Abstract

Objective: To provide updated evidence on US trends in: market exclusivity periods (MEPs, time between brand-name drug launch and first generic competitors) for new molecular entities (NMEs); likelihood, timing and number of Hatch-Waxman Act Paragraph IV patent challenges; and generic drug penetration.

Methods: This study used IMS Health National Sales PerspectivesTM US data to calculate MEPs for the 288 NMEs experiencing initial generic entry between January 1995 and December 2014, the number of generic competitors for 12 months afterward (by level of annual sales prior to generic entry), and generic penetration rates. The likelihood, timing and number of Paragraph IV challengers were calculated using data from Abbreviated New Drug Approval (ANDA) letters, the FDA website, public information searches, and ParagraphFour.com.

Results: For drugs experiencing initial generic entry in 2013–2014, the MEP was 12.5 years for drugs with sales greater than $250 million (in 2008 dollars) in the year prior to generic entry ($250 million + NMEs), 13.6 years overall. After generic entry, brands rapidly lost sales, with their average unit share being 7% at 1 year for $250 million + NMEs, 12% overall. Ninety-four percent of $250 million + NMEs experiencing initial generic entry in 2013–2014 had faced at least one Paragraph IV challenge, an average of 5.2 years after brand launch (76% and 5.9 years for all NMEs). NMEs faced an average of 5.1 and 6.2 Paragraph IV challenges per NME, for all and $250 million + NMEs, respectively.

Limitations: Analyses, including Paragraph IV calculations, were restricted to NMEs where generic entry had occurred.

Conclusion: The average 2013–2014 MEP of 12.5 years for $250 million + NMEs, 13.6 overall remains consistent with prior research. MEPs are lower, and Paragraph IV challenges are more frequent and occur earlier for $250 million + drugs. Generic share erosion is also greater, and continues to intensify for both NME types.

Introduction

Pharmaceutical competition in the US continues to evolve in the years since the passage in 1984 of the Hatch-Waxman Act, with continuing increases in rates of both generic penetration and patent litigation over time. In enacting the legislation, Congress’s objective was to increase generic competition while balancing the resulting cost savings with sufficient incentives to encourage continued medical innovation through the development of new drugs. The result is a system where new brand-name drugs typically generate nearly all of their US sales during a market exclusivity period (MEP), or the time period between the market launch of a brand-name drug and the market launch of its first generic. Generic manufacturers frequently challenge patents protecting brand-name drugs, and sales of generic drugs often rapidly replace sales of their corresponding brand-name drugs following generic drug market launch.

The Hatch-Waxman Act includes a number of provisions to facilitate approval of generic drugs sold in the US by the Food and Drug Administration (FDA) and encourage generic drug entry, together with other provisions encouraging branded-drug innovation, two of which are described below. Among these, the Act established an Abbreviated New Drug Application (ANDA) process for generic drugs, which greatly reduced the cost of completing an FDA application. Prior to the Hatch-Waxman Act, generic manufacturers were required to submit original safety and efficacy data on their products in order to gain market approval by the FDA. As a result, generic manufacturers generally had to duplicate many of the brand-name manufacturers’ trialsCitation1. Under the streamlined ANDA process, generic manufacturers instead need only demonstrate that their products have the same active ingredients as and are “bioequivalent” to their brand-name counterparts. Generic manufacturers also received a research exemption for the bioequivalence studies they must conduct to gain market approval, which allows them to begin their development of generic counterparts to the brand-name drugs prior to patent expiration without running afoul of patent law.

The Hatch-Waxman Act also created incentives for generic manufacturers to file challenges to brand-name drugs’ patents prior to their expiration. For example, under a so-called “Paragraph IV challenge”, a generic manufacturer files a Paragraph IV ANDA, notifying the FDA that it claims either that its generic product does not infringe on a listed patent of the brand-name drug, or that a patent held on the brand-name drug is not valid. If the brand-name drug manufacturer files a patent infringement action against the generic company within 45 days of receiving notice of the generic company’s Paragraph IV ANDA being filed, the FDA cannot approve the ANDA until the generic company prevails in court or through settlement, or until a 30-month stay expires, whichever comes first. As an inducement for generic manufacturers to challenge brand-name patents, the first generic manufacturer(s) to file a Paragraph IV challenge and to receive FDA final approval of its application, resulting in entry prior to patent expiration, receives a 180-day period of exclusivity. During this 180-day period, its drug is the only ANDA-approved generic version allowed on the market. The first to file a Paragraph IV challenge is determined by the day of filing, and multiple generic manufacturers can share first-to-file status. Paragraph IV challenges are made at the dosage form and strength level, and a generic manufacturer’s 180-day exclusivity period applies only to the dosage form and strength level for which that manufacturer was the first to file a Paragraph IV challenge (e.g. the 15 mg strength oral tablet).

The 180-day period of exclusivity generally is a critical element of profitability to a generic manufacturer because it tends to reduce price only modestly below the level of the brand price during this period, while generic share increases rapidly, and generic sales are enjoyed by a single manufacturer, or a few first-filing manufacturers and authorized generic manufacturer. Therefore, there are substantial incentives to be the first, or among the first, to file a Paragraph IV challenge.

Balancing these provisions aimed at encouraging more generic competition for brand-name drugs, the Hatch-Waxman Act also created new incentives for innovation for brand-name drug manufacturers. For example, under the so-called patent term restoration provision, the life of a single patent on a drug is extended by up to 5 years, with the aim of compensating for a portion of the time that the innovator company spent conducting human clinical trials on the drug before it applied to the FDA for approval of the drug through a New Drug Application (NDA), and for the time the NDA was under FDA review. The patent term restoration provision is capped in two regards: the life of the selected patent cannot be extended by more than 5 years, and the remaining patent term after FDA approval, including the extension, cannot exceed 14 years. In addition to patent term restoration, innovative brand-name drugs are also protected from early ANDA filings through a so-called data exclusivity provision. Data exclusivity, which runs concurrently with patent protection, restricts the FDA from accepting a generic application that relies on a brand-name drug’s safety and efficacy data for 5 years following that drug’s approval (unless there is a Paragraph IV challenge, in which case it is 4 years).

Under the Hatch-Waxman Act framework, therefore, the MEP for new brand-name drugs reflects the combined impact of a number of factors, including provisions aimed at facilitating earlier generic entry and other provisions aimed at maintaining incentives for innovation.

The use of generics has increased substantially in the years following the passage of the Hatch-Waxman Act, for a number of reasons, including: strengthened mechanisms promoting generic use, such as tiered formularies with lower patient co-payments for generic than for brand-name drugs, and commercial insurance and public coverage plan restrictions limiting formulary coverage to generics in certain therapeutic categories; and state laws allowing generic forms to be substituted automatically by pharmacists for brand-name drugs prescribed by physicians, so long as physicians have not specified that the prescription must be “dispensed as written”Citation2,Citation3. As a result, generic products’ share of total prescriptions in the US increased from 36% in 1994 to 88% in 2014Citation4.

The objective of this study is to update previous evidence on recent trends in three factors that have a potentially substantial influence on the balance of cost savings and incentives for continued innovation in the form of new drugs: (1) MEPs for new brand-name drugs; (2) the likelihood and timing of Paragraph IV patent challenges under the Hatch-Waxman Act; and (3) the rate and extent of generic drug penetration following initial generic entry. In addition, we provide new information on the number of generic manufacturer Paragraph IV patent challengers faced by brand-name drugs experiencing initial generic entry. Our analysis is restricted to the US, the largest brand-name drug market.

Patients and methods

Data sources

IMS Health National Sales PerspectivesTM data were used to calculate MEPs for brand-name drugs experiencing first generic entry in the US between October 2012 and December 2014. This is the same data source relied on for prior analyses, and the data obtained for this study was merged with similar data for the time period 1995 through September 2012. The data set used in the analysis contained information about all brand-name drugs experiencing first generic entry during this period (as defined by IMS-defined generic sales), including NMEs and new formulations of older drugs. New formulations include changes in the form of administration—for example, changing from an oral solid pill to an injection—but do not include new strengths or new indications. Our analysis focused just on NMEs, and we present data only on the 288 NMEs experiencing initial generic entry between January 1995 and December 2014, as regulations for generic entry differ if the brand-name product is a new formulation. This figure of 288 NMEs excludes several products from the analysis based on the following criteria: one product was excluded because generic versions of it were subsequently withdrawn as a result of litigation following initial generic entry; and eight products were excluded because FDA approval of the original brand-name drug pre-dated October 1962 and the requirements for safety and efficacy data introduced at that time.

In addition to providing the information necessary to calculate MEPs, the data also included information on drug characteristics, such as mode of administration and number of generic entrants. For ease of comparison with previous analyses, all sales data are presented in 2008 dollars, adjusted using the US Department of Labor’s Consumer Price Index for All Urban Consumers as the market deflator.

We supplemented the market exclusivity data with a detailed review of information from the FDA’s website on Paragraph IV ANDA filings. We also analyzed ANDA approval letters in the study period and searched other public information to identify all of the drugs in the data set that experienced Paragraph IV ANDA filings, and the date of the first filing for each drug. To determine the number of Paragraph IV challengers in each case where there was a Paragraph IV ANDA filing, we relied on data from ParagraphFour.com. ParagraphFour.com collects information from patent litigation court filings related to Paragraph IV ANDA submissions, including a list of generic manufacturer ANDA-filing defendants. For each NME where there was a Paragraph IV filing, we used the count of the number of unique ANDA-filing generic manufacturer defendants listed in patent litigation court filings for that NME to reflect the number of Paragraph IV challengers for that NME. Although generic companies may file ANDA challenges for multiple product strengths for the same NME (e.g. 15, 30, and 45 mg strengths), each ANDA-filing generic manufacturer patent litigation defendant is counted only once for each NME. The counts do not include any generic manufacturers that filed a Paragraph IV ANDA, but where there are no corresponding patent litigation court filings. Our data contained only drugs that experienced generic entry (i.e. drugs that have experienced a Paragraph IV ANDA filing but where generic entry has not yet occurred are not included in the analysis).

For the sub-set of drugs in our sample that experienced first generic entry between 1999 and December 2014, we reviewed IMS Health National Sales PerspectivesTM monthly data on standard units for the brand-name drug and for generic versions of the drug. Monthly sales data were not available for drugs experiencing first generic entry prior to 1999. The data were used to calculate the monthly erosion of brand-name drugs’ share of standard units for the 12 months following first generic entry. The extent of brand-name drug share erosion is summarized based on the timing of first generic entry (by 2-year cohorts), illustrating the increasing extent of brand-name drug erosion for drugs more recently experiencing first generic entry.

Methods

Consistent with prior research, we defined the MEP as the time between the market launch of a brand-name drug and the market launch of its first generic competitor. As noted, this definition reflects the often complex interaction among many technical, regulatory, and competitive factors, including: the timing of patent filings, the amount of patent term lost during product development, the duration of regulatory review before FDA approval, the eligibility for patent term restoration under the Hatch-Waxman Act, the likelihood and outcome of generic patent challenges (including the possibility of a stay on generic entry for up to 30 months pending court decisions on patent infringement suits), market entry commercial decisions by generic manufacturers, and the duration of FDA review of generics. Any one or a combination of these factors can affect the duration of the market exclusivity period of a particular drug. The average MEP remains a key determinant of brand-name drug profitability and incentives for innovation.

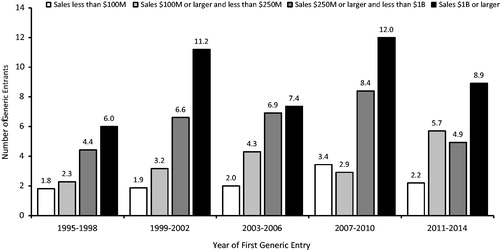

The average number of generic entrants within 1 year of first generic entry was calculated by level of sales (i.e. less than $100 million, greater than or equal to $100 million and less than $250 million, greater than or equal to $250 million and less than $1 billion, $1 billion or larger), based on sales in the year prior to generic entry and, for ease of comparison with prior research, inflation-adjusted to 2008 dollars using the US Department of Labor Consumer Price Index for All Urban Consumers. Results are presented by time period of initial generic entry (i.e. 1995–1998, 1999–2002, 2003–2006, 2007–2010, 2011–2014).

Paragraph IV filing frequency was calculated as the percentage of NMEs experiencing at least one Paragraph IV filing for any strength of that brand-name drug (as noted, NMEs may experience Paragraph IV challenges for multiple strengths) at any time prior to first generic entry, by year of first generic entry. Paragraph IV timing was calculated as the average time from NME launch to the first Paragraph IV filing for any strength for the NME. For each NME identified in the data set as having experienced at least one Paragraph IV filing, the number of challengers was calculated as the number of unique generic manufacturers filing ANDA challenges for at least one strength for the NME and who face patent litigation from the brand-name company as a result of those challenges, based on information obtained from Paragraphfour.com for the period 2004–2014. The information is drawn from initial complaints filed in patent litigation resulting from Paragraph IV ANDA filings and the average number of challengers was calculated only for those NMEs for whom patent litigation filing information could be identified (corresponding to 94% of NMEs in the data set with challenges and first generic entry between 2004–2014).

The generic penetration rate was defined as the share of units of the drug that are filled by a generic version of the drug rather than by the brand-name drug. As noted, generic penetration rates reflect market factors, an increase over time in the mechanisms available to commercial insurance and public plans to promote generic use, as well as state regulations and laws.

All figures presented are unweighted averages. Figures in parentheses following calculated averages are standard deviations, which are presented in tables. Figures for Paragraph IV filing frequency and timing, presented separately in for all NMEs and for NMEs with sales greater than $250 million (in 2008 dollars) in the year prior to generic entry (hereafter, $250 million + NMEs), are 3-year moving averages.

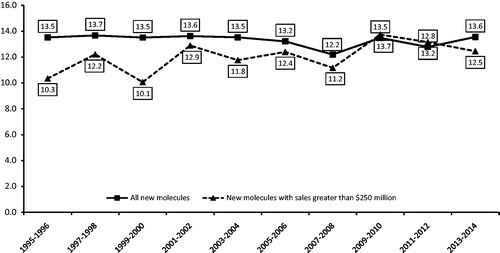

Figure 1. Average market exclusivity period by year of first generic entry, new molecular entities. Source: IMS Health data on all new drugs with initial generic entry in the period 1995 through December 2014. Notes: New molecules with sales greater than $250 million based on sales in the year prior to generic entry and inflation -adjusted to 2008 dollars using the Consumer Price Index for All Urban Consumers.

Results

Average period of market exclusivity

shows the average length of the market exclusivity period for all new drugs and for $250 million + NMEs, by year of first generic entry. Between 1995–2014, the average MEPs for all drugs experiencing first generic entry ranged between 12.2–13.7 years over the period, and between 10.1–13.7 for $250 million + NMEs.

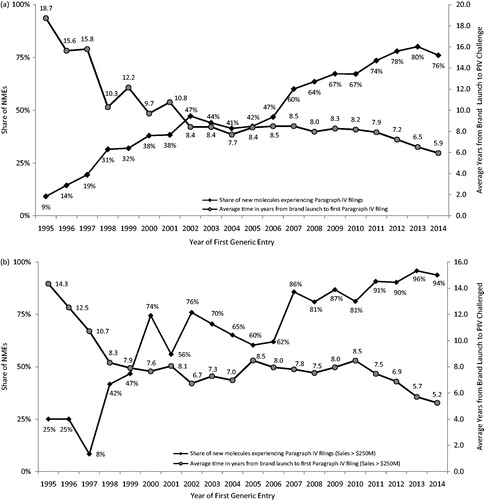

Figure 3. Paragraph IV filing frequency and timing; (a) all NMEs; (b) NMEs with sales >$250M (3-year moving average). Source: IMS Health data on all new drugs with initial generic entry in the period 1995 through December 2014. Food and Drug Administration data and general public information sources on Paragraph IV challenges. Notes: All numbers are three-year moving averages.

$250 million + NMEs represent 39% of all drugs and 92% of sales for all drugs in our data set experiencing generic entry, and only three of these NMEs had MEPs greater than 20 years. The average MEP for $250 million + NMEs was 12.5 years in the most recent period in our study (2013–2014) and 13.6 years for all NMEs. Figures for each cohort of NMEs, as defined by year of first generic entry, are presented in .

Table 1. Average market exclusivity period by year of first generic entry.

summarizes the average number of generic competitors to a brand-name drug in the market 12 months after the first generic entry, segmented by level of sales and by time period. The number of generic entrants is higher for drugs with larger sales before the first generic entry, generally increasing over time (although not for every drug sales cohort and subsequent time period). For example, in the period 1995–1998, there was one drug with over $1 billion in annual sales prior to generic entry, and it faced six generic entrants after 1 year. The corresponding figures for drugs with over $1 billion in annual sales (in 2008 dollars) prior to generic entry and experiencing first generic entry in later periods were an average of between 11–12 generic entrants for the period 1999–2002, between 7–8 for 2003–2006, 12 for 2007–2010 and between 8–9 for 2011–2014.

Figure 2. Average number of generic entrants within 1 year of first generic entry, new molecular entities. Source: IMS Health data on all new drugs with initial generic entry in the period 1995 through December 2014. Notes: New molecules with sales in the year prior to generic entry, inflation-adjusted to 2008 dollars using the Consumer Price Index for All Urban Consumers.

Paragraph IV challenges

The likelihood of a Paragraph IV challenge being filed has increased substantially in recent years, for all NMEs () and for $250 million + NMEs (). Only 9% of all NMEs experiencing first generic entry in 1995 had experienced a Paragraph IV challenge at any point prior to first generic launch. That share increased to 76% of drugs experiencing first generic entry in 2014. $250 million + NMEs faced an even higher probability of a Paragraph IV filing, increasing from 25% in 1995 to 94% in 2014. Similar trends were found when restricting the findings to oral formulation drugs, for which the percentage increased from 6% in 1995 to 95% in 2014 (data not shown, all figures are 3-year moving averages).

Paragraph IV challenges also occur sooner following the launch of a brand-name drug. For drugs experiencing first generic entry in 1995 and also experiencing a Paragraph IV challenge any time prior, the average time between launch and the first Paragraph IV challenge was 18.7 years for all drugs and 14.3 years (one drug) for $250 million + NMEs. That time fell to 5.9 years for all drugs experiencing first generic entry in 2014, and 5.2 years for $250 million + NMEs.

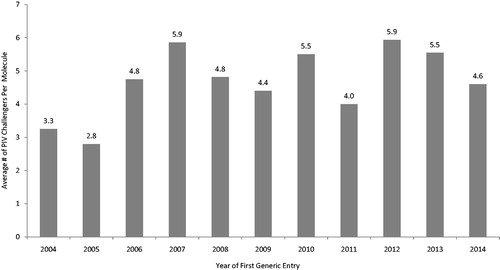

The average number of Paragraph IV challengers per NME varies by year of first generic entry, ranging between 2.8 (2005) and 5.9 (2007, 2012) (). The lowest number of unique challengers observed for any NME in any year was one and the highest was 20, for an average of 4.9 over all NMEs and over the time period 2004–2014. Together with other information on Paragraph IV challenges, these data are summarized in .

Figure 4. Paragraph IV challengers by year of first generic entry, 2004–2014. Source: MEP dataset, ParagraphFour.com, authors' calculations.

Table 2. Paragraph IV filing frequency, timing, and number of challengers.

The calculations reflected in represent averages across all NMEs experiencing first generic entry in a given year. They may vary according to factors such as the drug’s sales prior to generic entry, the nature of the patents protecting the drug, and the ease with which generic manufacturers can imitate the drug and satisfy FDA regulations. For higher-revenue drugs, generic manufacturers may be less selective when filing challenges, as even a low likelihood of success in litigation can yield a large expected return on the investment necessary to challenge a patent. Prior researchers have found that court decisions on Paragraph IV challenges filed prior to 2005 involved a disproportionate share of high-revenue drugsCitation5. Others have calculated that, as brand-name drug revenue increases, the probability of success required to justify a patent challenge by a generic manufacturer diminishes to below 1%Citation6, and that for patent cases decided by district courts between 2009–2012, brand companies prevailed in 54% of themCitation7.

Our analysis yields similar findings; we find that, controlling for year of brand launch and form (i.e. oral, injectable, other non-oral), higher brand sales (in 2008 dollars) 12 months prior to first generic entry are associated with a significantly higher probability of a Paragraph IV filing over the 1999–2014 time period. For instance, for the average drug in the analysis, increasing brand sales in the 12 months prior to first generic entry by a factor of five (e.g. from $100 million to $500 million) while holding all other variables constant was associated with approximately a 15 percentage point increase in the probability of a Paragraph IV challenge (marginal effect, evaluated at the means of other variables). Higher brand sales were also associated with a significantly shorter time to first Paragraph IV filing; controlling for year of brand launch and form, increasing brand sales in the 12 months prior to first generic entry by a factor of five was associated with approximately a half-year shorter time to first Paragraph IV filing ().

Table 3. Determinants of Paragraph IV filing frequency and timing.

Market share erosion after generic entry

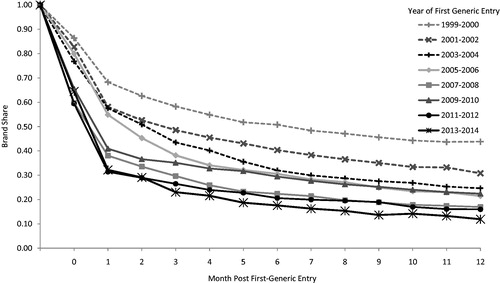

shows the erosion in brand-name drugs’ share for the 12 months following first generic entry, with share defined as the unit share of brands divided by the sum of brands and their corresponding generics (i.e. the brand-name share of all units sold). Generic erosion has increased dramatically and continuously since 1999–2000. For all NMEs facing first generic entry in 2013–2014, brands retained an average of only 12% of units at 1 year. For $250 million + NMEs, generic erosion was even more pronounced; the corresponding figure was only 7% of units at 1 year (data not shown).

Figure 5. Average monthly brand share of standard units of the molecule/form following first generic entry. Source: IMS Health data for all new molecular entities with first generic entry in the period 1999 through December 2014. Note: Initial generic entry occurs at some point during month “0”. Month “1” is the first full month of generic competition.

In comparison, brand-name drugs experiencing first generic entry in 1999–2000 maintained a share of 44% of units at 1 year following first generic entry. Grouping drugs into 2-year cohorts by the date of first generic entry illustrates the steady increase in the rate and extent of generic penetration over the past decade and a half.

Discussion

Our findings extend and expand upon closely-related research originally conducted by Grabowski and KyleCitation8 and updated in Grabowski et al.Citation9 and, most recently, Grabowski et al.Citation10, which evaluated data on MEPs for all new molecular entities (NMEs) experiencing initial generic entry between 1995 and September 2012. With the aim of providing a continuous data series, we further extend the prior analyses to include data on all NMEs experiencing initial generic entry through December 2014, and present results for all NMEs, and for NMEs with sales greater than $250 million (in 2008 dollars) in the year prior to generic entry.

Consistent with prior research, MEPs for drugs experiencing initial generic entry in 2013–2014 was 12.5 years for $250 million + NMEs, and 13.6 years for all NMEs. While the average MEP for brand-name drugs has remained relatively constant, generic manufacturers are challenging the patents protecting brand-name drugs more often and earlier, which may have a downward impact on future MEPs (we calculate MEPs only for those already experiencing generic entry). Seventy-six per cent of all brand-name drugs experiencing initial generic entry in 2014 had faced at least one Paragraph IV patent challenge from a generic manufacturer, up from only 9% for drugs experiencing initial generic entry in 1995. For $250 million + NMEs, the figure was even higher; 94% of $250 million + NMEs had faced at least one Paragraph IV patent challenge from a generic manufacturer, up from 25% for those experiencing initial generic entry in 1995. These challenges are filed relatively early in the brand drug life cycle, or 5.9 years after brand launch on average for all NMEs, and 5.2 years after brand launch for $250 million + NMEs. Most NMEs faced multiple patent challenges (74% of NMEs challenged faced more than one challenger), with an average of 4.9 challengers per NME experiencing a patent challenge over the time period 2004–2014.

Other research also finds that Paragraph IV patent challenges have an impact on MEPs. An analysis by one of the co-authors of observed and expected future generic entry dates (incorporating information from litigation outcomes and settlements) finds a statistically significant downward effect on MEPs from patent challenges, all else equal. In addition, top-quintile sales drugs experience a statistically significant downward trend in projected MEPs over timeCitation11. These findings from an analysis of 1994–2006 FDA-approved NMEs (rather than only those already experiencing initial generic entry) suggest that we may soon see future decreases in observed MEPs.

Generic competition has continued to intensify over the past 15 years. Because manufacturers earn almost all profits on a brand-name drug during the MEP, and brand-name drug shares rapidly drop following initial generic entry, the MEP is a key economic indicator for brand-name drugs. For $250 million + NMEs experiencing initial generic entry in 2013–2014, average brand unit share had fallen to just 7% at 1 year; for all NMEs with initial generic entry in 2013–14, average brand unit share at 1 year had fallen to 12%.

Conclusions

While the average MEP for brand-name drugs, currently 12.5 years for NMEs with pre-generic entry sales of $250 million+ (in 2008 dollars) and 13.6 years for all drugs, remains consistent with prior research, MEPs are lower and Paragraph IV challenges are more frequent and occur earlier for $250 million + drugs. Over the past two decades, Paragraph IV challenges have become increasingly frequent and occur earlier, with most NMEs experiencing multiple patent challenges. Generic share erosion also continues to intensify, both for all drugs and for $250 million + drugs.

Transparency

Declaration of funding

Analysis Group, Inc., received financial support from the Pharmaceutical Research and Manufacturers of America for this research. HG received no financial support.

Declaration of financial/other relationships

GL, RM, and AB are employees of Analysis Group, Inc., a consulting company that has provided services to biopharmaceutical manufacturers, both brand-name and generic. HG has served as an expert witness in pharmaceutical patent-related litigation on behalf of both plaintiffs and defendants. The analysis presented was designed and executed entirely by the authors, and therefore, they are responsible for any errors or misstatements.

References

- Grabowski H, Vernon J. Longer patents for lower imitation barriers: the 1984 drug act. Amer Econ Rev 1986;76:195-8

- Berndt E. Pharmaceuticals in U.S. health care: determinants of quantity and price. J Econ Perspect 2002;16:45-66

- Office of the Assistant Secretary for Planning and Evaluation (ASPE Issue Brief). Expanding the use of generic drugs. Washington, DC: ASPE, 2010. www.aspe.hhs.gov/sp/reports/2010/genericdrugs/ib.pdf. Accessed 2, October 2013

- Medicines use and spending shifts: a review of the use of medicines in the U.S. in 2014. IMS Institute for Healthcare Informatics. www.theimsinstitute.org/en/thought-leadership/ims-institute/reports/medicines-use-in-the-us-2014#ims-form. Accessed 14, December 2015

- Panattoni LE. The effect of Paragraph IV decisions and generic entry before patent expiration on brand pharmaceutical firms. J Health Econ 2011;30:126-45

- Smith K, Gleklen K. Generic drugmakers will challenge patents even when they have a 97% chance of losing: the FTC Report that K-Dur ignored. CPI Antitrust Chronicle, 2012. www.competitionpolicyinternational.com/generic-drugmakers-will-challenge-patents-even-when-they-have-a-97-chance-of-losing-the-ftc-report-that-k-dur-ignored/. Accessed 3, October 2013

- Glass G. Legal defenses and outcomes in paragraph IV patent litigation. J Generic Med 2013;10:4-13

- Grabowski H, Kyle M. Generic competition and market exclusivity periods in pharmaceuticals. Manage Decis Econ 2007;28:491-502

- Grabowski H, Kyle M, Mortimer R, et al. Evolving brand-name and generic drug competition may warrant a revision of the Hatch-Waxman Act. Health Affairs 2011;30:2157-66

- Grabowski H, Long G, Mortimer R, Recent trends in brand name and generic drug competition. J Med Econ 2014;17:207-14

- Grabowski H, Brain C, Taub A, et al. Pharmaceutical patent challenges: company strategies and litigation outcomes. Am J Health Econ (forthcoming)