ABSTRACT

The paper makes three contributions to the understanding of the post-crisis European banking governance. First, it offers a more comprehensive approach to banking governance, beyond the Banking Union, through its concept of ‘New European Banking Governance’ (NEBG) that incorporates EU state aid rules and fiscal regulations. Second, it considers the impact of NEBG on democratic institutions and processes in EU member states, an under-researched topic in the literature on European banking governance. Finally, through its in-depth case study of Slovenia it considers the NEBG in relation to peripheral Eurozone states. It argues that the post-crisis banking governance framework of the EU not only severely constrained the Slovenian state in its policy choices but rearranged its policy-making institutions in a way that restricted and continues to restrict democratic banking policy formation.

Introduction

In Europe, bank regulation and supervision has undergone fundamental changes since the global financial crisis. Bank and state ties have been loosened by the introduction of the Banking Union (BU) (Epstein Citation2017). The role of the European Central Bank (ECB) has been widened to policy areas previously unknown to central banking (Chang Citation2018). The European Semester and the Fiscal Compact increased the European Commission’s (EC) surveillance over member states’ fiscal policy and as a result over their banking policy as well (Verdun and Zeitlin Citation2018). The post-crisis remodelling of the governance of the European Union (EU) enhanced the multi-level polity character of member states (Scharpf Citation1999). In turn, the uneven redistribution of state competencies between the European institutions and member states have been identified as one of the causes behind the weakening of European democracy during the crisis (Scharpf Citation2014, Durand and Keucheyan Citation2015).

Relying on institutionalist analysis of the state from the comparative political economy literature, this article establishes a bridge between the politics of post-crisis banking literature (Epstein & Rhodes Citation2014, Howarth and Quaglia Citation2016, Spendzharova Citation2014, Lombardi and Moschella Citation2016, Donnelly Citation2018) and the crisis of democracy arguments (Scharpf Citation2014, Durand and Keucheyan Citation2015, Streeck Citation2015). We are particularly interested in the modalities of transformation of democratic oversight of policy formation in an EU member state during the process of bank restructuring. We contend that due to the systemic nature of finance and the interconnectedness of banks to all sectors of the economy, analysing the quality of democratic oversight of institutions that govern banking is insightful with regard to the operation of other public institutions.

Up to date, the most systemic account of the new European banking regulations and their impact on member states was provided by Epstein (Citation2017). She powerfully demonstrated how the BU decreased the Eurozone member states’ discretion over economic policy by delegating decision making power to the supranational level. However, her account of the transformation of ‘bank-state ties’ during the crisis has two limits. It studies mainly the changing relationship between the European and national authorities and institutions, leaving aside the relations between national authorities and citizens within the member states. Moreover, by focusing only on the BU, she leaves aside regulations from other macroeconomic fields that also impacted banking policy. To overcome these limitations, we propose a new conceptualisation of European regulations concerning the restructuring of banking during the crisis, introducing the term ‘New European Banking Governance’ (NEBG).

In regulatory terms, the NEBG is more encompassing than the BU. It includes (1) regulations of state aid, (2) fiscal coordination, (3) central banking, and (4) BU. The NEBG is a governance structure, which impacts the political relations of member states through a complex mechanism of multi-level political coordination of banking policy formation. The NEBG relocates significant decision-making powers from member states to the supranational level. In turn, it simultaneously increases the decision-making abilities and powers of the executive and central banking institutions and pro-NEBG experts at the national level at the expense of those related to more representative democratic policy-making and critical professionals and social groups. Rejecting local contestation to NEBG-policy is also made easier due to new legal barriers to contesting voices. The NEBG, therefore, undermines the legitimacy of both European and domestic institutions, and hence, contributes to the weakening of the European multi-level governance system as well. However, the NEBG impacts member states unevenly depending on their membership status, socio-economic situations (including the severity of the financial crisis) and political constellation. Through the case study of Slovenia, we demonstrate one particular process through which the NEBG-created constraint translates into a crisis of democracy.

As the first post-socialist Eurozone member, Slovenia is a particularly insightful case to study this process. The country has relatively new democratic institutions and represents a neo-corporatist exception in the post-socialist region (Bohle & Greskovits Citation2012, Lindstrom Citation2015). In addition, Slovenia was hard-hit by the crisis and shared with Greece, Portugal, Spain, and Cyprus both the experience of the sovereign debt crisis and the European institutions’ response to this crisis (Kržan Citation2014). However, the Slovenian government succeeded in recapitalising domestic banks without requiring the Troika’s financial assistance. Therefore, the study of bank restructuring in Slovenia allows to filter out the influence of the International Monetary Fund (IMF) and to bring forward the democracy- constraining effect of the new European regulatory framework. Hence, the Slovenian experience with the NEBG is to some extent unique. Nevertheless, the Slovenian case adds a critical variant to accounts of the post-crisis functioning of the EU and the impact of the new regulations on the institutions of EU member states.

The rest of the article is organised as follows. We first provide the theoretical background, explaining the main features of the NEBG. The following section analyses bank restructuring in Slovenia in the period of 200818 in three sub-sections. The last section concludes.

Banking Politics within the European Multi-Level Polity and the Crisis of Democracy

The deepening of the European integration after the global financial crisis has garnered significant academic attention (van Apeldoorn Citation2013, Oberndorfer Citation2015, Schimmelfenning Citation2015, Verdun Citation2015). Despite their theoretical differences, authors agree that with the post-crisis European architecture, relationships between the EU and the member states, as well as relationships within the states have changed, though significant national differences remain. This is because the changing of the levels of state regulation is not a neutral process; it unevenly reshapes state capacities and institutions and the ability of social actors to access these capacities and influence the policy-making process. Focused on preserving monetary and financial stability, the European crisis management reinforced the bargaining powers of the executive and institutions linked to finance, especially the EC, the European Council and the ECB (Keucheyan and Durand Citation2015). In addition, by interfering simultaneously in member states’ fiscal policy (including budgets over wage, health and education systems), competition rules and monetary regimes, these new regulations have significantly reduced member states’ macroeconomic capacities (Streeck and Mertens Citation2013). In turn, reduced macroeconomic policy scope narrowed down fiscal democracy, i.e. the policy choice and autonomy in government budgetary choices. Democracy not only needs to satisfy formal prerequisites such as equal voting rights, but also substantive prerequisites which are related to policy constraints (Genschel and Schwarz Citation2012). For Genschel and Schwartz (Citation2012, p. 1), ‘[f]iscal democracy is when […] the government has the power to change fiscal policies in light of voter preferences’. A democratic government must be able to actually chose from different policy choices with different redistributional consequences.

The new wave of supranational integration and deepened coordination has impacted European institutions in an uneven way. During the Eurozone crisis, the Economic and Financial Affairs Council (ECOFIN) and the European Council of the Head of the Eurozone governments became the key decision-making bodies. In contrast, no attempt was made to reinforce the powers of the European Parliament, with no right of legislative initiative or power to change the EU treaties (Streeck Citation2015). Moreover, already before the crisis, the European social dialogue was limited to specific domains and formed a ‘non-binding social partnership forum’ (Horn Citation2012, p. 583). Under the new European architecture, labour was even more side-lined. Durand and Keucheyan (Citation2015) reports that in 2011, the European Trade Union Confederation declared that ‘[d]iktats are being issued which are designed to lower living standards’ and requested an emergency meeting with Oli Rehn, EU Commissioner. ‘Social issues are not addressed for their own sake but, rather, operate as adjustment variables under the heading of financial stability, macro-supervision of fiscal policy and competitiveness’ (Durand and Keucheyan Citation2015, pp. 11–2).

Building on these insights into the weakening of European democracy, we contribute to the existing debates on bank restructuring during the crisis. Finance and banking have always been regarded as a key sector of economic policy formation by national governments. Nevertheless, governments’ capacity to shape financial markets has been decreasing ever since the liberalisation wave of the 1980s (Kurzer Citation1993, Loriaux et al. Citation1996). Contributing to the weakening control were developments in European banking regulations which shifted toward a tighter supranational harmonisation, but retained profound subsidiarity concerns, while becoming increasingly diffused among multiple actors, such as private banks, rating agencies, law firms (Sinclair Citation1994), independent government agencies (Majone Citation2001) as well as international organisations and powerful states (Germain Citation1997). In the meantime, the nature of banking has transformed as well with a shift from bank-based to market-based banking. This move had also important implications for the extent of government control (Hardie et al. Citation2013). Parallel to member states’ efforts to liberalise and re-regulate banking, banking nationalism also flourished, i.e. western European governments supported national banks with a protective regulatory environment in exchange for their support of governments’ economic policy (Perez Citation1997, Epstein and Rhodes Citation2016). As a result, democratic oversight of banking has been already substantially constrained prior to the 2008 crisis.

The global financial crisis has painfully revealed the weakness of the European banking regulatory infrastructure. The separating of the potential spill-over between the banks’ solvency problems and sovereign debt crisis was at the centre of the European crisis management. Post-crisis, researchers focused on national governments’ agreement to delegate a substantial part of decision-making power over banks to the supranational level (Epstein and Rhodes Citation2016, Lombardi and Moschella Citation2016). In addition, the characteristics of the BU was discussed such as the novelty of the new regulatory framework (De Rynck Citation2016), the dominance of powerful member-states’ interest such as Germany (Donnelly Citation2018), and the interest of other member-states (Howarth and Quaglia Citation2016), as well as the conditions under which non-Eurozone member states would join the BU (Spendzharova Citation2014, Mérő and Piroska Citation2016). However, fewer attempts have been made to link the new European banking governance to the restructuring of troubled banks in EU member states and to the weakening of democratic oversight of these policies.

Epstein’s (Citation2017) book is a notable exception. She argues that BU has transformed ‘bank-state ties’ and significantly downsized member states’ discretion over economic policy in the Eurozone. This article adds a new political dimension of state transformation to the analysis, citizens and democracy, which is unexplored in Epstein’s account. Moreover, Epstein (Citation2017) adopts a narrower definition of the new European banking regulatory and supervisory framework with an exclusive focus on the BU regulations. Because national banking systems interact with other institutional forms of national economies and macroeconomic policies, one should consider a wider array of regulations to understand the complex impact of the new European banking regulations on member states. In other words, Epstein (Citation2017) discusses the changing state capacity to pursue economic development through domestic banking policy formation. In contrast, we focus on the transformation of democratic oversight of banking policy formation, i.e. the transformation of the institutions and practices of formal democracy that define social actors’ access to power to impact upon banking policy.

New European Banking Governance

In light of the arguments put forth in the previous section, we introduce a new conceptualisation of European banking regulation. The NEBG is based on four regulatory pillars: (1) state aid policy, (2) fiscal coordination, (3) central banking, and (4) BU. A member state’s banking policy falls within all four domains to various degrees depending on the integration of the country into European structures. We think of the NEBG as a framework of governance and are interested in its overall structural impact on democratic oversight of national institutions, instead of the influence of its elements individually.

After the collapse of Lehman Brothers, the Directorate General for Competition (DG-COMP) launched six key directives to regulate state aid to the banking sector: The Banking Communication (October 2008), the Recapitalisation Communication (December 2008), the Impaired Assets Communication (February 2009), the Restructuring Communication (July 2009), the Prolongation Communication (December 2010) and the New Banking Communication (August 2013). While these directives reinforced the already existing principles regulating state aid to the corporate sector, they have proved to be too restrictive to deal with troubled banks effectively. National authorities were obliged to provide restructuring plans, with details such as the changes of management and corporate governance of the rescued banks. At the same time, the EC and external experts gained powers to check and confirm the evaluation of banks’ assets. In 2012, state aid regulation control in general was decentralised and most state aid measures were streamlined providing for faster decisions under the General Block Exemption Regulation and increasing the relevance of national authorities (Colombo Citation2019). By contrast, the administrative dominance of the Commission prevailed in case of troubled banking sectors, which required larger state aid (European Commission Citation2017). This dominance was the prevailing status quo when the BU came into force.

Until the outbreak of the Eurozone crisis, fiscal policy fell mostly under member states’ jurisdiction and remained flexible with regard to their specific circumstances. However, with the adoption of the European Semester (May 2010), Six-Pack (December 2011), Two-Pack (May 2013), and the Treaty on Stability, Coordination and Governance in the Economic and Monetary Union (March 2012), signed by all EU member states except the UK, the Czech Republic and Croatia, the competencies of the EC, especially the Directorate General for Economic and Financial Affairs (DG-ECFIN) have increased significantly. The EC was accorded the right to examine, in collaboration with the Council of the EU, the draft budget of a member state in order to provide an ex-ante opinion, and to demand revision if deemed necessary. Thus, the EC gained a policy toolkit to control and monitor the implementation of reform measures, and the power to launch the procedure to penalise a member state. Even if the new fiscal rules came with some built-in flexibility (European Commission Citation2019), overall, they restricted the government’s policy discretion and hence diminished the scope of fiscal democracy. This has impacted banking policies of member states in two ways. First, in states where banks accumulated significant burdens prior to the crisis, fiscal restrictions and austerity measures through decreasing aggregate demand caused the debt ratio to deteriorate. Second, the DG-ECFIN gained power, through the guise of budgetary concerns, to overrule significant elements of a member state’s banking policy such as taxing banks, buying and selling banks, rescuing banks, or setting up regulatory forbearance, etc.

Up to the crisis, central banks’ mandate had been narrowly defined to achieve only price stability, while the stability of the economy and the financial sector was to be achieved through the adherence to strict macroeconomic targets (Mishkin Citation2013). This has changed profoundly following the crisis, and the ECB and other off-Eurozone central banks now bear the responsibility for the supervision of the financial sector. However, the ECB and a few other central banks went further and developed competencies in a number of other domains allowing central banking authorities to become actively engaged in a member state’s macroeconomic policy-making with fiscal and redistributive consequences (Högenauer and Howarth Citation2016, Chang Citation2018). For instance, the ECB’s new crisis management instrument, the Outright Monetary Transactions (OMT) has granted it the right to put pressure on national governments with large public debt by allowing yields on government bonds to increase or by inducing such increases.Footnote1 In addition, as a member of the Troika, the ECB regularly intervened politically in the crisis management of member states and provided advice to governments (Chang Citation2018). Therefore, the ECB became active not only in shaping a member states’ monetary policy, but also their fiscal policy, and, most importantly to our argument, their banking policy (especially bank restructurings).

With the introduction of the Banking Union (2012), the ECB has assumed explicit rights to supervise, regulate and restructure banks in member states. The BU currently consists of the Capital Requirements Regulation and Directive (CRR/CRD), Single Supervisory Mechanism (SSM) and the Single Resolution Mechanism (SRM), while its third pillar, the European Deposit Insurance Scheme is still under discussion. CRR/CRD has harmonised regulation among EU member states, strengthened specific regulatory agencies within member states and accorded some discretionary powers to national authorities in using certain macroprudential tools, such as the loan-to-value and the debt-to-income ratios (Mérő and Piroska Citation2018). The SSM accorded the ECB the right to bank regulation and supervision, including the liquidation of banks. By law, the ECB was granted supremacy over national authorities in politically sensitive areas. This holds especially true in the field of bank authorisation where the ECB gained the right to make decisions over bank ownership. The SRM changed bank recapitalisation policy and introduced a new bail-in regime, obligating shareholders, bondholders and some depositors to participate in the rescuing of banks (Epstein and Rhodes Citation2016). Thus, the BU delegated substantial powers to the ECB as well as to designated national authorities.

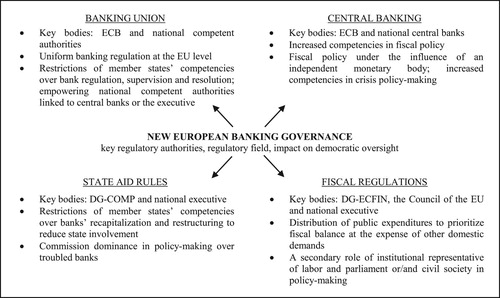

summarises the key actors and the political and regulatory characteristics of the NEBG. The NEBG operates within the European multi-level polity through the following mechanism: (1) The NEBG further re-scales a state’s decision-making by transferring considerable parts of (the remaining) macroeconomic sovereignty over fiscal, banking and competition policy to supranational institutions such as the European Commission, the Council and the ECB. At the same time, (2) the NEBG impacts the internal relations and institutions of member states’ polity and creates an executive bias at the national level through the empowering of governments and central banks in the restructuring of the financial sector. It weakens parliaments and other non-governmental actors to effectively influence banking policy. Thus, national institutions are integrated in the NEBG in an asymmetrical way. This shift in decision-making power is further enhanced by (3) a number of domestic institutional and regulatory changes through which domestic political actors try to curb the capacity of formal democratic institutions to facilitate bank restructuring. The examples for such actions include ‘fast track’ legislations and restrictions on referendum (either by constitutional courts or by legal changes) that impose legal and institutional barriers on the influence of actors contesting the NEBG policy priorities. Once implemented the institutional changes that serve short-term political interest of smoothing bank restructuring under the NEBG have long-lasting impacts as reduced democratic oversight over the banking policy-making in the consequent years. (4) The NEBG also narrows down the scope of fiscal democracy. This may occur either through prescribing restrictive budgetary targets or the constitutionalising of public debt targets. (5) The restructuring of banks under the NEBG also ease the getting into position of internationally educated and networked expert economists, while economists and experts with critical views to NEBG policy priorities are side-lined. Moreover, expert knowledge of international organisations such as the IMF, the ECB or audit firms is more often used to make sense of local banking problems, often resulting in the production of such knowledge that necessitates further curbing of discording voices. Finally, (6) local political actors might in addition use the NEBG to frame their political interest and policy choices as deriving from international obligations and to legitimate the retrenchment of democratic practices. All in all, the NEBG narrows policy-making space over banking restructuring through the changing of the scales of policy formation in favour of the European executive and technocratic actors. It also encourages national governments and central banks to by-pass or limit the influence of other state institutions and actors. The process results in the hollowing out of democratic institutions as well as increased political instability.

Figure 1. New European banking governance.

Case Study Selection and Methodology

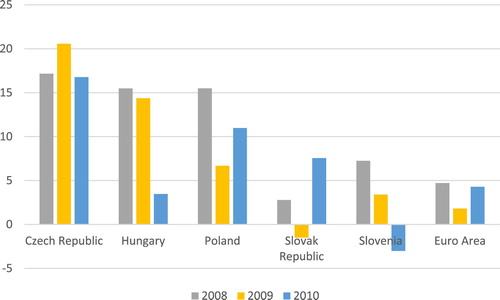

Slovenia, a Eurozone member state since 2007 with the highest GDP per capita among post-socialist countries, was exceptional in the post-socialist region, where economic nationalism supported social welfare provisions and neo-corporatism (Lindstrom Citation2015). However, the domestically owned banks accumulated significant external debt during the 2000s. Consequently, Slovenia was much harder hit by the Eurozone crisis than its post-socialist pears (see below). In fact, similarly to the Southern peripheral EU member states, the country faced a deep banking and sovereign debt crisis as well. Nevertheless, the country did not ask for the Troika’s assistance programme. Therefore, it is the ideal case to study the impact of the European governance structure without the interference of the IMF.

Figure 2. Bank return on equity (%, after tax). Source: Bloomberg.

We employ an exploratory case study method which allows us to advance theoretical insights into the influence of the NEBG on a member state’s policy formation (George and Bennett Citation2007). Since this research aims to review in time the interlinkages between the evolution of the NEBG and the bank restructuring in Slovenia, process tracing seems the most appropriate choice. This is because process tracing, as defined by Collier (Citation2011, p. 824), is ‘an analytic tool for drawing descriptive and causal inferences from diagnostic pieces of evidence – often understood as part of a temporal sequence of events or phenomena’.

In this research, for data collection, we used document analysis of official publications of the Slovenian parliament and government and the EU institutions, as well as press reviews of both the Slovenian and the international English language press. We reviewed publicly available statements made by the EU institutions and domestic actors, experts and government representatives.

Bank Restructuring under NEBG – the Case of Slovenia

Between 2008 and 2018, bank restructuring in Slovenia took place in three stages: (1) progressive destabilisation of the banking sector occurred between 2008 and 2012, followed by (2) a massive bank rescue operation in 2013 and (3) bank privatisation after 2013. In the remaining we examine the impact of the NEBG on the democratic oversight of state institutions during these three phases. In the first period, we show that the unfolding of the banking crisis was accompanied by an intense social struggle over policy priorities and the imposition of institutional and constitutional barriers to social opposition. Next, we analyse the formation of the 2013 bank rescue package to reveal an asymmetry in the integration of the Slovenian state institutions into European institutions. Finally, looking at the privatisation process of the two largest banks, the symbols of Slovenian exceptionalism during the post-socialist transition period, we demonstrate that under the NEBG, the Slovenian representative democratic institutions were side-lined, the executive was bound to ECB and EC policy choices, and social and political opposition was dismissed. All this led to the widespread sense in the Slovene population that democracy is in crisis.

Crisis Management with Undermined Fiscal Democracy

Stricter European regulations on competition and fiscal policy significantly narrowed down Slovenian fiscal democracy when the banking crisis started to deepen after 2010. The Slovenian authorities, who embraced NEBG’s priorities to restructure troubled banks, faced significant social contestation. To curb down the disapproving voices, the Slovenian executive increasingly circumvented the established neo-corporatist policy-making structures and implemented various institutional barriers. These processes culminated in increasing instability in Slovene institutions and hollowing out of democracy.

In 2008, Slovenian banks were highly exposed to the cooling of the international financial markets due to a strong concentration of foreign debt in the corporate sector (Kržan Citation2014). A full-blown banking crisis was prevented by fiscal packages that the Slovenian government implemented in coordination with the European Economic Recovery Plan and the EC’s removal of the Maastricht ceiling on public finances. The initial measures did not address the interlinkages between banks and corporate sector indebtedness. Corporate debt-to-equity ratio jumped to 146 per cent while the average ratio in the Eurozone stood at 105 per cent (Ponikvar et al. Citation2013).

In 2012, non-performing loans (NPLs) peaked at 15 per cent of total loans and represented almost a fifth of the total economic output (OECD Citation2013, p. 16). Resulting capital injections by the government into banks rapidly built up public debt, which experienced a four-fold increase between 2008 and 2014. Although the country’s public debt standing at about 54 per cent of GDP was still below the Maastricht criteria in 2012, Slovenia found itself in the middle of the Eurozone crisis turmoil once international financial markets started to lose confidence in the Eurozone countries (Kržan Citation2014).

Under the NEBG, the Slovene state was authorised to use its fiscal capacities for bank rescue at the expense of social expenditures, despite a rapid deterioration of labour market conditions. By 2013, unemployment reached its highest level after the early 1990s, exceeding 10 per cent. Even though the restructuring of banks had an important impact on the corporate sector, and hence, on employees, trade unions were largely excluded from influencing bank restructuring. In neo-corporatist Slovenia, where trade unions had significant mobilisation powers, such crisis management provoked strong social resistance from below.

Already in 2010, when the first round of austerity packages had to be adopted, the then centre-left Prime Minister Borut Pahor claimed that ‘we should not wait for the Greek scenario’ (Mekina Citation2010) to legitimize the unilateral implementation of reform package to further liberalise labour market and pension system (Stanojević and Klaric Mrčela Citation2014). When the trade unions called for a referendum against legislative changes, the Pahor administration called upon the Constitutional Court to assess the constitutional character of the implemented reform. The Constitutional Court, however, refused the government’s demand. In spring 2011, both reforms were rejected at the referendum and withdrawn from the legislation. This prompted the first early elections in the history of independent Slovenia, which took place in late 2011, and brought a right-wing government into power. Similar to its predecessor, the Janša administration used the threat of demanding conditional European financial assistance in order to legitimize an increasing disregard for the procedures of formal democracy and the rule of law (Vobič et al. Citation2014): between February and June, the coalition changed thirty-three laws under the ‘fast track’ customs procedure (Vukelič Citation2013). Despite protests by NGOs, the anti-corruption commission, and the ombudsman, the Slovenian executive continued to rapidly modify additional seventy laws by the end of 2012 (Mekina Citation2012).

During the autumn months, trade unions and the members of the recently established Positive Slovenia Party (PSP), called for a referendum against the proposed measures to resolve the banking crisis. Whereas the unions’ calls were dismissed (Dnevnik Citation2012), the PSP’s demand was reviewed by the Constitutional Court. This time, the court forbade the referendum, claiming that the gravity of the economic crisis and the state obligations included in the European treaties and intergovernmental agreements had priority over the basic principles of formal democracy. In other words, the Constitutional Court facilitated the power shift to the executive. For the Slovenian government, the Court’s decision ‘send a positive signal to the international community and financial markets’ (Pistotnik and Živčič Citation2015, p. 18).

After charges of corruption against Prime Minister Janša became public in the midst of the ‘Slovenian winter of discontent’, i.e. massive civil society mobilisation, contesting Janša’s austerity and ‘authoritarian turn’ another government change took place, bringing into power a centre-left coalition under Alenka Bratušek (PSP). When assuming power, Bratušek announced that it was necessary to ‘end the atmosphere of fear […] In Slovenia there will not be a Greek scenario […] We will try to re-establish a constructive dialogue with civil society, experts, and social partners’ (Delo.si Citation2013). However, in May 2013, the Parliament restricted referendum legislation, ‘expected to facilitate the introduction of fiscal consolidation measures’ (Council of the EU Citation2013). In the same month, the fiscal rule was brought in the constitution. Constitutionalised public debt targets together with restrictions on calling a referendum removed powerful regulatory tools that allowed Slovenian societal actors to contest the NEBG’s fiscal restrictions for social expenditures. Although these measures were not directly caused by the new European governance structures, their imposition was facilitated by the NEBG’ promotion of executive policy-making and anti-democratic bias.

The third crisis government soon lost its legitimacy and credibility. Less than a year after it took power, it was forced to resign. The early 2014 elections were won by the newly established centrist Miro Cerar Party, named after its leader. Despite being a newcomer in Slovenian politics, he remained fully committed to the main policy directions pursued by his predecessors (Stanojević et al. Citation2016, p. 6). Extreme political instability and high government turnover, with three ruling coalitions governing (on average) for less than a year and ten months (Zajc Citation2015), the early elections and fast track decision-making, as well as the undermining of fiscal democracy contributed to a loss of popular confidence in the Slovenian democratic policy-making process under the NEBG. In 2014, more than 90 per cent of the population was dissatisfied with the state of democracy, while prior to the crisis, a mere half of the population expressed similar opinion (Krašovec & Johannsen Citation2016, p. 6).

Bank Rescue with the ECB and the EC Intervention

A closer look at the 2013 banking rescue process in Slovenia reveals that the NEBG’s restriction of competition policy and state aid acted as one of the prime vehicles of the strengthening of the executive institutions at the expense of the representative democratic institutions. In addition, internationally networked economists took positions in the Ministry of Finance and the Bank of Slovenia (BS), the central bank; the local economists who criticised the enactment of the Troika’s crisis management recommendations, especially its one-size-fits-all approach, were side-lined. At the same time, the BS-coordinated bank restructuring resulted in exaggerated capital need for bank recapitalisation, increased public debt, and destined the two largest and traditionally government-controlled banks (NKBM and NLB) for privatisation.

The preparation for the massive state intervention in the banking sector started in 2012. The bank restructuring programme was designed by the Ministry of Finance, where Dejan Krušec took the position of secretary. Krušec brought with him the crisis management practices of international financial institutions. KrušecFootnote2 joined the ECB in 2006 and became a member of the IMF/EC/ECB team in 2010. As a representative of the ECB responsible for bank solvency, he participated in restructuring the banking sector in Ireland and Portugal. The restructuring of Irish banks in 2009–10 was also the model for the strategy adopted by the Slovenian governments. It consisted of creating a separate Bank Asset Management Company (BAMC) or ‘bad bank’ to take over the NPLs in return for government-guaranteed bonds. The financial framework for the operation was based on stress tests carried out by the BS in autumn 2012 based on the methodological proposals of the IMF mission (Bank of Slovenia Citation2013). It is noteworthy that many local experts disagreed with this ‘one-size-fits-all’ option, mostly because of its relatively higher public costs and the fact that this mechanism could not by itself resolve the problem of corporate indebtedness (Stošicki Citation2011, Ribnikar Citation2012, Kržan Citation2014). Those voices were, however, ignored by political authorities, while the calls for referenda were dismissed or forbidden by the government, as mentioned above.

The Bratušek coalition, coming into power in 2013, confirmed that it would continue with the restructuring strategy of its predecessor and announced a new recapitalisation plan for banks. This huge fiscal challenge coincided with a significant upgrading of the NEBG with the ‘Two-pack’ fiscal package and the launch of the BU. In addition, the decision by the EC that Slovenia was experiencing excessive macroeconomic imbalances, placed the country’s macroeconomic policies, especially state aid, under heightened control of the EU executive (Council of the EU Citation2013). During the fiscal coordination cycle in April and May, the EC stopped the excessive deficit procedures and, together with the ECB, demanded that the BS produce a new Asset Quality Review (AQR) of bank portfolios (Beloglavec and Beloglavec Citation2014). Moreover, to comply with the New Banking Communication, banking legislation regarding the provision of banking capital and insolvency procedures had to be changed in a very short time.

The AQR was carried out on banks representing about 70 per cent of the banking system. It was not only a very expensive task as only ECB accredited, multinational audit firms could be hired but also delayed much needed rehabilitation of the banking sector and produced the result that the total capital need of the banks was much higher than originally estimated by the BS (Mencinger et al. Citation2014). In addition, in mid-2013, the Governor position of the central banking authority was overtaken by Boštjan Jazbec, who has constructed a solid network of international financial institutions, like the EBRD, the WB, the BIS, as well as the IMF. The BS also strongly supported Slovenian authorities when they rapidly, and with no public discussion, modified the banking legislation to allow for the participation of bank owners and junior creditors in the recapitalisation of banks following the New Banking Communication. What is more, initially, the board of the BAMC was composed of international experts with links to the key European crisis management actors:

Lars Nyberg was president of the ECB’s crisis management group and member of a high-level expert group on financial supervision in the EU. Arne Berggren was a member of the IMF’s ‘Troika’ team in Spain, […] Carl-Johan Lindgren worked for the IMF as well. (Pistotnik and Živčič Citation2015, pp. 18–9)

Foreign-led Bank Privatisation Amidst Local Contestation

One impact of NEBG on Slovenian policy-making was to subject it to the European technocratic rule, as discussed above. In addition, it prompted Slovenian decision makers to leave the historical path of a domestic and state dominated financial sector, and to privatise the two largest banks (NKBM and NLB) amidst important social contestation.

To get the EC’s approval for recapitalisation, the Slovenian government had to commit, among other requests, to the full privatisation of NKBM by the end of 2016; the reduction of state ownership in NLB to 25 per cent plus 1 share by the end of 2017, and the merging of Abanka and Banka Celje, followed by the privatisation of the merged Abanka by the end of July 2019 (Beloglavec and Beloglavec Citation2014). These commitments expanded the privatisation programme adopted by the Parliament in the middle of 2013, which included 15 corporations from strategic sectors, such as the national airport.

In line with past experience of mass mobilisation against bank privatisation (Lindstrom and Piroska Citation2007), the planned selling of domestic banks provoked multiple forms of resistance. The new left-lined United Left Party (the Left) warned the public on several occasions that ‘[t]he Commitments that were given, are not legally binding, but are political’ (MMC RTV SLO Citation2015). The Left, as well as the trade unions, actively supported efforts by the civil society organisation ‘Citizens against privatization!’ and joined the petition movement against bank privatisation, launched by Jože Mencinger, the Slovenian economist known for being among the key designers of the country’s gradual transition path. For him ‘it [was] necessary that Slovenia increase its self-confidence in relation to the European Commission and we should not silently accept everything that they are imposing on us’ (MMC RTV SLO Citation2015). According to the public opinion poll conducted in early 2015, 64.5 per cent of participants were against the privatisation of NLB (Vičič Citation2015).

The privatisation process was controlled by the new centralised management agency, the Slovenian Sovereign Holding (SSH), established in 2014. The SSH, which received many greetings from the international financial and economic policy making community, was initially led by Matej Runjak, well-connected economist. The SSH operated as an independent regulatory agency (IRA) with low actual level of transparency. ‘[I]n July 2014, when the government asked SSH to halt the privatisation process […] SSH threatened with a lawsuit if the government did not repeal its decision’ (Pistotnik and Živčič Citation2015, p. 25). In the same year, a working task group composed of the SSH board members, and the representatives of the Minister of Finance and Infrastructure was formed that started preparations for the privatisation of the Slovenian highway system, althugh this was not mentioned in any SSH or government programmes (Mekina Citation2014). In June 2015, 100 per cent of the shares of NKBM, the second largest Slovenian bank with around 10 per cent market share, were offered to the hedge fund Apollo, a branch within Apollo Global Management, LLC that ended up owning 80 per cent of the bank’s shares (Gole Citation2015). Note that the new owner is not a commercial bank, but a hedge fund. The new owner will not provide NKBM’s customers with the well-known advantages of FDI such as know-how, international network of branches, access to capital and liquidity in times of crisis, etc. In 2015, the EBRD became the second owner of NKBM and acquired 20 per cent of the bank’s shares (Gole Citation2015).

The privatisation process of NLB was longer and invoked heated public debate. A large share of those arguing against privatisation were supporters of the party of the then Prime Minister (Vičič Citation2015). From mid-2016, the government tried to delay the privatisation process. By the beginning of 2017, the popularity of the ruling party was rapidly shrinking, and the government started to send the EC requests for changing the privatisation plan. As a consequence, the EC launched an in-depth investigation of the privatisation process that was closed in August 2018 with the EC’s approval of new commitments by the Slovenian government to privatise the bank in two steps (European Commission Citation2018). The summer months revealed that the concrete method and pace of NLB’s privatisation became an instrument of the pre-electoral competition for voters by the Miro Cerar Party. In particular, the party leader wanted to shelter himself from the political responsibility of selling the banking group that was one of the key symbols of Slovenian banking nationalist exception during the transition period.

In late 2018, 65 per cent of the bank’s shares have been sold in an initial public offering, and the EBRD became one of the biggest single institutional owners with almost 6.3 per cent of the bank’s shares. In June 2019, the remaining 10 per cent minus one share were sold through an accelerated bookbuild process to certain institutional investors. Balancing efforts between the privatisation demands by the EC and the government’s interest to maintain public support can be seen from the choice of dispersed ownership (with the government keeping 25 per cent + 1 shares) rather than selling the bank to one strategic investor. The privatisation will have a long-term negative impact on Slovenian fiscal balance, despite the one-off revenue related to the banks’ sale that would lower the Slovenian public debt and interest rates. The fiscal balance will lose significant income from the bank’s dividends which exceeded EUR 270 million in 2018. Kordež (Citation2018) estimates that the selling of the bank will worsen the fiscal result by at least EUR 130 million (0.3 per cent of GDP).

Conclusions

This paper advances a dual argument. First, it is argued that to understand the impact of post-crisis European regulations on bank restructuring in Slovenia, we must consider the new European governance structure of banking, which we referred to as the NEBG. Looking only at the interactions of state-controlled banks and Slovene governments or taking into consideration individually the impact of the Banking Union and the extended role of the ECB results only in partial accounts (Epstein Citation2017). This is because, although these regulatory and institutional changes are significant, only the consideration of the modifications made to the regulatory set up of the Single Market (in particular state aid regulations and the new fiscal rules) reveals the new European banking governance’s restricting impact on the functioning of democratic institutions in member states. Therefore, and secondly, this article argues that the NEBG did not simply reduce the scope of sovereign policy formation, but also incited a crisis in the forms and extent of democratic contestation in Slovenia.

The NEBG’s macroeconomic and policy restrictions prolonged and deepened the banking crisis in Slovenia and contributed to a costly state rescue, which boosted state debt and led to the privatisation of the key systemic banks. In addition, during the bank restructuring institutional and political capacities of the democratic ‘invoice’ of the Slovenian social actors, known for using their mobilisation capacities to actively participate in banking restructuring in the past, were significantly undermined.

The Slovenian experience is to some extent unique in the post-socialist periphery. We contend that the NEBG impacts member states differently depending on their membership in various EU regimes, their socio-economic status, and the severity of their financial crisis experience. However, it is noteworthy that the strengthening of the executive under the NEBG enhances the power of authoritarian leaders such as Orbán and Kaczyński as well to execute a nationalist banking policy even if they operate outside the BU and in the absence of a major bank crisis (Mérő and Piroska Citation2016). In fact, despite the corruption accusation (see above) and the over political alliance with Orbán, the Slovenian Democratic Party led by Janša increased its popularity in recent years and even won the elections in 2018 but was incapable of making a coalition. Another allusion to the hollowing out of democratic institutions can be seen in the harder-hit Romania when, in the framework of the Vienna Initiative, transnational banks forged a politicised public–private governance to manage the Romanian debt crisis (Cornel Citation2019). Similarly, post-crisis policy making in the Baltics states have been reported to suffer from consolidated technocratic rule and ethnic hollowness (Cianetti Citation2018). In our opinion, studying other states on the EU post-socialist periphery with the help of the framework provided by the NEBG may provide important insights into the functioning of democratic institution on the EU Eastern periphery.

Acknowledgements

We thank Daniel Mertens, Peter Volberding, Gergő Medve-Bálint, Joachim Becker and Robert Lieli who provided comments that greatly enriched this article, although they may not agree with all of our conclusions.

Disclosure Statement

No potential conflict of interest was reported by the authors.

Notes on contributors

Dóra Piroska is Visiting Professor at the Department of International Relations, CEU and an Associate Professor at the Department of Economic Policy, Corvinus University of Budapest. She holds a PhD from the CEU in Political Science IR track. She is a political economist with research and teaching interests in international and comparative political economy, politics of finance and institutional theories. She has a special interest in the Central and Eastern European region. Her latest research focuses on development finance both at the national and international levels. She has a special interest in the EBRD. Recently she has published on the macroprudential turn in bank regulation, on the Banking Union’s perception in Eastern non-Eurozone member states and on the competing crisis management approaches of the Troika institutions. She published in Competition and Change, Europe-Asia Studies, Journal of Economic Policy Reform, Policy and Society and Third World Thematics and in a number of Hungarian outlets.

Ana Podvršič is a Marie Curie Research Fellow at the Centre for Southeast European Studies at the Karl Franzens University in Graz. She holds a PhD from sociology and economics from the University of Ljubljana and University Paris13. She is a political economist with research and teaching interests in institutionalist and critical international and comparative political economy, post-socialist transformation, European integration and uneven development. She is especially interested in the Central, Eastern and Southeastern European region. Her latest research focuses on the role of finance in Yugoslav state disintegration, the crisis of democracy in the European Union, transformation of accumulation regime post-2008/2007 global crisis and the integration of post-socialist economies in global value chains. Recently she has published several articles on the peripherisation of the Slovenian economy.

Additional information

Funding

Notes

1 An example regarding Italy for the possible use of OMT: https://www.bloomberg.com/news/articles/2018-05-29/ecb-s-whatever-it-takes-toolbox-means-italy-has-to-blink-first.

2 The information provided here are based on Mekina (Citation2015).

Related Research Data

References

- Bank of Slovenia, 2013, October 17. Bank of Slovenia stress tests 2013. Retrieved from https://www.bsi.si/iskalniki/sporocila-zajavnost-en.asp?VsebinaId=15894&MapaId=202#15894.

- Bohle, D. and Greskovits, B., 2012. Capitalist diversity on Europe’s periphery, cornell studies in political economy. Ithaca, NY: Cornell University Press.

- Chang, M., 2018. The creeping competence of the European Central Bank during the Euro Crisis. Credit and capital markets – Kredit und Kapital, 51 (1), 41–53. doi: 10.3790/ccm.51.1.41

- Cianetti, L., 2018. Consolidated technocratic and ethnic hollowness, but no backsliding: reassessing Europeanisation in Estonia and Latvia. East European politics, 34 (3), 317–36. doi: 10.1080/21599165.2018.1482212

- Collier, D., 2011. Understanding process tracing. PS: political science & politics, 44 (4), 823–30.

- Colombo, C.M., 2019. State aid control in the modernisation era: moving towards a differentiated administrative integration? European law journal, 25 (3), 292–316. doi: 10.1111/eulj.12324

- Cornel, B., 2019. Dependent development at a crossroads? Romanian capitalism and its contradictions. West European politics, 42 (5), 1041–1068. doi: 10.1080/01402382.2018.1537045

- Council of the EU, 2013. Council recommendation on the national reform program of Slovenia 2013 (C 217/75).

- Delo.si. 2013. Alenka Bratušek je nova mandatarka, 27 February. Available from: http://www.delo.si/novice/vladna-kriza/v-zivo-alenka-bratusek-je-nova-mandatarka.html.

- De Rynck, S., 2016. Banking on a union: the politics of changing eurozone banking supervision. Journal of European public policy, 23, 119–35. doi: 10.1080/13501763.2015.1019551

- Dnevnik. 2012. Sindikat KNG: Kam je izginilo 394 podpisov na poti od DZ do MNZ?. Dnevnik, 5 November. Available from: https://www.dnevnik.si/1042561935/slovenija/sindikat-kng-kam-je-izginilo-394-podpisov-na-poti-od-dz-do-mnz.

- Donnelly, S., 2018. Power politics, banking union and EMU: adjusting Europe to Germany. London: Routledge.

- Durand, C., and Keucheyan, R., 2015. Financial hegemony and the unachieved European state. Competition & change, 19 (2), 129–44. doi: 10.1177/1024529415571870

- Epstein, R.A. 2017. Banking on markets: the transformation of bank-state ties in Europe and beyond.

- Epstein, R.A. and Rhodes, M.J., 2014. International in life, national in death? Banking nationalism on the road to banking union. KFG working paper series 61.

- Epstein, R.A., and Rhodes, M., 2016. The political dynamics behind Europe’s new banking union. West European politics, 39 (3), 415–37. doi: 10.1080/01402382.2016.1143238

- European Commission. 2017. State aid: how the EU rules apply to banks with a capital shortfall – Factsheet. (n.d.). Available from: http://europa.eu/rapid/press-release_MEMO-17-1792_en.htm [Accessed 18 January 2019].

- European Commission. 2018. State aid: commission approves new Slovenian commitment package for Nova Ljubljanska Banka. Press release IP/18/4961.

- European Commission. 2019. Applying the rules of the stability and growth pact. (n.d.). [Text]. Available from https://ec.europa.eu/info/business-economy-euro/economic-and-fiscal-policy-coordination/eu-economic-governance-monitoring-prevention-correction/stability-and-growth-pact/applying-rules-stability-and-growth-pact_en [Accessed 18 January 2019].

- Genschel, P., and Schwarz, P. 2012. Tax competition and fiscal democracy. TranState Working Papers (161).

- George, A.L., and Bennett, A., 2007. Case studies and theory development in the social sciences. Cambridge and London: MIT Press.

- Germain, R.D., 1997. The international organization of credit: states and global finance in the world-economy. Cambridge: Cambridge University Press.

- Gole, N. 2015. NKBM prodana Apollu in EBRD za 250 milijonov evrov Delo.si, 3 June. Available from: http://www.delo.si/gospodarstvo/finance/nkbm-prodana-apollu-in-ebrd-za-250-milijonov-evrov.html.

- Hardie, I., et al., 2013. Banks and the false dichotomy in the comparative political economy of finance. World politics, 65 (4), 691–728. doi: 10.1017/S0043887113000221

- Högenauer, A.-L., and Howarth, D. 2016. Unconventional monetary policies and the ECB’s problematic democratic legitimacy.

- Horn, L., 2012. Anatomy of a ‘critical friendship’: organized labour and the European state formation. Globalizations, 9 (4), 577–92. doi: 10.1080/14747731.2012.699935

- Howarth, D., and Quaglia, L., 2016. The political economy of European Banking Union. New York, NY: Oxford University Press.

- IMAD. 2014. Development report 2014.

- Keucheyan, R., and Durand, C., 2015. Bureaucratic caesarism. Historical materialism, 23 (2), 23–51. doi: 10.1163/1569206X-12341406

- Kordež, B. 2018. Tudi z bogato kupnino od prodaje NLB bo naš javni dolg še vedno 31 milijard evrov. Portalplus portal, 6 September. Available from: https://www.portalplus.si/2871/o-plusih-in-minusih-prodaje-nlb/.

- Krašovec, A. and Johannsen, L., 2016. Recent developments in democracy in Slovenia. Problems of Post-Communism, 63 (5–6), 313–322. doi: 10.1080/10758216.2016.1169932

- Kržan, M., 2014. Crisis in Slovenia: roots, effects, prospects. METU studies in development, 41 (3), 323–48.

- Kurzer, P., 1993. Business and Banking: Political Change and Economic Integration in Western Europe. Ithaca, NY: Cornell University Press.

- Lindstrom, N., 2015. Wither diversity of post-socialist welfare capitalist cultures? crisis and change in Estonia and Slovenia. European journal of sociology, 56 (1), 119–39. doi: 10.1017/S0003975615000065

- Lindstrom, N., and Piroska, D., 2007. The politics of privatization and Europeanization in Europe's periphery: Slovenian banks and breweries for sale? Competition & change, 11 (2), 117–35. doi: 10.1179/102452907X181938

- Lombardi, D., and Moschella, M., 2016. Domestic preferences and European banking supervision: Germany, Italy and the single Supervisory mechanism. West European politics, 39 (3), 462–82. doi: 10.1080/01402382.2016.1143242

- Loriaux, M., 1996. Capital ungoverned: liberalizing finance in interventionist states. Ithaca: Cornell University Press.

- Majone, G., 2001. Nonmajoritarian institutions and the limits of democratic governance: a political transaction-cost approach. Journal of institutional and theoretical economics (JITE)/Zeitschrift für die gesamte Staatswissenschaft, 157 (1), 57–78. doi: 10.1628/0932456012974747

- Mekina, B. 2010. Ivan Svetlik, minister za delo, družino in socialne zadeve. Mladina, 14 May. Available from: http://www.mladina.si/50541/ivan-svetlik-minister-za-delo-druzino-in-socialne-zadeve/.

- Mekina, B. 2012-Nazaj v leto 1988. Mladina, 23 November. Available from: https://www.mladina.si/118047/nazaj-v-leto-1988/.

- Mekina, B. 2014. Adijo, avtoceste. Mladina, 7 November. Available from: https://www.mladina.si/161788/adijo–avtoceste.

- Mekina, B. 2015. Saga o slabi banki. Mladina, 9 October. Available from: http://www.mladina.si/170046/saga-o-slabi-banki/.

- Mencinger, J., Juuse, E., and Kattel, R., 2014. Financial regulation in Slovenia. FESSUD working paper series 58.

- Mérő, K., and Piroska, D., 2016. Banking Union and banking nationalism — explaining opt-out choices of Hungary, Poland and the Czech Republic. Policy and society, 35 (3), 215–26. doi: 10.1016/j.polsoc.2016.10.001

- Mérő, K., and Piroska, D., 2018. Rethinking the allocation of macroprudential mandates within the Banking Union – a perspective from east of the BU. Journal of Economic policy reform, 21 (3), 240–56. doi: 10.1080/17487870.2017.1400435

- Mishkin, F.S. 2013. Central Banking after the crisis. Working papers Central Bank of Chile, 714.

- MMC RTV SLO. 2015. “Državljani proti razprodaji” predsedniku DZ-ja in vladi predali peticijo, 15 January. Available from: https://www.rtvslo.si/slovenija/drzavljani-proti-razprodaji-predsedniku-dz-ja-in-vladi-predali-peticijo/355838.

- Oberndorfer, L., 2015. From new constitutionalism to authoritarian constitutionalism: new economic governance and the state of European democracy. In: J. Jäger and E. Springler, eds. Asymmetric crisis in Europe and possible futures critical political economy and post-Keynesian perspectives. London: Routledge.

- OECD. 2013. Economic surveys: Slovenia 2013.

- Perez, S.A., 1997. Banking on privilege: The politics of Spanish financial reform. Ithaca: Cornell University Press.

- Pistotnik, A., and Živčič, L. 2015. Impact of international finance and other institutions on key policies of Slovenia. Available from: http://www.sinteza.co/wp-content/uploads/2015/11/07-Pri-reC5A1evanju-krize-smo-posluC5A1ali-le-tuje-akterje-C5A0TUDIJA-aa.pdf.

- Ponikvar, N., Tajnikar, M., and Došenović Bonča, P., 2013. A small EU country attempting to exit the economic crisis: rediscovering the post-Keynesian perspective on incomes and prices policy. Journal of post Keynesian economics, 36 (1), 153–74. doi: 10.2753/PKE0160-3477360108

- Ribnikar, I., 2012. Dokapitalizacija bank in strateški investitorji. Bančni vestnik, 61 (11), 4–10.

- Scharpf, F.W., 1999. Governing in Europe. Oxford: Oxford University Press.

- Scharpf, F.W., 2014. After the crash: a perspective on multilevel European democracy. MPIfG discussion paper, 14(21).

- Schimmelfennig, F., 2015. Liberal intergovernmentalism and the euro area crisis. Journal of european public policy, 22 (2), 177–95. doi: 10.1080/13501763.2014.994020

- Sinclair, T.J., 1994. Passing judgement: Credit rating processes as regulatory mechanisms of governance in the emerging world order. Review of international political economy, 1 (1), 133–59. doi: 10.1080/09692299408434271

- Spendzharova, A.B., 2014. Banking union under construction: the impact of foreign ownership and domestic bank internationalization on European Union memberstates’ regulatory preferences in banking supervision. Review of international political economy, 21 (4), 949–79. doi: 10.1080/09692290.2013.828648

- Stanojević, M. and Kanjuo Mrčela, A., 2014. Social dialogue during the Economic Crisis: the impact of industrial relations reforms on collective bargaining in the manufacturing sector: Slovenia. Ljubljana: University of Ljubljana, EU Commission.

- Stanojević, M., Kanjuo Mrčela, A., and Breznik, M., 2016. Slovenia at the crossroads: increasing dependence on supranational institutions and the weakening of social dialogue. European journal of industrial relations, 22 (3), 281–94. doi: 10.1177/0959680116643205

- Stošicki, N., 2011. Pogled finančnih holdingov in upravljavcev skladov na iskanje izhoda iz krize. Bančni vestnik: revija za denarništvo in bančništvo, 60 (6), 70–8.

- Streeck, W., 2015. Heller, schmitt and the Euro. European law journal, 21 (3), 361–70. doi: 10.1111/eulj.12134

- Streeck, W., and Mertens, D., 2013. Public finance and the decline of state capacity in democratic capitalism. In: A. Schäfer, and W. Streeck, ed. Cambridge: Polity Press, 26–58.

- Taškar Beloglavec, S., and Taškar Beloglavec, B., 2014. Sanacija bank - je izvedba prve in druge sanacije vsebinsko primerljiva? Bančni vestnik: revija za denarništvo in bančništvo, 63 (9), 39–45.

- van Apeldoorn, B., 2013. The European capitalist class and the crisis of its hegemonic project. Socialist register, 2014, 189–206.

- Verdun, A., 2015. A historical institutionalist explanation of the EU's responses to the euro area financial crisis. Journal of European public policy, 22 (2), 219–37. doi: 10.1080/13501763.2014.994023

- Verdun, A., and Zeitlin, J., 2018. Introduction: the European Semester as a new architecture of EU socioeconomic governance in theory and practice. Journal of European public policy, 25 (2), 137–48. doi: 10.1080/13501763.2017.1363807

- Vičič, D. 2015. Protesti proti razprodaji bodo 7. februarja. Mladina, 4 February. Available from: http://www.mladina.si/163842/protesti-proti-razprodaji-bodo-7-februarja/.

- Vobič, I., et al., 2014. Changing faces of Slovenia: Political, socio-economic and news media aspects of the crisis. Javnost - the Public, 21 (4), 77–97. doi: 10.1080/13183222.2014.11077104

- Vukelič, M. 2013. US razveljavilo ZUJF. Dobra novica za 26.000 upokojencev. Delo, 18 March. Available from: http://www.delo.si/novice/varcevalni-ukrepi/us-razveljavilo-zujf-dobra-novica-za-26-000-upokojencev.html.

- Zajc, D., 2015. The cycle of increasing instability within the coalition government: the impact of the economic crisis in Slovenia in the period from 2008 to 2014. Teorija in praksa, 52 (1–2), 175–95.