ABSTRACT

The onset of the coronavirus pandemic in early 2020 quickly gave rise to a concern that the resulting economic uncertainty would produce a collapse in angel investing. In view of the critical role that business angels play in financing the start of the entrepreneurial pipeline, a decline in their investment activity would have a negative effect on the ability of entrepreneurs to start and commence the scaling process which, in turn, would compromise an entrepreneur-led economic recovery from the coronavirus pandemic. This paper draws on two unique data sources on investments made by business angels in Scotland before and since the onset of the pandemic. It shows that business angels continued to invest since the onset of the crisis although their investment activity declined sharply between Q2 and Q3 2020. Investment activity stabilising in Q4 and has significantly increased during 2021 and is now above pre-Covid levels. Angels have increased their emphasis on follow-on investments and in businesses that have raised one or more previous rounds of funding. This highlights a potential problem for entrepreneurs seeking to raise their first round of angel funding that policy-makers need to address.

1. Introduction

It is widely accepted that ambitious, innovative start-ups that scale will play a key role in the road to economic recovery from the crisis created by the coronavirus pandemic (ScaleUp Institute Citation2021, Citation2021; Moules Citation2021). These types of businesses are recognized as key sources of employment (especially high skilled jobs), innovation and productivity growth. As we have seen in previous recessions, the disruptions that economic crises cause to established markets create opportunities for alert entrepreneurs to launch innovative businesses based on new products, services and business models. Risk capital is a key enabler for many innovative companies both to start and to scale (ScaleUp Institute Citation2021), prompting concerns that the strength and speed of economic recovery would be put at risk if, as a consequence of the Covid crisis, there was a decline in investing by business angels and venture capital funds.

Business angels – high net worth individuals who invest on their own or with others in unquoted companies in which they have no family connection (Mason and Botelho Citation2018) – are fundamental to the entrepreneurial ecosystem, funding the start of the “entrepreneurial pipeline”. Angel investors typically follow “3 F” and grant money, funding the seed, start-up and initial growth stages, with venture capital funds making larger follow-on rounds to fund the scale-up stage (“acceleration money”) in a process that has described as being analogous to a relay race (Benjamin and Margulis Citation2000). With angels increasingly organizing themselves into managed groups with anywhere from 10 to upwards of 100 members rather than investing informally on their own or with friends and colleagues (Mason, Botelho, and Harrison Citation2016) they now have the financial resources not only to make larger initial investments but also to participate in follow-on rounds to finance the early scale-up of their investee businesses (British Business Bank Citation2020). Angel groups also have the credibility and professionalism to co-invest with both institutional and government seed and venture funds in larger syndicated deals (Mason, Botelho, and Harrison Citation2013; Mason Citation2018). Many angel investments are not publicly disclosed, particularly those made by business angels who are not part of a recognised network or syndicate. However, it is estimated that business angels account for 60% of European early-stage investment activity in terms of amount invested, and well over 90% of investments, with venture capital accounting for 34% and equity crowdfunding 6% (EBAN Citation2019). It is estimated that in the USA angels make 18 times more investments than venture capital at the early stage (ACA, Citation2021). The importance of business angels in the entrepreneurial ecosystem is further underlined by the UK’s ScaleUp Institute (Citation2021) which reported that 63% of scale-ups received investment from business angels to fund their early growth.

The implications of a decline in angel investing during the COVID pandemic have been highlighted by several key stakeholders. For example, Luigi Amati, president of Business Angels Europe, remarked that “it would have a massive impact on the start-up economy in Europe. Indeed, if angel investing breaks down, you break down the whole pipeline of development” (Sifted Citation2020a). In similar vein, Jenny Tooth, chief executive of the UK Business Angels Association (UKBAA) commented that “angels are where VCs find deals so a contraction in angel investing will create a massive hole in the ecosystem going forward” (Sifted Citation2020a). The consequence would be “a lost generation” of entrepreneurs (CityAM, Citation2020).

However, it is unclear the extent to which this scenario has occurred. The available evidence on the impact of the pandemic on angel investing is limited. There have been some surveys of business angels along with commentary and other anecdotal sources (Mason Citation2021). Moreover, much of this evidence relates to the early stages of the pandemic. Deal specific information on angel investments is limited. Whereas venture capital funds, whose investments are captured by various commercial organisations (e.g., Pitchbook, Crunchbase, Beauhurst) and by industry associations, the coverage of investments by business angels in such databases is restricted to larger, more formally organised angel groups. Moreover, the coverage of their deals is often incomplete (Mason, Botelho, and Harrison Citation2019). Hence, whereas there is considerable evidence on venture capital investing during COVID-19 (e.g., Mason Citation2020; Arundale and Mason, Citation2020; Brown, Rocha, and Cowling Citation2020; Pitchbook Citation2021) this is not the case for business angel investing.

Our objective in this paper is to provide greater clarity on how the pandemic has impacted on angel investment activity in 2020 and into 2021. We overcome the data limitations discussed above by drawing upon two unique data sources on investments made by business angels in Scotland before and since the onset of the pandemic. Scotland has a long-established business angel market, including the oldest angel group in the world (Kemp, Lironi, and Shakeshaft Citation2017), that is recognised as one of the most developed in Europe. The OECD (Citation2011) has noted that “the United Kingdom has been the most active angel market in Europe with Scotland being particularly active.” Government has played a significant role in stimulating angel investment in Scotland, notably through the creation of the Scottish Co-Investment Fund in 2003 (Harrison Citation2018) and the establishment of LINC Scotland – the national association for business angels in Scotland – whose membership comprises over twenty structured angel groups with a collective membership of at least sixteen hundred angels plus over one hundred investors who operate individually. In 2019–20 LINC members invested £103 m in 114 deals involving 87 companies (some of which completed more than one funding round in the year) (LINC Scotland Citation2020a). Emphasising the significance of business angels in financing entrepreneurial activity, venture capital funds invested just £19 m in 32 businesses in 2019 (BVCA Citation2020).

2. COVID-19 and the creation of uncertainty for business angels

Angel investing is high risk, with more than half of all investments failing and returns highly skewed (Botelho, Harrison, and Mason Citation2021; Mason and Harrison Citation2002; Wiltbank and Boeker Citation2007; Wiltbank Citation2009). Indeed, it has been suggested that portfolios with more than 50 investments are required to significantly minimize the risk of poor returns and maximize returns potential (Gregson, Bock, and Harrison Citation2017). However, most business angels have much smaller portfolios. These risks have been magnified by the economic uncertainties that have resulted from the periodic lockdowns that governments have implemented since March 2020 to control the various waves of the COVID pandemic.

The first source of uncertainty for business angels has been the potential impact of the Covid crisis on their personal wealth. The UK’s FTSE All-Share Index fell 33% between 11 January and 14 March 2002 and although some of these losses were subsequently made up it had not fully recovered by the start of 2021 (O’Neill Citation2021). The US markets (S&P, NASDAQ) also recorded steep declines in March 2020 but subsequently recovered, ending 2020 higher than at the start of the year. Given the discretionary nature of investing in new and early-stage entrepreneurial businesses (with business angels typically investing between 5 and 15% of their financial assets to this asset class) the decline in the stock market, along with the uncertainty about the impact on the pandemic on their other financial assets (e.g., property) prompted some angels to pause their investment activity. A survey by the British Business Bank (Citation2020) in the autumn of 2020 noted that the impact of the economic uncertainty on angels’ own personal investment capacity was a key reason why they reduced their investment activity.

Evidence from surveys of business angels, webinars and commentaries, mainly reflecting developments in the immediate aftermath of the initial lockdown in late March 2020, indicated that business angels continued to invest during the early stage of COVID-19 and would continue to invest. A survey by Activate our Angels (Citation2020), undertaken in the first half of May 2020 that attracted responses from over 250 UK angels reported that only one-third of UK angels were not investing during the lockdown period, with 71% of these angels continuing to review deals but adopting a “wait and see” stance and only 29% were not planning to invest at all. Almost half (48%) of the latter group said that they were only going to invest again when they felt confident that the Covid-19 crisis was over.Footnote1 However, those angels who were continuing to invest were making fewer investments, with respondents to the Activate Our Angels survey completing an average of just 1.81 deals during the early lockdown period compared with 3.24 deals in 2019. Moreover, just over half (51%) expected to invest less in 2020 than in 2019; only 19% anticipated investing more. Evidence from a British Business Bank (BBB) online survey of the UK business angel market undertaken in July 2020Footnote2 also found that angels had continued to invest but the value of both their initial and follow-on investments were lower than in the previous year. Looking forward, most respondents planned to continue to invest but anticipated that the proportion of their investable assets that they would allocate to angel investing in the remainder of 2020/21 would be slightly lower than their allocation in 2019/20. Nevertheless, most of the angels surveyed were generally confident about the future growth in value of their portfolio over the next 12 months and close to half were open to building their portfolio in the remainder of the 2020/21 fiscal year, while only 12% said they intended to make no further investments (British Business Bank Citation2020). This is consistent with evidence from Seedlegals (Citation2020), – a legal platform for investors and entrepreneurs – covering the period from late March to late July 2020, which indicated that deal activity was down slightly, having bounced back from an initial decline, but that evidence from leading indicatorsFootnote3 suggested that investor confidence appeared to be recovering. European business angels who coinvest with the European Angel Fund also decreased the total amount that they invested between February and October 2020 and reduced the size of their investments. And although there was a significant improvement in their sentiment in October it remained below that of February 2020 (Kraemer-Eis et al. Citation2021). In the USA the Angel Capital Association (ACA) reported that interest amongst angel groups in investing had remained strong, with the willingness to invest higher in September 2020 compared with April 2020 (ACA (Angel Capital Association) Citation2020).

A further source of uncertainty for angels has been the effect on the crisis on their existing investments. This has a number of dimensions. First was the risk that their investee companies would run out of finance and therefore be unable to fund their ongoing operations. Typically, investments are staged, giving businesses 12 to 18 months of cash, at which point they will raise a further funding round at a new valuation. The portfolios of business angels were therefore likely to have included some businesses whose previous funding round was more than a year ago and were therefore reaching the end of their financial runway. The coronavirus crisis worsened the cash flow position of many of these companies as a result of the deterioration in their sales revenue prospects (Greene and Rosiello Citation2020). One survey undertaken in May 2020 reported that 49% of start-ups had six months or less of runway, with the smallest companies (10 or fewer employees) – those at the start of the scaling process – in the most vulnerable category (Slush Citation2020a). A follow-up survey in October 2020 reported that the situation had worsened, with 55% of respondents indicating that they had less than six months runway (Slush Citation2020b). In another small-scale survey of mostly tech companies that had previously raised finance, 77% reported that without raising funding they would not be able to survive more than six months (EISA Citation2020). A survey of European business angels reported that 44% of their portfolio companies had been negatively impacted by Covid (Kraemer-Eis et al. Citation2021). Many business angels therefore had to decide which portfolio companies to support with follow-on funding – companies that were further along their development, particularly those that have reached the revenue generation stage, and on certain business models (particularly recurring revenue business models) and sectors (Activate our Angels Citation2020). The British Business Bank survey noted that angels had been engaging more selectively with their portfolio companies since the onset of COVID-19, primarily supporting those that needed support to achieve their growth milestones, but in some cases those that needed help to survive (British Business Bank Citation2020), as well as those offering solutions to the new opportunities created by the crisis. These considerations will likely have taken precedent over making new investments during the crisis.

A further consideration for business angels is future funding risk – the risk for those business angels who have investee businesses that plan to raise follow on finance from VCFs that this might not be possible. A related concern is the potential downward pressure on valuations, particularly at later rounds, creating the risk of down-rounds, which reduces the value of their shareholding. This raises the possibility of a re-run of the post-2000 dotcom crash in which many business angels saw their investments wiped out by the predatory behaviour of venture capitalists, driving many of them out of the market. VCFs have also been conserving their cash to support their own portfolios (Sifted Citation2020b; Arundale and Mason, Citation2020; Mason Citation2020). Business angels have therefore needed to be aware that those businesses in their portfolios that are, or will be, seeking to raise a funding round from a VCF to scale-up may not be able to do so. This is a further reason for business angels to focus on their existing portfolios. Although the fear in the early months of the pandemic that the associated economic uncertainty would result in a collapse in venture capital investing did not materialise, their investment activity has been driven by larger, later stage and follow-on deals and there has been a decline in the number of first-time investments (Beauhurst Citation2021; Robot Mascot Citation2021; Pitchbook Citation2021).

Reinforcing these concerns was the associated fear amongst business angels that there would be fewer opportunities to exit in the immediate future and companies may need to have hit more milestones than in the past in order to become an attractive acquisition by a large corporate. Seeking an exit from a position of relative weakness is likely to generate sub-optimal returns. Both situations require angels to continue to support their investee companies for longer. European business angels reported a significant deterioration in their perception of the exit environment and valuations between February and October 2020 (Kraemer-Eis et al. Citation2021).

The expectation was that business angels would respond to these sources of risk by preserving their capital in order to be in a position to support their portfolio companies rather than making new investments. This would mean fewer seed and start-up investments. Although the Activate our Angels (Citation2020) survey found that 51% of respondents were investing in new deals and only 16% were exclusively investing in their existing portfolio, much of the other evidence indicated that the majority of angels were focusing on their existing portfolios, preserving their cash to make follow-on investments rather than making new investments. This shift to follow-on investing is supported by evidence from the Plexal (Citation2020) start-up tracker of 30,000 start-ups and fast growth firms which reported a 29% decline in the number of companies raising finance for the first time compared with the same period a year earlier and a 52% decline in the amount of funding that such companies raised. US angel groups also reported an increase in the proportion of follow-on investments (ACA (Angel Capital Association) Citation2020). Follow-on investing also dominated the aftermath of the post-2000 dotcom crash and the 2008–9 global financial crisis (Mason and Harrison Citation2015; Sohl, Lien, and Chen Citation2020).

The disruptive effects of Covid on investor-entrepreneur-intermediary relationships as the investment process shifted from face-to-face to online meetings has reinforced the difficulties in making new investments. Although the shift by angel groups and other intermediaries from in-person to online pitching events has ensured that businesses angels have continued to receive deal flow, and from a wider geography, because angels are “investing on the jockey rather than the horse”Footnote4 (Harrison and Mason Citation2017) investing in entrepreneurs who they have never met in person is seen to increase risk (Mason, Botelho, and Zygmunt Citation2017). One angel remarked that “taking pitches over a zoom call doesn’t really replace that face-to-face contact. As good as the technology is, I don’t believe that it replaces face-to-face contact particularly when you’re meeting someone and building a relationship” (Dobbin Citation2021).Footnote5 A prominent UK angel commented that “angels invest in people. We have got to get to know the people … to build trust and relationship. It is a two-way relationship. It is difficult to see how this can be overcome [in the current circumstances]” (Cowley Citation2020).Footnote6 Moreover, potential investors are influenced by non-verbal expressions, notably the use of gestures and facial expressions of emotion used by entrepreneurs in their pitch. Indeed, gestures have been shown to have a more important impact than language on the funding decision of investors (Clarke, Cornelissen, and Healey Citation2019; Warnick et al. Citation2021). However, it is much harder for investors to read these visual cues in online pitches

Angels might therefore be expected to mitigate these risks by concentrating their investments in situations where there is an existing relationship,Footnote7 first, in their existing investee businesses, second, alongside other investors investing in businesses that these investors have relationships with, and third, investing in businesses where a trusted intermediary is involved (e.g., advisor). This is reflected by the following comment from an angel: “angels need people who know the entrepreneur to place their bet”.Footnote8 A further way in which they might seek to mitigate this risk is to invest in companies that have previously raised finance from other investors. There is evidence from the Activate our Angels (Citation2020) survey that some investors will now only invest alongside other investors.

Finally, there is evidence that the Covid crisis has impacted on the investment criteria of business angels, with both the Activate our Angels (Citation2020) survey and Seedlegals (Citation2020) reporting increased interest in Fintech, Remote Education and Health/Med Tech. However, the British Business Bank (Citation2020) survey reported no significant change in the dominant sectors that angels will invest in. The Covid-19 crisis has also encouraged angels to be more selective in what start-ups they will invest in, with greater emphasis on length of financial runway, revenue generation, recurring revenue business models and a strong balance sheet as investment criteria (Activate our Angels Citation2020; (Kraemer-Eis et al. Citation2021). The EIF angels survey also found that high quality entrepreneurs are an even more important consideration than previously. But only a minority of angels have shifted their focus to later stage deals (Activate our Angels Citation2020).

3. Data sources

As various commentators have noted, there are enormous definitional and data challenges in measuring business angel investment activity (Mason and Harrison Citation2008; Farrell, Howorth, and Wright Citation2008; Avdeitchikova, Landström, and Månsson Citation2008; Mason Citation2016). The available evidence is largely confined to what has been termed the “visible market” (Mason and Harrison Citation2015) comprising angel groups and syndicates, angel investment platforms and prominent individual investors (sometimes termed “super angels”). Angel investing that occurs independently of networks and groups and platforms – the “invisible” or unorganised part of the market – continues to be largely undocumented.

This paper draws on two sources of evidence which capture different but overlapping segments of the angel market. The first is the investment activity of angel groups and individual angels that are members of LINC Scotland. Its web site lists 22 angel syndicates which are members.Footnote9 This information is reported in aggregate form (LINC Scotland Citation2020b). At our request LINC Scotland provided data on investments by quarter for 2019, 2020 and 2021 (to the end of Q3). With the Scottish economy entering lockdown in late March 2020 and remaining in lockdown throughout Q2 with restrictions gradually eased in June/July (Q3) but reintroduced from October (Q4) and further strengthened in Q1 2021 before being relaxed in April 2021 (Q2) the data therefore cover all three waves of Covid and their associated lockdowns. This source has two key strengths. First, it captures those investments by LINC members that have not been publicly disclosed. Second, although its coverage is dominated by angel groups it also includes investments made by some individual angels. Its key limitations are its bias to the larger actors in the market and that is only available in aggregate form.

The second source is the investment deals that are reported by Young Company Finance (YCF) (www.ycfscotland.co.uk) a monthly publication available on subscription that tracks and reports on early-stage high growth companies in Scotland. YCF is a partner organisation of LINC Scotland. The information includes investments by institutional investors (notably venture capital funds), government funds, equity crowdfunding platforms, angel groups and some individual angels. It provides the names of both the companies that have raised finance and the institutional investors (including angel groups) but most individual investors are not identified by name. It also provides the total amount invested in the deal; however, this is not provided for every investment and in the case of syndicated deals there is no breakdown of the amounts invested by each of the individual investors. YCF identified 132 deals that occurred during 2019, 139 in 2020 and 141 in Q1-Q3 2021. Here again we disaggregate these investments by quarter. We restrict our analysis to angel-backed companies – those companies whose investors included named angel groups, named individuals (typically high-profile entrepreneurs) or are described as either “private investors” or “individual investors”. These investors have participated in 52% of the total number of deals in the YCF data base in our study period, once again demonstrating the importance of angels in financing early-stage companies.

The database also includes investments made by other types of investor. These include deals in which angels were co-investors as well as those in which angels did not participate. Venture capital funds were involved in 35% of investments (of which 45% were with angels). The other types of investors (incubators and accelerators, crowdfunding, corporate venture capital) were each involved in around 10% of investments. Government is also a significant player, involved in 46% of investments, as a co-investor, most often, but not exclusively, with angel groups.Footnote10 This underscores the strong presence that governments have in the early-stage investment equity market, particularly in peripheral regions (Mason and Pierrakis Citation2013). By cross-referencing angel-backed companies with publicly available sources (e.g., Crunchbase, Pitchbook, Companies House, media webpages) it has been possible to identify those that have raised one or more previous rounds of funding and those which have existing investors that are making follow-on investments. The advantages of YCF’s coverage are, first, that it provides deal-specific data, and second, its coverage is not restricted to investments made by LINC members. The key disadvantage is that YCF only includes publicly disclosed investments. The deals that it reports therefore do not include undisclosed investments made by LINC members or by other investors. It should be noted that it is companies, not investors, who make the decision not to disclose the investment.Footnote11 A further disadvantage is that the information provided on investors requires some subjectivity in the classification of what constitutes an angel investment.

These two data sources therefore cover overlapping but not identical segments of the market (). Of the total number of angel deals identified by YCF in our study period 63% were made by angel groups that were members of LINC. And, as with the vast majority of evidence on angel investing, the coverage of both sources is heavily skewed to the organised and hence “visible” part of the market, primarily comprising angel groups.

Figure 1. Data set coverage.

4. Results: business angel investment activity in Scotland

In the UK, the first cases of COVID were identified at the end of January. However, the initial impact of the COVID pandemic on business angel investment activity was very limited. Although the pandemic impacted on the investment sentiment of angels from March 2020 (Kraemer-Eis et al. Citation2021) investment activity by LINC members in Q1 2020 was similar to the second half of 2019. Investment activity in Q2 2020 was also buoyant, with more deals than in the equivalent period in 2019 (+6; +27.3%) and just two fewer investments than in Q1 2020 (−6.7%) (). This reflects the fact that the investment process generally takes several months to progress from the due diligence process to the decision in principle to invest and the negotiation of the terms and conditions of the investment, to writing the cheque (Mason and Harrison Citation1996). Investments in Q2 2020 therefore reflect a process that will have started in Q1 if not earlier. Moreover, many business angels will have wanted to complete deals before the end of the tax year (5th April) to quality for tax relief under the Enterprise Investment Scheme (EIS) and Seed Investment Enterprise Scheme (SEIS). It may also reflect the “triaging” of their portfolios – making small investments to support their investee companies that required immediate funding either because of the need to delay a product launch or scale up or a decline in their revenues. The impact of COVID only became apparent in Q3 2020, with a 29% decline in the number of investments (- 6 deals) between Q2 and Q3. Investment activity stabilized in Q4 with just one fewer investment than in Q3. The number of investments in Q3 and Q4 2020 was 37% below the equivalent period in 2019. But because of the high level of investment activity in Q1 and Q2, the overall the number of deals was only 6% lower 2020 than in 2019. Moving into 2021, there was a modest rise in the number of investments in Q1 despite a second wave of covid cases and associated lockdown. Angel investment activity accelerated in Q2 and Q3, as the vaccination programme gained momentum, driving economic recovery, with the number of investments in Q3 up by 40% (+8) on the Q1 level.

Figure 2. Investment activity by LINC members: 2019 compared with 2020.

The amount invested exhibits a rather different trend which can be attributed, at least in part, to outliers – small numbers of large investments in specific time-periods. The amount invested declined sharply between Q1 and Q2 2020 (although the amount invested in Q1 2020 was unusually high and the amount invested in Q2 2020 was only slightly less than in Q2, 2019), but exhibited modest increases in Q3 2020 and again in Q4, although remained lower than in the same period in 2019. After a further modest increase in Q1, 2021 there was a huge increase in angel investment in Q2 (up 144% from Q1 and 277% higher than in Q2 2020) falling back slightly in Q3 (with amount invested 170% higher than in Q3 2020) (). Indeed, the amount invested in 2021 is on track to surpass the record annual total set in 2019 (Scottish Business Insider Citation2021).

YCF data also indicates that angel activity was buoyant in the first half of 2020, with the number of investments significantly higher in both Q1 and Q2 2020 than in the equivalent period in 2019, and with the number of investments increasing between Q1 and Q2 2020 (). Investment activity dropped sharply in Q3 2020 but made a small recovery in Q4 2020. It also shows that total angel investment was lower in Q3 (−28%) and Q4 (−12%) of 2020 than in the equivalent periods in 2019. Following a slight fall in investments in Q1, 2021, angel investment surged in Q2 and Q3 2021, with the total number of investments in the year to date (72) exceeding the total in 2019 (60).

Table 1. YCF evidence on business angel investments pre and during Covid

In summary, both LINC Scotland and YCF data show that covid had only a short-term impact on angel investment activity in Scotland. Investment activity was buoyant in Q1 2020 and remained at a high level of activity in Q2, but declined sharply in Q3, consistent with the survey evidence on angel sentiment that was reported in the early months of the pandemic. Investment activity stabilising and even exhibited some signs of a modest bounce-back in Q4 and in Q1 2021 and then rapidly accelerated in Q2 and Q3 2021. So, based on this evidence, the concerns that were voiced in the early months of the pandemic that there would be a collapse in angel investing, with adverse implications for entrepreneurial activity, have not materialised. Indeed, investment activity in Q2 and Q3 2021 is at record levels.

The recovery in angel investing from Q4 2020 and into 2021 reflects several factors. First is the increased confidence of angels as the covid vaccine roll-out programme started, driving economic recovery, and as they became more familiar with the new business environment. This will also have prompted business angels who had stopped investing to return to the market. Second, is the return to the market of entrepreneurs who had deferred seeking funding in the early months of the pandemic because uncertainty about their revenue prosects meant that they could not present a convincing case for investment. Third, angels have had the opportunity to see more deals as investment pitching moved online and had more time on their hands on account of restrictions on travel and social activity to be able to review investment proposals. Both angels and angel groups had also learned how to do pitching and due diligence online and become more accustomed to the digital environment for connecting with people and more comfortable in investing in entrepreneurs that they had never met. Fourth, attractive investment opportunities have emerged during the pandemic as entrepreneurs have developed innovate solutions to the problems that the covid-induced disruption has created, notably in digital health/healthcare, biotech/life science, software as service, fintech, fulfilment providers, education tech, and AI sectors. And there has also been a growth in interest amongst many business angels in “green” investment opportunities as climate change has become central in the media, politics, economy and society.

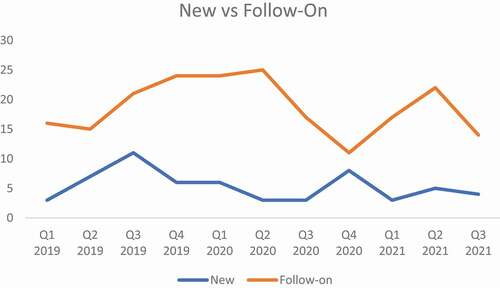

What these aggregate investment trends mask is that following the onset of the pandemic angels have increasingly focused their investment activity on making follow-on investments and scaled back new investment activity (). As noted earlier, a similar shift occurred in the aftermath of global financial crisis. The proportion of follow-on investments increased sharply in Q2 2020 (increase of 22 percentage points) and Q3 (increase of 20 percentage points) as angels focused on the need to support the companies in their portfolio. The drop-off in deal flow will have amplified this trend. New investments bounced back strongly in Q4 2020, with follow-on investments falling to 60% of all investments, but dropped back in 2021. Follow-on investments as a proportion of the total amount invested increased in Q2 and Q3 of 2020 compared with 2019, with a particularly large increase in Q3 from 79% to 99%. With the rebound in new investments in Q4 2020 follow-on investments dropped to just 54% of the amount invested but increased to 73% in Q1 2021 and over 90% in Q2 and Q3. This shift to follow-on investing is also identified in the YCF data (). It identifies an increase in the share of total investments accounted for by follow-on investments from Q1 2020 through to Q3 2020, with a particularly sharp increase between Q2 and Q3, followed by a drop in Q4 as new investments increased. This trend was reversed in 2021, with follow-on investments accounting for 84% of the amount invested in Q3 and 94% in Q3.

Table 2. Follow-on investments involving business angels: 2019 and 2020 by quarter

Figure 3. New and follow-on investments.

Deals involving angel groups are typically “bundled” (Mason Citation2018), with both angel groups and “super angels” investing alongside one or more other investors, including government venture capital funds, private venture capital funds and, less often, crowdfunding, incubators and accelerators and corporates (). Of particular note is the significant rise in the proportion of angel deals involving venture capital funds in Q2 and Q3 2021.

Table 3. Percentage of co-invested deals with angels

Typically, there are three investors in deals in which angels participate (). However, the number of co-investors dropped sharply in Q1 and Q2 2020 compared with 2019 before recovering in Q3 and Q4. It seems reasonable to infer that this decline in co-investors will have been a further reason why angels increased the proportion of the amount that they invested in follow-on investments in the early stages of the pandemic. There has been a significant increase during 2021 – particularly in Q2 and Q3 – in the number of investors in deals in which angels participated, reflecting the increase in size of deals. Disaggregating between new and follow-on reveals – not surprisingly – that follow-on deals have more co-investors than new investments, reflecting their larger deal size. The average number of investors in new investments increased in 2020 (+4%) then dropped in Q1 and Q2 2021 before rising sharply in Q3. In contrast, the number of investors in follow-on deals declined in 2020 (12%) and but has also increased significantly in 2021 (). The increase in the number of investors in new angel deals in Q2, Q3 and Q4 of 2020 is of particular note and consistent with a strategy of reducing the risk of investing in an entrepreneur that they have not met in person by investing alongside other investors who have connections with entrepreneur. Investing alongside other investors also minimises risk because it reduces the amount that any individual investor invests in the deal.

Table 4. Average number of investors in deals in which business angels participated

The public sector is the dominant co-investment partner of business angels (). The Scottish Government’s Scottish Investment Bank (SIB) has three funds: the Scottish Seed Fund, Scottish Venture Fund (SVF) and the Scottish Co-Investment fund (SCIF). Both the SVF and the SCIF invest with private sector partners. The SCIF invests alongside its accredited co-investment partners in qualifying deals.Footnote12 These include both business angel groups and venture capital funds.Footnote13 About 40% of LINC’s member groups – the larger and longer established groups – are co-investment partners. These groups account for over half of the partners of the SCIF. In 2019 the public sector invested £1 for every £3.4 invested by LINC members, increasing to £1 for every £2.9 invested by LINC members in 2020 but dropped back sharply in 2021 to £1 for every £5.5 of private investment in a context of sharply rising private investment.

Table 5. Angel investments involving the Scottish Co-Investment Fund

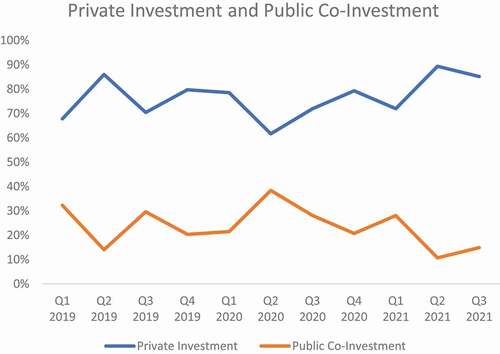

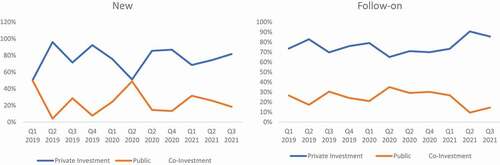

Given the co-investment model it not surprising that public sector investment tracks trends angel investment (). However, there are some deviations. Public sector investment recorded a much smaller decline in the amount investment from Q1 to Q2 2020 than business angels groups (−15% cf. −63%) but it continued to decline in both Q3 and Q4 2020 as angel groups increased the amount that they invested (although not the number of investments). Hence, public sector funds peaked at 38% of the total amount invested in Q2, falling back to 21% by Q4 (). With the recovery in angel investing in 2021 the public sector’s share of total investment fell back, accounting for 11% in Q2 2021 and 15% in Q3. The public sector therefore played an important role in maintaining liquidity in the market in the early stage of the pandemic. The public sector also tracked the increased focus of angel groups on follow-on investments, with the proportion invested in new deals falling from Q1 through Q3 2020 (reaching to its minimum in Q3, accounting for just 4% of total public sector investment, compared with 9% amongst angels) before recovering in Q4 (). Moreover, further highlighting the importance the public sector in supporting the liquidity of the market in the early stage of the pandemic, they allocated 31% of their funds to new investments in Q2 compared with 20% by angels.

Figure 4. Amounts invested by LINC members and public sector co-investment funds.

Figure 5. Amounts invested in new and follow-on investments: LINC members and public sector co-investment venture funds.

YCF data – which covers a wider range of investors who are not co-investment fund partners – confirms that there was an increase in the number of angel deals that include Scottish Government participation between Q1 and Q2 2020 (+4, +36%) followed by a sharp decline in Q3 (−9, −60%) recovering in Q4. This is consistent with the decline in angel investments in Q3 and its recovery in Q4, reflecting that the SCIF invests alongside its private sector investment partners and the Venture Fund also co-invests with private investors. Both the number and proportion of angel investments involving the SCIF has risen in 2021, although the proportion remains below the 2019 figure ().

Lastly, an additional way in which business angels are able to reduce risk is to invest in businesses that have been able to raise an earlier round of external finance. Angels would see this a positive signal of the quality of the business. The proportion of investments made by business angels in businesses that had raised an earlier round of finance was higher in all quarters of 2020 compared with 2019 (year-on-year increase of 14 percentage points), with a particularly marked increase between Q2 and Q3 2020, with increase continuing in 2021 ().

Table 6. Angel investments in deals that have raised earlier rounds of finance

5. Conclusion

Business angels are critical players in the entrepreneurial ecosystem, funding companies at their seed, start-up and early scale-up stages. A decline in investing by business angels would therefore put at risk the speed and strength of the economic recovery from the coronavirus crisis. In contrast to the institutional venture capital industry, there is a lack of clarity on business angel investment activity since the onset of the coronavirus crisis, being limited to anecdotal evidence and investor surveys undertaken in the early stage of the crisis. Focusing on Scotland, which has a long-established and, in relative terms, large angel market, this paper utilises data on investments made during 2019, 2020 and 2021 to offer a more robust picture of the impact of the coronavirus crisis on angel investment activity, albeit one that is inevitably biased on account of the nature of angel investing to the visible segment of the market.

Drawing upon two sources of data on investments made by business angels in Scotland it is clear that the adverse impact of the covid pandemic has been short-lived. Business angels continued to invest following the onset of coronavirus. Indeed, after a very active first quarter investment activity remained quite buoyant in the second quarter of 2020. However, there was a significant decline in the number of investments in Q3 although the amount invested actually increased. Investment activity stabilised in Q4 and Q1 2021 and then rose sharply in Q2 and Q3 2021. Looking at 2020 as a whole, investment activity was slightly lower compared with 2019 (−6% of deals and −17% in the amount invested). Investment in 2021 has risen sharply and is expected to surpass pre-covid levels. But the pandemic did result in angels focusing their investment activity on supporting their existing portfolios, and on businesses that have already raised at least one round of finance. New investments have declined as a proportion of total investments apart from a brief and short-lived jump in Q4 2020. And although there was a slight decline in number of co-investors in the deals in which angels participated in 2020 this figure has risen sharply in 2021, largely driven by a rise in the proportion of angel investments in deals in which VCFs have also participated. These trends, especially when taken in conjunction with the decline in seed investing by venture capital funds (Beauhurst Citation2021), point to potential problem for entrepreneurs seeking to raise their first round of angel funding. Comparative statistical evidence from other countries is limited. However, angel investment activity on the Island or Ireland is consistent with Scottish trends.Footnote14

These investment trends exhibit a remarkable similarity to how both the Scottish and UK angel markets reacted in the aftermath of the Global Financial Crisis (GFC), with angel investment exhibiting considerable stability in terms of both the number of investments and the amount invested and a marked shift to follow-on investments (Mason and Harrison Citation2015). But whereas the recovery in investment activity from the GFC took around two years, it has been much quicker on this occasion, as suggested by the evidence reported earlier on angel sentiment, reflecting positive economic growth forecasts as the vaccine programme has been rolled out (Financial Times Citation2021).

A further contribution of the paper is to highlight the shortcomings of investment data on angel investing which have typically been glossed over in prior quantitative studies. The first arises from how business angels are defined. As a membership organisation LINC Scotland data only include investments made by its members, predominantly angel groups. The YCF data provides deal-specific information (company and, in most cases, investor names) and so gives researchers some discretion regarding how angels are defined but at the same time introduces subjectivity concerning what is defined as an angel investment. The ongoing evolution of angel investing with, for example, the emergence of angel side-car funds, the transitions of angel group membership from active to passive members and the evolution of informal angel groups into formal seed funds, brings further fuzziness to the definition of what is an angel investment to those already highlighted in the literature (Mason, Botelho, and Harrison Citation2019). The second limitation relates to the coverage of investment activity, with both sources heavily skewed to the “visible” market comprising investments made by angel groups and prominent individual investors and in the case of the YCF data to deals that are publicly disclosed by investee companies. It therefore does not necessarily reflect how small-scale solo angels have responded to the covid pandemic. In summary, the availability of seemingly objective data on angel investments does not provide comprehensive coverage of angel investments even in the visible market nor does it solve the definitional difficulties.

Our analysis has implications for policy makers in Scotland and potentially elsewhere. The anecdotal evidence that emerged in the early months of the pandemic suggesting a decline in angel investing (Mason Citation2021) prompted calls to introduce new tax breaks for business angels or to enhance the generosity of the tax-breaks available in existing schemes. However, the evidence presented here – which indicates that angel investing did not collapse, the decline was short-term and that recovery has been strong – suggests that this would have been unnecessary. Nevertheless, there is scope for modifying some of the rules, notably the restriction to invest in ordinary shares and the “closely connected” exclusion to permit angels who work with the company prior to investing (e.g., as founding angels: Festel and De Cleyn Citation2013) to qualify for tax breaks. Our evidence that business angels are concentrating their investments on follow-on investments to support their existing portfolio companies and in larger syndicated deals, along with evidence of a decline in seed investing by venture capital funds and an increase in the size of such investments, also highlights the need for policy-makers to intervene to fill the emerging gap in first round (pre-Series A) funding, notably by expanding sources of non-dilutive funding such as grants and awards, and increasing the volume of seed and start-up investments by government investment vehicles. The evidence also highlights the important role that public sector co-investment funds played in maintaining liquidity in the market particularly in the early months of the pandemic (Q2 and Q3 2020). But because public sector funds are largely based on co-investment models this has meant that their investments have also become dominated by follow-on investments. A challenge for Governments is therefore to ensure that the investments made by these vehicles do not automatically “drift” to making larger and follow-on investments in line with the investments of their partners. In parallel with these interventions, the emphasis that angels place on knowing the entrepreneur before investing requires angel networks and platforms to work more closely with the entrepreneurs that they promote to their investors in order to give them confidence that they know the entrepreneurs and their businesses well. But this imposes increased costs on these organisations which will be passed on to their investors (Rees-Mogg Citation2021). Government should therefore consider supporting the operating costs of angel intermediary organisations. Without further interventions there is a real risk that entrepreneurs will be delayed in getting their innovations to market.

Finally, the study emphasises the need for the business angel research agenda to be informed by developments in the real world. Further research is still required to fully understand and measure the longer-term impacts of covid-19 on the angel market. Specifically, what is ongoing balance between new and follow-on investments? And in view of the widely expressed concerns about the adverse impact of the pandemic on the financing of women entrepreneurs (Barber Citation2020; Wilhelm, and Mascarenhas Citation2020) there is a need to examine the gender breakdown of angel investments. Additionally, given the uneven geographical distribution of angels (which in the UK is concentrated in the so-called “Golden Triangle” of London, Oxford and Cambridge: British Business Bank Citation2020) to what extent has the recovery in angel investment activity occurred equally across all regions? Second, there is a need to identify any changes in the investment process. Specifically, do angels still require to meet entrepreneurs face-to-face before investing or are they now comfortable making use of remote methods to undertake their investment appraisals? In which case, how might this influence the deals that they reject and those that they invest in? And to what extent will the changes that they have made to their investment criteria in response to the uncertainty created by the pandemic be maintained? Are business angels increasing their dependence on other investors both in terms of sourcing deals and to co-invest with? Additionally, have their co-investment preferences have changed? For example, are angels now more likely to invest alongside VCs, as appears to be the case, and with crowdfunding investors. And finally, will the shift to online investing be maintained? Evidence from Canadian angel groups indicates that some angels disengaged because they were not interested in investing if they could not meet the entrepreneurs in person and the initial enthusiasm of other angels to shift to online investing has waned over time as zoom-fatigue set in (NACO Citation2021). These considerations have prompted some groups to return to in-person events (Dorset Business Angels Citation2021) and others are now adopting a mixed approach. If angel groups and platforms continue with virtual rather than in-person pitches to what extent will this result in a weakening in the localised nature of angel investing (Harrison, Mason, and Robson Citation2010)? And, if so, will this be to the detriment of smaller, peripheral and economically lagging regions which, on account of their lower levels of entrepreneurial activity, have smaller pools of investment opportunities?

Acknowledgments

We are most grateful to David Grahame, OBE, Chief Executive of LINC Scotland and Jonathan Harris, publisher of Young Company Finance for making their data available to us.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1. Some of those that have dropped out of the market have been disparagingly described as “tourists”: “the classic ‘rich individual’ who sometimes dabbles in investing in tech start-ups” (Sifted Citation2020a).

2. Undertaken in conjunction with the UK Business Angels Association. The survey collected responses between 15th July and the 2nd and August 2020.

3. SEIS and EIS Advanced Assurance applications, shareholder agreement signatures and term sheet signatures.

4. One angel commented at the NACO West webinar on “The Future of Early-Stage Capital” (31 March 2021) that “as an angel investor my only criteria is the founder.”

5. Mark Dobbin is the founder and President of Killick Capital Inc., a Newfoundland based investment firm to invest in the aerospace sector and in Newfoundland and Labrador companies. He was an early angel investor in St. John’s-based Verafin, a FinTech giant in the anti-financial crime management space that was acquired by Nasdaq in November for $2.75 billion in cash. Dobbin was NACO’s angel of the year in 2020.

6. Peter Cowley is as an active angel investor based in Cambridge, UK. He has invested in more than 75 start-ups. He has been Chair of the board of the Cambridge Business Angels. He was President of the European Business Angels Network (EBAN) – the trade body representing the early-stage investor and start up community throughout Europe. (https://www.petercowley.org/).

7. Peter Cowley’s approach is as follows. “Unless I have known the entrepreneurial team for several years (i.e., I have been on a start-up journey with them already), I am no longer investing in start-ups. However, I am continuing to support my portfolio with time and investment.” (https://www.petercowley.org/).

8. Comment made at the NACO West webinar on “The Future of Early-Stage Capital” (31 March 2021).

9. LINC Scotland also has additional members that are not publicly disclosed (individual investors, angel groups, private offices and other investment organisation).

10. For more information about activity levels of other sources of finance see Appendix A.

11. Jonathan Harris, publisher of Young Company Finance.

12. Eligibility criteria include the following: significant presence in Scotland, meeting the EU SME definition, a deal size of between £20,000 and £10,000 (of which the SCIF will invest between £10,000 and £1.5m) and not operating in specific excluded sectors.

14. HBAN (Halo Business Angel Network), the all-Ireland organisation responsible for the promotion of business angel investment reported that its members invested €59m in 59 deals in 2020, only marginally down on 2019 (€16.8m in 66 deals) and significantly higher than in 2018 (€9.3m in 44 deals) (HBAN Citation2021a). The first half (H1) of 2021 a total of €8.38M in angel funding was invested in start-ups on the Island of Ireland – up 13.5% on H1 2019. The number of start-ups that received funding also increased from 29 to 37 (HBAN Citation2021b).

15. Note: It sums up more than 100% as some deals can have more than one type of investor (co-investment).

References

- ACA (Angel Capital Association). 2020. Angel Funders Report 2020. https://www.paperturn-view.com/angel-capital-association/angel-funders-report-2020?pid=MTI120986&v=3.2

- ACA (Angel Capital Association). 2021. Demystifying Angel Investing: An Introduction to the World of Early-Stage. Overland Park: Webinar. 17 February. https://files.constantcontact.com/eb22d7af701/a0518154-fc35-49b9-95a6-ad3ef1f86cc4.pdf

- Activate our Angels. 2020. Angels are investing during Lockdown, but it’s not all good news. https://www.activateourangels.com/results

- Arundale, K, and C. Mason. 2020. “Private Equity and Venture Capital - Riding the COVID-19 Crisis.” In A New World Post COVID-19: Lessons For Business, The Finance Industry And Policy Makers, edited by S Varotto. Venice: Ca’ Foscari University Press.

- Avdeitchikova, S, H Landström, and N Månsson. 2008. “What Do We Mean When We Talk about Business Angels? Some Reflections on Definitions and Sampling.” Venture Capital: An International Journal of Entrepreneurial Finance 10 (4): 371–394. doi:https://doi.org/10.1080/13691060802351214.

- Barber, L. (2020). The pandemic has hit female entrepreneurs hard, Wired, 8 October.

- Beauhurst. 2021. UK Equity Investment Market Update: Q3 2020. https://www.beauhurst.com/research/equity-investment-market-update/#:~:text=The%20key%20findings%20from%20Q3,1%25%20drop%20from%20Q3%202019.&text=Just%2087%20companies%20announced%20their,record%2C%20with%2060%20deals%20completed

- Benjamin, G. A., and J. B. Margulis. 2000. Angel Financing: How to Find and Invest in Private Equity. New York: Wiley.

- Botelho, T., R. Harrison, and C. Mason. 2021. “Business Angel Exits: A Theory of Planned Behaviour Perspective.” Small Business Economics 57: 1–20.

- British Business Bank. 2020. “The UK Business Angel Market 2020.” British Business Bank in Association with UK Business Angel Network. https://ukbaa.org.uk/wp-content/uploads/2020/10/20201008-BBB-Business-Angels-Report-Final.pdf

- Brown, R, A Rocha, and M Cowling. 2020. “Financing Entrepreneurship in Times of Crisis: Exploring the Impact of COVID-19 on the Market for Entrepreneurial Finance in the United Kingdom.” International Small Business Journal 38 (5): 380–390. doi:https://doi.org/10.1177/0266242620937464.

- BVCA. 2020. BVCA Report on Investment Activity 2019. London: British Venture Capital Association. https://www.bvca.co.uk/Portals/0/Documents/Research/Industry%20Activity/BVCA-RIA-2019.pdf

- City, AM. 2020. “A Lost Generation of Startups: Are Early-stage Companies Being Left Behind?” 15th October, https://www.cityam.com/a-lost-generation-of-startups-are-early-stage-companies-being-left-behind/?utm_source=newsletter&utm_medium=email&utm_campaign=2020+Five+at+5

- Clarke, J S, J P Cornelissen, and M P. Healey. 2019. “Actions Speak Louder than Words: How Figurative Language and Gesturing in Entrepreneurial Pitches Influences Investment Judgments.” Academy of Management Journal 62 (2): 335–360. doi:https://doi.org/10.5465/amj.2016.1008.

- Cowley, P. 2020. “Panelist at a Barclays Eagle Lab Webinar on Raising Angel Investment in the Current Landscape.” 25 June. https://labs.uk.barclays/support/continuity/understanding-the-angel-investment-landscape

- Dobbin, M. 2021. “East Coast Angel Investors Building Relationships via Virtual Pitches.” The Telegram, 25 February. https://www.thetelegram.com/business/local-business/east-coast-angel-investors-building-relationships-via-virtual-pitches-557490/

- Dorset Business Angels. 2021. “The Importance of Face-to-face Events.” 17 September. https://dorsetbusinessangels.co.uk/news/the-importance-of-face-to-face-pitch-events

- EBAN. 2019. European Early Stage Market Statistics 2018. Brussels: European Business Angel Network. https://www.eban.org/wp-content/uploads/2020/06/Statistics-Compendium-2018-FINAL-NEW.pdf

- EISA. 2020. Industry Survey Indicates 9 Out of 10 Growth Businesses Needing Investment Now May Disappear within 12 Months if Government Fails to Act. London: EIS Association. https://pressroom.journolink.com/eisa/release/industry_survey_indicates_9_out_of_10_growth_businesses_needing_investment_now_may_disappear_within__6497

- Farrell, E, C Howorth, and M Wright. 2008. “A Review of Sampling and Definitional Issues in Informal Venture Capital Research.” Venture Capital: An International Journal of Entrepreneurial Finance 10 (4): 331–353. doi:https://doi.org/10.1080/13691060802151986.

- Festel, G W, and S H De Cleyn. 2013. “Founding Angels as an Emerging Subtype of the Angel Investment Model in High-tech Businesses.” Venture Capital: An International Journal of Entrepreneurial Finance 15 (3): 261–282. doi:https://doi.org/10.1080/13691066.2013.807059.

- Financial Times. (2021). UK turns corner on vaccine rollout, 18 January.

- Greene, F J, and A Rosiello. 2020. “A Commentary on the Impacts of ‘Great Lockdown’ and Its Aftermath on Scaling Firms: What are the Implications for Entrepreneurial Research?” International Small Business Journal 38 (7): 583–592. doi:https://doi.org/10.1177/0266242620961912.

- Gregson, G., A. J. Bock, and R. T. Harrison. 2017. “A Review and Simulation of Business Angel Investment Returns.” Venture Capital 19 (4): 285–311. doi:https://doi.org/10.1080/13691066.2017.1332546.

- Harrison, R., C. Mason, and P. Robson. 2010. “Determinants of Long-distance Investing by Business Angels in the UK.” Entrepreneurship and Regional Development 22 (2): 113–137. doi:https://doi.org/10.1080/08985620802545928.

- Harrison, R. 2018. “Crossing the Chasm: The Role of Co-investment Funds in Strengthening the Regional Business Angel Ecosystem.” Small Enterprise Research 25 (1): 3–22. doi:https://doi.org/10.1080/13215906.2018.1428910.

- Harrison, R, and C Mason. 2017. “Backing the Horse or the Jockey? Due Diligence, Agency Costs, Information and the Evaluation of Risk by Business Angel Investors.” International Review of Entrepreneurship 15 (3): 269–290.

- HBAN. 2021a. “HBAN Angels Invested €14m in 2020, despite the Pandemic Turbulence.” https://www.hban.org/learning-centre/news/hban-angels-invested-%E2%82%AC14m-in-2020-despite-the-pandemic-turbulence

- HBAN. 2021b. “HBAN Angel Investments Exceed Pre-pandemic Levels.” https://www.hban.org/learning-centre/news/hban-angel-investments-exceed-pre-pandemic-levels

- Kemp, K, G Lironi, and P Shakeshaft. 2017. The Archangels’ Share: The Story of the World’s First Syndicate of Business. Salford, UK: Angels, Saraband.

- Kraemer-Eis, H, A Botsari, K Kiefer, and F Lang. 2021. “EIF Venture Capital, Private Equity Mid-Market and Business Angels Survey. Market Sentiment – Covid 19 – Policy Measures.” EIF Research and Market Analysis. Working Paper 2021/71 https://www.eif.org/news_centre/publications/eif_working_paper_2021_71.pdf

- LINC Scotland. 2020a. “Business Angel Investment Reaches New Heights.” 6 May. https://lincscot.co.uk/business-angel-investment-reaches-new-heights/

- LINC Scotland. 2020b. Another Strong Quarter from Business Angel Syndicates. July 9. Glasgow, Scotland: LINC Scotland.

- Mascot, Robot. 2021. “2020 European Investment Report.” https://www.robotmascot.co.uk/free-resources/2020-european-investment-report/

- Mason, C M, and R T Harrison. 1996. “Informal Venture Capital: A Study of the Investment Process and Post-investment Experience.” Entrepreneurship and Regional Development 9 (2): 105–126. doi:https://doi.org/10.1080/08985629600000007.

- Mason, C M, and R T Harrison. 2002. “Is It Worth It? Rates of Return from Informal Venture Capital Investment.” Journal of Business Venturing 17 (3): 211–236. doi:https://doi.org/10.1016/S0883-9026(00)00060-4.

- Mason, C M, and R T Harrison. 2008. “Measuring Business Angel Investment Activity in the United Kingdom: A Review of Potential Data Sources.” Venture Capital: An International Journal of Entrepreneurial Finance 10 (4): 309–330. doi:https://doi.org/10.1080/13691060802380098.

- Mason, C M, and R T Harrison. 2015. “Business Angel Investment Activity in the Financial Crisis: UK Evidence and Policy Implications.” Environment and Planning C; Government and Policy 33 (1): 43–60. doi:https://doi.org/10.1068/c12324b.

- Mason, C M, T Botelho, and R Harrison. 2013. The Transformation of the Business Angel Market: Evidence from Scotland. Adam Smith Business School, University of Glasgow and Queen's University Belfast. SSRN 2306653.

- Mason, C. 2020. The Coronavirus Economic Crisis: Its Impact on Venture Capital and High Growth Enterprises. Luxembourg: Publications Office of the European Union. JRC120612.63 https://ec.europa.eu/jrc/en/publication/coronavirus-economic-crisis-its-impact-venture-capital-and-high-growth-enterprises

- Mason, C. 2016. “Researching Business Angels: Definitional and Data Challenges.” In Handbook on Research on Venture Capital. edited by, H Landström and C Mason, 25–52. Edward Elgar: Cheltenham. Business Angels. https://lincscot.co.uk/another-strong-quarter-from-business-angel-syndicates/3

- Mason, C. 2021. “Financing an Entrepreneur-led Economic Recovery: The Impact of the Coronavirus on Business Angel Investing.” In Productivity and the Pandemic, edited by P McCann, and T Vorley, 73–87, Cheltenham, UK: Edward Elgar.

- Mason, C. 2018. “Financing Entrepreneurial Ventures.” In The Sage Handbook of Small Business and Entrepreneurship, edited by R. Blackburn, D. de Clercq, and J. Heinonen, 321–349, London: SAGE.

- Mason, C, T Botelho, and J Zygmunt. 2017. “Why Business Angels Reject Investment Opportunities: It Is Personal?” International Small Business Journal 35 (5): 519–534. doi:https://doi.org/10.1177/0266242616646622.

- Mason, C, and T Botelho. 2018. “Early Sources of Funding (2): Business Angels.” In Entrepreneurial Finance: The Art And Science Of Growing Ventures, edited by L Alemany, and J Andreoli, 60–96, Cambridge, UK: Cambridge University Press.

- Mason, C, T Botelho, and R Harrison. 2016. “The Transformation of the Business Angel Market: Evidence and Research Implications.” Venture Capital: An International Journal of Entrepreneurial Finance 18 (4): 321–344. doi:https://doi.org/10.1080/13691066.2016.1229470.

- Mason, C, T Botelho, and R Harrison. 2019. “The Changing Nature of Angel Investing: Some Research Implications.” Venture Capital: An International Journal of Entrepreneurial Finance 21 (2–3): 177–194. doi:https://doi.org/10.1080/13691066.2019.1612921.

- Mason, C, and Y Pierrakis. 2013. “Venture Capital, the Regions and Public Policy: The United Kingdom since the Post-2000 Technology Crash.” Regional Studies 47 (5): 1156–1171. doi:https://doi.org/10.1080/00343404.2011.588203.

- Moules, J. 2021. “How ‘Scale-up’ Business Became the Engine of Job Creation.” Financial Times, February 11. https://www.ft.com/content/fee31b91-e023-48a2-ba3a-137fe56cce5b

- NACO. 2021. “The Changing Landscape: 2021 Annual Report on Angel Investment in Canada.” Toronto: National Angel Capital Organisation. https://digital.builtbyangels.com/link/228783/

- O’Neill, M. 2021. “Protecting Your Money from Covid-23.” Financial Times: FT Money, 27 February. https://www.ft.com/content/9e87b151-6c76-4719-9dcc-b722522fe252

- OECD. 2011. Financing High-Growth Firms: The Role of Angel Investors. Paris: OECD.

- Pitchbook. 2021. “European Venture Report: 2020 Annual Report.” https://files.pitchbook.com/website/files/pdf/2020_Annual_European_Venture_Report.pdf

- Plexal. 2020. “A Record Number of Startups Close Shop as the Impact of Government Schemes Wanes: Latest Data from Plexal and Beauhurst.” https://www.plexal.com/a-record-number-of-startups-close-shop-as-the-impact-of-government-schemes-wanes-latest-data-from-plexal-and-beauhurst/

- Rees-Mogg, M. 2021. “Only Connect – What We are Learning from Covid Times?” Angel News, Accessed March 23 2021. https://www.angelnews.co.uk/blog/perspectives/only-connect-what-we-are-learning-from-covid-times/

- ScaleUp Institute. 2021. “ScaleUp Annual Review 2021.” https://www.scaleupinstitute.org.uk/scaleup-review-2020/introduction/

- Scottish Business Insider.(2021). Scottish angel investment set for a record year, 16 September.

- Seedlegals. 2020. “SeedLegals Data Reveals CoVid-19 Effect on UK Startup Funding Rounds – August 2020 Update.” 4 August. https://seedlegals.com/resources/seedlegals-data-reveals-covid19-effect-on-uk-startup-funding-rounds/

- Sifted. 2020a. “What’s Happened to the Angels?” 21 May. https://sifted.eu/articles/angel-investing-startups-europe-covid/

- Sifted. 2020b. “Funding for Seed-stage UK Startups Drops over 80%.” Accessed May 21 2020. https://sifted.eu/articles/first-time-founders-funding/

- Slush. 2020a. “COVID-19 Report: Gauging How The Ecosystem Is Coping With The Pandemic.” Helsinki: Slush. https://s3-eu-north-1.amazonaws.com/evermade-slush-org-2019/wp-content/uploads/2020/05/14103329/Slushs-COVID-19-survey-results.pdf

- Slush. 2020b. Quarantined Growth Founders’ Perspectives on the Covid-19 Crisis and a Helsinki Startup Ecosystem Deep Dive. Helsinki: Slush. https://s3-eu-north-1.amazonaws.com/evermade-slush-org-2019/wp-content/uploads/2020/12/01121035/Helsinki-Slush-Quarantined-Growth-4.pdf

- Sohl, J, W-C Lien, and J Chen. 2020. The Angel Market and COVID-19: Building Bridges or Piers? Durham, NH: University of New Hampshire, Centre for Venture Research.

- Warnick, B J, B C Davis, T H Allison, and A H Anglin. 2021. “Express Yourself: Facial Expression of Happiness, Anger, Fear, and Sadness in Funding Pitches.” Journal of Business Venturing 36 (4): 106109. doi:https://doi.org/10.1016/j.jbusvent.2021.106109.

- Wilhlm, A, and Mascarnhas, N. (2020). Pandemic's impact dirproportionately reduced VC funding for female founders, Tech Crunch, 2 November.

- Wiltbank, R., and W Boeker. 2007. Returns to Angel Investors in Groups. Kansas City: Kauffman Foundation.

- Wiltbank, R. 2009. Siding with the Angels: Business Angel Investing – Promising Outcomes and Effective Strategies. May. London: NESTA/British Business Angels Association.

Appendix AFootnote15

Percentage of deals by source of entrepreneurial finance reported by Young Company Finance