?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the evolution of the capital structure of European firms during the global financial crisis and European debt crisis. We compare the experiences of SMEs, listed firms and private firms in different industries and investigate the role of country and institutional factors in affecting capital structure. We find that SMEs, private firms, and non-listed firms experience lower declines in leverage relative to large firms during the global financial crisis and the European debt crisis. During these crises’ periods, SMEs experience steeper declines in debt maturity, which suggests reliance on short term debt that carries high roll over risks. This behaviour is protracted for firms in the agriculture industry. Both the global financial crisis and EU debt crisis have asymmetric effects on leverage, long term debt issuance and debt maturity across different industries, and across firms of different sizes. Moreover, in countries with more developed financial systems, stronger frameworks for insolvency, resolving firm insolvency, and strong systems for shareholder suits, and director liability, SMEs experience much lower reduction in leverage and debt maturity. This finding suggests that institutional factors help attenuate adverse capital supply shocks.

1. Introduction

The global financial crisis and European debt crisis are deemed to have altered the capital structure decisions of firms across Europe. The increasing threats of bankruptcy and insolvency due to heightened financial and macroeconomic instability during these periods triggers a series of deleveraging across different countries, as companies become more risk averse (Demirgüç-Kunt, Peria, and Tressel Citation2020; World Bank Citation2015). In Europe and across the world, countries experience widening credit spreads (Stracca Citation2013), elevated liquidity risks (Allen and Moessner Citation2013; Collignon Citation2012), a decline in equity prices (Grima and Caruana Citation2017), and a near-freeze of credit markets. In Europe, where most economies are bank-dependent, bank lending deteriorates in response to depleted capital positions (Allen and Moessner Citation2013). Consequently, several firms engage in systematic deleveraging and scale back on investments (Campello et al. Citation2012).Footnote1 However, little is known about the cross-industry impacts of these global shocks on firms’ capital structures in Europe.

The global financial crisis and European sovereign debt crisis raises important questions about how financial and macroeconomic instability that affect capital supply channels impact firms’ capital structures decisions across different industries. Several questions arise such as, do the global financial crisis and European debt crisis affect firms in different industries the same? Do institutional and financial factors influence the evolution of capital structure in response to capital supply shocks? Do market access and firm size play a role? Given that Small to Medium Enterprises and private firms are significant drivers of the real economy in Europe, and command a significant share of entrepreneurship, innovation, employment, and economic growth (Ayyagari, Beck, and Demirguc-Kunt Citation2007; Kirchhoff et al. Citation2007; Lee et al. Citation2010), practitioners and policy-makers are interested in knowing how these firms are impacted by financial and macroeconomic shocks that affect the industries in which they operate. Moreover, private firms, and small to medium enterprises that face significant financial constraints due to high information asymmetries and agency cost related frictions find it difficult to access external finance relative to large firms (Jensen and Meckling Citation1976). As a result, capital market shocks are likely to have an asymmetric impact on these firms.

Moreover, different industries respond differently to business cycle changes that influence capital supply and costs of debt or equity. In addition, product market characteristics, and associated cashflow volatility and firm riskFootnote2 tend to influence capital structure (Frank and Goyal Citation2009; Harris and Roark Citation2019; Martin Citation2022). Titman (Citation1984) suggests that businesses that produce products requiring specialised servicing and spare parts face high liquidation and bankruptcy costs, and often seek to maintain low levels of leverage. This implies that companies in such industries choose low leverage in periods when demand for the firms’ products is low and financial distress costs are high. Financial structure, technology, and risk are jointly determined at the industry level and industry factors account for both inter- and intra-industry variability in the capital structure (MacKay and Phillips Citation2005).Footnote3 And if global shocks have a differential impact on the equilibrium factors that drive financial structure, risk, and technology within industries, such variations may be detected in the observed cross-industry variability of capital structure, thus providing an indication of the impact of the financial crisis on different industries. As a result, we expect to find differential reactions of capital structure to capital supply shocks in these industries.

This study examines how the capital structure of firms across different industry groups in Europe behave during the global financial crisis and the European debt crisis using a unique firm level-dataset of both public and private firms. Our dataset has more than 1.2 million observations from 159,000 European companies in 38 countries. The dataset covers the period 2004–2020. Since the two crises have different origins, dimensions, and relatively dissimilar outcomes in the global economy, it is possible that they differ in their impact on firms’ financing choices across industries. We test whether the two crises alter the level and composition of firms’ capital structure across different industries in Europe and explore the role of firm size, listing status, institutional factors, and country characteristics in the evolution of capital structure decisions across different industries in response to capital supply shocks.

Earlier studies focus on the within-country effects of financial crises on the investment behaviour of innovative versus non-innovative firms (Giebel and Kraft Citation2019), investment behaviour of companies of different size groups (Zubair, Kabir, and Huang Citation2020), and the role of institutional and country characteristics in explaining capital structure decisions during the crisis (Bae and Goyal Citation2009; World Bank Citation2015) among other things. Our study focuses on the impact of the global financial crisis and European debt crisis on firms’ capital structure decisions across eight different industry groups. We examine whether industries are affected the same by these two crises. A study closely related to ours is that of Demirgüç-Kunt, Peria, and Tressel (Citation2020).

We find that capital supply shocks arising from the global financial crisis and European debt crisis have differential impacts across industries. For instance, we find that the crises result in a decline in leverage across all industries except the mining industry which experienced an increase in leverage during the European debt crisis but suffered no material impact from the global financial crisis. While long term debt financing declined across all industries during both the global financial crisis and European debt crisis, long-term debt financing and debt maturity seemed to increase for firms in the mining sector during the European debt crisis period. However, the increase in long-term debt and debt maturity seems to be enjoyed by large firms in this industry. The two crises had asymmetric effects across different industries in Europe and across firms of different sizes and listing statuses. We show that total debt to total assets, long-term debt to total assets, and debt maturity respond differently across industries to the global financial crisis and the European debt crisis.

We also find that these differential effects vary in both magnitude and direction for companies in countries in different income groups, institutional arrangements, and levels of financial development. Moreover, we find that factors such as banking sector competition, deeper financial markets, strong insolvency, and resolution frameworks help attenuate the adverse impact of financial crises in general, but that they are much more important in protecting SMEs in the manufacturing, construction, wholesale, transport, and telecommunications industries. Contrary to popular beliefs, we find that in high-income European countries, deleveraging is more pronounced among large and listed firms than among SMEs and unlisted firms. This finding seems to corroborate the findings of Campello, Graham, and Harvey (Citation2009); Campello et al. (Citation2012). However, the reverse is true in upper-middle-income and lower-middle-income countries, where small firms and non-listed firms face steeper declines in leverage relative to large firms.

Our finding that the decline in leverage is less severe for SMEs and non-listed companies in Europe relative to listed companies and large firms, coupled with the observation that these SMEs rely more on short maturity debt during this period, suggests that firms use pre-contracted credit lines during this period, consistent with Campello et al. (Citation2012) and Acharya and Steffen (Citation2020). Our results point to the important role of banks in Europe, where most economies are bank dependent.

The remainder of this paper is organised as follows. Section 2 provides a brief review of the relevant literature. Section 3 describes the data and provides summary statistics. Section 4 presents the empirical model used in this study. Section 5 discusses the empirical findings, and Section 6 concludes.

2. Literature review and hypothesis development

Financial crises impact firms through a variety of mechanisms that transmit through capital supply and demand channels (Brunnermeier Citation2009; Gorton Citation2010; Kahle and Stulz Citation2013; Shleifer and Vishny Citation2010). Increases in uncertainty and risk, and the intensification of information asymmetry problems often make lenders reluctant to lend (Dang and Nguyen Citation2023; Gissler, Oldfather, and Ruffino Citation2016) which affects net debt issuance and capital expenditure for bank dependent firms (Huang Citation2003). In Europe, where many economies are bank dependent, the impact of financial crises are likely to be higher and more protracted among constrained, bank dependent firms. On the demand side, firms may choose to forgo investment opportunities in periods of high uncertainty resulting in a reduction in demand for external finance (see Campello, Graham, and Harvey Citation2009; Kahle and Stulz Citation2013). To the extent that firms can obtain funding during periods of economic turmoil, these firms are likely to opt for long term finance to minimise roll over risks associated with short term funding. Small to medium enterprises, which in theory face high information asymmetry costs, agency costs, higher financial distress, and bankruptcy costs as well as higher debt overhang problems and are less likely to obtain long term loans – may instead increase drawdowns from pre-contracted lines of credit during periods of financial crisis (see Campello, Graham, and Harvey Citation2009). However, the degree to which the financial crises may impact firm’s capital structure is likely to depend on the characteristics of the financial system and institutional environments in which firms operate (Demirgüç-Kunt, Peria, and Tressel Citation2020), as well as the nature of the firms’ product markets (Frank and Goyal Citation2009; Harris and Roark Citation2019; Martin Citation2022).

Reddy, Mirza, and Yahanpath (Citation2022), note that the quality of a country's institutional factors significantly influences the speed of adjustment of leverage for small and medium sized firms during financial crisis periods. They find that during the sovereign debt crisis period, small and medium sized companies adjust their capital structure faster in non-stressed countries compared to similar firms in the stressed countries. In a related study, Demirgüç-Kunt, Peria, and Tressel (Citation2020) find that leverage and debt maturity reductions among SMEs are more pronounced in nations with less effective legal systems, fewer effective information-sharing mechanisms, underdeveloped financial sectors, and more limitations on bank entry. However, they also observe that a considerable drop in leverage and debt maturity among listed corporations is less certain – these firms are typically much larger than other firms and are more likely to benefit from the ‘spare tire’ of improved access to capital market financing.

Domenichelli (Citation2020) examines the impact of the limited availability of bank credit during the financial crisis on corporate leverage among listed, unlisted, family, and non-family-owned firms. The study finds that unlisted companies lower their leverage due to a shortage of bank credit, whereas listed companies, who have access to financial markets, typically kept their debt levels the same as they can offset the decline in bank lending through capital market borrowing. For large and listed firms, capital markets access act as a ‘spare tire’ during financial crises (Demirgüç-Kunt, Peria, and Tressel Citation2020). Domenichelli (Citation2020) also finds that unlisted family enterprises do not significantly lower their leverage relative to unlisted nonfamily firms, despite their focus on socio-emotional wealth and its protection.

The above logic leads to the following hypothesis:

H1: During crisis periods, SMEs and unlisted firms across all industries reduce their leverage, relative to that of listed firms and large firms.

H2: During periods of financial turmoil, firms increase the maturity of their debt portfolios, and this effect is more pronounced among SMEs and unlisted firms.

H3: Country and institutional factors may help amplify or attenuate the adverse effects of financial crises on firms’ capital structure decisions across different industries.

3. Data and descriptive statistics

Firm-level data were obtained from Bureau van Dijk’s Amadeus database, which covers both private and publicly listed companies in Europe. Our data spanned the period from 2004 to 2020. As in Frank and Goyal (Citation2003), we exclude firms with missing, negative or zero total assets. We drop all public utility firms, financial firms, government and quasi government institutions, real estate firms, companies with limited financials and companies with consolidation code C2. Similar to the procedure used by Demirgüç-Kunt, Peria, and Tressel (Citation2020), companies with no employee data or average employees of less than 10 over the sample period were also excluded.

To limit the extent of survivorship bias, our sample includes active firms, liquidated firms, and firms undergoing liquidation or reorganisation. However, firms with fewer than four consecutive years of financial data are dropped from the sample, which may induce survivorship bias. We conducted several estimations over different samples and relaxed the restriction on consecutive years to gauge the extent of this bias.Footnote4 Companies from offshore financial centre countries and countries with fewer than ten firms in each reporting year were also eliminated from the sample. Our final sample includes more than 1.2 million observations from more than 159,000 companies in 38 countries in Europe.

Data on country characteristics were obtained from the World Bank’s Global Financial Development database, while GDP data were taken from the World Bank’s World Development Indicators database. Information on insolvency frameworks, credit information etc. was sourced from the World Bank’s Doing Business database. The industry classification in this study is based on 3 digits SIC code titles.

Our main variables of interest are the ratios of total financial debt to total assets (TDTA), long term debt to total assets (LTDTA) and long-term debt to total debt (LTDTD). The first two variables capture the extent to which companies finance their assets with debt and long-term debt, respectively. The LTDTD variable is a proxy for debt maturity composition in the firm’s capital structure. Like Rajan and Zingales (Citation1995), Demirgüç-Kunt, Peria, and Tressel (Citation2020), we adopt a narrow measure of total financial debt that includes only short-term debt and long-term debt and excludes other short-term liabilities, such as creditors and other current liabilities.Footnote5 This is consistent with capital structure theory, which focuses on externally sourced finance. On average, the ratios of total debt to total assets, long term debt to total assets and long-term debt to total debt reported in Table were 0.352, 0.078 and 0.191, respectively. However, about 45.25% of the firms in the sample have no long-term debt, and about 2.15% are zero-leverage firms.

Table 1. Summary statistics.

The firm-level determinants of capital structure used in this study include firm size, asset tangibility, profitability, growth opportunities, and cash ratios. These control variables capture the effects of agency costs, information asymmetry problems, and bankruptcy costs that influence capital structure decisions. Further detail on the construction of the variables is provided in Table 12, supplemental online.

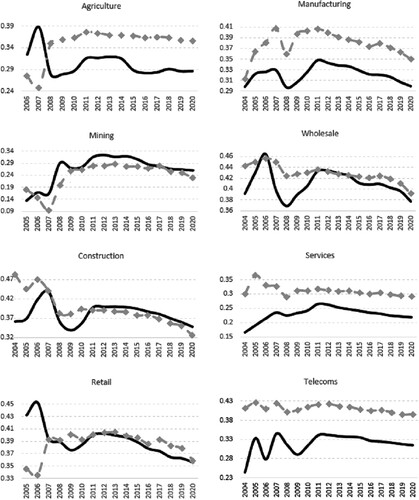

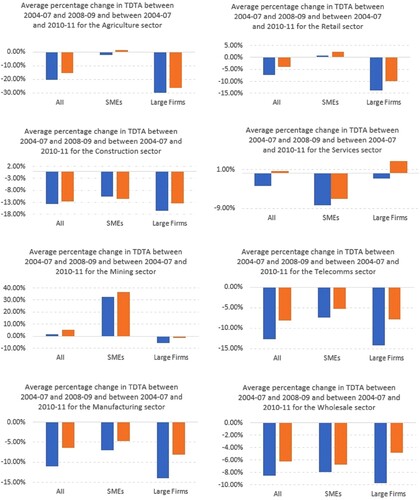

The average firm in our sample has US$77 million in total assets (of which 24.7% of those assets are tangible fixed assets), keeps approximately 9.9% of its balance sheet in cash and cash equivalents, and is profitable with a return on assets ratio of about 7.2%. The median firm in the sample has approximately US$20 million in total assets. SMEs constitute approximately 47.5% of our sample, and about 1.5% of the firms in our sample are listed on a publicly traded exchange, whereas almost 98.5% of the firms in the sample are privately held. Table shows that firm characteristics and capital structures vary by industry. On average, companies in the mining, telecommunications, manufacturing, services, construction, retail, wholesale, and agriculture industries have total assets of approximately US$510 million, US$120 million, US$80 million, US$80 million, US$70 million, US$70 million, US$50 million, and US$40 million, respectively. Firms in wholesale, retail, and construction industries tend to have more debt and shorter debt maturities. The average total debt to total assets ratios in these industries are 0.42, 0.39, and 0.38, respectively. In the services, mining, and agricultural industries, companies seem to have lower leverage and higher debt maturities. Leverage ratios in these industries are 0.26, 0.28, 0.32, respectively. However, there tends to be considerable variation in capital structures in these industries among companies of varied sizes. Figure shows the trends in the leverage ratios of small to medium enterprises (SMEs) and large firms over the sample period. Figures and show the average changes in the total debt-to-total assets ratios and long-term debt to total debt ratios for the period 2004–2020, respectively. The figures suggest that both the global financial crisis of 2008–2009 and the European debt crisis of 2010–2011 had differential and asymmetric impacts on SMEs and large firms across different industries in Europe.

Figure 1. Trends in the total debt to total assets (by size).

Figure 2. Evolution of Total debt to total assets.

Figure 3. Evolution of debt maturity.

Table 2. Summary statistics by industry.

4. Empirical models

To assess the changes in firms’ capital structures in response to the global financial crisis and European debt crisis across different industry groups we estimate a simple model linking the firms’ capital structure to observable firm level variables, unobservable time invariant characteristics, and time dummies that capture the global financial crisis and European debt crisis. The baseline empirical model employed in this study is as follows:

(1)

(1) where

is the dependent variable (either total debt to total assets ratio, long-term debt to total assets ratio, or long-term debt to total debt ratio) for firm i in country j at time t.

is a vector of control variables for firm i in country j at time t.

is a set of firms fixed effects to capture firm heterogeneity and t controls for time fixed effects that are common for all firms such as changes in macroeconomic policy. GF crisis is a dummy variable for the 2008/2009 global financial crisis, and Euro debt crisis is a dummy indicator variable for the European debt crisis of 2010/2011. The coefficients of interest are

and

which capture the behaviour of firms’ capital structures in response to the global financial crisis and the European debt crisis, respectively.

is a firm-level residual term. In the complete sample, regressing the ratios of total debt to total assets, long term debt to total assets, and long-term debt to total debt ratios against their own lags we find correlations of 0.53, 0.39, and 0.43, respectively. Although we find relatively low persistence, there is likely to be within panel serial correlation and cross panel correlation because firms that operate within the same industry may share similar supply chains, international financial market conditions for capital, and similar markets for final goods and services. Moreover, firms operating within the same country may be exposed to similar macroeconomic policy shocks. To correct for the possibility of both within and cross panel correlations, we estimate our results using the Driscoll and Kraay standard errors that correct for both heteroskedasticity, and cross panel and within correlations up to two lags.Footnote6

We distinguish between small and medium sized enterprises, listed and unlisted firms to investigate the impact of the crisis on these firms. Listed companies only constitute about 1.5% of the total number of firms in the sample.

(2)

(2)

To examine the impact on listed versus unlisted companies we estimate the following model:

(3)

(3)

In both estimations, our coefficients of interest are and

which capture the differential behaviour of SMEs and listed firms’ capital structures in response to the global financial crisis and the European debt crisis, respectively. The impacts of the global financial crisis and European debt crisis on the average firm are given by

and

, respectively, while their impacts on listed companies and SMEs are given by

and

, respectively.

Jõeveer (Citation2013) and Giannetti (Citation2003) assert that a substantial portion of the variation in firm leverage is due to macroeconomic and institutional factors. To examine whether country characteristics influence capital structure behaviour across industries, we modify our model specification to include the influence of country characteristics.

(4)

(4) where CCj represents the country characteristics associated with country j. The coefficients

and

capture the impact of the global financial crisis and European debt crisis on large corporations in countries associated with country characteristic CC. The differential impacts of the global financial crisis and European debt crisis on SMEs in countries with a given country characteristic are given by

and

, respectively. The country characteristic variables employed in this study capture institutional factors at the country level that are likely to impact capital structure, such as the degree of investor protection, private contract enforcement, presence of insolvency resolution regimes, strength of the country’s insolvency framework, extent of director liability, information disclosure, level of bank competition, and financial market depth among other factors.

5. Results

5.1. Baseline regression results

Table presents results from estimating the average effects of the global financial crisis and European debt crisis on the capital structure of firms across different industries in Europe. The estimation accounts for time invariant firm level heterogeneity and time varying firm characteristics that may impact firms’ capital structure.Footnote7 Panel A shows that on average the global financial crisis and European debt crisis result in a decline in the total debt to total assets ratio of 2 percentage points and 3 percentage points, respectively. The impact of both the global financial crisis and the European debt crisis seems to be more protracted on firms in the agriculture industry which suffer a decline on 4 percentage points in their total leverage during both crises. Companies in manufacturing experience declines of 1 percentage point and 3 percentage points in their total debt ratios during the global financial crisis and European debt crisis, respectively. These effects are significant at the 0.1% level. However, the results seem to suggest that on average, firms in mining do not seem to experience a statistically significant decline in leverage during the global financial crisis (the coefficient in not statistically significant at the 5% level) but register a 2.4 percentage point increase in leverage during the European debt crisis. Results also show that for all but the construction and agriculture industries, the magnitudes of the impact of the global financial crisis and European debt crisis on leverage were different across all industries.

Table 3. Total debt to total assets.

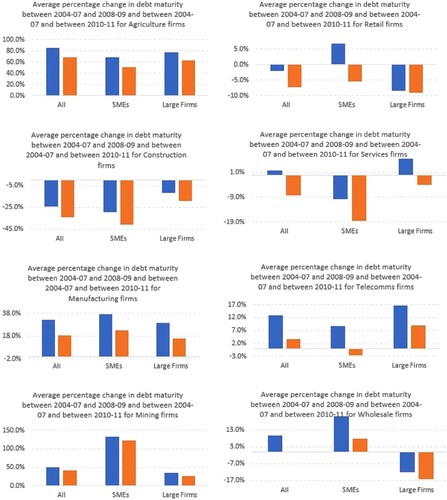

Table results show that the long-term debt to total assets ratio for the average firm declined by almost 1 percentage point for both the global financial crisis and the European debt crisis. The impacts of the global financial crisis and European debt crisis on the long-term debt to total debt ratio differ for firms in the agriculture, manufacturing and mining industries which register increases of 2.9 percentage point and 2.4 percentage points, 0.8 percentage points and 0.7 percentage points, 1.1 percentage points, respectively.Footnote8 Results in Table also highlight that the average firm experienced a change in debt composition, with long term debt declining by 1 percentage point during the global financial crisis and European debt crisis, respectively. Companies in all but the construction and retail industries experience an increase in debt maturity. For companies in the agriculture industry, the long-term debt to total debt ratio increases by 6-percentage points and 4 percentage points during the global financial crisis and the European debt crisis, respectively. This result seems to suggest that firms in the agriculture, mining, manufacturing, services, and telecoms industries may have lowered their total indebtedness by reducing the level of short-term debt in their capital structure during the crises. However, firms in the mining industry seem to have increased their overall leverage by contracting more long-term debt during the global financial crisis and European debt crisis periods. This finding of increased debt maturities during periods of financial crisis is consistent with Diamond and He (Citation2014) who argue that firms aim at lengthening debt maturity because roll over costs of short-term debt increase during periods of financial crises.

Table 4. Long term debt to total assets.

Table 5. Long term debt to total debt.

5.2. Small versus large companies

Results in Table Panel A column 1 show that although both the global financial crisis and European debt crisis lead to a significant reduction in total debt to total assets ratios, long term debt to total asset ratios, and debt maturities of the average firm across all industry groups, the impact of both crises on the leverage of SMEs was lower relative to large firms. The results also show that on average SMEs experienced lesser declines in long term debt issuance relative to larger firms during the global financial crisis. However, results on debt maturity indicate that SMEs shorten the maturity structure of debt relative to large firms during periods of crisis. This finding seems to be consistent with Campello et al. (Citation2012) and Campello, Graham, and Harvey (Citation2009) who also find that smaller, constrained, private, and less profitable firms draw-down on their lines of credit more than large, listed, and profitable companies with less financial constraints.

Table 6. Impact of crisis on SME and Large firms.

Table Panel A column 3 shows that in the agriculture industry, SMEs suffer steeper declines in leverage relative to large firms. Panels B and C also show that for SMEs in the agriculture sector, the reduction in leverage is associated with a decline in long term debt and a corresponding decline in debt maturity. Our results also show that SMEs in the mining sector (Table columns 4) witness steep reductions in long-term debt and debt maturity relative to large firms during both crises. In the wholesale sector, only the European debt crisis results in a decline in long-term debt, and debt maturity among SMEs relative to large firms (Table columns 7).

These results seem to indicate that small firms experience a smaller reduction in leverage relative to larger firms in both crises but witness a steeper decline in long-term debt issuance and debt maturity during the global financial crisis and European debt crisis periods. These results seem to suggest that SMEs draw down on short-term credit lines during crisis periods. These findings appear to be consistent with Alves and Francisco (Citation2015) who find that during periods of financial strain, some companies increase their leverage by relying on short-term debt and taking heightened rollover risks. Campello, Graham, and Harvey (Citation2009; Citation2012), Acharya and Steffen (Citation2020) and Li, Strahan, and Zhang (Citation2020) also find that constrained firms draw more heavily on credit lines during the two crises periods due to fears that banks may restrict their access to finance in future periods relative to unconstrained firms.Footnote9

5.3. Listed versus unlisted companies

Contrary to Becker and Ivashina (Citation2014) and Demirgüç-Kunt, Peria, and Tressel (Citation2020), we find that on average, large, listed companies experience sharp declines in leverage, long term debt and debt maturity during both the global financial crisis and the European debt crisis relative to private firms (see Table , column 1). Our results are in line with the survey evidence from Campello, Graham, and Harvey (Citation2009) and Campello et al. (Citation2012). We also find that for all but companies in the mining (Table , column 4) and wholesale industries (Table , column 7), the total debt to total assets ratio declines faster for listed firms than for private firms during both the global financial crisis and European debt crisis. While listed companies in the construction sector experience a sharper decline in leverage relative to unlisted firms, there were no differential impacts on the long-term debt to total assets ratio and the long-term debt to total debt ratio when compared to the average unlisted firm in the sample (Table , column 5). Only listed companies in agricultural industries suffer a sharper decline in debt maturity during both the global financial crisis and the European debt crisis relative to the average unlisted firm. Listed firms in the manufacturing, transport, and telecommunications industries suffer a decline in debt maturity during the global financial crisis and European debt crisis, respectively. In all the other sectors, there were no material differences in the debt maturities of listed and unlisted firms during the two crises.

Table 7. Impact of crisis on listed companies and non-listed companies.

5.4. Country characteristics and institutional environments

On average, SMEs in G7 and high-income countries in Europe experience less severe declines in leverage relative to larger firms during the two crises. However, SMEs in upper-middle-income and lower-middle-income countries experience a sharp decline in their total debt to total assets ratios relative to large countries (see Table , column 1) during the same period. The results show that in countries with strong institutional environments characterised by competitive banking systems, deeper financial markets, strong insolvency frameworks and rules that make it easy to sue shareholders and directors, SMEs face less severe declines in total leverage relative to large companies during both crises. However, in countries with poor information disclosure rules, poor contract enforcement systems, and longer time lags in enforcing contracts, SMEs face a larger reduction in leverage relative to large firms. In countries with weak institutional environments, an increase of one standard deviation in contract enforcement time results in an average decline in total leverage of approximately 0.7% among SMEs compared to only 0.3% among large firms.

Table 8. Impact of country characteristics capital structure of SMEs relative to large firms across different industries during the global financial crisis and European debt crisis (Total financial debt to total assets).

Our results (Table , columns 2–9) also show that the presence of bank competition, deeper financial systems, strong insolvency frameworks and strong rules for investor protection and corporate governance result in lower declines in leverage for SMEs relative to large firms in the manufacturing, agriculture, construction, transport, telecommunications, and wholesale industries during both crises.Footnote10

Table 9. Impact of country on characteristics capital structure of SMEs relative to large firms across different industries during the global financial crisis and European debt crisis (Long term debt to total assets).

Results in (Table ) also show that in concentrated banking markets, SMEs in the manufacturing, wholesale, and retail industries experience a much lower decline in debt maturity than the average large firm. The positive relationship between bank concentration and leverage, and bank concentration and debt maturity seem to be consistent with Gonzalez and González (Citation2008), who argue that bank concentration substitutes for creditor protection and asset tangibility to reduce agency problems between managers and shareholders. We also find that, in countries with strong insolvency frameworks and resolution regimes, high extent of director liability, ease of shareholder suit, and deeper financial markets, SMEs experience a lesser impact of both the global financial crisis and the European debt crisis. However, in countries with longer time frames in contract enforcement, SMEs face a steeper decline in their long-term debt to total assets ratio than large firms during both the global financial crisis and the European debt crisis. This effect seems to be prevalent among SMEs in the manufacturing, retail, and wholesale industries.

We also find that for countries that directly faced sovereign debt crises, that is, Portugal, Italy, Ireland, Greece and Spain, SMEs in the manufacturing industry experience an increase in total leverage and a steeper decline in their long-term debt to total assets ratios and debt maturity relative to large firms. This result seems to suggest that in these countries banks specialise in lending at shorter maturities to SMEs and that this role becomes much more important during periods of financial crisis (Diamond Citation1991).

Table column 1 highlights that in G7 countries, high-income countries, countries that previously suffered systemic banking crisis, countries with long times for contract enforcement, competitive banking systems; SMEs experience a steeper decline in debt maturity relative to the average large firm during the global financial crisis and the European debt crisis. This seems protracted for SMEs in manufacturing, construction, wholesale, and services industries. Our findings seem to suggest that SMEs make use of pre-negotiated credit lines during times of financial crises, and that banks play a key role in providing credit during times of turmoil. Our results appear to be consistent with Campello, Graham, and Harvey (Citation2009; Citation2012) and Ivashina and Scharfstein (Citation2008) who find an increase in ‘just in case’ draw downs on credit lines during the global financial crisis.

Table 10. Differential impact of the global financial crisis and the European debt crisis on the long-term debt to total debt ratios of SMEs relative to large firms in countries with different country characteristics (Debt Maturity).

In upper-middle-income countries, there were no significant differences in the decline in the debt maturity of SMEs and large firms during both the global financial crisis and European debt crisis, except for SMEs in agricultural industries that experienced a 3.24 percentage point decline in debt maturity relative to large firms during the European debt crisis (see Table columns 3). Our results suggest that firms in the manufacturing and wholesale industries are more responsive to changes in country and institutional characteristics than those in other industries. Overall, these results show that the global financial crisis and European debt crisis have differential impacts across industries, firms of different sizes and countries with different institutional characteristics.

5.5. Dynamic effects

In this section, we estimate the dynamic adjustment of capital structure across different industries for SMEs relative to large firms in our sample, using Flannery and Hankins’ (Citation2013) partial adjustment model. The partial adjustment model takes the following form:

(5)

(5) where Zi,t−1 is a vector of variables that influence the speed of adjustment,

, towards the target leverage, and

and

are composite parameters. The model is estimated using Blundell and Bond’s (Citation1998) generalised method of moments (GMM) which controls for possible endogeneity problems. Similar to Aybar-Arias, Casino-Martinez, and Lopez-Gracia (Citation2012), we consider size to be a factor that influences the speed of adjustment.

Our results in Table show that while the global financial crisis results in a slowdown in the speed of adjustment towards target leverage, SMEs tend to adjust faster relative to large firms. SMEs in the mining, wholesale, and services sectors seem to actively adjust their leverage levels relative to large firms during the global financial crisis and European debt crisis. These results seem to corroborate the ‘dash-to-cash’ phenomenon in Acharya and Steffen (Citation2020), which occurs during periods of economic turmoil among firms facing financial constraints.

Table 12. Dynamic adjustment of leverage across industries.

5.6. Robustness checks

In our robustness checks, we change the dependent variable for leverage to a broader measure of total leverage which is measured by the total non-equity liabilities to total assets ratio and drop the filter of four consecutive observations and positive debt issuance. We find that our results remain consistent for all leverage regressions. We also note that the magnitudes of the coefficients for both the global financial crisis and European debt crisis become large for both the full sample and each industry (see Table 13, supplemental online). Furthermore, we find that, on average, SMEs and non-listed firms experience a lesser decline in total leverage relative to large firms during both financial crises. Like earlier results, we also find that SMEs in the agriculture industry faced a steeper decline in leverage during both the global financial crisis and European debt crisis (see Table 14, supplemental online). The result in Table 15, supplemental online confirms the earlier results in Table and show that, except for firms in the agriculture industry, the leverage of listed firms fell more than that of unlisted firms during both the global financial crisis and the European debt crisis. Similar to Campello et al. (Citation2012), we also use a larger employee threshold of 250 employees for defining SMEs and re-examine the impact of this on our results. We also find that the results for leverage remain relatively unchanged, even when we consider the effect of country and institutional characteristics (see Table 16, supplemental online). Our robustness tests show that changes in the definition of leverage, sample size or changes in the definition of SMEs do not change the results of how the global financial crisis and the European debt crisis impact SMEs relative to large firms, nor of the effect of institutional and country characteristics in attenuating the impact of financial crises on SMEs. Furthermore, the results of our rolling regressions (see Tables 17, supplemental online and 18, supplemental online) for the leverage and debt maturity of SMEs relative to large firms during the crises periods seem consistent with our earlier findings and show that the coefficients for the SMEs variables tend to vary throughout the sample. This is also confirmed by the Chow test results for structural breaks in Table 19, supplemental online.

5.7. Limitations of the study and suggestions for further research

A major challenge we encounter in this dataset is attrition bias; many firms tend to fall out of the sample because of either insolvency or a lack of financial reporting data, particularly for private firms that voluntarily report their results. In addition, our filtering method may induce survival bias in the regression results; however, we run several robustness checks wherein we change the filter from four consecutive observations to all firms with at least two consecutive observations. We find that our results generally remained consistent for different filter levels. However, survivorship and attrition bias cannot be ruled out as having some degree of effect on the estimates.

Furthermore, our sample consisted of companies from Western and Eastern Europe. As a result, differences in reporting standards between countries induce measurement bias in our estimated results. Although we filtered out countries with known reporting weaknesses, it is possible that we did not completely cure this problem. While including private firms in the sample helps enrich the study, it is not possible to use market variables as controls in the regressions, which might induce a missing variable problem. However, we use several firm-level control variables and macroeconomic variables to reduce this bias. Lastly, our results may be plagued by endogeneity problems between our dependent variable and our firm-level control variables. To limit the degree of endogeneity, we include macroeconomic variables in our regressions. In addition, we run GMM regressions to examine the capital structure dynamics of firms across different industries, which helps us capture potential feedback effects. We find that our results remain largely consistent, even when we consider capital structure dynamics during periods of financial crisis.

Further studies should consider directly examining the impact of dislocations in the funding markets as measured by disparities in the covered interest rate parity relations, disparities in spreads between the FX swap and Libor funding markets, and dislocations in the markets for inflation-linked bonds, on the speed of adjustment of firms with different ownership structures, sizes, listing status, and operating in countries with different institutional environments.

6. Conclusion

This study examines the impact of the global financial crisis of 2008–2009 and the European sovereign debt crisis of 2010–2011 on the capital structure of firms of different sizes, and listing statuses across different industry groups in Europe. The study also seeks to establish whether country and institutional factors amplify or help attenuate the impact of the global financial crisis and European debt crisis on the capital structures of firms in Europe. We control for firm-level heterogeneity, time fixed effects, and other firm level demand-related determinants of capital structure. We find that both the global financial crisis of 2008–2009 and the European debt crisis of 2010–2011 result in sharp declines in leverage, long-term debt and debt maturity of firms in Europe. However, contrary to popular belief, we find that SMEs, and private firms or non-listed firms experience smaller declines in leverage relative to large firms during both the global financial crisis and European debt crisis. We also find that this effect is persistent across industries other than the agriculture and mining. In the agriculture industry, SMEs experienced much larger declines in leverage, long-term debt, and debt maturity relative to large firms during both the global financial crisis and European debt crisis. In the mining sector, we observe that SMEs faced sharp reduction in long term debt and debt maturity during the global financial crisis but there were no differential effects between SMEs and large firms during the European debt crisis. We also find that listed firms experience much sharper declines in leverage, long-term debt, and debt maturity, relative to non-listed firms. We also find that these effects are persistent in agricultural and manufacturing industries. However, there were no significant differences in leverage, long-term debt, and debt maturity between listed and non-listed firms during both the global financial crisis and European debt crisis. Our results also show that in countries with deep financial systems, concentrated banking sectors, and strong insolvency and resolution frameworks, SMEs in the manufacturing, mining, construction, transport, and telecommunications industries face less steep declines in leverage relative to large firms. We find evidence that institutional factors such as stronger corporate governance systems, insolvency frameworks, and banking sector competition assist in reducing the impact of financial crises on SME funding. Surprisingly, we find that in concentrated banking markets, SMEs obtain short term finance during both the global financial crisis and the European debt crisis. Our results s suggest that banks play a unique role in SME financing in Europe.

7. Message of the study

The message of our study is that firms in different industries respond differently to financial crises, which tend to impact capital supply channels. In periods of financial crisis, SMEs experience an increase in leverage and a decline in debt maturity, which tend to reflect reliance on short-term debt (most likely precontracted lines of credit). This implies that banking institutions tend to play a significant role in providing crucial funding to SMEs during periods of stress. Moreover, SMEs in countries with stronger institutional environments tend to be more resilient to funding shocks that restrict or disrupt their access to finance.

8. Message to policy makers

Strengthening institutional frameworks for insolvency, bank resolution, governance etc., helps build the resilience of SMEs to financial stress, particularly emerging from financial crises that impact capital supply channels.

Supplemental Material

Download MS Word (100.5 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Tinashe C. Bvirindi

Tinashe C. Bvirindi is a Lecturer at Coventry University. His research interest include Corporate Finance, Monetary policy and Macroprudential policy, Stock markets and the Macroeconomy, Bank regulation & competition, and Return predictability.

Ode-Ichakpa Inalegwu

Ode-Ichakpa Inalegwu is an Associate Professor in Accounting at East Stroudsburg University of Pennsylvania in the United States. His research interest is in corporate governance, corporate social responsibility, financial reporting, sustainability, and corporate finance. He has publications in journals such as Building Research & Information (RBRI) and International Journal of Business Governance & Ethics among others.

Notes

1 In addition, Giebel and Kraft (Citation2019) using data for German firms show that the global financial crisis had differential impact on the investment behaviour of innovative firms that rely on external finance relative to non-innovative firms, and on innovative firms that rely on internal finance. They show that innovative firms suffer the most in terms of access to financial markets, leading to a reduction in capital investments.

2 Harris and Raviv (Citation1990) note that industries with less opportunities for asset substitution generally have higher leverage ratios.

3 Reinartz and Schmid (Citation2016) in an examination of worldwide energy utilities find evidence of a positive relationship between higher production flexibility and leverage. This implies that in industries where production volumes can be quickly, easily, and efficiently reduced to avoid operational losses when price falls below marginal costs, firms may operate with higher levels of leverage relative to other industries.

4 We discuss the results of these estimations under robustness tests.

5 Welch (Citation2011) proposes the use of total non-equity liabilities to assets ratio as an alternative to the narrow leverage measures. We use this measure in our robustness tests provided in Table .

6 However, one drawback of this model is that it requires a large T and a large N sample. Although our N is fairly large, the sample is only for a 17-year period.

7 Coefficients on the control variables seem to support both the pecking order and the trade-off theories of capital structure. Firms size is positively related to leverage, consistent with the trade-off theory, whilst the profitability and the cash ratio are negatively related to leverage as suggested by the pecking order theory. However, the coefficients on growth opportunities seem to be inconsistent with expectations.

8 A formal test of the magnitude of the coefficient shows that there are no material differences in the impact of the global financial crisis and the European debt crisis on the long-term debt to total asset ratios of firms in the construction, transport and telecommunications, and services industries. However, the two crises result in material differences in debt maturity across all industries.

9 Campello, Graham, and Harvey (Citation2009) note that in the US, constrained firms have pre-contracted credit lines of approximately 26% of their book asset value whereas unconstrained firms have about 19% of their book asset value as pre-arranged credit. During the crisis, 17% of constrained firms draw down their credit lines as a precaution in case banks may deny them credit relative to only 6% of unconstrained firms.

10 This result is consistent with Demirgüç-Kunt, Peria, and Tressel (Citation2020).

References

- Acharya, V., and S. Steffen. 2020. “The Risk of Being a Fallen Angel and the Corporate Dash for Cash in the Midst of Covid.” The Review of Corporate Finance Studies 9 (3): 430–471. https://doi.org/10.1093/rcfs/cfaa013

- Allen, W. A., and R. Moessner. 2013. “The Liquidity Consequences of the Euro Area Sovereign Debt Crisis.” Working Paper Series WP02/13. Centre for Banking Research, Cass Business School, City University London. Accessed August 2, 2022. https://www.bayes.city.ac.uk/__data/assets/pdf_file/0020/420419/CBR-WP02-13.pdf.

- Alves, P., and P. Francisco. 2015. “The Impact of Institutional Environment on the Capital Structure of Firms During Recent Financial Crises.” The Quarterly Review of Economics and Finance 57: 129–146. https://doi.org/10.1016/j.qref.2014.12.001

- Aybar-Arias, C., C. Casino-Martinez, and J. Lopez-Gracia. 2012. “On the Adjustment Speed of SMEs to Their Optimal Capital Structure.” Small Business Economics 39 (4): 977–996. https://doi.org/10.1007/s11187-011-9327-6

- Ayyagari, M., T. Beck, and A. Demirguc-Kunt. 2007. “Small and Medium Enterprises Across the Globe.” Small Business Economics 29 (4): 415–434. https://doi.org/10.1007/s11187-006-9002-5

- Bae, K. H., and V. K. Goyal. 2009. “Creditor Rights, Enforcement, and Bank Loans.” The Journal of Finance 64 (2): 823–860. https://doi.org/10.1111/j.1540-6261.2009.01450.x

- Becker, B., and V. Ivashina. 2014. “Cyclicality of Credit Supply: Firm Level Evidence.” Journal of Monetary Economics 62 (C): 76–92.

- Blundell, R., and S. Bond. 1998. “Initial Conditions and Moment Restrictions in Dynamic Panel Data Models.” Journal of Econometrics 87 (1): 115–143. https://doi.org/10.1016/S0304-4076(98)00009-8

- Brunnermeier, M. K. 2009. “Deciphering the Liquidity and Credit Crunch 2007–2008.” Journal of Economic Perspectives 23 (1): 77–100. https://doi.org/10.1257/jep.23.1.77

- Campello, M., E. Giambona, J. R. Graham, and C. R. Harvey. 2012. “Access to Liquidity and Corporate Investment in Europe During the Financial Crisis.” Review of Finance 16 (2): 323–346. https://doi.org/10.1093/rof/rfr030

- Campello, M., J. Graham, and C. R. Harvey. 2009. “The Real Effects of Financial Constraints: Evidence from a Financial Crisis.” Working Paper 15552. NBER Working Paper Series. National Bureau of Economic Research.

- Collignon, S. 2012. “Europe’s Debt Crisis, Co-ordination Failures and International Effects.” ADBI Working Paper Series No 370/July 2012. Asian Development Banking Institute. Accessed August 2, 2022. https://www.adb.org/sites/default/files/publication/156225/adbi-wp370.pdf.

- Dang, V. D., and H. C. Nguyen. 2023. “Banking Uncertainty and Lending: Does Bank Competition Matter?” Journal of Asia Business Studies 17 (4): 741–765. https://doi.org/10.1108/JABS-09-2021-0360

- Demirgüç-Kunt, A., M. S. M. Peria, and T. Tressel. 2020. “The Global Financial Crisis and the Capital Structure of Firms: Was the Impact More Severe Among SMEs and Non-Listed Firms?” Journal of Corporate Finance 60: 101514. https://doi.org/10.1016/j.jcorpfin.2019.101514

- Diamond, D. W. 1991. “Monitoring and Reputation: The Choice Between Bank Loans and Directly Placed Debt.” Journal of Political Economy 99: 689–721.

- Diamond, D., and Z. He. 2014. “A Theory of Debt Maturity: The Long and Short of Debt Overhang.” The Journal of Finance 69 (2): 719–762. https://doi.org/10.1111/jofi.12118

- Domenichelli, O. 2020. “Sovereign Debt Crisis and Capital Structure Decisions of Firms in GIPSI Countries.” African Journal of Business Management 14 (10): 313–323. https://doi.org/10.5897/AJBM2020.9076

- Flannery, M., and K. Hankins. 2013. “Estimating Dynamic Panel Models in Corporate Finance.” Journal of Corporate Finance 19 (C): 1–19.

- Frank, M. Z., and V. K. Goyal. 2003. “Testing the Pecking Order Theory of Capital Structure.” Journal of Financial Economics 67 (2): 217–248. https://doi.org/10.1016/S0304-405X(02)00252-0

- Frank, M. Z., and V. K. Goyal. 2009. “Capital Structure Decisions: Which Factors Are Reliably Important?” Financial Management 38 (1): 1–37. https://doi.org/10.1111/j.1755-053X.2009.01026.x

- Giannetti, M. 2003. “Do Better Institutions Mitigate Agency Problems? Evidence from Corporate Finance Choices.” The Journal of Financial and Quantitative Analysis 38 (1): 185–212. https://doi.org/10.2307/4126769

- Giebel, M., and K. Kraft. 2019. “The Impact of the Financial Crisis on Capital Investments in Innovative Firms.” Industrial and Corporate Change 28 (5): 1079–1099. https://doi.org/10.1093/icc/dty050

- Gissler, S., J. Oldfather, and D. Ruffino. 2016. “Lending on Hold: Regulatory Uncertainty and Bank Lending Standards.” Journal of Monetary Economics 81: 89–101. https://doi.org/10.1016/j.jmoneco.2016.03.011

- Gonzalez, V. M., and F. González. 2008. “Influence of Bank Concentration and Institutions on Capital Structure: New International Evidence.” Journal of Corporate Finance 14 (4): 363–375. https://doi.org/10.1016/j.jcorpfin.2008.03.010

- Gorton, G. B. 2010. “Questions and Answers About the Financial Crisis (No. w15787).” National Bureau of Economic Research.

- Grima, S., and L. Caruana. 2017. “The Effect of the Financial Crisis on Emerging Markets: A Comparative Analysis of the Stock Market Situation Before and After.” European Research Studies Journal 0 (4B): 727–753.

- Harris, M., and A. Raviv. 1990. “Capital Structure and the Informational Role of Debt.” The Journal of Finance 45 (2): 321–349. https://doi.org/10.1111/j.1540-6261.1990.tb03693.x

- Harris, C., and S. Roark. 2019. “Cashflow Risk and Capital Structure Decisions.” Finance Research Letters.

- Huang, Z. 2003. “Evidence of a Bank Lending Channel in the UK.” Journal of Banking & Finance 27 (3): 491–510. https://doi.org/10.1016/S0378-4266(02)00388-6

- Ivashina, V., and D. Scharfstein. 2008. “Bank Lending During the Financial Crisis of 2008.” Working Paper. Harvard Business School.

- Jensen, M. C., and W. H. Meckling. 1976. “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.” Journal of Financial Economics 3 (4): 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jõeveer, K. 2013. “Firm, Country, and Macroeconomic Determinants of Capital Structure: Evidence from Transition Economies.” Journal of Comparative Economics 41 (1): 294–308. https://doi.org/10.1016/j.jce.2012.05.001

- Kahle, K. M., and R. M. Stulz. 2013. “Access to Capital, Investment, and the Financial Crisis.” Journal of Financial Economics 110 (2): 280–299. https://doi.org/10.1016/j.jfineco.2013.02.014

- Kirchhoff, B. A., S. L. Newbert, I. Hasan, and C. Armington. 2007. “The Influence of University R & D Expenditures on New Business Formations and Employment Growth.” Entrepreneurship Theory and Practice 31 (4): 543–559. https://doi.org/10.1111/j.1540-6520.2007.00187.x

- Lee, S., G. Park, B. Yoon, and J. Park. 2010. “Open Innovation in SMEs—An Intermediated Network Model.” Research Policy 39 (2): 290–300. https://doi.org/10.1016/j.respol.2009.12.009

- Li, L., P. E. Strahan, and S. Zhang. 2020. “Banks as Lenders of First Resort: Evidence from the COVID-19 Crisis.” The Review of Corporate Finance Studies 9 (3): 472–500. https://doi.org/10.1093/rcfs/cfaa009

- MacKay, P., and G. M. Phillips. 2005. “How Does Industry Affect Firm Financial Structure?” Review of Financial Studies 18 (4): 1433–1466. https://doi.org/10.1093/rfs/hhi032

- Martin, J. D. 2022. “Industry Influence on Capital Structure-Revisited.” Available at SSRN 4124295.

- Rajan, R. G., and L. Zingales. 1995. “What Do We Know About Capital Structure? Some Evidence from International Data.” The Journal of Finance 50 (5): 1421–1460. https://doi.org/10.1111/j.1540-6261.1995.tb05184.x

- Reddy, K., N. Mirza, and N. Yahanpath. 2022. “Capital Structure Determinants During the Sovereign Debt Crisis Period.” Australasian Business, Accounting and Finance Journal 16 (4): 29–63. https://doi.org/10.14453/aabfj.v16i4.04

- Reinartz, S. J., and T. Schmid. 2016. “Production Flexibility, Product Markets, and Capital Structure Decisions.” Review of Financial Studies 29 (6): 1501–1548. https://doi.org/10.1093/rfs/hhv126

- Shleifer, A., and R. W. Vishny. 2010. “Asset Fire Sales and Credit Easing.” American Economic Review 100 (2): 46–50. https://doi.org/10.1257/aer.100.2.46

- Stracca, L. 2013. “The Global Effects of the Euro Debt Crisis.” Working Paper Series, No 1573/August 2013. European Central Bank. Accessed August 2, 2022. https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1573.pdf.

- Titman, S. 1984. “The Effect of Capital Structure on a Firm’s Liquidation Decision.” Journal of Financial Economics 13 (1): 137–151. https://doi.org/10.1016/0304-405X(84)90035-7

- Welch, I. 2011. “Two Common Problems in Capital Structure Research: The Financial-Debt-To-Asset Ratio and Issuing Activity Versus Leverage Changes.” International Review of Finance 11 (1): 1–17. https://doi.org/10.1111/j.1468-2443.2010.01125.x

- World Bank. 2015. Global Finance Development Report 2015: Long-Term Finance. Washington, DC: World Bank.

- Zubair, S., R. Kabir, and X. Huang. 2020. “Does the Financial Crisis Change the Effect of Financing on Investment? Evidence from Private SMEs.” Journal of Business Research 110: 456–463. https://doi.org/10.1016/j.jbusres.2020.01.063