?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Analyzing 70 countries over the period 1973–2006, we empirically show that, in the aftermath of financial crises, income inequality exhibits no general pattern of change. This holds for both advanced and emerging economies. However, when we break down the analysis by crisis types, we find that, after stock market crises, inequality goes down in advanced countries, while there is no statistically significant association in emerging ones.

KEYWORDS:

I. Introduction

The recent financial crisis has put income inequality once again at centre stage of day-to-day discussions among politicians, economists and policymakers. Within this context, understanding the distributional impact of financial crises remains a crucial prerequisite for optimal policy design. While anecdotal evidence suggests a catalytic role for crises in driving subsequent inequality,Footnote1 whether this constitutes an empirical regularity is still an open question that requires more systematic data analysis.

While some researchers investigate the financial crisis – inequality nexus arguing that widening inequality led to the recent financial crisis (Bordo and Meissner Citation2012; Kumhof, Rancière, and Winant Citation2015; Kirschenmann, Malinen, and Nyberg Citation2016; Perugini, Holscher, and Collie Citation2016), we focus on whether financial crises impact the distribution of income. Crises might have distributional effects through a variety of channels: differing responses of labour and capital income, relative price changes and heterogeneous change in the availability of credit across the income distribution, among others. Our understanding of the consequences of financial crises on income inequality has so far been limited to country studies (Grabka Citation2015; Callan et al. Citation2014; Wolff Citation2013).Footnote2 We make a first step to fill this gap in the literature by implementing a difference-in-differences analysis in a panel of advanced and emerging economies to examine whether financial crises are a precursor to income inequality.

Analyzing 70 countries over the period 1973–2006, we show that, in the aftermath of financial crises, there is no general pattern in the evolution of income inequality. This holds for both advanced and emerging economies. However, when we break down the analysis by crisis types, we find that, after stock market crises, inequality goes down in advanced countries, while there is no statistically significant association in emerging countries. The results, therefore, suggest that stock market crises reduce wealth at the top of the wealth distribution, where portfolios are dominated by business equity, in countries where capital markets are more developed.

II. Data and econometric specification

We identify financial crisis occurrences using the database of ‘Dates for Banking Crises, Currency Crashes, Sovereign Domestic or External Default (or Restructuring), Inflation Crises and Stock Market Crashes (Varieties)’ by Reinhart and Rogoff (Reinhart Citation2010; Reinhart and Rogoff Citation2009, Citation2011), which covers 70 countries over 1800–2010.Footnote3

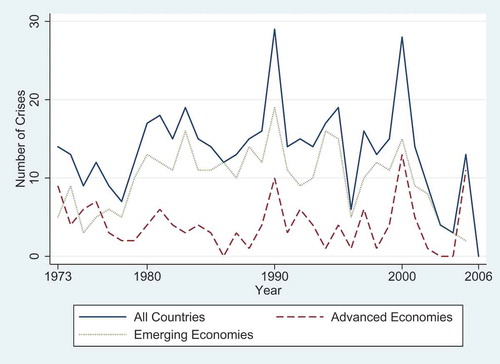

The database distinguishes six financial crisis types: Stock Market, Currency, Inflation, Domestic Debt, External Debt and Banking Crises. On average, 13.5 crisis incidents take place in a given year. illustrates the prevalence of crises over time. To evaluate inequality in the aftermath of financial crises, we first combine all financial crisis types into a single measure. We construct a Post-Crisis indicator that equals one within the 5-year aftermath of any crisis (including the crisis year). Next, we break down our analysis into different crisis types.

Figure 1. Total number of crisis occurrence over time.

As per inequality, we rely on the Standardized World Income Inequality Database by Frederick Solt (Citation2009).Footnote4 This data set provides comparable Gini indices of market (gross) and net income inequality (after taxes and redistribution) for 192 countries in the past 40 years and is well suited for cross-country analysis of income inequality as it maximizes comparability for the largest possible sample of countries and years. After matching with the Reinhart and Rogoff’s data on financial crises, we are left with a data set containing information on 70 countries for the period 1973–2006.

We estimate the following difference-in-differences specification:

where denotes the outcome of interest, inequality, at time t for country i; PostCrisis is an indicator variable equal to one within 5 years (including the crisis year) after the start of any of the six crises;

and

are country and time fixed effects; and

is the error term. SEs are clustered at the country level. In the main estimations, we restrict the sample to countries that experienced at least one crisis and the time window to 20 years around the start of a crisis, so as to compare a crisis episode with the relevant set of countries and time periods.

III. Empirical results

Baseline results

presents regressions of both inequality measures on the post-crisis indicator controlling for country and year fixed effects. There is no evidence of a statistically significant general relationship between the occurrence of financial crises and a subsequent change in inequality. Even though the coefficient on Post-Crisis is positive in columns 1 and 2, it is not statistically different from zero. Therefore, in general, we do not observe a change in inequality in the aftermath of financial crises. Columns 3 and 4 and columns 5 and 6 show robustness to the use of 10-year and 30-year windows, respectively.

Table 1. Inequality after financial crises.

Heterogeneity across advanced and emerging economies

We now investigate heterogeneity across advanced and emerging economies.Footnote5 This is a natural next step as financial market development varies across advanced and emerging economies.

In , the signs of the correlations between financial crises and inequality differ across advanced and emerging economies. In the aftermath of financial crises, inequality trends downwards in advanced economies and upwards in emerging ones, albeit insignificantly (columns 1 and 3).

Table 2. Inequality after financial crises across advanced and emerging economies.

A breakdown by crisis types

We now present a breakdown by crisis types. shows that most of the coefficients enter negatively. This suggests that there is no increase in inequality in any of the post-crisis environments. Moreover, the coefficient on post-currency crisis suggests that inequality is reduced after currency crises.

Table 3. Inequality after financial crises and heterogeneity across crisis types.

To better capture differing dynamics, Panels A and B of provide results for advanced and emerging economies. Panel B shows that the correlation between financial crisis and inequality is never significant in emerging economies. In contrast, for advanced economies, we observe that inequality significantly goes down in the aftermath of stock market crises. The income share of the wealthy is reduced as they usually invest more in the stock market. The coefficient in column 1 of Panel A corresponds to a 2.4% reduction with respect to the mean inequality in advanced countries. Furthermore, we obtain that (i) inequality trends upwards after inflation crisis (Panel A column 5); (ii) there are no domestic or external debt crises in advanced economies; and (iii) inequality is reduced after banking crisis only after taxes and redistribution.

Table 4. Inequality after financial crises and heterogeneity across crisis types for advanced and emerging economies.

IV. Concluding remarks

This article shows that, in the aftermath of financial crises, there is no general pattern in the evolution of income inequality. When we break down the analysis by crisis types, we find that, after stock market crises, inequality goes down in advanced countries, while there is no association in emerging ones.

Acknowledgements

We thank Vincenzo Bove, Casper Hansen, Dario Pozzoli and Pierre-Louis Vezina for their comments.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 See Financial Times (Citation2016, Citation2017); Kuhn, Schularick, and Steins (Citation2018).

2 Data availability is a reason for scant empirical evidence, as cross-country data with comparable financial crises and inequality measures became available recently.

3 Available at http://www.carmenreinhart.com/data/browse-by-topic/topics/7. See Reinhart and Rogoff (Citation2009, 7–11) for definitions of crises.

5 IMF classification. https://www.imf.org/external/datamapper/NGDPD@WEO/OEMDC/ADVEC/WEOWORLD.

References

- Bordo, M. D., and C. M. Meissner. 2012. “Does Inequality Lead to a Financial Crisis?” Journal of International Money and Finance 31 (8): 2147–2161. doi:10.1016/j.jimonfin.2012.05.006.

- Callan, T., B. Nolan, C. Keane, M. Savage, and J. R. Walsh. 2014. “Crisis, Response and Distributional Impact: The Case of Ireland.” IZA Journal of European Labor Studies 3 (1): 9. doi:10.1186/2193-9012-3-9.

- Financial Times. 2016. “Inequality Decreased after Global Financial Crisis.” Financial Times, October 2.

- Financial Times. 2017. “How Global Income Inequality Has Shifted Since the Crisis.” Financial Times, August 12.

- Grabka, M. M. 2015. “Income and Wealth Inequality after the Financial Crisis: The Case of Germany.” Empirica 42 (2): 371–390. doi:10.1007/s10663-015-9280-8.

- Kirschenmann, K., T. Malinen, and H. Nyberg. 2016. “The Risk of Financial Crises: Is There a Role for Income Inequality?” Journal of International Money and Finance 68: 161–180. doi:10.1016/j.jimonfin.2016.07.010.

- Kuhn, M., M. Schularick, and U. Steins. 2018. “How the Financial Crisis Drastically Increased Wealth Inequality in the U.S.” Technical Report, Harvard Business Review. Cambridge, Massachusett: Harvard Business School Publishing.

- Kumhof, M., R. Rancière, and P. Winant. 2015. “Inequality, Leverage, and Crises.” American Economic Review 105 (3): 1217–1245. doi:10.1257/aer.20110683.

- Perugini, C., J. Holscher, and S. Collie. 2016. “Inequality, Credit and Financial Crises.” Cambridge Journal of Economics 40 (1): 227–257. doi:10.1093/cje/beu075.

- Reinhart, C. M., and K. S. Rogoff. 2009. This Time It’s Different: Eight Centuries of Financial Folly. Princeton, NJ: Princeton University Press.

- Reinhart, C. M. 2010. “This Time Is Different Chartbook: Country Histories on Debt, Default, and Financial Crises.” NBER Working Papers 15815.

- Reinhart, C. M., and K. S. Rogoff. 2011. “From Financial Crash to Debt Crisis.” American Economic Review 101 (5): 1676–1706. doi:10.1257/aer.101.5.1676.

- Solt, F. 2009. “The Standardized World Income Inequality Database.” Technical Report, Harvard Dataverse, V20.

- Wolff, E. N. 2013. “The Asset Price Meltdown, Rising Leverage, and the Wealth of the Middle Class.” Journal of Economic Issues 47 (2): 333–342. doi:10.2753/JEI0021-3624470205.