’. Economists working within this tradition, therefore, do not have the luxury of deciding on a case-by-case basis whether they want to take behavioral factors into account or not. For this reason, the decision to incorporate behavioral factors is unlike the decision to use a time-separable utility function, contrary to what Chetty thinks. Nothing in the neoclassical tradition says that the utility function has to have this or that mathematical form. It is, therefore, both possible and appropriate for neoclassical economists to choose which form they wish to use based on more or less pragmatic considerations concerning what will work under the circumstances. And there is no need to distinguish ‘time-separable’ from ‘non-time-separable’ neoclassical economists.

At this point, it may be objected that I have misrepresented neoclassical economics. So, for example, it may be proposed that neoclassical economics just is what self-described neoclassical economists do. Given that self-described neoclassical economists increasingly incorporate behavioral factors into their models, then, it would follow that doing so must be consistent with the neoclassical approach. And yet, defining neoclassical economics in this way would make it impossible for contemporary neoclassical economists to deviate from orthodoxy, in the sense that literally anything they do would be consistent with it, which trivializes the question. It is better to capture the nature of neoclassical economics by situating it historically, in the manner of Mandler (Citation1999) and Angner and Loewenstein (Citation2012), so that the conception is logically independent of what contemporary economists happen to do.

While neoclassical economists cannot consistently incorporate behavioral factors into their models, there is nothing in behavioral economics that makes the use of neoclassical theory illegitimate. To the contrary, as I pointed out in Section 3, behavioral economists have consistently advocated using neoclassical theory for all sorts of purposes. By and large, they treat neoclassical models and theories as heuristic devices or analytical tools, which can be helpful for a range of scientific purposes – in spite of the fact that they are often literally false as a general description of behavior.Footnote6

The manner in which behavioral economists use neoclassical theory is helpfully elucidated by a passage in which Camerer and Loewenstein (Citation2004, p. 7) describe a ‘recipe’ that behavioral economists tend to follow in their work. The recipe recommends (i) starting off by identifying some assumption or model that is widely used by neoclassical economists, (ii) exploring conditions under which its implications are contradicted by data, and (iii) using deviations from predictions – in combination with insights drawn from psychology – to develop more general, alternative models of choice behavior. Once we dig deeper into the manner in which behavioral economists work, it becomes clear that they use neoclassical theory in numerous ways:

Orthodox theory is used to describe and classify behavior. Thus, behavioral patterns are labeled ‘rational’ insofar as they conform to the theory and ‘irrational’ insofar as they do not.

Orthodox theory is used to establish the conditions under which people's observed behavior deviates from the predictions of orthodox theory. Once behavior can be categorized as rational and irrational, it is possible to study scientifically under what conditions one observes the one category and under what conditions one observes the other.

Orthodox theory can also be used to assess the degree to which observed behavior deviates from rational behavior. By using the predictions of standard theory as a benchmark, it is possible to estimate numerically the magnitude of any deviation.

Orthodox economic theory is frequently used as a basis for theoretical developments in behavioral economics. In particular, orthodox theory is used to develop causal hypotheses, e.g. about what causal factors were responsible for generating the deviations.

Standard theory serves as a source of null hypotheses. Such hypotheses are required for classical statistical testing in both lab and field studies.

The theory helps define the very language that behavioral economists use to describe their subject matter. Terms such as ‘anomalies’ and ‘effects’ make no sense except in the presence of some theoretical predictions relative to which anomalies and effects constitute deviations.

Finally, orthodox theory remains a normative ideal and standard of evaluation in many contexts. The fact that behavioral economists reject the theory as a descriptive model does not mean that they must reject it as a normative one, and by and large (though not always) behavioral economists have accepted the conception of rationality associated with neoclassical economics.

In sum, there is an important asymmetry between neoclassical and behavioral economics. Neoclassical economists cannot consistently incorporate behavioral factors into their models, but there is nothing in behavioral economics that makes the use of neoclassical theory illegitimate. Any synthesis involving neoclassical theory and behavioral factors, therefore, cannot be neoclassical. It must be behavioral.

5. Discussion

In this paper, I have argued that Chetty's so-called pragmatic approach to behavioral economics just is behavioral economics and that what I called the new synthesis is distinctly behavioral in nature – not neoclassical. First, I pointed out that if Chetty and his fellow travelers are right, it is a mystery how neoclassical and behavioral economists could come to disagree so vigorously for so long. Second, I argued that adding behavioral factors to neoclassical theory as required to enhance its explanatory and predictive power, which is what Chetty recommends, is the very textbook definition of behavioral economics. Third, I maintained that there is an important asymmetry between neoclassical and behavioral economics, such that neoclassical economists strictly speaking cannot consistently incorporate behavioral factors, but behavioral economists can and do rely on neoclassical theory in various ways. If this is correct, it vindicates Thaler's (Citation2016, p. 1597) prediction that ‘the term “behavioral economics” will eventually disappear from our lexicon. All economics will be as behavioral as the topic requires’.

One caveat: I have not argued – and do not mean to imply – that pressure from behavioral economics was the only factor behind the emergence of the behavioral synthesis. Another factor may have been the demise of behaviorism in psychology, logical positivism in philosophy, and operationalism in physics, which may have influenced the way contemporary economists think about methodology more directly. Yet another factor may have been the development of the economics of information, epistemic game theory, etc., which impose much more structure on an agent's beliefs than can reasonably be expected to be reduced to mere behavior (cf. Hausman, Citation2012, ch. 5).Footnote7

It may be objected that the controversy surrounding libertarian paternalism and the nudge agenda (due to Thaler & Sunstein, Citation2003, Citation2008) undermines my case, by showing that neoclassical and behavioral economists are radically different after all. For example, one could argue that behavioral economists are paternalists whereas neoclassical economists are not. Upon closer inspection, however, the normative foundations of neoclassical and behavioral welfare economics are surprisingly similar. Like their neoclassical counterparts, behavioral economists take their central normative concern to be that of welfare or well-being; think of individual welfare in terms of preference satisfaction; and treat social welfare as total or average individual welfare (Angner, Citation2016b, p. 495). Moreover, arguments to the effect that behavioral economists are paternalists whereas neoclassical economists are not tend to equivocate on the meaning of ‘paternalism’ (Angner, Citation2016a, pp. 263–264). If by ‘paternalism’ we just mean a disposition or desire to make people better off, neoclassical economists are paternalists too; if we mean a disposition or desire to promote welfare by interfering with people's autonomy and freedom of choice, libertarian paternalists are not strictly speaking paternalists. It is also interesting to note that libertarian paternalism and the nudge agenda have supporters across the ideological spectrum. While the original authors of Nudge (Thaler & Sunstein, Citation2008) come across as left of center, Bryan Caplan (Citation2013) defends nudging from a libertarian perspective and Tyler Cowen (Citation2017) from a conservative one.

A corollary of my thesis is that it is misleading to describe behavioral economics as ‘controversial’ (cf. Grüne-Yanoff, Citation2017, p. 61). The existence of the behavioral synthesis shows that there is, in fact, wide agreement on the foundational principles of behavioral economics among contemporary economists – even among those who for whatever reason eschew the label. The disputes that remain are of two kinds. First, there are internal disagreements of a form we find within any healthy normal science, about proper methodology, econometrics, experimental design, modeling decisions, etc. This kind of disagreement over problem-solving can lead to heated arguments but does not make behavioral economics any more controversial than any other scientific discipline. Second, there are external critiques, originating with psychologists, philosophers, sociologists, and other non-economists, of a kind that economics seems particularly prone to attract. As Ross (Citation2012b, p. 241) has pointed out, economics has always been accompanied by a tradition of ‘anti-economics’ that is quite unique among the sciences – with the possible exception of evolutionary theory. Yet, such external critiques do not make behavioral economics any more controversial than any other subdiscipline of economics.

My account undercuts a common critique of behavioral economics, according to which it is premised on a major misunderstanding of the nature and/or subject matter of economics (Herfeld, Citation2018, p. 187; Ross, Citation2012a, p. 708). The argument is not necessarily that behavioral economics is not good behavioral science, but rather that behavioral economics is not economics. And yet, the fact that leading mainstream economists such as Chetty find a variety of behavioral models useful for their own, mainstream economic aims and purposes makes it unlikely that those models would be based on a radical misunderstanding of what economics is all about. To my mind, we can confidently reject the possibility that a wide variety of fundamentally misconceived behavioral models would nonetheless by complete coincidence turn out to be highly useful for mainstream economic aims and purposes.

The analysis contradicts a narrative according to which mainstream economics is churchlike, in the sense that neoclassical orthodoxy is sacrosanct and apostasy punished harshly. This narrative is common in public discourse about economics – although less so, unsurprisingly, among practicing economists. Writing in The Guardian under the heading ‘How Economics Became a Religion’, for example, Rapley (Citation2017) claims that economics ‘has always operated more like a church’ whose ‘high priests … uphold orthodoxy in the face of heresy’. And yet, what I have called the behavioral synthesis shows that the foundations of contemporary economics have shifted sharply away from neoclassical orthodoxy. And Chetty, being one of the most celebrated economists of his generation, has not exactly been crucified for abandoning it.

The analysis also helps explain how the economics-as-church narrative got so much traction in spite of being false. The shift that I have discussed in the above may not be immediately obvious to an outsider – or even an inattentive insider. You have to know quite a bit about both neoclassical and behavioral economics and about their history and methodology to see clearly how thoroughly Chetty departs from the orthodoxy. This fact helps explain how even radical changes within the mainstream can go unnoticed and how the economic mainstream can develop a reputation as less dynamic than it really is. Either way, it is clear that mainstream economics is more open to change and responsive to evidence than many critics allow.Footnote8

Finally, the analysis contradicts the narrative according to which behavioral economics is doomed. Far from showing that behavioral economics as a stand-alone research program is over, Chetty represents the consummate conversion of neoclassical economists into behavioral ones. To the extent that practicing economists endorse the new behavioral synthesis, we are all doing behavioral economics – whether we are aware of it or not. In the mid-1960s, Chicago economist Milton Friedman coined the phrase ‘We're all Keynesians now’. Half a century later, we might say instead: ‘We're all behavioral economists now’.Footnote9

Notes on contributor

Erik Angner is Professor of Practical Philosophy at Stockholm University and Researcher at the Institute for Futures Studies in Stockholm. As a result of serious mission creep, he holds two PhDs – one in Economics and one in History and Philosophy of Science – both from the University of Pittsburgh. He is the author of two books, Hayek and natural law and A course in behavioral economics (now in its second edition), as well as multiple journal articles and book chapters on behavioral and experimental economics; the economics of happiness; and the history, philosophy, and methodology of contemporary economics.

Acknowledgments

This article is based on a keynote lecture at the ‘Economics and/or Psychology’ conference in Helsinki in May of 2017 and a presentation at the ‘Prospect Theory as a Model of Risky Choice’ conference in Cork in October of 2017. I am grateful to Magdalena Małecka and Michiru Nagatsu and to Glenn Harrison and Don Ross for their invitations, and to participants in both conferences for helpful feedback. I thank Åsa Burman, Niels Geiger, Niklas Olsson Yaouzis, Robert Östling, Orri Stefánsson, and two anonymous referees for their insightful comments on earlier drafts. The usual caveats apply.

Disclosure statement

No potential conflict of interest was reported by the author.

ORCID

Erik Angner http://orcid.org/0000-0002-8256-8446

Additional information

Funding

Notes

1 Although this passage only mentions prediction and policy decisions, the rest of the paper makes it clear that Chetty is concerned with explanation as well.

2 I will limit my attention to the ‘new’ behavioral economists, meaning (roughly) Tversky and Kahneman and those who were significantly inspired by them (cf. Sent, Citation2004).

3 Data were gathered from the website of the American Economic Association at https://www.aeaweb.org/conference/past-annual-meetings, which offers pdf versions of old programs. The program from 1991 was missing. Counts were obtained using the ‘Advanced Search’ function of Adobe Acrobat Pro DC 2015.006 for Mac. Data were analyzed with Stata 12.1 for Mac.

4 Data were collected from Google Books Ngram Viewer at https://books.google.com/ngrams using a search for ‘behavioral economics’ from 1979 onwards, in the English corpus and with a smoothing of 3. Data were analyzed with Stata 12.1 for Mac.

5 See Mandler (Citation1999, ch. 4) and Angner and Loewenstein (Citation2012, sec. 2) for a more detailed history.

6 What follows is based on Angner (Citation2014).

7 I thank Robert Östling for suggesting this point.

8 Mainstream economics could still be insufficiently open to change and responsive to evidence. I am not taking a stand on this issue here.

9 This claim is not supposed to be literally true, just like it wasn't literally true in the 1960s that everyone was a Keynesian.

References

- Angner, E. (2014). “To navigate safely in the vast sea of empirical facts”: Ontology and methodology in behavioral economics. Synthese, 192(11), 3557–3575. doi:10.1007/s11229-014-0552-9

- Angner, E. (2016a). A course in behavioral economics. 2nd ed. London: Palgrave Macmillan.

- Angner, E. (2016b). Well-being and economics. In G. Fletcher (Ed.), The Routledge handbook of philosophy of well-being (pp. 492–503). London: Routledge.

- Angner, E., & Loewenstein, G. (2012). Behavioral economics. In U. Mäki (Ed.), Philosophy of economics (pp. 641–690). Amsterdam: North-Holland. doi:10.1016/B978-0-444-51676-3.50022-1

- Binmore, K. (1999). Why experiment in economics? The Economic Journal, 109(453), F16–F24. doi:10.1111/1468-0297.00399

- Camerer, C. F., & Loewenstein, G. (2004). Behavioral economics: Past, present, future. In C. F. Camerer, G. Loewenstein, & M. Rabin (Eds.), Advances in behavioral economics (pp. 3–51). New York, NY and Princeton, NJ: Russell Sage Foundation and Princeton University Press.

- Caplan, B. (2013, July 31). Nudge, policy, and the endowment effect. Library of Economics and Liberty. Retrieved from http://econlog.econlib.org/archives/2013/07/nudge_policy_an.html

- Chetty, R. (2015). Behavioral economics and public policy: A pragmatic perspective. American Economic Review, 105(5), 1–33. doi:10.1257/aer.p20151108

- Cowen, T. (2017, October 9). Why conservatives should celebrate Thaler's Nobel. Bloomberg View. Retrieved from https://www.bloomberg.com/view/articles/2017-10-09/why-conservatives-shouldcelebrate-thaler-s-nobel

- Doyen, S., Klein, O., Pichon, C.-L., & Cleeremans, A. (2012). Behavioral priming: It's all in the mind, but whose mind? PLoS ONE, 7(1), e29081. doi:10.1371/journal.pone.0029081

- Geiger, N. (2017). The rise of behavioral economics: A quantitative assessment. Social Science History, 41(3), 555–583. doi:10.1017/ssh.2017.17

- Grüne-Yanoff, T. (2017). Reflections on the 2017 Nobel Memorial Prize awarded to Richard Thaler. Erasmus Journal for Philosophy and Economics, 10(2), 61–75. doi:10.23941/ejpe.v10i2.307

- Haack, S. (2003). Pragmatism. In N. Bunnin & E. P. Tsui-James (Eds.), The Blackwell companion to philosophy (2nd ed., pp. 774–789). Oxford: Blackwell. doi:10.1002/9780470996362.ch38

- Hausman, D. M. (2012). Preference, value, choice, and welfare. Cambridge: Cambridge University Press.

- Herfeld, C. (2018). Explaining patterns, not details: Reevaluating rational choice models in light of their explananda. Journal of Economic Methodology, 25(2), 179–209. doi:10.1080/1350178X.2018.1427882

- Huxley, J. (1942). Evolution: The modern synthesis. London: G. Allen & Unwin.

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–291. doi:10.2307/1914185

- Levine, D. K. (2012). Is behavioral economics doomed? The ordinary versus the extraordinary. Cambridge: Open Book. Retrieved from https://www.jstor.org/stable/j.ctt5vjtfs

- Loewenstein, G., & Chater, N. (2017). Putting nudges in perspective. Behavioural Public Policy, 1(1), 26–53. doi:10.1017/bpp.2016.7

- Mandler, M. (1999). Dilemmas in economic theory: Persisting foundational problems of microeconomics. New York, NY: Oxford University Press.

- Mullainathan, S., & Thaler, R. H. (2001). Behavioral economics. In N. J. Smelser & P. B. Baltes (Eds.), International encyclopedia of the social & behavioral sciences (Vol. 2, pp. 1094–1100). Oxford: Pergamon. doi:10.1016/B0-08-043076-7/02247-6

- Rabin, M. (2002). A perspective on psychology and economics. European Economic Review, 46(4–5), 657–685. doi:10.1016/S0014-2921(01)00207-0

- Rapley, J. (2017, July 11). How economics became a religion. The Guardian. Retrieved from https://www.theguardian.com/news/2017/jul/11/how-economics-became-a-religion

- Ross, D. (2012a). The economic agent: Not human, but important. In U. Mäki (Ed.), Philosophy of economics (pp. 691–735). Amsterdam: North-Holland. doi:10.1016/B978-0-444-51676-3.50010-5

- Ross, D. (2012b). Economic theory, anti-economics, and political ideology. In U. Mäki (Ed.), Philosophy of economics (pp. 241–285). Amsterdam: North-Holland. doi:10.1016/B978-0-444-51676-3.50023-3

- Samuelson, P. A. (1955). Economics: An introductory analysis. 3rd ed. New York, NY: McGraw-Hill.

- Sent, E.-M. (2004). Behavioral economics: How psychology made its (limited) way back into economics. History of Political Economy, 36(4), 735–760. doi:10.1215/00182702-36-4-735

- Simon, H. A. (1976). From substantive to procedural rationality. In T. J. Kastelein, S. K. Kuipers, W. A. Nijenhuis, & G. R.Wagenaar (Eds.), 25 years of economic theory: Retrospect and prospect (pp. 65–86). Boston, MA: Springer. doi:10.1007/978-1-4613-4367-7_6

- Starmer, C. (1999). Experimental economics: Hard science or wasteful tinkering? The Economic Journal, 109(453), F5–F15. doi:10.1111/1468-0297.00398

- Thaler, C. (2016). Behavioral economics: Past, present, and future. American Economic Review, 106(7), 1577–1600. doi:10.1257/aer.106.7.1577

- Thaler, R. H., & Sunstein, C. R. (2003). Libertarian paternalism. American Economic Review, 93(2), 175–179. doi:10.1257/000282803321947001

- Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving decisions about health, wealth, and happiness. New Haven, CT: Yale University Press.

- Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science (New York, N.Y.), 185(4157), 1124–1131. doi:10.1126/science.185.4157.1124